Accounting and Finance: WAACC and Capital Structure of AMP Ltd

VerifiedAdded on 2023/06/04

|15

|3256

|305

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles, focusing on capital structure and risk assessment. It begins with an evaluation of a proposed capital investment, calculating after-tax cash flows, payback period, net present value, and profitability index. Sensitivity analysis is conducted by considering scenarios with 5% higher and 5% lower estimated values. The report then shifts to an analysis of AMP Limited's weighted average cost of capital (WAACC) and capital structure, comparing it with Canaccord Genuity Group Inc. Significant changes in AMP Limited's capital structure over the past three years are examined, followed by a risk analysis based on annual reports and financial statements. The report concludes with a recommendation regarding the proposed capital investment and an assessment of AMP Limited's financial strategies.

Accounting and finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Part A.........................................................................................................................................3

Required (i)............................................................................................................................3

Required (ii)...........................................................................................................................5

A.........................................................................................................................................5

B.........................................................................................................................................5

C.........................................................................................................................................6

Required (iii)..........................................................................................................................6

Part B..........................................................................................................................................8

Executive summary................................................................................................................8

Introduction............................................................................................................................8

Body.......................................................................................................................................8

Comparative analysis of WAACC and capital structure....................................................8

Significant changes occurred in the capital structure of AMP limited in past three years

..........................................................................................................................................11

Risk analysis of AMP Limited.........................................................................................12

Conclusion............................................................................................................................14

References................................................................................................................................15

Part A.........................................................................................................................................3

Required (i)............................................................................................................................3

Required (ii)...........................................................................................................................5

A.........................................................................................................................................5

B.........................................................................................................................................5

C.........................................................................................................................................6

Required (iii)..........................................................................................................................6

Part B..........................................................................................................................................8

Executive summary................................................................................................................8

Introduction............................................................................................................................8

Body.......................................................................................................................................8

Comparative analysis of WAACC and capital structure....................................................8

Significant changes occurred in the capital structure of AMP limited in past three years

..........................................................................................................................................11

Risk analysis of AMP Limited.........................................................................................12

Conclusion............................................................................................................................14

References................................................................................................................................15

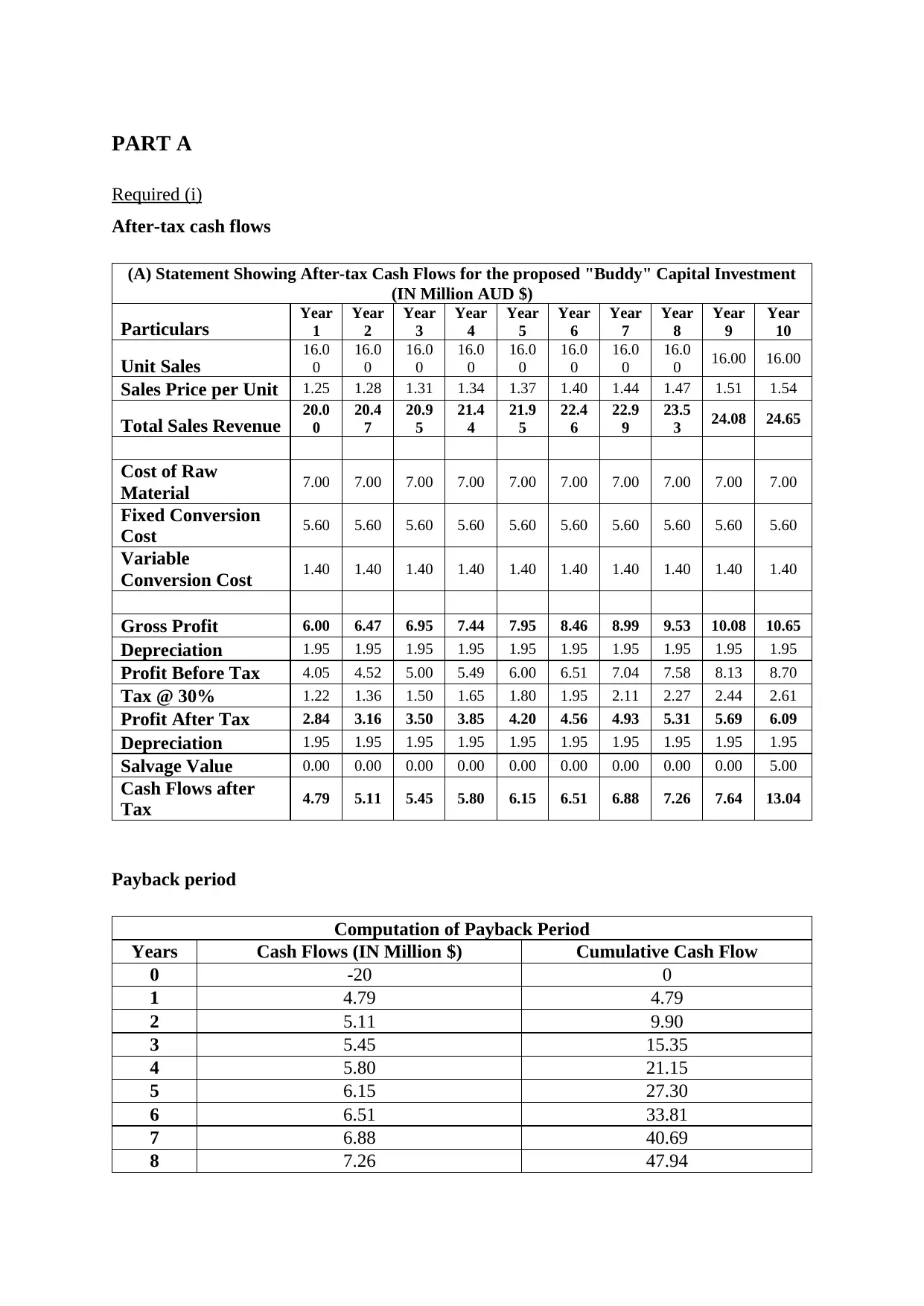

PART A

Required (i)

After-tax cash flows

(A) Statement Showing After-tax Cash Flows for the proposed "Buddy" Capital Investment

(IN Million AUD $)

Particulars Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 16.0

0

16.0

0

16.0

0

16.0

0

16.0

0

16.0

0

16.0

0

16.0

0 16.00 16.00

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 20.0

0

20.4

7

20.9

5

21.4

4

21.9

5

22.4

6

22.9

9

23.5

3 24.08 24.65

Cost of Raw

Material 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00

Fixed Conversion

Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable

Conversion Cost 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40

Gross Profit 6.00 6.47 6.95 7.44 7.95 8.46 8.99 9.53 10.08 10.65

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.05 4.52 5.00 5.49 6.00 6.51 7.04 7.58 8.13 8.70

Tax @ 30% 1.22 1.36 1.50 1.65 1.80 1.95 2.11 2.27 2.44 2.61

Profit After Tax 2.84 3.16 3.50 3.85 4.20 4.56 4.93 5.31 5.69 6.09

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after

Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Payback period

Computation of Payback Period

Years Cash Flows (IN Million $) Cumulative Cash Flow

0 -20 0

1 4.79 4.79

2 5.11 9.90

3 5.45 15.35

4 5.80 21.15

5 6.15 27.30

6 6.51 33.81

7 6.88 40.69

8 7.26 47.94

Required (i)

After-tax cash flows

(A) Statement Showing After-tax Cash Flows for the proposed "Buddy" Capital Investment

(IN Million AUD $)

Particulars Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 16.0

0

16.0

0

16.0

0

16.0

0

16.0

0

16.0

0

16.0

0

16.0

0 16.00 16.00

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 20.0

0

20.4

7

20.9

5

21.4

4

21.9

5

22.4

6

22.9

9

23.5

3 24.08 24.65

Cost of Raw

Material 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00

Fixed Conversion

Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable

Conversion Cost 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40

Gross Profit 6.00 6.47 6.95 7.44 7.95 8.46 8.99 9.53 10.08 10.65

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.05 4.52 5.00 5.49 6.00 6.51 7.04 7.58 8.13 8.70

