PDF Management Accounting - Sample Assignment

VerifiedAdded on 2021/05/29

|20

|4451

|23

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Nguyen Thi Thuy Linh_10190552_MA_A2.1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction.................................................................................................................3

Scenario 1....................................................................................................................4

Question 1:...............................................................................................................4

Question 2:...............................................................................................................5

Question 3:...............................................................................................................6

Question 4:...............................................................................................................8

Question 5:...............................................................................................................9

PEST analysis.......................................................................................................9

SWOT analysis....................................................................................................10

Balanced Scorecard analysis.............................................................................11

Scenario 2..................................................................................................................12

Question 1 + Question 2:.......................................................................................13

Question 3:.............................................................................................................15

Conclusion.................................................................................................................16

References.................................................................................................................. 18

Introduction.................................................................................................................3

Scenario 1....................................................................................................................4

Question 1:...............................................................................................................4

Question 2:...............................................................................................................5

Question 3:...............................................................................................................6

Question 4:...............................................................................................................8

Question 5:...............................................................................................................9

PEST analysis.......................................................................................................9

SWOT analysis....................................................................................................10

Balanced Scorecard analysis.............................................................................11

Scenario 2..................................................................................................................12

Question 1 + Question 2:.......................................................................................13

Question 3:.............................................................................................................15

Conclusion.................................................................................................................16

References.................................................................................................................. 18

Introduction

Planning tools are important in management accounting that each company should

conduct them well to reduce costs and reach high profits. To analyze and evaluate the

advantages and effectiveness of planning tools in management accounting, this

assignment is going to analyze the management accounting activities of Ricegreen and

compare to the SpaceZ to discover how management accouting respond to solve

financial problems.

Planning tools are important in management accounting that each company should

conduct them well to reduce costs and reach high profits. To analyze and evaluate the

advantages and effectiveness of planning tools in management accounting, this

assignment is going to analyze the management accounting activities of Ricegreen and

compare to the SpaceZ to discover how management accouting respond to solve

financial problems.

Scenario 1

Question 1:

a. Standard cost

Standard cost is used for estimating and controlling the cost of a product. According to

Bragg (2019), the variance can be reported after using standard cost to show the

different between the actual cost and the budgeted cost

- Advantages (Paul, 2016):

+ Effectively control the costs

+ Measure the actual costs to minimize the operations cost

+ Avoid wasting materials and labor forces as well as determine the best methods

and materials.

+ It is effective accouting system that requires low resources

+ Provide information for planning more accurate budgets

- Disadvantages (Paul, 2016)

+ It can affect the quality of materials because good quality may cost more compared

to the budget

+ Non-reporting of negative exceptions and variances may decrease the effectiveness

+ When standards are too high, employees may be under pressure to act unethically

to reach those standards

b. Standard price

Standard price predetermined price of products based on previous price, replacement

cost and market price (Definition of standard price, n.d)

- Advantages:

+ Help to adjust and control the costs to the prevailing trends

+ Easy to apply

+ Lead to effectiveness of purchasing department

- Disadvantages:

+ Difficulty in setting specific standard price due to the price depends on many

unspecified variable factors

c. Budget

Question 1:

a. Standard cost

Standard cost is used for estimating and controlling the cost of a product. According to

Bragg (2019), the variance can be reported after using standard cost to show the

different between the actual cost and the budgeted cost

- Advantages (Paul, 2016):

+ Effectively control the costs

+ Measure the actual costs to minimize the operations cost

+ Avoid wasting materials and labor forces as well as determine the best methods

and materials.

+ It is effective accouting system that requires low resources

+ Provide information for planning more accurate budgets

- Disadvantages (Paul, 2016)

+ It can affect the quality of materials because good quality may cost more compared

to the budget

+ Non-reporting of negative exceptions and variances may decrease the effectiveness

+ When standards are too high, employees may be under pressure to act unethically

to reach those standards

b. Standard price

Standard price predetermined price of products based on previous price, replacement

cost and market price (Definition of standard price, n.d)

- Advantages:

+ Help to adjust and control the costs to the prevailing trends

+ Easy to apply

+ Lead to effectiveness of purchasing department

- Disadvantages:

+ Difficulty in setting specific standard price due to the price depends on many

unspecified variable factors

c. Budget

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

According to Harold (n.d.), budget is a plan in terms of finance for future activities of

a company.

- Advantages (Mariana, 2015)

+ Help manager to decide which activities should be done and how to utilize the

resources

+ Help the company to control the actual costs and avoid over spending

- Disadvantages (Mariana, 2015):

+ Can be time-wasting and expensive

+ Can be strict and unrealistic

d. Balanced scorecard:

The balanced scorecard is a framework which is used for tracking and controlling

company’s strategies (Ted, n.d.). The manager can use BSC to determine both

financial and non-financial problems of the company.

- Advantages (Patricia, Lucia, Beatriz, 2017):

+ Provide a specific view of the strategy in both long-term and short-term

+ Allow the company to work on four perspectives at three levels: mission and vision,

goals, measures and innitiatives.

