Evaluating Financial Projects: NPV, IRR, YTM, and Monetary Policy

VerifiedAdded on 2023/06/13

|14

|4322

|255

Report

AI Summary

This report provides a comprehensive analysis of various financial concepts and tools. It begins with a calculation of Net Present Value (NPV) and Internal Rate of Return (IRR) for a given project, offering a recommendation based on these metrics. The report then explains how Yield to Maturity (YTM) is used to calculate the Yield Curve, followed by an analysis of the importance of financial intermediaries in a well-functioning financial system, discussing their advantages and disadvantages. Finally, it explores the factors that determine the time-lag between the application of monetary policy instruments and the achievement of ultimate goals. The report utilizes calculations, definitions, and examples to illustrate these key financial principles.

Money banking and

finance

finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................3

I) Calculate the Net present value (NPV) of the project..............................................................3

II) Compute of Internal Rate of Return (IRR) for this project.....................................................4

III) Recommend the Manager regarding the project....................................................................5

PART B............................................................................................................................................5

Explain how Yield to Maturity is used to calculate the Yield Curve..........................................5

PART C............................................................................................................................................6

Analyse the statement 'Financial Intermediaries are vital to a well-functioning financial

system.'.........................................................................................................................................6

PART D...........................................................................................................................................9

Discussion related to the factors which determine the time-lag between the application of

instrument or tool of monetary policy and the achievement of the ultimate goal.......................9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................3

I) Calculate the Net present value (NPV) of the project..............................................................3

II) Compute of Internal Rate of Return (IRR) for this project.....................................................4

III) Recommend the Manager regarding the project....................................................................5

PART B............................................................................................................................................5

Explain how Yield to Maturity is used to calculate the Yield Curve..........................................5

PART C............................................................................................................................................6

Analyse the statement 'Financial Intermediaries are vital to a well-functioning financial

system.'.........................................................................................................................................6

PART D...........................................................................................................................................9

Discussion related to the factors which determine the time-lag between the application of

instrument or tool of monetary policy and the achievement of the ultimate goal.......................9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

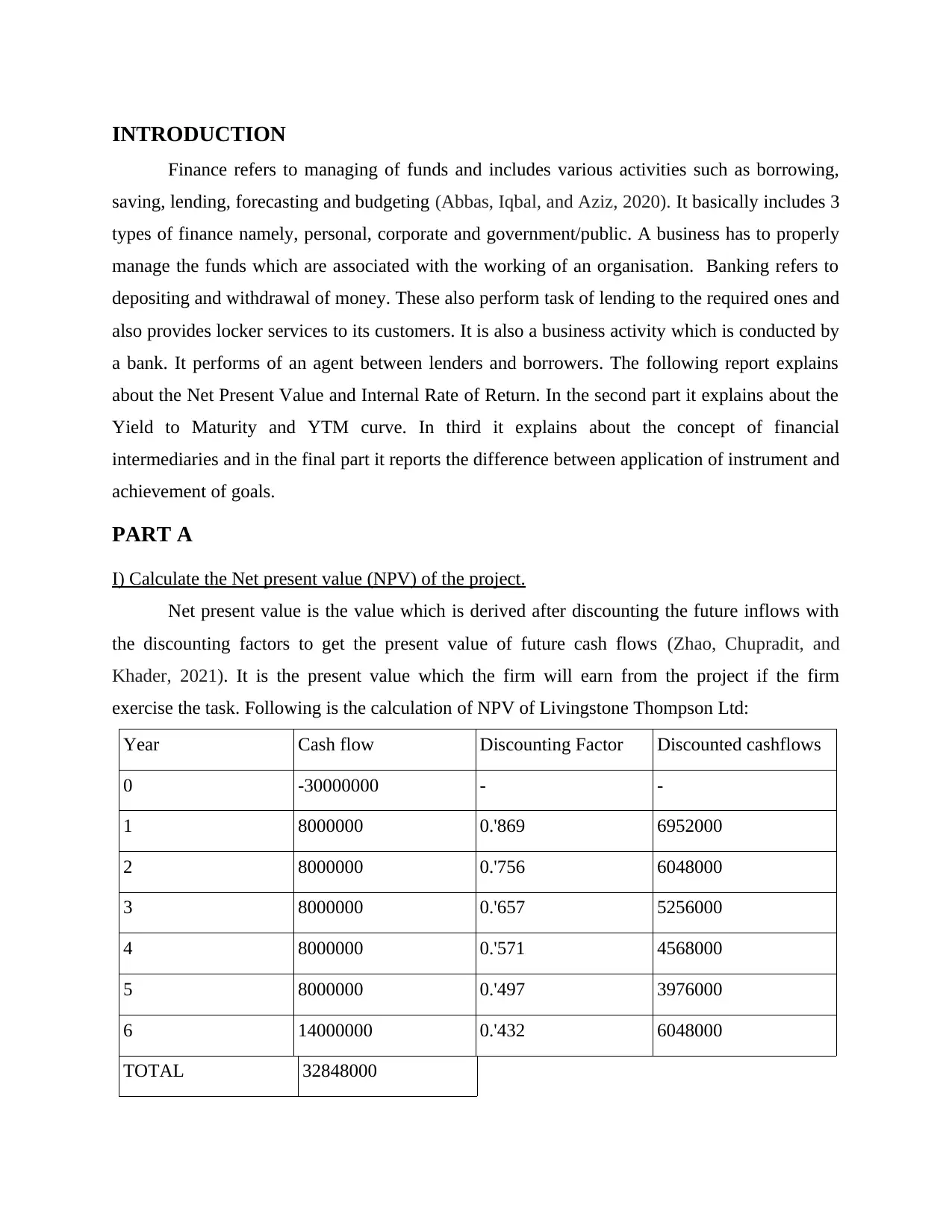

INTRODUCTION

Finance refers to managing of funds and includes various activities such as borrowing,

saving, lending, forecasting and budgeting (Abbas, Iqbal, and Aziz, 2020). It basically includes 3

types of finance namely, personal, corporate and government/public. A business has to properly

manage the funds which are associated with the working of an organisation. Banking refers to

depositing and withdrawal of money. These also perform task of lending to the required ones and

also provides locker services to its customers. It is also a business activity which is conducted by

a bank. It performs of an agent between lenders and borrowers. The following report explains

about the Net Present Value and Internal Rate of Return. In the second part it explains about the

Yield to Maturity and YTM curve. In third it explains about the concept of financial

intermediaries and in the final part it reports the difference between application of instrument and

achievement of goals.