Tax @ 30% 1.22 1.36 1.50 1.65 1.80 1.95 2.11 2.27 2.44 2.61

Profit After Tax 2.84 3.16 3.50 3.85 4.20 4.56 4.93 5.31 5.69 6.09

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after

Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Payback period

Computation of Payback Period

Years Cash Flows (IN Million $) Cumulative Cash Flow

0 -20 0

1 4.79 4.79

2 5.11 9.90

3 5.45 15.35

4 5.80 21.15

5 6.15 27.30

6 6.51 33.81

7 6.88 40.69

8 7.26 47.94

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 7.64 55.59

10 13.04 68.63

Payback Period = 3 + (21.15 - 20) / 5.80

3.19 Years

Net present value

(C) Statement Showing Net Present Value for the proposed "Buddy" Capital

Investment (IN Million AUD $)

Particulars Year 1 Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 20.00 20.47 20.95 21.44 21.95 22.46 22.99 23.53 24.08 24.65

Cost of Raw Material 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00

Fixed Conversion

Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable Conversion

Cost 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40

Gross Profit 6.00 6.47 6.95 7.44 7.95 8.46 8.99 9.53 10.08 10.65

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.05 4.52 5.00 5.49 6.00 6.51 7.04 7.58 8.13 8.70

Tax @ 30% 1.22 1.36 1.50 1.65 1.80 1.95 2.11 2.27 2.44 2.61

Profit After Tax 2.84 3.16 3.50 3.85 4.20 4.56 4.93 5.31 5.69 6.09

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Present Value Factor

@ 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows 3.988 3.551 3.154 2.795 2.471 2.180 1.920 1.688 1.481 2.106

Total Present Value of

Cash Flows 25.33

Initial Capital Outlay 20.00

Net Present Value 5.334

Profitability index

Present Value of Cash Inflows / Present Value of Cash Outflows

25.33/20

10 13.04 68.63

Payback Period = 3 + (21.15 - 20) / 5.80

3.19 Years

Net present value

(C) Statement Showing Net Present Value for the proposed "Buddy" Capital

Investment (IN Million AUD $)

Particulars Year 1 Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00 16.00

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 20.00 20.47 20.95 21.44 21.95 22.46 22.99 23.53 24.08 24.65

Cost of Raw Material 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00

Fixed Conversion

Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable Conversion

Cost 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40 1.40

Gross Profit 6.00 6.47 6.95 7.44 7.95 8.46 8.99 9.53 10.08 10.65

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.05 4.52 5.00 5.49 6.00 6.51 7.04 7.58 8.13 8.70

Tax @ 30% 1.22 1.36 1.50 1.65 1.80 1.95 2.11 2.27 2.44 2.61

Profit After Tax 2.84 3.16 3.50 3.85 4.20 4.56 4.93 5.31 5.69 6.09

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Present Value Factor

@ 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows 3.988 3.551 3.154 2.795 2.471 2.180 1.920 1.688 1.481 2.106

Total Present Value of

Cash Flows 25.33

Initial Capital Outlay 20.00

Net Present Value 5.334

Profitability index

Present Value of Cash Inflows / Present Value of Cash Outflows

25.33/20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

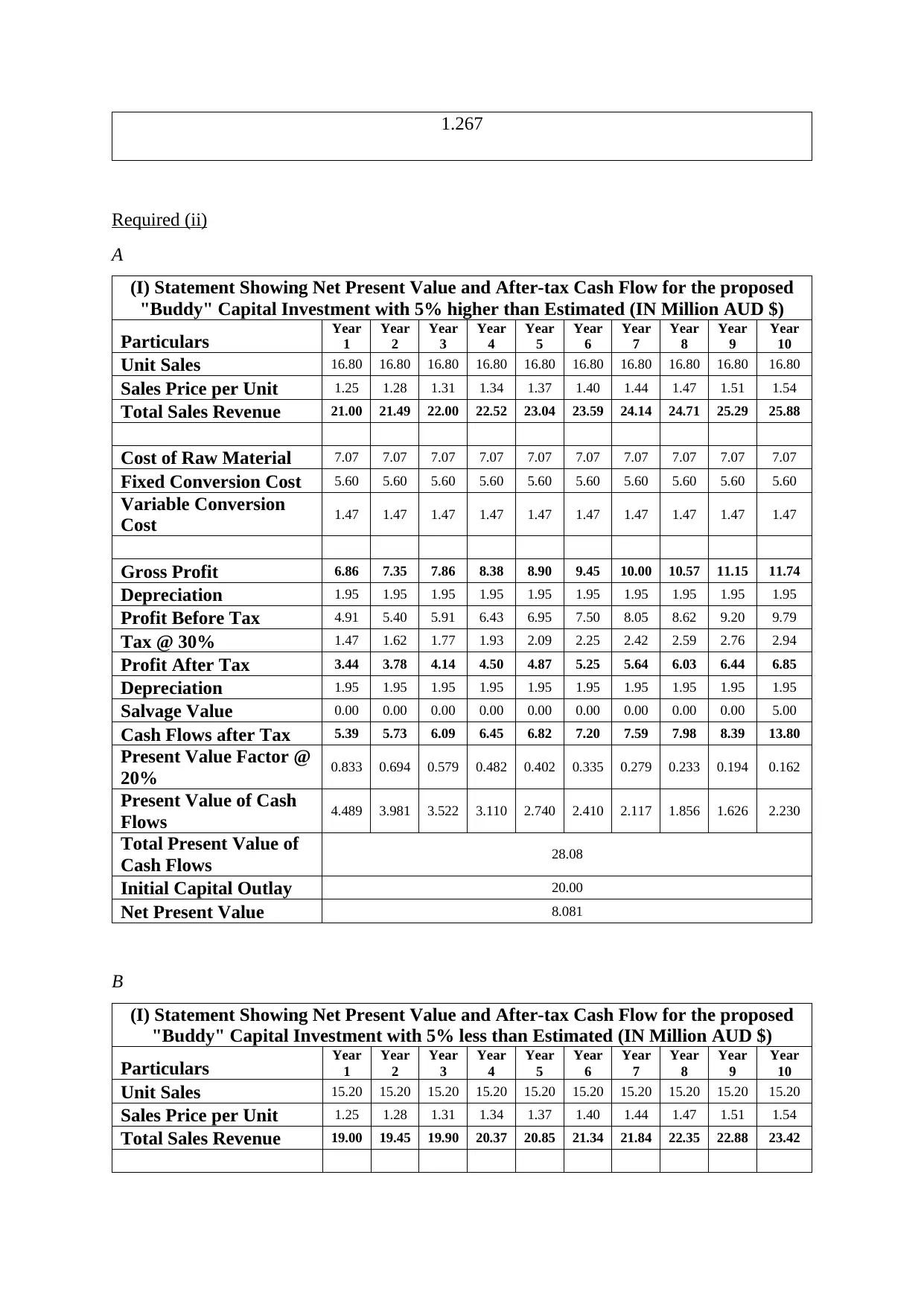

1.267

Required (ii)

A

(I) Statement Showing Net Present Value and After-tax Cash Flow for the proposed

"Buddy" Capital Investment with 5% higher than Estimated (IN Million AUD $)

Particulars Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 21.00 21.49 22.00 22.52 23.04 23.59 24.14 24.71 25.29 25.88

Cost of Raw Material 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07

Fixed Conversion Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable Conversion

Cost 1.47 1.47 1.47 1.47 1.47 1.47 1.47 1.47 1.47 1.47

Gross Profit 6.86 7.35 7.86 8.38 8.90 9.45 10.00 10.57 11.15 11.74

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.91 5.40 5.91 6.43 6.95 7.50 8.05 8.62 9.20 9.79