+ Easier to report the strategies regularly

+ Enhance the connection and communication between employees and company

- Disadvantages (Salem, Hasnan, Nor, 2012)

+ BSC does not concentrate on external factors, which results in missing risk analysis

+ There is no time dimension to evaluate the performance

Question 2:

- Predetermined overhead rate: ($3.6 + $2) * 50% = $2.8

Standard cost of 1kg rice = material cost + direct labor cost + overhead cost =

$3.6 + $2 + $2.8 = $8.4

- Allocated overhead in October = $2.8 * 36000 = $100,800

- Actual overhead in October =$102,000

Under-allocated overhead accounted for Cost of goods sold (COGS):

$102,000 - $100,800 = $1,200

a company.

- Advantages (Mariana, 2015)

+ Help manager to decide which activities should be done and how to utilize the

resources

+ Help the company to control the actual costs and avoid over spending

- Disadvantages (Mariana, 2015):

+ Can be time-wasting and expensive

+ Can be strict and unrealistic

d. Balanced scorecard:

The balanced scorecard is a framework which is used for tracking and controlling

company’s strategies (Ted, n.d.). The manager can use BSC to determine both

financial and non-financial problems of the company.

- Advantages (Patricia, Lucia, Beatriz, 2017):

+ Provide a specific view of the strategy in both long-term and short-term

+ Allow the company to work on four perspectives at three levels: mission and vision,

goals, measures and innitiatives.

+ Easier to report the strategies regularly

+ Enhance the connection and communication between employees and company

- Disadvantages (Salem, Hasnan, Nor, 2012)

+ BSC does not concentrate on external factors, which results in missing risk analysis

+ There is no time dimension to evaluate the performance

Question 2:

- Predetermined overhead rate: ($3.6 + $2) * 50% = $2.8

Standard cost of 1kg rice = material cost + direct labor cost + overhead cost =

$3.6 + $2 + $2.8 = $8.4

- Allocated overhead in October = $2.8 * 36000 = $100,800

- Actual overhead in October =$102,000

Under-allocated overhead accounted for Cost of goods sold (COGS):

