Taxation Advice for J&D Partners, Joanne Tran, and Haufmann Pty Ltd

VerifiedAdded on 2023/01/06

|6

|1789

|63

Homework Assignment

AI Summary

This assignment provides a detailed analysis of three distinct tax scenarios. The first case focuses on J & D Partners, calculating partnership net income, partner distributions, and taxable income, including the application of a CGT discount. The second case addresses Joanne Tran's trust, determini...

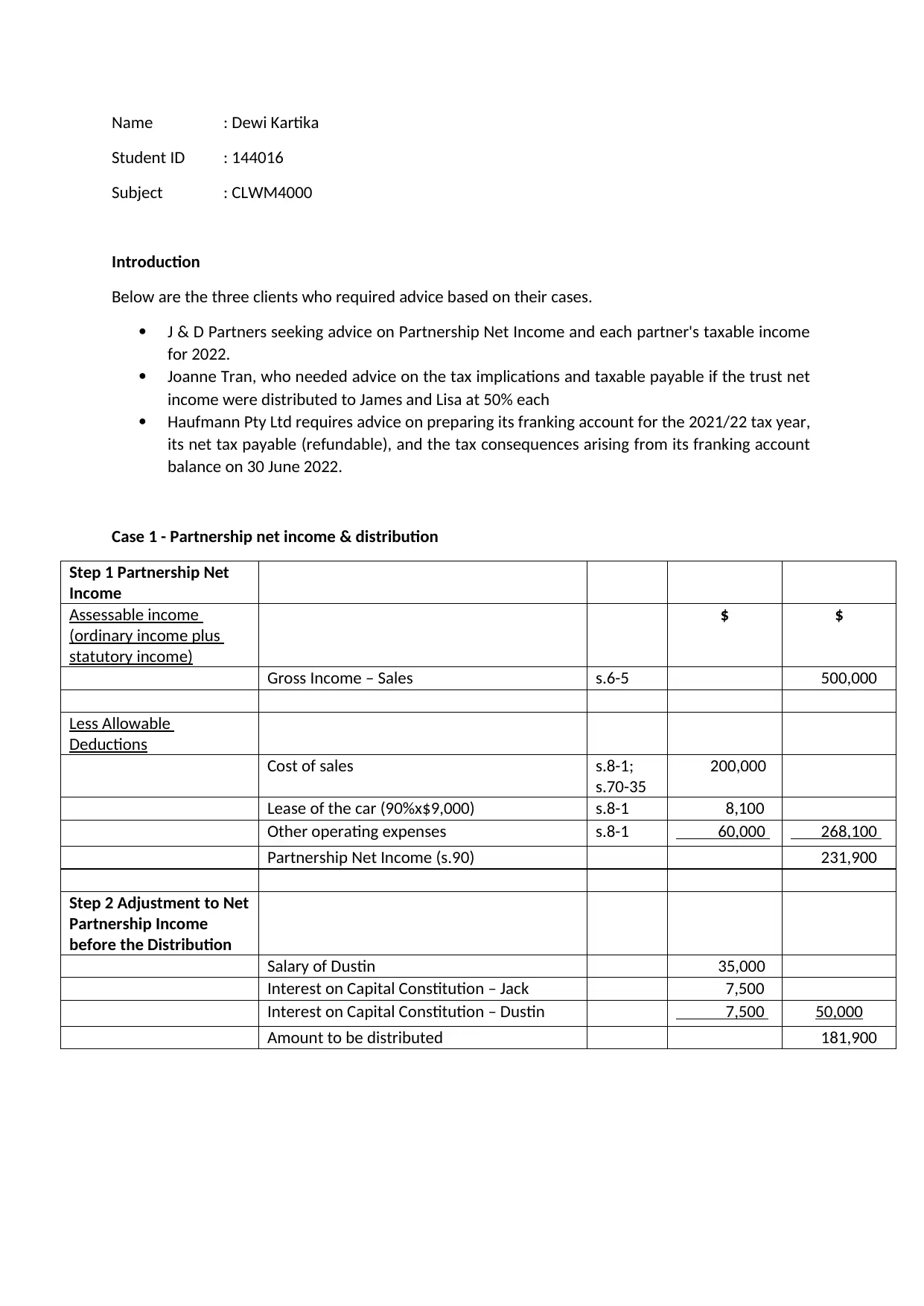

Name : Dewi Kartika

Student ID : 144016

Subject : CLWM4000

Introduction

Below are the three clients who required advice based on their cases.

J & D Partners seeking advice on Partnership Net Income and each partner's taxable income

for 2022.

Joanne Tran, who needed advice on the tax implications and taxable payable if the trust net

income were distributed to James and Lisa at 50% each

Haufmann Pty Ltd requires advice on preparing its franking account for the 2021/22 tax year,

its net tax payable (refundable), and the tax consequences arising from its franking account

balance on 30 June 2022.

