Capital Budgeting: Investment Analysis for SSHA New Model in Finance

VerifiedAdded on 2023/06/11

|12

|2503

|434

Report

AI Summary

This report assesses the financial viability of Booli Enterprise's new Smart Speaker and Home Assistant (SSHA) model using several capital budgeting techniques. It calculates the non-discounted payback period, profitability index (PI), internal rate of return (IRR), and net present value (NPV) to determine the project's acceptability. Sensitivity analysis is conducted to evaluate the impact of changes in selling price and quantity on the project's NPV. The analysis reveals a positive NPV, a PI of 1.65, a payback period of 2.14 years, and an IRR of 19.7%, leading to the conclusion that the project is financially viable and should be pursued. The report also recommends incorporating potential losses from other products into the investment amount for a more accurate assessment and suggests that the project should only be accepted if the adjusted NPV remains positive.

Running head: BUSINESS FINANCE

Business finance

Name of the student

Name of the university

Student ID

Author note

Business finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS FINANCE

Table of Contents

Introduction................................................................................................................................2

1. Non-discounted payback period.........................................................................................2

2. Profitability index...............................................................................................................3

3. Internal rate of return..........................................................................................................3

4. Net present value................................................................................................................3

5. Sensitivity analysis for price change..................................................................................4

6. Sensitivity analysis for price change..................................................................................6

7. Conclusion..........................................................................................................................8

8. Recommendation................................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

1. Non-discounted payback period.........................................................................................2

2. Profitability index...............................................................................................................3

3. Internal rate of return..........................................................................................................3

4. Net present value................................................................................................................3

5. Sensitivity analysis for price change..................................................................................4

6. Sensitivity analysis for price change..................................................................................6

7. Conclusion..........................................................................................................................8

8. Recommendation................................................................................................................8

Reference....................................................................................................................................9

2BUSINESS FINANCE

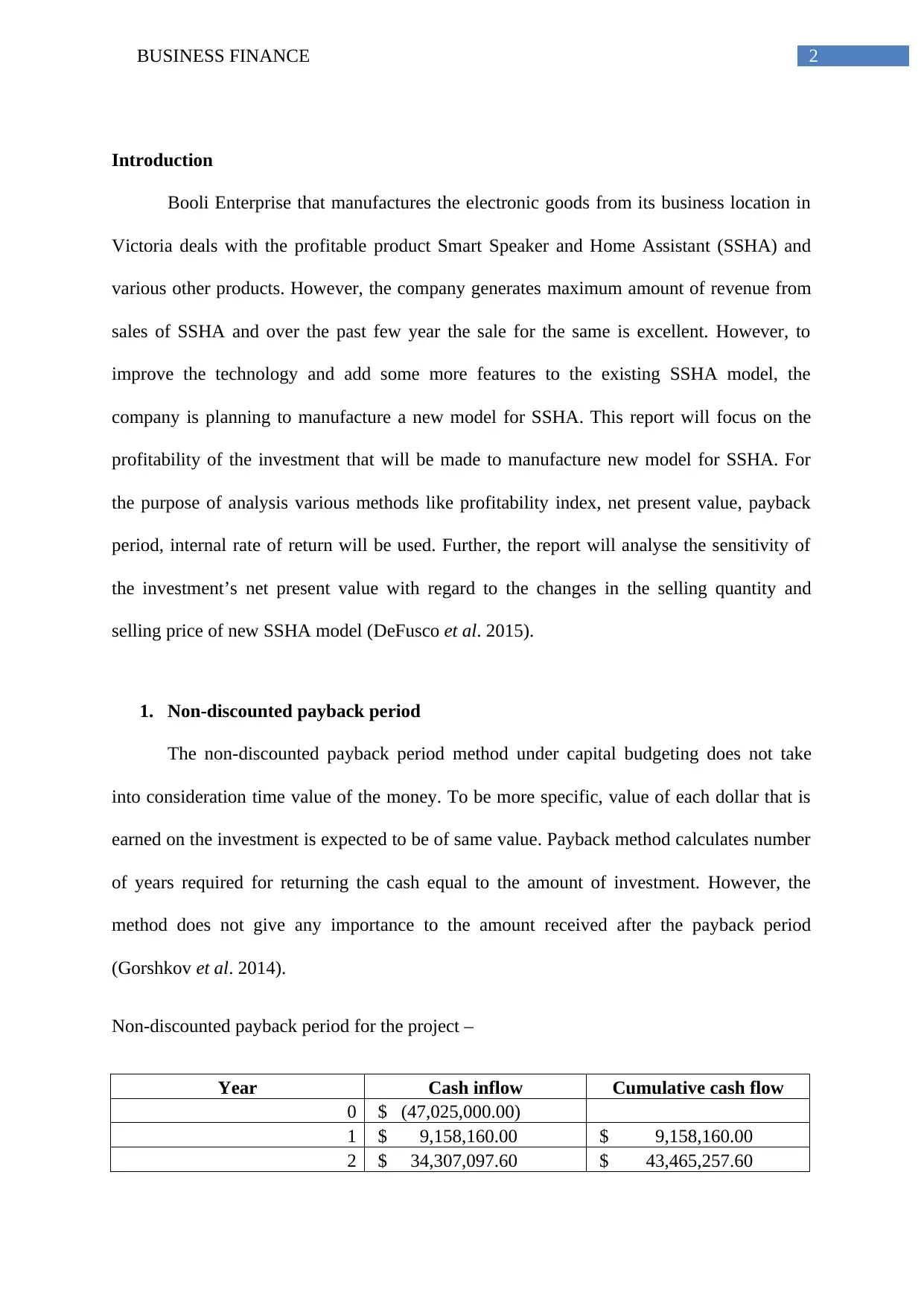

Introduction

Booli Enterprise that manufactures the electronic goods from its business location in

Victoria deals with the profitable product Smart Speaker and Home Assistant (SSHA) and

various other products. However, the company generates maximum amount of revenue from

sales of SSHA and over the past few year the sale for the same is excellent. However, to

improve the technology and add some more features to the existing SSHA model, the

company is planning to manufacture a new model for SSHA. This report will focus on the

profitability of the investment that will be made to manufacture new model for SSHA. For

the purpose of analysis various methods like profitability index, net present value, payback

period, internal rate of return will be used. Further, the report will analyse the sensitivity of

the investment’s net present value with regard to the changes in the selling quantity and

selling price of new SSHA model (DeFusco et al. 2015).

