Concept of Terotechnology, Capital Investment Analysis, Gaps in life cycle costing

VerifiedAdded on 2022/12/20

|11

|2626

|1

AI Summary

This document discusses the concept of Terotechnology, capital investment analysis, and gaps in life cycle costing. It provides recommendations for optimizing CAPEX and OPEX, maximizing facility performance, and minimizing time-to-first-production. The document also explains the idea of annual worth, present value, and internal rate of return. It concludes with a discussion on the conventional benefit-cost ratio and the modified cost-benefit ratio.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MREGC5001Assignment22019

Name of the Student

Name of the University

Author Note

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Answer to question 1....................................................................................................5

Concept of Terotechnology.......................................................................................5

Capital Investment Analysis......................................................................................5

Gaps in life cycle costing..........................................................................................6

Recommendations....................................................................................................7

Answer to question 2....................................................................................................7

Answer to question 3....................................................................................................9

Answer to question 4..................................................................................................11

Answer to question 5..................................................................................................12

Reference...................................................................................................................14

Answer to question 1....................................................................................................5

Concept of Terotechnology.......................................................................................5

Capital Investment Analysis......................................................................................5

Gaps in life cycle costing..........................................................................................6

Recommendations....................................................................................................7

Answer to question 2....................................................................................................7

Answer to question 3....................................................................................................9

Answer to question 4..................................................................................................11

Answer to question 5..................................................................................................12

Reference...................................................................................................................14

Answer to question 1

Concept of Terotechnology

This particular research work was intended about exhibiting some philosophical

thoughts for the future improvement of terotechnology as order inside the general

field of industrial management. Likewise, some general ideas are proposed in

regards to the conceivable future advancement of life-cycle costing as a strategy

inside the broad area of monetary assessment and examination for built frameworks.

A few proposals for further research work are likewise made.

Of the many conclusions drawn by the Maddock Report, the most noteworthy in the

advancement of terotechnology was aimed about three important plant qualities and

the board capacities that is, consistent quality, viability and the criticism of data to

planners. The idea of terotechnology can be characterized as the innovation of

establishment, authorizing, substitution and expulsion of plant, hardware, and gear,

of input to structure and activity thereof, and related subjects and practices.

Farinha (2018) has expressed that Terotechnology is a between the disciplinary

matter" and Atkinson depicted terotechnology as a between disciplinary issue,

including transaction among electrical and electronic building, mechanical designing,

structural designing and so on. The underlying perplexity communicated in the

Department of Industry booklets appears to have prompted some disarray in writing.

Nonetheless, this survey has demonstrated that most of the creators take the view

that terotechnology is a multi-disciplinary innovation. In this manner, this is the view

which will be communicated all through this exploration work.

Capital Investment Analysis

Capital speculation choices that include the buy of things, for example, land,

apparatus, structures, or hardware are among the most significant decisions

attempted by the business administrator. These choices regularly include the

responsibility of substantial aggregates of cash, and they will influence the business

over various years. Besides, the assets to buy a capital thing must be paid out

promptly, while the payor advantages accumulate after some time. Since the

benefits depend on future occasions and the capacity to anticipate what's to come is

defective, you should endeavor to assess venture choices as altogether as could

reasonably be expected. The most significant assignment of speculation examination

Concept of Terotechnology

This particular research work was intended about exhibiting some philosophical

thoughts for the future improvement of terotechnology as order inside the general

field of industrial management. Likewise, some general ideas are proposed in

regards to the conceivable future advancement of life-cycle costing as a strategy

inside the broad area of monetary assessment and examination for built frameworks.

A few proposals for further research work are likewise made.

Of the many conclusions drawn by the Maddock Report, the most noteworthy in the

advancement of terotechnology was aimed about three important plant qualities and

the board capacities that is, consistent quality, viability and the criticism of data to

planners. The idea of terotechnology can be characterized as the innovation of

establishment, authorizing, substitution and expulsion of plant, hardware, and gear,

of input to structure and activity thereof, and related subjects and practices.

Farinha (2018) has expressed that Terotechnology is a between the disciplinary

matter" and Atkinson depicted terotechnology as a between disciplinary issue,

including transaction among electrical and electronic building, mechanical designing,

structural designing and so on. The underlying perplexity communicated in the

Department of Industry booklets appears to have prompted some disarray in writing.

Nonetheless, this survey has demonstrated that most of the creators take the view

that terotechnology is a multi-disciplinary innovation. In this manner, this is the view

which will be communicated all through this exploration work.

Capital Investment Analysis

Capital speculation choices that include the buy of things, for example, land,

apparatus, structures, or hardware are among the most significant decisions

attempted by the business administrator. These choices regularly include the

responsibility of substantial aggregates of cash, and they will influence the business

over various years. Besides, the assets to buy a capital thing must be paid out

promptly, while the payor advantages accumulate after some time. Since the

benefits depend on future occasions and the capacity to anticipate what's to come is

defective, you should endeavor to assess venture choices as altogether as could

reasonably be expected. The most significant assignment of speculation examination

is gathering the fitting information. The methodology examined in this production

show you how to assess the choice, yet on the off chance that you have wrong or

fragmented data, at that point a generally intensive and complete investigation will

delude. Choosing ventures that will improve the money related execution of the

business includes two important undertakings: 1) monetary productivity examination

and 2) budgetary plausibility investigation. The financial benefit will appear if an

option is financially beneficial. In any case, speculation may not be monetarily

achievable: that is, the money streams might be inadequate to make the required

main and premium installments.

