Understanding the Impact of Bad Loans on Indian Banking Industry

VerifiedAdded on 2023/04/21

|68

|16989

|140

AI Summary

This research paper focuses on the impact of bad loans on the Indian banking industry. It discusses the challenges faced by banks due to non-performing assets and explores the macroeconomic factors that contribute to bad loans. The paper also highlights the measures taken by the government to reduce the risk associated with non-performing assets.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Name of the Student

Name of the University

Author’s Note

1

Name of the University

Author’s Note

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Chapter 1: Introduction................................................................................................................4

What is the issue/problem?.......................................................................................................5

Why is the issue/problem important?......................................................................................6

Context of Research...................................................................................................................6

Research Questions:....................................................................................................................14

Chapter 2: Literature Review.....................................................................................................14

Summary of Literature............................................................................................................19

Methodology.............................................................................................................................21

Research Type..........................................................................................................................22

Data Analysis Tools..................................................................................................................23

Chapter 4: Findings and Analysis..............................................................................................39

Limitations of the Research....................................................................................................53

Chapter 5: Conclusion & Findings............................................................................................54

Causes that led to rising bad loans.........................................................................................57

Curative Measures...................................................................................................................59

References.....................................................................................................................................62

2

Chapter 1: Introduction................................................................................................................4

What is the issue/problem?.......................................................................................................5

Why is the issue/problem important?......................................................................................6

Context of Research...................................................................................................................6

Research Questions:....................................................................................................................14

Chapter 2: Literature Review.....................................................................................................14

Summary of Literature............................................................................................................19

Methodology.............................................................................................................................21

Research Type..........................................................................................................................22

Data Analysis Tools..................................................................................................................23

Chapter 4: Findings and Analysis..............................................................................................39

Limitations of the Research....................................................................................................53

Chapter 5: Conclusion & Findings............................................................................................54

Causes that led to rising bad loans.........................................................................................57

Curative Measures...................................................................................................................59

References.....................................................................................................................................62

2

Chapter 1: Introduction

The major challenges that are being faced by the Indian banking industry circumscribes

not only issues related to financial statements but also the incorporation of that long and the way

to understand its impact upon the financial health of the firms. Notably there are various

macroeconomic parameters that renders their impact in a significant level due to inter temporal

level of environment of the non-performing assets considered to be bad loans, the market

capitalization and the core competence factors. It is to be understood that the macroeconomic

parametric factors that examines the bad loans in accordance with the four key causes which are

awful supervision, cost consciousness, uncertainties in the market and many more. The feedback

phase is from 2005 to 2017 where various panels of data are being statistically estimated to

understand the Frontier model Garner causality, dynamic panel models, etc. that crucial impact

upon the banks. In this paper, this deterministic approach have been implemented to understand

the outcome of bad loans and their response that impact the banks as well as the macroeconomic

parametric factors that are associated with the commercial banking sector in India.

The non-performing assets are one of the crucial aspect of concern for every Banks is not

only the entire performance but also simultaneously the areas through which the bank can

improve their performance. From a critical point of view, the realistic Sinha you incorporate that

Indian banking division is in the process of experiencing serious issues regarding the non-

performing assets. The NPAs has relatively bigger impact upon ballistic view the credit non

payments as well as upon the liquidity of the banks. Specifically, upon the public division Bank

it has been found that the non-performing assets if handled properly then it enhances the

competence and effectiveness of Banking performance. Various steps are considered by the

3

The major challenges that are being faced by the Indian banking industry circumscribes

not only issues related to financial statements but also the incorporation of that long and the way

to understand its impact upon the financial health of the firms. Notably there are various

macroeconomic parameters that renders their impact in a significant level due to inter temporal

level of environment of the non-performing assets considered to be bad loans, the market

capitalization and the core competence factors. It is to be understood that the macroeconomic

parametric factors that examines the bad loans in accordance with the four key causes which are

awful supervision, cost consciousness, uncertainties in the market and many more. The feedback

phase is from 2005 to 2017 where various panels of data are being statistically estimated to

understand the Frontier model Garner causality, dynamic panel models, etc. that crucial impact

upon the banks. In this paper, this deterministic approach have been implemented to understand

the outcome of bad loans and their response that impact the banks as well as the macroeconomic

parametric factors that are associated with the commercial banking sector in India.

The non-performing assets are one of the crucial aspect of concern for every Banks is not

only the entire performance but also simultaneously the areas through which the bank can

improve their performance. From a critical point of view, the realistic Sinha you incorporate that

Indian banking division is in the process of experiencing serious issues regarding the non-

performing assets. The NPAs has relatively bigger impact upon ballistic view the credit non

payments as well as upon the liquidity of the banks. Specifically, upon the public division Bank

it has been found that the non-performing assets if handled properly then it enhances the

competence and effectiveness of Banking performance. Various steps are considered by the

3

government in order to decrease the non-performing assets as well as the risk associated due to

the nonperformance of banking assets. It is to be understood that 0% non-performing assets is

quite impractical and hence in that case Indian banks must printer their attention to make sure

that the offer loans but most importantly to the creditworthy clients.

What is the issue/problem?

The implication of the bad loans is associated with its importance for which it arises in

the commercial banks of India. Notably every Indian banks needs assets we can provide credit

loans to potential consumer service becomes a matter of worrying if those assets becomes non-

performing for the banks. Non-performing assets are one of the most excellent tool that measures

the effectiveness of the bank and how sound performance it is executing in the market where it

prevail. Bad loans representative of a Bank's performance but also an essential. The towards the

credit risk associated with the banking performance. Bad loans are the allowable stress that every

banking business have to suffer subsequently. However, crucial necessity loans available the cost

of the fact that it remains unutilized or non-performing. Understanding on this aspect focuses on

the reliability of the customers as well as the banks’ ability to strategize the process of

overseeing bad loans. Locate me the public sector banks of demonstrated their greater execution

as compared to the private divisional banks of the country of India to the extent up to which

money that leads to the task under consideration.

The public Centre banks on this respect of non-performing assets have found to

demonstrate their performance coupled with greater outcome. How were the main issue of the

public sector bank without expanding level of non-performing assets despite of the fact that

4

the nonperformance of banking assets. It is to be understood that 0% non-performing assets is

quite impractical and hence in that case Indian banks must printer their attention to make sure

that the offer loans but most importantly to the creditworthy clients.

What is the issue/problem?

The implication of the bad loans is associated with its importance for which it arises in

the commercial banks of India. Notably every Indian banks needs assets we can provide credit

loans to potential consumer service becomes a matter of worrying if those assets becomes non-

performing for the banks. Non-performing assets are one of the most excellent tool that measures

the effectiveness of the bank and how sound performance it is executing in the market where it

prevail. Bad loans representative of a Bank's performance but also an essential. The towards the

credit risk associated with the banking performance. Bad loans are the allowable stress that every

banking business have to suffer subsequently. However, crucial necessity loans available the cost

of the fact that it remains unutilized or non-performing. Understanding on this aspect focuses on

the reliability of the customers as well as the banks’ ability to strategize the process of

overseeing bad loans. Locate me the public sector banks of demonstrated their greater execution

as compared to the private divisional banks of the country of India to the extent up to which

money that leads to the task under consideration.