1. Non-discounted payback period

The non-discounted payback period method under capital budgeting does not take

into consideration time value of the money. To be more specific, value of each dollar that is

earned on the investment is expected to be of same value. Payback method calculates number

of years required for returning the cash equal to the amount of investment. However, the

method does not give any importance to the amount received after the payback period

(Gorshkov et al. 2014).

Non-discounted payback period for the project –

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

Introduction

Booli Enterprise that manufactures the electronic goods from its business location in

Victoria deals with the profitable product Smart Speaker and Home Assistant (SSHA) and

various other products. However, the company generates maximum amount of revenue from

sales of SSHA and over the past few year the sale for the same is excellent. However, to

improve the technology and add some more features to the existing SSHA model, the

company is planning to manufacture a new model for SSHA. This report will focus on the

profitability of the investment that will be made to manufacture new model for SSHA. For

the purpose of analysis various methods like profitability index, net present value, payback

period, internal rate of return will be used. Further, the report will analyse the sensitivity of

the investment’s net present value with regard to the changes in the selling quantity and

selling price of new SSHA model (DeFusco et al. 2015).

1. Non-discounted payback period

The non-discounted payback period method under capital budgeting does not take

into consideration time value of the money. To be more specific, value of each dollar that is

earned on the investment is expected to be of same value. Payback method calculates number

of years required for returning the cash equal to the amount of investment. However, the

method does not give any importance to the amount received after the payback period

(Gorshkov et al. 2014).

Non-discounted payback period for the project –

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS FINANCE

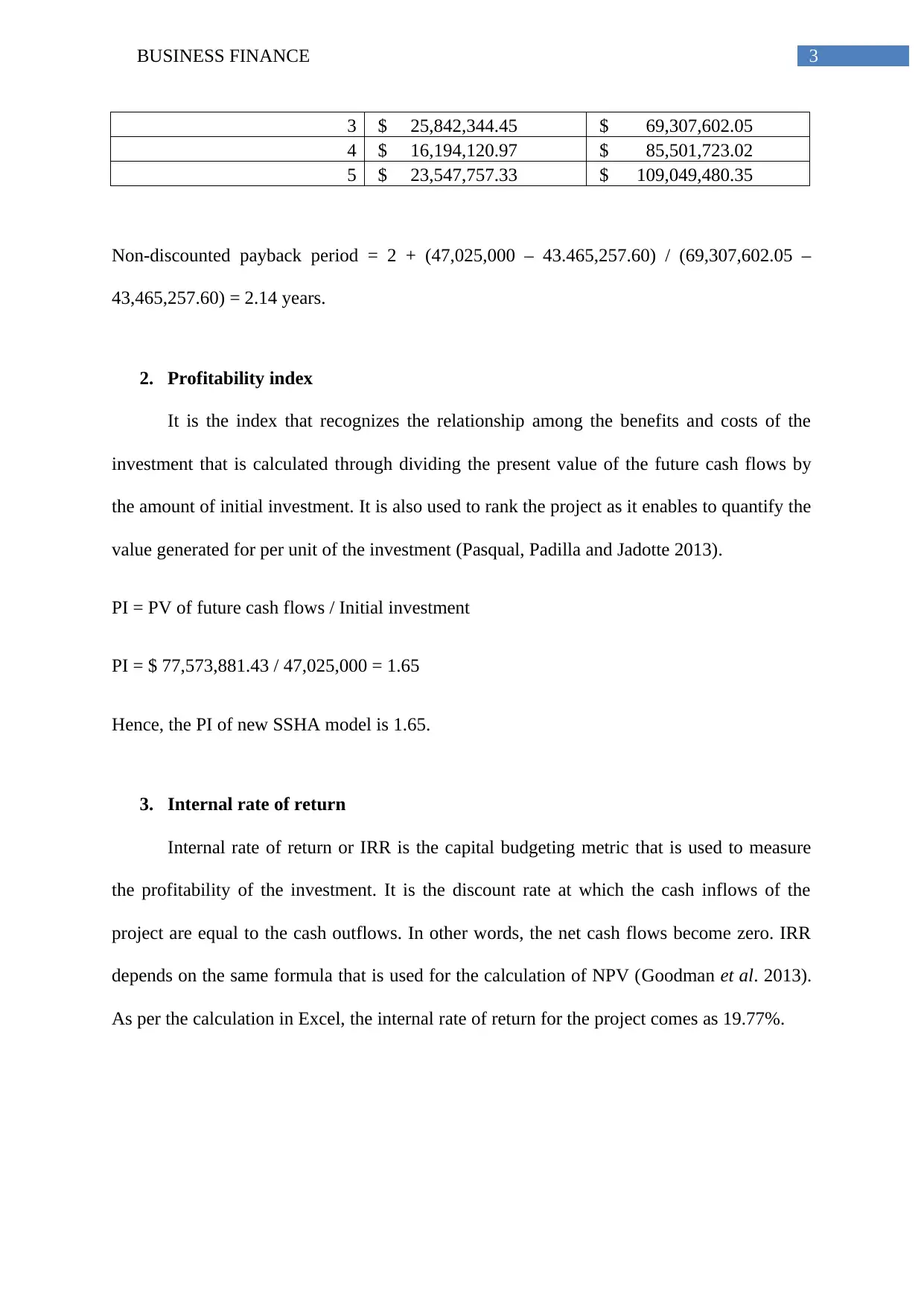

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

2. Profitability index

It is the index that recognizes the relationship among the benefits and costs of the

investment that is calculated through dividing the present value of the future cash flows by

the amount of initial investment. It is also used to rank the project as it enables to quantify the

value generated for per unit of the investment (Pasqual, Padilla and Jadotte 2013).

PI = PV of future cash flows / Initial investment

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Hence, the PI of new SSHA model is 1.65.

3. Internal rate of return

Internal rate of return or IRR is the capital budgeting metric that is used to measure

the profitability of the investment. It is the discount rate at which the cash inflows of the

project are equal to the cash outflows. In other words, the net cash flows become zero. IRR

depends on the same formula that is used for the calculation of NPV (Goodman et al. 2013).

As per the calculation in Excel, the internal rate of return for the project comes as 19.77%.

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

2. Profitability index

It is the index that recognizes the relationship among the benefits and costs of the

investment that is calculated through dividing the present value of the future cash flows by

the amount of initial investment. It is also used to rank the project as it enables to quantify the

value generated for per unit of the investment (Pasqual, Padilla and Jadotte 2013).

