Movement From Traditional to Modern Cost Accounting Methods in Manufacturing Companies

Added on 2023-05-27

26 Pages8219 Words162 Views

155

Movement From Traditional to Modern

Cost Accounting Methods in

Manufacturing Companies (*)

Hrvoje Perčević

University of Zagreb, Croatia

Mirjana Hladika

University of Zagreb, Croatia

Abstract

Significant changes in business environment at the end of 20th century and

the beginning of 21st century enable the development and application of modern

cost accounting methods which main purpose is to give required information to

management regarding the effectiveness of certain products, projects, activities,

consumers, responsibility centres etc. Traditional cost accounting methods were

developed in the middle of 20th century due to the automation of production. The

focus of traditional cost accounting methods was on manufacturing cost and ways

of indirect manufacturing costs allocation to products or services. But, further

development of technology, changes in consumer’s preferences, global competition

face modern manufacturing companies with permanent challenges of survival at

the global market. Traditional cost accounting methods are no longer appropriate in

modern business conditions, because cost accounting methods should indicate the

potential areas in companies where are possible cost savings. Therefore, modern

cost accounting methods are focused on cost rationalization and cost reduction,

since modern manufacturing companies cannot effect on market prices but can

effect on their costs. In current business conditions, modern cost accounting methods

(*) Bu Araştırma, 19-22 Haziran 2013 tarihinde İstanbul’da yapılan 3rd

International Conference on Luca Pacioli in Accounting History’de ve 3rd Balkans

and Middle East Countries Conference on Accounting and Accounting History

(3 BMAC) Konferansı’nda bildiri olarak sunulmuştur.

Movement From Traditional to Modern

Cost Accounting Methods in

Manufacturing Companies (*)

Hrvoje Perčević

University of Zagreb, Croatia

Mirjana Hladika

University of Zagreb, Croatia

Abstract

Significant changes in business environment at the end of 20th century and

the beginning of 21st century enable the development and application of modern

cost accounting methods which main purpose is to give required information to

management regarding the effectiveness of certain products, projects, activities,

consumers, responsibility centres etc. Traditional cost accounting methods were

developed in the middle of 20th century due to the automation of production. The

focus of traditional cost accounting methods was on manufacturing cost and ways

of indirect manufacturing costs allocation to products or services. But, further

development of technology, changes in consumer’s preferences, global competition

face modern manufacturing companies with permanent challenges of survival at

the global market. Traditional cost accounting methods are no longer appropriate in

modern business conditions, because cost accounting methods should indicate the

potential areas in companies where are possible cost savings. Therefore, modern

cost accounting methods are focused on cost rationalization and cost reduction,

since modern manufacturing companies cannot effect on market prices but can

effect on their costs. In current business conditions, modern cost accounting methods

(*) Bu Araştırma, 19-22 Haziran 2013 tarihinde İstanbul’da yapılan 3rd

International Conference on Luca Pacioli in Accounting History’de ve 3rd Balkans

and Middle East Countries Conference on Accounting and Accounting History

(3 BMAC) Konferansı’nda bildiri olarak sunulmuştur.

156

are more appropriate while they are focused on the total costs through the whole

product life cycle. This paper deals with the modern cost accounting methods and

their application in manufacturing companies. The results are showing that modern

cost accounting methods enables more confidential determination of the real product

profitability. But it is also important to state that research results show that modern

cost accounting methods should be applied together with traditional cost accounting

methods. Traditional cost accounting methods give information regarding cost in

short term, while modern methods are orientated on longer period (e. g. on the whole

product life cycle).

Key words: Traditional Cost Accounting Methods, Modern Cost Accounting

Methods, ABC, Target Costing, Life Cycle Costing, Product Profitability.