The public Centre banks on this respect of non-performing assets have found to

demonstrate their performance coupled with greater outcome. How were the main issue of the

public sector bank without expanding level of non-performing assets despite of the fact that

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

segments ok banking industry which non-performing Assets has crucial impact is monotonically

decreasing impact on the NPAs. To emphasize this issue it can be incorporated that the decrease

in the badlands have reinforced the examination of credit system of the consumers as well as

implementation of appropriate regulatory governance over the risk associated with it. The Indian

banking division has confirmed that major issues with the public sector banks in comparison to

thought of the day with division banks when the major aspect of concern is to enhance The

Prophecy and see and success level of the banks which is getting hamper due to improper control

over the non-performing assets.

Why is the issue/problem important?

The issue is important as per Mukherjee (2016), because of the fact that Indian banks are

top list of bad loans has collected by the lenders of the country. Compare to other economy is

like that of United Kingdom, states of America Japan, china, etc. it is been found that India is

consulted with dog challenge regarding non-performing assets being 5TH Nation among the 39

big Economics of the world that is suffered due to improper regulation or methodical

systematization of bad loans as well as non-performing assets.

Context of Research

The research is being performed upon the Indian banking industry and objectives of the

research is associated to create a proper information regarding the performance of the non-

performing assets like bad loans and to understand the extent of impact of it upon the Indian

banking sector. Confrontation with the problem of bad loans that is extensively taking place in

the Indian banking industry dog it is being rent at V nation in the world with such problem there

5

decreasing impact on the NPAs. To emphasize this issue it can be incorporated that the decrease

in the badlands have reinforced the examination of credit system of the consumers as well as

implementation of appropriate regulatory governance over the risk associated with it. The Indian

banking division has confirmed that major issues with the public sector banks in comparison to

thought of the day with division banks when the major aspect of concern is to enhance The

Prophecy and see and success level of the banks which is getting hamper due to improper control

over the non-performing assets.

Why is the issue/problem important?

The issue is important as per Mukherjee (2016), because of the fact that Indian banks are

top list of bad loans has collected by the lenders of the country. Compare to other economy is

like that of United Kingdom, states of America Japan, china, etc. it is been found that India is

consulted with dog challenge regarding non-performing assets being 5TH Nation among the 39

big Economics of the world that is suffered due to improper regulation or methodical

systematization of bad loans as well as non-performing assets.

Context of Research

The research is being performed upon the Indian banking industry and objectives of the

research is associated to create a proper information regarding the performance of the non-

performing assets like bad loans and to understand the extent of impact of it upon the Indian

banking sector. Confrontation with the problem of bad loans that is extensively taking place in

the Indian banking industry dog it is being rent at V nation in the world with such problem there

5

is requisition for understanding the industrial scenario of the first Commercial Bank of India and

these financial data and information regarding non-performing assets are being utilized to

conduct the research.

Banking environment in India

The environment of the research circumscribes the Indian banking industry and

specifically the commercial banks of the country. The problems comes under focus due to the

challenges of bad loans confronted by banks. The ranking of the country in terms of faced

problem regarding bad loans is five throughout the world. The growth of the banking sector is

rapid and hence commercial banks are being taken under consideration for a better research to

understand the fast moving complex market scenarios based on fluctuating industrial conditions.

The co-operative banks and the commercial; banks together comprises of the Indian banking

industry in terms of facing challenges regarding the problems of non-performing assets. Hence,

banking industry of India has large involvement of the commercial banks as well as cooperative

banks. The proportion of the commercial banks are segregated with scheduled and non-

scheduled commercial banks upon which the scheduled commercial banks are one of the

commercial banks that incorporates the second schedule of The Reserve Bank of India Act 1934.

This scheduled commercial banks the activity based on certain circumstances where the

connection with paid up capital, reserves, etc. are of crucial importance. On the other hand the

scheduled commercial banks conquerors of the old and new domestic private sector banks, local

rural banks, overseas sector banks, State bank of India and its subsidiaries. The banks in India is

thus state owned specifically in two phases by the year 1969 and 1980 where 14 major private

sector banks were commenced and the remaining other 6 were established by the 1980 followed

6

these financial data and information regarding non-performing assets are being utilized to

conduct the research.

Banking environment in India

The environment of the research circumscribes the Indian banking industry and

specifically the commercial banks of the country. The problems comes under focus due to the

challenges of bad loans confronted by banks. The ranking of the country in terms of faced

problem regarding bad loans is five throughout the world. The growth of the banking sector is

rapid and hence commercial banks are being taken under consideration for a better research to

understand the fast moving complex market scenarios based on fluctuating industrial conditions.

The co-operative banks and the commercial; banks together comprises of the Indian banking

industry in terms of facing challenges regarding the problems of non-performing assets. Hence,

banking industry of India has large involvement of the commercial banks as well as cooperative

banks. The proportion of the commercial banks are segregated with scheduled and non-

scheduled commercial banks upon which the scheduled commercial banks are one of the

commercial banks that incorporates the second schedule of The Reserve Bank of India Act 1934.

This scheduled commercial banks the activity based on certain circumstances where the

connection with paid up capital, reserves, etc. are of crucial importance. On the other hand the

scheduled commercial banks conquerors of the old and new domestic private sector banks, local

rural banks, overseas sector banks, State bank of India and its subsidiaries. The banks in India is

thus state owned specifically in two phases by the year 1969 and 1980 where 14 major private

sector banks were commenced and the remaining other 6 were established by the 1980 followed

6

by the era of nationalization. The assessment was done based on the share of the credit for which

90 % of the divisional segment were done for government possessed bank while the rest of the

segment is being done by uniformly segregating them among the foreign banks and that of the

small privately owned banks whose size limit were set by the government as per the protocols of

nationalization. It is being found that from 1980 to 1992 the public sector banks were completely

owned by the government of the country. The first and foremost bank that shifted to become a

public sector bank was State Bank of India (SBI) by the year 1992-1993.

Figure 1: Comparison of different countries in terms of loans borrowed from the financial institutions

7

90 % of the divisional segment were done for government possessed bank while the rest of the

segment is being done by uniformly segregating them among the foreign banks and that of the

small privately owned banks whose size limit were set by the government as per the protocols of

nationalization. It is being found that from 1980 to 1992 the public sector banks were completely

owned by the government of the country. The first and foremost bank that shifted to become a

public sector bank was State Bank of India (SBI) by the year 1992-1993.

