MSc Professional Accounting - Essay

26 Pages7708 Words18 Views

Added on 2021-05-31

MSc Professional Accounting - Essay

Added on 2021-05-31

ShareRelated Documents

Running head: MSC PROFESSIONAL ACCOUNTING

MSc Professional Accounting

Name of the Student

Name of the University

Author’s Note

MSc Professional Accounting

Name of the Student

Name of the University

Author’s Note

1

MSC PROFESSIONAL ACCOUNTING

Table of Contents

Section 1..............................................................................................................................2

Introduction..........................................................................................................................2

Mergers and Acquisition Overview.....................................................................................3

Factors affecting merger and acquisition advisory choice..................................................6

Critical Success Factors for the target company..................................................................8

Project Success Criteria.......................................................................................................9

Critical success factors......................................................................................................12

Critical success factors for projects...................................................................................12

Spotting Winning Mergers’ Critical Characteristics.........................................................13

Conclusion.........................................................................................................................14

References for Section 1....................................................................................................16

Section 2............................................................................................................................19

Reflective Essay.................................................................................................................19

References for Section 2....................................................................................................23

MSC PROFESSIONAL ACCOUNTING

Table of Contents

Section 1..............................................................................................................................2

Introduction..........................................................................................................................2

Mergers and Acquisition Overview.....................................................................................3

Factors affecting merger and acquisition advisory choice..................................................6

Critical Success Factors for the target company..................................................................8

Project Success Criteria.......................................................................................................9

Critical success factors......................................................................................................12

Critical success factors for projects...................................................................................12

Spotting Winning Mergers’ Critical Characteristics.........................................................13

Conclusion.........................................................................................................................14

References for Section 1....................................................................................................16

Section 2............................................................................................................................19

Reflective Essay.................................................................................................................19

References for Section 2....................................................................................................23

2

MSC PROFESSIONAL ACCOUNTING

Section 1

Introduction

As discussed by El-Khatib, Fogel and Jandik (2015), the corporate mergers and

acquisitions have received a lot of publicity in the academic as well as corporate world. In 2005,

Thompson Financial reports were seen to announce a worldwide deal volume of US $ 2.7 trillion

which is an increase of more than 38% from $ 2 trillion in 2004. In compared to this, the value of

the deal increased by 33.3% to USD 1.1 trillion an announced in 2005. Additionally, the Europe

deal volume also went up by 37% to US $ 1.2 trillion and additionally the Asian deal volume

also experienced a surge of 64% to USD to 280 million. Several corporations around the world

considered M&A strategies for realizing the cost synergies as for the increased competition,

product mix, pricing pressures and concentration of the asset.

In the recent times, as the number of M&A transactions keeps on increasing, the advisory

entities of M&A as those opposed to the global investment banking have been benefited from

this trend. The global investment banking and brokerage industry is depicted to generate total

revenue of USD 57.5 billion in 2005 in which USD 19 billion was as a result of M&A activities.

Additionally, it is also not common for the company’s especially small and medium companies

with insufficient expertise to manage thine house M&A activities. It is more common for the

large corporations for establishing the in-house financial and corporate deployment departments

for employing the advisory services and utilizing the valuable content network and efficient use

of client personal close to monitor the transactions (Products 2015).

The main purpose of the study inside discussing the fact that shareholders in “target

company gain more in the short-term and medium-term compared to the shareholders in the

MSC PROFESSIONAL ACCOUNTING

Section 1

Introduction

As discussed by El-Khatib, Fogel and Jandik (2015), the corporate mergers and

acquisitions have received a lot of publicity in the academic as well as corporate world. In 2005,

Thompson Financial reports were seen to announce a worldwide deal volume of US $ 2.7 trillion

which is an increase of more than 38% from $ 2 trillion in 2004. In compared to this, the value of

the deal increased by 33.3% to USD 1.1 trillion an announced in 2005. Additionally, the Europe

deal volume also went up by 37% to US $ 1.2 trillion and additionally the Asian deal volume

also experienced a surge of 64% to USD to 280 million. Several corporations around the world

considered M&A strategies for realizing the cost synergies as for the increased competition,

product mix, pricing pressures and concentration of the asset.

In the recent times, as the number of M&A transactions keeps on increasing, the advisory

entities of M&A as those opposed to the global investment banking have been benefited from

this trend. The global investment banking and brokerage industry is depicted to generate total

revenue of USD 57.5 billion in 2005 in which USD 19 billion was as a result of M&A activities.