Jel Classificiation: M21, M4A, M51

1. Introduction

The basic purpose of costing systems is to determine the cost of a

product or service by assigning manufacturing costs to products or services

that company produces or provides. Costing system consist of different

accounting methods used in order to define the cost per unit. Accounting

methods used in costing system enable the evaluation of products as a result

from the manufacturing process. It is important to point out that different

costing systems differently affect the product evaluation. The choice of

costing system was based on the type of the production process. Therefore,

job order costing was used in job order production, while process costing

was applied in process or mass production. Today, these two costing systems

are considered as traditional costing systems which are no longer suitable to

use in modern operating conditions. Business conditions are changing rapidly

becoming more and more complex. Manufacturing processes in modern

production companies are almost fully automated and computerized. The

process of manufacturing automation and computerization causes significant

change in manufacturing cost structure. The most important cost element in

modern manufacturing cost structure becomes indirect manufacturing costs

are more appropriate while they are focused on the total costs through the whole

product life cycle. This paper deals with the modern cost accounting methods and

their application in manufacturing companies. The results are showing that modern

cost accounting methods enables more confidential determination of the real product

profitability. But it is also important to state that research results show that modern

cost accounting methods should be applied together with traditional cost accounting

methods. Traditional cost accounting methods give information regarding cost in

short term, while modern methods are orientated on longer period (e. g. on the whole

product life cycle).

Key words: Traditional Cost Accounting Methods, Modern Cost Accounting

Methods, ABC, Target Costing, Life Cycle Costing, Product Profitability.

Jel Classificiation: M21, M4A, M51

1. Introduction

The basic purpose of costing systems is to determine the cost of a

product or service by assigning manufacturing costs to products or services

that company produces or provides. Costing system consist of different

accounting methods used in order to define the cost per unit. Accounting

methods used in costing system enable the evaluation of products as a result

from the manufacturing process. It is important to point out that different

costing systems differently affect the product evaluation. The choice of

costing system was based on the type of the production process. Therefore,

job order costing was used in job order production, while process costing

was applied in process or mass production. Today, these two costing systems

are considered as traditional costing systems which are no longer suitable to

use in modern operating conditions. Business conditions are changing rapidly

becoming more and more complex. Manufacturing processes in modern

production companies are almost fully automated and computerized. The

process of manufacturing automation and computerization causes significant

change in manufacturing cost structure. The most important cost element in

modern manufacturing cost structure becomes indirect manufacturing costs

157

(manufacturing overheads). This change in manufacturing cost structure

found traditional costing systems inappropriate for product evaluation.

In order to avoid the inaccuracy of traditional costing systems in product

evaluation, the new costing system, based on activities, has been developed.

This costing system is known as Activity based costing.

2. The Types of Costing Systems

Costing system can be defined as a system used to assign costs to

cost objects (products or services). The main purpose of costing system is to

enable cost assignment. Cost assignment is the process of assigning direct

and indirect costs to products or services in order to determine the cost of a

product or service.

Each costing system consists of five basic elements:1

1. cost object – anything for which a measurement of cost is

desired. Usually, cost objects are products or services that certain company

manufactures or provides.

2. direct costs of a cost object – these are costs that can be traced to

a particular product or service

3. indirect costs of a cost object – these are costs that cannot be traced

to a particular product or service. Indirect costs need to be allocated to cost

objects using a proper cost allocation method.

4. cost pool – a grouping of individual cost item. The cost pools are

formed when company uses more cost allocation bases. In ABC system, cost

pools are identified activities to which indirect costs are assigning.

5. cost allocation base – the factor that links in a systematic way an

indirect cost (or group of indirect cost) to a particular cost object.

1) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey, p. 96-97.

(manufacturing overheads). This change in manufacturing cost structure

found traditional costing systems inappropriate for product evaluation.

In order to avoid the inaccuracy of traditional costing systems in product

evaluation, the new costing system, based on activities, has been developed.

This costing system is known as Activity based costing.

2. The Types of Costing Systems

Costing system can be defined as a system used to assign costs to

cost objects (products or services). The main purpose of costing system is to

enable cost assignment. Cost assignment is the process of assigning direct

and indirect costs to products or services in order to determine the cost of a

product or service.

Each costing system consists of five basic elements:1

1. cost object – anything for which a measurement of cost is

desired. Usually, cost objects are products or services that certain company

manufactures or provides.

2. direct costs of a cost object – these are costs that can be traced to

a particular product or service

3. indirect costs of a cost object – these are costs that cannot be traced

to a particular product or service. Indirect costs need to be allocated to cost

objects using a proper cost allocation method.

4. cost pool – a grouping of individual cost item. The cost pools are

formed when company uses more cost allocation bases. In ABC system, cost

pools are identified activities to which indirect costs are assigning.

5. cost allocation base – the factor that links in a systematic way an

indirect cost (or group of indirect cost) to a particular cost object.