Figure 1: Comparison of different countries in terms of loans borrowed from the financial institutions

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2: Trends of housing loans Figure 3: Bank wise segmentation of the loans taken by households

Source: Ganapathy, Alagarsamy and Raguraman. (2017)

Since the nationalization of the banks it is been found that the banking sector is booming

based on it expansion in the market. From 1969 to 2015 the commercial banking sector have

found to grow up to 152 from 89. This raised the credibility of the banking financial services and

the products that are being deployed by them in the market. The images reveals that fact that

among the credit enjoyed by the households that are being obtained from various countries

throughout the world a brief comparison is being made between Brazil, China, Germany, India,

Indonesia, Kenya, UK, USA and Russia. There it is been seen that the borrowing from the

financial institutions specifically in India have lessened as compared to other countries. This may

be due to the reason that the company is not able to maintain the balance between acquiring

deposits to make and siphoning them off to the people who are making requisitions for loans.

8

Source: Ganapathy, Alagarsamy and Raguraman. (2017)

Since the nationalization of the banks it is been found that the banking sector is booming

based on it expansion in the market. From 1969 to 2015 the commercial banking sector have

found to grow up to 152 from 89. This raised the credibility of the banking financial services and

the products that are being deployed by them in the market. The images reveals that fact that

among the credit enjoyed by the households that are being obtained from various countries

throughout the world a brief comparison is being made between Brazil, China, Germany, India,

Indonesia, Kenya, UK, USA and Russia. There it is been seen that the borrowing from the

financial institutions specifically in India have lessened as compared to other countries. This may

be due to the reason that the company is not able to maintain the balance between acquiring

deposits to make and siphoning them off to the people who are making requisitions for loans.

8

Due to this reason the banks are raising their interest rate upon loans within fixed stipulated

periods and the common people are not found to properly repay their loans on time. This

consequently leads to low recovery rate of the bank debts and hence the bad loans becomes

higher and are being considered as the non-preforming assets for the banks. Also another reason

comes out as it is been seen that there are households within the country of India that are not able

to return bank the loans on time due to the reason that accounts of bad loans is getting higher in

case of the commercial banks of the country. These factors altogether is commencing the

provision of bad loans that are not being matched with equally payable amount by the loan takers

from the banks. Based on the problem it is being seen from the other two figures that the share of

the total credits from the banks is lower than the amount that the loan takers have to pay in return

of taking the loans. Moreover, it is also been seen from figure 3 that the common people are thus

getting interested in the foreign banks rather than the commercial banks of the country. The shift

is extracting the consumer share of the commercial banks and siphoning them off to the foreign

banks that are getting more amount of grip upon the country of India in terms of market

capitalization.

The commercial banks of the country are performing salient functions regarding

allowance for deposits made as well as lending loans as required. However, there is no risk

associated with the deposits made by the people as the banks are performing enough responsibly

in repaying the deposits along with the allotted rate of interest. On the other hand, in case of the

lending of the loans there is presence of sufficient amount of risk as there is less amount of

certainty regarding the repayment of loans. These non-repaid loans are no found to again work as

an asset for the banks and due to this reason these assets are not found to add any more amount

9

periods and the common people are not found to properly repay their loans on time. This

consequently leads to low recovery rate of the bank debts and hence the bad loans becomes

higher and are being considered as the non-preforming assets for the banks. Also another reason

comes out as it is been seen that there are households within the country of India that are not able

to return bank the loans on time due to the reason that accounts of bad loans is getting higher in

case of the commercial banks of the country. These factors altogether is commencing the

provision of bad loans that are not being matched with equally payable amount by the loan takers

from the banks. Based on the problem it is being seen from the other two figures that the share of

the total credits from the banks is lower than the amount that the loan takers have to pay in return

of taking the loans. Moreover, it is also been seen from figure 3 that the common people are thus

getting interested in the foreign banks rather than the commercial banks of the country. The shift

is extracting the consumer share of the commercial banks and siphoning them off to the foreign

banks that are getting more amount of grip upon the country of India in terms of market

capitalization.

The commercial banks of the country are performing salient functions regarding

allowance for deposits made as well as lending loans as required. However, there is no risk

associated with the deposits made by the people as the banks are performing enough responsibly

in repaying the deposits along with the allotted rate of interest. On the other hand, in case of the

lending of the loans there is presence of sufficient amount of risk as there is less amount of

certainty regarding the repayment of loans. These non-repaid loans are no found to again work as

an asset for the banks and due to this reason these assets are not found to add any more amount

9

of value in the banking performance and hence get allotted as the non-performing assets for the

banks that are termed as the bad loans. However, if proper emphasize is being given in

understanding the reason behinds such anomaly then it can be seen that the loans are given in

order to earn return from the lend people. However, their ability to repay the loans are not only

the factor in determining their ability to repay the loans bank. The banks are found not to be able

to maintain the balance between the deposits that are being made by people in the banks and

moreover they are raising the rate of interest upon loans. This is creating more gap between the

lending of capital and depositing of capital into the banks. When the mismatch or the imbalance

needs to be covered up then to do so the banks focuses upon raising the rate of interest in order to

cover up the gap. This is leading to further gap in the commercial banking sector and directing

the consumers to shift upon the foreign banks which are to found to be better competitors in

comparison to the commercial banks of the country. The whole scenario is a mismanagement of

the funds as well as a tendency to cover up the risk associated with the borrower and the lenders

at a faster rate without looking forward upon the ill effect of such financial discrepancies and

working strategy of the banks in the sole motive of profit maximization. Since the efficiency of

the banks and the condition of the financial health of the banks are sufficiently reflected by the

amount of bad loans that the banks have hence it is important that the commercial banks of India

should focus upon recovering their non-performing assets without losing customers to foreign

competitors and with accomplishing this activity based upon financially feasible manner that

would not threaten their stability in the industry for the long run. Since the bad loans are key

reflector of the banks financial stability hence the banks should such sort of plans that guarantees

that the loans will be recovered with the constant that loss of consumer share in the industry will

10

banks that are termed as the bad loans. However, if proper emphasize is being given in

understanding the reason behinds such anomaly then it can be seen that the loans are given in

order to earn return from the lend people. However, their ability to repay the loans are not only

the factor in determining their ability to repay the loans bank. The banks are found not to be able

to maintain the balance between the deposits that are being made by people in the banks and

moreover they are raising the rate of interest upon loans. This is creating more gap between the

lending of capital and depositing of capital into the banks. When the mismatch or the imbalance

needs to be covered up then to do so the banks focuses upon raising the rate of interest in order to

cover up the gap. This is leading to further gap in the commercial banking sector and directing

the consumers to shift upon the foreign banks which are to found to be better competitors in

comparison to the commercial banks of the country. The whole scenario is a mismanagement of

the funds as well as a tendency to cover up the risk associated with the borrower and the lenders

at a faster rate without looking forward upon the ill effect of such financial discrepancies and

working strategy of the banks in the sole motive of profit maximization. Since the efficiency of

the banks and the condition of the financial health of the banks are sufficiently reflected by the

amount of bad loans that the banks have hence it is important that the commercial banks of India

should focus upon recovering their non-performing assets without losing customers to foreign

competitors and with accomplishing this activity based upon financially feasible manner that

would not threaten their stability in the industry for the long run. Since the bad loans are key

reflector of the banks financial stability hence the banks should such sort of plans that guarantees

that the loans will be recovered with the constant that loss of consumer share in the industry will