Tax @ 30% 1.47 1.62 1.77 1.93 2.09 2.25 2.42 2.59 2.76 2.94

Profit After Tax 3.44 3.78 4.14 4.50 4.87 5.25 5.64 6.03 6.44 6.85

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 5.39 5.73 6.09 6.45 6.82 7.20 7.59 7.98 8.39 13.80

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows 4.489 3.981 3.522 3.110 2.740 2.410 2.117 1.856 1.626 2.230

Total Present Value of

Cash Flows 28.08

Initial Capital Outlay 20.00

Net Present Value 8.081

B

(I) Statement Showing Net Present Value and After-tax Cash Flow for the proposed

"Buddy" Capital Investment with 5% less than Estimated (IN Million AUD $)

Particulars Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 15.20 15.20 15.20 15.20 15.20 15.20 15.20 15.20 15.20 15.20

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 19.00 19.45 19.90 20.37 20.85 21.34 21.84 22.35 22.88 23.42

Required (ii)

A

(I) Statement Showing Net Present Value and After-tax Cash Flow for the proposed

"Buddy" Capital Investment with 5% higher than Estimated (IN Million AUD $)

Particulars Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 21.00 21.49 22.00 22.52 23.04 23.59 24.14 24.71 25.29 25.88

Cost of Raw Material 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07

Fixed Conversion Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable Conversion

Cost 1.47 1.47 1.47 1.47 1.47 1.47 1.47 1.47 1.47 1.47

Gross Profit 6.86 7.35 7.86 8.38 8.90 9.45 10.00 10.57 11.15 11.74

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.91 5.40 5.91 6.43 6.95 7.50 8.05 8.62 9.20 9.79

Tax @ 30% 1.47 1.62 1.77 1.93 2.09 2.25 2.42 2.59 2.76 2.94

Profit After Tax 3.44 3.78 4.14 4.50 4.87 5.25 5.64 6.03 6.44 6.85

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 5.39 5.73 6.09 6.45 6.82 7.20 7.59 7.98 8.39 13.80

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows 4.489 3.981 3.522 3.110 2.740 2.410 2.117 1.856 1.626 2.230

Total Present Value of

Cash Flows 28.08

Initial Capital Outlay 20.00

Net Present Value 8.081

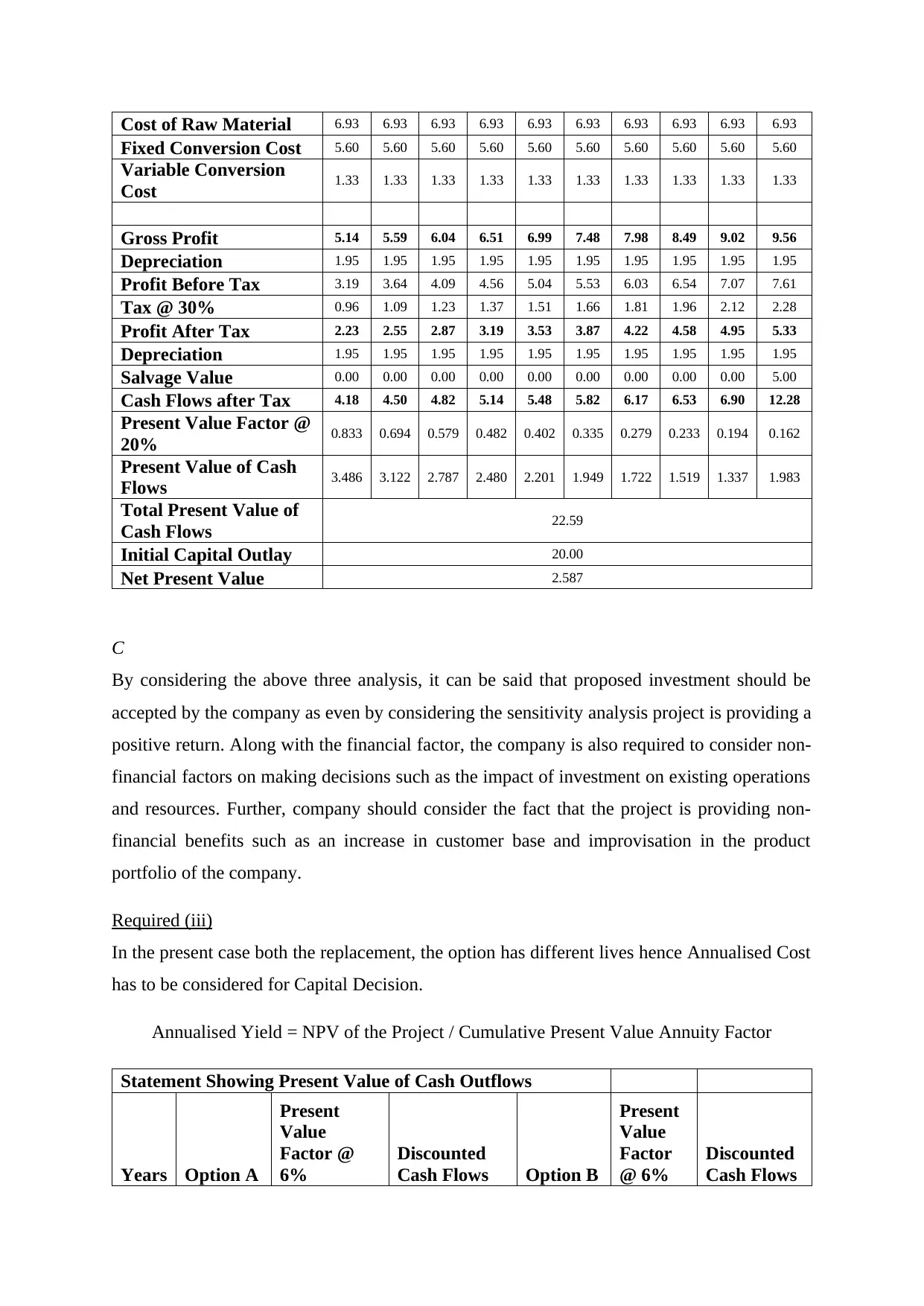

B

(I) Statement Showing Net Present Value and After-tax Cash Flow for the proposed

"Buddy" Capital Investment with 5% less than Estimated (IN Million AUD $)

Particulars Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Unit Sales 15.20 15.20 15.20 15.20 15.20 15.20 15.20 15.20 15.20 15.20

Sales Price per Unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales Revenue 19.00 19.45 19.90 20.37 20.85 21.34 21.84 22.35 22.88 23.42

Cost of Raw Material 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93

Fixed Conversion Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable Conversion

Cost 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33

Gross Profit 5.14 5.59 6.04 6.51 6.99 7.48 7.98 8.49 9.02 9.56

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 3.19 3.64 4.09 4.56 5.04 5.53 6.03 6.54 7.07 7.61

Tax @ 30% 0.96 1.09 1.23 1.37 1.51 1.66 1.81 1.96 2.12 2.28

Profit After Tax 2.23 2.55 2.87 3.19 3.53 3.87 4.22 4.58 4.95 5.33

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.18 4.50 4.82 5.14 5.48 5.82 6.17 6.53 6.90 12.28

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows 3.486 3.122 2.787 2.480 2.201 1.949 1.722 1.519 1.337 1.983

Total Present Value of

Cash Flows 22.59

Initial Capital Outlay 20.00

Net Present Value 2.587

C

By considering the above three analysis, it can be said that proposed investment should be

accepted by the company as even by considering the sensitivity analysis project is providing a

positive return. Along with the financial factor, the company is also required to consider non-

financial factors on making decisions such as the impact of investment on existing operations

and resources. Further, company should consider the fact that the project is providing non-

financial benefits such as an increase in customer base and improvisation in the product

portfolio of the company.