Gaps in life cycle costing

Foundation ventures are the impetus that drives financial development. Concrete

foundation, for example, streets, ports, rail, interstates, airplane terminals, power and

water supply are required for the transportation of merchandise, individuals

portability, guaranteeing the creation of makers thus many other days by day

exercises.

Foundation, much the same as different sorts of capital consumption, will end up out

of date following quite a while of persistent utilization and introduction to mixed-use

and natural components (CONTUK, 2018). To proceed with the activities, these

maturing framework will require intermittent support, modernization, and substitution

in whole or parts. By and large, the yearly use on upkeep and modernization would

regularly running from 2% to 20% or all the more relying upon different elements by

the size, nature, limit yet in addition including their for reason, plan, materials, quality

of development and above all, the manner in which it works and keeps up. These

OPEX things are consumptions over a time of 20 to 30 years or more! It is

profoundly conceivable that the capital spending on a foundation for an incredible

duration cycles to be significantly more than the underlying capital consumption to

assemble it. Furthermore, we don't see enough of this investigation being done when

we are building our advantage, city venture.

There is a basic need to investigate this and improve the use to be spent on the

framework for an incredible duration cycle. Life-Cycle Cost Analysis (LCCA) is

especially useful in this circumstance to guarantee the cost-viability of a foundation

venture. LCCA is a device to decide the most practical choice among various

contending choices to buy, possess, work, keep up and, at long last, discard an

show you how to assess the choice, yet on the off chance that you have wrong or

fragmented data, at that point a generally intensive and complete investigation will

delude. Choosing ventures that will improve the money related execution of the

business includes two important undertakings: 1) monetary productivity examination

and 2) budgetary plausibility investigation. The financial benefit will appear if an

option is financially beneficial. In any case, speculation may not be monetarily

achievable: that is, the money streams might be inadequate to make the required

main and premium installments.

Gaps in life cycle costing

Foundation ventures are the impetus that drives financial development. Concrete

foundation, for example, streets, ports, rail, interstates, airplane terminals, power and

water supply are required for the transportation of merchandise, individuals

portability, guaranteeing the creation of makers thus many other days by day

exercises.

Foundation, much the same as different sorts of capital consumption, will end up out

of date following quite a while of persistent utilization and introduction to mixed-use

and natural components (CONTUK, 2018). To proceed with the activities, these

maturing framework will require intermittent support, modernization, and substitution

in whole or parts. By and large, the yearly use on upkeep and modernization would

regularly running from 2% to 20% or all the more relying upon different elements by

the size, nature, limit yet in addition including their for reason, plan, materials, quality

of development and above all, the manner in which it works and keeps up. These

OPEX things are consumptions over a time of 20 to 30 years or more! It is

profoundly conceivable that the capital spending on a foundation for an incredible

duration cycles to be significantly more than the underlying capital consumption to

assemble it. Furthermore, we don't see enough of this investigation being done when

we are building our advantage, city venture.

There is a basic need to investigate this and improve the use to be spent on the

framework for an incredible duration cycle. Life-Cycle Cost Analysis (LCCA) is

especially useful in this circumstance to guarantee the cost-viability of a foundation

venture. LCCA is a device to decide the most practical choice among various

contending choices to buy, possess, work, keep up and, at long last, discard an

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

article or procedure when each is similarly fitting to be actualized on specialized

grounds. The LCCA thinks about every one of the expenses acquired in the life-cycle

of the foundation, and this alludes to the savviest choice to manufacture, work, keep

up and decommission the framework (Djurović et al. 2015).

To provide further clearness, for a thruway asphalt, notwithstanding the underlying

development cost, LCCA considers all the client costs, (e.g., decreased limit at work

zones), and organization costs identified with future exercises, including future

occasional upkeep and recovery. Every one of the expenses is typically limited and

aggregate to present-day esteem known as net present esteem (NPV). A life-cycle

model is generally joined with the complete loss of possession to give a

progressively comprehensive and far-reaching costing model to the engineer or all

the more the proprietor of the framework resource (Wijnia, 2016).

To give sureness in Asset Performance, it's critical to supplant the advantages at the

ideal time following great practice, association strategy, and producer's proposals.

Along these lines, a compelling capital arranging to precede the real expense

brought about can improve the productivity in the use of time and assets. Cost

reserve funds can likewise be because of the institutionalizing of way to deal with

acquiring, smoothening out of expenses, and out of date quality through the

acquirement of advantages through inventory network accomplices. The point is

added to improve the partner's certainty as a diminished vulnerability in cost

arranging can prompt better resource execution and lessening the interruption and

dangers to the business.

Recommendations

Optimize the harmony between CAPEX and OPEX dependent on accurate

information as opposed to subjectivity

Maximize the exhibition of the office and limit the danger of disappointment

through guaranteeing that the plan consolidates ideal operability, unwavering

quality, and viability attributes

Minimize time-to-first-creation through successful charging approaches

Ensure vitality productive or 'green' working at excellent Life Cycle Cost with

no wellbeing or creation related trade-offs

grounds. The LCCA thinks about every one of the expenses acquired in the life-cycle

of the foundation, and this alludes to the savviest choice to manufacture, work, keep

up and decommission the framework (Djurović et al. 2015).

