HI6026 - Audit Assurance and Compliance Report on Newcrest Mining

VerifiedAdded on 2023/06/13

|20

|4397

|379

Report

AI Summary

This report assesses the audit assurance and compliance practices of Newcrest Mining in relation to the ASX Corporate Governance Principles. It covers risk assessment, including foreign currency, liquidity, interest rate, and credit risks, and analyzes financial ratios and common-size financial statements to identify potential areas of concern. The report also discusses the internal control framework, external audit processes with EY, and management assurance measures implemented by Newcrest to mitigate risks. Despite a decrease in profit in 2017, the company demonstrates improvements in sales, risk management, and efficiency through various initiatives and regular reviews of governance practices. The document is available on Desklib, a platform offering a wide range of study tools and resources for students.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ASSURANCE AND COMPLIANCE

Executive Summary

The study aims to address the implication of ASX Corporate Governance Principles for

Newcrest Mining. Some of the various types of scope of discussion has been seen to be based on

relevant audit risk and potential steps to reduce risk. The latter part of the report has further

computed the income statement and balance sheet ratio, and Development of common-size

financial statements and suggested the potential steps to reduce the overall risk in audit. The

main findings have been able to state that the company follows “Corporate governance as

published by the Australian Securities Exchange (ASX) Corporate Governance Council (3rd

edition ASX Principles and Recommendations)” and observed to regularly review the

“governance and compliance practices”. The risk assessment has been further able to state that

“Foreign currency risk, Liquidity risk, Interest rate risk, credit risk, Commodity and other price

risks”. Furthermore, the audit risk paradigms have been segregated as per the Internal Control

Framework, External Audit, internal Audit and management assurance. Despite of the decreased

profit in the 2017, the company has been able to improve itself in term of the increasing sales

and minimising the risk in terms of current assists, debt to equity ratio and increased efficiency.

Some of the major initiatives taken by Newcrest Mining to reduce risk is recognised with “sound

management” and oversight of matters of key audit responsibility. Newcrest has been able to

detail the internal control framework which is seen to be regularly reviewed by the Board. The

internal control framework risks are mitigated by following an n “integrated, robust planning and

budgeting process” thereby delivering a detailed two-year budget. The company’s current

external auditor is identified to be EY and “reappointment of the external auditor” is seen to be

reviewed annually. The EY’s Audit and risk committee is seen to acknowledge in the “areas of

knowledge, quality of team, coverage ability, industry knowledge, cost and audit methodology,”

which the company believes to be critical for the service delivery.

Executive Summary

The study aims to address the implication of ASX Corporate Governance Principles for

Newcrest Mining. Some of the various types of scope of discussion has been seen to be based on

relevant audit risk and potential steps to reduce risk. The latter part of the report has further

computed the income statement and balance sheet ratio, and Development of common-size

financial statements and suggested the potential steps to reduce the overall risk in audit. The

main findings have been able to state that the company follows “Corporate governance as

published by the Australian Securities Exchange (ASX) Corporate Governance Council (3rd

edition ASX Principles and Recommendations)” and observed to regularly review the

“governance and compliance practices”. The risk assessment has been further able to state that

“Foreign currency risk, Liquidity risk, Interest rate risk, credit risk, Commodity and other price

risks”. Furthermore, the audit risk paradigms have been segregated as per the Internal Control

Framework, External Audit, internal Audit and management assurance. Despite of the decreased

profit in the 2017, the company has been able to improve itself in term of the increasing sales

and minimising the risk in terms of current assists, debt to equity ratio and increased efficiency.

Some of the major initiatives taken by Newcrest Mining to reduce risk is recognised with “sound

management” and oversight of matters of key audit responsibility. Newcrest has been able to

detail the internal control framework which is seen to be regularly reviewed by the Board. The

internal control framework risks are mitigated by following an n “integrated, robust planning and

budgeting process” thereby delivering a detailed two-year budget. The company’s current

external auditor is identified to be EY and “reappointment of the external auditor” is seen to be

reviewed annually. The EY’s Audit and risk committee is seen to acknowledge in the “areas of

knowledge, quality of team, coverage ability, industry knowledge, cost and audit methodology,”

which the company believes to be critical for the service delivery.

2AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Introduction......................................................................................................................................3

Implementation of ASX CGC principles for Newcrest Mining......................................................3

Risk Assessment..............................................................................................................................5

Computation of income statement and balance sheet ratio, and Development of common-size

financial statements.........................................................................................................................6

Potential steps to reduce risk.........................................................................................................15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

Table of Contents

Introduction......................................................................................................................................3

Implementation of ASX CGC principles for Newcrest Mining......................................................3

Risk Assessment..............................................................................................................................5

Computation of income statement and balance sheet ratio, and Development of common-size

financial statements.........................................................................................................................6

Potential steps to reduce risk.........................................................................................................15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ASSURANCE AND COMPLIANCE

Introduction

Newcrest is recognised as one of the “world’s largest gold mining companies” operating

in four countries. The company is “headquartered in Melbourne”, Australia and among the top

50 companies listed in the Australian securities exchange. The mines of the company are seen to

be in “Australia, Papua New Guinea (PNG), Indonesia, and Côte d’Ivoire”. The company’s main

emphasis is seen with three key value drivers: “maintaining low costs, growing reserves and

production and using capital efficiently”. The main mission of the company has been further

identified with delivering “superior returns from finding, developing and operating gold/copper

mines”. The vision of the company has been further identified with providing “safe, responsible,

efficient and profitable mining” (Newcrest Mining Limited 2018).

