Taxation Theory, Practice & Law: Capital Gains Tax & FBT Analysis T2

VerifiedAdded on 2023/06/14

|9

|1314

|227

Report

AI Summary

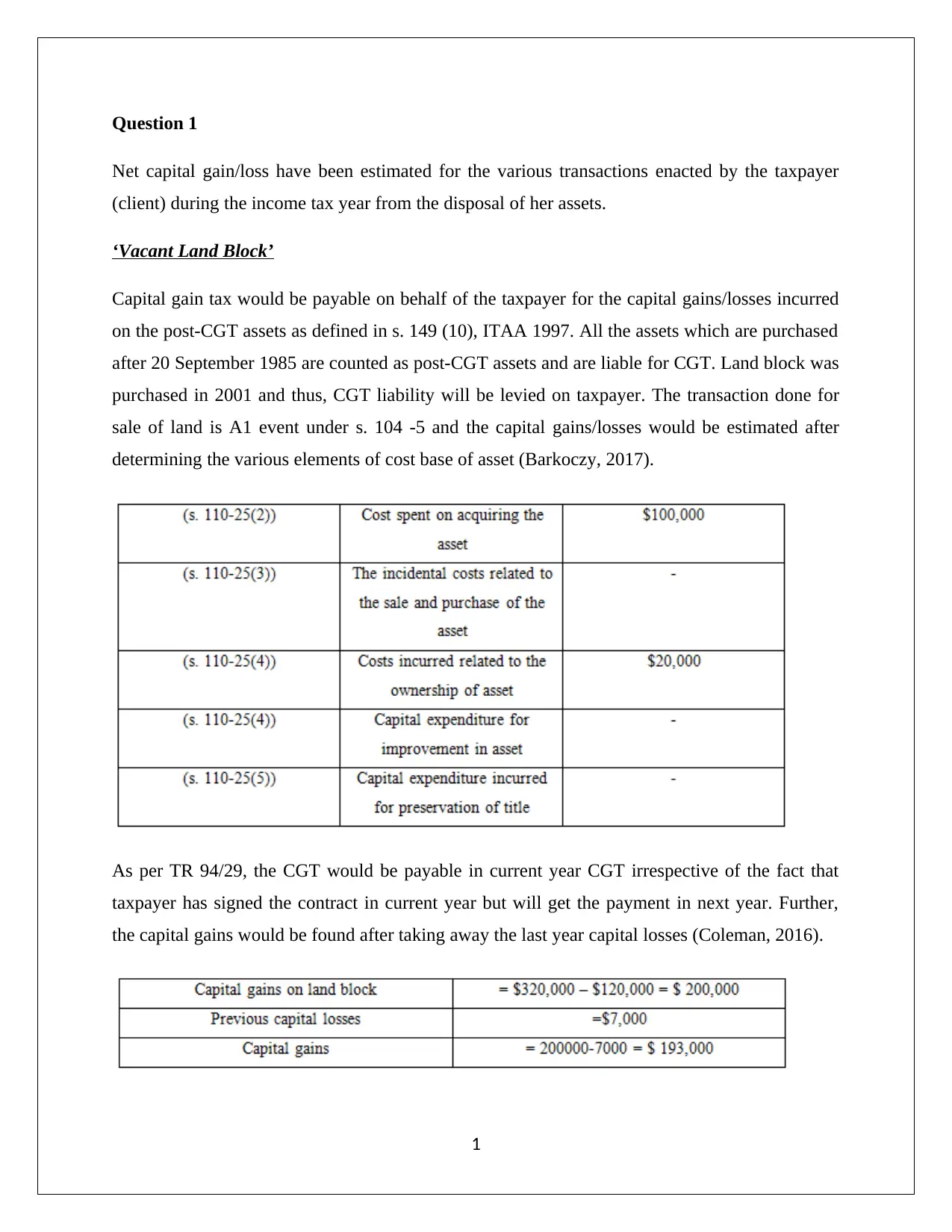

