HI6028 Taxation: Capital Gains,Fringe Benefits, & Tax Implications

VerifiedAdded on 2023/06/04

|12

|2971

|81

Report

AI Summary

This report provides a comprehensive analysis of capital gains tax (CGT) and fringe benefits tax (FBT) based on a hypothetical client scenario. It details the CGT implications of selling various assets, including land, antiques, paintings, shares, and a violin, considering factors like purchase date, collectables rules, and personal use exemptions. The report also examines FBT liabilities arising from car and loan fringe benefits provided to an employee, Jasmine, by Rapid Heat Pty Ltd. It calculates taxable values, applicable tax rates, and potential deductions, referencing relevant sections of the ITAA 1997 and FBTAA 1986. The analysis considers the impact of concessional interest rates on loans and the use of loan funds for personal and investment purposes.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The computation of net capital gains/losses for the income received from disposed capital assets

of the taxpayer is the main objective. All the transactions of the taxpayer have derived capital

receipts since the transactions are non-business in nature and thus, would be liable for Capital

Gains Tax (CGT) treatment.

Capital Asset 1: Sale of Block of Vacant Land

The asset has been purchased well after September 20, 1985 and therefore, the block of vacant

land is not named as pre-CGT asset of client as mentioned in details in s. 149 (10) ITAA 1997

(Barkoczy, 2017). Hence, the application of CGT will be valid on the proceeds of the disposal

for the calculation of capital gains or losses. Also, as per the underlying clauses of s. 104 (5)

ITAA 1997, the type of transaction for disposing the block of land is a capital gains tax event

(CGT event) of A1 type (Wilmot, 2014). According to this sub class, the capital gains or capital

losses could be determined by subtracting the cost base of asset and the capital receipts received

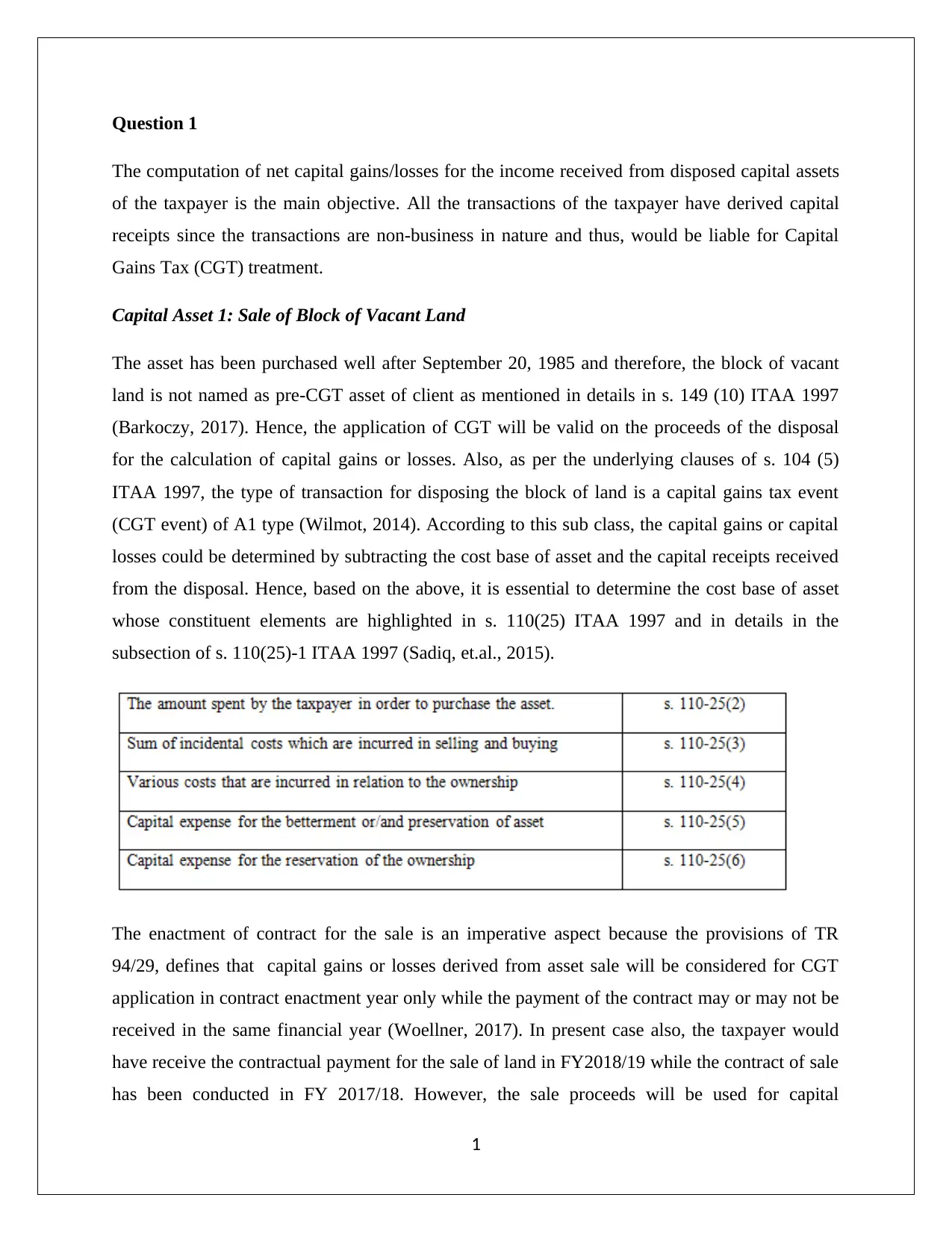

from the disposal. Hence, based on the above, it is essential to determine the cost base of asset

whose constituent elements are highlighted in s. 110(25) ITAA 1997 and in details in the

subsection of s. 110(25)-1 ITAA 1997 (Sadiq, et.al., 2015).

The enactment of contract for the sale is an imperative aspect because the provisions of TR

94/29, defines that capital gains or losses derived from asset sale will be considered for CGT

application in contract enactment year only while the payment of the contract may or may not be

received in the same financial year (Woellner, 2017). In present case also, the taxpayer would

have receive the contractual payment for the sale of land in FY2018/19 while the contract of sale

has been conducted in FY 2017/18. However, the sale proceeds will be used for capital

1

The computation of net capital gains/losses for the income received from disposed capital assets

of the taxpayer is the main objective. All the transactions of the taxpayer have derived capital

receipts since the transactions are non-business in nature and thus, would be liable for Capital

Gains Tax (CGT) treatment.