Discovery of the new ore bodies is identified as the main strategy of the company and

Newcrest possess a successful exploration track record in this aspect.

The main discussions of the report have been seen to with addressing the implication of

ASX Corporate Governance Principles for Newcrest Mining. Some of the various types of the

other scope of discussion has been seen to be based on relevant audit risk and potential steps to

reduce risk. The latter part of the report has further computed the income statement and balance

sheet ratio, and Development of common-size financial statements and suggested the potential

steps to reduce the overall risk in audit.

Implementation of ASX CGC principles for Newcrest Mining

The company has been recognised with the maximum standard of maintaining CG which

is critical to the vision. The company has been identified to following the effective procedure of

“Corporate governance as published by the Australian Securities Exchange (ASX) Corporate

Governance Council (3rd edition ASX Principles and Recommendations)” and observed to

regularly review the governance and compliance practices. The board of directors is seen to

consist of ten directors. The board has determined all “Non-Executive Directors including the

Chairman are considered independent” as per the “Board’s Independence Policy”. The main

purpose of the board have been further set out with the Board charter. The charters of each board

have been able to set out the responsibilities as per the board charter. In addition to this, the

Introduction

Newcrest is recognised as one of the “world’s largest gold mining companies” operating

in four countries. The company is “headquartered in Melbourne”, Australia and among the top

50 companies listed in the Australian securities exchange. The mines of the company are seen to

be in “Australia, Papua New Guinea (PNG), Indonesia, and Côte d’Ivoire”. The company’s main

emphasis is seen with three key value drivers: “maintaining low costs, growing reserves and

production and using capital efficiently”. The main mission of the company has been further

identified with delivering “superior returns from finding, developing and operating gold/copper

mines”. The vision of the company has been further identified with providing “safe, responsible,

efficient and profitable mining” (Newcrest Mining Limited 2018).

Discovery of the new ore bodies is identified as the main strategy of the company and

Newcrest possess a successful exploration track record in this aspect.

The main discussions of the report have been seen to with addressing the implication of

ASX Corporate Governance Principles for Newcrest Mining. Some of the various types of the

other scope of discussion has been seen to be based on relevant audit risk and potential steps to

reduce risk. The latter part of the report has further computed the income statement and balance

sheet ratio, and Development of common-size financial statements and suggested the potential

steps to reduce the overall risk in audit.

Implementation of ASX CGC principles for Newcrest Mining

The company has been recognised with the maximum standard of maintaining CG which

is critical to the vision. The company has been identified to following the effective procedure of

“Corporate governance as published by the Australian Securities Exchange (ASX) Corporate

Governance Council (3rd edition ASX Principles and Recommendations)” and observed to

regularly review the governance and compliance practices. The board of directors is seen to

consist of ten directors. The board has determined all “Non-Executive Directors including the

Chairman are considered independent” as per the “Board’s Independence Policy”. The main

purpose of the board have been further set out with the Board charter. The charters of each board

have been able to set out the responsibilities as per the board charter. In addition to this, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ASSURANCE AND COMPLIANCE

charters of each “Board Committee” set out the “roles and responsibilities for the committees”

(Bryce, Ali and Mather 2015).

The company has been further seen to recognises to fully market the “company’s

activities and stakeholder communication in a timely, transparent and balanced style”.

Furthermore, the board has adopted the “Market Disclosure Policy” for ensuring that the

company adheres to the continuous disclosure requirements as stated by the ASX. The board of

Newcrest is seen to be supported by the “Disclosure Committee: Disclosure Committee Charter”.

The employees are encouraged to be the “long-term holders of Newcrest's” shares. It has been

seen to be necessary for the company to take the necessary decisions on “acquisition or disposal

of those shares or securities in any company in which the person may possess inside

information”. The “Securities Dealing Policy” has included the blackout period when the

employees are not allowed to deal in the securities of the company (Martinov-Bennie, Soh and

Tweedie 2015).

It has been further seen ta the company has been seen to be adopting the “Code of

Conduct” pertinent to all directors, employees and officers. In conjunction with the “Code of

Conduct” the company has a “Speak Out Standard and Service” which is kept confidential,

independent and anonymous. The various types of the employees, suppliers and contractors are

seen to be encouraged for raising the concerns of unethical or inappropriate behaviour which are

seen to be in good faith for receiving security from negative consequences. The “Anti-Bribery

and Corruption Policy” and “code of conduct” are associated to the policies which prohibits the

activities such as “bribery, corruption, unauthorised payments or exercising improper influence

by all employees and contractors”. In addition to this, the workforce diversity and organisational

diversity is led by board in driven by the recognition of the diverse workforce which is supported

by high performance. The “Diversity and Inclusion Policy” depicts the way “Newcrest supports”

a diverse and inclusive workforce. The oversight of the risk management practices and internal

controls are identified as the key accountability of the board. The company has been able to

detail the risk management and the “internal control framework policies and procedures” which

sets out the various types of the “roles, responsibilities and guidelines” for the identification and

managing of material business risks. The effectiveness of the framework is reviewed regularly by

charters of each “Board Committee” set out the “roles and responsibilities for the committees”

(Bryce, Ali and Mather 2015).

The company has been further seen to recognises to fully market the “company’s

activities and stakeholder communication in a timely, transparent and balanced style”.

Furthermore, the board has adopted the “Market Disclosure Policy” for ensuring that the

company adheres to the continuous disclosure requirements as stated by the ASX. The board of

Newcrest is seen to be supported by the “Disclosure Committee: Disclosure Committee Charter”.