$102,000 - $100,800 = $1,200

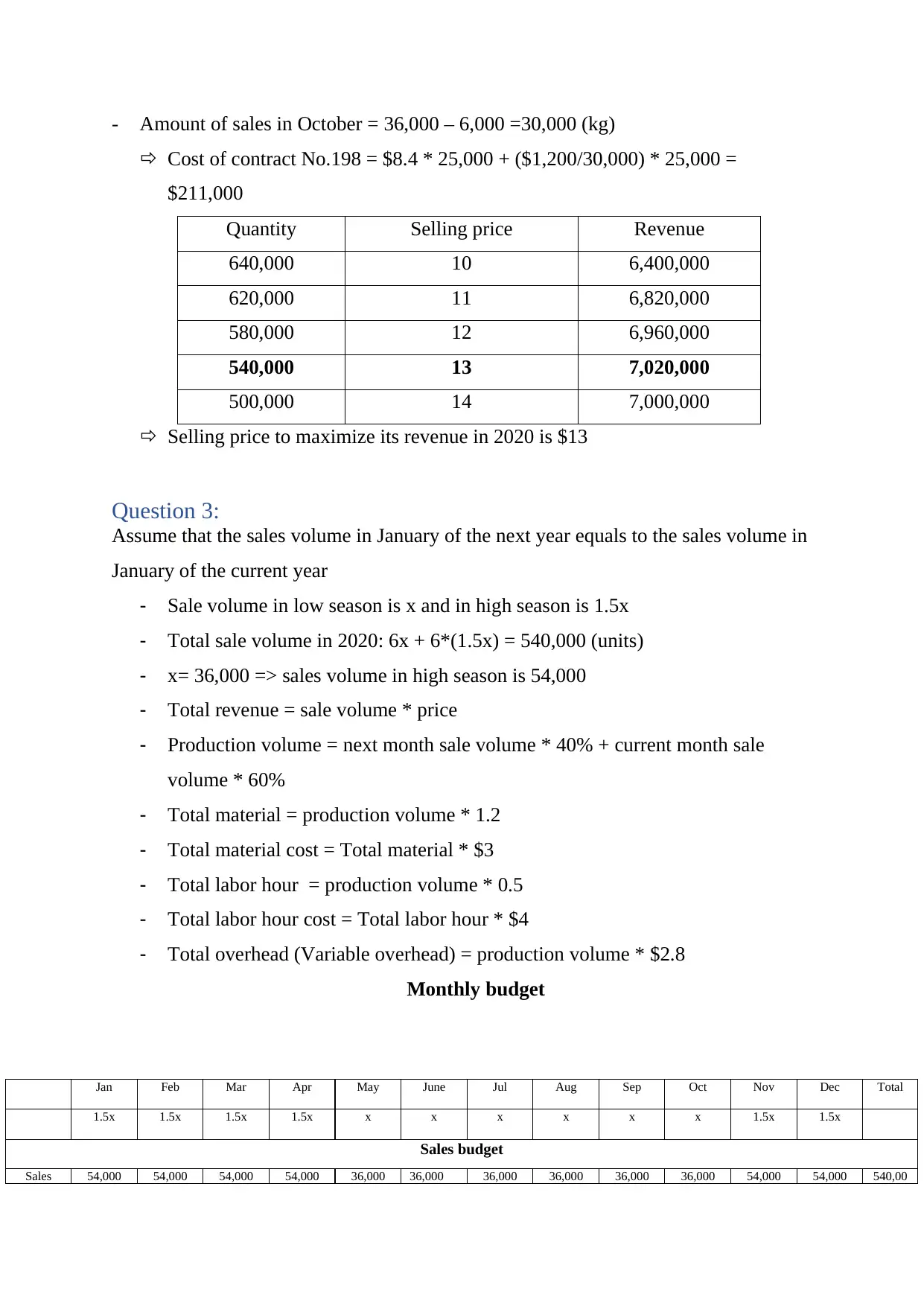

- Amount of sales in October = 36,000 – 6,000 =30,000 (kg)

Cost of contract No.198 = $8.4 * 25,000 + ($1,200/30,000) * 25,000 =

$211,000

Quantity Selling price Revenue

640,000 10 6,400,000

620,000 11 6,820,000

580,000 12 6,960,000

540,000 13 7,020,000

500,000 14 7,000,000

Selling price to maximize its revenue in 2020 is $13

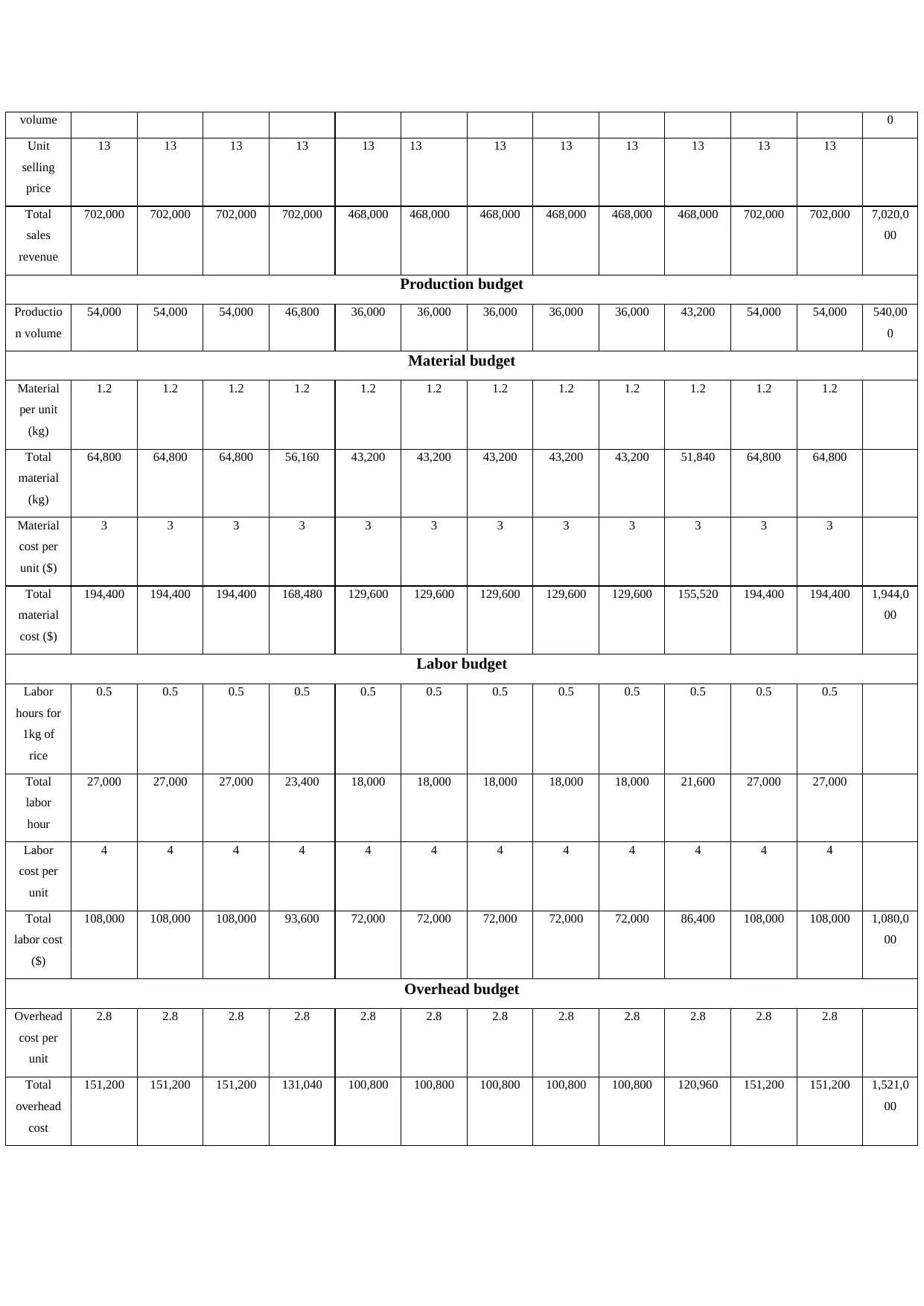

Question 3:

Assume that the sales volume in January of the next year equals to the sales volume in

January of the current year

- Sale volume in low season is x and in high season is 1.5x

- Total sale volume in 2020: 6x + 6*(1.5x) = 540,000 (units)

- x= 36,000 => sales volume in high season is 54,000

- Total revenue = sale volume * price

- Production volume = next month sale volume * 40% + current month sale

volume * 60%

- Total material = production volume * 1.2

- Total material cost = Total material * $3

- Total labor hour = production volume * 0.5

- Total labor hour cost = Total labor hour * $4

- Total overhead (Variable overhead) = production volume * $2.8

Monthly budget

Jan Feb Mar Apr May June Jul Aug Sep Oct Nov Dec Total

1.5x 1.5x 1.5x 1.5x x x x x x x 1.5x 1.5x

Sales budget

Sales 54,000 54,000 54,000 54,000 36,000 36,000 36,000 36,000 36,000 36,000 54,000 54,000 540,00

Cost of contract No.198 = $8.4 * 25,000 + ($1,200/30,000) * 25,000 =

$211,000

Quantity Selling price Revenue

640,000 10 6,400,000

620,000 11 6,820,000

580,000 12 6,960,000

540,000 13 7,020,000

500,000 14 7,000,000

Selling price to maximize its revenue in 2020 is $13

Question 3:

Assume that the sales volume in January of the next year equals to the sales volume in

January of the current year

- Sale volume in low season is x and in high season is 1.5x

- Total sale volume in 2020: 6x + 6*(1.5x) = 540,000 (units)

- x= 36,000 => sales volume in high season is 54,000

- Total revenue = sale volume * price

- Production volume = next month sale volume * 40% + current month sale

volume * 60%

- Total material = production volume * 1.2

- Total material cost = Total material * $3

- Total labor hour = production volume * 0.5

- Total labor hour cost = Total labor hour * $4

- Total overhead (Variable overhead) = production volume * $2.8

Monthly budget

Jan Feb Mar Apr May June Jul Aug Sep Oct Nov Dec Total

1.5x 1.5x 1.5x 1.5x x x x x x x 1.5x 1.5x

Sales budget

Sales 54,000 54,000 54,000 54,000 36,000 36,000 36,000 36,000 36,000 36,000 54,000 54,000 540,00

volume 0

Unit

selling

price

13 13 13 13 13 13 13 13 13 13 13 13

Total

sales

revenue

702,000 702,000 702,000 702,000 468,000 468,000 468,000 468,000 468,000 468,000 702,000 702,000 7,020,0

00

Production budget

Productio

n volume

54,000 54,000 54,000 46,800 36,000 36,000 36,000 36,000 36,000 43,200 54,000 54,000 540,00

0

Material budget

Material

per unit

(kg)

1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2

Total

material

(kg)

64,800 64,800 64,800 56,160 43,200 43,200 43,200 43,200 43,200 51,840 64,800 64,800

Material

cost per

unit ($)

3 3 3 3 3 3 3 3 3 3 3 3

Total

material

cost ($)

194,400 194,400 194,400 168,480 129,600 129,600 129,600 129,600 129,600 155,520 194,400 194,400 1,944,0

00

Labor budget

Labor

hours for

1kg of

rice

0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5

Total

labor

hour

27,000 27,000 27,000 23,400 18,000 18,000 18,000 18,000 18,000 21,600 27,000 27,000

Labor

cost per

unit

4 4 4 4 4 4 4 4 4 4 4 4

Total

labor cost

($)

108,000 108,000 108,000 93,600 72,000 72,000 72,000 72,000 72,000 86,400 108,000 108,000 1,080,0

00

Overhead budget

Overhead

cost per

unit

2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8

Total

overhead

cost

151,200 151,200 151,200 131,040 100,800 100,800 100,800 100,800 100,800 120,960 151,200 151,200 1,521,0

00

Unit

selling

price

13 13 13 13 13 13 13 13 13 13 13 13

Total

sales

revenue

702,000 702,000 702,000 702,000 468,000 468,000 468,000 468,000 468,000 468,000 702,000 702,000 7,020,0

00

Production budget

Productio

n volume

54,000 54,000 54,000 46,800 36,000 36,000 36,000 36,000 36,000 43,200 54,000 54,000 540,00

0

Material budget

Material

per unit

(kg)

1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2 1.2

Total

material

(kg)

64,800 64,800 64,800 56,160 43,200 43,200 43,200 43,200 43,200 51,840 64,800 64,800

Material

cost per

unit ($)

3 3 3 3 3 3 3 3 3 3 3 3

Total

material

cost ($)

194,400 194,400 194,400 168,480 129,600 129,600 129,600 129,600 129,600 155,520 194,400 194,400 1,944,0