To provide further clearness, for a thruway asphalt, notwithstanding the underlying

development cost, LCCA considers all the client costs, (e.g., decreased limit at work

zones), and organization costs identified with future exercises, including future

occasional upkeep and recovery. Every one of the expenses is typically limited and

aggregate to present-day esteem known as net present esteem (NPV). A life-cycle

model is generally joined with the complete loss of possession to give a

progressively comprehensive and far-reaching costing model to the engineer or all

the more the proprietor of the framework resource (Wijnia, 2016).

To give sureness in Asset Performance, it's critical to supplant the advantages at the

ideal time following great practice, association strategy, and producer's proposals.

Along these lines, a compelling capital arranging to precede the real expense

brought about can improve the productivity in the use of time and assets. Cost

reserve funds can likewise be because of the institutionalizing of way to deal with

acquiring, smoothening out of expenses, and out of date quality through the

acquirement of advantages through inventory network accomplices. The point is

added to improve the partner's certainty as a diminished vulnerability in cost

arranging can prompt better resource execution and lessening the interruption and

dangers to the business.

Recommendations

Optimize the harmony between CAPEX and OPEX dependent on accurate

information as opposed to subjectivity

Maximize the exhibition of the office and limit the danger of disappointment

through guaranteeing that the plan consolidates ideal operability, unwavering

quality, and viability attributes

Minimize time-to-first-creation through successful charging approaches

Ensure vitality productive or 'green' working at excellent Life Cycle Cost with

no wellbeing or creation related trade-offs

Answer to question 2

Idea of Annual worth:

Annual worth (AW) is an investigation system dependent on the idea of

equivalencies. Annual worth is standardizes resources, which permits examination of

advantages with definitely various attributes, (for example, life expectancy,

introductory expense, and adjusting cost). AW changes over rising and falling

expenses of a speculation over a given timeframe into a steady expense for each

year esteem.

Present worth:

Present worth (PW) investigation is a comparability strategy for examination of

speculation choices in which an undertaking's money streams are displayed as a

solitary present esteem. PW is a standout amongst the most fundamental and

proficient strategies accessible for deciding the adequacy of a venture on a financial

premise.

Internal rate of return:

The IRR can be characterized as the rebate rate which, when connected to the

money streams of a venture, delivers a net present esteem (NPV) of nil. This

markdown rate would then be able to be thought of as the figure return for the

undertaking. On the off chance that the IRR is more prominent than a pre-set rate

focus on, the undertaking is acknowledged. On the off chance that the IRR is not

exactly the objective, the venture is rejected.

Idea of Annual worth:

Annual worth (AW) is an investigation system dependent on the idea of

equivalencies. Annual worth is standardizes resources, which permits examination of

advantages with definitely various attributes, (for example, life expectancy,

introductory expense, and adjusting cost). AW changes over rising and falling

expenses of a speculation over a given timeframe into a steady expense for each

year esteem.

Present worth:

Present worth (PW) investigation is a comparability strategy for examination of

speculation choices in which an undertaking's money streams are displayed as a

solitary present esteem. PW is a standout amongst the most fundamental and

proficient strategies accessible for deciding the adequacy of a venture on a financial

premise.

Internal rate of return:

The IRR can be characterized as the rebate rate which, when connected to the

money streams of a venture, delivers a net present esteem (NPV) of nil. This

markdown rate would then be able to be thought of as the figure return for the

undertaking. On the off chance that the IRR is more prominent than a pre-set rate

focus on, the undertaking is acknowledged. On the off chance that the IRR is not

exactly the objective, the venture is rejected.