Capital Asset 1: Sale of Block of Vacant Land

The asset has been purchased well after September 20, 1985 and therefore, the block of vacant

land is not named as pre-CGT asset of client as mentioned in details in s. 149 (10) ITAA 1997

(Barkoczy, 2017). Hence, the application of CGT will be valid on the proceeds of the disposal

for the calculation of capital gains or losses. Also, as per the underlying clauses of s. 104 (5)

ITAA 1997, the type of transaction for disposing the block of land is a capital gains tax event

(CGT event) of A1 type (Wilmot, 2014). According to this sub class, the capital gains or capital

losses could be determined by subtracting the cost base of asset and the capital receipts received

from the disposal. Hence, based on the above, it is essential to determine the cost base of asset

whose constituent elements are highlighted in s. 110(25) ITAA 1997 and in details in the

subsection of s. 110(25)-1 ITAA 1997 (Sadiq, et.al., 2015).

The enactment of contract for the sale is an imperative aspect because the provisions of TR

94/29, defines that capital gains or losses derived from asset sale will be considered for CGT

application in contract enactment year only while the payment of the contract may or may not be

received in the same financial year (Woellner, 2017). In present case also, the taxpayer would

have receive the contractual payment for the sale of land in FY2018/19 while the contract of sale

has been conducted in FY 2017/18. However, the sale proceeds will be used for capital

1

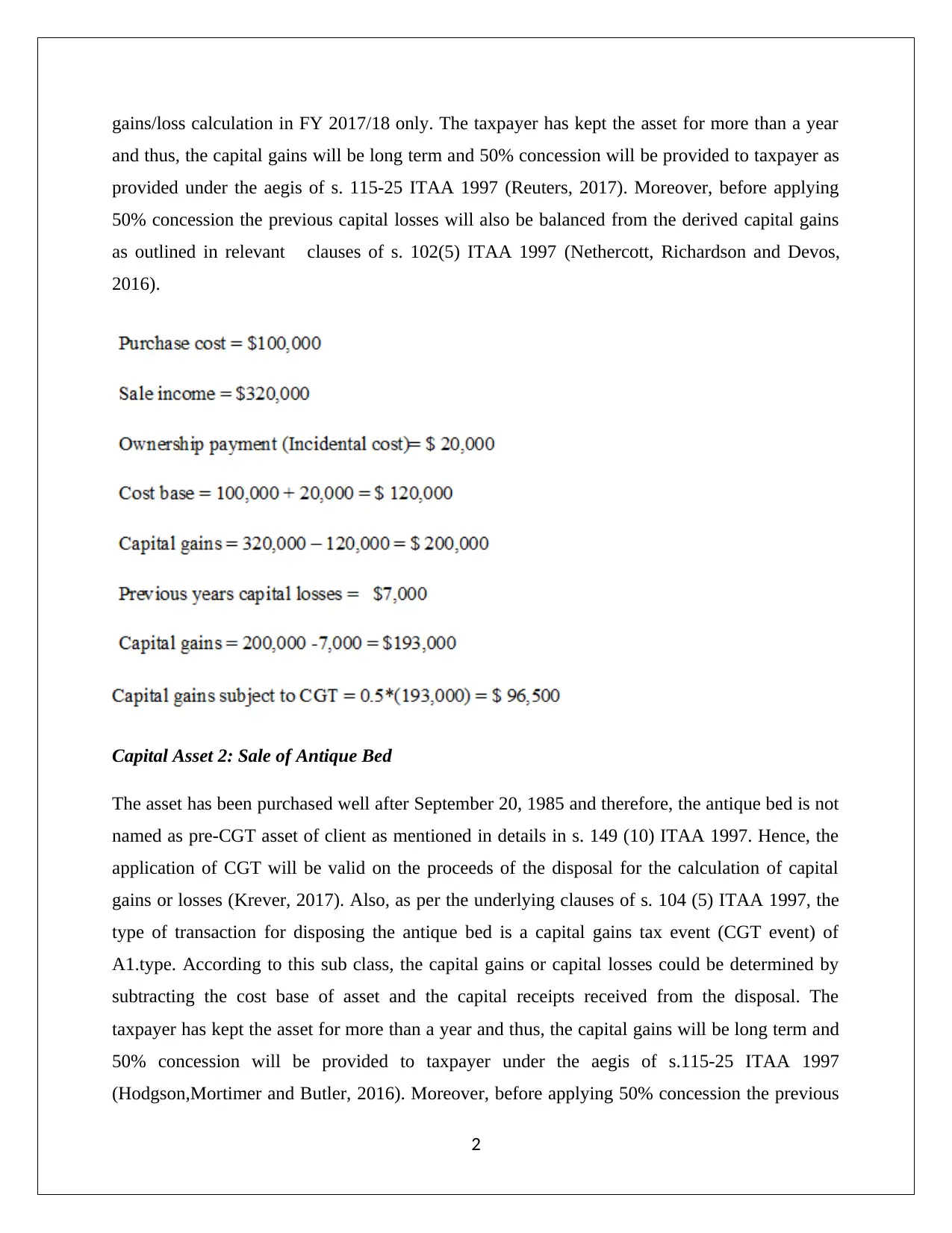

gains/loss calculation in FY 2017/18 only. The taxpayer has kept the asset for more than a year

and thus, the capital gains will be long term and 50% concession will be provided to taxpayer as

provided under the aegis of s. 115-25 ITAA 1997 (Reuters, 2017). Moreover, before applying

50% concession the previous capital losses will also be balanced from the derived capital gains

as outlined in relevant clauses of s. 102(5) ITAA 1997 (Nethercott, Richardson and Devos,

2016).

Capital Asset 2: Sale of Antique Bed

The asset has been purchased well after September 20, 1985 and therefore, the antique bed is not

named as pre-CGT asset of client as mentioned in details in s. 149 (10) ITAA 1997. Hence, the

application of CGT will be valid on the proceeds of the disposal for the calculation of capital

gains or losses (Krever, 2017). Also, as per the underlying clauses of s. 104 (5) ITAA 1997, the

type of transaction for disposing the antique bed is a capital gains tax event (CGT event) of

A1.type. According to this sub class, the capital gains or capital losses could be determined by

subtracting the cost base of asset and the capital receipts received from the disposal. The

taxpayer has kept the asset for more than a year and thus, the capital gains will be long term and

50% concession will be provided to taxpayer under the aegis of s.115-25 ITAA 1997

(Hodgson,Mortimer and Butler, 2016). Moreover, before applying 50% concession the previous

2

and thus, the capital gains will be long term and 50% concession will be provided to taxpayer as

provided under the aegis of s. 115-25 ITAA 1997 (Reuters, 2017). Moreover, before applying

50% concession the previous capital losses will also be balanced from the derived capital gains

as outlined in relevant clauses of s. 102(5) ITAA 1997 (Nethercott, Richardson and Devos,

2016).