PART A

I) Calculate the Net present value (NPV) of the project.

Net present value is the value which is derived after discounting the future inflows with

the discounting factors to get the present value of future cash flows (Zhao, Chupradit, and

Khader, 2021). It is the present value which the firm will earn from the project if the firm

exercise the task. Following is the calculation of NPV of Livingstone Thompson Ltd:

Year Cash flow Discounting Factor Discounted cashflows

0 -30000000 - -

1 8000000 0.'869 6952000

2 8000000 0.'756 6048000

3 8000000 0.'657 5256000

4 8000000 0.'571 4568000

5 8000000 0.'497 3976000

6 14000000 0.'432 6048000

TOTAL 32848000

Finance refers to managing of funds and includes various activities such as borrowing,

saving, lending, forecasting and budgeting (Abbas, Iqbal, and Aziz, 2020). It basically includes 3

types of finance namely, personal, corporate and government/public. A business has to properly

manage the funds which are associated with the working of an organisation. Banking refers to

depositing and withdrawal of money. These also perform task of lending to the required ones and

also provides locker services to its customers. It is also a business activity which is conducted by

a bank. It performs of an agent between lenders and borrowers. The following report explains

about the Net Present Value and Internal Rate of Return. In the second part it explains about the

Yield to Maturity and YTM curve. In third it explains about the concept of financial

intermediaries and in the final part it reports the difference between application of instrument and

achievement of goals.

PART A

I) Calculate the Net present value (NPV) of the project.

Net present value is the value which is derived after discounting the future inflows with

the discounting factors to get the present value of future cash flows (Zhao, Chupradit, and

Khader, 2021). It is the present value which the firm will earn from the project if the firm

exercise the task. Following is the calculation of NPV of Livingstone Thompson Ltd:

