Momentum and Bubbles: Analysis of Cyprus Stock Exchange Performance

VerifiedAdded on 2020/02/14

|15

|2650

|35

Report

AI Summary

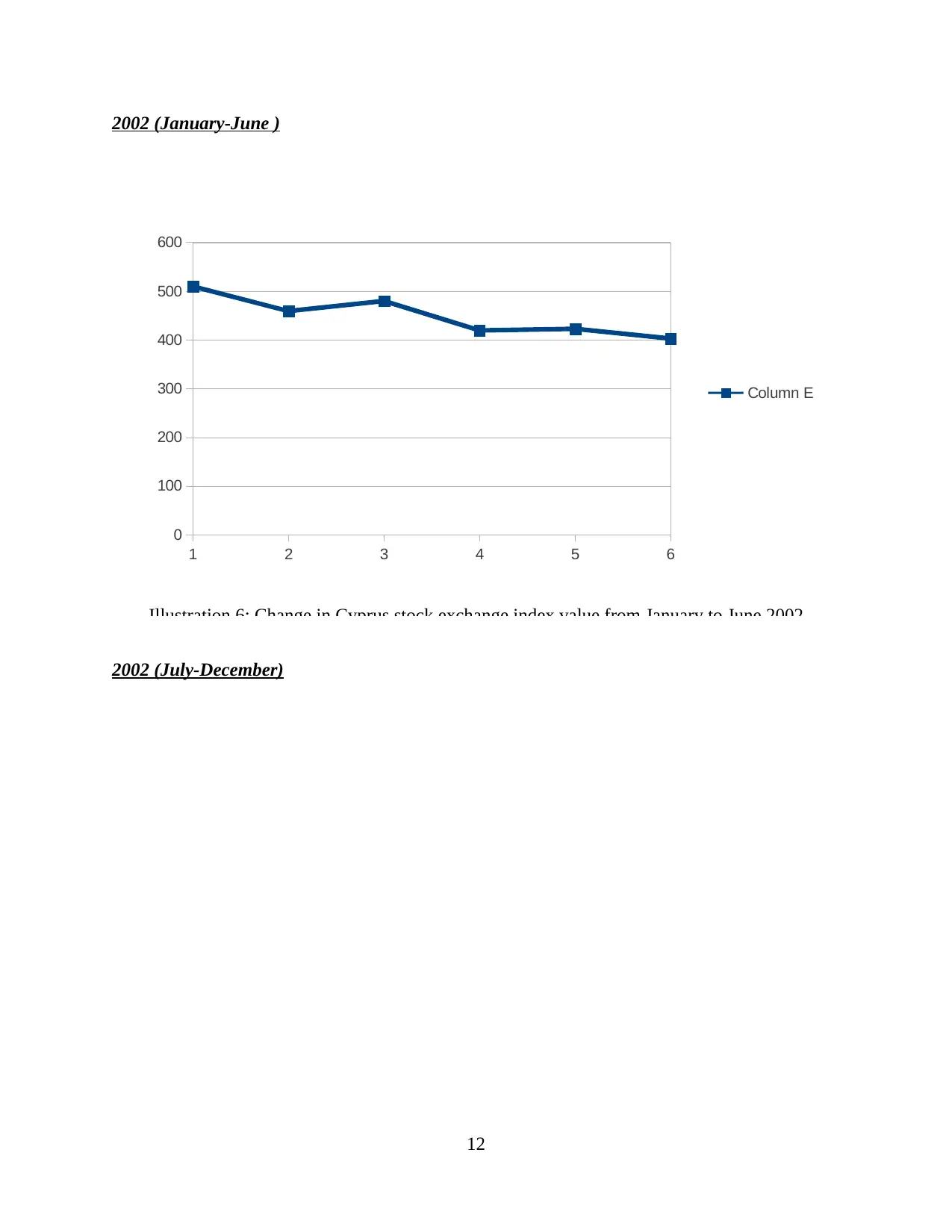

This report investigates the application of momentum theory within the Cyprus Stock Exchange, focusing on the period between 1999 and 2008. It examines how market trends, specifically periods of significant growth and decline, impact investment strategies. The study utilizes financial tools such as the coefficient of intercept of regression, Capital Asset Pricing Model (CAPM), and Sharpe ratio to assess the performance of stocks during both bullish and bearish market conditions. The methodology involves analyzing data from the Cyprus Stock Exchange, including index values and share prices, to compute and correlate these statistical measures. The report aims to determine the effectiveness of momentum-based investment strategies by comparing the performance of portfolios during different market phases. Historical data from the Cyprus stock exchange is examined to determine the practical application of momentum theory in the real world.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.