Capital Asset 2: Sale of Antique Bed

The asset has been purchased well after September 20, 1985 and therefore, the antique bed is not

named as pre-CGT asset of client as mentioned in details in s. 149 (10) ITAA 1997. Hence, the

application of CGT will be valid on the proceeds of the disposal for the calculation of capital

gains or losses (Krever, 2017). Also, as per the underlying clauses of s. 104 (5) ITAA 1997, the

type of transaction for disposing the antique bed is a capital gains tax event (CGT event) of

A1.type. According to this sub class, the capital gains or capital losses could be determined by

subtracting the cost base of asset and the capital receipts received from the disposal. The

taxpayer has kept the asset for more than a year and thus, the capital gains will be long term and

50% concession will be provided to taxpayer under the aegis of s.115-25 ITAA 1997

(Hodgson,Mortimer and Butler, 2016). Moreover, before applying 50% concession the previous

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital losses will be balanced from the derived capital gains as outlined in the relevant clauses

of s. 102(5) ITAA 1997 (Barkoczy, 2017). However, the imperative factor before executing the

computation is that antique bed is a type of collectable and therefore, the condition required for

CGT treatment of collectable must be met.

Condition: The antique item must be procured for a sum amount higher than $500 as indicated in

s. 118-10 ITAA 1997 (Krever, 2017).

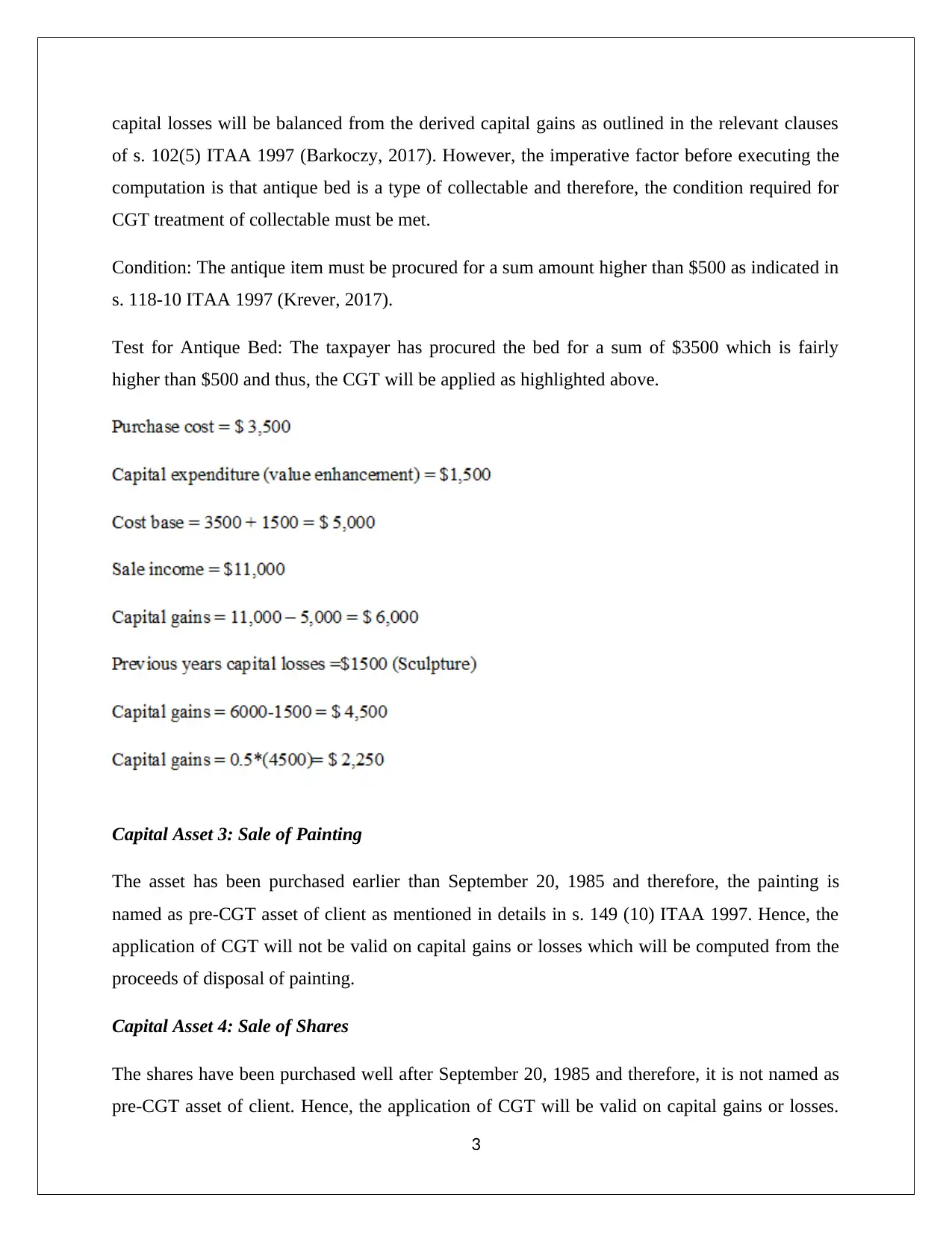

Test for Antique Bed: The taxpayer has procured the bed for a sum of $3500 which is fairly

higher than $500 and thus, the CGT will be applied as highlighted above.

Capital Asset 3: Sale of Painting

The asset has been purchased earlier than September 20, 1985 and therefore, the painting is

named as pre-CGT asset of client as mentioned in details in s. 149 (10) ITAA 1997. Hence, the

application of CGT will not be valid on capital gains or losses which will be computed from the

proceeds of disposal of painting.

Capital Asset 4: Sale of Shares

The shares have been purchased well after September 20, 1985 and therefore, it is not named as

pre-CGT asset of client. Hence, the application of CGT will be valid on capital gains or losses.

3

of s. 102(5) ITAA 1997 (Barkoczy, 2017). However, the imperative factor before executing the

computation is that antique bed is a type of collectable and therefore, the condition required for

CGT treatment of collectable must be met.

Condition: The antique item must be procured for a sum amount higher than $500 as indicated in

s. 118-10 ITAA 1997 (Krever, 2017).

Test for Antique Bed: The taxpayer has procured the bed for a sum of $3500 which is fairly

higher than $500 and thus, the CGT will be applied as highlighted above.

Capital Asset 3: Sale of Painting

The asset has been purchased earlier than September 20, 1985 and therefore, the painting is

named as pre-CGT asset of client as mentioned in details in s. 149 (10) ITAA 1997. Hence, the

application of CGT will not be valid on capital gains or losses which will be computed from the

proceeds of disposal of painting.