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

be low from their side as no customer will feel insecure regarding their investments in the banks

as well as their credibility upon the banks will be intact. Notably, bad loans hinders the revenue

generation process up to the anticipated level if they are not recovered within or by 3 months

from the estimated recovery periods. However, banks faces the pressure of returning back the

deposits to the lenders and hence they have to create provisions for bank loans. When the banks

faces too much of bad loans then the performance of the banks are thus hindered as they are

committed to return the deposits back to the lenders. Moreover, the depositors have deposited

their money in order to gain interest form the banks. So the amount of interest upon the

principles of the deposited amount becomes also a liability for the banks as the banks are not

able to recover the amount due to the non-performing assets that is not able to add value to the

financial performance of the banks. Thus not only the banks but also the overall economy in

which the banks are being performing also gets affected by the bad loans of the commercial

banks. The net worth of the banks falls due to these non-performing assets as the extra amount of

valuation that their performing assets earns gets equally subtracted due to the provision made for

the non-performing assets that uncertainly took place. The account linked with the loans as not

sufficiently supervised due to which the bad loans are increasing followed by playing a key

factor in deteriorating the worth of the bank’s financial performance as well as leading to the

increase in the collateral securities due to the wilful non-repayment made to the borrowers. It is

also been seen that the amount of bad loans are more in the public sector banks in comparison to

that of the private sector banks. This signifies the fact that the banks needs to cover up their

loopholes in order to perform in a better way and lower their non-performing assets. Moreover,

11

as well as their credibility upon the banks will be intact. Notably, bad loans hinders the revenue

generation process up to the anticipated level if they are not recovered within or by 3 months

from the estimated recovery periods. However, banks faces the pressure of returning back the

deposits to the lenders and hence they have to create provisions for bank loans. When the banks

faces too much of bad loans then the performance of the banks are thus hindered as they are

committed to return the deposits back to the lenders. Moreover, the depositors have deposited

their money in order to gain interest form the banks. So the amount of interest upon the

principles of the deposited amount becomes also a liability for the banks as the banks are not

able to recover the amount due to the non-performing assets that is not able to add value to the

financial performance of the banks. Thus not only the banks but also the overall economy in

which the banks are being performing also gets affected by the bad loans of the commercial

banks. The net worth of the banks falls due to these non-performing assets as the extra amount of

valuation that their performing assets earns gets equally subtracted due to the provision made for

the non-performing assets that uncertainly took place. The account linked with the loans as not

sufficiently supervised due to which the bad loans are increasing followed by playing a key

factor in deteriorating the worth of the bank’s financial performance as well as leading to the

increase in the collateral securities due to the wilful non-repayment made to the borrowers. It is

also been seen that the amount of bad loans are more in the public sector banks in comparison to

that of the private sector banks. This signifies the fact that the banks needs to cover up their

loopholes in order to perform in a better way and lower their non-performing assets. Moreover,

11

this will help in increasing the overall productivity of the banks in a short span of time ensuring

financial stability of the banks.

The role of the asset restructuring companies (ARCs) can be considered as a key risk

drawing institutions and support the banks from suffering due to bad debts as these agencies

work sufficiently only keeping in focus the recovering of the loans. A powerful system is the

pillar in stimulating a country and encouraging it towards acquisition of investments as well as

reserves that will support the ill situation of the financial health of the financial institutions. At

the initial stage of the liberalization in 1991 followed by the financial reforms that took place due

to effective economic growth. It is been found that 90 % of the assets of the country is been

owned by the commercial banks and the foreign banks, tiny local banks in the rural areas of the

country possess less amount of market share in the banking system of the country. However, due

to deficit in properly managing the non-performing assets the problem is downgrading the

quality of the banks performance in the banking sector of India. The asset quality is not a big

issue before the era of globalization in India but after the liberalization or globalization took

place in the country the market entry and exist by overseas competitors became high and

consumers within the country prefer to become brand loyal to those foreign banks as they are

found to be more financially safe as compared to that of the domestic commercial banks. Before

1991 the asset quality was not linked with the key goals of the banks. However after

liberalization the banks is faced by the challenge in considering that how much value is being

added by their assets in the market based on which the banks is able to lend loans to the

borrowers and acquire deposits. The banks are now focused much more on the banking

environment from overall perspectives as well as the key factors like diversification, growth in

12

financial stability of the banks.

The role of the asset restructuring companies (ARCs) can be considered as a key risk

drawing institutions and support the banks from suffering due to bad debts as these agencies

work sufficiently only keeping in focus the recovering of the loans. A powerful system is the

pillar in stimulating a country and encouraging it towards acquisition of investments as well as

reserves that will support the ill situation of the financial health of the financial institutions. At

the initial stage of the liberalization in 1991 followed by the financial reforms that took place due

to effective economic growth. It is been found that 90 % of the assets of the country is been

owned by the commercial banks and the foreign banks, tiny local banks in the rural areas of the

country possess less amount of market share in the banking system of the country. However, due

to deficit in properly managing the non-performing assets the problem is downgrading the

quality of the banks performance in the banking sector of India. The asset quality is not a big

issue before the era of globalization in India but after the liberalization or globalization took

place in the country the market entry and exist by overseas competitors became high and

consumers within the country prefer to become brand loyal to those foreign banks as they are

found to be more financially safe as compared to that of the domestic commercial banks. Before

1991 the asset quality was not linked with the key goals of the banks. However after

liberalization the banks is faced by the challenge in considering that how much value is being

added by their assets in the market based on which the banks is able to lend loans to the

borrowers and acquire deposits. The banks are now focused much more on the banking

environment from overall perspectives as well as the key factors like diversification, growth in

12

the rural segments, creation of job opportunities and boosting the level of employment within the

country, etc. Banks are found to become less careful regarding giving out loans to public rather

they focuses more upon acquisition of deposits. However this leads to the occurrence of poor

financial performance as the banks has less amount of focus in snatching out value from the bad

loans and recovering the non-performing assets.

Research Questions:

1. What are the classification of the banking sector in India?

2. What is the impact of non-performing assets upon the commercial banks performance of

India?