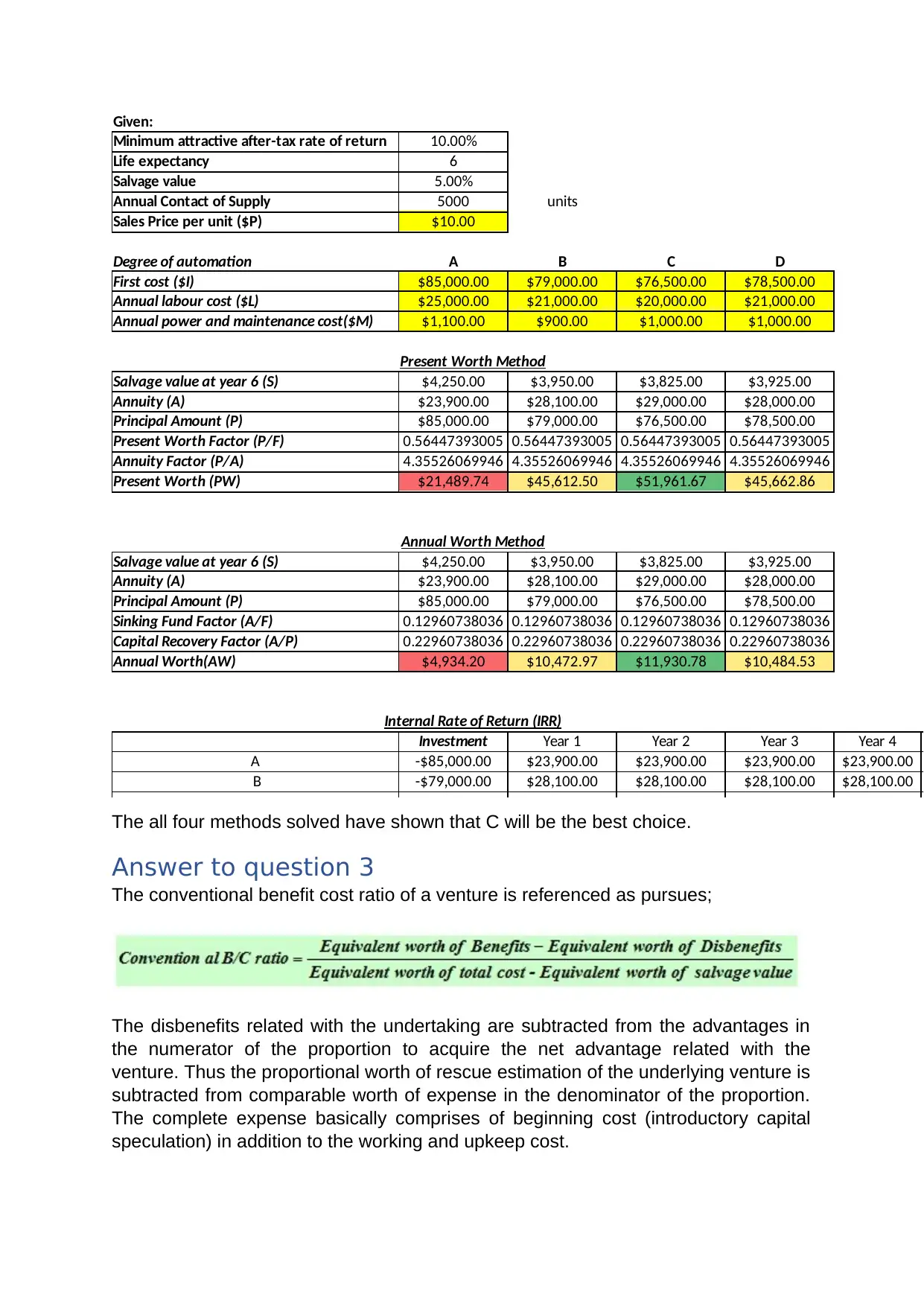

Given:

Minimum attractive after-tax rate of return 10.00%

Life expectancy 6

Salvage value 5.00%

Annual Contact of Supply 5000 units

Sales Price per unit ($P) $10.00

Degree of automation A B C D

First cost ($I) $85,000.00 $79,000.00 $76,500.00 $78,500.00

Annual labour cost ($L) $25,000.00 $21,000.00 $20,000.00 $21,000.00

Annual power and maintenance cost($M) $1,100.00 $900.00 $1,000.00 $1,000.00

Present Worth Method

Salvage value at year 6 (S) $4,250.00 $3,950.00 $3,825.00 $3,925.00

Annuity (A) $23,900.00 $28,100.00 $29,000.00 $28,000.00

Principal Amount (P) $85,000.00 $79,000.00 $76,500.00 $78,500.00

Present Worth Factor (P/F) 0.56447393005 0.56447393005 0.56447393005 0.56447393005

Annuity Factor (P/A) 4.35526069946 4.35526069946 4.35526069946 4.35526069946

Present Worth (PW) $21,489.74 $45,612.50 $51,961.67 $45,662.86

Annual Worth Method

Salvage value at year 6 (S) $4,250.00 $3,950.00 $3,825.00 $3,925.00

Annuity (A) $23,900.00 $28,100.00 $29,000.00 $28,000.00

Principal Amount (P) $85,000.00 $79,000.00 $76,500.00 $78,500.00

Sinking Fund Factor (A/F) 0.12960738036 0.12960738036 0.12960738036 0.12960738036

Capital Recovery Factor (A/P) 0.22960738036 0.22960738036 0.22960738036 0.22960738036

Annual Worth(AW) $4,934.20 $10,472.97 $11,930.78 $10,484.53

Internal Rate of Return (IRR)

Investment Year 1 Year 2 Year 3 Year 4

A -$85,000.00 $23,900.00 $23,900.00 $23,900.00 $23,900.00

B -$79,000.00 $28,100.00 $28,100.00 $28,100.00 $28,100.00

The all four methods solved have shown that C will be the best choice.

Answer to question 3

The conventional benefit cost ratio of a venture is referenced as pursues;

The disbenefits related with the undertaking are subtracted from the advantages in

the numerator of the proportion to acquire the net advantage related with the

venture. Thus the proportional worth of rescue estimation of the underlying venture is

subtracted from comparable worth of expense in the denominator of the proportion.

The complete expense basically comprises of beginning cost (introductory capital

speculation) in addition to the working and upkeep cost.

Minimum attractive after-tax rate of return 10.00%

Life expectancy 6

Salvage value 5.00%

Annual Contact of Supply 5000 units

Sales Price per unit ($P) $10.00

Degree of automation A B C D

First cost ($I) $85,000.00 $79,000.00 $76,500.00 $78,500.00

Annual labour cost ($L) $25,000.00 $21,000.00 $20,000.00 $21,000.00

Annual power and maintenance cost($M) $1,100.00 $900.00 $1,000.00 $1,000.00

Present Worth Method

Salvage value at year 6 (S) $4,250.00 $3,950.00 $3,825.00 $3,925.00

Annuity (A) $23,900.00 $28,100.00 $29,000.00 $28,000.00

Principal Amount (P) $85,000.00 $79,000.00 $76,500.00 $78,500.00

Present Worth Factor (P/F) 0.56447393005 0.56447393005 0.56447393005 0.56447393005

