PGDAF Auditing and Assurance: Narrative Report on Everbright Group

VerifiedAdded on 2022/10/04

|11

|2861

|17

Report

AI Summary

This report provides an in-depth analysis of an audit process, focusing on the audit of Everbright Group. It explores the auditor's role in examining financial statements, assessing financial ratios to identify potential misstatements, and evaluating risks inherent in the business. The report delves into the significance of inherent and control risks, detailing the accounting system and internal control systems employed by the company. It highlights the importance of various financial ratios, such as liquidity, profitability, and efficiency ratios, in evaluating the company's performance. The report also outlines how auditors respond to identified risks through various procedures, including tests of control and substantive testing. Furthermore, the report discusses the accounting systems, including payroll, fixed asset, general ledger, and computerized accounting systems, and the importance of a robust internal control system in mitigating business risks. The conclusion summarizes the key aspects of the auditing process, emphasizing the auditor's responsibility in identifying and addressing potential fraud and misstatements. The assignment is based on a case study of Everbright Group, a company operating restaurants and food outlets in Region M, and follows the guidelines of the PGDAF (Macau Program) Auditing and Assurance course.

Running head: NARRATIVE REPORTING

AUDITING

Name of the Student

Name of the University

Author Note

NARRATIVE REPORTING

AUDITING

Name of the Student

Name of the University

Author Note

NARRATIVE REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1NARRATIVE REPORTING

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................3

Financial Ratio of Company......................................................................................................3

Risk in the business....................................................................................................................3

Inherent Risk..........................................................................................................................3

Response to above mentioned risk.............................................................................................4

Accounting System in Company................................................................................................4

Internal Control System in Company.........................................................................................5

Conclusion..................................................................................................................................6

Reference....................................................................................................................................7

Appendix 1.................................................................................................................................8

NARRATIVE REPORTING

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................3

Financial Ratio of Company......................................................................................................3

Risk in the business....................................................................................................................3

Inherent Risk..........................................................................................................................3

Response to above mentioned risk.............................................................................................4

Accounting System in Company................................................................................................4

Internal Control System in Company.........................................................................................5

Conclusion..................................................................................................................................6

Reference....................................................................................................................................7

Appendix 1.................................................................................................................................8

NARRATIVE REPORTING

2NARRATIVE REPORTING

Executive Summary

The report is based upon the audit process as it show how the company is able to get audited

its financial statement, it show how the auditor is able to inspect and examine the financial

statement of the company so that it can able to give proper opinion about the company

financial statement. The report show how the auditor able to ascertain material misstatement

in company with the help of financial ratio of the company, the report all show how the

auditor is able to ascertain the risk which is associated in the company financial statement. It

also show the procedure which the company have to follow in regards of financial statement

of the company. The last part of the report shows about the new accounting system which the

company is able to utilize in their business activities and also show the meaning of the

internal control in the business.

NARRATIVE REPORTING

Executive Summary

The report is based upon the audit process as it show how the company is able to get audited

its financial statement, it show how the auditor is able to inspect and examine the financial

statement of the company so that it can able to give proper opinion about the company

financial statement. The report show how the auditor able to ascertain material misstatement

in company with the help of financial ratio of the company, the report all show how the

auditor is able to ascertain the risk which is associated in the company financial statement. It

also show the procedure which the company have to follow in regards of financial statement

of the company. The last part of the report shows about the new accounting system which the

company is able to utilize in their business activities and also show the meaning of the

internal control in the business.