Capital Asset 4: Sale of Shares

The shares have been purchased well after September 20, 1985 and therefore, it is not named as

pre-CGT asset of client. Hence, the application of CGT will be valid on capital gains or losses.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

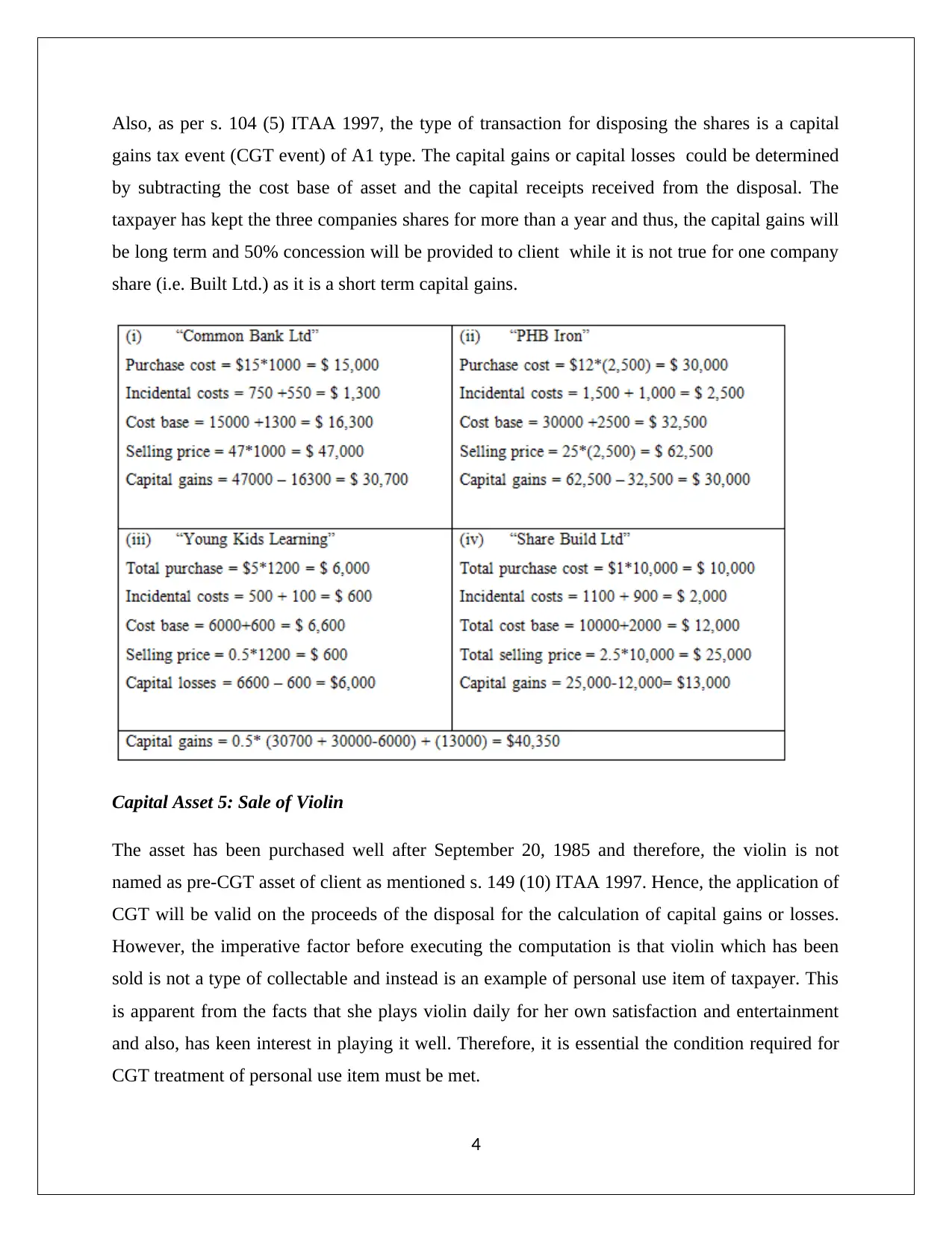

Also, as per s. 104 (5) ITAA 1997, the type of transaction for disposing the shares is a capital

gains tax event (CGT event) of A1 type. The capital gains or capital losses could be determined

by subtracting the cost base of asset and the capital receipts received from the disposal. The

taxpayer has kept the three companies shares for more than a year and thus, the capital gains will

be long term and 50% concession will be provided to client while it is not true for one company

share (i.e. Built Ltd.) as it is a short term capital gains.

Capital Asset 5: Sale of Violin

The asset has been purchased well after September 20, 1985 and therefore, the violin is not

named as pre-CGT asset of client as mentioned s. 149 (10) ITAA 1997. Hence, the application of

CGT will be valid on the proceeds of the disposal for the calculation of capital gains or losses.

However, the imperative factor before executing the computation is that violin which has been

sold is not a type of collectable and instead is an example of personal use item of taxpayer. This

is apparent from the facts that she plays violin daily for her own satisfaction and entertainment

and also, has keen interest in playing it well. Therefore, it is essential the condition required for

CGT treatment of personal use item must be met.

4

gains tax event (CGT event) of A1 type. The capital gains or capital losses could be determined

by subtracting the cost base of asset and the capital receipts received from the disposal. The

taxpayer has kept the three companies shares for more than a year and thus, the capital gains will

be long term and 50% concession will be provided to client while it is not true for one company

share (i.e. Built Ltd.) as it is a short term capital gains.

Capital Asset 5: Sale of Violin

The asset has been purchased well after September 20, 1985 and therefore, the violin is not

named as pre-CGT asset of client as mentioned s. 149 (10) ITAA 1997. Hence, the application of

CGT will be valid on the proceeds of the disposal for the calculation of capital gains or losses.

However, the imperative factor before executing the computation is that violin which has been

sold is not a type of collectable and instead is an example of personal use item of taxpayer. This

is apparent from the facts that she plays violin daily for her own satisfaction and entertainment

and also, has keen interest in playing it well. Therefore, it is essential the condition required for

CGT treatment of personal use item must be met.

