Analyzing Money and Banking Concepts: Finance Assignment

VerifiedAdded on 2021/06/17

|16

|2370

|45

Homework Assignment

AI Summary

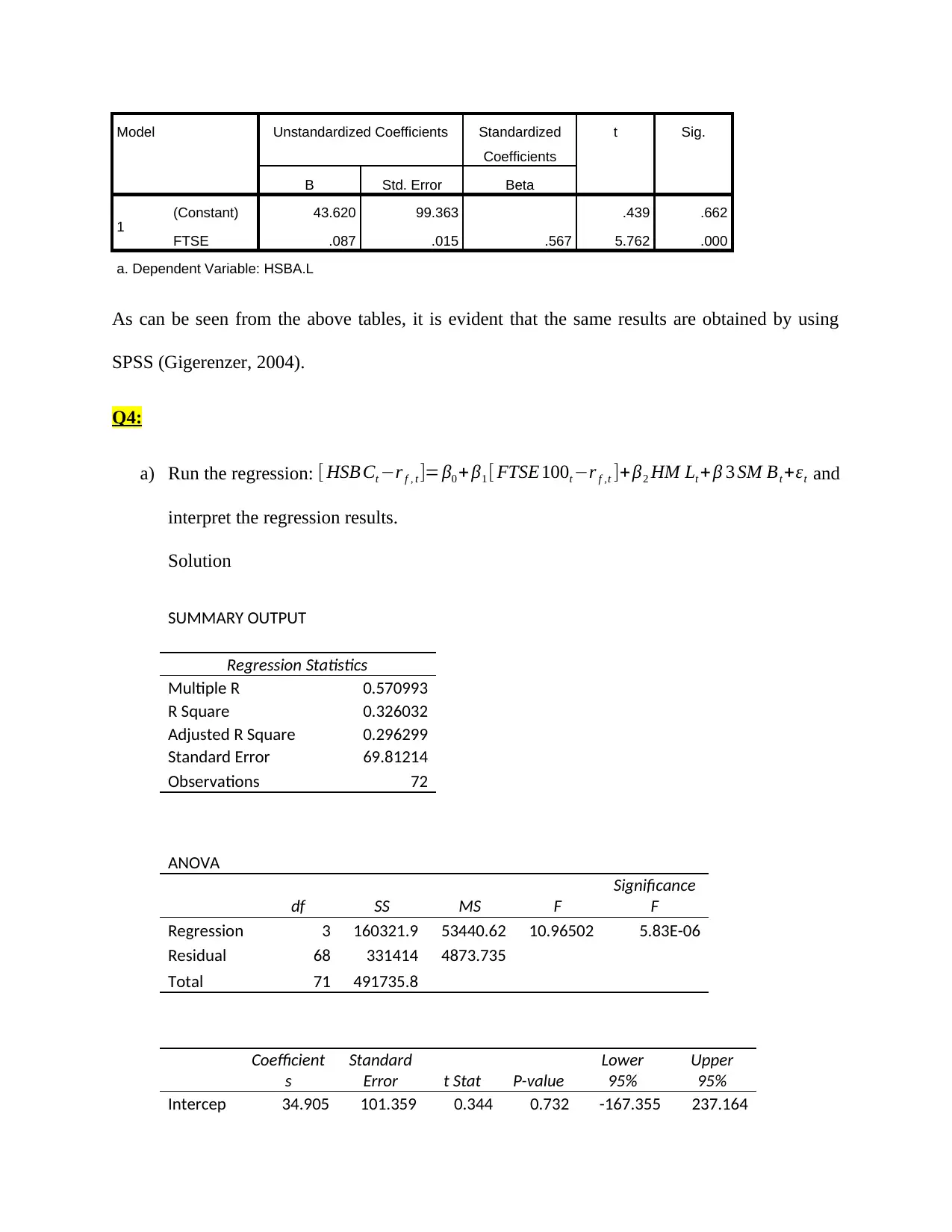

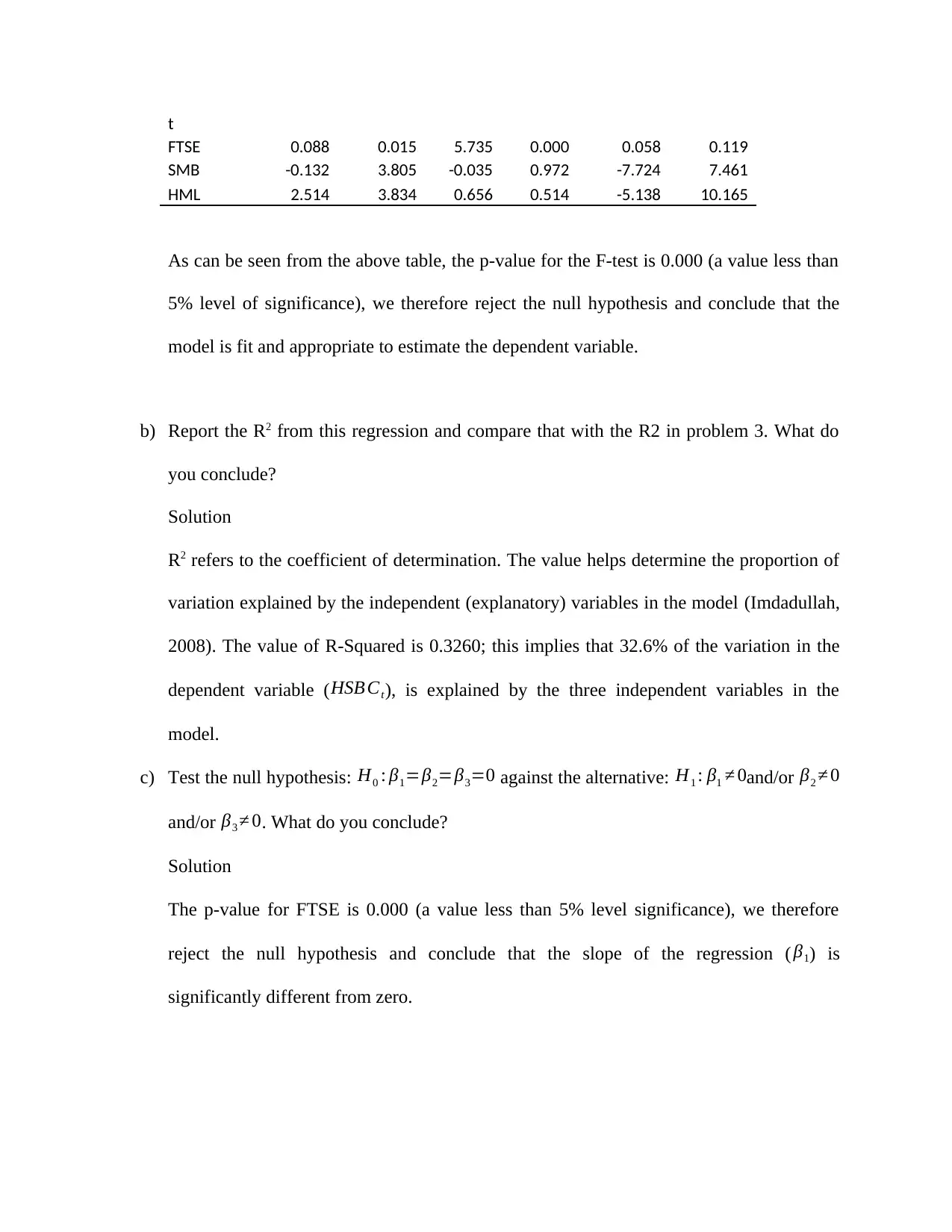

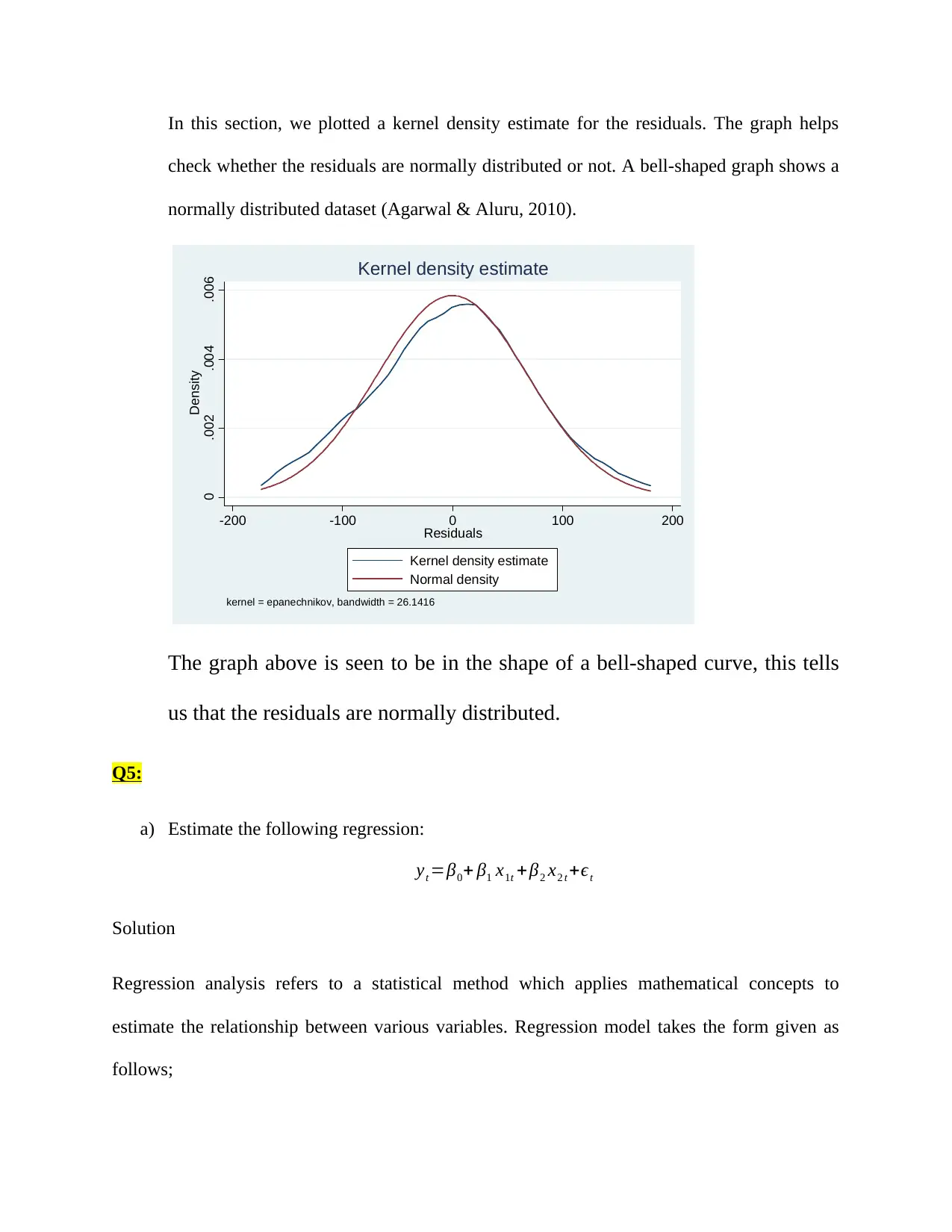

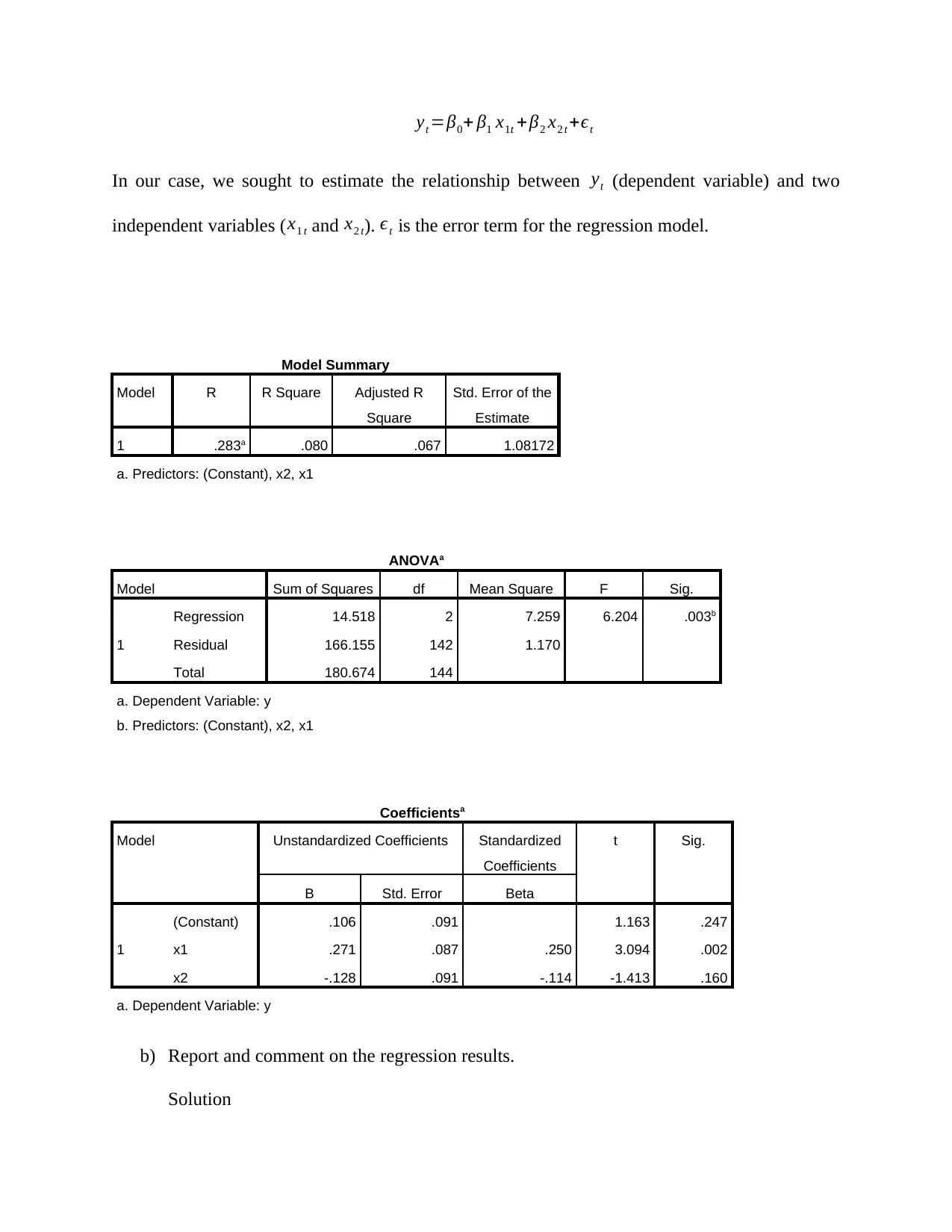

This document presents a comprehensive solution to a money and banking assignment. It addresses various financial concepts, including calculating portfolio returns, constructing confidence intervals, and performing hypothesis testing. The assignment involves regression analysis, interpreting regression results, and conducting diagnostic checks for heteroscedasticity, autocorrelation, and normality. The solution provides detailed explanations, formulas, and statistical outputs, including results from SPSS, to support the analysis. The assignment covers topics like testing null hypotheses, interpreting coefficients, and assessing the significance of variables in regression models. Furthermore, the document highlights potential issues with the regression results, such as non-normality and heteroscedasticity, and suggests methods for addressing these problems. This resource is designed to assist students in understanding and completing similar assignments in finance and related fields.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.