Year Cash flow Discounting Factor Discounted cashflows

0 -30000000 - -

1 8000000 0.'869 6952000

2 8000000 0.'756 6048000

3 8000000 0.'657 5256000

4 8000000 0.'571 4568000

5 8000000 0.'497 3976000

6 14000000 0.'432 6048000

TOTAL 32848000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

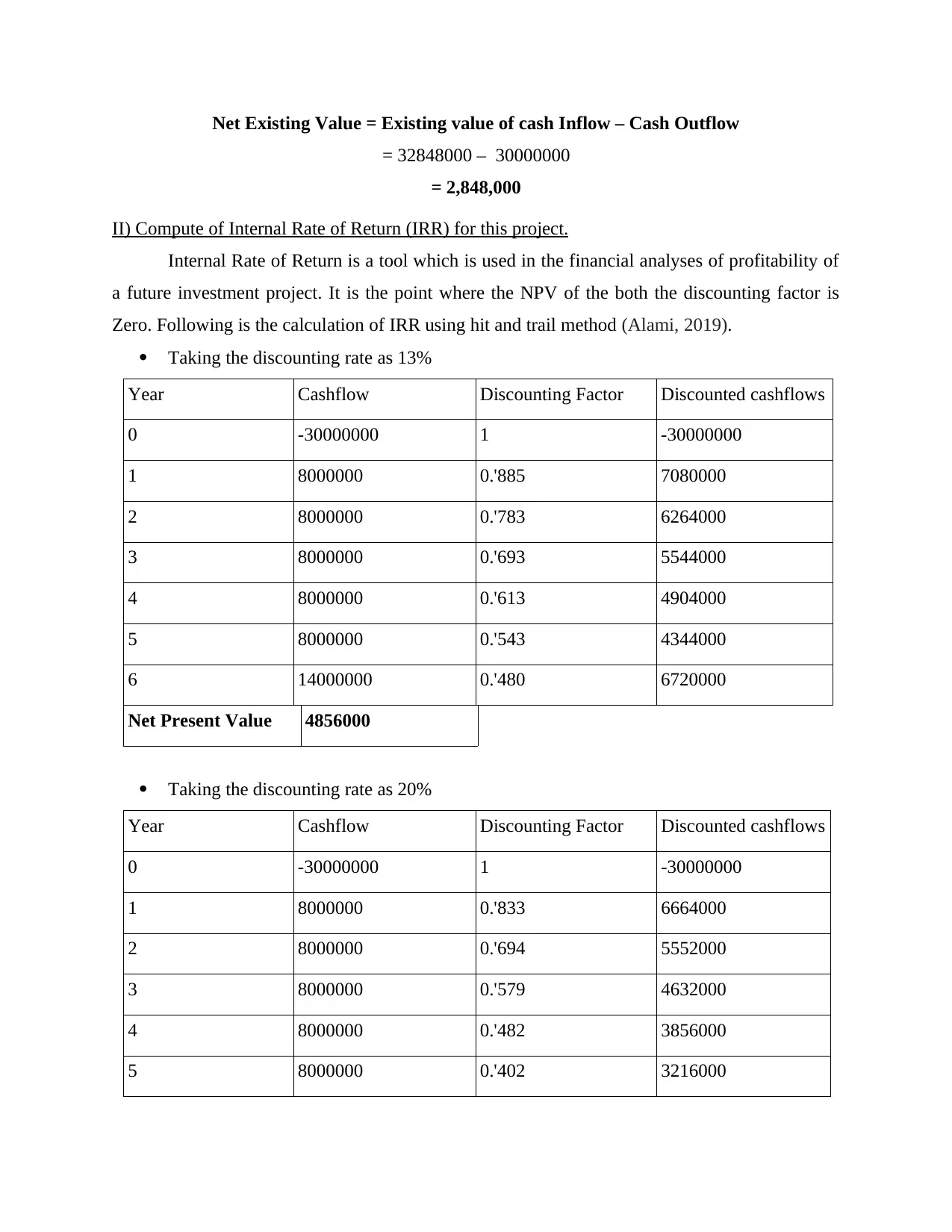

Net Existing Value = Existing value of cash Inflow – Cash Outflow

= 32848000 – 30000000

= 2,848,000

II) Compute of Internal Rate of Return (IRR) for this project.

Internal Rate of Return is a tool which is used in the financial analyses of profitability of

a future investment project. It is the point where the NPV of the both the discounting factor is

Zero. Following is the calculation of IRR using hit and trail method (Alami, 2019).

Taking the discounting rate as 13%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 1 -30000000

1 8000000 0.'885 7080000

2 8000000 0.'783 6264000

3 8000000 0.'693 5544000

4 8000000 0.'613 4904000

5 8000000 0.'543 4344000

6 14000000 0.'480 6720000

Net Present Value 4856000

Taking the discounting rate as 20%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 1 -30000000

1 8000000 0.'833 6664000

2 8000000 0.'694 5552000

3 8000000 0.'579 4632000

4 8000000 0.'482 3856000

5 8000000 0.'402 3216000

= 32848000 – 30000000

= 2,848,000

II) Compute of Internal Rate of Return (IRR) for this project.

Internal Rate of Return is a tool which is used in the financial analyses of profitability of

a future investment project. It is the point where the NPV of the both the discounting factor is

Zero. Following is the calculation of IRR using hit and trail method (Alami, 2019).

Taking the discounting rate as 13%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 1 -30000000

1 8000000 0.'885 7080000

2 8000000 0.'783 6264000

3 8000000 0.'693 5544000

4 8000000 0.'613 4904000

5 8000000 0.'543 4344000

6 14000000 0.'480 6720000

Net Present Value 4856000

Taking the discounting rate as 20%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 1 -30000000

1 8000000 0.'833 6664000

2 8000000 0.'694 5552000

3 8000000 0.'579 4632000

4 8000000 0.'482 3856000

5 8000000 0.'402 3216000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6 14000000 0.'335 4690000

Net Present Value -1390000

IRR = Lower rate + Lower rate NPV / (Lower rate NPV – Higher rate NPV) * Difference

in rates

= 13 + 4856000 / (4856000 + 1390000) * (20-13)

= 13 + 5.44

=18.44%

III) Recommend the Manager regarding the project.

According to NPV method the project should be selected.

According to IRR method, in the following case the IRR is 18.44% which means that the

project can be selected as it provides good returns. IRR is the rate which defines that if an

individual invest 100 pounds then in return, 118.44 pounds will be received. In a nutshell

it can be concluded that the project will earn more than the money invested in the project

(Borini, 2018).

PART B

Explain how Yield to Maturity is used to calculate the Yield Curve.

Internal Rate of Return is used to evaluate the return business will earn from the project

and also check whether the project is viable or not. Higher IRR is considered good which means

the project will earn more income. In this method return of the project is calculated by the

investors themselves. Yield to maturity is tool to evaluate the capital gain or loss from a project.

YTM stands for the return the investor will get at the maturity of the bonds purchased. It

is calculated by subtracting the current market price of the bonds with the value of bonds

purchased. The maturity amount includes both the principle and the interest payment associated

with it. YTM is the current price of the maturity value that will be receivable by the investor

after the maturity date. The bonds are redeemed after the maturity period associated with the

bonds (Cao, 2021).

Yield to Maturity is calculated with the use of IRR method, following is the alternative way of

calculating the YTM.

Net Present Value -1390000

IRR = Lower rate + Lower rate NPV / (Lower rate NPV – Higher rate NPV) * Difference

in rates

= 13 + 4856000 / (4856000 + 1390000) * (20-13)

= 13 + 5.44

=18.44%

III) Recommend the Manager regarding the project.

According to NPV method the project should be selected.

According to IRR method, in the following case the IRR is 18.44% which means that the

project can be selected as it provides good returns. IRR is the rate which defines that if an

individual invest 100 pounds then in return, 118.44 pounds will be received. In a nutshell

it can be concluded that the project will earn more than the money invested in the project

(Borini, 2018).

PART B

Explain how Yield to Maturity is used to calculate the Yield Curve.

Internal Rate of Return is used to evaluate the return business will earn from the project

and also check whether the project is viable or not. Higher IRR is considered good which means

the project will earn more income. In this method return of the project is calculated by the

investors themselves. Yield to maturity is tool to evaluate the capital gain or loss from a project.

YTM stands for the return the investor will get at the maturity of the bonds purchased. It

is calculated by subtracting the current market price of the bonds with the value of bonds

purchased. The maturity amount includes both the principle and the interest payment associated

with it. YTM is the current price of the maturity value that will be receivable by the investor

after the maturity date. The bonds are redeemed after the maturity period associated with the

bonds (Cao, 2021).

Yield to Maturity is calculated with the use of IRR method, following is the alternative way of

calculating the YTM.