Case 1 - Partnership net income & distribution

Step 1 Partnership Net

Income

Assessable income

(ordinary income plus

statutory income)

$ $

Gross Income – Sales s.6-5 500,000

Less Allowable

Deductions

Cost of sales s.8-1;

s.70-35

200,000

Lease of the car (90%x$9,000) s.8-1 8,100

Other operating expenses s.8-1 60,000 268,100

Partnership Net Income (s.90) 231,900

Step 2 Adjustment to Net

Partnership Income

before the Distribution

Salary of Dustin 35,000

Interest on Capital Constitution – Jack 7,500

Interest on Capital Constitution – Dustin 7,500 50,000

Amount to be distributed 181,900

Student ID : 144016

Subject : CLWM4000

Introduction

Below are the three clients who required advice based on their cases.

J & D Partners seeking advice on Partnership Net Income and each partner's taxable income

for 2022.

Joanne Tran, who needed advice on the tax implications and taxable payable if the trust net

income were distributed to James and Lisa at 50% each

Haufmann Pty Ltd requires advice on preparing its franking account for the 2021/22 tax year,

its net tax payable (refundable), and the tax consequences arising from its franking account

balance on 30 June 2022.

Case 1 - Partnership net income & distribution

Step 1 Partnership Net

Income

Assessable income

(ordinary income plus

statutory income)

$ $

Gross Income – Sales s.6-5 500,000

Less Allowable

Deductions

Cost of sales s.8-1;

s.70-35

200,000

Lease of the car (90%x$9,000) s.8-1 8,100

Other operating expenses s.8-1 60,000 268,100

Partnership Net Income (s.90) 231,900

Step 2 Adjustment to Net

Partnership Income

before the Distribution

Salary of Dustin 35,000

Interest on Capital Constitution – Jack 7,500

Interest on Capital Constitution – Dustin 7,500 50,000

Amount to be distributed 181,900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