4

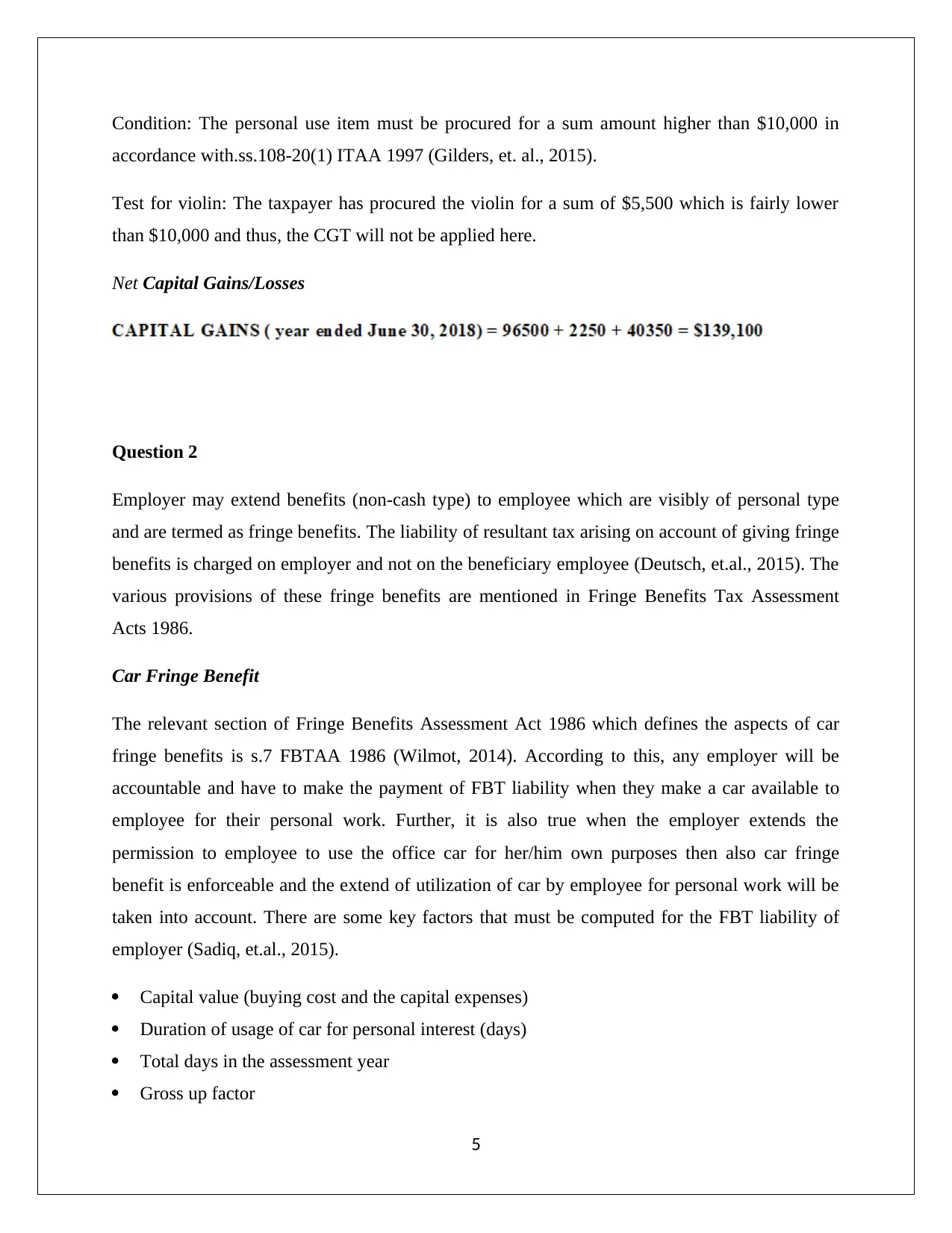

Condition: The personal use item must be procured for a sum amount higher than $10,000 in

accordance with.ss.108-20(1) ITAA 1997 (Gilders, et. al., 2015).

Test for violin: The taxpayer has procured the violin for a sum of $5,500 which is fairly lower

than $10,000 and thus, the CGT will not be applied here.

Net Capital Gains/Losses

Question 2

Employer may extend benefits (non-cash type) to employee which are visibly of personal type

and are termed as fringe benefits. The liability of resultant tax arising on account of giving fringe

benefits is charged on employer and not on the beneficiary employee (Deutsch, et.al., 2015). The

various provisions of these fringe benefits are mentioned in Fringe Benefits Tax Assessment

Acts 1986.

Car Fringe Benefit

The relevant section of Fringe Benefits Assessment Act 1986 which defines the aspects of car

fringe benefits is s.7 FBTAA 1986 (Wilmot, 2014). According to this, any employer will be

accountable and have to make the payment of FBT liability when they make a car available to

employee for their personal work. Further, it is also true when the employer extends the

permission to employee to use the office car for her/him own purposes then also car fringe

benefit is enforceable and the extend of utilization of car by employee for personal work will be

taken into account. There are some key factors that must be computed for the FBT liability of

employer (Sadiq, et.al., 2015).

Capital value (buying cost and the capital expenses)

Duration of usage of car for personal interest (days)

Total days in the assessment year

Gross up factor

5

accordance with.ss.108-20(1) ITAA 1997 (Gilders, et. al., 2015).

Test for violin: The taxpayer has procured the violin for a sum of $5,500 which is fairly lower

than $10,000 and thus, the CGT will not be applied here.

Net Capital Gains/Losses

Question 2

Employer may extend benefits (non-cash type) to employee which are visibly of personal type

and are termed as fringe benefits. The liability of resultant tax arising on account of giving fringe

benefits is charged on employer and not on the beneficiary employee (Deutsch, et.al., 2015). The

various provisions of these fringe benefits are mentioned in Fringe Benefits Tax Assessment

Acts 1986.

Car Fringe Benefit

The relevant section of Fringe Benefits Assessment Act 1986 which defines the aspects of car

fringe benefits is s.7 FBTAA 1986 (Wilmot, 2014). According to this, any employer will be

accountable and have to make the payment of FBT liability when they make a car available to

employee for their personal work. Further, it is also true when the employer extends the

permission to employee to use the office car for her/him own purposes then also car fringe

benefit is enforceable and the extend of utilization of car by employee for personal work will be

taken into account. There are some key factors that must be computed for the FBT liability of

employer (Sadiq, et.al., 2015).

Capital value (buying cost and the capital expenses)

Duration of usage of car for personal interest (days)

Total days in the assessment year

Gross up factor

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fringe benefit tax rate

1) The fringe benefit amount would be calculation by using capital value, durations of usage of

car for personal interest of employee, total days in the assessment year (Gilders, et. al.,

2015).

2) Taxable value of fringe benefit would be the multiplication of the two variables one is fringe

benefit amount and the second is gross up factor based on the underlying type of benefit

(Coleman, 2016).

3) Fringe Benefit Tax Liability (FBT Liability) is multiplication of taxable value of the fringe

benefit and the applicable fringe benefit tax rate. This amount would have to pay on the part

of employer in order to fulfil the FBT liability. Further, no FBT liability is imposed on

employee (Woellner, 2017).

