APC312 Money, Banking, and Finance: Financial System Analysis

VerifiedAdded on 2023/06/14

|14

|3778

|244

Report

AI Summary

This report provides a comprehensive analysis of key financial concepts, including the calculation of Net Present Value (NPV) and Internal Rate of Return (IRR) for a project, along with a recommendation based on these calculations. It explains how Yield to Maturity (YTM) is used to calculate the Yield Curve and its significance. The report also analyzes the vital role of financial intermediaries in a well-functioning financial system, discussing various types of intermediaries and their functions. Furthermore, it discusses the time lag between the implementation of monetary policy instruments and the achievement of ultimate goals, exploring the monetary policy transmission process. Desklib offers this report as a valuable resource for students studying finance, providing insights and solutions to complex financial topics.

APC312 Money

Banking and Finance

Banking and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

I) Calculation of NPV..................................................................................................................3

II) Calculation of IRR..................................................................................................................3

III) Recommendation...................................................................................................................3

PART B...........................................................................................................................................4

Explain how Yield to maturity is used to calculate the Yield Curve and also explain why is

calculated.....................................................................................................................................4

PART C...........................................................................................................................................5

Analyse the statement ‘Financial Intermediaries are vital to well- functioning financial

system.’........................................................................................................................................5

PART D...........................................................................................................................................8

Discuss the time lag between the application of instruments or tool of monetary policies and

also explain the achievement of the ultimate goals.....................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

I) Calculation of NPV..................................................................................................................3

II) Calculation of IRR..................................................................................................................3

III) Recommendation...................................................................................................................3

PART B...........................................................................................................................................4

Explain how Yield to maturity is used to calculate the Yield Curve and also explain why is

calculated.....................................................................................................................................4

PART C...........................................................................................................................................5

Analyse the statement ‘Financial Intermediaries are vital to well- functioning financial

system.’........................................................................................................................................5

PART D...........................................................................................................................................8

Discuss the time lag between the application of instruments or tool of monetary policies and

also explain the achievement of the ultimate goals.....................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION

Finance refers to the actions that are taken by a business or an individual which are

associated with the management of the financial funds. Any business needs financial

funds to strategically manage the different operations related to the business. Banking

refers to activities which are taken up by the banks in an economy which helps in the

mobility of the financial funds of the people (Hamadi, . and Awdeh, ., 2020). Banking

acts as a bridge between the lenders and the borrowers of the financial funds. The

following report highlights the calculation of net present values, IRR following a

recommendation about the project. The YTM concept of IRR is also discussed. The

discussion related to the financial intermediaries is present following the factors which

determine the monetary transmission in an economy.