3. How the bad loans can be recovered in case of the commercial; banks of India?

Chapter 2: Literature Review

The banking industry in any country is composed of the cash and credit segments that

they renders to the individual entities or large organization in order to support them to achieve

economic stability and ensure quantitative as well as qualitative change. The quantitative change

is accomplished based on the ability of the individuals or big organizations to ensure economic

growth whereas the aspect of qualitative change is an outcome of development through the

process of continuous and sustainable growth. Both of these is achieved if and only if the

organization or individual entities is able to consider the macroeconomic factors that are

impacting them significantly and to improvise their performance based on the restraints that are

imposed the external or macroeconomic factors as well as the internal or the microeconomic

13

country, etc. Banks are found to become less careful regarding giving out loans to public rather

they focuses more upon acquisition of deposits. However this leads to the occurrence of poor

financial performance as the banks has less amount of focus in snatching out value from the bad

loans and recovering the non-performing assets.

Research Questions:

1. What are the classification of the banking sector in India?

2. What is the impact of non-performing assets upon the commercial banks performance of

India?

3. How the bad loans can be recovered in case of the commercial; banks of India?

Chapter 2: Literature Review

The banking industry in any country is composed of the cash and credit segments that

they renders to the individual entities or large organization in order to support them to achieve

economic stability and ensure quantitative as well as qualitative change. The quantitative change

is accomplished based on the ability of the individuals or big organizations to ensure economic

growth whereas the aspect of qualitative change is an outcome of development through the

process of continuous and sustainable growth. Both of these is achieved if and only if the

organization or individual entities is able to consider the macroeconomic factors that are

impacting them significantly and to improvise their performance based on the restraints that are

imposed the external or macroeconomic factors as well as the internal or the microeconomic

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

factors. Thus the literature review is an endeavour to delve into these aspects based on the

previous analysis that are being theoretically or empirically rendered by different researchers. It

is shown as follows:

According to Anand, (2018) the institutional bodies that accepts deposits and provides

loans are the risk taker within any country. In India the apex banking institution is Reserve Bank

of India (RBI) that determines the monetary policy and sets them for the economy so that not

only the banking sector within the country but also the entities whether individual or

multinational is able to perform better with the support of the banks. In order to regulate the

banks effectively it is important that the banks should be able to recover the bad loans from the

borrowers in a financially sustainable manner. The micro foundation behind the macro economic

factors that hinders this borrowers to repay back their loans is the inability to counter the

challenge that is being led poverty as well as inequality within the country. It is a common

known fact that the country of India is in its transition phase from a less develop country towards

a advance developing country. The human development index and the other indices reveals the

fact that the country is able to boost their population though it lacks in raising their per capita

income. The country goes with its common loophole of considering that growth is an effective

parametric factor in determining its continuous progress overtime. However, the financial

stability of india which is correcting a developing country lies in its ability to bring qualitative

change from all respect. Monotonic decease in the growth rate of India can temporarily hamper

ist gross domestic product as well as the national income. However, in the long run it is

important to understand that the strength of an economy is not determined by the inclusive

growth within the economy only but by the economic development it is able to brought forward

14

previous analysis that are being theoretically or empirically rendered by different researchers. It

is shown as follows:

According to Anand, (2018) the institutional bodies that accepts deposits and provides

loans are the risk taker within any country. In India the apex banking institution is Reserve Bank

of India (RBI) that determines the monetary policy and sets them for the economy so that not

only the banking sector within the country but also the entities whether individual or

multinational is able to perform better with the support of the banks. In order to regulate the

banks effectively it is important that the banks should be able to recover the bad loans from the

borrowers in a financially sustainable manner. The micro foundation behind the macro economic

factors that hinders this borrowers to repay back their loans is the inability to counter the

challenge that is being led poverty as well as inequality within the country. It is a common

known fact that the country of India is in its transition phase from a less develop country towards

a advance developing country. The human development index and the other indices reveals the

fact that the country is able to boost their population though it lacks in raising their per capita

income. The country goes with its common loophole of considering that growth is an effective

parametric factor in determining its continuous progress overtime. However, the financial

stability of india which is correcting a developing country lies in its ability to bring qualitative

change from all respect. Monotonic decease in the growth rate of India can temporarily hamper

ist gross domestic product as well as the national income. However, in the long run it is

important to understand that the strength of an economy is not determined by the inclusive

growth within the economy only but by the economic development it is able to brought forward

14

overtime. If the trend analysis reveals that the economy of the country is deteriorating but the

development of the country is able to drive it towards sustainability then that kind of economic

conditions should be highly appreciated. This requires the ability of the country’s major financial

institution to take the risks of supporting reducing poverty as well as inequality by ensuring

sustainable development. The paper highlighted the fact in order to boost the macroeconomic

factors that impacts the banking sector of the country the microeconomic factors should be taken

care of. The price of goods and services that are being deployed within the country for

production, consumption, distribution and exchange purpose should be manipulated not at low

rates or high rates but at a balanced rate that will not hamper the economic equilibrium of the

domestic market place. The trade balance or the balance of payment of the country should not be

accompanied by trade deficits through high import and low export rather domestic production

should be supported by the bank loans which would be recovered after the production level is

followed as well as marketed and bought. This will ensure acquisition of foreign reserves for thr

country as well as will help the banking sector to bring economic development.

In accordance with Abidi & Joshi, (2017) there is importance to understand the role of

the banking sector in a country’s economy especially for India. This will only takes place if the

banking sector of the country prefer to perform based on maintaining the macroeconomic

balance within the country and ensuring that they are able to bring infrastructural development in

the country. The country should redesign their monetary and fiscal policies based on the

condition of their economy. Over 60 % of the country’s population is dependent upon the

agrarian society that persists within India. However, it was in an effective desire to transform to

an industry based economic structure. This requires availability of huge funds for boosting the

15

development of the country is able to drive it towards sustainability then that kind of economic

conditions should be highly appreciated. This requires the ability of the country’s major financial

institution to take the risks of supporting reducing poverty as well as inequality by ensuring

sustainable development. The paper highlighted the fact in order to boost the macroeconomic

factors that impacts the banking sector of the country the microeconomic factors should be taken

care of. The price of goods and services that are being deployed within the country for

production, consumption, distribution and exchange purpose should be manipulated not at low

rates or high rates but at a balanced rate that will not hamper the economic equilibrium of the

domestic market place. The trade balance or the balance of payment of the country should not be

accompanied by trade deficits through high import and low export rather domestic production

should be supported by the bank loans which would be recovered after the production level is

followed as well as marketed and bought. This will ensure acquisition of foreign reserves for thr

country as well as will help the banking sector to bring economic development.