Annuity Factor (P/A) 4.35526069946 4.35526069946 4.35526069946 4.35526069946

Present Worth (PW) $21,489.74 $45,612.50 $51,961.67 $45,662.86

Annual Worth Method

Salvage value at year 6 (S) $4,250.00 $3,950.00 $3,825.00 $3,925.00

Annuity (A) $23,900.00 $28,100.00 $29,000.00 $28,000.00

Principal Amount (P) $85,000.00 $79,000.00 $76,500.00 $78,500.00

Sinking Fund Factor (A/F) 0.12960738036 0.12960738036 0.12960738036 0.12960738036

Capital Recovery Factor (A/P) 0.22960738036 0.22960738036 0.22960738036 0.22960738036

Annual Worth(AW) $4,934.20 $10,472.97 $11,930.78 $10,484.53

Internal Rate of Return (IRR)

Investment Year 1 Year 2 Year 3 Year 4

A -$85,000.00 $23,900.00 $23,900.00 $23,900.00 $23,900.00

B -$79,000.00 $28,100.00 $28,100.00 $28,100.00 $28,100.00

The all four methods solved have shown that C will be the best choice.

Answer to question 3

The conventional benefit cost ratio of a venture is referenced as pursues;

The disbenefits related with the undertaking are subtracted from the advantages in

the numerator of the proportion to acquire the net advantage related with the

venture. Thus the proportional worth of rescue estimation of the underlying venture is

subtracted from comparable worth of expense in the denominator of the proportion.

The complete expense basically comprises of beginning cost (introductory capital

speculation) in addition to the working and upkeep cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

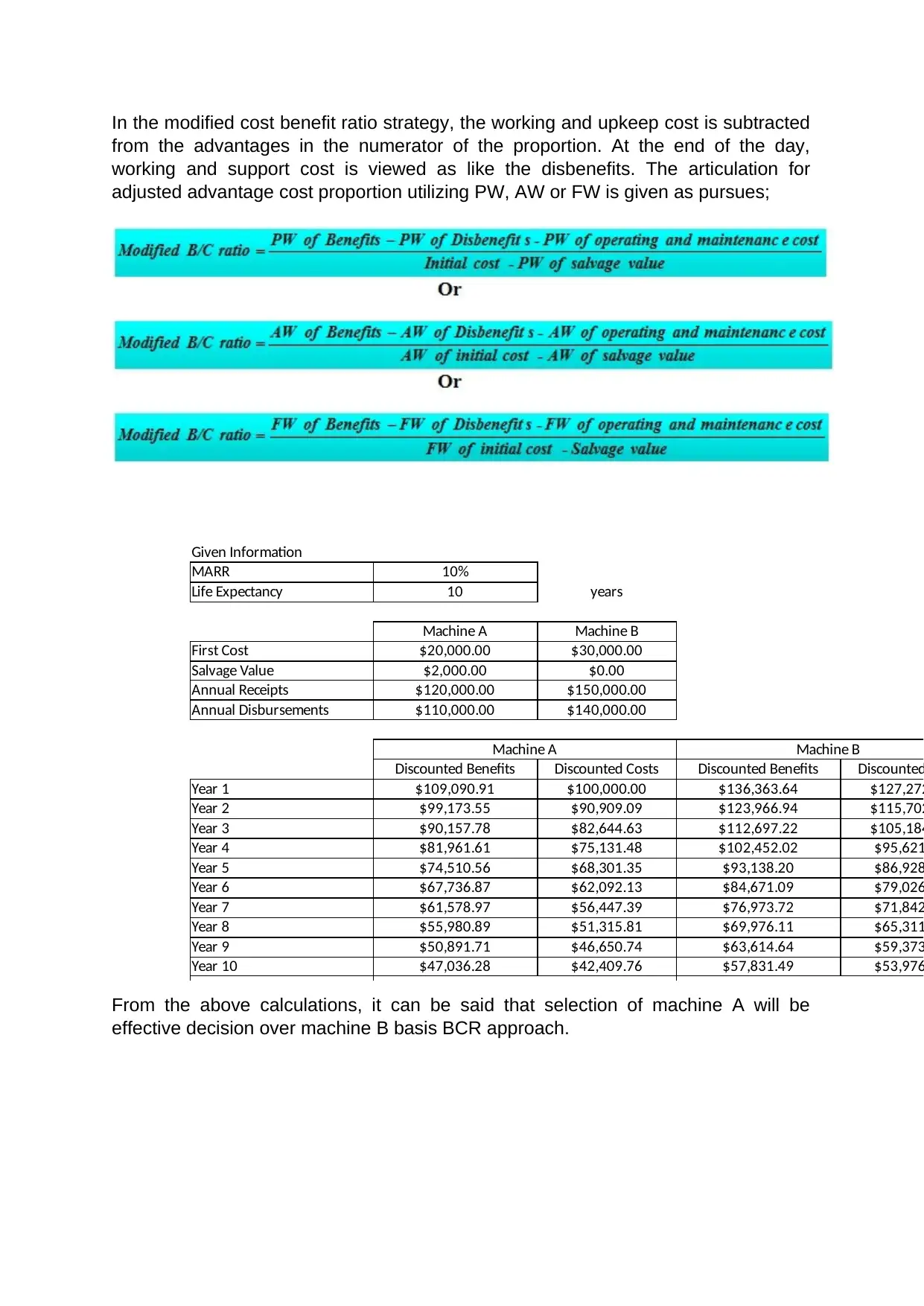

In the modified cost benefit ratio strategy, the working and upkeep cost is subtracted

from the advantages in the numerator of the proportion. At the end of the day,

working and support cost is viewed as like the disbenefits. The articulation for

adjusted advantage cost proportion utilizing PW, AW or FW is given as pursues;