Required (iii)

In the present case both the replacement, the option has different lives hence Annualised Cost

has to be considered for Capital Decision.

Annualised Yield = NPV of the Project / Cumulative Present Value Annuity Factor

Statement Showing Present Value of Cash Outflows

Years Option A

Present

Value

Factor @

6%

Discounted

Cash Flows Option B

Present

Value

Factor

@ 6%

Discounted

Cash Flows

Fixed Conversion Cost 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60 5.60

Variable Conversion

Cost 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33

Gross Profit 5.14 5.59 6.04 6.51 6.99 7.48 7.98 8.49 9.02 9.56

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 3.19 3.64 4.09 4.56 5.04 5.53 6.03 6.54 7.07 7.61

Tax @ 30% 0.96 1.09 1.23 1.37 1.51 1.66 1.81 1.96 2.12 2.28

Profit After Tax 2.23 2.55 2.87 3.19 3.53 3.87 4.22 4.58 4.95 5.33

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Salvage Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.18 4.50 4.82 5.14 5.48 5.82 6.17 6.53 6.90 12.28

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash

Flows 3.486 3.122 2.787 2.480 2.201 1.949 1.722 1.519 1.337 1.983

Total Present Value of

Cash Flows 22.59

Initial Capital Outlay 20.00

Net Present Value 2.587

C

By considering the above three analysis, it can be said that proposed investment should be

accepted by the company as even by considering the sensitivity analysis project is providing a

positive return. Along with the financial factor, the company is also required to consider non-

financial factors on making decisions such as the impact of investment on existing operations

and resources. Further, company should consider the fact that the project is providing non-

financial benefits such as an increase in customer base and improvisation in the product

portfolio of the company.

Required (iii)

In the present case both the replacement, the option has different lives hence Annualised Cost

has to be considered for Capital Decision.

Annualised Yield = NPV of the Project / Cumulative Present Value Annuity Factor

Statement Showing Present Value of Cash Outflows

Years Option A

Present

Value

Factor @

6%

Discounted

Cash Flows Option B

Present

Value

Factor

@ 6%

Discounted

Cash Flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

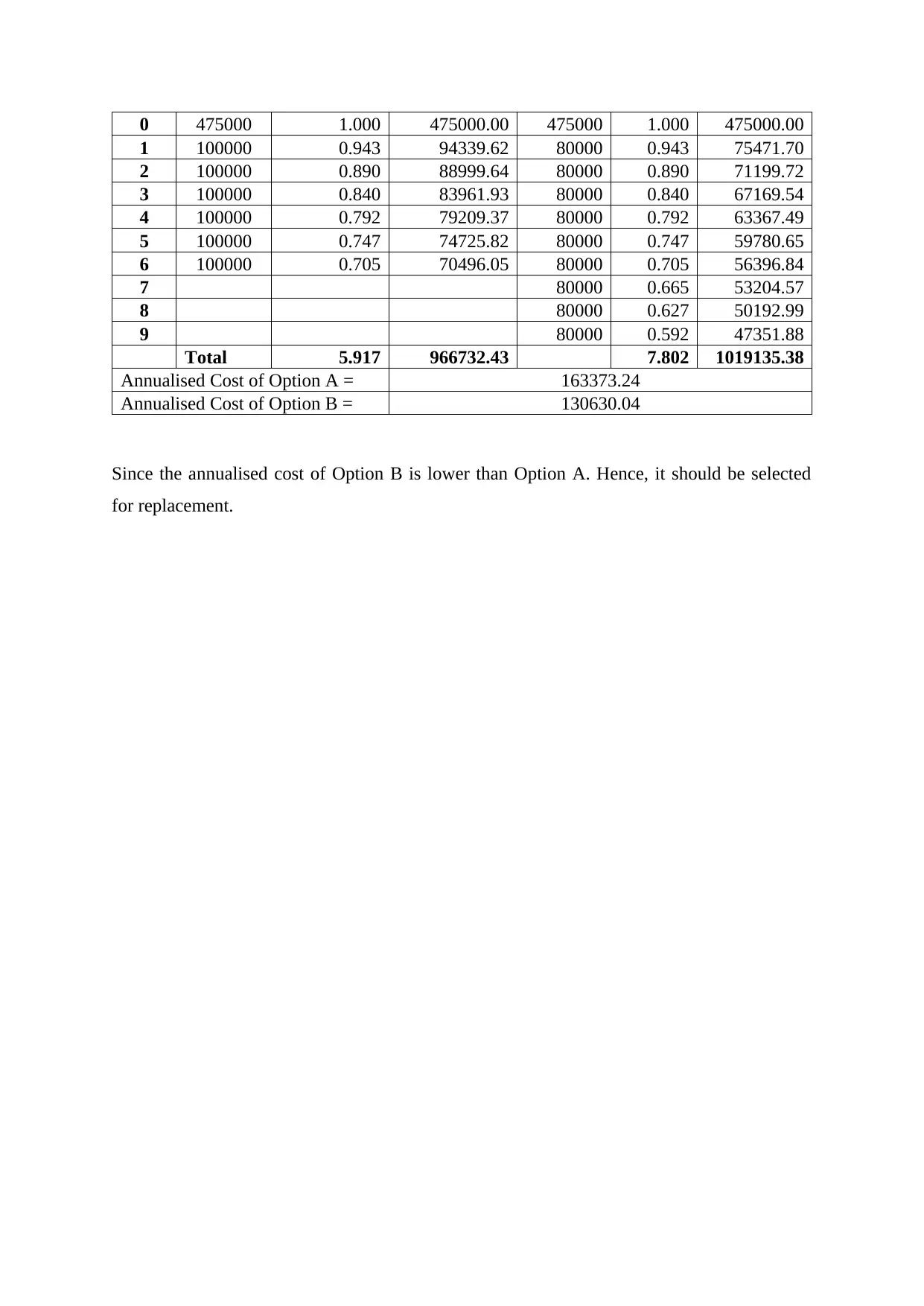

0 475000 1.000 475000.00 475000 1.000 475000.00

1 100000 0.943 94339.62 80000 0.943 75471.70

2 100000 0.890 88999.64 80000 0.890 71199.72

3 100000 0.840 83961.93 80000 0.840 67169.54

4 100000 0.792 79209.37 80000 0.792 63367.49

5 100000 0.747 74725.82 80000 0.747 59780.65

6 100000 0.705 70496.05 80000 0.705 56396.84

7 80000 0.665 53204.57

8 80000 0.627 50192.99

9 80000 0.592 47351.88

Total 5.917 966732.43 7.802 1019135.38

Annualised Cost of Option A = 163373.24

Annualised Cost of Option B = 130630.04

Since the annualised cost of Option B is lower than Option A. Hence, it should be selected

for replacement.