YTM = Interest + (Redeemable value – Current Market Price) / N

(Current Market Price + Redeemable Value) / 2

The above formula only calculates the estimated YTM and does not calculate the actual YTM of

a project. The amount of YTM is calculated by Trial and Error method of calculating IRR. The

estimated amount of return equals the current market price of bonds suggests that the YTM

calculated is correct.

Yield curve represents on graph the interest payments received by an investor by the end of the

period of securities. It mainly focuses on the value which the capitalist will receive at the

maturity date. The amount receivable by the investor changes the curve also changes. X-axis

shows interest payment and Y-axis shows the period of the bonds.

Future investors will track the progress of the the bonds on regular process to determine

whether to invest in the business or not. Not only the interest but current investor also tracks the

progress by tracking the current market price of the bonds, and if the bonds do not perform as per

the expected rate of return the investor will sell of its securities. In order to safeguard from the

risk of losing money the investor have to track the prices on the regular basis (Chazi, Mirzaei,

and Azad, 2020).

Curve may be of different types normal, parallel, upturned and others. The shape of the curve

changes because of external factors such as economic growth, market interest rate and inflation.

The investor has to carefully these factors before investing the securities of any business

concern.

The following are the factors used to analyse the yield curve:

Normal Yield curve states that the securities are profitable as expected at the beginning.

An upward sloping yield curve signifies that the corporation is earning a significant

amount of revenue.

Downward Yield curve signifies that the company is not able to generate the sufficient

cash flows in order to earn more profits.

Flat Yield curve indicates that the neither the company have appreciated the revenue nor

it depreciated. Thus the value of the securities remains the same as of in the beginning.

(Current Market Price + Redeemable Value) / 2

The above formula only calculates the estimated YTM and does not calculate the actual YTM of

a project. The amount of YTM is calculated by Trial and Error method of calculating IRR. The

estimated amount of return equals the current market price of bonds suggests that the YTM

calculated is correct.

Yield curve represents on graph the interest payments received by an investor by the end of the

period of securities. It mainly focuses on the value which the capitalist will receive at the

maturity date. The amount receivable by the investor changes the curve also changes. X-axis

shows interest payment and Y-axis shows the period of the bonds.

Future investors will track the progress of the the bonds on regular process to determine

whether to invest in the business or not. Not only the interest but current investor also tracks the

progress by tracking the current market price of the bonds, and if the bonds do not perform as per

the expected rate of return the investor will sell of its securities. In order to safeguard from the

risk of losing money the investor have to track the prices on the regular basis (Chazi, Mirzaei,

and Azad, 2020).

Curve may be of different types normal, parallel, upturned and others. The shape of the curve

changes because of external factors such as economic growth, market interest rate and inflation.

The investor has to carefully these factors before investing the securities of any business

concern.

The following are the factors used to analyse the yield curve:

Normal Yield curve states that the securities are profitable as expected at the beginning.

An upward sloping yield curve signifies that the corporation is earning a significant

amount of revenue.

Downward Yield curve signifies that the company is not able to generate the sufficient

cash flows in order to earn more profits.

Flat Yield curve indicates that the neither the company have appreciated the revenue nor

it depreciated. Thus the value of the securities remains the same as of in the beginning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART C

Analyse the statement 'Financial Intermediaries are vital to a well-functioning financial system.'

Financial intermediaries include an organisation, individual or a group of people which

acts as an agent to complete a financial transaction. These intermediaries include investment

banks, mutual funds, pension funds and commercial banks. Clients gets benefits like liquidity,

financial safety, etc. from such intermediaries. User of financial market get help from these

intermediaries in order to lower the cost of the transactions and also provides efficient deals.

They help in lowering the cost and economics of scale (Chen, 2018).

Financial intermediaries help in making the funds to invest in the securities which are

shortlisted. These intermediaries help in sourcing funds for the required once whom are in need,

for example, big companies or start-ups. They borrow goods from the lenders and individuals to

provide the once whom want to acquire. There are mainly two types of intermediaries, one is

asset based financial intermediaries and the other is fee based financial intermediaries which

provides broking services (Golubic, 2019).

The financial intermediaries play a central role in efficient allocation of resources.

Maturity transformation: These organisation helps in providing long term funds to the

organisation and ensuring borrowers the facilities of liquidity. It depends on the investors

whether they want to invest for short or long term basis.

Value Transformation: These firms pool penny savings and lend these funds to needy

one's.

Expertise: These are the expert in their field and provides specialised knowledge in

forecasting and anticipating the risk involved.

Reduction in transaction costs: These are the only one's whom act as an intermediary in

providing loans. Thus non other cost or brokerage is associated with it.

Ease of borrowing: The borrowers does not have to go here and there for the

requirement of funds.

These financial intermediaries may seem to be a good alternative just because they allow

the borrowers and lenders to connect with each other. Despite of advantages, they have major

disadvantages as well. The disadvantages are as follows-

Analyse the statement 'Financial Intermediaries are vital to a well-functioning financial system.'

Financial intermediaries include an organisation, individual or a group of people which

acts as an agent to complete a financial transaction. These intermediaries include investment

banks, mutual funds, pension funds and commercial banks. Clients gets benefits like liquidity,

financial safety, etc. from such intermediaries. User of financial market get help from these

intermediaries in order to lower the cost of the transactions and also provides efficient deals.

They help in lowering the cost and economics of scale (Chen, 2018).

Financial intermediaries help in making the funds to invest in the securities which are

shortlisted. These intermediaries help in sourcing funds for the required once whom are in need,

for example, big companies or start-ups. They borrow goods from the lenders and individuals to

provide the once whom want to acquire. There are mainly two types of intermediaries, one is

asset based financial intermediaries and the other is fee based financial intermediaries which

provides broking services (Golubic, 2019).