NARRATIVE REPORTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3NARRATIVE REPORTING

Introduction

Auditing help the company to gain proper information about the company financial

statement to the user of the company. Auditor is able to inspect and examination the company

financial statement so that it can know about the company financial performance and how the

company is able to maintain the financial aspects in the company (Alzeban and Gwilliam

2014). It should able to carry many procedures which help them to gain the value in the

company financial statement. Auditor have to gain many audit evidence which help it to gain

proper amount of knowledge about the company business activities. The auditor have to

access the internal control system so that it can know about each company problem more

easily as all the main problem always remain in the internal control (Chen et al., 2014). The

company having lack of management is also have less amount of control internally so this led

to increase in overall risk in the company financial system. It should also take into

consideration all the aspects in the company business activities so that the company is able to

have proper amount of activities in regards of financial statement of the company. The report

show about the company audit process so this will help the user to gain proper amount of

information and also show different company ratio in the business. It also show about the

company risk matter in the business as well as how the company is able to manage its

business operation in the company.

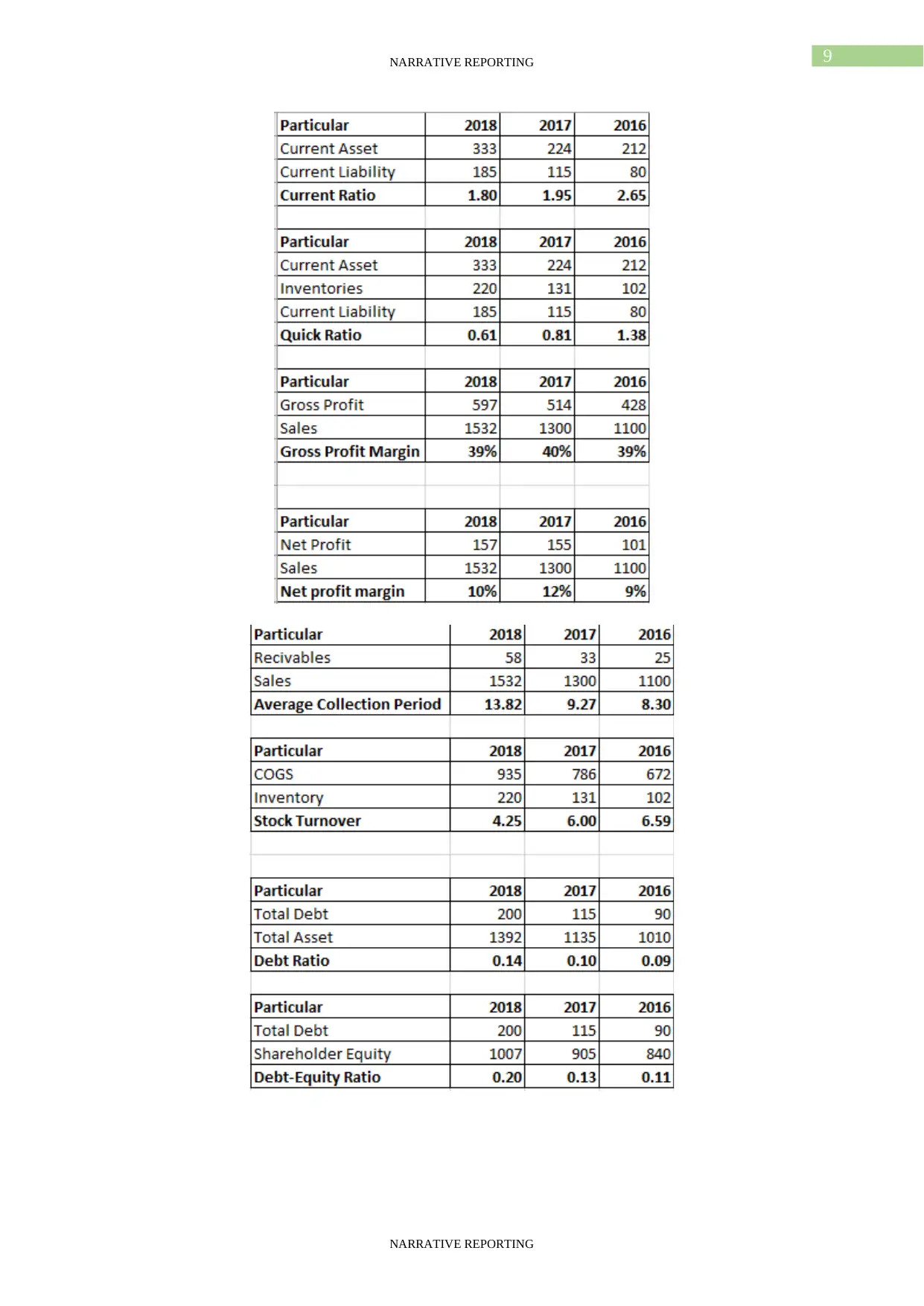

Financial Ratio of Company

These ratios show about the company performance as it takes into consideration about

the different aspects of company financial position. It takes into consideration the liquidity

aspects, profitability, efficiency and leverage ratio. All the ratio is able to show about the

company different aspects of the company and how the company is able to carry all the

operation easily and effectively in the business.

Risk in the business

Each business is able to have to proper amount of risk in the business as this help the

company to manage its business operation more easily and effectively in the business. the

auditor have to check many activities so that it can access have proper strategies in regards of

risk of the company (De Simone, Ege and Stomberg 2014). There are two types of risk in the

company financial statement, which are inherent risk and control risk in the company.

Inherent Risk

This are the risk which are associated with company financial statement as this are the

risk which happen in the company due to error and omission in the business (DeFond and

Zhang 2014). This risk happens due to some proper error or omission of the company

financial information so this should be taken into consideration by the auditor in the company

financial statement.

The Inherent Risk involved in company financial statement are:

As the company is having less amount in liquidity ratio so it signifies that the

company is having an error in company financial statement so due to that there can be mis-

statement in company current asset so that this can help the company to reduce the liquidity