The employees are encouraged to be the “long-term holders of Newcrest's” shares. It has been

seen to be necessary for the company to take the necessary decisions on “acquisition or disposal

of those shares or securities in any company in which the person may possess inside

information”. The “Securities Dealing Policy” has included the blackout period when the

employees are not allowed to deal in the securities of the company (Martinov-Bennie, Soh and

Tweedie 2015).

It has been further seen ta the company has been seen to be adopting the “Code of

Conduct” pertinent to all directors, employees and officers. In conjunction with the “Code of

Conduct” the company has a “Speak Out Standard and Service” which is kept confidential,

independent and anonymous. The various types of the employees, suppliers and contractors are

seen to be encouraged for raising the concerns of unethical or inappropriate behaviour which are

seen to be in good faith for receiving security from negative consequences. The “Anti-Bribery

and Corruption Policy” and “code of conduct” are associated to the policies which prohibits the

activities such as “bribery, corruption, unauthorised payments or exercising improper influence

by all employees and contractors”. In addition to this, the workforce diversity and organisational

diversity is led by board in driven by the recognition of the diverse workforce which is supported

by high performance. The “Diversity and Inclusion Policy” depicts the way “Newcrest supports”

a diverse and inclusive workforce. The oversight of the risk management practices and internal

controls are identified as the key accountability of the board. The company has been able to

detail the risk management and the “internal control framework policies and procedures” which

sets out the various types of the “roles, responsibilities and guidelines” for the identification and

managing of material business risks. The effectiveness of the framework is reviewed regularly by

5AUDIT ASSURANCE AND COMPLIANCE

the “Board with the support of the Audit and Risk Committee” (Boritz, Kochetova-Kozloski and

Robinson 2015).

Risk Assessment

The different facets of the risk assessment are seen with those aspects which may

adversely affect Newcrest’s “financial assets, liabilities or future cash flows”. Some of these

risks factors are mainly identified with “Foreign currency risk, Liquidity risk, Interest rate risk,

credit risk, Commodity and other price risks”. The various types of the commodity and other

price risks are identified with the copper production which are sold into the global market. The

market price of the gold and copper act as the key driver to generate cash flow for Newcrest’s

overall capacity. The company has been identified as mainly an unhedged producer which

provides its shareholders exposed to various risks pertaining to “changes in the market price of

gold and copper”. In addition to this, the Foreign currency risk are considered with the different

types of the fluctuations in the exchange rate. The revenue of the group is seen to be primarily

dominated by the “US dollars whereas a material proportion of costs (including capital

expenditure) are collectively in Australian dollars and PNG Kina”. In addition to this, the

Australian entities have AUD functional currencies whereas “non-Australian operating entities

have USD functional currencies” (Ruwanpathirana et al. 2014).

The various types of the risks are seen with the “Group’s Statement of Financial Position

can also be affected materially by movements in the AUD:USD exchange rate”. Moreover, the

audit committee of the company has identified that the different types of the risks pertaining to

the liquidity has been considered with the “capital management policies and objectives, which

utilise debt as a key element of the Group’s capital structure”. The specific exposure to the risk

in this aspect has been seen to be based on the “sufficiency of available unutilised facilities and

the repayment maturity profile of existing financial instruments”. The various types of credit risk

arses from the potential default of the “counterparty to the Group’s financial assets” which

includes the different types of the derivative instruments, trade, cash equivalents and other

receivable’s. The group has been further identified to limit the counterparty credit risk on the

liquid funds and derivative financial instrument is seen with dealings only with banks or

“financial institutions with credit ratings of at least BBB (S&P) equivalent”. Additionally, the

the “Board with the support of the Audit and Risk Committee” (Boritz, Kochetova-Kozloski and

Robinson 2015).

Risk Assessment

The different facets of the risk assessment are seen with those aspects which may

adversely affect Newcrest’s “financial assets, liabilities or future cash flows”. Some of these

risks factors are mainly identified with “Foreign currency risk, Liquidity risk, Interest rate risk,

credit risk, Commodity and other price risks”. The various types of the commodity and other

price risks are identified with the copper production which are sold into the global market. The

market price of the gold and copper act as the key driver to generate cash flow for Newcrest’s

overall capacity. The company has been identified as mainly an unhedged producer which

provides its shareholders exposed to various risks pertaining to “changes in the market price of

gold and copper”. In addition to this, the Foreign currency risk are considered with the different

types of the fluctuations in the exchange rate. The revenue of the group is seen to be primarily

dominated by the “US dollars whereas a material proportion of costs (including capital

expenditure) are collectively in Australian dollars and PNG Kina”. In addition to this, the

Australian entities have AUD functional currencies whereas “non-Australian operating entities

have USD functional currencies” (Ruwanpathirana et al. 2014).

The various types of the risks are seen with the “Group’s Statement of Financial Position

can also be affected materially by movements in the AUD:USD exchange rate”. Moreover, the

audit committee of the company has identified that the different types of the risks pertaining to

the liquidity has been considered with the “capital management policies and objectives, which

utilise debt as a key element of the Group’s capital structure”. The specific exposure to the risk

in this aspect has been seen to be based on the “sufficiency of available unutilised facilities and

the repayment maturity profile of existing financial instruments”. The various types of credit risk

arses from the potential default of the “counterparty to the Group’s financial assets” which

includes the different types of the derivative instruments, trade, cash equivalents and other

receivable’s. The group has been further identified to limit the counterparty credit risk on the

liquid funds and derivative financial instrument is seen with dealings only with banks or

“financial institutions with credit ratings of at least BBB (S&P) equivalent”. Additionally, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ASSURANCE AND COMPLIANCE

credit risks are limited with guaranteeing variation considered with maximum investment limits

are considered with the credit ratings. The customers intending to trade on credit terms or the

financial counterparties are subject to credit risk analysis. The audit risk paradigms have been

segregated as per the Internal Control Framework, External Audit, internal Audit and

management assurance (Pickett 2015).