PART A

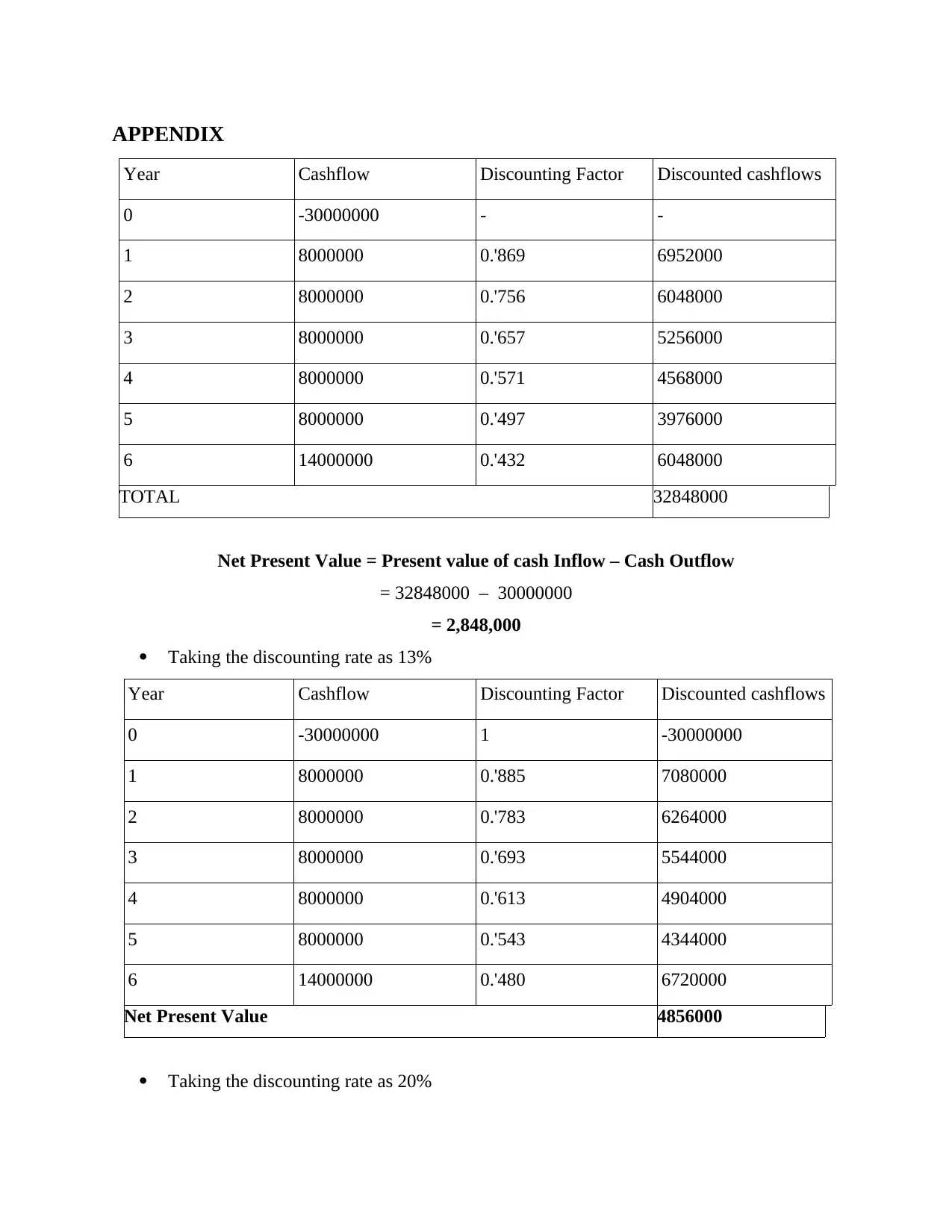

I) Calculation of NPV

The NPV for the project is £ 2,848,000

Note: Calculations are shown in Appendix

II) Calculation of IRR

The calculated IRR rate is 18.44%

Note: Calculations are shown in Appendix

III) Recommendation

The NPV shows the current values of the future cash flows from the project. The NPV

for the project is £ 2,848,000 which is positive for the business. The project is able to

earn 28 lacs of profit from the future years which makes the project a viable option for

the business (Zwass, , 2017).

The IRR from the business project is 18.44. any project is considered a viable option if

the IRR of the project is higher. The IRR of the project makes the project more viable.

Finance refers to the actions that are taken by a business or an individual which are

associated with the management of the financial funds. Any business needs financial

funds to strategically manage the different operations related to the business. Banking

refers to activities which are taken up by the banks in an economy which helps in the

mobility of the financial funds of the people (Hamadi, . and Awdeh, ., 2020). Banking

acts as a bridge between the lenders and the borrowers of the financial funds. The

following report highlights the calculation of net present values, IRR following a

recommendation about the project. The YTM concept of IRR is also discussed. The

discussion related to the financial intermediaries is present following the factors which

determine the monetary transmission in an economy.

PART A

I) Calculation of NPV

The NPV for the project is £ 2,848,000

Note: Calculations are shown in Appendix

II) Calculation of IRR

The calculated IRR rate is 18.44%

Note: Calculations are shown in Appendix

III) Recommendation

The NPV shows the current values of the future cash flows from the project. The NPV

for the project is £ 2,848,000 which is positive for the business. The project is able to

earn 28 lacs of profit from the future years which makes the project a viable option for

the business (Zwass, , 2017).

The IRR from the business project is 18.44. any project is considered a viable option if

the IRR of the project is higher. The IRR of the project makes the project more viable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART B

Explain how Yield to maturity is used to calculate the Yield Curve and also explain why is

calculated.

Internal Rate of Return for a project or business is determined by considering discounting

factor. This method is used to check the viability and feasibility. A higher rate of IRR is

considered to be good to accept a project. It shows that business will be able to earn a significant

amount of profit by selecting the project. Higher IRR is considered to be good for a project.

Yield to maturity is related with the investor in which investor themselves calculate the amount

of desired profit which they want to earn in future from their investment. YTM is a tool which

considers interest and capital gain/loss in determining the income derived from the project

(Haseeb, 2018).

YTM is a total sum which an individual will receive on the maturity of bonds. It is

basically a long term bond on which rate of return is calculated on yearly basis. In other terms, it

is the IRR of an investment as it is the final value after the maturity of the bond, all the payments

are to be on time and reinvested on the same interest rate. YTM is generally a Internal Rate of

return if the bonds are held till their maturity date. It is a complicated process to ascertain the

interest or coupon because it considers payments that are reinvested at the same rate as of the

bond (Wilson, , Wong, and Toms, eds., 2020).