PI = PV of future cash flows / Initial investment

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Hence, the PI of new SSHA model is 1.65.

3. Internal rate of return

Internal rate of return or IRR is the capital budgeting metric that is used to measure

the profitability of the investment. It is the discount rate at which the cash inflows of the

project are equal to the cash outflows. In other words, the net cash flows become zero. IRR

depends on the same formula that is used for the calculation of NPV (Goodman et al. 2013).

As per the calculation in Excel, the internal rate of return for the project comes as 19.77%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS FINANCE

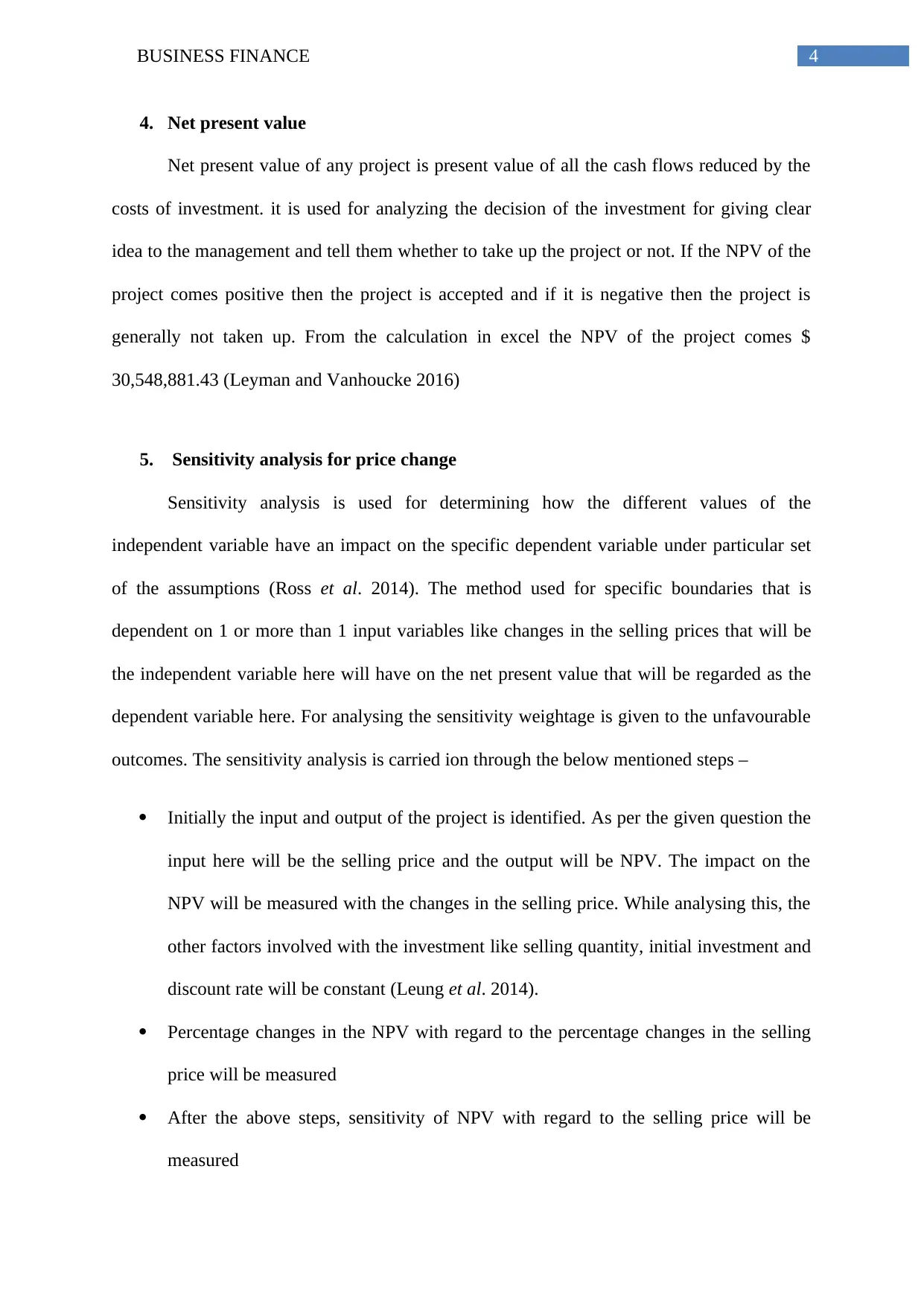

4. Net present value

Net present value of any project is present value of all the cash flows reduced by the

costs of investment. it is used for analyzing the decision of the investment for giving clear

idea to the management and tell them whether to take up the project or not. If the NPV of the

project comes positive then the project is accepted and if it is negative then the project is

generally not taken up. From the calculation in excel the NPV of the project comes $

30,548,881.43 (Leyman and Vanhoucke 2016)