00

Labor budget

Labor

hours for

1kg of

rice

0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5

Total

labor

hour

27,000 27,000 27,000 23,400 18,000 18,000 18,000 18,000 18,000 21,600 27,000 27,000

Labor

cost per

unit

4 4 4 4 4 4 4 4 4 4 4 4

Total

labor cost

($)

108,000 108,000 108,000 93,600 72,000 72,000 72,000 72,000 72,000 86,400 108,000 108,000 1,080,0

00

Overhead budget

Overhead

cost per

unit

2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8 2.8

Total

overhead

cost

151,200 151,200 151,200 131,040 100,800 100,800 100,800 100,800 100,800 120,960 151,200 151,200 1,521,0

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

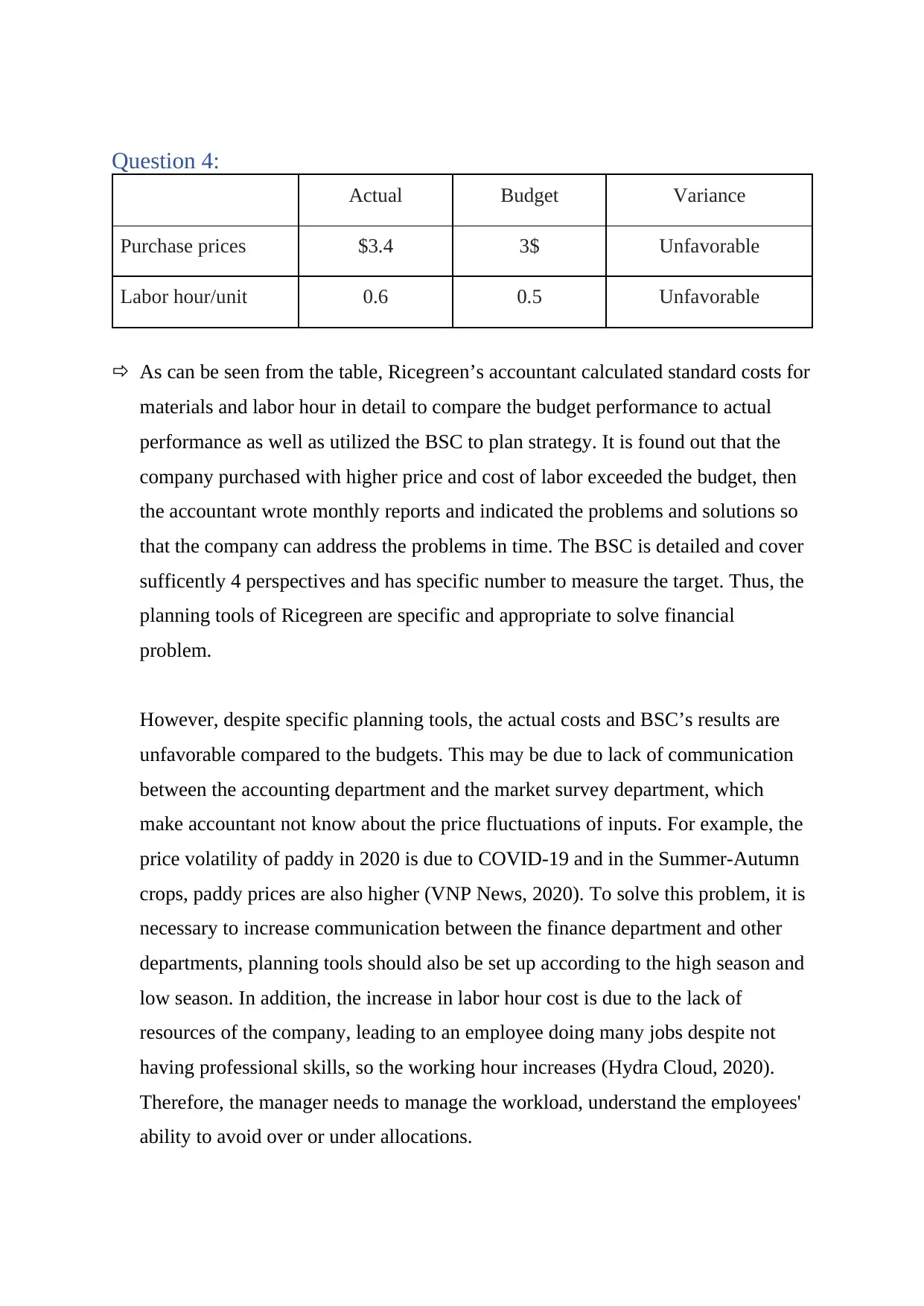

Question 4:

Actual Budget Variance

Purchase prices $3.4 3$ Unfavorable

Labor hour/unit 0.6 0.5 Unfavorable

As can be seen from the table, Ricegreen’s accountant calculated standard costs for

materials and labor hour in detail to compare the budget performance to actual

performance as well as utilized the BSC to plan strategy. It is found out that the

company purchased with higher price and cost of labor exceeded the budget, then

the accountant wrote monthly reports and indicated the problems and solutions so

that the company can address the problems in time. The BSC is detailed and cover

sufficently 4 perspectives and has specific number to measure the target. Thus, the

planning tools of Ricegreen are specific and appropriate to solve financial

problem.