Additionally, it is also not common for the company’s especially small and medium companies

with insufficient expertise to manage thine house M&A activities. It is more common for the

large corporations for establishing the in-house financial and corporate deployment departments

for employing the advisory services and utilizing the valuable content network and efficient use

of client personal close to monitor the transactions (Products 2015).

The main purpose of the study inside discussing the fact that shareholders in “target

company gain more in the short-term and medium-term compared to the shareholders in the

3

MSC PROFESSIONAL ACCOUNTINGacquiring company”. This discussion is further supported with various types of assessments

which are associated to the process of conducting is business combination activities.

Additionally, the project’s success criteria are also measured from the merger and acquisition of

advisory firms (Belleflamme, Lambert and Schwienbacher 2014).

Mergers and Acquisition Overview

The topic of merger and activity is gaining increasing importance in the last two decades

with response to more and more merger and activities being increasingly complex in terms of

transactions involved. In a broad sense, M&A activity implies the total number of different

transactions which ranges from a number of purchase and sales activity is concentrated between

the joint ventures, alliances and undertakings for ensuring independence of business. There are

several explanations to this theory which leads to confusion and misunderstanding due to the

strategic alliances. Merger is identified as a combination between two entities for creating a

separate entity. Acquisition is the act of purchasing assets or shares of another company for

achieving managerial influence which may not be or maybe in the mutual agreement (Kansal and

Chandani 2014). The model of M&A has been depicted below as follows

MSC PROFESSIONAL ACCOUNTINGacquiring company”. This discussion is further supported with various types of assessments

which are associated to the process of conducting is business combination activities.

Additionally, the project’s success criteria are also measured from the merger and acquisition of

advisory firms (Belleflamme, Lambert and Schwienbacher 2014).

Mergers and Acquisition Overview

The topic of merger and activity is gaining increasing importance in the last two decades

with response to more and more merger and activities being increasingly complex in terms of

transactions involved. In a broad sense, M&A activity implies the total number of different

transactions which ranges from a number of purchase and sales activity is concentrated between

the joint ventures, alliances and undertakings for ensuring independence of business. There are

several explanations to this theory which leads to confusion and misunderstanding due to the

strategic alliances. Merger is identified as a combination between two entities for creating a

separate entity. Acquisition is the act of purchasing assets or shares of another company for

achieving managerial influence which may not be or maybe in the mutual agreement (Kansal and

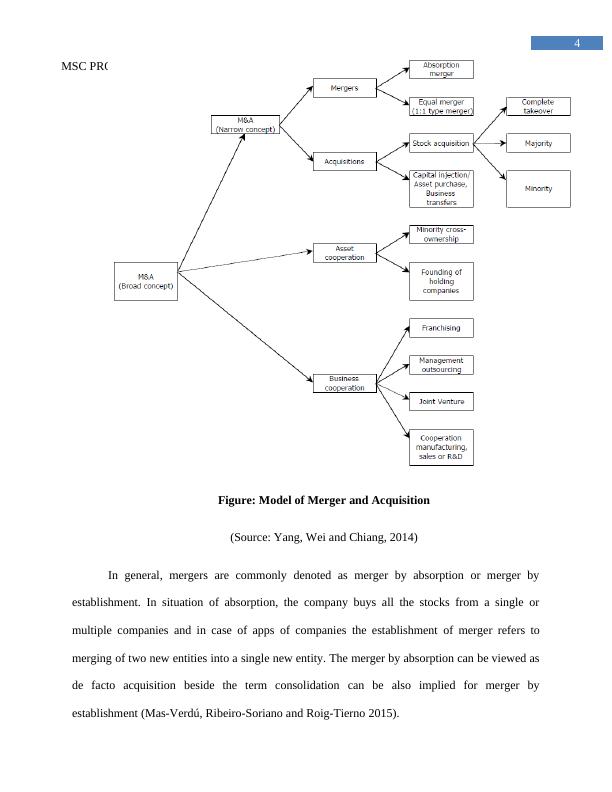

Chandani 2014). The model of M&A has been depicted below as follows

4

MSC PROFESSIONAL ACCOUNTING

Figure: Model of Merger and Acquisition

(Source: Yang, Wei and Chiang, 2014)

In general, mergers are commonly denoted as merger by absorption or merger by

establishment. In situation of absorption, the company buys all the stocks from a single or

multiple companies and in case of apps of companies the establishment of merger refers to

merging of two new entities into a single new entity. The merger by absorption can be viewed as

de facto acquisition beside the term consolidation can be also implied for merger by

establishment (Mas-Verdú, Ribeiro-Soriano and Roig-Tierno 2015).