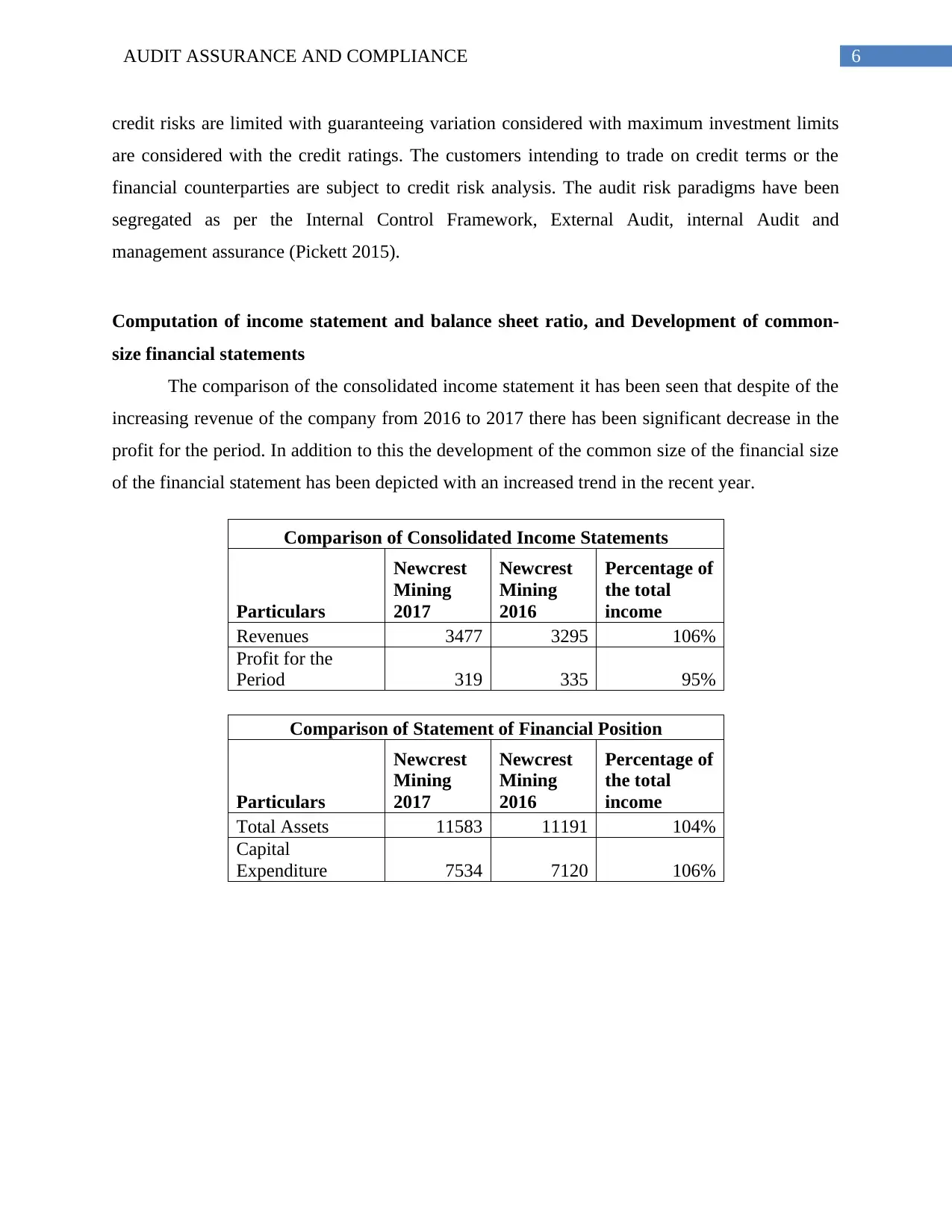

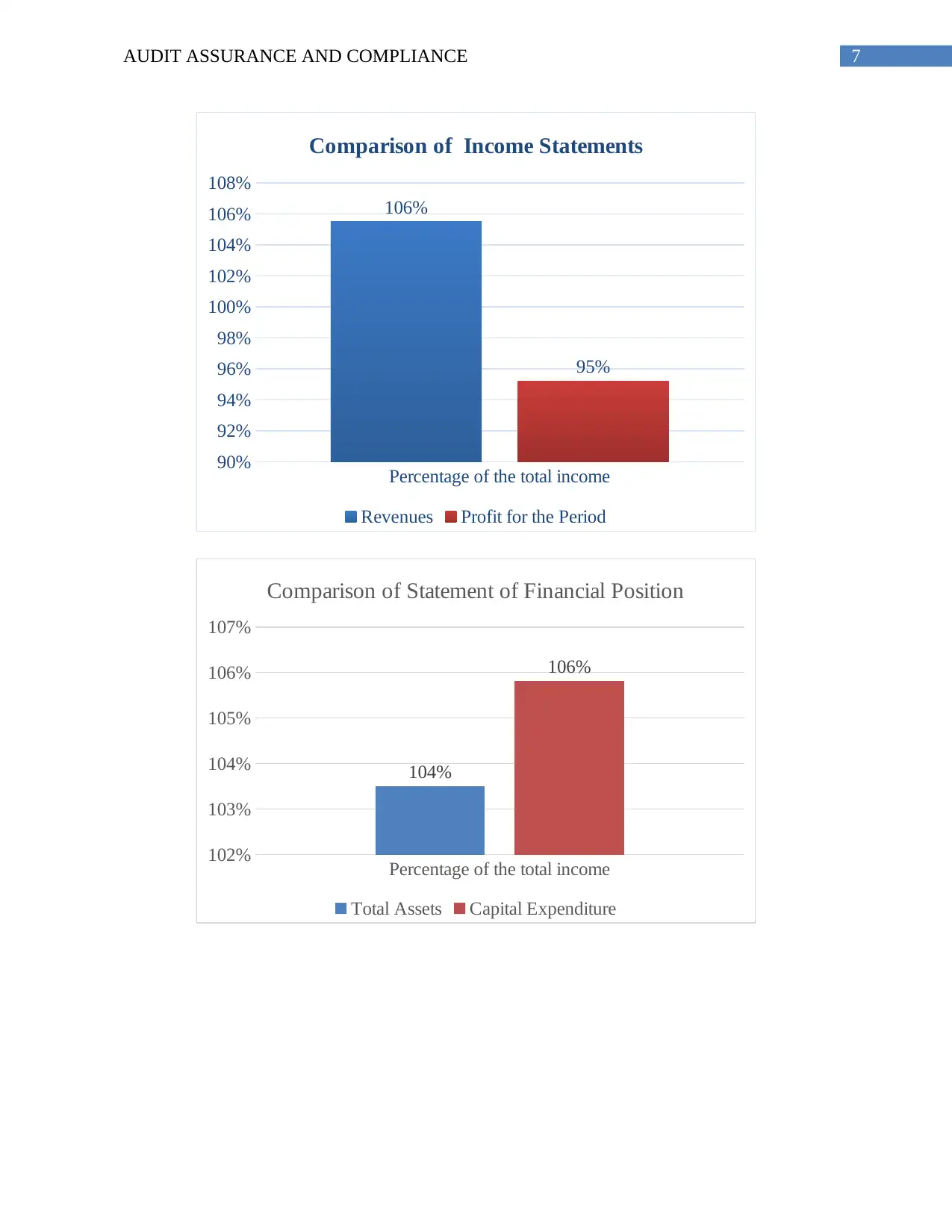

Computation of income statement and balance sheet ratio, and Development of common-

size financial statements

The comparison of the consolidated income statement it has been seen that despite of the

increasing revenue of the company from 2016 to 2017 there has been significant decrease in the

profit for the period. In addition to this the development of the common size of the financial size

of the financial statement has been depicted with an increased trend in the recent year.

Comparison of Consolidated Income Statements

Particulars

Newcrest

Mining

2017

Newcrest

Mining

2016

Percentage of

the total

income

Revenues 3477 3295 106%

Profit for the

Period 319 335 95%

Comparison of Statement of Financial Position

Particulars

Newcrest

Mining

2017

Newcrest

Mining

2016

Percentage of

the total

income

Total Assets 11583 11191 104%

Capital

Expenditure 7534 7120 106%

credit risks are limited with guaranteeing variation considered with maximum investment limits

are considered with the credit ratings. The customers intending to trade on credit terms or the

financial counterparties are subject to credit risk analysis. The audit risk paradigms have been

segregated as per the Internal Control Framework, External Audit, internal Audit and

management assurance (Pickett 2015).

Computation of income statement and balance sheet ratio, and Development of common-

size financial statements

The comparison of the consolidated income statement it has been seen that despite of the

increasing revenue of the company from 2016 to 2017 there has been significant decrease in the

profit for the period. In addition to this the development of the common size of the financial size

of the financial statement has been depicted with an increased trend in the recent year.

Comparison of Consolidated Income Statements

Particulars

Newcrest

Mining

2017

Newcrest

Mining

2016

Percentage of

the total

income

Revenues 3477 3295 106%

Profit for the

Period 319 335 95%

Comparison of Statement of Financial Position

Particulars

Newcrest

Mining

2017

Newcrest

Mining

2016

Percentage of

the total

income

Total Assets 11583 11191 104%

Capital

Expenditure 7534 7120 106%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ASSURANCE AND COMPLIANCE