ratio of the company. As due to these company is having a bad ratio as it can keep on

reducing from 2016 to 2018 it keep reducing in company financial statement so it is found

that the company is having some inherent risk in their liquid ratio (DeFond and Lennox

2017). The auditor should able to analysis the internal control system so that it can able to

NARRATIVE REPORTING

Introduction

Auditing help the company to gain proper information about the company financial

statement to the user of the company. Auditor is able to inspect and examination the company

financial statement so that it can know about the company financial performance and how the

company is able to maintain the financial aspects in the company (Alzeban and Gwilliam

2014). It should able to carry many procedures which help them to gain the value in the

company financial statement. Auditor have to gain many audit evidence which help it to gain

proper amount of knowledge about the company business activities. The auditor have to

access the internal control system so that it can know about each company problem more

easily as all the main problem always remain in the internal control (Chen et al., 2014). The

company having lack of management is also have less amount of control internally so this led

to increase in overall risk in the company financial system. It should also take into

consideration all the aspects in the company business activities so that the company is able to

have proper amount of activities in regards of financial statement of the company. The report

show about the company audit process so this will help the user to gain proper amount of

information and also show different company ratio in the business. It also show about the

company risk matter in the business as well as how the company is able to manage its

business operation in the company.

Financial Ratio of Company

These ratios show about the company performance as it takes into consideration about

the different aspects of company financial position. It takes into consideration the liquidity

aspects, profitability, efficiency and leverage ratio. All the ratio is able to show about the

company different aspects of the company and how the company is able to carry all the

operation easily and effectively in the business.

Risk in the business

Each business is able to have to proper amount of risk in the business as this help the

company to manage its business operation more easily and effectively in the business. the

auditor have to check many activities so that it can access have proper strategies in regards of

risk of the company (De Simone, Ege and Stomberg 2014). There are two types of risk in the

company financial statement, which are inherent risk and control risk in the company.

Inherent Risk

This are the risk which are associated with company financial statement as this are the

risk which happen in the company due to error and omission in the business (DeFond and

Zhang 2014). This risk happens due to some proper error or omission of the company

financial information so this should be taken into consideration by the auditor in the company

financial statement.