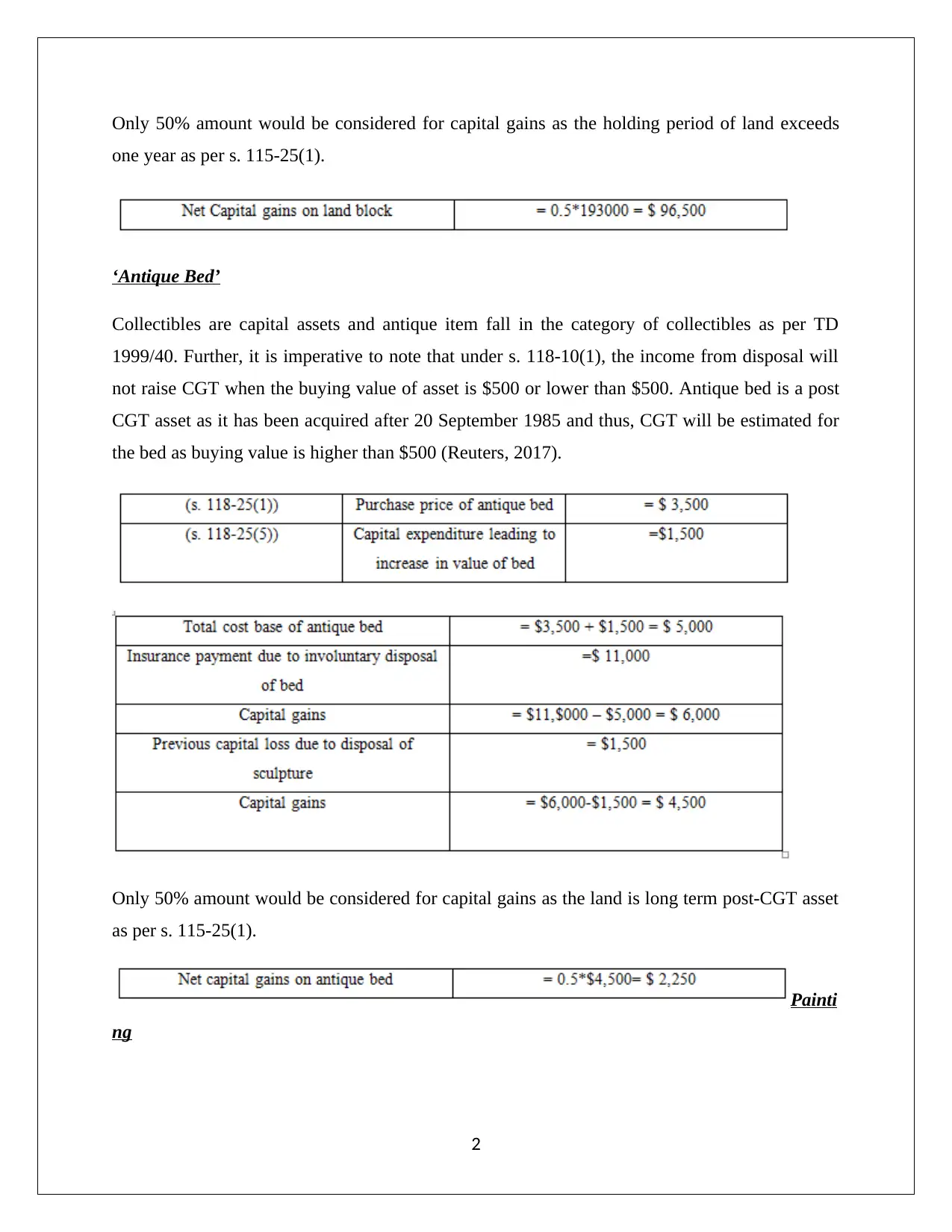

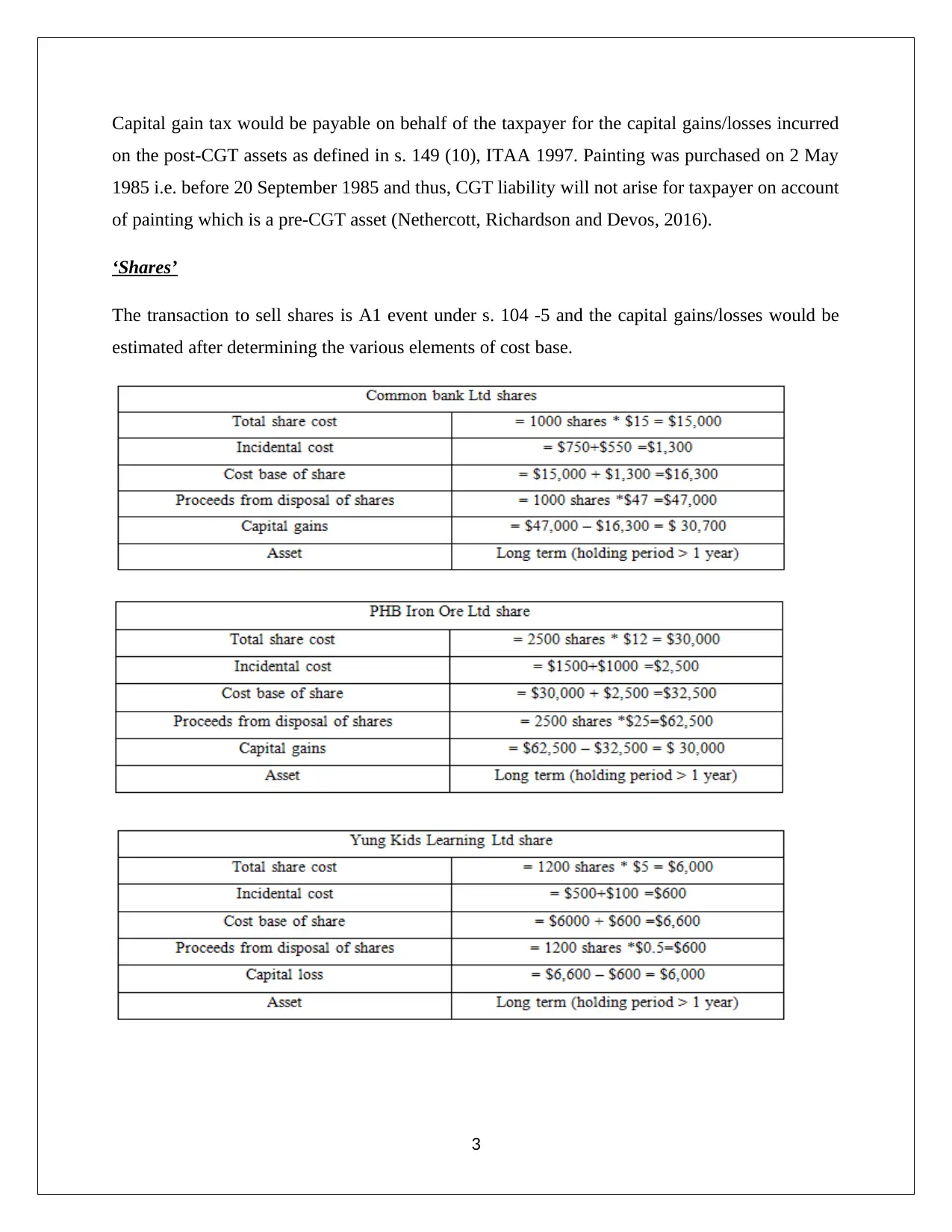

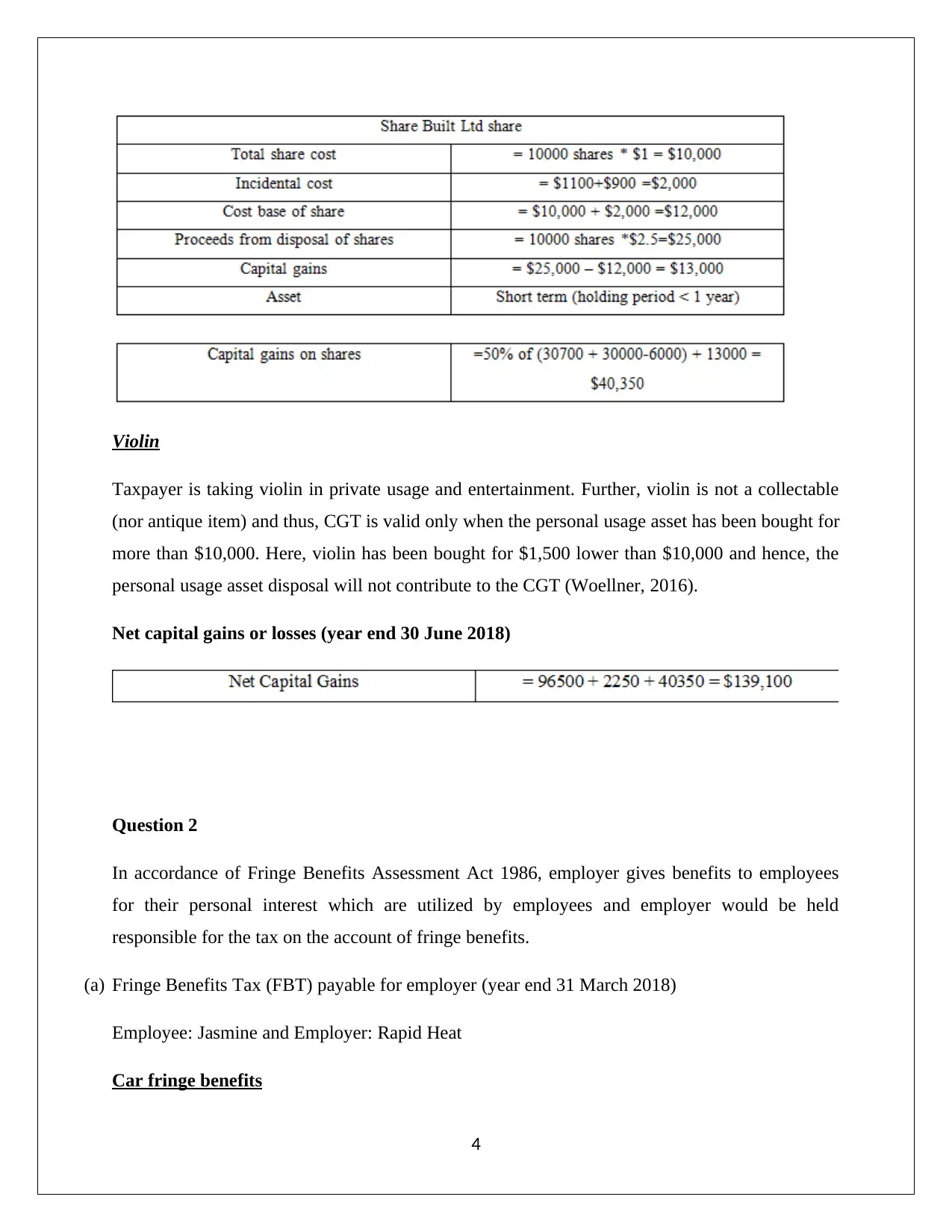

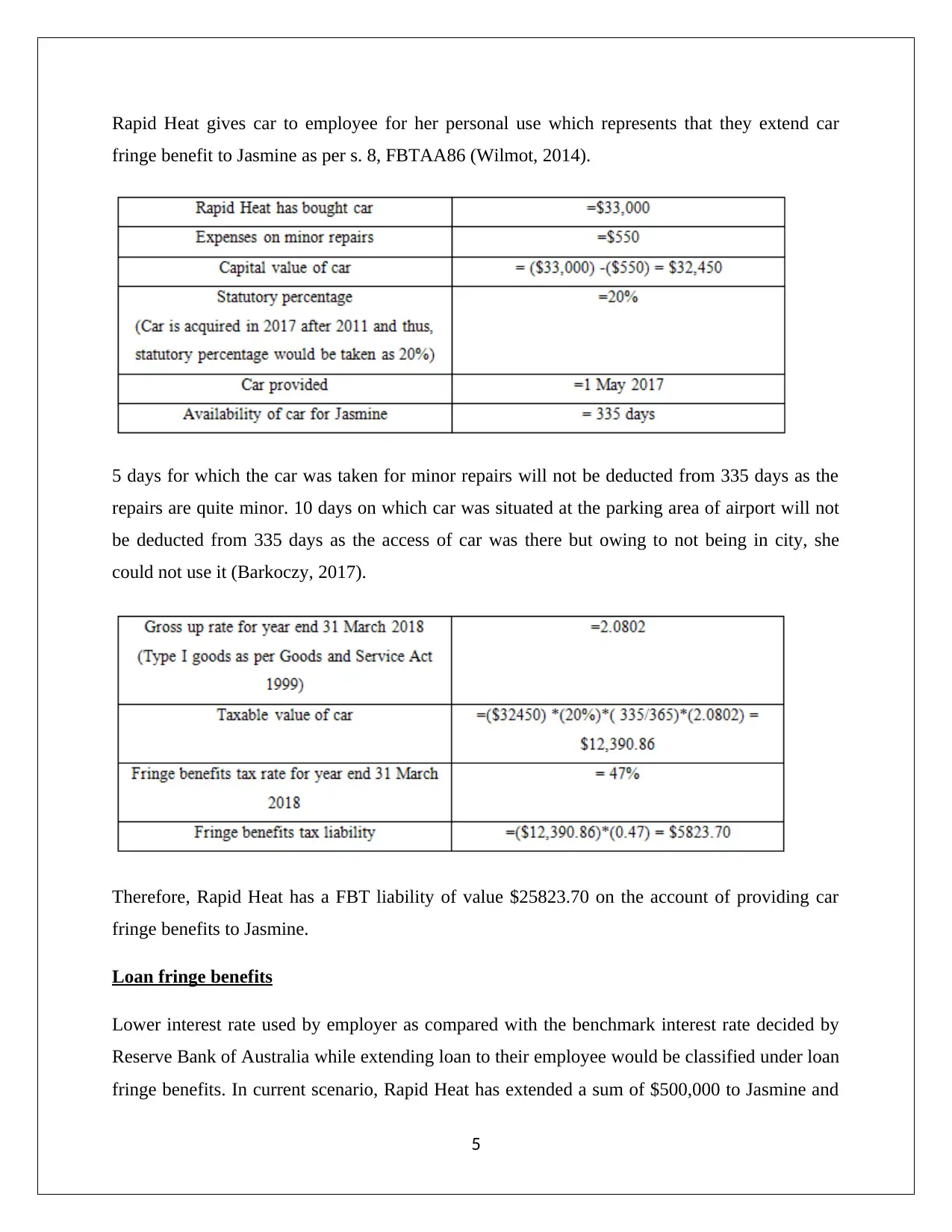

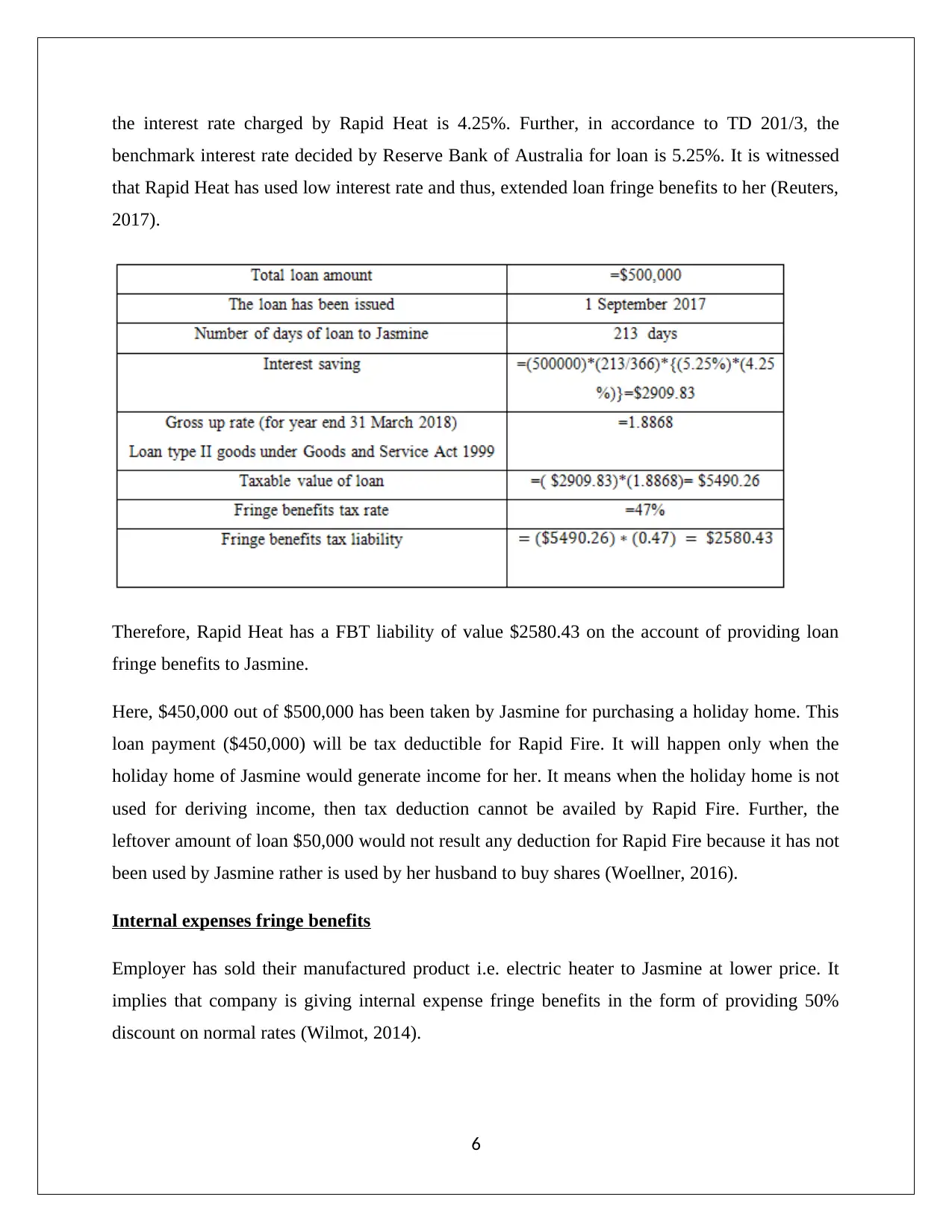