Yield to Maturity divides the actual cash with the market price of the bonds to determine

the amount of money that the investor can realise from the investment made. It a price that the

investor will receive on future date by investing a sum at present. IRR is best way to calculate

the YTM and there is an alternate way of calculating yield to maturity,

YTM = Interest + (Redeemable value – Current Market Price) / N

(Current Market Price + Redeemable Value) / 2

From the above formula only estimated YTM is calculated and not the actual YTM. The amount

is calculated by using trial and error method in IRR method. The amount predicted on the

securities equals the amount of current value of the bond, the value of YTM is correct (Carlin,

and Lokanan, 2018).

Yield Curve is graphical representation of interest payment of the amount invested by the

investor, until they mature. It also includes the maturity value that the stakeholder will receive at

the time of maturity. If the amount received by the investor fluctuate up or down, then it can be

Explain how Yield to maturity is used to calculate the Yield Curve and also explain why is

calculated.

Internal Rate of Return for a project or business is determined by considering discounting

factor. This method is used to check the viability and feasibility. A higher rate of IRR is

considered to be good to accept a project. It shows that business will be able to earn a significant

amount of profit by selecting the project. Higher IRR is considered to be good for a project.

Yield to maturity is related with the investor in which investor themselves calculate the amount

of desired profit which they want to earn in future from their investment. YTM is a tool which

considers interest and capital gain/loss in determining the income derived from the project

(Haseeb, 2018).

YTM is a total sum which an individual will receive on the maturity of bonds. It is

basically a long term bond on which rate of return is calculated on yearly basis. In other terms, it

is the IRR of an investment as it is the final value after the maturity of the bond, all the payments

are to be on time and reinvested on the same interest rate. YTM is generally a Internal Rate of

return if the bonds are held till their maturity date. It is a complicated process to ascertain the

interest or coupon because it considers payments that are reinvested at the same rate as of the

bond (Wilson, , Wong, and Toms, eds., 2020).

Yield to Maturity divides the actual cash with the market price of the bonds to determine

the amount of money that the investor can realise from the investment made. It a price that the

investor will receive on future date by investing a sum at present. IRR is best way to calculate

the YTM and there is an alternate way of calculating yield to maturity,

YTM = Interest + (Redeemable value – Current Market Price) / N

(Current Market Price + Redeemable Value) / 2

From the above formula only estimated YTM is calculated and not the actual YTM. The amount

is calculated by using trial and error method in IRR method. The amount predicted on the

securities equals the amount of current value of the bond, the value of YTM is correct (Carlin,

and Lokanan, 2018).

Yield Curve is graphical representation of interest payment of the amount invested by the

investor, until they mature. It also includes the maturity value that the stakeholder will receive at

the time of maturity. If the amount received by the investor fluctuate up or down, then it can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tracked on the chart. X-axis represents interest payment and Y-axis represents number of years

until the maturity of the bonds (Roy, and Das, , 2020).

The individual whom are interested in the bonds monitor whether the firm is able to produce

good return to the existing investors or not. The investors monitor the curve on regular basis to

see the growth of the amount invested. If the investors get good return, then they continue to

hold the securities and if the bonds do not perform according to the expectation so the investors

then they sell the securities in the financial market. In order to save money from losing the

investor have to keep tracking on the current market prices.

The graph can be a normal curve, upturned curve, steep curve or parallel curve. The curve is

influenced by various factors such as economic growth, inflation and market interest rate. Before

taking final decision on the investment the investor needs to be thoroughly from the issue that

have caused such decline.

Followings factors are to evaluate before and after investing in funds.

Normal yield curve shows the stability of the organization in order to provide returns on

regular basis.

The curve of yield curve implies that the business concern is earning good returns on the

business operations.

Downward sloping Yield curve shows that the company is not able to perform well in

financial terms.

A Flat Curve shows the company is not able to give any return or any losses to the

investor on the amount invested in the bonds. For example, a person invests $1000 into a

company’s bond and current market price of the remains the same as of the issue price.

In this case the investor does not earn any return on the amount invested (Bennett, ,

2017).

PART C

Analyse the statement ‘Financial Intermediaries are vital to well- functioning financial system.’

Monetary Intermediate refers to an individual, group of individuals or an administration

which is a middleman among two or more bodies which are making a monetary transaction.

These may include, commercial banks, investment banks, mutual fund and pension fund. These

intermediaries provide the clients with variety of benefits like monetary safety, liquidity etc.

until the maturity of the bonds (Roy, and Das, , 2020).