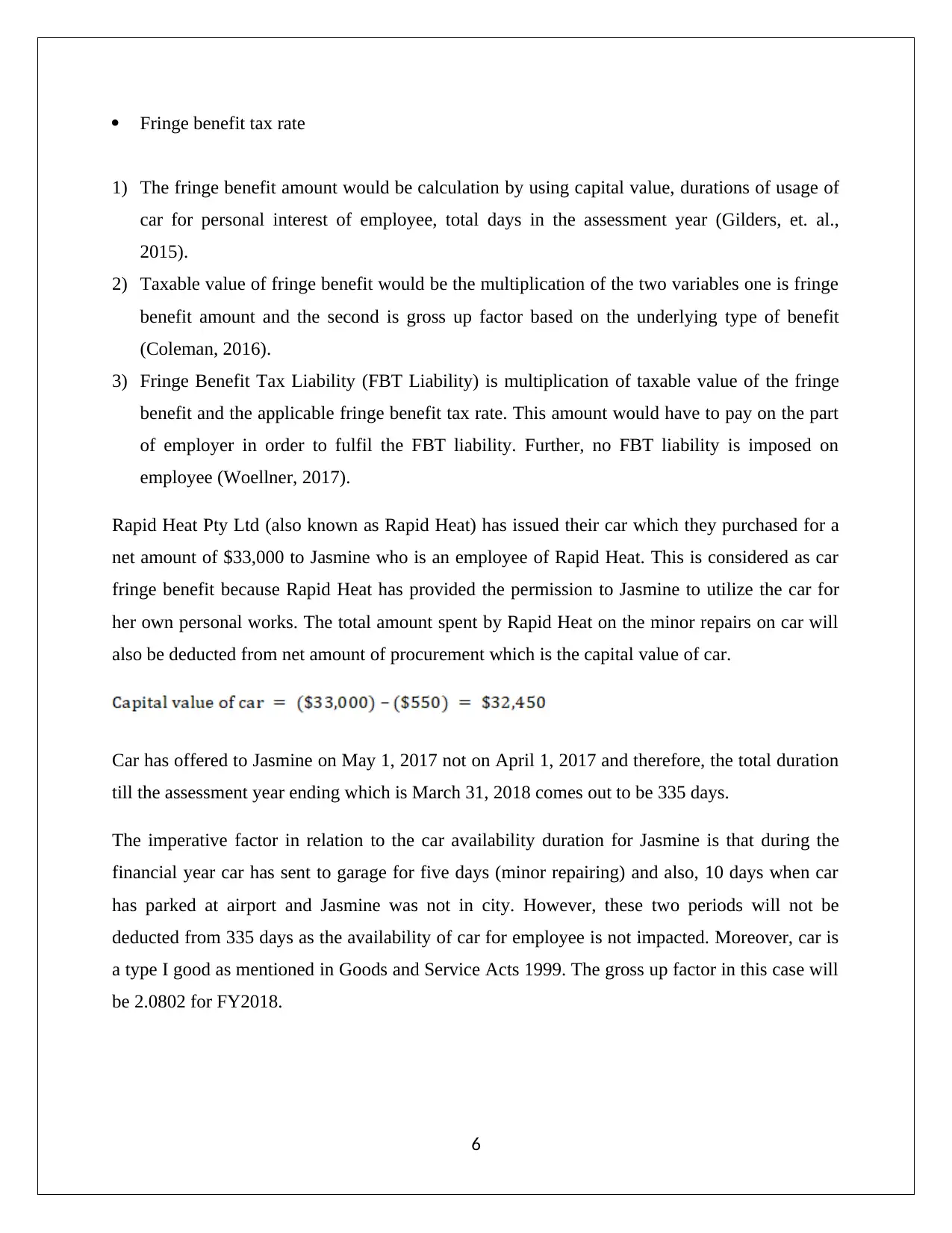

Rapid Heat Pty Ltd (also known as Rapid Heat) has issued their car which they purchased for a

net amount of $33,000 to Jasmine who is an employee of Rapid Heat. This is considered as car

fringe benefit because Rapid Heat has provided the permission to Jasmine to utilize the car for

her own personal works. The total amount spent by Rapid Heat on the minor repairs on car will

also be deducted from net amount of procurement which is the capital value of car.

Car has offered to Jasmine on May 1, 2017 not on April 1, 2017 and therefore, the total duration

till the assessment year ending which is March 31, 2018 comes out to be 335 days.

The imperative factor in relation to the car availability duration for Jasmine is that during the

financial year car has sent to garage for five days (minor repairing) and also, 10 days when car

has parked at airport and Jasmine was not in city. However, these two periods will not be

deducted from 335 days as the availability of car for employee is not impacted. Moreover, car is

a type I good as mentioned in Goods and Service Acts 1999. The gross up factor in this case will

be 2.0802 for FY2018.

6

1) The fringe benefit amount would be calculation by using capital value, durations of usage of

car for personal interest of employee, total days in the assessment year (Gilders, et. al.,

2015).

2) Taxable value of fringe benefit would be the multiplication of the two variables one is fringe

benefit amount and the second is gross up factor based on the underlying type of benefit

(Coleman, 2016).

3) Fringe Benefit Tax Liability (FBT Liability) is multiplication of taxable value of the fringe

benefit and the applicable fringe benefit tax rate. This amount would have to pay on the part

of employer in order to fulfil the FBT liability. Further, no FBT liability is imposed on

employee (Woellner, 2017).

Rapid Heat Pty Ltd (also known as Rapid Heat) has issued their car which they purchased for a

net amount of $33,000 to Jasmine who is an employee of Rapid Heat. This is considered as car

fringe benefit because Rapid Heat has provided the permission to Jasmine to utilize the car for

her own personal works. The total amount spent by Rapid Heat on the minor repairs on car will

also be deducted from net amount of procurement which is the capital value of car.

Car has offered to Jasmine on May 1, 2017 not on April 1, 2017 and therefore, the total duration

till the assessment year ending which is March 31, 2018 comes out to be 335 days.

The imperative factor in relation to the car availability duration for Jasmine is that during the

financial year car has sent to garage for five days (minor repairing) and also, 10 days when car

has parked at airport and Jasmine was not in city. However, these two periods will not be

deducted from 335 days as the availability of car for employee is not impacted. Moreover, car is

a type I good as mentioned in Goods and Service Acts 1999. The gross up factor in this case will