In accordance with Abidi & Joshi, (2017) there is importance to understand the role of

the banking sector in a country’s economy especially for India. This will only takes place if the

banking sector of the country prefer to perform based on maintaining the macroeconomic

balance within the country and ensuring that they are able to bring infrastructural development in

the country. The country should redesign their monetary and fiscal policies based on the

condition of their economy. Over 60 % of the country’s population is dependent upon the

agrarian society that persists within India. However, it was in an effective desire to transform to

an industry based economic structure. This requires availability of huge funds for boosting the

15

machinery intensive sectors and siphoning off labour from the agricultural segment to the

industrial segments. The country did the same but missed the focus upon the agricultural sector

and for this they lost skilled labour force in the agricultural sector now a days. Moreover, the

labour force that are being siphoned off in the industrial sector are not trained to be sufficiently

skilled and educated. This led to the lowering of the potential productivity of the country in the

agrarian sector and at the cost of that they are not able to raise the efficiency of the labour force

in the industrial sector that are being siphoned off from the agricultural sector. People found to

migrate in order to earn faster but this was not found to get executed. The current scenario is

being found that major people of this labour force is not able to become successful in the

industrial sector and preferred to return back in their profession of agricultural activities. They

took the initiative to take loan from the banks and restart their agricultural endeavours but due to

imbalance in the economy is not able to recover their business as it was before and confronted

with suicides, exile, etc. activities. This created an economic mishap within the rural sector of the

economy. The bad loans are the outcome of the economic turmoil whose seed is been injected in

the economy decades before.

According to Bhaskaran et al. (2016) the banking sector of the country is a major

building block in absorbing the risk that is generated within the economy due to macroeconomic

parameters that affect the performance of the economy as a whole. The commercial bank are

monitored by the Banking Regulation Act, 1949 implemented to ensure economic effectiveness

that is helpful for the people of the country as well as the organizations that adds value to the

national income of the country. The primary role of this banks are to grant loans as well as

deposits for the corporates, government, general public and other economic entities of the

16

industrial segments. The country did the same but missed the focus upon the agricultural sector

and for this they lost skilled labour force in the agricultural sector now a days. Moreover, the

labour force that are being siphoned off in the industrial sector are not trained to be sufficiently

skilled and educated. This led to the lowering of the potential productivity of the country in the

agrarian sector and at the cost of that they are not able to raise the efficiency of the labour force

in the industrial sector that are being siphoned off from the agricultural sector. People found to

migrate in order to earn faster but this was not found to get executed. The current scenario is

being found that major people of this labour force is not able to become successful in the

industrial sector and preferred to return back in their profession of agricultural activities. They

took the initiative to take loan from the banks and restart their agricultural endeavours but due to

imbalance in the economy is not able to recover their business as it was before and confronted

with suicides, exile, etc. activities. This created an economic mishap within the rural sector of the

economy. The bad loans are the outcome of the economic turmoil whose seed is been injected in

the economy decades before.

According to Bhaskaran et al. (2016) the banking sector of the country is a major

building block in absorbing the risk that is generated within the economy due to macroeconomic

parameters that affect the performance of the economy as a whole. The commercial bank are

monitored by the Banking Regulation Act, 1949 implemented to ensure economic effectiveness

that is helpful for the people of the country as well as the organizations that adds value to the

national income of the country. The primary role of this banks are to grant loans as well as

deposits for the corporates, government, general public and other economic entities of the

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

country. The public sector banks are held by the government whereas the private sector banks

have major stakes or equity by the private shareholders. Moreover, the foreign banks are also

effective operating within the country that fulfils their commercial purpose though headquartered

in a foreign country. HSBC, Citi Bank, Standard Chartered, etc. are the leading foreign banks in

India. The rural regional banks as also the scheduled commercial banks that works to meet the

objective of assisting the weaker sections of the economy specifically agricultural labourer, small

and medium size enterprises as well as the marginal labourers. These banks their branches

majorly in the rural areas of the country though possess their head offices in the urban areas of

the country. The major functions of this banks are consist of providing banking financial services

to the semi-urban and rural areas of the country followed by encouraging the government

activities like MNREGA, distribution of pensions, etc. as well as initiating para-banking

facilities like financial services through debit cards, credit cards as well as locker facilities. The

other classification of the commercial banks comprises of the small financing banks that created

a niche market with the sole objective of rendering financial inclusion to those sections of the

society that are not being served by other banks. These comprises majorly of the micro industries

of the unorganized sector. Finally the cooperative banks are the other segment of the banking

sector that is covered under the Cooperative societies Act, 1912 and they are ran by the

managing committees. This works in accordance with the purpose of boosting the economic

framework of the country as a non-profit organization and serve the small businesses,

entrepreneurs, industries for empowering them and generating self-employment facilities as well

as new opportunities that have the ability to capitalize them into better economic infrastructure.

The banks works also to boost the segments of the economy that facilitates initiatives like

17

have major stakes or equity by the private shareholders. Moreover, the foreign banks are also

effective operating within the country that fulfils their commercial purpose though headquartered

in a foreign country. HSBC, Citi Bank, Standard Chartered, etc. are the leading foreign banks in

India. The rural regional banks as also the scheduled commercial banks that works to meet the

objective of assisting the weaker sections of the economy specifically agricultural labourer, small

and medium size enterprises as well as the marginal labourers. These banks their branches

majorly in the rural areas of the country though possess their head offices in the urban areas of

the country. The major functions of this banks are consist of providing banking financial services

to the semi-urban and rural areas of the country followed by encouraging the government

activities like MNREGA, distribution of pensions, etc. as well as initiating para-banking

facilities like financial services through debit cards, credit cards as well as locker facilities. The

other classification of the commercial banks comprises of the small financing banks that created

a niche market with the sole objective of rendering financial inclusion to those sections of the

society that are not being served by other banks. These comprises majorly of the micro industries

of the unorganized sector. Finally the cooperative banks are the other segment of the banking

sector that is covered under the Cooperative societies Act, 1912 and they are ran by the

managing committees. This works in accordance with the purpose of boosting the economic

framework of the country as a non-profit organization and serve the small businesses,

entrepreneurs, industries for empowering them and generating self-employment facilities as well

as new opportunities that have the ability to capitalize them into better economic infrastructure.

The banks works also to boost the segments of the economy that facilitates initiatives like

17

hatcheries, livestock as well as farming activities. The other banking model that is newly

incorporated in the country’s banking industry is the payment banks. It was being conceptualized

by the RBI in order to allow restricted deposits where the limit is currently set into 1 lakh for

each and every customers. Services like mobile banking, net banking, debit and ATM card, etc.

are the major financial instruments that are provided by these banks. The paper highlighted the

classification and the importance of the banking industry as well as the gap that is being created

in disguise of then economic fluctuations due to improper fund management initiatives.

Summary of Literature

The NPAs are rising in the economy of India due to inability of the banking sector of the

country to effectively supervise the funds that are being provided as loans to the potential

borrowers and not estimating their ability or provisions available to them for repaying the loans.

Effective risk management initiatives should be undertaken for empowering them as only

providence of funds by the financial institutions is not able to effectively make the non-

performing assets, performing assets. Rather it is required that the general public or the

corporates that are taking loans are providing transparent information regarding their financial

transaction and is able to keep transparency about the accounting information. In case of the rural

sectors where there is presence of both the organized as well as unorganized sector it is important

that the banks should not only focus on providing funds to the individuals or multinationals

rather will focus more in their ability to return the funds back. Moreover, they should proper

alternative plans for the borrowers. It was being highlighted in the paper that the banks should

not only remain keeping in focus that whether the capital support that they are rendering to the

18

incorporated in the country’s banking industry is the payment banks. It was being conceptualized

by the RBI in order to allow restricted deposits where the limit is currently set into 1 lakh for

each and every customers. Services like mobile banking, net banking, debit and ATM card, etc.

are the major financial instruments that are provided by these banks. The paper highlighted the

classification and the importance of the banking industry as well as the gap that is being created

in disguise of then economic fluctuations due to improper fund management initiatives.