1 100000 0.943 94339.62 80000 0.943 75471.70

2 100000 0.890 88999.64 80000 0.890 71199.72

3 100000 0.840 83961.93 80000 0.840 67169.54

4 100000 0.792 79209.37 80000 0.792 63367.49

5 100000 0.747 74725.82 80000 0.747 59780.65

6 100000 0.705 70496.05 80000 0.705 56396.84

7 80000 0.665 53204.57

8 80000 0.627 50192.99

9 80000 0.592 47351.88

Total 5.917 966732.43 7.802 1019135.38

Annualised Cost of Option A = 163373.24

Annualised Cost of Option B = 130630.04

Since the annualised cost of Option B is lower than Option A. Hence, it should be selected

for replacement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

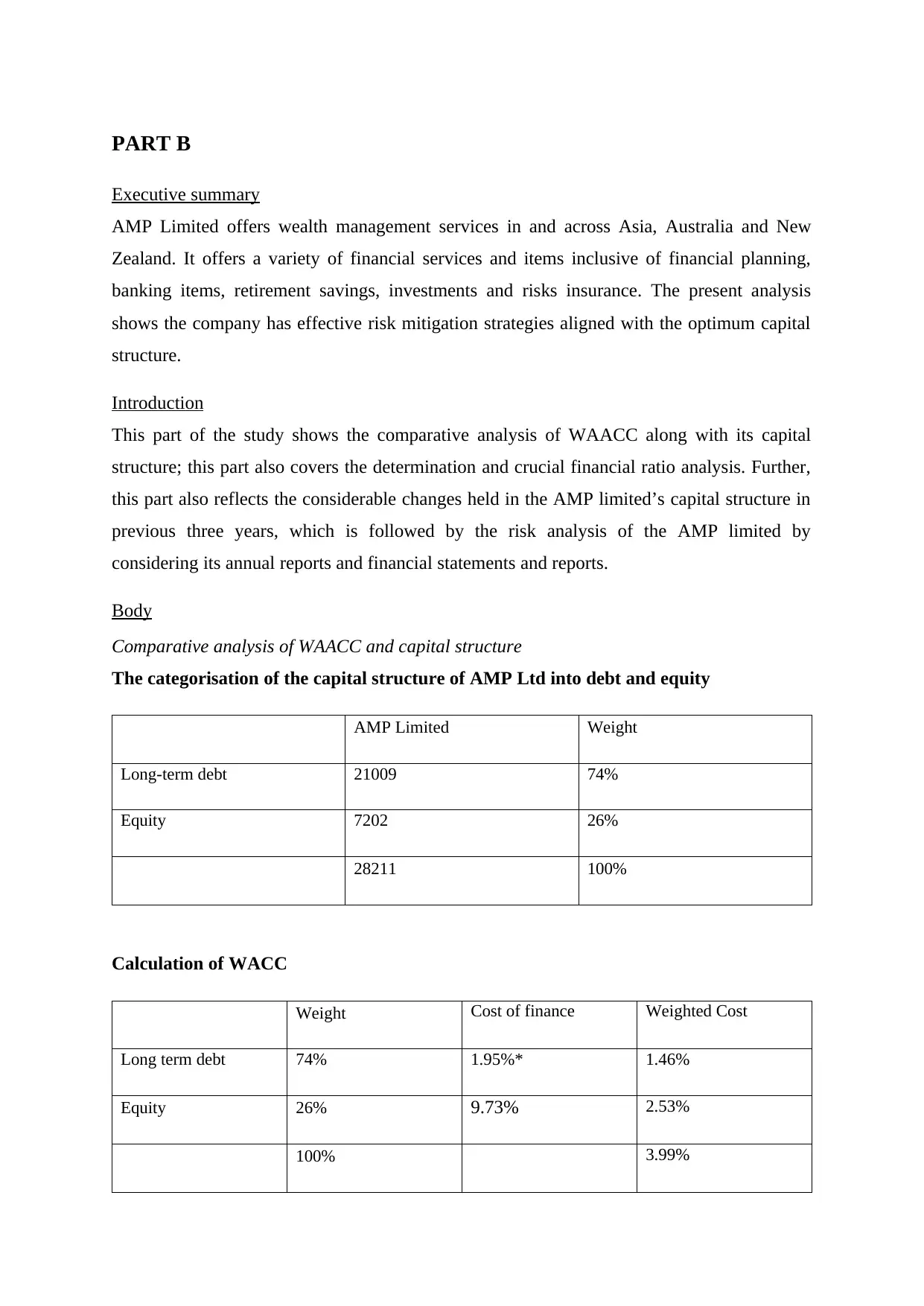

PART B

Executive summary

AMP Limited offers wealth management services in and across Asia, Australia and New

Zealand. It offers a variety of financial services and items inclusive of financial planning,

banking items, retirement savings, investments and risks insurance. The present analysis

shows the company has effective risk mitigation strategies aligned with the optimum capital

structure.

Introduction

This part of the study shows the comparative analysis of WAACC along with its capital

structure; this part also covers the determination and crucial financial ratio analysis. Further,

this part also reflects the considerable changes held in the AMP limited’s capital structure in

previous three years, which is followed by the risk analysis of the AMP limited by

considering its annual reports and financial statements and reports.

Body

Comparative analysis of WAACC and capital structure

The categorisation of the capital structure of AMP Ltd into debt and equity

AMP Limited Weight

Long-term debt 21009 74%

Equity 7202 26%

28211 100%

Calculation of WACC

Weight Cost of finance Weighted Cost

Long term debt 74% 1.95%* 1.46%

Equity 26% 9.73% 2.53%

100% 3.99%

Executive summary

AMP Limited offers wealth management services in and across Asia, Australia and New

Zealand. It offers a variety of financial services and items inclusive of financial planning,

banking items, retirement savings, investments and risks insurance. The present analysis

shows the company has effective risk mitigation strategies aligned with the optimum capital

structure.

Introduction

This part of the study shows the comparative analysis of WAACC along with its capital

structure; this part also covers the determination and crucial financial ratio analysis. Further,

this part also reflects the considerable changes held in the AMP limited’s capital structure in

previous three years, which is followed by the risk analysis of the AMP limited by

considering its annual reports and financial statements and reports.