Percentage of the total income

90%

92%

94%

96%

98%

100%

102%

104%

106%

108%

106%

95%

Comparison of Income Statements

Revenues Profit for the Period

Percentage of the total income

102%

103%

104%

105%

106%

107%

104%

106%

Comparison of Statement of Financial Position

Total Assets Capital Expenditure

Percentage of the total income

90%

92%

94%

96%

98%

100%

102%

104%

106%

108%

106%

95%

Comparison of Income Statements

Revenues Profit for the Period

Percentage of the total income

102%

103%

104%

105%

106%

107%

104%

106%

Comparison of Statement of Financial Position

Total Assets Capital Expenditure

8AUDIT ASSURANCE AND COMPLIANCE

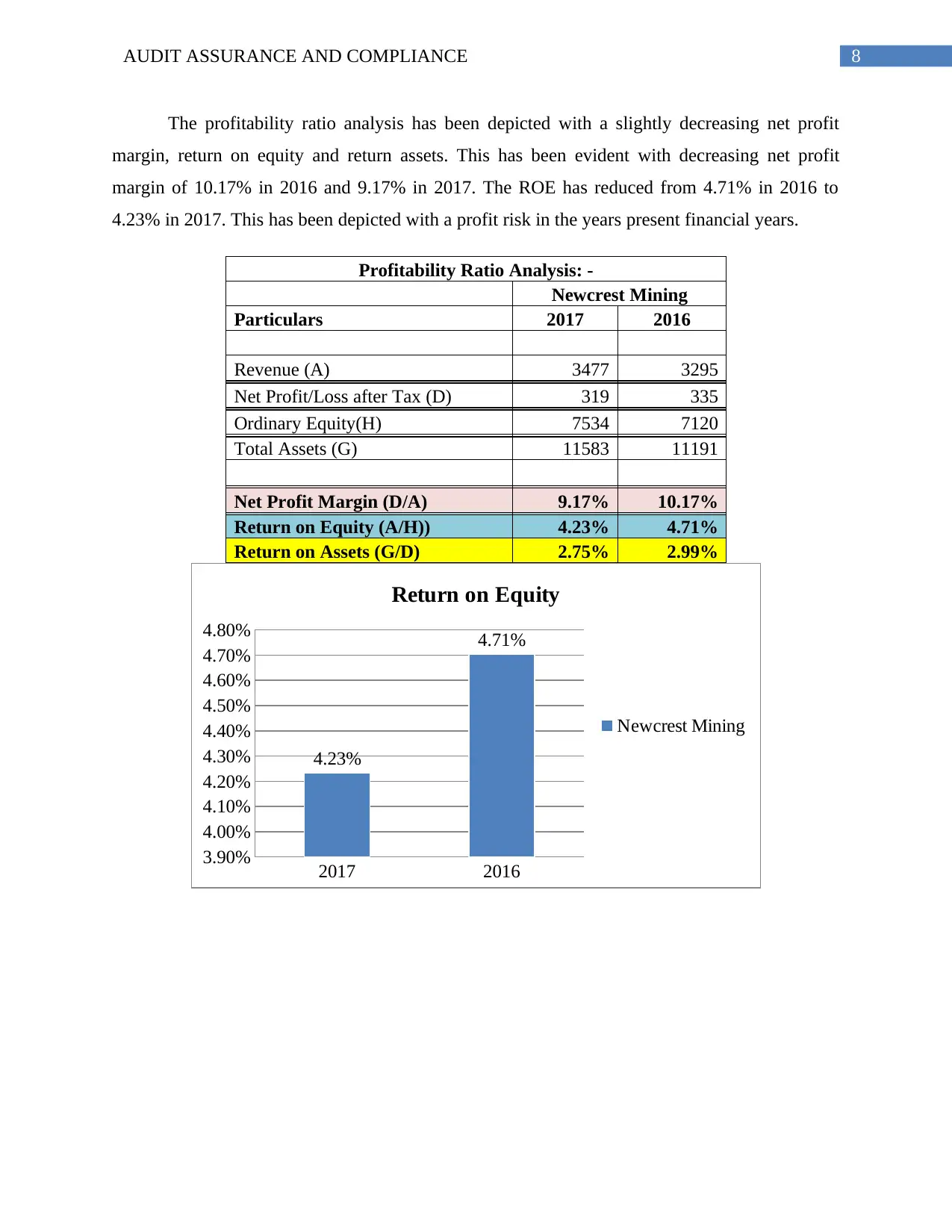

The profitability ratio analysis has been depicted with a slightly decreasing net profit

margin, return on equity and return assets. This has been evident with decreasing net profit

margin of 10.17% in 2016 and 9.17% in 2017. The ROE has reduced from 4.71% in 2016 to

4.23% in 2017. This has been depicted with a profit risk in the years present financial years.

Profitability Ratio Analysis: -

Newcrest Mining

Particulars 2017 2016

Revenue (A) 3477 3295

Net Profit/Loss after Tax (D) 319 335

Ordinary Equity(H) 7534 7120

Total Assets (G) 11583 11191

Net Profit Margin (D/A) 9.17% 10.17%

Return on Equity (A/H)) 4.23% 4.71%

Return on Assets (G/D) 2.75% 2.99%

2017 2016

3.90%

4.00%

4.10%

4.20%

4.30%

4.40%

4.50%

4.60%

4.70%

4.80%

4.23%

4.71%

Return on Equity

Newcrest Mining

The profitability ratio analysis has been depicted with a slightly decreasing net profit

margin, return on equity and return assets. This has been evident with decreasing net profit

margin of 10.17% in 2016 and 9.17% in 2017. The ROE has reduced from 4.71% in 2016 to

4.23% in 2017. This has been depicted with a profit risk in the years present financial years.