The financial intermediaries play a central role in efficient allocation of resources.

Maturity transformation: These organisation helps in providing long term funds to the

organisation and ensuring borrowers the facilities of liquidity. It depends on the investors

whether they want to invest for short or long term basis.

Value Transformation: These firms pool penny savings and lend these funds to needy

one's.

Expertise: These are the expert in their field and provides specialised knowledge in

forecasting and anticipating the risk involved.

Reduction in transaction costs: These are the only one's whom act as an intermediary in

providing loans. Thus non other cost or brokerage is associated with it.

Ease of borrowing: The borrowers does not have to go here and there for the

requirement of funds.

These financial intermediaries may seem to be a good alternative just because they allow

the borrowers and lenders to connect with each other. Despite of advantages, they have major

disadvantages as well. The disadvantages are as follows-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Low returns on investments- In the end of the process, the ultimate goal of a financial

intermediaries is to earn profits, for this they usually provide with the low rate of interests

on investments which are made by the depositors.

Commissions and Fees- Another drawback is that they charge extra money from the

lenders and borrowers in providing the financial assistance service (Jalili, 2020).

Mismatched goals- A financial advisor and stock brokers might give the right advices

about the investments and saving opportunities. But their suggestions can come up with

the hidden risks that an investor might face. These intermediaries can take advantage of

the customers by giving the sub-optimal advice.

High interests on loans to the borrowers- As the ultimate goal of the financial

intermediaries is to earn profit, so in order to achieve the same they may even charge

high interest on the loan from its borrowers and this rate of interests helps in the

development of their organisation.

False opportunities- To provide the financial assistance services, these intermediaries

may come up with the different investment opportunities that ensures there will be high

return on investments with the involvement of little hidden risk (Kaakeh, Hassan, and van

Hemmen Almazor, 2018). The yield from such investments cannot be guaranteed and this

can be very risky for the customers.

In financial setting of an organisation, there are different kinds of financial intermediaries

present which have different motives to work as intermediary between the investors and the

borrowers. These are as follows-

1. Banks- These are the most popular source to provide the services on financial assistance.

They come up with the various specialities that involves saving, investing, lending etc.

They act as a linking pin between the lenders and the borrowers. Big companies also use

bank as a medium to find the investors.

2. Credit Unions- These are the union that bring up all the people together who are in need

of the money and those who have the money. So, if a person needs a loan from credit

union, they would receive it by using the funds that other person has contributed to the

credit union.

intermediaries is to earn profits, for this they usually provide with the low rate of interests

on investments which are made by the depositors.

Commissions and Fees- Another drawback is that they charge extra money from the

lenders and borrowers in providing the financial assistance service (Jalili, 2020).

Mismatched goals- A financial advisor and stock brokers might give the right advices

about the investments and saving opportunities. But their suggestions can come up with

the hidden risks that an investor might face. These intermediaries can take advantage of

the customers by giving the sub-optimal advice.

High interests on loans to the borrowers- As the ultimate goal of the financial

intermediaries is to earn profit, so in order to achieve the same they may even charge

high interest on the loan from its borrowers and this rate of interests helps in the

development of their organisation.

False opportunities- To provide the financial assistance services, these intermediaries

may come up with the different investment opportunities that ensures there will be high

return on investments with the involvement of little hidden risk (Kaakeh, Hassan, and van

Hemmen Almazor, 2018). The yield from such investments cannot be guaranteed and this

can be very risky for the customers.

In financial setting of an organisation, there are different kinds of financial intermediaries

present which have different motives to work as intermediary between the investors and the

borrowers. These are as follows-

1. Banks- These are the most popular source to provide the services on financial assistance.

They come up with the various specialities that involves saving, investing, lending etc.

They act as a linking pin between the lenders and the borrowers. Big companies also use

bank as a medium to find the investors.

2. Credit Unions- These are the union that bring up all the people together who are in need

of the money and those who have the money. So, if a person needs a loan from credit

union, they would receive it by using the funds that other person has contributed to the

credit union.

3. Pension Funds- This is the another very popular financial intermediary. It is used by the

millions of workers to save their retirement money by investing (Makanyeza, and

Mutambayashata, 2018).

4. Insurance companies- These are the entities known as insurer which are engaged in

providing the business services like annuities, casualty, credit life, dental, health, workers

compensation insurance to offset the risks for premium.

5. Stock Exchange- It is a market that connects the buyers with the stock sellers. In the

financial intermediary of this kind, trading of stock is the one of those companies that are

listed on the stock exchange, for which the sellers charges fees and interest rates.

6. Clearing Houses- These are the intermediaries that ensures the smooth flow for the

process of trade. They impose margin requirements to reduce the risk by providing extra

security so that the investors can trade freely. They safeguard the financial market

stability by providing security and efficiency.

7. Financial Advisors- These are the intermediaries that are in charge of performing trades

in the interests of their clients. These advisors use the experts to attain the financial

objectives of the customers. They assist the client in financial planning that involves the

areas like budgets, savings, insurance and tax-strategies (Mayes, Siklos, and Sturm,

2019).

PART D

Discussion related to the factors which determine the time-lag between the application of

instrument or tool of monetary policy and the achievement of the ultimate goal.

The transmission mechanism of monetary plan of action can be defined as a process of

formulating monetary policy decisions that affect prices of assets and economic conditions in

general. Such decisions affect the interest rates, amount of money, credit and aggregate demand

which would influence overall economic performance of a country and companies working in it.

It is a complex situation for economic analyst to predict how monetary policies would impact

economic conditions.

Actions planned by Central Bank:

millions of workers to save their retirement money by investing (Makanyeza, and

Mutambayashata, 2018).