The individual whom are interested in the bonds monitor whether the firm is able to produce

good return to the existing investors or not. The investors monitor the curve on regular basis to

see the growth of the amount invested. If the investors get good return, then they continue to

hold the securities and if the bonds do not perform according to the expectation so the investors

then they sell the securities in the financial market. In order to save money from losing the

investor have to keep tracking on the current market prices.

The graph can be a normal curve, upturned curve, steep curve or parallel curve. The curve is

influenced by various factors such as economic growth, inflation and market interest rate. Before

taking final decision on the investment the investor needs to be thoroughly from the issue that

have caused such decline.

Followings factors are to evaluate before and after investing in funds.

Normal yield curve shows the stability of the organization in order to provide returns on

regular basis.

The curve of yield curve implies that the business concern is earning good returns on the

business operations.

Downward sloping Yield curve shows that the company is not able to perform well in

financial terms.

A Flat Curve shows the company is not able to give any return or any losses to the

investor on the amount invested in the bonds. For example, a person invests $1000 into a

company’s bond and current market price of the remains the same as of the issue price.

In this case the investor does not earn any return on the amount invested (Bennett, ,

2017).

PART C

Analyse the statement ‘Financial Intermediaries are vital to well- functioning financial system.’

Monetary Intermediate refers to an individual, group of individuals or an administration

which is a middleman among two or more bodies which are making a monetary transaction.

These may include, commercial banks, investment banks, mutual fund and pension fund. These

intermediaries provide the clients with variety of benefits like monetary safety, liquidity etc.

these intermediaries serve as a middleman for the trades that take place between different

monetary institutions and their clients. These help the users of financial markets to have an

efficient deal and lower the different costs of the transactions. They make the threats lower,

provide economies of scale and decrease the prices (Rashid, Yousaf, and

Khaleequzzaman, , 2017).

The monetary intermediaries make the excess funds mobile. They help in transferring the

funds from parties who have extra of them and parties which require the funds for different

development aspects. In a economic system, the intermediaries that help in its operational. These

are in important source for the big corporations and start-ups of exterior funding. They borrow

goods from the creditors and persons who want to safeguard their assets and further lend these

excess funds to the businesses. Mainly, it’s the banks who play the role of intermediaries in a

monetary setting. There are two types of intermediaries which are, asset based fiscal

intermediaries like the banks and fee based economic intermediaries like the brokers which

provide portfolio organization.

The financial intermediaries have to play a dominant role in the fiscal market to ensure

efficient allocation of the resources. The main advantage of having economic intermediaries are

as follows:

Maturity transformation: Economic intermediaries provide long term funds to the

debtors meanwhile ensuring that the investors manage the fluidity. This is due to the fact

that dissimilar investors, invest their resources for short term and long term.

Worth Transformation: These intermediaries help in joining different small sums from

varied depositors and lend huge amount of money with the combining of the reserves.

Expertise: These individuals have detailed and specialist knowledge about the risk

management and foreseeing the productivity of the projects which the lenders and

borrowers may planning to take.

Reduction in transaction costs: These reduce the transaction cost by acting as a source

between the borrowers and lenders.

Ease of borrowing: The borrowers in any economy may find it easy as they do not have

to approach different lenders and may go to any one monetary intermediary.

monetary institutions and their clients. These help the users of financial markets to have an

efficient deal and lower the different costs of the transactions. They make the threats lower,

provide economies of scale and decrease the prices (Rashid, Yousaf, and

Khaleequzzaman, , 2017).

The monetary intermediaries make the excess funds mobile. They help in transferring the

funds from parties who have extra of them and parties which require the funds for different

development aspects. In a economic system, the intermediaries that help in its operational. These

are in important source for the big corporations and start-ups of exterior funding. They borrow

goods from the creditors and persons who want to safeguard their assets and further lend these

excess funds to the businesses. Mainly, it’s the banks who play the role of intermediaries in a

monetary setting. There are two types of intermediaries which are, asset based fiscal

intermediaries like the banks and fee based economic intermediaries like the brokers which

provide portfolio organization.

The financial intermediaries have to play a dominant role in the fiscal market to ensure

efficient allocation of the resources. The main advantage of having economic intermediaries are

as follows:

Maturity transformation: Economic intermediaries provide long term funds to the

debtors meanwhile ensuring that the investors manage the fluidity. This is due to the fact

that dissimilar investors, invest their resources for short term and long term.

Worth Transformation: These intermediaries help in joining different small sums from

varied depositors and lend huge amount of money with the combining of the reserves.

Expertise: These individuals have detailed and specialist knowledge about the risk

management and foreseeing the productivity of the projects which the lenders and

borrowers may planning to take.

Reduction in transaction costs: These reduce the transaction cost by acting as a source

between the borrowers and lenders.