Given Information

MARR 10%

Life Expectancy 10 years

Machine A Machine B

First Cost $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual Receipts $120,000.00 $150,000.00

Annual Disbursements $110,000.00 $140,000.00

Machine A Machine B

Discounted Benefits Discounted Costs Discounted Benefits Discounted

Year 1 $109,090.91 $100,000.00 $136,363.64 $127,272

Year 2 $99,173.55 $90,909.09 $123,966.94 $115,702

Year 3 $90,157.78 $82,644.63 $112,697.22 $105,184

Year 4 $81,961.61 $75,131.48 $102,452.02 $95,621

Year 5 $74,510.56 $68,301.35 $93,138.20 $86,928

Year 6 $67,736.87 $62,092.13 $84,671.09 $79,026

Year 7 $61,578.97 $56,447.39 $76,973.72 $71,842

Year 8 $55,980.89 $51,315.81 $69,976.11 $65,311

Year 9 $50,891.71 $46,650.74 $63,614.64 $59,373

Year 10 $47,036.28 $42,409.76 $57,831.49 $53,976

From the above calculations, it can be said that selection of machine A will be

effective decision over machine B basis BCR approach.

from the advantages in the numerator of the proportion. At the end of the day,

working and support cost is viewed as like the disbenefits. The articulation for

adjusted advantage cost proportion utilizing PW, AW or FW is given as pursues;

Given Information

MARR 10%

Life Expectancy 10 years

Machine A Machine B

First Cost $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual Receipts $120,000.00 $150,000.00

Annual Disbursements $110,000.00 $140,000.00

Machine A Machine B

Discounted Benefits Discounted Costs Discounted Benefits Discounted

Year 1 $109,090.91 $100,000.00 $136,363.64 $127,272

Year 2 $99,173.55 $90,909.09 $123,966.94 $115,702

Year 3 $90,157.78 $82,644.63 $112,697.22 $105,184

Year 4 $81,961.61 $75,131.48 $102,452.02 $95,621

Year 5 $74,510.56 $68,301.35 $93,138.20 $86,928

Year 6 $67,736.87 $62,092.13 $84,671.09 $79,026

Year 7 $61,578.97 $56,447.39 $76,973.72 $71,842

Year 8 $55,980.89 $51,315.81 $69,976.11 $65,311

Year 9 $50,891.71 $46,650.74 $63,614.64 $59,373

Year 10 $47,036.28 $42,409.76 $57,831.49 $53,976

From the above calculations, it can be said that selection of machine A will be

effective decision over machine B basis BCR approach.