The Inherent Risk involved in company financial statement are:

As the company is having less amount in liquidity ratio so it signifies that the

company is having an error in company financial statement so due to that there can be mis-

statement in company current asset so that this can help the company to reduce the liquidity

ratio of the company. As due to these company is having a bad ratio as it can keep on

reducing from 2016 to 2018 it keep reducing in company financial statement so it is found

that the company is having some inherent risk in their liquid ratio (DeFond and Lennox

2017). The auditor should able to analysis the internal control system so that it can able to

NARRATIVE REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4NARRATIVE REPORTING

have to proper assertion in company financial statement so this will help the auditor to gain

proper knowledge about the company business easily and effectively.

The company is having high amount of complexity in the company business so this

can able to give proper amount of material misstatement in company business, as the

company is having so much of complexity so this can able to have an increase in risk in the

company financial statement. So, the company sales can be mis-stated as due to these the

company is not having proper amount of profit in the company business (Furnham and

Gunter 2015). Auditor should able to have proper process in the company so that it can able

to judge the complexity of the business and able to carry its operation more easily and

effectively in the company. Auditor should able to analysis company transaction properly so

this will help the auditor to gain proper amount of work as well as it able to get more amount

of audit evidence in regards of company statement and the auditor will able to give proper

opinion about the company business.

Response to above mentioned risk

Auditor should able to carry different procedure so that it can able to analysis the

company financial system easily and effectively in the business, as it should able to carry all

the activities properly (Griffiths 2016). The procedure which the auditor is able to follow is

that, it have to get proper utilization of company information and also able to perform

substantive test as this will help the company to gain proper amount of return in the company

business. It should able to have proper amount of test of control in company business so that

the auditor is able to ascertain the amount of materiality which is there in company financial

statement.

Risk in the

Business

Account

Affected

Assertion Test of Control

Decrease in

Liquidity

Ratio

Current

Asset and

Current

Liability

Completeness – The

company should able to

record all the transaction in

the financial statement

Auditor should able to

analysis all the information

in books of accounts so that

it can know whether the

company have carried all the

transaction in financial

statement

Complexity

in Business

Sales

Account

Accuracy – The company

should record all the

transaction properly as their

so much complexity so

company should able to have

proper record of transaction

Auditor able to check that

the company is have proper

internal control and how it

able to manage the business

operation in the company.

Accounting System in Company

Each company should able to have proper accounting system as this will help the

company to carry its business operation more easily and effectively in the business, as the

company is able to meet all the criteria than only it able to reach the goal and objective in the

business (Groomer and Murthy 2018). The system which should be adopted in the company

are:

Payroll System – This is the system which the company can adopt to make proper entry in

company system, as this system involve all the detailed of company transaction from the

NARRATIVE REPORTING

have to proper assertion in company financial statement so this will help the auditor to gain

proper knowledge about the company business easily and effectively.

The company is having high amount of complexity in the company business so this

can able to give proper amount of material misstatement in company business, as the

company is having so much of complexity so this can able to have an increase in risk in the

company financial statement. So, the company sales can be mis-stated as due to these the

company is not having proper amount of profit in the company business (Furnham and

Gunter 2015). Auditor should able to have proper process in the company so that it can able

to judge the complexity of the business and able to carry its operation more easily and

effectively in the company. Auditor should able to analysis company transaction properly so

this will help the auditor to gain proper amount of work as well as it able to get more amount

of audit evidence in regards of company statement and the auditor will able to give proper

opinion about the company business.

Response to above mentioned risk

Auditor should able to carry different procedure so that it can able to analysis the

company financial system easily and effectively in the business, as it should able to carry all

the activities properly (Griffiths 2016). The procedure which the auditor is able to follow is

that, it have to get proper utilization of company information and also able to perform

substantive test as this will help the company to gain proper amount of return in the company

business. It should able to have proper amount of test of control in company business so that

the auditor is able to ascertain the amount of materiality which is there in company financial

statement.