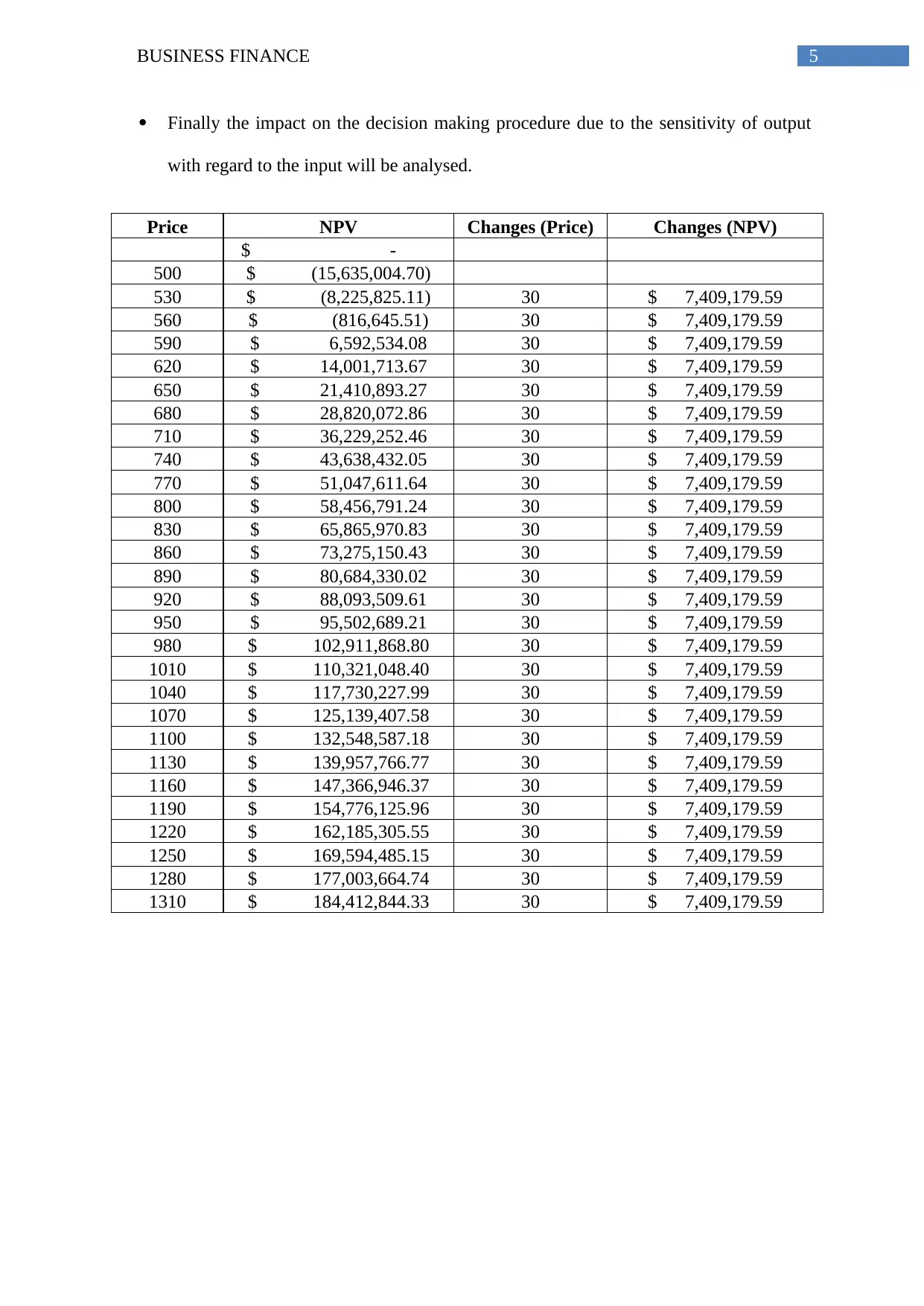

5. Sensitivity analysis for price change

Sensitivity analysis is used for determining how the different values of the

independent variable have an impact on the specific dependent variable under particular set

of the assumptions (Ross et al. 2014). The method used for specific boundaries that is

dependent on 1 or more than 1 input variables like changes in the selling prices that will be

the independent variable here will have on the net present value that will be regarded as the

dependent variable here. For analysing the sensitivity weightage is given to the unfavourable

outcomes. The sensitivity analysis is carried ion through the below mentioned steps –

Initially the input and output of the project is identified. As per the given question the

input here will be the selling price and the output will be NPV. The impact on the

NPV will be measured with the changes in the selling price. While analysing this, the

other factors involved with the investment like selling quantity, initial investment and

discount rate will be constant (Leung et al. 2014).

Percentage changes in the NPV with regard to the percentage changes in the selling

price will be measured

After the above steps, sensitivity of NPV with regard to the selling price will be

measured

4. Net present value

Net present value of any project is present value of all the cash flows reduced by the

costs of investment. it is used for analyzing the decision of the investment for giving clear

idea to the management and tell them whether to take up the project or not. If the NPV of the

project comes positive then the project is accepted and if it is negative then the project is

generally not taken up. From the calculation in excel the NPV of the project comes $

30,548,881.43 (Leyman and Vanhoucke 2016)

5. Sensitivity analysis for price change

Sensitivity analysis is used for determining how the different values of the

independent variable have an impact on the specific dependent variable under particular set

of the assumptions (Ross et al. 2014). The method used for specific boundaries that is

dependent on 1 or more than 1 input variables like changes in the selling prices that will be

the independent variable here will have on the net present value that will be regarded as the

dependent variable here. For analysing the sensitivity weightage is given to the unfavourable

outcomes. The sensitivity analysis is carried ion through the below mentioned steps –

Initially the input and output of the project is identified. As per the given question the

input here will be the selling price and the output will be NPV. The impact on the

NPV will be measured with the changes in the selling price. While analysing this, the

other factors involved with the investment like selling quantity, initial investment and

discount rate will be constant (Leung et al. 2014).

Percentage changes in the NPV with regard to the percentage changes in the selling

price will be measured

After the above steps, sensitivity of NPV with regard to the selling price will be

measured

5BUSINESS FINANCE

Finally the impact on the decision making procedure due to the sensitivity of output

with regard to the input will be analysed.

Price NPV Changes (Price) Changes (NPV)

$ -

500 $ (15,635,004.70)

530 $ (8,225,825.11) 30 $ 7,409,179.59

560 $ (816,645.51) 30 $ 7,409,179.59

590 $ 6,592,534.08 30 $ 7,409,179.59

620 $ 14,001,713.67 30 $ 7,409,179.59

650 $ 21,410,893.27 30 $ 7,409,179.59

680 $ 28,820,072.86 30 $ 7,409,179.59

710 $ 36,229,252.46 30 $ 7,409,179.59

740 $ 43,638,432.05 30 $ 7,409,179.59

770 $ 51,047,611.64 30 $ 7,409,179.59

800 $ 58,456,791.24 30 $ 7,409,179.59

830 $ 65,865,970.83 30 $ 7,409,179.59

860 $ 73,275,150.43 30 $ 7,409,179.59

890 $ 80,684,330.02 30 $ 7,409,179.59

920 $ 88,093,509.61 30 $ 7,409,179.59

950 $ 95,502,689.21 30 $ 7,409,179.59

980 $ 102,911,868.80 30 $ 7,409,179.59

1010 $ 110,321,048.40 30 $ 7,409,179.59

1040 $ 117,730,227.99 30 $ 7,409,179.59

1070 $ 125,139,407.58 30 $ 7,409,179.59

1100 $ 132,548,587.18 30 $ 7,409,179.59

1130 $ 139,957,766.77 30 $ 7,409,179.59

1160 $ 147,366,946.37 30 $ 7,409,179.59

1190 $ 154,776,125.96 30 $ 7,409,179.59

1220 $ 162,185,305.55 30 $ 7,409,179.59

1250 $ 169,594,485.15 30 $ 7,409,179.59

1280 $ 177,003,664.74 30 $ 7,409,179.59

1310 $ 184,412,844.33 30 $ 7,409,179.59

Finally the impact on the decision making procedure due to the sensitivity of output

with regard to the input will be analysed.