However, despite specific planning tools, the actual costs and BSC’s results are

unfavorable compared to the budgets. This may be due to lack of communication

between the accounting department and the market survey department, which

make accountant not know about the price fluctuations of inputs. For example, the

price volatility of paddy in 2020 is due to COVID-19 and in the Summer-Autumn

crops, paddy prices are also higher (VNP News, 2020). To solve this problem, it is

necessary to increase communication between the finance department and other

departments, planning tools should also be set up according to the high season and

low season. In addition, the increase in labor hour cost is due to the lack of

resources of the company, leading to an employee doing many jobs despite not

having professional skills, so the working hour increases (Hydra Cloud, 2020).

Therefore, the manager needs to manage the workload, understand the employees'

ability to avoid over or under allocations.

Actual Budget Variance

Purchase prices $3.4 3$ Unfavorable

Labor hour/unit 0.6 0.5 Unfavorable

As can be seen from the table, Ricegreen’s accountant calculated standard costs for

materials and labor hour in detail to compare the budget performance to actual

performance as well as utilized the BSC to plan strategy. It is found out that the

company purchased with higher price and cost of labor exceeded the budget, then

the accountant wrote monthly reports and indicated the problems and solutions so

that the company can address the problems in time. The BSC is detailed and cover

sufficently 4 perspectives and has specific number to measure the target. Thus, the

planning tools of Ricegreen are specific and appropriate to solve financial

problem.

However, despite specific planning tools, the actual costs and BSC’s results are

unfavorable compared to the budgets. This may be due to lack of communication

between the accounting department and the market survey department, which

make accountant not know about the price fluctuations of inputs. For example, the

price volatility of paddy in 2020 is due to COVID-19 and in the Summer-Autumn

crops, paddy prices are also higher (VNP News, 2020). To solve this problem, it is

necessary to increase communication between the finance department and other

departments, planning tools should also be set up according to the high season and

low season. In addition, the increase in labor hour cost is due to the lack of

resources of the company, leading to an employee doing many jobs despite not

having professional skills, so the working hour increases (Hydra Cloud, 2020).

Therefore, the manager needs to manage the workload, understand the employees'

ability to avoid over or under allocations.

Question 5:

PEST analysis

Political

According to Nhat Linh (2018), Vietnamese government always supports cooperation on

producing and exporting rice as well as plans strategies for developing rice export markets.

Additionally, the rice production and export industry is supported a lot in terms of taxes by

the government, signing with CPTPP and EVFTA is also an advantage for Ricegreen

because there will be no more trade restrictions. Although these factors may help

Ricegreen expand its market and gain more revenue, the company also has to face high

requirements for rice quality as well as compete with many other rice exporters. Besides,

due to COVID-19, the government has a policy of restricting rice exports to ensure

domestic food sources and limit the risk of disease transmission (Nam Khanh, 2020),

which has a negative impact on Ricegreen due to its large inventory.

Economic

The growth rate, inflation rate, interest rate as well as exchange rate have significant

impact on the rice exporting industry. According to the statistics of Trading Economics

(2020), Vietnam’ GDP went up from 0.39% to 2.62% after the COVID pandamic. The

recovery of GDP after COVID-19 is a positive sign for rice industry because domestic

purchase goes up, then there will be higher rice consumption. Additionally, the low

inflation of 2.47 % in October of 2020 and the low interest rate result in the low cost of

capital, materials and labor, then the company can set the cheaper prices for consumers.

Moreover, the exchange rate in Vietnam is stable in 2020 (Nguyen Long, 2020), which

may bring Rice Green many benefits in export activity.

Social

Vietnam is an argricultural country with over 97 million of population is a potential market

of rice industry. Additionally, the annual growth rate in Vietnamese population is 1,12%,

which results in a prospective sales of rice company in the fututre. Furthermore, according

to the scenario 1, Vietnamese people currently takes more concern about health and accept

to pay more for high quality rice, this is a favorable point for higher sales because of

increasing consumption.

Technology

PEST analysis

Political

According to Nhat Linh (2018), Vietnamese government always supports cooperation on

producing and exporting rice as well as plans strategies for developing rice export markets.

Additionally, the rice production and export industry is supported a lot in terms of taxes by

the government, signing with CPTPP and EVFTA is also an advantage for Ricegreen

because there will be no more trade restrictions. Although these factors may help

Ricegreen expand its market and gain more revenue, the company also has to face high

requirements for rice quality as well as compete with many other rice exporters. Besides,

due to COVID-19, the government has a policy of restricting rice exports to ensure

domestic food sources and limit the risk of disease transmission (Nam Khanh, 2020),

which has a negative impact on Ricegreen due to its large inventory.