Body

Comparative analysis of WAACC and capital structure

The categorisation of the capital structure of AMP Ltd into debt and equity

AMP Limited Weight

Long-term debt 21009 74%

Equity 7202 26%

28211 100%

Calculation of WACC

Weight Cost of finance Weighted Cost

Long term debt 74% 1.95%* 1.46%

Equity 26% 9.73% 2.53%

100% 3.99%

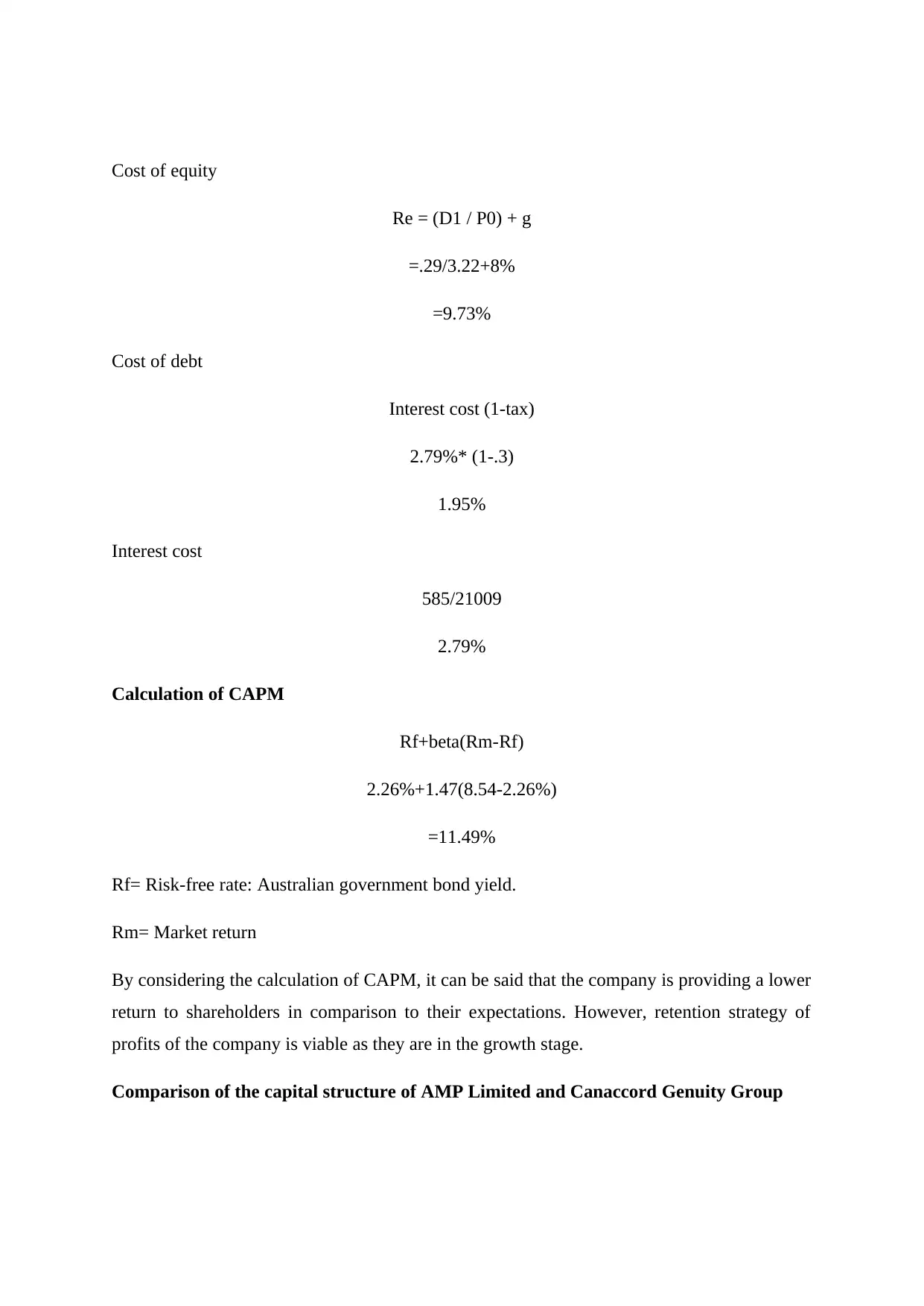

Cost of equity

Re = (D1 / P0) + g

=.29/3.22+8%

=9.73%

Cost of debt

Interest cost (1-tax)

2.79%* (1-.3)

1.95%

Interest cost

585/21009

2.79%

Calculation of CAPM

Rf+beta(Rm-Rf)

2.26%+1.47(8.54-2.26%)

=11.49%

Rf= Risk-free rate: Australian government bond yield.

Rm= Market return

By considering the calculation of CAPM, it can be said that the company is providing a lower

return to shareholders in comparison to their expectations. However, retention strategy of

profits of the company is viable as they are in the growth stage.

Comparison of the capital structure of AMP Limited and Canaccord Genuity Group

Re = (D1 / P0) + g

=.29/3.22+8%

=9.73%

Cost of debt

Interest cost (1-tax)

2.79%* (1-.3)

1.95%

Interest cost

585/21009

2.79%

Calculation of CAPM

Rf+beta(Rm-Rf)

2.26%+1.47(8.54-2.26%)

=11.49%

Rf= Risk-free rate: Australian government bond yield.

Rm= Market return

By considering the calculation of CAPM, it can be said that the company is providing a lower

return to shareholders in comparison to their expectations. However, retention strategy of

profits of the company is viable as they are in the growth stage.

Comparison of the capital structure of AMP Limited and Canaccord Genuity Group

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

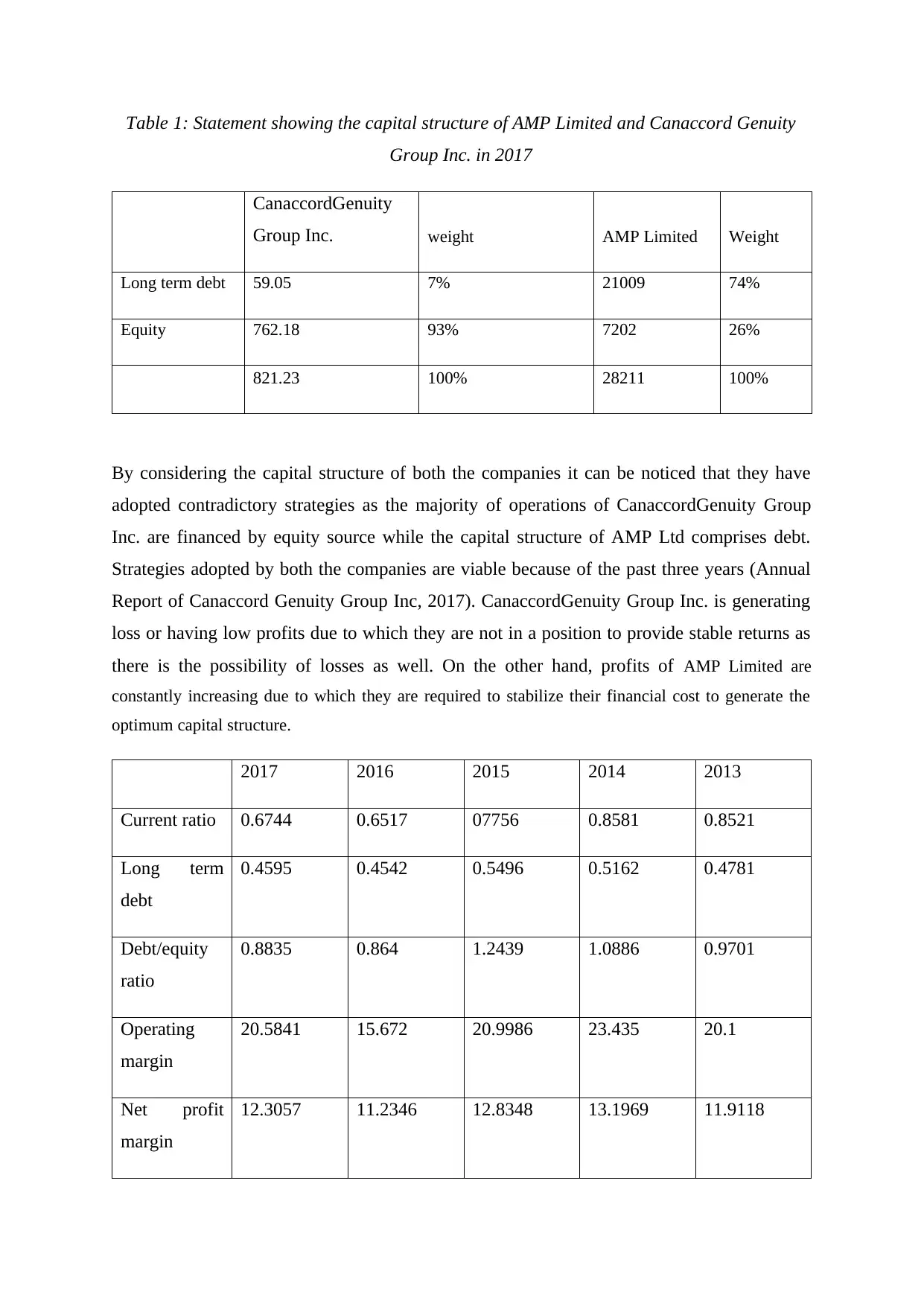

Table 1: Statement showing the capital structure of AMP Limited and Canaccord Genuity

Group Inc. in 2017

CanaccordGenuity

Group Inc. weight AMP Limited Weight

Long term debt 59.05 7% 21009 74%

Equity 762.18 93% 7202 26%

821.23 100% 28211 100%

By considering the capital structure of both the companies it can be noticed that they have

adopted contradictory strategies as the majority of operations of CanaccordGenuity Group

Inc. are financed by equity source while the capital structure of AMP Ltd comprises debt.

Strategies adopted by both the companies are viable because of the past three years (Annual

Report of Canaccord Genuity Group Inc, 2017). CanaccordGenuity Group Inc. is generating

loss or having low profits due to which they are not in a position to provide stable returns as

there is the possibility of losses as well. On the other hand, profits of AMP Limited are

constantly increasing due to which they are required to stabilize their financial cost to generate the

optimum capital structure.