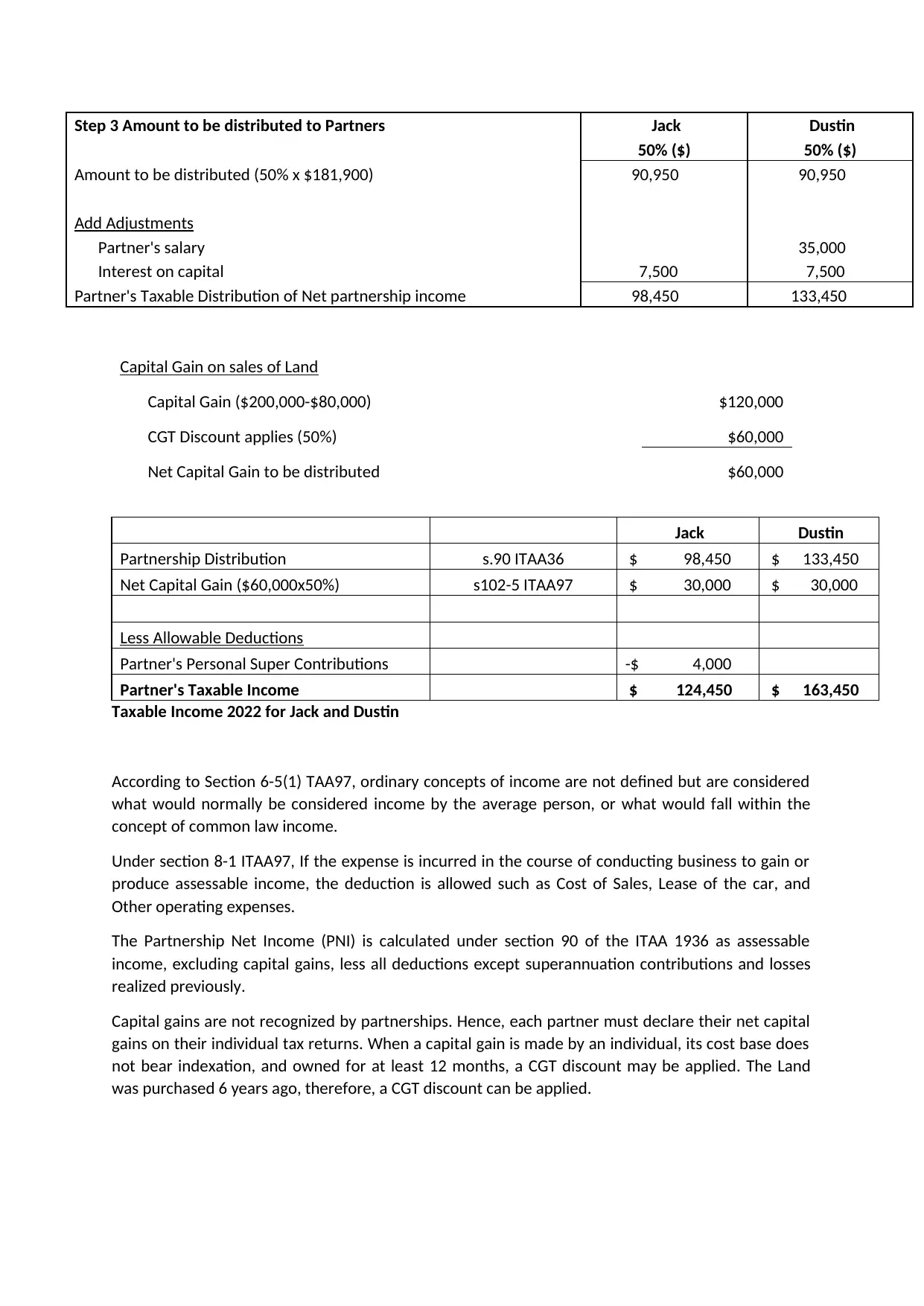

Step 3 Amount to be distributed to Partners Jack Dustin

50% ($) 50% ($)

Amount to be distributed (50% x $181,900) 90,950 90,950

Add Adjustments

Partner's salary 35,000

Interest on capital 7,500 7,500

Partner's Taxable Distribution of Net partnership income 98,450 133,450

Capital Gain on sales of Land

Capital Gain ($200,000-$80,000) $120,000

CGT Discount applies (50%) $60,000

Net Capital Gain to be distributed $60,000

Jack Dustin

Partnership Distribution s.90 ITAA36 $ 98,450 $ 133,450

Net Capital Gain ($60,000x50%) s102-5 ITAA97 $ 30,000 $ 30,000

Less Allowable Deductions

Partner's Personal Super Contributions -$ 4,000

Partner's Taxable Income $ 124,450 $ 163,450

Taxable Income 2022 for Jack and Dustin

According to Section 6-5(1) TAA97, ordinary concepts of income are not defined but are considered

what would normally be considered income by the average person, or what would fall within the

concept of common law income.

Under section 8-1 ITAA97, If the expense is incurred in the course of conducting business to gain or

produce assessable income, the deduction is allowed such as Cost of Sales, Lease of the car, and

Other operating expenses.

The Partnership Net Income (PNI) is calculated under section 90 of the ITAA 1936 as assessable

income, excluding capital gains, less all deductions except superannuation contributions and losses

realized previously.

Capital gains are not recognized by partnerships. Hence, each partner must declare their net capital

gains on their individual tax returns. When a capital gain is made by an individual, its cost base does

not bear indexation, and owned for at least 12 months, a CGT discount may be applied. The Land

was purchased 6 years ago, therefore, a CGT discount can be applied.

50% ($) 50% ($)

Amount to be distributed (50% x $181,900) 90,950 90,950

Add Adjustments

Partner's salary 35,000

Interest on capital 7,500 7,500

Partner's Taxable Distribution of Net partnership income 98,450 133,450

Capital Gain on sales of Land

Capital Gain ($200,000-$80,000) $120,000

CGT Discount applies (50%) $60,000

Net Capital Gain to be distributed $60,000

Jack Dustin

Partnership Distribution s.90 ITAA36 $ 98,450 $ 133,450

Net Capital Gain ($60,000x50%) s102-5 ITAA97 $ 30,000 $ 30,000

Less Allowable Deductions

Partner's Personal Super Contributions -$ 4,000

Partner's Taxable Income $ 124,450 $ 163,450

Taxable Income 2022 for Jack and Dustin

According to Section 6-5(1) TAA97, ordinary concepts of income are not defined but are considered

what would normally be considered income by the average person, or what would fall within the

concept of common law income.

Under section 8-1 ITAA97, If the expense is incurred in the course of conducting business to gain or

produce assessable income, the deduction is allowed such as Cost of Sales, Lease of the car, and

Other operating expenses.

The Partnership Net Income (PNI) is calculated under section 90 of the ITAA 1936 as assessable

income, excluding capital gains, less all deductions except superannuation contributions and losses

realized previously.

Capital gains are not recognized by partnerships. Hence, each partner must declare their net capital

gains on their individual tax returns. When a capital gain is made by an individual, its cost base does

not bear indexation, and owned for at least 12 months, a CGT discount may be applied. The Land

was purchased 6 years ago, therefore, a CGT discount can be applied.

Case 2 - Trust income and distributions

Due to the fact that trusts are not separate legal entities, they do not have to pay taxes. The

beneficiary distribution must be documented on a tax return. There is no taxable income for the

trust; it calculates a net income or loss on the same basis as a resident taxpayer.

To calculate the Franking dividend, 30% was assumed to be the company tax rate for Joanne Tran

Family Trust.