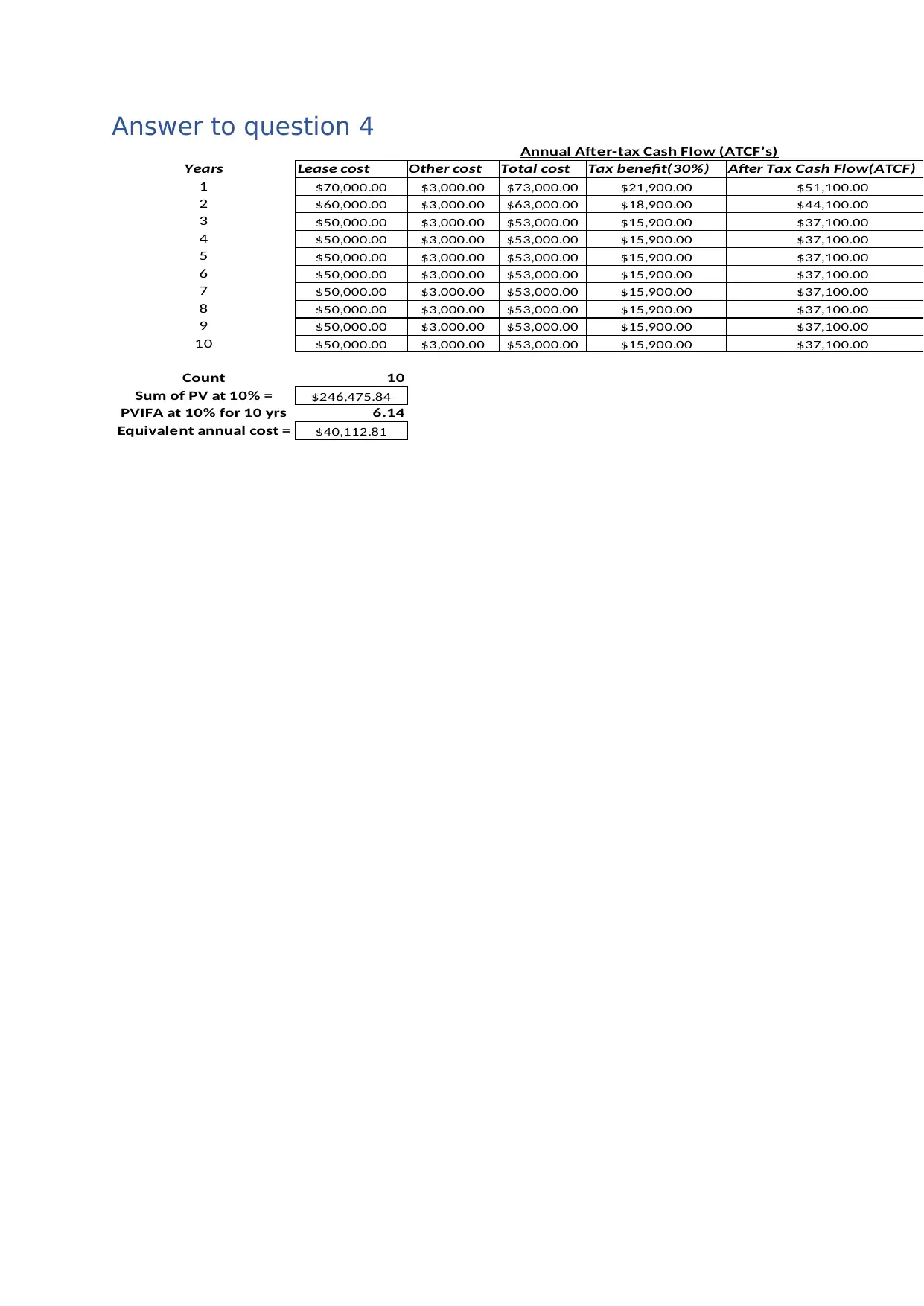

Answer to question 4 Annual After-tax Cash Flow (ATCF’s)

Years Lease cost Other cost Total cost Tax benefit(30%) After Tax Cash Flow(ATCF)

1 $70,000.00 $3,000.00 $73,000.00 $21,900.00 $51,100.00

2 $60,000.00 $3,000.00 $63,000.00 $18,900.00 $44,100.00

3 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

4 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

5 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

6 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

7 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

8 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

9 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

10 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

Count 10

Sum of PV at 10% = $246,475.84

PVIFA at 10% for 10 yrs 6.14

Equivalent annual cost = $40,112.81

Years Lease cost Other cost Total cost Tax benefit(30%) After Tax Cash Flow(ATCF)