2017 2016 2015 2014 2013

Current ratio 0.6744 0.6517 07756 0.8581 0.8521

Long term

debt

0.4595 0.4542 0.5496 0.5162 0.4781

Debt/equity

ratio

0.8835 0.864 1.2439 1.0886 0.9701

Operating

margin

20.5841 15.672 20.9986 23.435 20.1

Net profit

margin

12.3057 11.2346 12.8348 13.1969 11.9118

Group Inc. in 2017

CanaccordGenuity

Group Inc. weight AMP Limited Weight

Long term debt 59.05 7% 21009 74%

Equity 762.18 93% 7202 26%

821.23 100% 28211 100%

By considering the capital structure of both the companies it can be noticed that they have

adopted contradictory strategies as the majority of operations of CanaccordGenuity Group

Inc. are financed by equity source while the capital structure of AMP Ltd comprises debt.

Strategies adopted by both the companies are viable because of the past three years (Annual

Report of Canaccord Genuity Group Inc, 2017). CanaccordGenuity Group Inc. is generating

loss or having low profits due to which they are not in a position to provide stable returns as

there is the possibility of losses as well. On the other hand, profits of AMP Limited are

constantly increasing due to which they are required to stabilize their financial cost to generate the

optimum capital structure.

2017 2016 2015 2014 2013

Current ratio 0.6744 0.6517 07756 0.8581 0.8521

Long term

debt

0.4595 0.4542 0.5496 0.5162 0.4781

Debt/equity

ratio

0.8835 0.864 1.2439 1.0886 0.9701

Operating

margin

20.5841 15.672 20.9986 23.435 20.1

Net profit

margin

12.3057 11.2346 12.8348 13.1969 11.9118

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

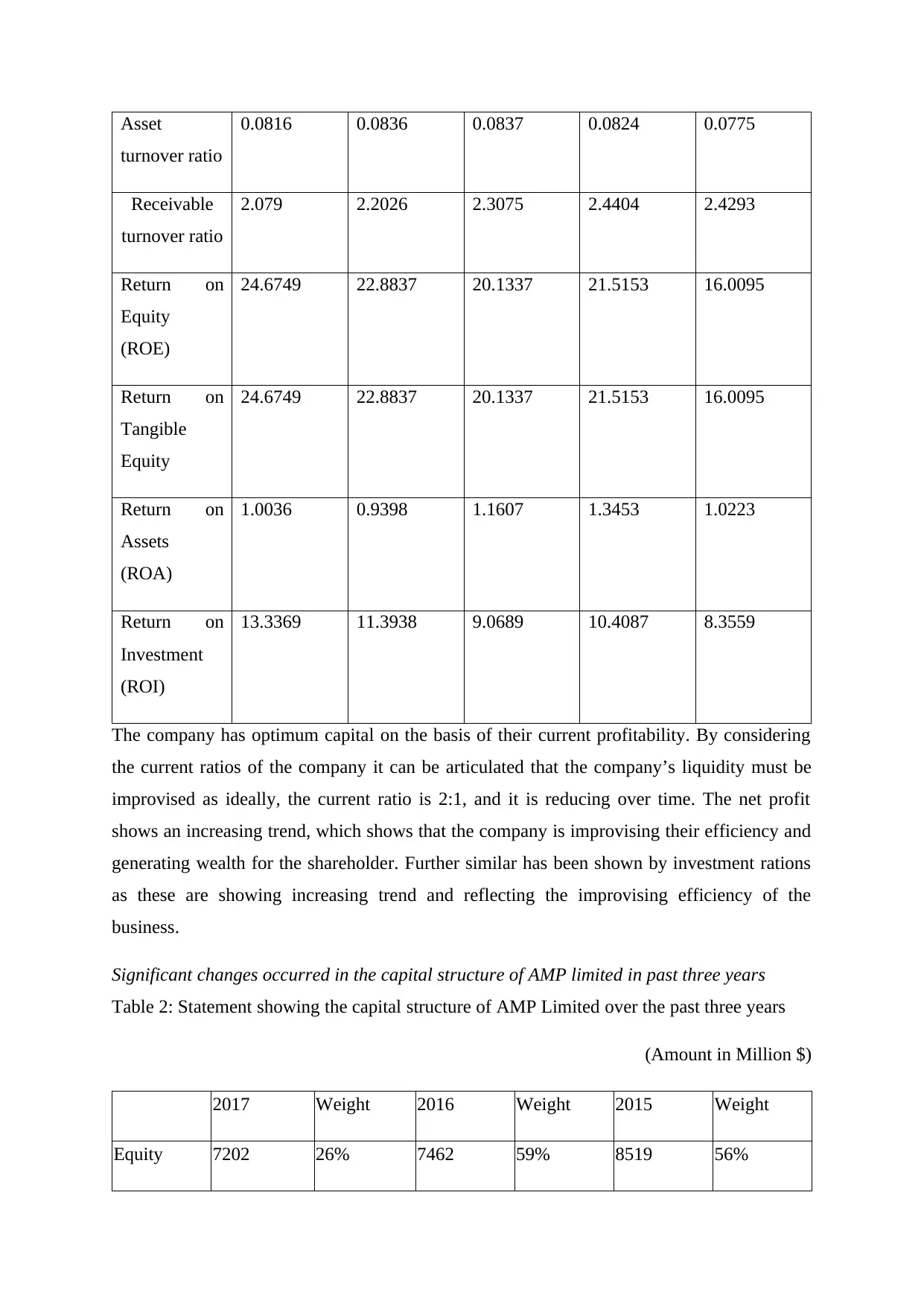

Asset

turnover ratio

0.0816 0.0836 0.0837 0.0824 0.0775

Receivable

turnover ratio

2.079 2.2026 2.3075 2.4404 2.4293

Return on

Equity

(ROE)

24.6749 22.8837 20.1337 21.5153 16.0095

Return on

Tangible

Equity

24.6749 22.8837 20.1337 21.5153 16.0095

Return on

Assets

(ROA)

1.0036 0.9398 1.1607 1.3453 1.0223

Return on

Investment

(ROI)

13.3369 11.3938 9.0689 10.4087 8.3559

The company has optimum capital on the basis of their current profitability. By considering

the current ratios of the company it can be articulated that the company’s liquidity must be

improvised as ideally, the current ratio is 2:1, and it is reducing over time. The net profit

shows an increasing trend, which shows that the company is improvising their efficiency and

generating wealth for the shareholder. Further similar has been shown by investment rations

as these are showing increasing trend and reflecting the improvising efficiency of the

business.

Significant changes occurred in the capital structure of AMP limited in past three years

Table 2: Statement showing the capital structure of AMP Limited over the past three years

(Amount in Million $)

2017 Weight 2016 Weight 2015 Weight

Equity 7202 26% 7462 59% 8519 56%

turnover ratio

0.0816 0.0836 0.0837 0.0824 0.0775

Receivable

turnover ratio

2.079 2.2026 2.3075 2.4404 2.4293

Return on

Equity

(ROE)

24.6749 22.8837 20.1337 21.5153 16.0095

Return on

Tangible

Equity

24.6749 22.8837 20.1337 21.5153 16.0095

Return on

Assets

(ROA)

1.0036 0.9398 1.1607 1.3453 1.0223

Return on

Investment

(ROI)

13.3369 11.3938 9.0689 10.4087 8.3559

The company has optimum capital on the basis of their current profitability. By considering

the current ratios of the company it can be articulated that the company’s liquidity must be

improvised as ideally, the current ratio is 2:1, and it is reducing over time. The net profit

shows an increasing trend, which shows that the company is improvising their efficiency and

generating wealth for the shareholder. Further similar has been shown by investment rations

as these are showing increasing trend and reflecting the improvising efficiency of the

business.