Ease of borrowing: The borrowers in any economy may find it easy as they do not have

to approach different lenders and may go to any one monetary intermediary.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In a fiscal setting of an organisation, there are different types of monetary intermediaries present

which have different purpose to work as in middle between the depositors and the debtors

(Robin, I Salim, and Bloch, , 2018). These different intermediaries are discussed below:

The different intermediaries are:

1. Banks- these refer to the main intermediary in a financial system and provide different credit

services to the customers. These services include, debit cards, credit card, net banking, loan

policies etc.

2. Stock Exchange- these are the financial marketplace which helps in buying and selling of the

stock of companies. They charge brokerage for the services provided.

3. Credit Unions- they are working in the cooperative sector and provide credit services to the

members of the union.

4. Non-banking finance companies- they provide services to attain loans for clients of the

business at large interest rates.

5. Insurance Companies- They provide security to the clients on the different unforeseeable

events like accidents, crash, natural calamity etc. The attain premium for the insurance provided

for assets.

6. Mutual Fund Companies- They provide services to invest the funds of individuals in different

securities bonds and other options to attain a capital gain in long run. These organizations collect

amount from various capitalist with investment verifiable which are identical and have the power

to take risks connected with investment (Mhella, 2019).

7. Financial Advisors and brokers- They are the people who advise the individuals about the

different risks which are associated with the financial investments. The brokers help in bridging

the gap between investors and the companies.

8. Investment Bankers- They help in satisfying the conditions for IPOs of a company.

9.Escrow Companies- These companies help the borrowers to attain loan and fully satisfy the

mortgage conditions of a business.

10.Collective Investment Schemes- This is a group of investors which have a common motive

and hence, they come together to add their funds and invest into a major investment option.

which have different purpose to work as in middle between the depositors and the debtors

(Robin, I Salim, and Bloch, , 2018). These different intermediaries are discussed below:

The different intermediaries are:

1. Banks- these refer to the main intermediary in a financial system and provide different credit

services to the customers. These services include, debit cards, credit card, net banking, loan

policies etc.

2. Stock Exchange- these are the financial marketplace which helps in buying and selling of the

stock of companies. They charge brokerage for the services provided.

3. Credit Unions- they are working in the cooperative sector and provide credit services to the

members of the union.

4. Non-banking finance companies- they provide services to attain loans for clients of the

business at large interest rates.

5. Insurance Companies- They provide security to the clients on the different unforeseeable

events like accidents, crash, natural calamity etc. The attain premium for the insurance provided

for assets.

6. Mutual Fund Companies- They provide services to invest the funds of individuals in different

securities bonds and other options to attain a capital gain in long run. These organizations collect

amount from various capitalist with investment verifiable which are identical and have the power

to take risks connected with investment (Mhella, 2019).

7. Financial Advisors and brokers- They are the people who advise the individuals about the

different risks which are associated with the financial investments. The brokers help in bridging

the gap between investors and the companies.

8. Investment Bankers- They help in satisfying the conditions for IPOs of a company.

9.Escrow Companies- These companies help the borrowers to attain loan and fully satisfy the

mortgage conditions of a business.

10.Collective Investment Schemes- This is a group of investors which have a common motive

and hence, they come together to add their funds and invest into a major investment option.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART D

Discuss the time lag between the application of instruments or tool of monetary policies and also

explain the achievement of the ultimate goals.

The communication tool of monetary policy refers to the procedure with which the price level in

an economy and the overall rates are exaggerated. The process is lengthy and vigorous having

tentative time lags. Hence, it is hard for the economist to forecast the consequence of the

monetary procedure on the economy. The transmission process affects the monetary policy of the

business and the economic growth, prices and other aspects (Königstorfer,. and Thalmann,

2020).

Action of central bank:

National banks from one side of the globe to the other have proportional objectives.

Worth security is the vital objective of national banks, although low unemployment and long

haul fiscal growth are often important objects also.

National banks can exploit a diversity of currency related technique instruments to

accomplish their aims, containing loan costs, measureable facilitating/fixing, grip prerequisites,

and superior on saves.

The effects of fiscal procedure on the economy may not be punctually marked, especially

assuming that the idea of cash objectivity is upheld. The actions of national banks to try to

outcome the economy, then again, infer that countrywide investor feel that, essentially in the

close to word, economic approach can influence the economy rather than only growth stages.

The best well-known tool applied by national banks to distress the economy is the

authorized interest rate (Maison, 2019).. We'll take a glimpse at the money associated

transmission gadget essentially from the viewpoint of the consultant loan fee.

Market rates, conventions, source costs, and profession rates are viewed as the four roads

through which variations in the ability loan fee are flourished to the economy.