Risk in the

Business

Account

Affected

Assertion Test of Control

Decrease in

Liquidity

Ratio

Current

Asset and

Current

Liability

Completeness – The

company should able to

record all the transaction in

the financial statement

Auditor should able to

analysis all the information

in books of accounts so that

it can know whether the

company have carried all the

transaction in financial

statement

Complexity

in Business

Sales

Account

Accuracy – The company

should record all the

transaction properly as their

so much complexity so

company should able to have

proper record of transaction

Auditor able to check that

the company is have proper

internal control and how it

able to manage the business

operation in the company.

Accounting System in Company

Each company should able to have proper accounting system as this will help the

company to carry its business operation more easily and effectively in the business, as the

company is able to meet all the criteria than only it able to reach the goal and objective in the

business (Groomer and Murthy 2018). The system which should be adopted in the company

are:

Payroll System – This is the system which the company can adopt to make proper entry in

company system, as this system involve all the detailed of company transaction from the

NARRATIVE REPORTING

5NARRATIVE REPORTING

payment to workers to filling the tax return in the company (Hall 2015). This help the

company to maintain proper information in regards of wages, hours and taxes in related to

company employee. This help the company to gain proper knowledge of each transaction so

that the company is able to maintain proper amount of business operation. The auditor is able

to gain proper amount of knowledge in regards of company financial statement so that it can

know the amount of risk which is associated with company financial statement in company

business operation (Vovchenko et al., 2017).

Fixed Asset System – This system help the company to record all the transaction properly

and effectively in company business system (Khlif and Samaha 2014). This system help the

company to record all the transaction in regards of its fixed asset so that the company is able

to know all the detail about the fixed asset in the company financial statement. Auditor is able

to meet all the requirement in the company as it able to gain proper information of the

company so this help the auditor to obtain proper evidence and the auditor is able to give

correct opinion upon the company financial statement.

General Ledger System – Each company should able to have proper amount of transaction

so that it can able to have proper amount of information in the company financial statement,

as this help the company (Knechel and Salterio 2016). Auditor is able to meet all the criteria

in the company and able to check the account easily which so that this will help the company

to provide all the detailed information about the financial statement of the company.

Computerised Accounting System – This are the system which able to carry its business

operation with the help of the computerised accounting system as this will help the company

to record the transaction more easily in the business as this help the company to gain an

advantage in the business (Lisic et al., 2016). Auditor is able to check all the transaction

properly and effectively in the business, it also able to conduct different process which help

the auditor to gain more audit evidence in the company business activities.

Internal Control System in Company

This is the system which every company should able to maintain in their business

structure so that the company can able to carry its business operation more easily and

effectively in the business (Newton et al., 2015). This system help the company to reach their

goals and objective more easily and effectively in the business, the company is able to carry

its operation more effectively so that it can manage the business risk in the company more

easily and effectively. This system help the company to observe, monitored the company

resources easily and effectively in the business. The company having proper amount of

internal control is able to have less amount of material effect in company business as well as

it help the company to gain proper control on the business risk which is associated in the

company business activity.

Auditor responsibility is to ascertain the internal control system of the company so

that the user is able to get proper detailed of company information in the business (Power and

Gendron 2015). It should be interpreted properly so that the company is able to have proper

valuation in respect of its financial statement. Internal control help the company to maintain

and reduce the overall business risk so if there is an weakness in overall company financial

activity.

Company should able to have proper amount of control so that it can able to meet up

the business risk easily as it should able to have proper lower management which will control

all the company transaction easily and effectively in company business (Sandvig et al., 2014).

NARRATIVE REPORTING

payment to workers to filling the tax return in the company (Hall 2015). This help the

company to maintain proper information in regards of wages, hours and taxes in related to

company employee. This help the company to gain proper knowledge of each transaction so

that the company is able to maintain proper amount of business operation. The auditor is able

to gain proper amount of knowledge in regards of company financial statement so that it can

know the amount of risk which is associated with company financial statement in company

business operation (Vovchenko et al., 2017).