Profitability Ratio Analysis: -

Newcrest Mining

Particulars 2017 2016

Revenue (A) 3477 3295

Net Profit/Loss after Tax (D) 319 335

Ordinary Equity(H) 7534 7120

Total Assets (G) 11583 11191

Net Profit Margin (D/A) 9.17% 10.17%

Return on Equity (A/H)) 4.23% 4.71%

Return on Assets (G/D) 2.75% 2.99%

2017 2016

3.90%

4.00%

4.10%

4.20%

4.30%

4.40%

4.50%

4.60%

4.70%

4.80%

4.23%

4.71%

Return on Equity

Newcrest Mining

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ASSURANCE AND COMPLIANCE

2017 2016

8.60%

8.80%

9.00%

9.20%

9.40%

9.60%

9.80%

10.00%

10.20%

10.40%

9.17%

10.17%

Net Profit Margin

Newcrest Mining

2017 2016

2.60%

2.65%

2.70%

2.75%

2.80%

2.85%

2.90%

2.95%

3.00%

3.05%

2.75%

2.99%

Return on Assets

Newcrest Mining

2017 2016

8.60%

8.80%

9.00%

9.20%

9.40%

9.60%

9.80%

10.00%

10.20%

10.40%

9.17%

10.17%

Net Profit Margin

Newcrest Mining

2017 2016

2.60%

2.65%

2.70%

2.75%

2.80%

2.85%

2.90%

2.95%

3.00%

3.05%

2.75%

2.99%

Return on Assets

Newcrest Mining

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ASSURANCE AND COMPLIANCE

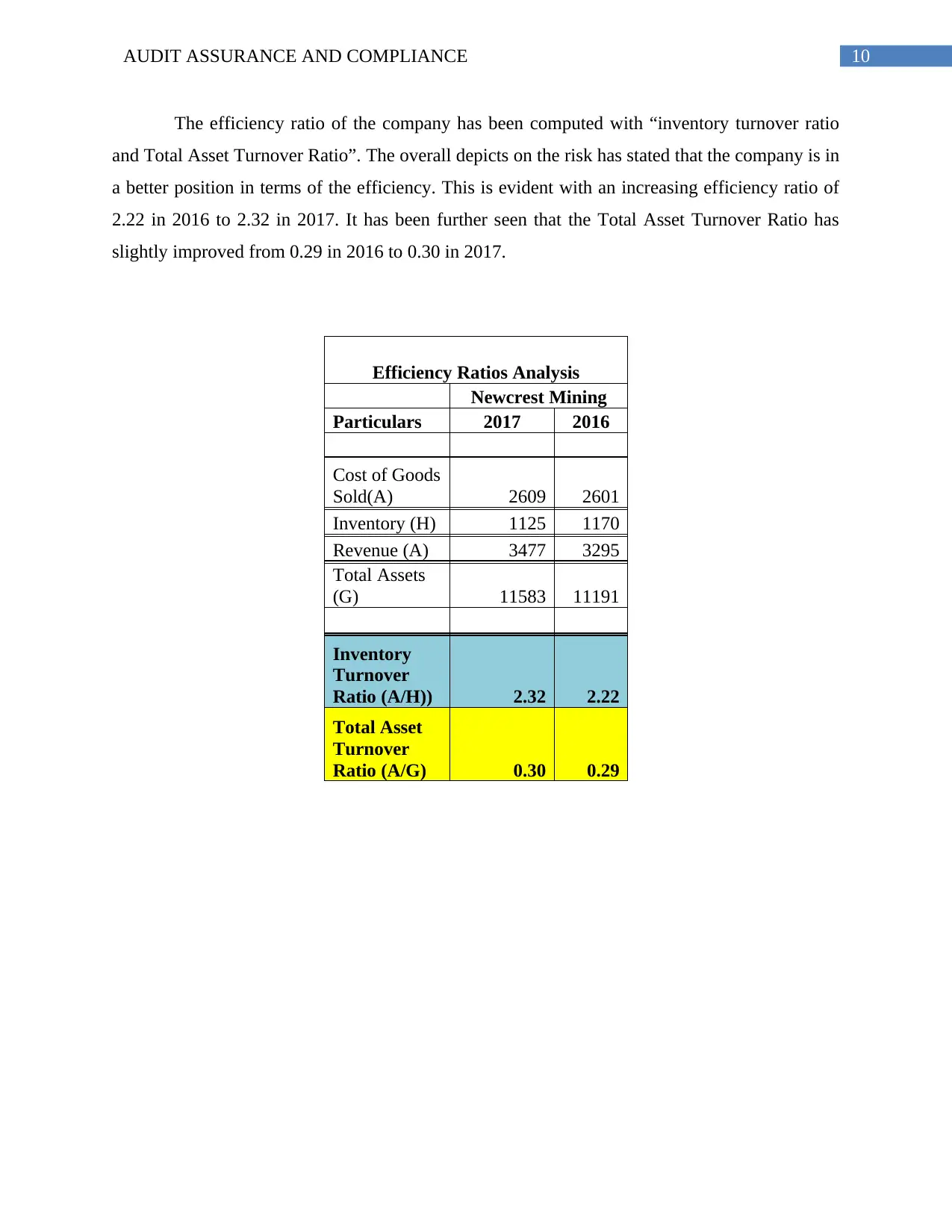

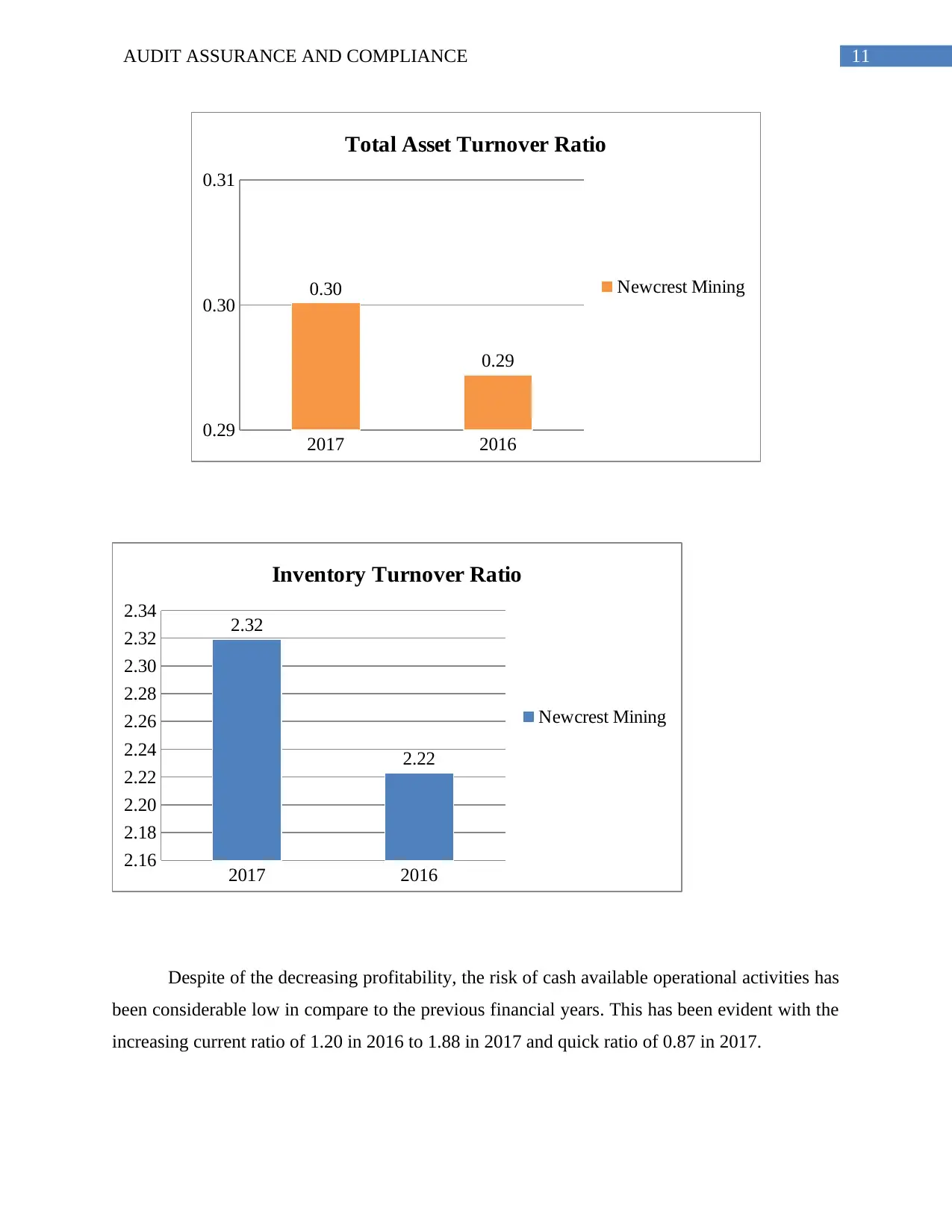

The efficiency ratio of the company has been computed with “inventory turnover ratio

and Total Asset Turnover Ratio”. The overall depicts on the risk has stated that the company is in

a better position in terms of the efficiency. This is evident with an increasing efficiency ratio of

2.22 in 2016 to 2.32 in 2017. It has been further seen that the Total Asset Turnover Ratio has

slightly improved from 0.29 in 2016 to 0.30 in 2017.

Efficiency Ratios Analysis

Newcrest Mining

Particulars 2017 2016

Cost of Goods

Sold(A) 2609 2601

Inventory (H) 1125 1170

Revenue (A) 3477 3295

Total Assets

(G) 11583 11191

Inventory

Turnover