Beneficiary Presentl

y

Entitled

Distributio

n %

Legal

Disabilit

y

ITAA

Sectio

n

Amount

Presently

Entitled

Tax Paid

by Tax Rate

James

18 years

Yes

(s.101) 50% No s97 (1) $ 31,571.43

Beneficiar

y

Marginal Rates of tax for

an Australian resident

individual

Lisa

16 years

Yes

(s.101) 50% Yes s98 (1) $ 31,571.43 Trustee

Tax will be paid by the

trustee at the rate of

45% under Division 6AA.

$ 63,142.86

According to Section 101, If the trustee distributes the trust to the beneficiary, the beneficiary is

considered to be presently entitled to the trust.

As stated in section 97(1), a beneficiary must be presently entitled to receive benefits and not legally

disabled. Beneficiaries are required to include this income in their assessable incomes.

In accordance with section 98(1), the beneficiary is presently entitled to and under a legal disability.

The beneficiary gets a tax credit from the trustee when the trustee pays tax on the beneficiary's

share of income. Taylor v FCT demonstrates the existence of a legal disability when the beneficiary is

unable to give the legal discharge for the benefit received. A person's age, insanity or bankruptcy

may be contributing factors. The legal age in Australia is 18 years old, James is 18 years old, so he is

not legally disabled. However, Lisa is 16 years old, and because of this she is under legal disability.

Net rental income $ 57,000.00

Fully Franked dividend $ 4,300.00

Franking credit ($4,300 x 30/70) $ 1,842.86

Net Trust Income s.95 ITAA36 $ 63,142.86

Due to the fact that trusts are not separate legal entities, they do not have to pay taxes. The

beneficiary distribution must be documented on a tax return. There is no taxable income for the

trust; it calculates a net income or loss on the same basis as a resident taxpayer.

To calculate the Franking dividend, 30% was assumed to be the company tax rate for Joanne Tran

Family Trust.

Beneficiary Presentl

y

Entitled

Distributio

n %

Legal

Disabilit

y

ITAA

Sectio

n

Amount

Presently

Entitled

Tax Paid

by Tax Rate

James

18 years

Yes

(s.101) 50% No s97 (1) $ 31,571.43

Beneficiar

y

Marginal Rates of tax for

an Australian resident

individual

Lisa

16 years

Yes

(s.101) 50% Yes s98 (1) $ 31,571.43 Trustee

Tax will be paid by the

trustee at the rate of

45% under Division 6AA.

$ 63,142.86

According to Section 101, If the trustee distributes the trust to the beneficiary, the beneficiary is

considered to be presently entitled to the trust.

As stated in section 97(1), a beneficiary must be presently entitled to receive benefits and not legally

disabled. Beneficiaries are required to include this income in their assessable incomes.

In accordance with section 98(1), the beneficiary is presently entitled to and under a legal disability.

The beneficiary gets a tax credit from the trustee when the trustee pays tax on the beneficiary's

share of income. Taylor v FCT demonstrates the existence of a legal disability when the beneficiary is

unable to give the legal discharge for the benefit received. A person's age, insanity or bankruptcy

may be contributing factors. The legal age in Australia is 18 years old, James is 18 years old, so he is

not legally disabled. However, Lisa is 16 years old, and because of this she is under legal disability.

Net rental income $ 57,000.00

Fully Franked dividend $ 4,300.00

Franking credit ($4,300 x 30/70) $ 1,842.86

Net Trust Income s.95 ITAA36 $ 63,142.86

You're viewing a preview

Unlock full access by subscribing today!