MSC PROFESSIONAL ACCOUNTING

Figure: Model of Merger and Acquisition

(Source: Yang, Wei and Chiang, 2014)

In general, mergers are commonly denoted as merger by absorption or merger by

establishment. In situation of absorption, the company buys all the stocks from a single or

multiple companies and in case of apps of companies the establishment of merger refers to

merging of two new entities into a single new entity. The merger by absorption can be viewed as

de facto acquisition beside the term consolidation can be also implied for merger by

establishment (Mas-Verdú, Ribeiro-Soriano and Roig-Tierno 2015).

5

MSC PROFESSIONAL ACCOUNTINGDuring the acquisition of companies, the buying company may pursue a significant share

of the stocks of a target company. Similarly, there are important forms of acquisition, namely

share acquisition and asset acquisitions. In a share acquisition, the company is depicted to

purchase certain percentage of stocks of the target company for influencing the management.

Whereas, during asset acquisition the company buys all parts of the target company’s assets and

the target sustains as a legal entity. Based on the significance of shares of stocks, the company

acquisitions are further categorized into three types. This includes: “complete take over (100%

of target’s issued shares)”, “majority (50-99%)”, and “minority (less than 50%)” (Yilmaz and

Tanyeri 2016). In addition to this, the merger and acquisition are depicted as to separate from the

actions which have several consequences based on the legal obligations, tax liabilities and

procedure of acquisition. Despite of this, in general the final outcome of M&A transactions

considered in which two or more companies are seen to combine their business affords and we

do not make an effort to separate this merger transaction from acquisition ones. In such a

situation, M&A is treated as a corporate finance service which provides M&A advice to the

firms (Ferris, Houston and Javakhadze 2016).

In context of classification of mergers and acquisitions, the main perspective of value

chain for M&A is categorized as horizontal, vertical or conglomerate. In case of horizontal

M&A, the target companies and the acquiring companies are depicted as competing in the same

industry. In addition to this, in horizontal business combination process the restructuring in

business occurs as a result of technological changes and liberalization. This particular trade is

evident in industries related to petroleum, the mobile and pharmaceuticals (Yılmaz and Tanyeri

2016). A similar example of this can be seen with the merger of two US giants namely Glaxo

and SmithKline Beecham with a total value of USD 76 billion. Based on the statement of the

former CEO of SmithKline Beecham the main aim of combination of two companies was

depicted with research and development synergies to drive the revenues and explore enormous

MSC PROFESSIONAL ACCOUNTINGDuring the acquisition of companies, the buying company may pursue a significant share

of the stocks of a target company. Similarly, there are important forms of acquisition, namely

share acquisition and asset acquisitions. In a share acquisition, the company is depicted to

purchase certain percentage of stocks of the target company for influencing the management.

Whereas, during asset acquisition the company buys all parts of the target company’s assets and

the target sustains as a legal entity. Based on the significance of shares of stocks, the company

acquisitions are further categorized into three types. This includes: “complete take over (100%

of target’s issued shares)”, “majority (50-99%)”, and “minority (less than 50%)” (Yilmaz and

Tanyeri 2016). In addition to this, the merger and acquisition are depicted as to separate from the

actions which have several consequences based on the legal obligations, tax liabilities and

procedure of acquisition. Despite of this, in general the final outcome of M&A transactions

considered in which two or more companies are seen to combine their business affords and we

do not make an effort to separate this merger transaction from acquisition ones. In such a

situation, M&A is treated as a corporate finance service which provides M&A advice to the

firms (Ferris, Houston and Javakhadze 2016).

In context of classification of mergers and acquisitions, the main perspective of value

chain for M&A is categorized as horizontal, vertical or conglomerate. In case of horizontal

M&A, the target companies and the acquiring companies are depicted as competing in the same

industry. In addition to this, in horizontal business combination process the restructuring in

business occurs as a result of technological changes and liberalization. This particular trade is

evident in industries related to petroleum, the mobile and pharmaceuticals (Yılmaz and Tanyeri

2016). A similar example of this can be seen with the merger of two US giants namely Glaxo

and SmithKline Beecham with a total value of USD 76 billion. Based on the statement of the

former CEO of SmithKline Beecham the main aim of combination of two companies was

depicted with research and development synergies to drive the revenues and explore enormous

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

New Technologies - M&S Assignmentlg...

|9

|2308

|72

Financial Decision Making: Importance of Accountancy and Monetary Tasks in Businesslg...

|14

|3031

|211