Economic

The growth rate, inflation rate, interest rate as well as exchange rate have significant

impact on the rice exporting industry. According to the statistics of Trading Economics

(2020), Vietnam’ GDP went up from 0.39% to 2.62% after the COVID pandamic. The

recovery of GDP after COVID-19 is a positive sign for rice industry because domestic

purchase goes up, then there will be higher rice consumption. Additionally, the low

inflation of 2.47 % in October of 2020 and the low interest rate result in the low cost of

capital, materials and labor, then the company can set the cheaper prices for consumers.

Moreover, the exchange rate in Vietnam is stable in 2020 (Nguyen Long, 2020), which

may bring Rice Green many benefits in export activity.

Social

Vietnam is an argricultural country with over 97 million of population is a potential market

of rice industry. Additionally, the annual growth rate in Vietnamese population is 1,12%,

which results in a prospective sales of rice company in the fututre. Furthermore, according

to the scenario 1, Vietnamese people currently takes more concern about health and accept

to pay more for high quality rice, this is a favorable point for higher sales because of

increasing consumption.

Technology

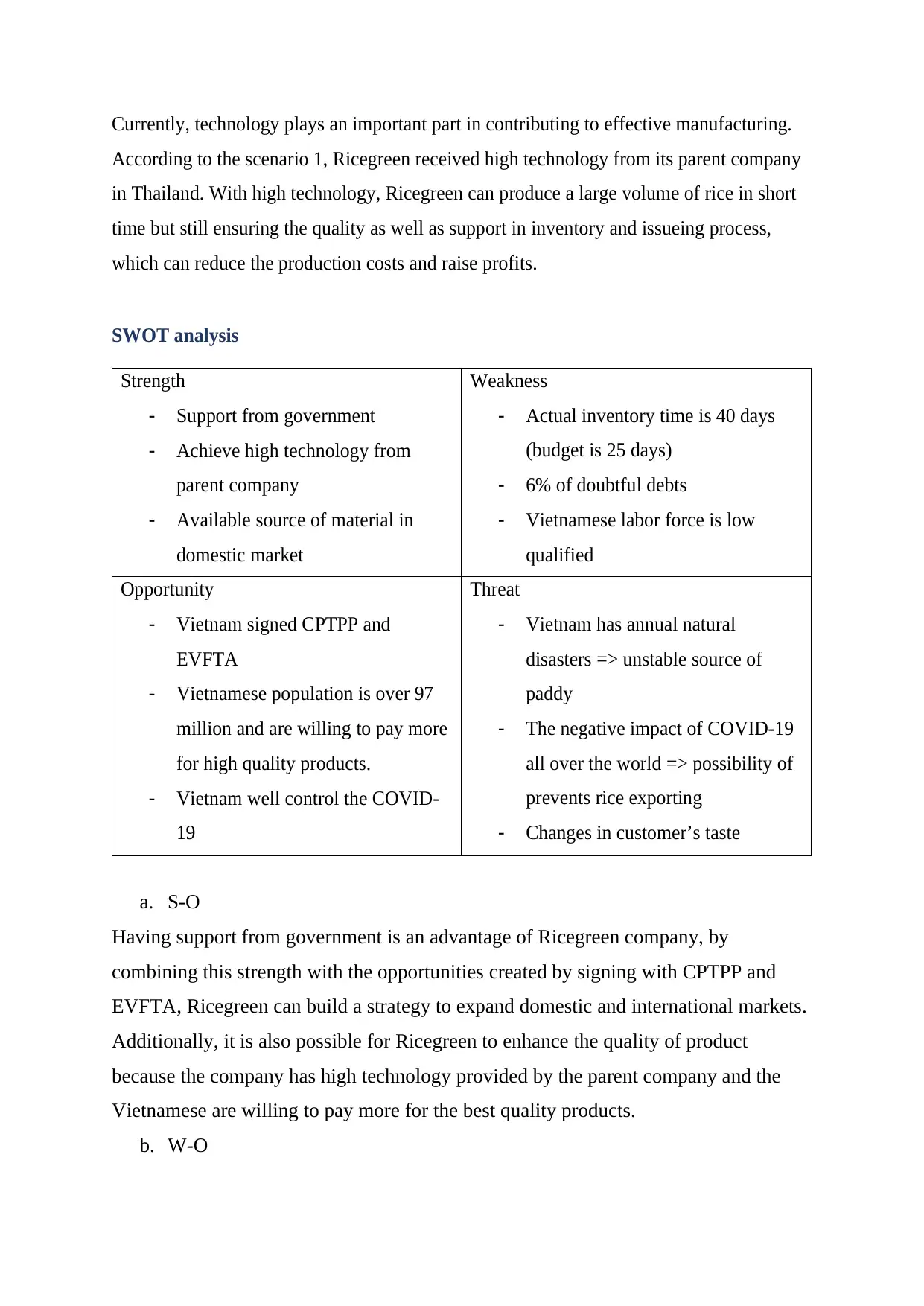

Currently, technology plays an important part in contributing to effective manufacturing.