As a outcome of central banks rising (lowering) the official interest rate, bank advancing

rates and pledge yields will upsurge (fall). Changes in the authorised interest rate are one way for

central banks to impact the charge of borrowing for concerns and customers.

Changes in the four stations studied impact demand for goods and facilities,

Discuss the time lag between the application of instruments or tool of monetary policies and also

explain the achievement of the ultimate goals.

The communication tool of monetary policy refers to the procedure with which the price level in

an economy and the overall rates are exaggerated. The process is lengthy and vigorous having

tentative time lags. Hence, it is hard for the economist to forecast the consequence of the

monetary procedure on the economy. The transmission process affects the monetary policy of the

business and the economic growth, prices and other aspects (Königstorfer,. and Thalmann,

2020).

Action of central bank:

National banks from one side of the globe to the other have proportional objectives.

Worth security is the vital objective of national banks, although low unemployment and long

haul fiscal growth are often important objects also.

National banks can exploit a diversity of currency related technique instruments to

accomplish their aims, containing loan costs, measureable facilitating/fixing, grip prerequisites,

and superior on saves.

The effects of fiscal procedure on the economy may not be punctually marked, especially

assuming that the idea of cash objectivity is upheld. The actions of national banks to try to

outcome the economy, then again, infer that countrywide investor feel that, essentially in the

close to word, economic approach can influence the economy rather than only growth stages.

The best well-known tool applied by national banks to distress the economy is the

authorized interest rate (Maison, 2019).. We'll take a glimpse at the money associated

transmission gadget essentially from the viewpoint of the consultant loan fee.

Market rates, conventions, source costs, and profession rates are viewed as the four roads

through which variations in the ability loan fee are flourished to the economy.

As a outcome of central banks rising (lowering) the official interest rate, bank advancing

rates and pledge yields will upsurge (fall). Changes in the authorised interest rate are one way for

central banks to impact the charge of borrowing for concerns and customers.

Changes in the four stations studied impact demand for goods and facilities,

Variations in market rates have an impact on borrowing prices, which has an

influence on credit request and intake. For example, all other variables remain

constant, a drop in interest rates may make a hypothecation for the acquisition of a

household more tempting or make customer credit more available. The wealth

impact disturbs people's intake as asset ethics change. A person who lookouts the

value of his or her assortment of properties rise may feel richer and be more likely to

spend, or even trade part of his or her properties to fund expenditure or receive credit

using their growing assets as security (Nesvetailova, ed., 2017)(Naheem, ,

2018)

Changes in self-confidence and hopes can also have an influence on claim. People

may be less careful and more tending to use on goods and facilities if they forecast

financial expansion.

Exchange rate variations can have an effect on imports and exports. Exports can

yield profit from a decrease in the worth of the home exchange, while imports can

increase from a rise in the price.

Variations in authorised interest rates, as earlier indicated, can impact demand through a

variation of opportunities. Fluctuations in demand have an influence on valuing, causing

inflationary weights to rise or fall. A reduction in interest rates, for example, would have an

inflationary impact if all other circumstances were equal, principally because:

Rises in asset values, enhanced confidence, and more loan accessibility would all support

to boost intake. Morals will be driven advanced if demand familiarises quicker than quantity.

Inferior interest rates would help the devaluation of the home exchange against the overseas

currency, resulting in a rise in import costs. An rise in the authorised interest rate would have the

contradictory effect.

Tools of Monetary Policy are as follows:

1. Interest rate adjustment- By changing the interest rate, a domestic bank can disturb

loan fees. A national bank's reimbursement rate (base rate) is the funding cost it burdens

banks for fleeting loaning. When a national bank increases the rebate rate, for instance,

the expenditure of getting for banks rises. Banks will advance the funding cost they

influence on credit request and intake. For example, all other variables remain

constant, a drop in interest rates may make a hypothecation for the acquisition of a

household more tempting or make customer credit more available. The wealth

impact disturbs people's intake as asset ethics change. A person who lookouts the

value of his or her assortment of properties rise may feel richer and be more likely to

spend, or even trade part of his or her properties to fund expenditure or receive credit

using their growing assets as security (Nesvetailova, ed., 2017)(Naheem, ,

2018)

Changes in self-confidence and hopes can also have an influence on claim. People

may be less careful and more tending to use on goods and facilities if they forecast

financial expansion.

Exchange rate variations can have an effect on imports and exports. Exports can

yield profit from a decrease in the worth of the home exchange, while imports can

increase from a rise in the price.

Variations in authorised interest rates, as earlier indicated, can impact demand through a

variation of opportunities. Fluctuations in demand have an influence on valuing, causing

inflationary weights to rise or fall. A reduction in interest rates, for example, would have an

inflationary impact if all other circumstances were equal, principally because:

Rises in asset values, enhanced confidence, and more loan accessibility would all support

to boost intake. Morals will be driven advanced if demand familiarises quicker than quantity.