Price NPV Changes (Price) Changes (NPV)

$ -

500 $ (15,635,004.70)

530 $ (8,225,825.11) 30 $ 7,409,179.59

560 $ (816,645.51) 30 $ 7,409,179.59

590 $ 6,592,534.08 30 $ 7,409,179.59

620 $ 14,001,713.67 30 $ 7,409,179.59

650 $ 21,410,893.27 30 $ 7,409,179.59

680 $ 28,820,072.86 30 $ 7,409,179.59

710 $ 36,229,252.46 30 $ 7,409,179.59

740 $ 43,638,432.05 30 $ 7,409,179.59

770 $ 51,047,611.64 30 $ 7,409,179.59

800 $ 58,456,791.24 30 $ 7,409,179.59

830 $ 65,865,970.83 30 $ 7,409,179.59

860 $ 73,275,150.43 30 $ 7,409,179.59

890 $ 80,684,330.02 30 $ 7,409,179.59

920 $ 88,093,509.61 30 $ 7,409,179.59

950 $ 95,502,689.21 30 $ 7,409,179.59

980 $ 102,911,868.80 30 $ 7,409,179.59

1010 $ 110,321,048.40 30 $ 7,409,179.59

1040 $ 117,730,227.99 30 $ 7,409,179.59

1070 $ 125,139,407.58 30 $ 7,409,179.59

1100 $ 132,548,587.18 30 $ 7,409,179.59

1130 $ 139,957,766.77 30 $ 7,409,179.59

1160 $ 147,366,946.37 30 $ 7,409,179.59

1190 $ 154,776,125.96 30 $ 7,409,179.59

1220 $ 162,185,305.55 30 $ 7,409,179.59

1250 $ 169,594,485.15 30 $ 7,409,179.59

1280 $ 177,003,664.74 30 $ 7,409,179.59

1310 $ 184,412,844.33 30 $ 7,409,179.59

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS FINANCE

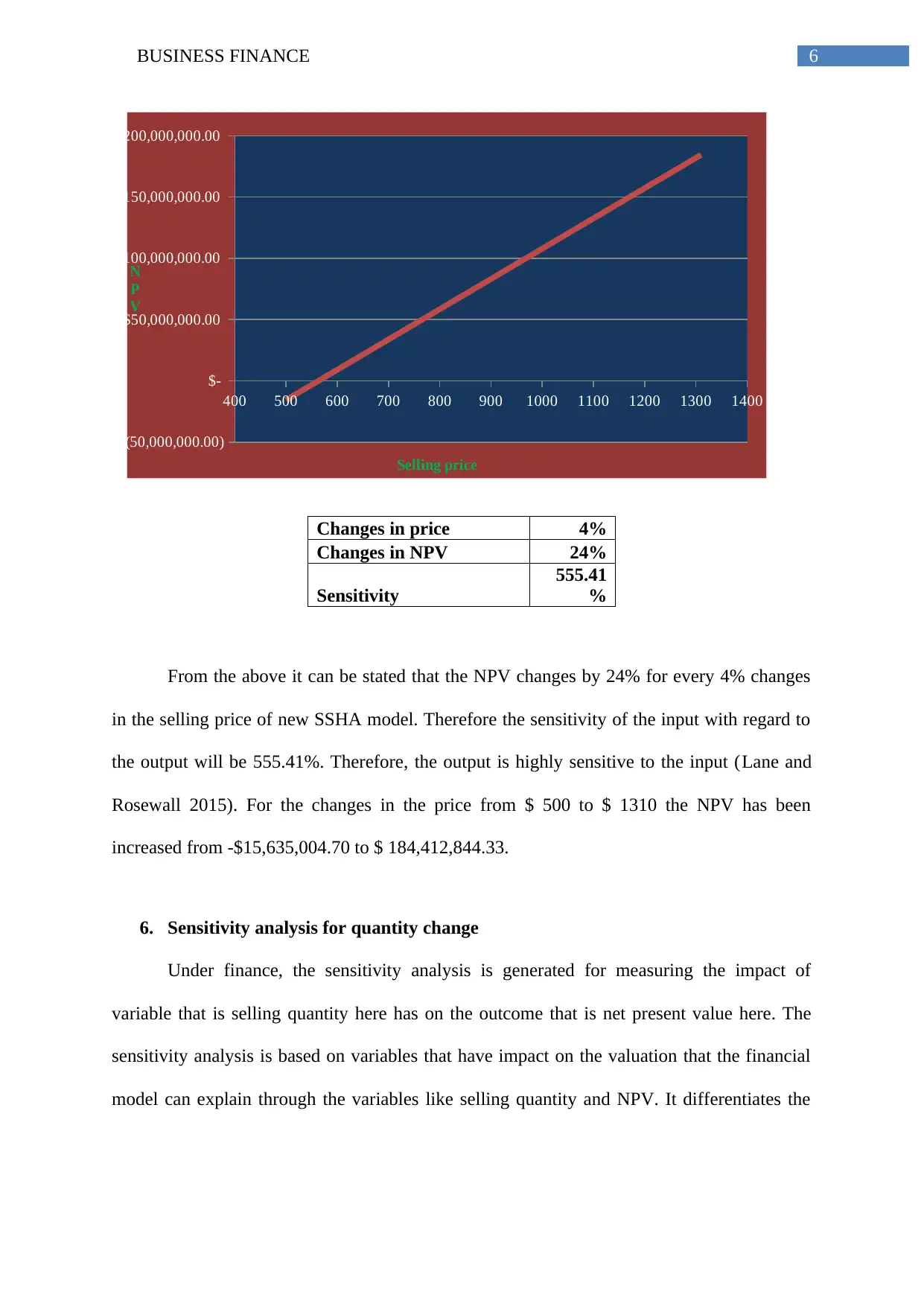

400 500 600 700 800 900 1000 1100 1200 1300 1400

$(50,000,000.00)

$-

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

Selling price

N

P

V

Changes in price 4%

Changes in NPV 24%

Sensitivity

555.41

%

From the above it can be stated that the NPV changes by 24% for every 4% changes

in the selling price of new SSHA model. Therefore the sensitivity of the input with regard to

the output will be 555.41%. Therefore, the output is highly sensitive to the input (Lane and

Rosewall 2015). For the changes in the price from $ 500 to $ 1310 the NPV has been

increased from -$15,635,004.70 to $ 184,412,844.33.