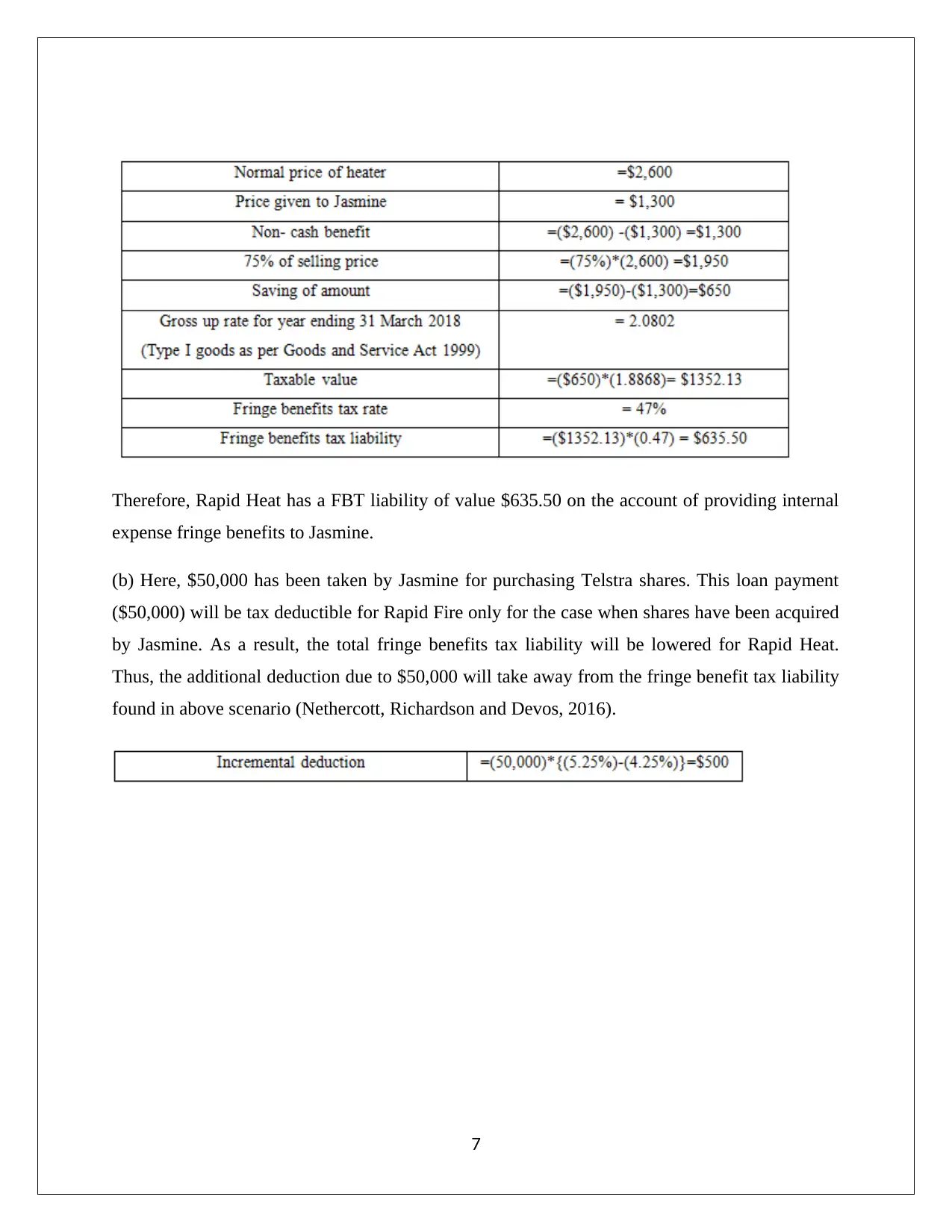

This report provides a detailed analysis of capital gains tax (CGT) implications for an investor in Mayfield, NSW, focusing on the disposal of assets such as vacant land, an antique bed, and shares, while also addressing the CGT treatment of a painting and a violin. It further examines fringe benefits tax (FBT) liabilities for an employer, Rapid Heat, concerning benefits provided to an employee, Jasmine, including car fringe benefits, loan fringe benefits, and internal expenses fringe benefits, with consideration of tax deductions related to loan usage for a holiday home and Telstra shares. The analysis is conducted in accordance with the Income Tax Assessment Act 1997 (ITAA 1997) and the Fringe Benefits Assessment Act 1986 (FBTAA86), incorporating relevant tax rulings and case laws to determine the tax consequences for both the investor and the employer.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.