Significant changes occurred in the capital structure of AMP limited in past three years

Table 2: Statement showing the capital structure of AMP Limited over the past three years

(Amount in Million $)

2017 Weight 2016 Weight 2015 Weight

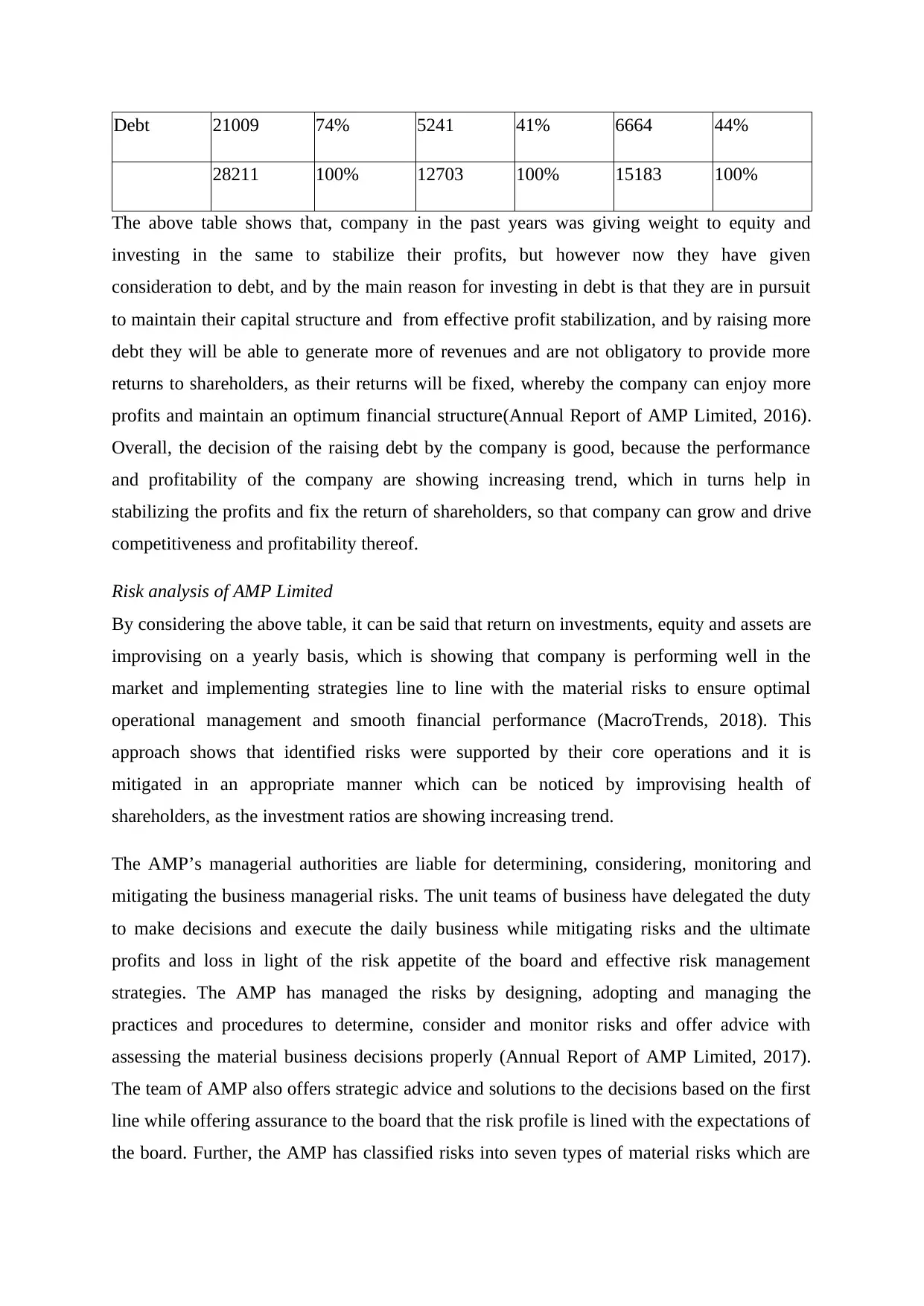

Equity 7202 26% 7462 59% 8519 56%

Debt 21009 74% 5241 41% 6664 44%

28211 100% 12703 100% 15183 100%

The above table shows that, company in the past years was giving weight to equity and

investing in the same to stabilize their profits, but however now they have given

consideration to debt, and by the main reason for investing in debt is that they are in pursuit

to maintain their capital structure and from effective profit stabilization, and by raising more

debt they will be able to generate more of revenues and are not obligatory to provide more

returns to shareholders, as their returns will be fixed, whereby the company can enjoy more

profits and maintain an optimum financial structure(Annual Report of AMP Limited, 2016).

Overall, the decision of the raising debt by the company is good, because the performance

and profitability of the company are showing increasing trend, which in turns help in

stabilizing the profits and fix the return of shareholders, so that company can grow and drive

competitiveness and profitability thereof.

Risk analysis of AMP Limited

By considering the above table, it can be said that return on investments, equity and assets are

improvising on a yearly basis, which is showing that company is performing well in the

market and implementing strategies line to line with the material risks to ensure optimal

operational management and smooth financial performance (MacroTrends, 2018). This

approach shows that identified risks were supported by their core operations and it is

mitigated in an appropriate manner which can be noticed by improvising health of

shareholders, as the investment ratios are showing increasing trend.

The AMP’s managerial authorities are liable for determining, considering, monitoring and

mitigating the business managerial risks. The unit teams of business have delegated the duty

to make decisions and execute the daily business while mitigating risks and the ultimate

profits and loss in light of the risk appetite of the board and effective risk management

strategies. The AMP has managed the risks by designing, adopting and managing the

practices and procedures to determine, consider and monitor risks and offer advice with

assessing the material business decisions properly (Annual Report of AMP Limited, 2017).

The team of AMP also offers strategic advice and solutions to the decisions based on the first

line while offering assurance to the board that the risk profile is lined with the expectations of

the board. Further, the AMP has classified risks into seven types of material risks which are

28211 100% 12703 100% 15183 100%

The above table shows that, company in the past years was giving weight to equity and

investing in the same to stabilize their profits, but however now they have given

consideration to debt, and by the main reason for investing in debt is that they are in pursuit

to maintain their capital structure and from effective profit stabilization, and by raising more

debt they will be able to generate more of revenues and are not obligatory to provide more

returns to shareholders, as their returns will be fixed, whereby the company can enjoy more

profits and maintain an optimum financial structure(Annual Report of AMP Limited, 2016).

Overall, the decision of the raising debt by the company is good, because the performance

and profitability of the company are showing increasing trend, which in turns help in

stabilizing the profits and fix the return of shareholders, so that company can grow and drive

competitiveness and profitability thereof.

Risk analysis of AMP Limited

By considering the above table, it can be said that return on investments, equity and assets are

improvising on a yearly basis, which is showing that company is performing well in the

market and implementing strategies line to line with the material risks to ensure optimal

operational management and smooth financial performance (MacroTrends, 2018). This

approach shows that identified risks were supported by their core operations and it is

mitigated in an appropriate manner which can be noticed by improvising health of

shareholders, as the investment ratios are showing increasing trend.

The AMP’s managerial authorities are liable for determining, considering, monitoring and

mitigating the business managerial risks. The unit teams of business have delegated the duty

to make decisions and execute the daily business while mitigating risks and the ultimate

profits and loss in light of the risk appetite of the board and effective risk management

strategies. The AMP has managed the risks by designing, adopting and managing the

practices and procedures to determine, consider and monitor risks and offer advice with

assessing the material business decisions properly (Annual Report of AMP Limited, 2017).

The team of AMP also offers strategic advice and solutions to the decisions based on the first

line while offering assurance to the board that the risk profile is lined with the expectations of

the board. Further, the AMP has classified risks into seven types of material risks which are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.