be 2.0802 for FY2018.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

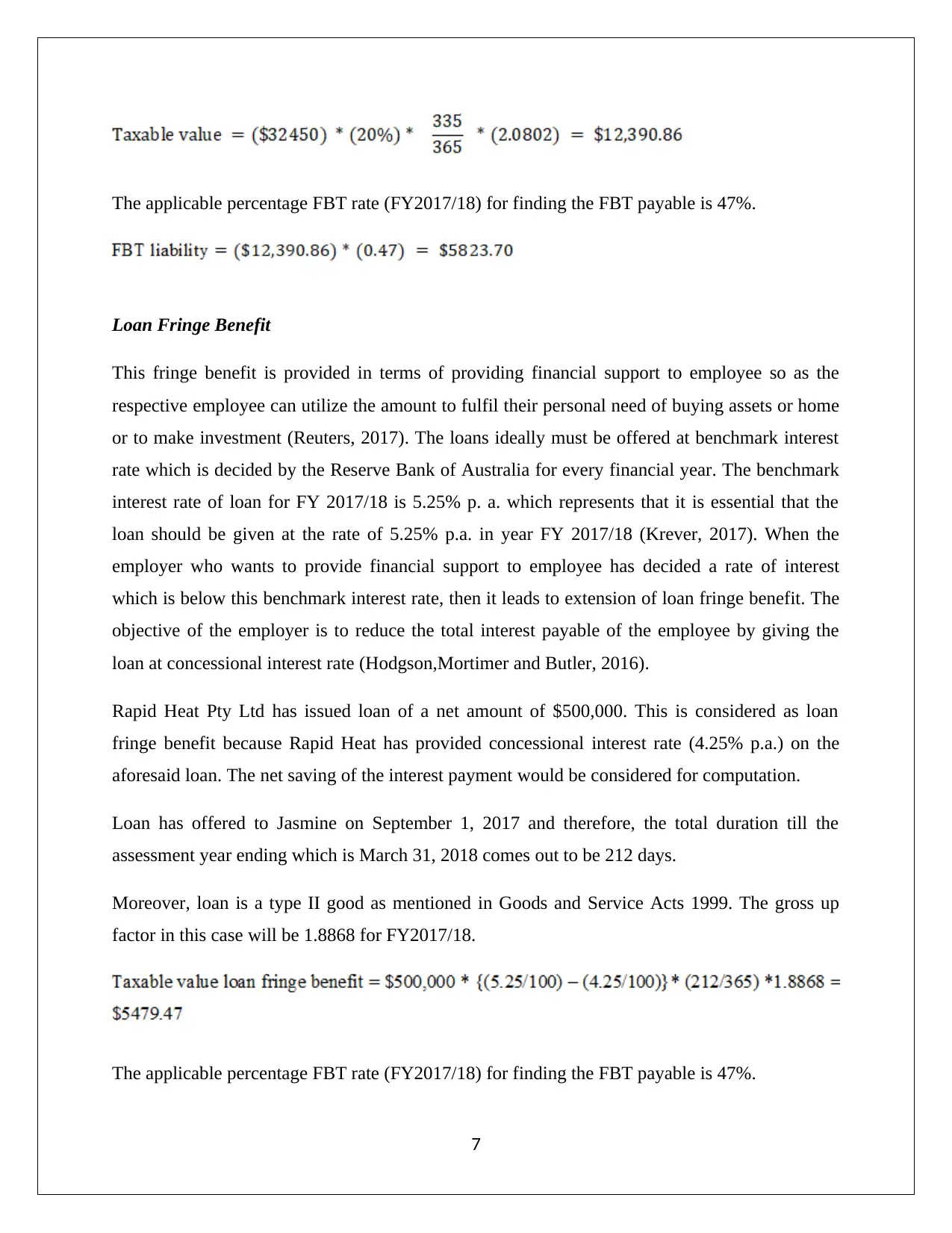

The applicable percentage FBT rate (FY2017/18) for finding the FBT payable is 47%.

Loan Fringe Benefit

This fringe benefit is provided in terms of providing financial support to employee so as the

respective employee can utilize the amount to fulfil their personal need of buying assets or home

or to make investment (Reuters, 2017). The loans ideally must be offered at benchmark interest

rate which is decided by the Reserve Bank of Australia for every financial year. The benchmark

interest rate of loan for FY 2017/18 is 5.25% p. a. which represents that it is essential that the

loan should be given at the rate of 5.25% p.a. in year FY 2017/18 (Krever, 2017). When the

employer who wants to provide financial support to employee has decided a rate of interest

which is below this benchmark interest rate, then it leads to extension of loan fringe benefit. The

objective of the employer is to reduce the total interest payable of the employee by giving the

loan at concessional interest rate (Hodgson,Mortimer and Butler, 2016).

Rapid Heat Pty Ltd has issued loan of a net amount of $500,000. This is considered as loan

fringe benefit because Rapid Heat has provided concessional interest rate (4.25% p.a.) on the

aforesaid loan. The net saving of the interest payment would be considered for computation.

Loan has offered to Jasmine on September 1, 2017 and therefore, the total duration till the

assessment year ending which is March 31, 2018 comes out to be 212 days.

Moreover, loan is a type II good as mentioned in Goods and Service Acts 1999. The gross up

factor in this case will be 1.8868 for FY2017/18.