4. Insurance companies- These are the entities known as insurer which are engaged in

providing the business services like annuities, casualty, credit life, dental, health, workers

compensation insurance to offset the risks for premium.

5. Stock Exchange- It is a market that connects the buyers with the stock sellers. In the

financial intermediary of this kind, trading of stock is the one of those companies that are

listed on the stock exchange, for which the sellers charges fees and interest rates.

6. Clearing Houses- These are the intermediaries that ensures the smooth flow for the

process of trade. They impose margin requirements to reduce the risk by providing extra

security so that the investors can trade freely. They safeguard the financial market

stability by providing security and efficiency.

7. Financial Advisors- These are the intermediaries that are in charge of performing trades

in the interests of their clients. These advisors use the experts to attain the financial

objectives of the customers. They assist the client in financial planning that involves the

areas like budgets, savings, insurance and tax-strategies (Mayes, Siklos, and Sturm,

2019).

PART D

Discussion related to the factors which determine the time-lag between the application of

instrument or tool of monetary policy and the achievement of the ultimate goal.

The transmission mechanism of monetary plan of action can be defined as a process of

formulating monetary policy decisions that affect prices of assets and economic conditions in

general. Such decisions affect the interest rates, amount of money, credit and aggregate demand

which would influence overall economic performance of a country and companies working in it.

It is a complex situation for economic analyst to predict how monetary policies would impact

economic conditions.

Actions planned by Central Bank:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Every bank working in any corner of the nation has comparative and essential objectives

which must be achieved by National banks. Value security, development of finance based areas

can be explained as an important goal which is laid down by national banks.

National banks can take the the help of money related approach instrument which would

help to cover loan related costs, achieve their objectives, manage savings, facilitate to manage

quantitative areas and hold exclusive rights (Minhas, 2020).

The impact of finance related arrangements in economy might not be clearly visible,

specifically when idea of cash partiality exists. The projects carried out by national banks can

affect economy and it might be possible that investor's present on national level have a feeling of

it. In simple words it can be concluded that approaches applied in financial areas can affect the

economy other than expansion & growth levels.

The very well-known method which is helpful for national banks that would affect the

economic conditions is the interest rate. Money related transmission is helpful from the point of

view of authority loan fee charged. It helps to calculate loan related issues and amounts which

would impact working of banks in an environment and affect economic conditions as well.

Assumptions, cost of resources, trade costs, assumptions, market rates can be viewed as

methods which help to assess changes in the authority loan fee which are to be conveyed in the

market and economy as well.

When central banks decide on increasing the official interest rate, lending rates of banks

to customers and bond yields will also rise. Alternation and modification in interest rate are

techniques used by central banks which would influence cost of borrowing in companies and in

case of consumers as well (Nso, 2018).

Modification in four channels are being examined which influence demand of products

and services:

Alteration in expectations and confidence level affect demand through direct channels.

People might seem less cautious and more focused for spending on goods and services if

they are capable of predicting future and what is the level of development in economy.

The wealth possessed have a direct impact on people's activity which will also prevail

changes in value of assets. People having a regular check on assets that are having the

right on such as watching increase or decrease in stock market or portfolio might give

them a wealthier feeling and they might have more power to spend in purchasing areas or

which must be achieved by National banks. Value security, development of finance based areas

can be explained as an important goal which is laid down by national banks.

National banks can take the the help of money related approach instrument which would

help to cover loan related costs, achieve their objectives, manage savings, facilitate to manage

quantitative areas and hold exclusive rights (Minhas, 2020).

The impact of finance related arrangements in economy might not be clearly visible,

specifically when idea of cash partiality exists. The projects carried out by national banks can

affect economy and it might be possible that investor's present on national level have a feeling of

it. In simple words it can be concluded that approaches applied in financial areas can affect the

economy other than expansion & growth levels.

The very well-known method which is helpful for national banks that would affect the

economic conditions is the interest rate. Money related transmission is helpful from the point of

view of authority loan fee charged. It helps to calculate loan related issues and amounts which

would impact working of banks in an environment and affect economic conditions as well.

Assumptions, cost of resources, trade costs, assumptions, market rates can be viewed as

methods which help to assess changes in the authority loan fee which are to be conveyed in the

market and economy as well.

When central banks decide on increasing the official interest rate, lending rates of banks

to customers and bond yields will also rise. Alternation and modification in interest rate are

techniques used by central banks which would influence cost of borrowing in companies and in

case of consumers as well (Nso, 2018).

Modification in four channels are being examined which influence demand of products

and services:

Alteration in expectations and confidence level affect demand through direct channels.

People might seem less cautious and more focused for spending on goods and services if

they are capable of predicting future and what is the level of development in economy.

The wealth possessed have a direct impact on people's activity which will also prevail

changes in value of assets. People having a regular check on assets that are having the

right on such as watching increase or decrease in stock market or portfolio might give

them a wealthier feeling and they might have more power to spend in purchasing areas or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have a feeling to sell part of their assets which will help to increase funds or apply for

credit using such assets as collateral.

Change in Exchange rate will affect import and export activities directly which would be

difficult to tackle. Exports can be beneficial if there is a decline in value of home

currency whereas It will be profitable in case of imports if rates increases.

Modification in market prices affect borrowing rates which affect demand and

consumption done on credit basis. It can be explained with the help of an example such

as if all the factors are kept at constant rate and there is a decline observed in case of

interest rates it might be possible that it appears more appealing for the one who is

planning to purchase home the reason being credit would be more easily available with

the customers for accessing credits. It will help consumer to collect funds easily and plan

its actions accordingly (NUREDINI, 2021).