Inferior interest rates would help the devaluation of the home exchange against the overseas

currency, resulting in a rise in import costs. An rise in the authorised interest rate would have the

contradictory effect.

Tools of Monetary Policy are as follows:

1. Interest rate adjustment- By changing the interest rate, a domestic bank can disturb

loan fees. A national bank's reimbursement rate (base rate) is the funding cost it burdens

banks for fleeting loaning. When a national bank increases the rebate rate, for instance,

the expenditure of getting for banks rises. Banks will advance the funding cost they

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

burden their clients afterward. Subsequently, the expenditure of obtaining will ascend all

through the economy, while the cash source will shrink.

2. Change reserve requirements- The base degree of stores that a commercial bank should

have is normally established by national banks. The national bank can disturb the cash

quantity in the economy by changing the required amount. Assuming monetary

specialists raise the essential save level, corporate banks would have less cash to loan to

their clients, declining cash supply (Isedu, 2017.. The stores can't be operated to make

advances or put incomes into new undertakings by business banks. National banks pay

commercial banks revenue on protects since it is a wasted an open door for them. The

pace of interest is mentioned to as IOR or IORR.

Open market Operations- To impact the cash supply, the chief bank can purchase or trade

government-issued properties. Central banks, for example, can buy administration bonds. As a

consequence, banks will be able to derive extra funds, permitting them to increase lending and

the economy's cash quantity.

CONCLUSION

From the above mentioned report it can be concluded that the concept of banking and

finance is important to be understood and the financial intermediaries play a vital role in

an economy. The calculation of NPV shows the current price of the future cash flow

from a project. The IRR is a trial and error method which helps the strategic managers

to take decision related to a project.

through the economy, while the cash source will shrink.

2. Change reserve requirements- The base degree of stores that a commercial bank should

have is normally established by national banks. The national bank can disturb the cash

quantity in the economy by changing the required amount. Assuming monetary

specialists raise the essential save level, corporate banks would have less cash to loan to

their clients, declining cash supply (Isedu, 2017.. The stores can't be operated to make

advances or put incomes into new undertakings by business banks. National banks pay

commercial banks revenue on protects since it is a wasted an open door for them. The

pace of interest is mentioned to as IOR or IORR.

Open market Operations- To impact the cash supply, the chief bank can purchase or trade

government-issued properties. Central banks, for example, can buy administration bonds. As a

consequence, banks will be able to derive extra funds, permitting them to increase lending and

the economy's cash quantity.

CONCLUSION

From the above mentioned report it can be concluded that the concept of banking and

finance is important to be understood and the financial intermediaries play a vital role in

an economy. The calculation of NPV shows the current price of the future cash flow

from a project. The IRR is a trial and error method which helps the strategic managers

to take decision related to a project.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Bennett, G., 2017. China's finance and trade: a policy reader. Routledge.

Carlin, A. and Lokanan, M.E., 2018. Ritualisation and money laundering in the Swiss banking

sector. Journal of Money Laundering Con

Hamadi, H. and Awdeh, A., 2020. Banking concentration and financial development in the

MENA region. International Journal of Islamic and Middle Eastern Finance and

Management.

Haseeb, M., 2018. Emerging issues in islamic banking & finance: Challenges and Solutions.

Academy of Accounting and Financial Studies Journal, 22, pp.1-5.

Isedu, M.O., 2017. Effects of Monetary Policy on Commercial Banks Performance in Nigeria.

Königstorfer, F. and Thalmann, S., 2020. Applications of Artificial Intelligence in commercial

banks–A research agenda for behavioral finance. Journal of behavioral and

experimental finance, 27, p.100352.

Maison, D., 2019. Banking, Unbanking, and New Banking. In The Psychology of Financial

Consumer Behavior (pp. 185-208). Springer, Cham.

Mhella, D.J., 2019, August. Banking Sector’s Response to the High Levels of Financial

Inclusion Caused by Mobile Money Innovations in Tanzania. In [2019-MADRID]

Congreso Internacional de Tecnología, Ciencia y Sociedad.

Naheem, M.A., 2018. FIFA–highlighting the links between global banking and international

money laundering. Journal of Money Laundering Control.

Nesvetailova, A. ed., 2017. Shadow banking: Scope, origins and theories. Routledge.

Rashid, A., Yousaf, S. and Khaleequzzaman, M., 2017. Does Islamic banking really strengthen

financial stability? Empirical evidence from Pakistan. International Journal of Islamic

and Middle Eastern Finance and Management.