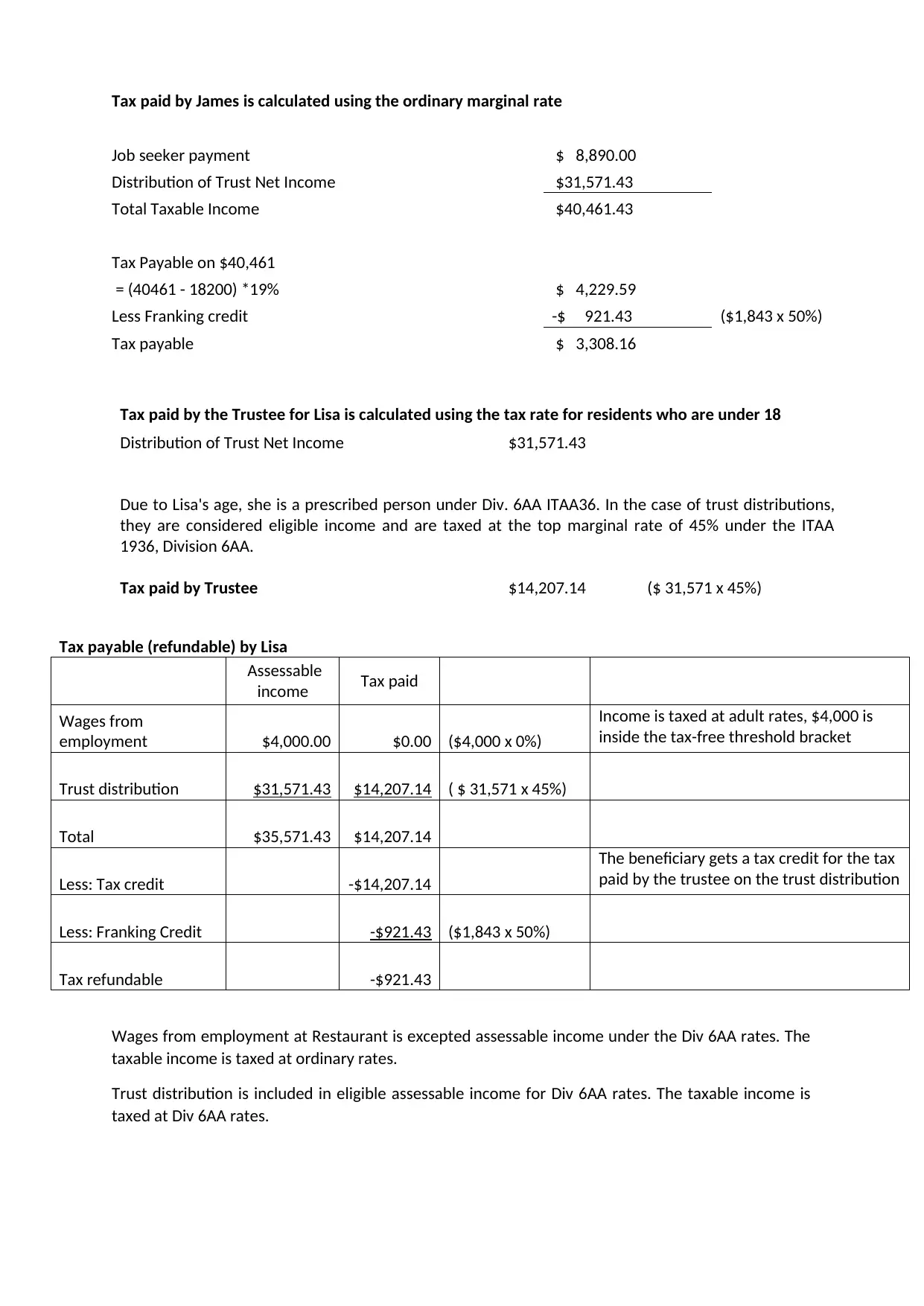

Tax paid by the Trustee for Lisa is calculated using the tax rate for residents who are under 18

Distribution of Trust Net Income $31,571.43

Due to Lisa's age, she is a prescribed person under Div. 6AA ITAA36. In the case of trust distributions,

they are considered eligible income and are taxed at the top marginal rate of 45% under the ITAA

1936, Division 6AA.

Tax paid by Trustee $14,207.14 ($ 31,571 x 45%)

Tax payable (refundable) by Lisa

Assessable

income Tax paid

Wages from

employment $4,000.00 $0.00 ($4,000 x 0%)

Income is taxed at adult rates, $4,000 is

inside the tax-free threshold bracket

Trust distribution $31,571.43 $14,207.14 ( $ 31,571 x 45%)

Total $35,571.43 $14,207.14

Less: Tax credit -$14,207.14

The beneficiary gets a tax credit for the tax

paid by the trustee on the trust distribution

Less: Franking Credit -$921.43 ($1,843 x 50%)

Tax refundable -$921.43

Wages from employment at Restaurant is excepted assessable income under the Div 6AA rates. The

taxable income is taxed at ordinary rates.

Trust distribution is included in eligible assessable income for Div 6AA rates. The taxable income is

taxed at Div 6AA rates.

Tax paid by James is calculated using the ordinary marginal rate

Job seeker payment $ 8,890.00

Distribution of Trust Net Income $31,571.43

Total Taxable Income $40,461.43

Tax Payable on $40,461

= (40461 - 18200) *19% $ 4,229.59

Less Franking credit -$ 921.43 ($1,843 x 50%)

Tax payable $ 3,308.16

Distribution of Trust Net Income $31,571.43

Due to Lisa's age, she is a prescribed person under Div. 6AA ITAA36. In the case of trust distributions,

they are considered eligible income and are taxed at the top marginal rate of 45% under the ITAA

1936, Division 6AA.

Tax paid by Trustee $14,207.14 ($ 31,571 x 45%)

Tax payable (refundable) by Lisa

Assessable

income Tax paid

Wages from

employment $4,000.00 $0.00 ($4,000 x 0%)

Income is taxed at adult rates, $4,000 is

inside the tax-free threshold bracket

Trust distribution $31,571.43 $14,207.14 ( $ 31,571 x 45%)

Total $35,571.43 $14,207.14

Less: Tax credit -$14,207.14

The beneficiary gets a tax credit for the tax

paid by the trustee on the trust distribution

Less: Franking Credit -$921.43 ($1,843 x 50%)

Tax refundable -$921.43

Wages from employment at Restaurant is excepted assessable income under the Div 6AA rates. The

taxable income is taxed at ordinary rates.