Alternation in interest rates as stated above can have a direct effect on demand through

various steps. Changes in demand curve have a direct effect on pressure being felt due to

inflationary situations which would lead rise or decline in rates and would also have an impact

on pricing policies being decided. For example: A decline in interest rate would have a direct

effect on inflationary conditions if all situations are examined as equal the reason being:

Rise in value of assets, improved level of confidence and more accessibility in applying

for loans would in short help to have a boost in increased consumption. Prices can be observed to

be at peak if the demand rate rises higher than supply. Lower rate of interest will have

depreciation in home currency against the international currency which will result in rising cost

of imports. Rise in official rate of interest would have an adverse effect.

Methods of monetary policy are stated below:

Open market operations: For having an impact on supply of money, central banks

can purchase or sell assets issued by government. Central banks can purchase

government bonds. As a result, banks would be having the chance to apply for more

funds from the market which will help them to increase lending operations and economic

supply of money.

Interest rate adjustments: With the help of alternation made in interest rates, national

bank can have a direct impact on loan fees (Sabir and Qayyum, 2018). A national bank's

credit using such assets as collateral.

Change in Exchange rate will affect import and export activities directly which would be

difficult to tackle. Exports can be beneficial if there is a decline in value of home

currency whereas It will be profitable in case of imports if rates increases.

Modification in market prices affect borrowing rates which affect demand and

consumption done on credit basis. It can be explained with the help of an example such

as if all the factors are kept at constant rate and there is a decline observed in case of

interest rates it might be possible that it appears more appealing for the one who is

planning to purchase home the reason being credit would be more easily available with

the customers for accessing credits. It will help consumer to collect funds easily and plan

its actions accordingly (NUREDINI, 2021).

Alternation in interest rates as stated above can have a direct effect on demand through

various steps. Changes in demand curve have a direct effect on pressure being felt due to

inflationary situations which would lead rise or decline in rates and would also have an impact

on pricing policies being decided. For example: A decline in interest rate would have a direct

effect on inflationary conditions if all situations are examined as equal the reason being:

Rise in value of assets, improved level of confidence and more accessibility in applying

for loans would in short help to have a boost in increased consumption. Prices can be observed to

be at peak if the demand rate rises higher than supply. Lower rate of interest will have

depreciation in home currency against the international currency which will result in rising cost

of imports. Rise in official rate of interest would have an adverse effect.

Methods of monetary policy are stated below:

Open market operations: For having an impact on supply of money, central banks

can purchase or sell assets issued by government. Central banks can purchase

government bonds. As a result, banks would be having the chance to apply for more

funds from the market which will help them to increase lending operations and economic

supply of money.

Interest rate adjustments: With the help of alternation made in interest rates, national

bank can have a direct impact on loan fees (Sabir and Qayyum, 2018). A national bank's

base rate can be defined as finance related costs which is applied by banks for transient

loans. The time when national bank increases rebate rates the cost of expense availing it

from banks also rises. Banks increase finance related costs as they charge their

customers afterwards. The cost of getting will decrease in the economy which will shrink

the supply of cash as well.

Change reserve requirements: The standard of stores that a bank must have is set by

national banks. The national banks impact cash supply in the market by altering the kept

amount in banks. It is assumed that financial analysts increase the saving level which in

return would assess business banks to give less cash loans to their respected clients that

will result in decline of cash supply as well. The stores do not have the authority to

facilitate advance or put resources in new ventures by business bank (Wullweber, 2020).

CONCLUSION

From the above prepared report, it can be concluded that money, banking and finance

have various concepts which would help business and economy. The calculation of Net present

value and IRR are also explained in the report so carried. Borrowers and investors take help from

financial intermediaries in finance related areas. It also explains what have been the factors

which explains the applications and implementation of tools such as monetary policies that

would help to achieve desired goals and objectives. It helps how national banks will affect

financial arrange and how demand and supply of economy can be managed. There are many

tools which have been taken in account such as interest rate adjustments, change reserve

requirements and open market operations as well. There is analysis made for financial

intermediaries which would help in proper functioning of financial system. This report also

highlights the reason behind uses of yield to maturity, how it is calculated and what are the

reasons behind its calculation. It will help consumers and bank to have an idea about

intermediaries, market and economy as well.

loans. The time when national bank increases rebate rates the cost of expense availing it

from banks also rises. Banks increase finance related costs as they charge their

customers afterwards. The cost of getting will decrease in the economy which will shrink

the supply of cash as well.

Change reserve requirements: The standard of stores that a bank must have is set by

national banks. The national banks impact cash supply in the market by altering the kept

amount in banks. It is assumed that financial analysts increase the saving level which in

return would assess business banks to give less cash loans to their respected clients that

will result in decline of cash supply as well. The stores do not have the authority to

facilitate advance or put resources in new ventures by business bank (Wullweber, 2020).

CONCLUSION

From the above prepared report, it can be concluded that money, banking and finance

have various concepts which would help business and economy. The calculation of Net present

value and IRR are also explained in the report so carried. Borrowers and investors take help from

financial intermediaries in finance related areas. It also explains what have been the factors

which explains the applications and implementation of tools such as monetary policies that

would help to achieve desired goals and objectives. It helps how national banks will affect

financial arrange and how demand and supply of economy can be managed. There are many

tools which have been taken in account such as interest rate adjustments, change reserve

requirements and open market operations as well. There is analysis made for financial

intermediaries which would help in proper functioning of financial system. This report also

highlights the reason behind uses of yield to maturity, how it is calculated and what are the

reasons behind its calculation. It will help consumers and bank to have an idea about

intermediaries, market and economy as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abbas, F., Iqbal, S. and Aziz, B., 2020. The role of bank liquidity and bank risk in determining

bank capital: Empirical analysis of asian banking industry. Review of Pacific Basin Financial

Markets and Policies, 23(03), p.2050020.