1) Horngren, C.T., Datar, S.M., Foster, G. (2003), Cost Accounting – A

Managerial Emphasis, Prentice Hall, New Jersey, p. 96-97.

158

These five elements are using to design an adequate costing system.

There are three basic costing systems used in

manufacturing companies in order to determine the cost of

a particular product or to evaluate product profitability:2

1. job order costing,

2. process costing,

3. activity based costing.

The first two costing systems are known as traditional costing

systems. While the appliance of traditional costing systems depend on the

type of a manufacturing process, activity based costing system can be applied

regardless the type of manufacturing process. The main issue for companies is:

when is convenient to use traditional costing systems and when activity based

costing system should be applied? To answer on this question the operating

conditions and the manufacturing cost structure should be considered.

2.1. Cost allocation in traditional costing systems

The basic distinction between job costing and process costing system

is in determination of cost object. In job costing cost object is a job which

consists of a unit or multiple units of distinct products or services. In process

costing cost object is masses of identical or similar units of a product or service.

Therefore, job costing can be applied in manufacturing which is initiated by a

customer’s order, while process costing can be used in mass production which

is continually performing and is not initiated by a customer’s order.

Cost allocation is similar in job costing and in process costing. In

both costing systems direct manufacturing costs are traced to products or

services. These costs are directly assigned to particular products or services

which cause their appearance. Direct manufacturing costs include direct

material costs and direct labour costs. The main problem of every costing

system is indirect manufacturing costs allocation. Because these costs cannot

2) Lucey, T. (1996), Costing, DP Publications, London, p. 175-176.

These five elements are using to design an adequate costing system.

There are three basic costing systems used in

manufacturing companies in order to determine the cost of

a particular product or to evaluate product profitability:2

1. job order costing,

2. process costing,

3. activity based costing.

The first two costing systems are known as traditional costing

systems. While the appliance of traditional costing systems depend on the

type of a manufacturing process, activity based costing system can be applied

regardless the type of manufacturing process. The main issue for companies is:

when is convenient to use traditional costing systems and when activity based

costing system should be applied? To answer on this question the operating

conditions and the manufacturing cost structure should be considered.

2.1. Cost allocation in traditional costing systems

The basic distinction between job costing and process costing system

is in determination of cost object. In job costing cost object is a job which

consists of a unit or multiple units of distinct products or services. In process

costing cost object is masses of identical or similar units of a product or service.

Therefore, job costing can be applied in manufacturing which is initiated by a

customer’s order, while process costing can be used in mass production which

is continually performing and is not initiated by a customer’s order.

Cost allocation is similar in job costing and in process costing. In

both costing systems direct manufacturing costs are traced to products or

services. These costs are directly assigned to particular products or services

which cause their appearance. Direct manufacturing costs include direct

material costs and direct labour costs. The main problem of every costing

system is indirect manufacturing costs allocation. Because these costs cannot

2) Lucey, T. (1996), Costing, DP Publications, London, p. 175-176.

Shubham Mishra_JPR

12/11/2018, 11:33:17 AM

159

be directly identified to particular product or service, indirect manufacturing

costs need to be allocated to products or services on some reasonable bases

which correctly present the relationship between indirect manufacturing

costs and certain product. This relationship is often very difficult to

express by a single allocation base. It is important to emphasise that there

is no allocation base which can accurately provide indirect cost allocation

to products. Chosen cost allocation base can be more or less objective,

but it can’t be 100% accurate. Indirect manufacturing costs are usually

assigned to products or services using the following cost allocation bases:3

1. direct labour hours,

2. machine hours,

3. direct material costs,

4. total direct costs,

5. quantity of production.

Indirect manufacturing costs are assigned to cost object by an

overhead allocation rate which is computing on the chosen cost allocation base.4

total indirect manufacturing costs

OAR = --------------------------------------------

cost allocation base

Companies can use either one or more overhead allocation rate for

assigning indirect manufacturing costs to products or services. It is considered

that the more overhead allocation rates are used the cost per unit is more

accurate and the product profitability evaluation is more reliable and more

objective for decision making.