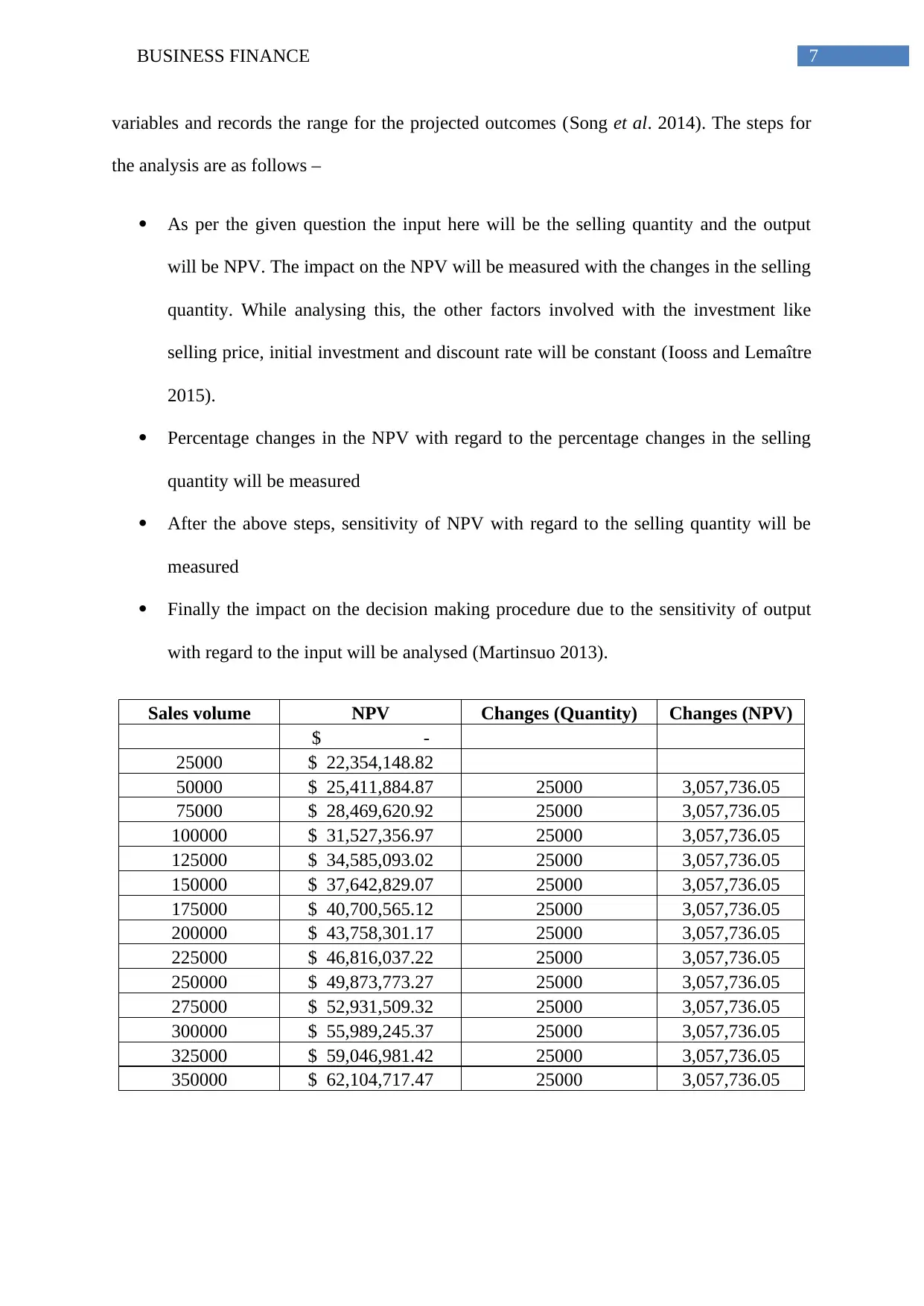

6. Sensitivity analysis for quantity change

Under finance, the sensitivity analysis is generated for measuring the impact of

variable that is selling quantity here has on the outcome that is net present value here. The

sensitivity analysis is based on variables that have impact on the valuation that the financial

model can explain through the variables like selling quantity and NPV. It differentiates the

400 500 600 700 800 900 1000 1100 1200 1300 1400

$(50,000,000.00)

$-

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

Selling price

N

P

V

Changes in price 4%

Changes in NPV 24%

Sensitivity

555.41

%

From the above it can be stated that the NPV changes by 24% for every 4% changes

in the selling price of new SSHA model. Therefore the sensitivity of the input with regard to

the output will be 555.41%. Therefore, the output is highly sensitive to the input (Lane and

Rosewall 2015). For the changes in the price from $ 500 to $ 1310 the NPV has been

increased from -$15,635,004.70 to $ 184,412,844.33.

6. Sensitivity analysis for quantity change

Under finance, the sensitivity analysis is generated for measuring the impact of

variable that is selling quantity here has on the outcome that is net present value here. The

sensitivity analysis is based on variables that have impact on the valuation that the financial

model can explain through the variables like selling quantity and NPV. It differentiates the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

variables and records the range for the projected outcomes (Song et al. 2014). The steps for

the analysis are as follows –

As per the given question the input here will be the selling quantity and the output

will be NPV. The impact on the NPV will be measured with the changes in the selling

quantity. While analysing this, the other factors involved with the investment like

selling price, initial investment and discount rate will be constant (Iooss and Lemaître

2015).

Percentage changes in the NPV with regard to the percentage changes in the selling

quantity will be measured

After the above steps, sensitivity of NPV with regard to the selling quantity will be

measured

Finally the impact on the decision making procedure due to the sensitivity of output

with regard to the input will be analysed (Martinsuo 2013).

Sales volume NPV Changes (Quantity) Changes (NPV)

$ -

25000 $ 22,354,148.82

50000 $ 25,411,884.87 25000 3,057,736.05

75000 $ 28,469,620.92 25000 3,057,736.05

100000 $ 31,527,356.97 25000 3,057,736.05

125000 $ 34,585,093.02 25000 3,057,736.05

150000 $ 37,642,829.07 25000 3,057,736.05

175000 $ 40,700,565.12 25000 3,057,736.05

200000 $ 43,758,301.17 25000 3,057,736.05

225000 $ 46,816,037.22 25000 3,057,736.05

250000 $ 49,873,773.27 25000 3,057,736.05

275000 $ 52,931,509.32 25000 3,057,736.05

300000 $ 55,989,245.37 25000 3,057,736.05

325000 $ 59,046,981.42 25000 3,057,736.05

350000 $ 62,104,717.47 25000 3,057,736.05

variables and records the range for the projected outcomes (Song et al. 2014). The steps for

the analysis are as follows –

As per the given question the input here will be the selling quantity and the output

will be NPV. The impact on the NPV will be measured with the changes in the selling

quantity. While analysing this, the other factors involved with the investment like

selling price, initial investment and discount rate will be constant (Iooss and Lemaître

2015).