Alami, I., 2019. Money power and financial capital in emerging markets: Facing the liquidity

tsunami. Routledge.

Borini, R., 2018. More Banking for Less Money. The WealthTech Book: The FinTech Handbook

for Investors, Entrepreneurs and Finance Visionaries, pp.273-274.

Cao, J., 2021. The Economics of Banking. Routledge.

Chazi, A., Mirzaei, A., and Azad, A.S., 2020. Does the size of Islamic banking matter for

industry growth: international evidence? Applied Economics, 52(4), pp.361-374.

Chen, K., 2018. Financial innovation and technology firms: A smart new world with machines.

In Banking and finance issues in emerging markets. Emerald Publishing Limited.

Golubic, G., 2019. Do Digital Technologies Have the Power to Disrupt Commercial

Banking. InterEULawEast: J. Int'l & Eur. L., Econ. & Market Integrations, 6, p.83.

Jalili, R., 2020. The Essentials of Islamic Banking, Finance, and Capital Markets by John

Oluseyi Kuforiji. Journal of Global South Studies, 37(2), pp.376-379.

Kaakeh, A., Hassan, M.K. and van Hemmen Almazor, S.F., 2018. Attitude of Muslim minority

in Spain towards Islamic finance. International Journal of Islamic and Middle Eastern

Finance and Management.

Makanyeza, C. and Mutambayashata, S., 2018. Consumers’ acceptance and use of plastic money

in Harare, Zimbabwe: Application of the unified theory of acceptance and use of

technology 2. International Journal of Bank Marketing.

Mayes, D.G., Siklos, P.L. and Sturm, J.E., 2019. The Oxford handbook of the economics of

central banking. Oxford Handbooks.

Minhas, I.H., 2020. Shariah Compliant Model of Islamic Banking. Journal of Islamic Banking &

Finance, 37(3).

Nso, M.A., 2018. Impact of Technology on E-Banking; Cameroon Perspectives. International

Journal of Advanced Networking and Applications, 9(6), pp.3645-3653.

NUREDINI, B., 2021. LEGAL ASPECTS OF INTEREST IN ISLAMIC VS.

CONVENTIONAL BANKING. Vizione, (36).

Sabir, S. and Qayyum, A., 2018. Competition in the Banking Sector of Pakistan: Evidence from

Unscaled and Scaled Revenue Equations1. Journal of Economic Cooperation &

Development, 39(1), pp.19-37.

Wullweber, J., 2020. Embedded finance: the shadow banking system, sovereign power, and a

new state–market hybridity. Journal of Cultural Economy, 13(5), pp.592-609.

Zhao, Y., Chupradit, S., and Khader, J., 2021. The role of technical efficiency, market

competition and risk in the banking performance in G20 countries. Business Process

Management Journal.

Books and Journals

Abbas, F., Iqbal, S. and Aziz, B., 2020. The role of bank liquidity and bank risk in determining

bank capital: Empirical analysis of asian banking industry. Review of Pacific Basin Financial

Markets and Policies, 23(03), p.2050020.

Alami, I., 2019. Money power and financial capital in emerging markets: Facing the liquidity

tsunami. Routledge.

Borini, R., 2018. More Banking for Less Money. The WealthTech Book: The FinTech Handbook

for Investors, Entrepreneurs and Finance Visionaries, pp.273-274.

Cao, J., 2021. The Economics of Banking. Routledge.

Chazi, A., Mirzaei, A., and Azad, A.S., 2020. Does the size of Islamic banking matter for

industry growth: international evidence? Applied Economics, 52(4), pp.361-374.

Chen, K., 2018. Financial innovation and technology firms: A smart new world with machines.

In Banking and finance issues in emerging markets. Emerald Publishing Limited.

Golubic, G., 2019. Do Digital Technologies Have the Power to Disrupt Commercial

Banking. InterEULawEast: J. Int'l & Eur. L., Econ. & Market Integrations, 6, p.83.

Jalili, R., 2020. The Essentials of Islamic Banking, Finance, and Capital Markets by John

Oluseyi Kuforiji. Journal of Global South Studies, 37(2), pp.376-379.

Kaakeh, A., Hassan, M.K. and van Hemmen Almazor, S.F., 2018. Attitude of Muslim minority

in Spain towards Islamic finance. International Journal of Islamic and Middle Eastern

Finance and Management.

Makanyeza, C. and Mutambayashata, S., 2018. Consumers’ acceptance and use of plastic money

in Harare, Zimbabwe: Application of the unified theory of acceptance and use of

technology 2. International Journal of Bank Marketing.

Mayes, D.G., Siklos, P.L. and Sturm, J.E., 2019. The Oxford handbook of the economics of

central banking. Oxford Handbooks.

Minhas, I.H., 2020. Shariah Compliant Model of Islamic Banking. Journal of Islamic Banking &

Finance, 37(3).

Nso, M.A., 2018. Impact of Technology on E-Banking; Cameroon Perspectives. International

Journal of Advanced Networking and Applications, 9(6), pp.3645-3653.

NUREDINI, B., 2021. LEGAL ASPECTS OF INTEREST IN ISLAMIC VS.

CONVENTIONAL BANKING. Vizione, (36).

Sabir, S. and Qayyum, A., 2018. Competition in the Banking Sector of Pakistan: Evidence from

Unscaled and Scaled Revenue Equations1. Journal of Economic Cooperation &

Development, 39(1), pp.19-37.

Wullweber, J., 2020. Embedded finance: the shadow banking system, sovereign power, and a

new state–market hybridity. Journal of Cultural Economy, 13(5), pp.592-609.

Zhao, Y., Chupradit, S., and Khader, J., 2021. The role of technical efficiency, market

competition and risk in the banking performance in G20 countries. Business Process

Management Journal.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.