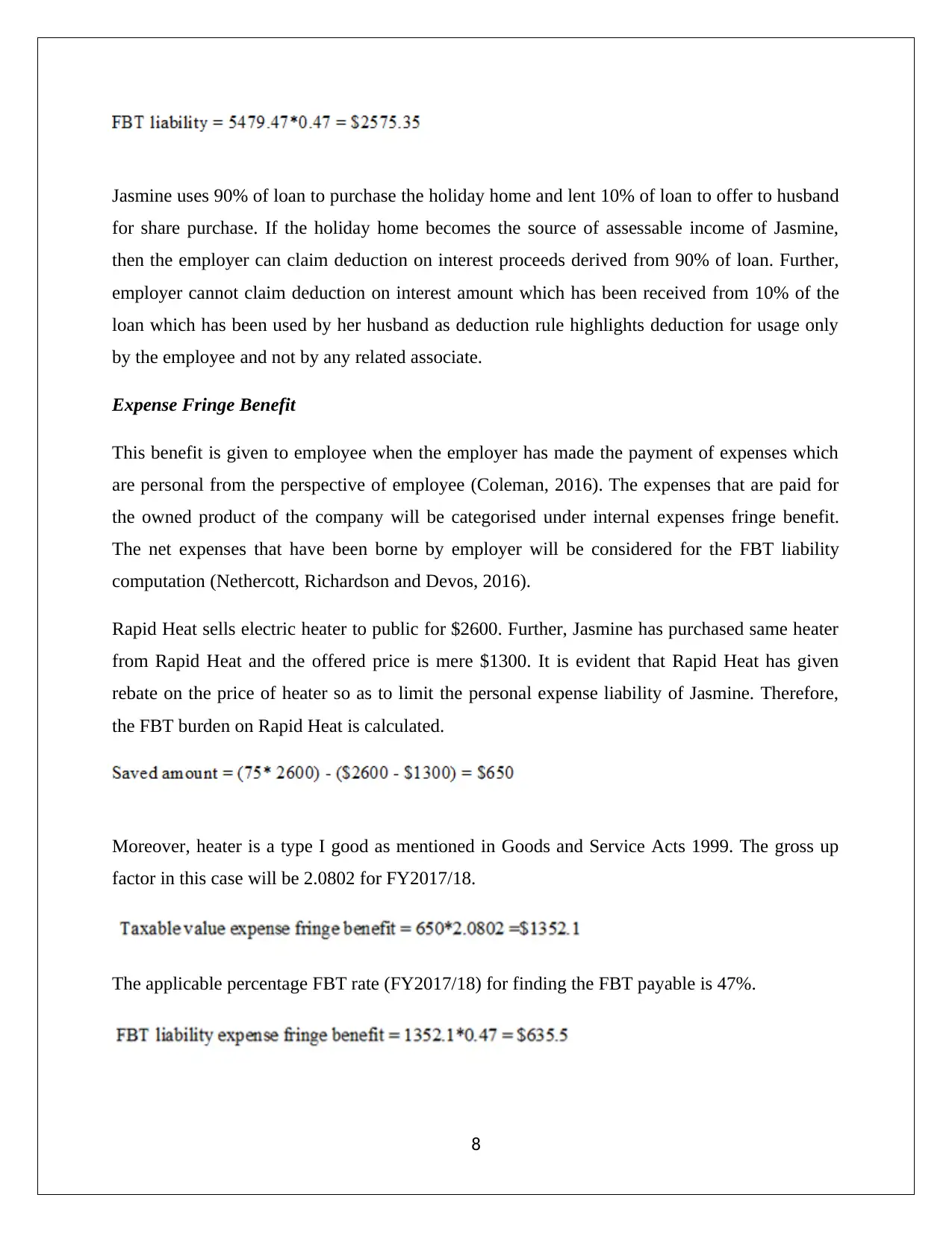

The applicable percentage FBT rate (FY2017/18) for finding the FBT payable is 47%.

7

Loan Fringe Benefit

This fringe benefit is provided in terms of providing financial support to employee so as the

respective employee can utilize the amount to fulfil their personal need of buying assets or home

or to make investment (Reuters, 2017). The loans ideally must be offered at benchmark interest

rate which is decided by the Reserve Bank of Australia for every financial year. The benchmark

interest rate of loan for FY 2017/18 is 5.25% p. a. which represents that it is essential that the

loan should be given at the rate of 5.25% p.a. in year FY 2017/18 (Krever, 2017). When the

employer who wants to provide financial support to employee has decided a rate of interest

which is below this benchmark interest rate, then it leads to extension of loan fringe benefit. The

objective of the employer is to reduce the total interest payable of the employee by giving the

loan at concessional interest rate (Hodgson,Mortimer and Butler, 2016).

Rapid Heat Pty Ltd has issued loan of a net amount of $500,000. This is considered as loan

fringe benefit because Rapid Heat has provided concessional interest rate (4.25% p.a.) on the

aforesaid loan. The net saving of the interest payment would be considered for computation.

Loan has offered to Jasmine on September 1, 2017 and therefore, the total duration till the

assessment year ending which is March 31, 2018 comes out to be 212 days.

Moreover, loan is a type II good as mentioned in Goods and Service Acts 1999. The gross up

factor in this case will be 1.8868 for FY2017/18.

The applicable percentage FBT rate (FY2017/18) for finding the FBT payable is 47%.

7

Jasmine uses 90% of loan to purchase the holiday home and lent 10% of loan to offer to husband

for share purchase. If the holiday home becomes the source of assessable income of Jasmine,

then the employer can claim deduction on interest proceeds derived from 90% of loan. Further,

employer cannot claim deduction on interest amount which has been received from 10% of the

loan which has been used by her husband as deduction rule highlights deduction for usage only

by the employee and not by any related associate.

Expense Fringe Benefit

This benefit is given to employee when the employer has made the payment of expenses which

are personal from the perspective of employee (Coleman, 2016). The expenses that are paid for

the owned product of the company will be categorised under internal expenses fringe benefit.

The net expenses that have been borne by employer will be considered for the FBT liability

computation (Nethercott, Richardson and Devos, 2016).

Rapid Heat sells electric heater to public for $2600. Further, Jasmine has purchased same heater

from Rapid Heat and the offered price is mere $1300. It is evident that Rapid Heat has given

rebate on the price of heater so as to limit the personal expense liability of Jasmine. Therefore,

the FBT burden on Rapid Heat is calculated.

Moreover, heater is a type I good as mentioned in Goods and Service Acts 1999. The gross up

factor in this case will be 2.0802 for FY2017/18.

The applicable percentage FBT rate (FY2017/18) for finding the FBT payable is 47%.

8

for share purchase. If the holiday home becomes the source of assessable income of Jasmine,

then the employer can claim deduction on interest proceeds derived from 90% of loan. Further,

employer cannot claim deduction on interest amount which has been received from 10% of the

loan which has been used by her husband as deduction rule highlights deduction for usage only

by the employee and not by any related associate.

Expense Fringe Benefit

This benefit is given to employee when the employer has made the payment of expenses which

are personal from the perspective of employee (Coleman, 2016). The expenses that are paid for

the owned product of the company will be categorised under internal expenses fringe benefit.

The net expenses that have been borne by employer will be considered for the FBT liability

computation (Nethercott, Richardson and Devos, 2016).

Rapid Heat sells electric heater to public for $2600. Further, Jasmine has purchased same heater

from Rapid Heat and the offered price is mere $1300. It is evident that Rapid Heat has given

rebate on the price of heater so as to limit the personal expense liability of Jasmine. Therefore,

the FBT burden on Rapid Heat is calculated.

Moreover, heater is a type I good as mentioned in Goods and Service Acts 1999. The gross up

factor in this case will be 2.0802 for FY2017/18.

The applicable percentage FBT rate (FY2017/18) for finding the FBT payable is 47%.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Earlier Jasmine used 100% of loan to in such a way that 90% of loan will be used to purchase

the holiday home and lent 10% of loan to purchase share to husband. Now the share purchase is

also being carried out by Jasmine instead of her husband. In this situation, the dividend amount

that results from shares will also be part of assessable income of Jasmine and thus, employer can

potentially claim deduction on interest amount which would be received from 10% of the loan

which has been used by her. The deduction from 10% of loan which is $50,000 will be used to

decrease the net fringe benefit tax payable of Rapid Heat. The increase in deduction available to

the employer is exhibited thorough the following working.

9

the holiday home and lent 10% of loan to purchase share to husband. Now the share purchase is

also being carried out by Jasmine instead of her husband. In this situation, the dividend amount

that results from shares will also be part of assessable income of Jasmine and thus, employer can

potentially claim deduction on interest amount which would be received from 10% of the loan

which has been used by her. The deduction from 10% of loan which is $50,000 will be used to

decrease the net fringe benefit tax payable of Rapid Heat. The increase in deduction available to

the employer is exhibited thorough the following working.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2017) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

10

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2017) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

10

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.