Percentage changes in the NPV with regard to the percentage changes in the selling

quantity will be measured

After the above steps, sensitivity of NPV with regard to the selling quantity will be

measured

Finally the impact on the decision making procedure due to the sensitivity of output

with regard to the input will be analysed (Martinsuo 2013).

Sales volume NPV Changes (Quantity) Changes (NPV)

$ -

25000 $ 22,354,148.82

50000 $ 25,411,884.87 25000 3,057,736.05

75000 $ 28,469,620.92 25000 3,057,736.05

100000 $ 31,527,356.97 25000 3,057,736.05

125000 $ 34,585,093.02 25000 3,057,736.05

150000 $ 37,642,829.07 25000 3,057,736.05

175000 $ 40,700,565.12 25000 3,057,736.05

200000 $ 43,758,301.17 25000 3,057,736.05

225000 $ 46,816,037.22 25000 3,057,736.05

250000 $ 49,873,773.27 25000 3,057,736.05

275000 $ 52,931,509.32 25000 3,057,736.05

300000 $ 55,989,245.37 25000 3,057,736.05

325000 $ 59,046,981.42 25000 3,057,736.05

350000 $ 62,104,717.47 25000 3,057,736.05

8BUSINESS FINANCE

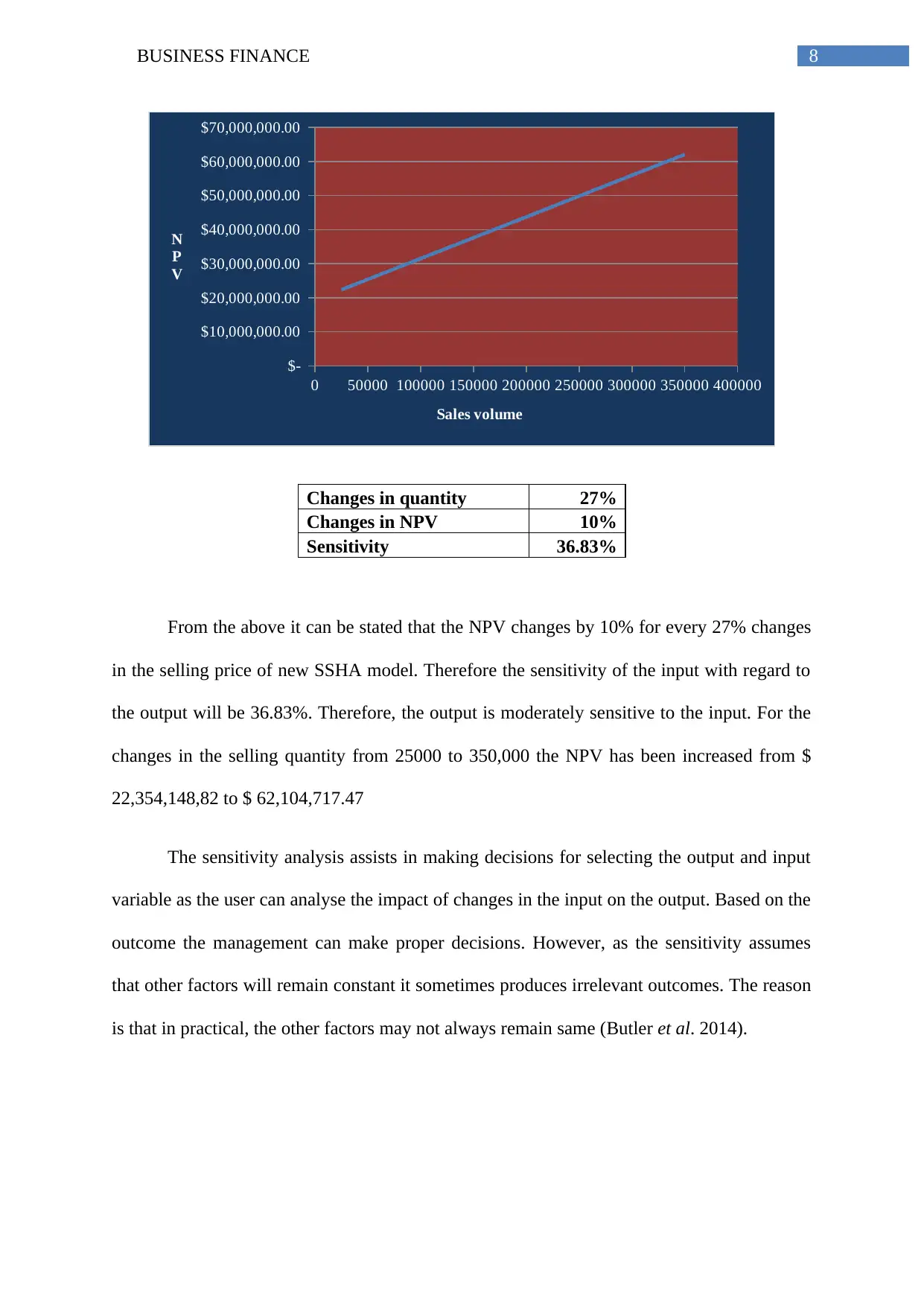

0 50000 100000 150000 200000 250000 300000 350000 400000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Sales volume

N

P

V

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

From the above it can be stated that the NPV changes by 10% for every 27% changes

in the selling price of new SSHA model. Therefore the sensitivity of the input with regard to

the output will be 36.83%. Therefore, the output is moderately sensitive to the input. For the

changes in the selling quantity from 25000 to 350,000 the NPV has been increased from $

22,354,148,82 to $ 62,104,717.47

The sensitivity analysis assists in making decisions for selecting the output and input

variable as the user can analyse the impact of changes in the input on the output. Based on the

outcome the management can make proper decisions. However, as the sensitivity assumes

that other factors will remain constant it sometimes produces irrelevant outcomes. The reason

is that in practical, the other factors may not always remain same (Butler et al. 2014).