Trust distribution is included in eligible assessable income for Div 6AA rates. The taxable income is

taxed at Div 6AA rates.

Tax paid by James is calculated using the ordinary marginal rate

Job seeker payment $ 8,890.00

Distribution of Trust Net Income $31,571.43

Total Taxable Income $40,461.43

Tax Payable on $40,461

= (40461 - 18200) *19% $ 4,229.59

Less Franking credit -$ 921.43 ($1,843 x 50%)

Tax payable $ 3,308.16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

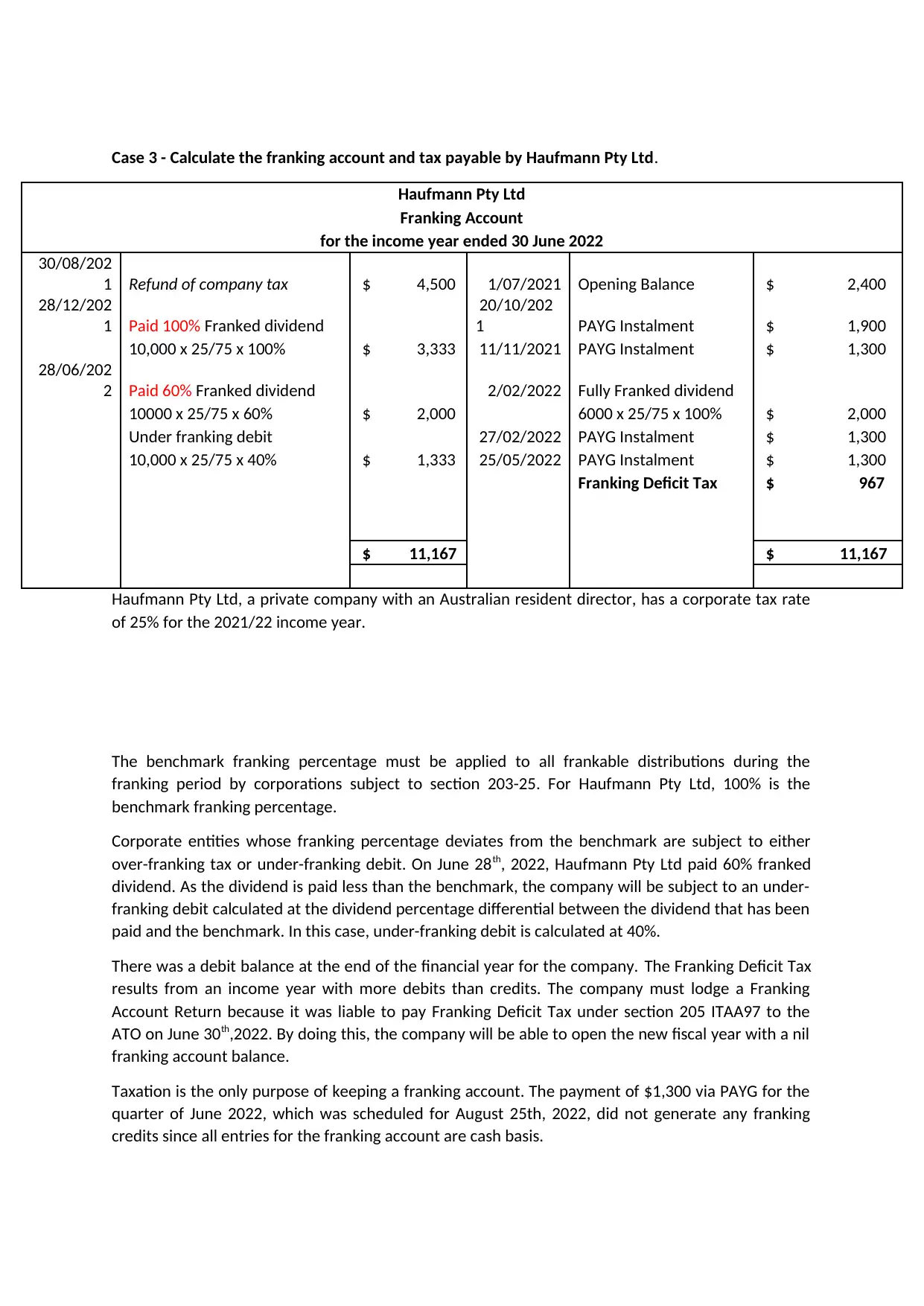

Case 3 - Calculate the franking account and tax payable by Haufmann Pty Ltd.