Fixed Asset System – This system help the company to record all the transaction properly

and effectively in company business system (Khlif and Samaha 2014). This system help the

company to record all the transaction in regards of its fixed asset so that the company is able

to know all the detail about the fixed asset in the company financial statement. Auditor is able

to meet all the requirement in the company as it able to gain proper information of the

company so this help the auditor to obtain proper evidence and the auditor is able to give

correct opinion upon the company financial statement.

General Ledger System – Each company should able to have proper amount of transaction

so that it can able to have proper amount of information in the company financial statement,

as this help the company (Knechel and Salterio 2016). Auditor is able to meet all the criteria

in the company and able to check the account easily which so that this will help the company

to provide all the detailed information about the financial statement of the company.

Computerised Accounting System – This are the system which able to carry its business

operation with the help of the computerised accounting system as this will help the company

to record the transaction more easily in the business as this help the company to gain an

advantage in the business (Lisic et al., 2016). Auditor is able to check all the transaction

properly and effectively in the business, it also able to conduct different process which help

the auditor to gain more audit evidence in the company business activities.

Internal Control System in Company

This is the system which every company should able to maintain in their business

structure so that the company can able to carry its business operation more easily and

effectively in the business (Newton et al., 2015). This system help the company to reach their

goals and objective more easily and effectively in the business, the company is able to carry

its operation more effectively so that it can manage the business risk in the company more

easily and effectively. This system help the company to observe, monitored the company

resources easily and effectively in the business. The company having proper amount of

internal control is able to have less amount of material effect in company business as well as

it help the company to gain proper control on the business risk which is associated in the

company business activity.

Auditor responsibility is to ascertain the internal control system of the company so

that the user is able to get proper detailed of company information in the business (Power and

Gendron 2015). It should be interpreted properly so that the company is able to have proper

valuation in respect of its financial statement. Internal control help the company to maintain

and reduce the overall business risk so if there is an weakness in overall company financial

activity.

Company should able to have proper amount of control so that it can able to meet up

the business risk easily as it should able to have proper lower management which will control

all the company transaction easily and effectively in company business (Sandvig et al., 2014).

NARRATIVE REPORTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6NARRATIVE REPORTING

Conclusion

The report concludes about auditing process in the company. Auditor responsibility to

ascertain all the fraud and material mis-statement which is there in company financial books

of the company. It able to conclude about how the company is able to meet all the

requirement of audit and how the auditor is able to carry its process in the company financial

statement. The report conclude about the financial analysis which is done with the help of

financial ratio as this help the company to gain proper information about the overall

performance of company in last few years. It also shows the risk which is associated with the

company as this will help the user to know about the risk and how the company is able to

manage its business operation in company financial activity. It also concludes about the

process which the auditor will able to take in regards of the above risk and how the company

is able to get proper information in regards of company financial statement. Lastly it

concludes about the company internal control so this show that each company should able to

have proper amount internal control in the business and also how the company is able to meet

the requirement of internal control easily and effectively in the business.

NARRATIVE REPORTING

Conclusion

The report concludes about auditing process in the company. Auditor responsibility to

ascertain all the fraud and material mis-statement which is there in company financial books

of the company. It able to conclude about how the company is able to meet all the

requirement of audit and how the auditor is able to carry its process in the company financial

statement. The report conclude about the financial analysis which is done with the help of

financial ratio as this help the company to gain proper information about the overall

performance of company in last few years. It also shows the risk which is associated with the

company as this will help the user to know about the risk and how the company is able to

manage its business operation in company financial activity. It also concludes about the

process which the auditor will able to take in regards of the above risk and how the company

is able to get proper information in regards of company financial statement. Lastly it

concludes about the company internal control so this show that each company should able to

have proper amount internal control in the business and also how the company is able to meet

the requirement of internal control easily and effectively in the business.