Summary of Literature

The NPAs are rising in the economy of India due to inability of the banking sector of the

country to effectively supervise the funds that are being provided as loans to the potential

borrowers and not estimating their ability or provisions available to them for repaying the loans.

Effective risk management initiatives should be undertaken for empowering them as only

providence of funds by the financial institutions is not able to effectively make the non-

performing assets, performing assets. Rather it is required that the general public or the

corporates that are taking loans are providing transparent information regarding their financial

transaction and is able to keep transparency about the accounting information. In case of the rural

sectors where there is presence of both the organized as well as unorganized sector it is important

that the banks should not only focus on providing funds to the individuals or multinationals

rather will focus more in their ability to return the funds back. Moreover, they should proper

alternative plans for the borrowers. It was being highlighted in the paper that the banks should

not only remain keeping in focus that whether the capital support that they are rendering to the

18

stakeholders but also should keep a keen focus in helping them empowering the stakeholders

rather than maximizing their own profit only if they really wants to strengthen the country’s

banking system as well as bring forwards sustainable economic framework for economic

development which will only get possible if there exist a retardation in the rate of increase of the

NPAs.

The objective of the banks should not only be to diversify the banking structure and

utilizing the notion of division of labour and segmenting banking units that are specialized in

different activities followed by ensuring economic development but also should focus in

maximizing the asset utilization of them that they have loaned to other economic entities that

adds value to the national income of the country. The various kind of risks that are practically

handled through a pragmatic approach of planning, arranging, leading and controlling through

risk management techniques that traces all the daily as well as the last performance of the

organization. The major aspect of concern is also been related with the credit risk involved in

case of the banks. The crucial hitch is concerned with the disability of the clients to pay back the

credit that they have taken from the bank and other private sector financial institutions. As long

as the banks are focusing upon mitigating the default issue from the beginning of the credits that

are given out, it can be said that the banks have already lessen out the possibility of the defaults.

It India non-performing assets are always remained an issue of concern due to the reason that the

banks have taken less consideration in case of helping the consumers payback the same within

stipulated time frame. Along with that the banks are found to focus much more in providing

credit and credit opportunities though they lack in focusing upon monitoring the credits and

hence the risk involved in the process is found to become cumbersome when they tries to handle

19

rather than maximizing their own profit only if they really wants to strengthen the country’s

banking system as well as bring forwards sustainable economic framework for economic

development which will only get possible if there exist a retardation in the rate of increase of the

NPAs.

The objective of the banks should not only be to diversify the banking structure and

utilizing the notion of division of labour and segmenting banking units that are specialized in

different activities followed by ensuring economic development but also should focus in

maximizing the asset utilization of them that they have loaned to other economic entities that

adds value to the national income of the country. The various kind of risks that are practically

handled through a pragmatic approach of planning, arranging, leading and controlling through

risk management techniques that traces all the daily as well as the last performance of the

organization. The major aspect of concern is also been related with the credit risk involved in

case of the banks. The crucial hitch is concerned with the disability of the clients to pay back the

credit that they have taken from the bank and other private sector financial institutions. As long

as the banks are focusing upon mitigating the default issue from the beginning of the credits that

are given out, it can be said that the banks have already lessen out the possibility of the defaults.

It India non-performing assets are always remained an issue of concern due to the reason that the

banks have taken less consideration in case of helping the consumers payback the same within

stipulated time frame. Along with that the banks are found to focus much more in providing

credit and credit opportunities though they lack in focusing upon monitoring the credits and

hence the risk involved in the process is found to become cumbersome when they tries to handle

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

them at the end when already the clients become defaulter of the loans that they have taken from

the banks. The management procedure in the banks have accelerated the recovery periods and

hence the effect of the defaulting issue have affected the economy as a whole also. The issue of

this recovery is not related with the small borrowers of the loan but due to the non-stringent

strategies that are applied by the banks to recover the loans from the big borrowers. Since the big

borrowers take huge amount of loans hence this impact upon the liquidity of the banks that

affects its overall financial performance in the long run if remained unrecovered. Due to this

reason it is been found that the Reserve Bank of India (RBI) is rendering keen focus upon

assisting the banks on this issue for escaping the defaulting risk with the implementation of

effective strategic endeavours.

Methodology

The years from 2014 to 2017 is being taken under consideration based on the information

that are available from the banks in order to interpret the correlation within private sector banks

and the open division banks.

Sample Population: Information that are identified with transfer of awful credits for open and

private division banks are being utilized as the population sample in the study.

Research Approach: The approach of the research is considered to be descriptive as it will help

in understanding the characteristics of the population as well as delve into the phenomenon taken

under consideration. It is where a causal relationship is not considered rather how one variable is

been affected by the other is taken under focus.

20

the banks. The management procedure in the banks have accelerated the recovery periods and

hence the effect of the defaulting issue have affected the economy as a whole also. The issue of

this recovery is not related with the small borrowers of the loan but due to the non-stringent

strategies that are applied by the banks to recover the loans from the big borrowers. Since the big

borrowers take huge amount of loans hence this impact upon the liquidity of the banks that

affects its overall financial performance in the long run if remained unrecovered. Due to this

reason it is been found that the Reserve Bank of India (RBI) is rendering keen focus upon

assisting the banks on this issue for escaping the defaulting risk with the implementation of

effective strategic endeavours.

Methodology

The years from 2014 to 2017 is being taken under consideration based on the information

that are available from the banks in order to interpret the correlation within private sector banks

and the open division banks.

Sample Population: Information that are identified with transfer of awful credits for open and

private division banks are being utilized as the population sample in the study.

Research Approach: The approach of the research is considered to be descriptive as it will help

in understanding the characteristics of the population as well as delve into the phenomenon taken

under consideration. It is where a causal relationship is not considered rather how one variable is

been affected by the other is taken under focus.

20

Information gathering: Supplementary information is been acquired from the source of RBI

followed by utilizing the survey results and I formation that are incorporated by them.

Age & day: thee correlation is being executed taking under consideration that the information

that are available in the past years of the trend analysis. Moreover, the problem is been studies

based on the analysis that is being reflected by the secondary data in the reference papers of the

Reserve bank of India along with the directions, instructions as well as the policies that are taken

under consideration by the banks. Also the texts, editorials and various research thesis are being

utilized too taking from IIB, Indian Banking Association (IBA), seminar events, etc. in order to

ensure that the information that this research will project upon should be an effective analysis

that possess higher credibility and transparency followed by revealing the existing situation that

is being prevalent in the commercial banking industry of India.