Ratio (A/H)) 2.32 2.22

Total Asset

Turnover

Ratio (A/G) 0.30 0.29

The efficiency ratio of the company has been computed with “inventory turnover ratio

and Total Asset Turnover Ratio”. The overall depicts on the risk has stated that the company is in

a better position in terms of the efficiency. This is evident with an increasing efficiency ratio of

2.22 in 2016 to 2.32 in 2017. It has been further seen that the Total Asset Turnover Ratio has

slightly improved from 0.29 in 2016 to 0.30 in 2017.

Efficiency Ratios Analysis

Newcrest Mining

Particulars 2017 2016

Cost of Goods

Sold(A) 2609 2601

Inventory (H) 1125 1170

Revenue (A) 3477 3295

Total Assets

(G) 11583 11191

Inventory

Turnover

Ratio (A/H)) 2.32 2.22

Total Asset

Turnover

Ratio (A/G) 0.30 0.29

11AUDIT ASSURANCE AND COMPLIANCE

2017 2016

0.29

0.30

0.31

0.30

0.29

Total Asset Turnover Ratio

Newcrest Mining

2017 2016

2.16

2.18

2.20

2.22

2.24

2.26

2.28

2.30

2.32

2.34 2.32

2.22

Inventory Turnover Ratio

Newcrest Mining

Despite of the decreasing profitability, the risk of cash available operational activities has

been considerable low in compare to the previous financial years. This has been evident with the

increasing current ratio of 1.20 in 2016 to 1.88 in 2017 and quick ratio of 0.87 in 2017.

2017 2016

0.29

0.30

0.31

0.30

0.29

Total Asset Turnover Ratio

Newcrest Mining

2017 2016

2.16

2.18

2.20

2.22

2.24

2.26

2.28

2.30

2.32

2.34 2.32

2.22

Inventory Turnover Ratio

Newcrest Mining

Despite of the decreasing profitability, the risk of cash available operational activities has

been considerable low in compare to the previous financial years. This has been evident with the

increasing current ratio of 1.20 in 2016 to 1.88 in 2017 and quick ratio of 0.87 in 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.