NARRATIVE REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7NARRATIVE REPORTING

Reference

Alzeban, A. and Gwilliam, D., 2014. Factors affecting the internal audit effectiveness: A

survey of the Saudi public sector. Journal of International Accounting, Auditing and

Taxation, 23(2), pp.74-86.

Chen, Y., Smith, A.L., Cao, J. and Xia, W., 2014. Information technology capability, internal

control effectiveness, and audit fees and delays. Journal of Information Systems, 28(2),

pp.149-180.

De Simone, L., Ege, M.S. and Stomberg, B., 2014. Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), pp.1469-1496.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

DeFond, M.L. and Lennox, C.S., 2017. Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), pp.591-627.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Hall, J.A., 2015. Information technology auditing. Cengage Learning.

Khlif, H. and Samaha, K., 2014. Internal Control Quality, E gyptian Standards on Auditing

and External Audit Delays: Evidence from the E gyptian Stock Exchange. International

Journal of Auditing, 18(2), pp.139-154.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lisic, L.L., Neal, T.L., Zhang, I.X. and Zhang, Y., 2016. CEO power, internal control quality,

and audit committee effectiveness in substance versus in form. Contemporary Accounting

Research, 33(3), pp.1199-1237.

Newton, N.J., Persellin, J.S., Wang, D. and Wilkins, M.S., 2015. Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), pp.603-623.

Power, M.K. and Gendron, Y., 2015. Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), pp.147-165.

Sandvig, C., Hamilton, K., Karahalios, K. and Langbort, C., 2014. Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Vovchenko, N.G., Holina, M.G., Orobinskiy, A.S. and Sichev, R.A., 2017. Ensuring financial

stability of companies on the basis of international experience in construction of risks maps,

internal control and audit. European Research Studies Journal, 20(1), pp.350-368.

NARRATIVE REPORTING

Reference

Alzeban, A. and Gwilliam, D., 2014. Factors affecting the internal audit effectiveness: A

survey of the Saudi public sector. Journal of International Accounting, Auditing and

Taxation, 23(2), pp.74-86.

Chen, Y., Smith, A.L., Cao, J. and Xia, W., 2014. Information technology capability, internal

control effectiveness, and audit fees and delays. Journal of Information Systems, 28(2),

pp.149-180.

De Simone, L., Ege, M.S. and Stomberg, B., 2014. Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), pp.1469-1496.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

DeFond, M.L. and Lennox, C.S., 2017. Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), pp.591-627.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Hall, J.A., 2015. Information technology auditing. Cengage Learning.

Khlif, H. and Samaha, K., 2014. Internal Control Quality, E gyptian Standards on Auditing

and External Audit Delays: Evidence from the E gyptian Stock Exchange. International

Journal of Auditing, 18(2), pp.139-154.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lisic, L.L., Neal, T.L., Zhang, I.X. and Zhang, Y., 2016. CEO power, internal control quality,

and audit committee effectiveness in substance versus in form. Contemporary Accounting

Research, 33(3), pp.1199-1237.

Newton, N.J., Persellin, J.S., Wang, D. and Wilkins, M.S., 2015. Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), pp.603-623.

Power, M.K. and Gendron, Y., 2015. Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), pp.147-165.

Sandvig, C., Hamilton, K., Karahalios, K. and Langbort, C., 2014. Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Vovchenko, N.G., Holina, M.G., Orobinskiy, A.S. and Sichev, R.A., 2017. Ensuring financial

stability of companies on the basis of international experience in construction of risks maps,

internal control and audit. European Research Studies Journal, 20(1), pp.350-368.

NARRATIVE REPORTING

8NARRATIVE REPORTING

Appendix 1

Total Word – 2000 words

NARRATIVE REPORTING

Appendix 1

Total Word – 2000 words

NARRATIVE REPORTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9NARRATIVE REPORTING

NARRATIVE REPORTING

NARRATIVE REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10NARRATIVE REPORTING

NARRATIVE REPORTING

NARRATIVE REPORTING

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.