Research Type

Descriptive research approach is being implemented in order to ensure that the study is

done extensively taking under consideration all the related incidents in the management of the

bank’s credit risk and the aspects of bad loans. The yearly reports of the RBI journals and the

progress of banking in India reports from the year 2005 to 2015 are being utilized as the

secondary source of data. The relevant statistical tables are linked with the banks followed by the

writings and information that are being acquired from the magazines, webpages, books, papers,

etc. that have worked upon the banks performance of India and provided substantial documents

related to it.

21

followed by utilizing the survey results and I formation that are incorporated by them.

Age & day: thee correlation is being executed taking under consideration that the information

that are available in the past years of the trend analysis. Moreover, the problem is been studies

based on the analysis that is being reflected by the secondary data in the reference papers of the

Reserve bank of India along with the directions, instructions as well as the policies that are taken

under consideration by the banks. Also the texts, editorials and various research thesis are being

utilized too taking from IIB, Indian Banking Association (IBA), seminar events, etc. in order to

ensure that the information that this research will project upon should be an effective analysis

that possess higher credibility and transparency followed by revealing the existing situation that

is being prevalent in the commercial banking industry of India.

Research Type

Descriptive research approach is being implemented in order to ensure that the study is

done extensively taking under consideration all the related incidents in the management of the

bank’s credit risk and the aspects of bad loans. The yearly reports of the RBI journals and the

progress of banking in India reports from the year 2005 to 2015 are being utilized as the

secondary source of data. The relevant statistical tables are linked with the banks followed by the

writings and information that are being acquired from the magazines, webpages, books, papers,

etc. that have worked upon the banks performance of India and provided substantial documents

related to it.

21

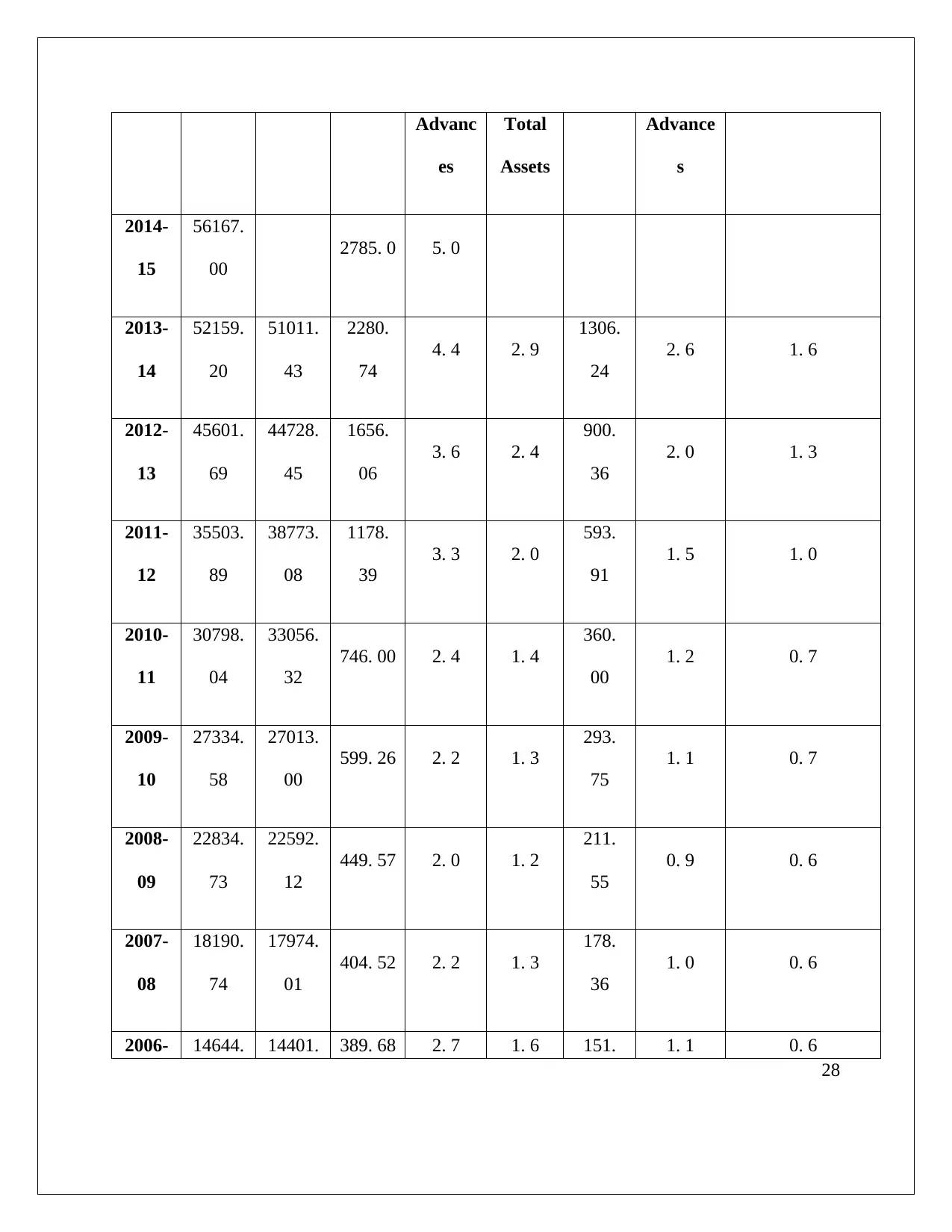

Data Analysis Tools

The data that are taken under consideration are transferred into tabular format to visualize

the numerical values involved along with computing the calculations that will reveal significant

information related to the credit risk management and aspect of bad loans in case of the

commercial banks of the Indian banking industry. The process is done for incorporating the

finding through the analysis of the trends, ratio analysis, the net and gross bad loans involved,

etc. The aggregate sum of the doubtful loans, lost assets, sub-standard assets as well as the loss

of interest that are to be paid upon them, etc. all together comprises of the gross bad loans. The

rate to that of the gross credit assets of the bank are taken under consideration in the process of

examining the assets that created the bad loans for the banks. When the arrangements are left

aside from that of the aggregate o the real bad assets then it gives the Net bad loans. However, to

get an exact clarification regarding the net bad loans, the proportion of the net bad loans to that

of the net advances is been taken under consideration. The actual figure renders information

regarding the situation of the bad loans in the past in case of the commercial banking industry of

India that can be shown as follows:

Scheduled Commercial Banks

Year

(March-

End)

Advances Non-Performing Assets

Gross Net Gross Net

Amou

As

Percenta

As

Percent

Amou

nt

As

Percent

As Percentage of

Total Assets

22

The data that are taken under consideration are transferred into tabular format to visualize

the numerical values involved along with computing the calculations that will reveal significant

information related to the credit risk management and aspect of bad loans in case of the

commercial banks of the Indian banking industry. The process is done for incorporating the