Haufmann Pty Ltd

Franking Account

for the income year ended 30 June 2022

30/08/202

1 Refund of company tax $ 4,500 1/07/2021 Opening Balance $ 2,400

28/12/202

1 Paid 100% Franked dividend

20/10/202

1 PAYG Instalment $ 1,900

10,000 x 25/75 x 100% $ 3,333 11/11/2021 PAYG Instalment $ 1,300

28/06/202

2 Paid 60% Franked dividend 2/02/2022 Fully Franked dividend

10000 x 25/75 x 60% $ 2,000 6000 x 25/75 x 100% $ 2,000

Under franking debit 27/02/2022 PAYG Instalment $ 1,300

10,000 x 25/75 x 40% $ 1,333 25/05/2022 PAYG Instalment $ 1,300

Franking Deficit Tax $ 967

$ 11,167 $ 11,167

Haufmann Pty Ltd, a private company with an Australian resident director, has a corporate tax rate

of 25% for the 2021/22 income year.

The benchmark franking percentage must be applied to all frankable distributions during the

franking period by corporations subject to section 203-25. For Haufmann Pty Ltd, 100% is the

benchmark franking percentage.

Corporate entities whose franking percentage deviates from the benchmark are subject to either

over-franking tax or under-franking debit. On June 28th, 2022, Haufmann Pty Ltd paid 60% franked

dividend. As the dividend is paid less than the benchmark, the company will be subject to an under-

franking debit calculated at the dividend percentage differential between the dividend that has been

paid and the benchmark. In this case, under-franking debit is calculated at 40%.

There was a debit balance at the end of the financial year for the company. The Franking Deficit Tax

results from an income year with more debits than credits. The company must lodge a Franking

Account Return because it was liable to pay Franking Deficit Tax under section 205 ITAA97 to the

ATO on June 30th,2022. By doing this, the company will be able to open the new fiscal year with a nil

franking account balance.

Taxation is the only purpose of keeping a franking account. The payment of $1,300 via PAYG for the

quarter of June 2022, which was scheduled for August 25th, 2022, did not generate any franking

credits since all entries for the franking account are cash basis.

Haufmann Pty Ltd

Franking Account

for the income year ended 30 June 2022

30/08/202

1 Refund of company tax $ 4,500 1/07/2021 Opening Balance $ 2,400

28/12/202

1 Paid 100% Franked dividend

20/10/202

1 PAYG Instalment $ 1,900

10,000 x 25/75 x 100% $ 3,333 11/11/2021 PAYG Instalment $ 1,300

28/06/202

2 Paid 60% Franked dividend 2/02/2022 Fully Franked dividend

10000 x 25/75 x 60% $ 2,000 6000 x 25/75 x 100% $ 2,000

Under franking debit 27/02/2022 PAYG Instalment $ 1,300

10,000 x 25/75 x 40% $ 1,333 25/05/2022 PAYG Instalment $ 1,300

Franking Deficit Tax $ 967

$ 11,167 $ 11,167

Haufmann Pty Ltd, a private company with an Australian resident director, has a corporate tax rate

of 25% for the 2021/22 income year.

The benchmark franking percentage must be applied to all frankable distributions during the

franking period by corporations subject to section 203-25. For Haufmann Pty Ltd, 100% is the

benchmark franking percentage.

Corporate entities whose franking percentage deviates from the benchmark are subject to either

over-franking tax or under-franking debit. On June 28th, 2022, Haufmann Pty Ltd paid 60% franked

dividend. As the dividend is paid less than the benchmark, the company will be subject to an under-

franking debit calculated at the dividend percentage differential between the dividend that has been

paid and the benchmark. In this case, under-franking debit is calculated at 40%.

There was a debit balance at the end of the financial year for the company. The Franking Deficit Tax

results from an income year with more debits than credits. The company must lodge a Franking

Account Return because it was liable to pay Franking Deficit Tax under section 205 ITAA97 to the

ATO on June 30th,2022. By doing this, the company will be able to open the new fiscal year with a nil

franking account balance.

Taxation is the only purpose of keeping a franking account. The payment of $1,300 via PAYG for the

quarter of June 2022, which was scheduled for August 25th, 2022, did not generate any franking

credits since all entries for the franking account are cash basis.