0 50000 100000 150000 200000 250000 300000 350000 400000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Sales volume

N

P

V

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

From the above it can be stated that the NPV changes by 10% for every 27% changes

in the selling price of new SSHA model. Therefore the sensitivity of the input with regard to

the output will be 36.83%. Therefore, the output is moderately sensitive to the input. For the

changes in the selling quantity from 25000 to 350,000 the NPV has been increased from $

22,354,148,82 to $ 62,104,717.47

The sensitivity analysis assists in making decisions for selecting the output and input

variable as the user can analyse the impact of changes in the input on the output. Based on the

outcome the management can make proper decisions. However, as the sensitivity assumes

that other factors will remain constant it sometimes produces irrelevant outcomes. The reason

is that in practical, the other factors may not always remain same (Butler et al. 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS FINANCE

7. Conclusion

Taking into consideration all the above mentioned measures to analyse the

acceptability of the project it can be concluded that Booli Enterprise shall manufacture new

model for SSHA. The reason is that the NPV of the project is positive, PI of the project is

1.65, payback period is 2.14 years that is less than 5 years and IRR is 19.7% that is more than

the required rate of return.

8. Recommendation

If manufacturing the new model for existing SSHA generates loss for any other

product then the amount of loss shall be included in the amount of investment. If including

the amount of loss results into negative NPV then the project shall not be accepted. However,

if including the amount of loss results into positive NPV then the project shall be accepted.

7. Conclusion

Taking into consideration all the above mentioned measures to analyse the

acceptability of the project it can be concluded that Booli Enterprise shall manufacture new

model for SSHA. The reason is that the NPV of the project is positive, PI of the project is

1.65, payback period is 2.14 years that is less than 5 years and IRR is 19.7% that is more than

the required rate of return.

8. Recommendation

If manufacturing the new model for existing SSHA generates loss for any other

product then the amount of loss shall be included in the amount of investment. If including

the amount of loss results into negative NPV then the project shall not be accepted. However,

if including the amount of loss results into positive NPV then the project shall be accepted.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS FINANCE

Reference

Butler, M.P., Reed, P.M., Fisher-Vanden, K., Keller, K. and Wagener, T., 2014. Identifying

parametric controls and dependencies in integrated assessment models using global

sensitivity analysis. Environmental modelling & software, 59, pp.10-29.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Goodman, T.H., Neamtiu, M., Shroff, N. and White, H.D., 2013. Management forecast

quality and capital investment decisions. The Accounting Review, 89(1), pp.331-365.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of

calculating the payback period of investment for renovation of building facades. Stroitel'stvo

Unikal'nyh Zdanij i Sooruzenij, (2), p.82.

Iooss, B. and Lemaître, P., 2015. A review on global sensitivity analysis methods.

In Uncertainty management in simulation-optimization of complex systems (pp. 101-122).

Springer, Boston, MA.

Lane, K. and Rosewall, T., 2015. Firms’ investment decisions and interest rates. Reserve

Bank of Australia Bulletin. June quarter, pp.1-7.

Leung, B., Springborn, M.R., Turner, J.A. and Brockerhoff, E.G., 2014. Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in Ecology

and the Environment, 12(5), pp.273-279.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

Reference

Butler, M.P., Reed, P.M., Fisher-Vanden, K., Keller, K. and Wagener, T., 2014. Identifying

parametric controls and dependencies in integrated assessment models using global

sensitivity analysis. Environmental modelling & software, 59, pp.10-29.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Goodman, T.H., Neamtiu, M., Shroff, N. and White, H.D., 2013. Management forecast

quality and capital investment decisions. The Accounting Review, 89(1), pp.331-365.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of

calculating the payback period of investment for renovation of building facades. Stroitel'stvo

Unikal'nyh Zdanij i Sooruzenij, (2), p.82.

Iooss, B. and Lemaître, P., 2015. A review on global sensitivity analysis methods.

In Uncertainty management in simulation-optimization of complex systems (pp. 101-122).

Springer, Boston, MA.

Lane, K. and Rosewall, T., 2015. Firms’ investment decisions and interest rates. Reserve

Bank of Australia Bulletin. June quarter, pp.1-7.

Leung, B., Springborn, M.R., Turner, J.A. and Brockerhoff, E.G., 2014. Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in Ecology

and the Environment, 12(5), pp.273-279.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

11BUSINESS FINANCE

Martinsuo, M., 2013. Project portfolio management in practice and in context. International

Journal of Project Management, 31(6), pp.794-803.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Ross, S.A., Bianchi, R., Christensen, M., Drew, M., Westerfield, R. and Jordan, B.D.,

2014. Fundamentals of Corporate Finance: Introduction to corporate finance Chapter: 2

Financial statements, taxes and cash flow PART 2 Chapter: 3 Working with financial

statements Chapter: 4 Long-term financial planning and corporate growth PART 3 Chapter: 5

First principles of valuation: TVM Chapter: 6 Valuing shares and bonds PART 4 Chapter: 7

Net present value and other investment criteria Chapter: 8 Making capital investment

decisions Chapter: 9 Project analysis and evaluation PART 5 Chapter: 10 Lessons ....

McGraw-Hill Education (Australia).

Song, Z., Li, Z., Wei, M., Lai, F. and Bai, B., 2014. Sensitivity analysis of water-alternating-

CO2 flooding for enhanced oil recovery in high water cut oil reservoirs. Computers &

Fluids, 99, pp.93-103.

Martinsuo, M., 2013. Project portfolio management in practice and in context. International

Journal of Project Management, 31(6), pp.794-803.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Ross, S.A., Bianchi, R., Christensen, M., Drew, M., Westerfield, R. and Jordan, B.D.,

2014. Fundamentals of Corporate Finance: Introduction to corporate finance Chapter: 2

Financial statements, taxes and cash flow PART 2 Chapter: 3 Working with financial

statements Chapter: 4 Long-term financial planning and corporate growth PART 3 Chapter: 5

First principles of valuation: TVM Chapter: 6 Valuing shares and bonds PART 4 Chapter: 7

Net present value and other investment criteria Chapter: 8 Making capital investment

decisions Chapter: 9 Project analysis and evaluation PART 5 Chapter: 10 Lessons ....

McGraw-Hill Education (Australia).

Song, Z., Li, Z., Wei, M., Lai, F. and Bai, B., 2014. Sensitivity analysis of water-alternating-

CO2 flooding for enhanced oil recovery in high water cut oil reservoirs. Computers &

Fluids, 99, pp.93-103.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.