1 $70,000.00 $3,000.00 $73,000.00 $21,900.00 $51,100.00

2 $60,000.00 $3,000.00 $63,000.00 $18,900.00 $44,100.00

3 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

4 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

5 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

6 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

7 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

8 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

9 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

10 $50,000.00 $3,000.00 $53,000.00 $15,900.00 $37,100.00

Count 10

Sum of PV at 10% = $246,475.84

PVIFA at 10% for 10 yrs 6.14

Equivalent annual cost = $40,112.81

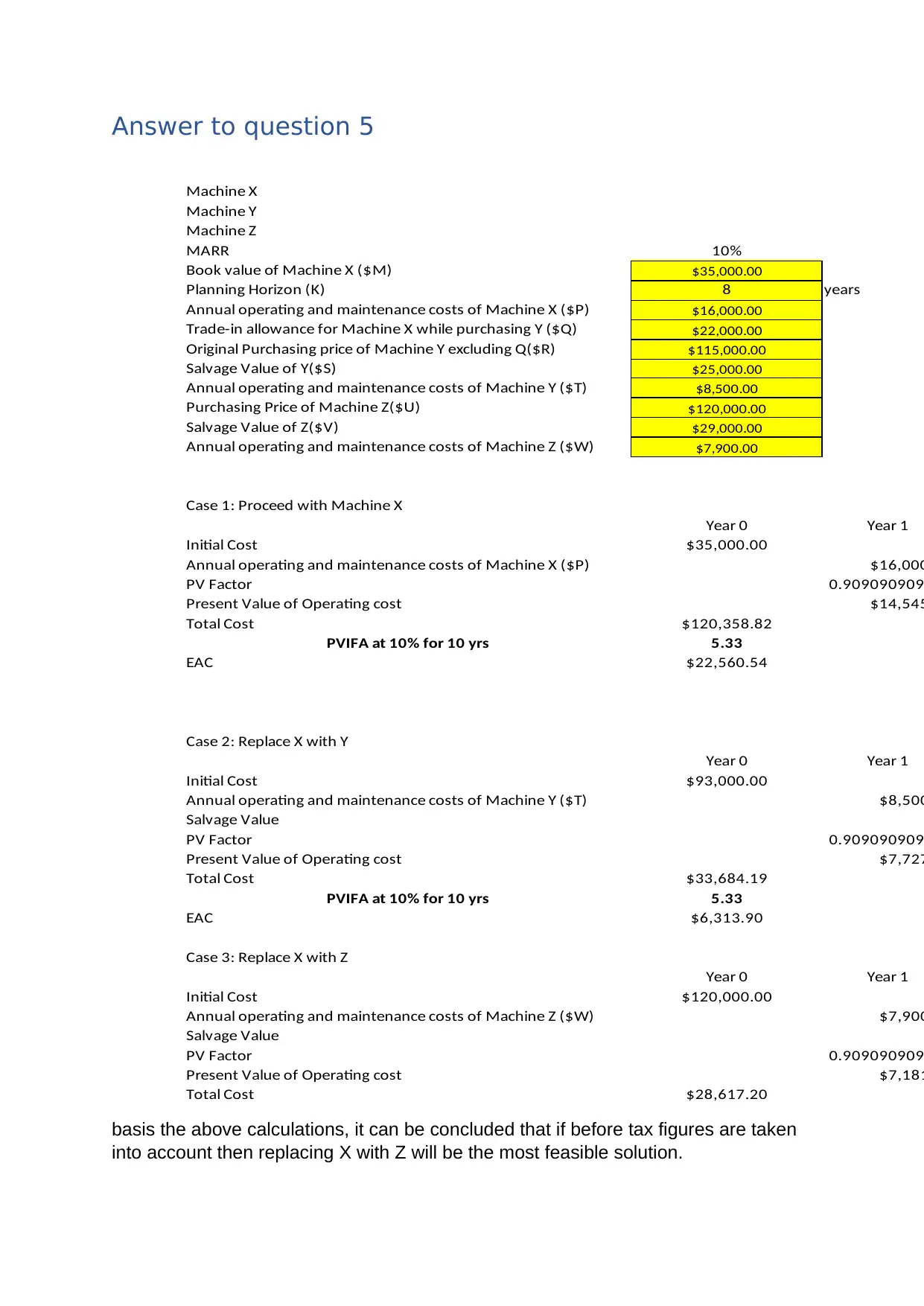

Answer to question 5

Machine X

Machine Y

Machine Z

MARR 10%

Book value of Machine X ($M) $35,000.00

Planning Horizon (K) 8 years

Annual operating and maintenance costs of Machine X ($P) $16,000.00

Trade-in allowance for Machine X while purchasing Y ($Q) $22,000.00

Original Purchasing price of Machine Y excluding Q($R) $115,000.00

Salvage Value of Y($S) $25,000.00

Annual operating and maintenance costs of Machine Y ($T) $8,500.00

Purchasing Price of Machine Z($U) $120,000.00

Salvage Value of Z($V) $29,000.00

Annual operating and maintenance costs of Machine Z ($W) $7,900.00

Case 1: Proceed with Machine X

Year 0 Year 1

Initial Cost $35,000.00

Annual operating and maintenance costs of Machine X ($P) $16,000

PV Factor 0.909090909

Present Value of Operating cost $14,545

Total Cost $120,358.82

PVIFA at 10% for 10 yrs 5.33

EAC $22,560.54

Case 2: Replace X with Y

Year 0 Year 1

Initial Cost $93,000.00

Annual operating and maintenance costs of Machine Y ($T) $8,500

Salvage Value

PV Factor 0.909090909

Present Value of Operating cost $7,727

Total Cost $33,684.19

PVIFA at 10% for 10 yrs 5.33

EAC $6,313.90

Case 3: Replace X with Z

Year 0 Year 1

Initial Cost $120,000.00

Annual operating and maintenance costs of Machine Z ($W) $7,900

Salvage Value

PV Factor 0.909090909

Present Value of Operating cost $7,181

Total Cost $28,617.20

basis the above calculations, it can be concluded that if before tax figures are taken

into account then replacing X with Z will be the most feasible solution.

Machine X

Machine Y

Machine Z

MARR 10%

Book value of Machine X ($M) $35,000.00

Planning Horizon (K) 8 years

Annual operating and maintenance costs of Machine X ($P) $16,000.00

Trade-in allowance for Machine X while purchasing Y ($Q) $22,000.00

Original Purchasing price of Machine Y excluding Q($R) $115,000.00

Salvage Value of Y($S) $25,000.00

Annual operating and maintenance costs of Machine Y ($T) $8,500.00

Purchasing Price of Machine Z($U) $120,000.00

Salvage Value of Z($V) $29,000.00

Annual operating and maintenance costs of Machine Z ($W) $7,900.00

Case 1: Proceed with Machine X

Year 0 Year 1

Initial Cost $35,000.00

Annual operating and maintenance costs of Machine X ($P) $16,000

PV Factor 0.909090909

Present Value of Operating cost $14,545

Total Cost $120,358.82

PVIFA at 10% for 10 yrs 5.33

EAC $22,560.54

Case 2: Replace X with Y

Year 0 Year 1

Initial Cost $93,000.00

Annual operating and maintenance costs of Machine Y ($T) $8,500

Salvage Value

PV Factor 0.909090909

Present Value of Operating cost $7,727

Total Cost $33,684.19

PVIFA at 10% for 10 yrs 5.33

EAC $6,313.90

Case 3: Replace X with Z

Year 0 Year 1

Initial Cost $120,000.00

Annual operating and maintenance costs of Machine Z ($W) $7,900

Salvage Value

PV Factor 0.909090909

Present Value of Operating cost $7,181

Total Cost $28,617.20

basis the above calculations, it can be concluded that if before tax figures are taken

into account then replacing X with Z will be the most feasible solution.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Reference

CONTUK, F.Y., 2018. Product Life Cycle Costing Method: A General Evaluation.

Social Sciences Researches in the Globalizing World, p.744.

Djurović, D., Bulatović, M., Soković, M. and Stoić, A., 2015. Measurement of

maintenance excellence. Tehnički vjesnik, 22(5), pp.1263-1268.

Farinha, J.M.T., 2018. Asset Maintenance Engineering Methodologies. CRC Press.

Wijnia, Y., 2016. Towards Quantification of Asset Management Optimality. In

Proceedings of the 10th World Congress on Engineering Asset Management

(WCEAM 2015) (pp. 663-670). Springer, Cham.

CONTUK, F.Y., 2018. Product Life Cycle Costing Method: A General Evaluation.

Social Sciences Researches in the Globalizing World, p.744.

Djurović, D., Bulatović, M., Soković, M. and Stoić, A., 2015. Measurement of

maintenance excellence. Tehnički vjesnik, 22(5), pp.1263-1268.

Farinha, J.M.T., 2018. Asset Maintenance Engineering Methodologies. CRC Press.

Wijnia, Y., 2016. Towards Quantification of Asset Management Optimality. In

Proceedings of the 10th World Congress on Engineering Asset Management

(WCEAM 2015) (pp. 663-670). Springer, Cham.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.