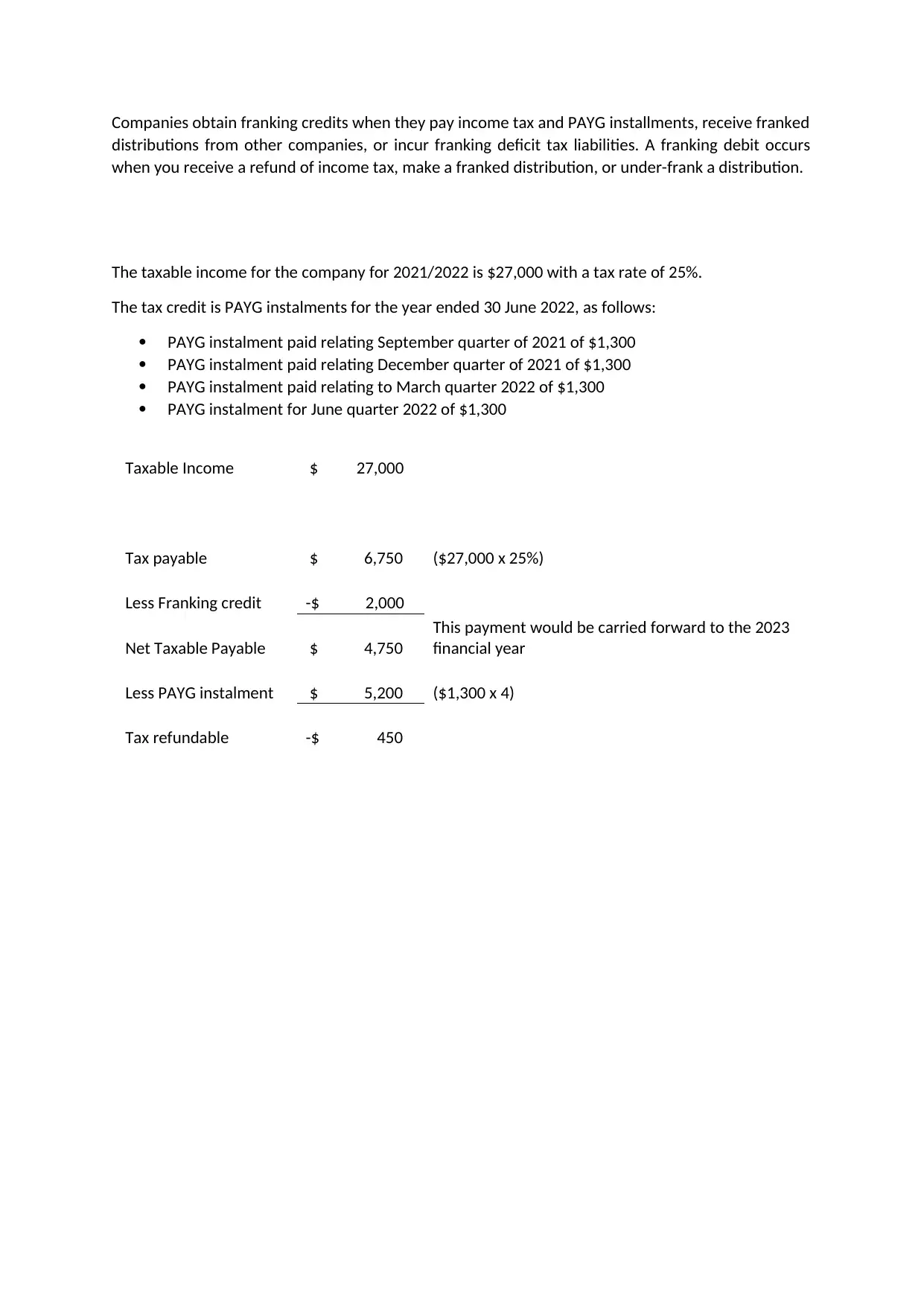

Companies obtain franking credits when they pay income tax and PAYG installments, receive franked

distributions from other companies, or incur franking deficit tax liabilities. A franking debit occurs

when you receive a refund of income tax, make a franked distribution, or under-frank a distribution.

The taxable income for the company for 2021/2022 is $27,000 with a tax rate of 25%.

The tax credit is PAYG instalments for the year ended 30 June 2022, as follows:

PAYG instalment paid relating September quarter of 2021 of $1,300

PAYG instalment paid relating December quarter of 2021 of $1,300

PAYG instalment paid relating to March quarter 2022 of $1,300

PAYG instalment for June quarter 2022 of $1,300

Taxable Income $ 27,000

Tax payable $ 6,750 ($27,000 x 25%)

Less Franking credit -$ 2,000

Net Taxable Payable $ 4,750

This payment would be carried forward to the 2023

financial year

Less PAYG instalment $ 5,200 ($1,300 x 4)

Tax refundable -$ 450

distributions from other companies, or incur franking deficit tax liabilities. A franking debit occurs

when you receive a refund of income tax, make a franked distribution, or under-frank a distribution.

The taxable income for the company for 2021/2022 is $27,000 with a tax rate of 25%.

The tax credit is PAYG instalments for the year ended 30 June 2022, as follows:

PAYG instalment paid relating September quarter of 2021 of $1,300

PAYG instalment paid relating December quarter of 2021 of $1,300

PAYG instalment paid relating to March quarter 2022 of $1,300

PAYG instalment for June quarter 2022 of $1,300

Taxable Income $ 27,000

Tax payable $ 6,750 ($27,000 x 25%)

Less Franking credit -$ 2,000

Net Taxable Payable $ 4,750

This payment would be carried forward to the 2023

financial year

Less PAYG instalment $ 5,200 ($1,300 x 4)

Tax refundable -$ 450

You're viewing a preview

Unlock full access by subscribing today!

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.