3) Engler, C. (1988), Managerial Accounting, Irwin, Homewood, Illinois,

p. 427

4) Lucey, T. (1996), Costing, DP Publications, London, p. 88

be directly identified to particular product or service, indirect manufacturing

costs need to be allocated to products or services on some reasonable bases

which correctly present the relationship between indirect manufacturing

costs and certain product. This relationship is often very difficult to

express by a single allocation base. It is important to emphasise that there

is no allocation base which can accurately provide indirect cost allocation

to products. Chosen cost allocation base can be more or less objective,

but it can’t be 100% accurate. Indirect manufacturing costs are usually

assigned to products or services using the following cost allocation bases:3

1. direct labour hours,

2. machine hours,

3. direct material costs,

4. total direct costs,

5. quantity of production.

Indirect manufacturing costs are assigned to cost object by an

overhead allocation rate which is computing on the chosen cost allocation base.4

total indirect manufacturing costs

OAR = --------------------------------------------

cost allocation base

Companies can use either one or more overhead allocation rate for

assigning indirect manufacturing costs to products or services. It is considered

that the more overhead allocation rates are used the cost per unit is more

accurate and the product profitability evaluation is more reliable and more

objective for decision making.

3) Engler, C. (1988), Managerial Accounting, Irwin, Homewood, Illinois,

p. 427

4) Lucey, T. (1996), Costing, DP Publications, London, p. 88

160

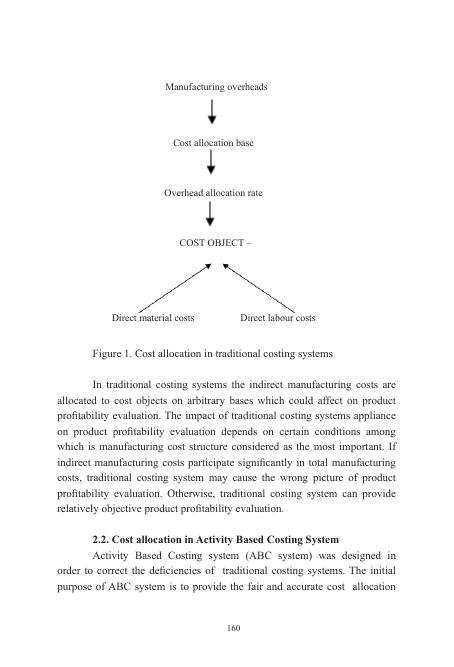

Figure 1. Cost allocation in traditional costing systems

In traditional costing systems the indirect manufacturing costs are

allocated to cost objects on arbitrary bases which could affect on product

profitability evaluation. The impact of traditional costing systems appliance

on product profitability evaluation depends on certain conditions among

which is manufacturing cost structure considered as the most important. If

indirect manufacturing costs participate significantly in total manufacturing

costs, traditional costing system may cause the wrong picture of product

profitability evaluation. Otherwise, traditional costing system can provide

relatively objective product profitability evaluation.

2.2. Cost allocation in Activity Based Costing System

Activity Based Costing system (ABC system) was designed in

order to correct the deficiencies of traditional costing systems. The initial

purpose of ABC system is to provide the fair and accurate cost allocation

Cost allocation base

Overhead allocation rate

COST OBJECT –

Direct material costs Direct labour costs

Manufacturing overheads

Figure 1. Cost allocation in traditional costing systems

In traditional costing systems the indirect manufacturing costs are

allocated to cost objects on arbitrary bases which could affect on product

profitability evaluation. The impact of traditional costing systems appliance

on product profitability evaluation depends on certain conditions among

which is manufacturing cost structure considered as the most important. If

indirect manufacturing costs participate significantly in total manufacturing

costs, traditional costing system may cause the wrong picture of product

profitability evaluation. Otherwise, traditional costing system can provide

relatively objective product profitability evaluation.

2.2. Cost allocation in Activity Based Costing System

Activity Based Costing system (ABC system) was designed in

order to correct the deficiencies of traditional costing systems. The initial

purpose of ABC system is to provide the fair and accurate cost allocation

Cost allocation base

Overhead allocation rate

COST OBJECT –

Direct material costs Direct labour costs

Manufacturing overheads

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting and finance Assignment PDFlg...

|7

|1804

|172

Management Accounting - Assignment PDFlg...

|9

|1846

|161

Management Accounting - Assignment PDFlg...

|7

|1472

|157

Product Costing and Pricing Doclg...

|8

|2193

|96

Management Accounting for Costs and Control - Assignmentlg...

|14

|2536

|43

SUSTAINABLE DESIGN PROCESS 2022lg...

|9

|1273

|31