Robin, I., Salim, R. and Bloch, H., 2018. Financial performance of commercial banks in the

post-reform era: Further evidence from Bangladesh. Economic Analysis and Policy, 58,

pp.43-54.

Roy, S. and Das, S., 2020. Impact of Environmental Elements on Sustainable Economic

Growth: Evidence from BIMSTEC. Wealth: International Journal of Money, Banking &

Finance, 9(1).

Wilson, J.F., Wong, N.D. and Toms, S. eds., 2020. Banking and Finance: Case studies in the

development of the UK financial sector. Routledge.

Zwass, A., 2017. Money, Banking, & Credit in the Soviet Union & Eastern Europe. Routledge.

Books and Journals

Bennett, G., 2017. China's finance and trade: a policy reader. Routledge.

Carlin, A. and Lokanan, M.E., 2018. Ritualisation and money laundering in the Swiss banking

sector. Journal of Money Laundering Con

Hamadi, H. and Awdeh, A., 2020. Banking concentration and financial development in the

MENA region. International Journal of Islamic and Middle Eastern Finance and

Management.

Haseeb, M., 2018. Emerging issues in islamic banking & finance: Challenges and Solutions.

Academy of Accounting and Financial Studies Journal, 22, pp.1-5.

Isedu, M.O., 2017. Effects of Monetary Policy on Commercial Banks Performance in Nigeria.

Königstorfer, F. and Thalmann, S., 2020. Applications of Artificial Intelligence in commercial

banks–A research agenda for behavioral finance. Journal of behavioral and

experimental finance, 27, p.100352.

Maison, D., 2019. Banking, Unbanking, and New Banking. In The Psychology of Financial

Consumer Behavior (pp. 185-208). Springer, Cham.

Mhella, D.J., 2019, August. Banking Sector’s Response to the High Levels of Financial

Inclusion Caused by Mobile Money Innovations in Tanzania. In [2019-MADRID]

Congreso Internacional de Tecnología, Ciencia y Sociedad.

Naheem, M.A., 2018. FIFA–highlighting the links between global banking and international

money laundering. Journal of Money Laundering Control.

Nesvetailova, A. ed., 2017. Shadow banking: Scope, origins and theories. Routledge.

Rashid, A., Yousaf, S. and Khaleequzzaman, M., 2017. Does Islamic banking really strengthen

financial stability? Empirical evidence from Pakistan. International Journal of Islamic

and Middle Eastern Finance and Management.

Robin, I., Salim, R. and Bloch, H., 2018. Financial performance of commercial banks in the

post-reform era: Further evidence from Bangladesh. Economic Analysis and Policy, 58,

pp.43-54.

Roy, S. and Das, S., 2020. Impact of Environmental Elements on Sustainable Economic

Growth: Evidence from BIMSTEC. Wealth: International Journal of Money, Banking &

Finance, 9(1).

Wilson, J.F., Wong, N.D. and Toms, S. eds., 2020. Banking and Finance: Case studies in the

development of the UK financial sector. Routledge.

Zwass, A., 2017. Money, Banking, & Credit in the Soviet Union & Eastern Europe. Routledge.

APPENDIX

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 - -

1 8000000 0.'869 6952000

2 8000000 0.'756 6048000

3 8000000 0.'657 5256000

4 8000000 0.'571 4568000

5 8000000 0.'497 3976000

6 14000000 0.'432 6048000

TOTAL 32848000

Net Present Value = Present value of cash Inflow – Cash Outflow

= 32848000 – 30000000

= 2,848,000

Taking the discounting rate as 13%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 1 -30000000

1 8000000 0.'885 7080000

2 8000000 0.'783 6264000

3 8000000 0.'693 5544000

4 8000000 0.'613 4904000

5 8000000 0.'543 4344000

6 14000000 0.'480 6720000

Net Present Value 4856000

Taking the discounting rate as 20%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 - -

1 8000000 0.'869 6952000

2 8000000 0.'756 6048000

3 8000000 0.'657 5256000

4 8000000 0.'571 4568000

5 8000000 0.'497 3976000

6 14000000 0.'432 6048000

TOTAL 32848000

Net Present Value = Present value of cash Inflow – Cash Outflow

= 32848000 – 30000000

= 2,848,000

Taking the discounting rate as 13%

Year Cashflow Discounting Factor Discounted cashflows

0 -30000000 1 -30000000

1 8000000 0.'885 7080000

2 8000000 0.'783 6264000

3 8000000 0.'693 5544000

4 8000000 0.'613 4904000

5 8000000 0.'543 4344000

6 14000000 0.'480 6720000

Net Present Value 4856000

Taking the discounting rate as 20%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.