According to the scenario 1, Ricegreen received high technology from its parent company

in Thailand. With high technology, Ricegreen can produce a large volume of rice in short

time but still ensuring the quality as well as support in inventory and issueing process,

which can reduce the production costs and raise profits.

SWOT analysis

Strength

- Support from government

- Achieve high technology from

parent company

- Available source of material in

domestic market

Weakness

- Actual inventory time is 40 days

(budget is 25 days)

- 6% of doubtful debts

- Vietnamese labor force is low

qualified

Opportunity

- Vietnam signed CPTPP and

EVFTA

- Vietnamese population is over 97

million and are willing to pay more

for high quality products.

- Vietnam well control the COVID-

19

Threat

- Vietnam has annual natural

disasters => unstable source of

paddy

- The negative impact of COVID-19

all over the world => possibility of

prevents rice exporting

- Changes in customer’s taste

a. S-O

Having support from government is an advantage of Ricegreen company, by

combining this strength with the opportunities created by signing with CPTPP and

EVFTA, Ricegreen can build a strategy to expand domestic and international markets.

Additionally, it is also possible for Ricegreen to enhance the quality of product

because the company has high technology provided by the parent company and the

Vietnamese are willing to pay more for the best quality products.

b. W-O

According to the scenario 1, Ricegreen received high technology from its parent company

in Thailand. With high technology, Ricegreen can produce a large volume of rice in short

time but still ensuring the quality as well as support in inventory and issueing process,

which can reduce the production costs and raise profits.

SWOT analysis

Strength

- Support from government

- Achieve high technology from

parent company

- Available source of material in

domestic market

Weakness

- Actual inventory time is 40 days

(budget is 25 days)

- 6% of doubtful debts

- Vietnamese labor force is low

qualified

Opportunity

- Vietnam signed CPTPP and

EVFTA

- Vietnamese population is over 97

million and are willing to pay more

for high quality products.

- Vietnam well control the COVID-

19

Threat

- Vietnam has annual natural

disasters => unstable source of

paddy

- The negative impact of COVID-19

all over the world => possibility of

prevents rice exporting

- Changes in customer’s taste

a. S-O

Having support from government is an advantage of Ricegreen company, by

combining this strength with the opportunities created by signing with CPTPP and

EVFTA, Ricegreen can build a strategy to expand domestic and international markets.

Additionally, it is also possible for Ricegreen to enhance the quality of product

because the company has high technology provided by the parent company and the

Vietnamese are willing to pay more for the best quality products.

b. W-O

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The poor labour force is a weakness of Ricegreen because using technology in rice

processing is still a new thing in Vietnam. However, this weakness can be overcome

because Vietnam has a large and intelligent labor force, along with easy access to

international markets thanks to the signing of CPTPP and EVFTA, Ricegreen can

learn knowledge and skills from foreign employees and train for Vietnamese

employees. The signing with CPTPP and EVFTA also helps Ricegreen export more

rice, thereby reducing inventory time.

c. S-T

In addition to its advantages, Ricegreen also faces a number of threats of natural

disasters and COVID-19. As an agricultural country, Vietnam is one of the five

countries most affected by climate change such as floods, droughts, and mangroves

(Nguyen Thi Lan, 2019). This seriously affects the inputs of Ricegreen. COVID-19 is

also a burden to the rice production and export. However, support from the

government can partly help the business overcome natural disasters, using technology

is also a good strategy to reduce the severity of natural disasters and epidemics.

d. W-T

A weakness of Ricegreen is the numer of doubtful debts of up to 6%, higher than

expected. To limit this, Ricegreen should have contracts with customers to deal with

the debt more easily. Additionally, Ricegreen should also invest in training courses for

employees so that they can performance better and increase productivity.

Balanced Scorecard analysis

In general, Ricegreen's BSC is specific and uses data to set strategic goals, but the

criteria set are not enough. In the Finance section, setting a goal to increase profit by

measuring the profit increase from the price and the sale volume is reasonable because

this will help the company try to sell more. However, Ricegreen plan to minimize

costs because the material costs and the labor costs of the company are higher

compared to the budget. In the customer perspective, the company should divide the

market share in the domestic market and the international market because Ricegreen

mainly focuses on exporting rice. In addition, it is unreasonable to measure market

share by % of market share, the measure should be the total revenue or sales volume

processing is still a new thing in Vietnam. However, this weakness can be overcome

because Vietnam has a large and intelligent labor force, along with easy access to

international markets thanks to the signing of CPTPP and EVFTA, Ricegreen can

learn knowledge and skills from foreign employees and train for Vietnamese

employees. The signing with CPTPP and EVFTA also helps Ricegreen export more

rice, thereby reducing inventory time.

c. S-T

In addition to its advantages, Ricegreen also faces a number of threats of natural

disasters and COVID-19. As an agricultural country, Vietnam is one of the five

countries most affected by climate change such as floods, droughts, and mangroves

(Nguyen Thi Lan, 2019). This seriously affects the inputs of Ricegreen. COVID-19 is

also a burden to the rice production and export. However, support from the

government can partly help the business overcome natural disasters, using technology

is also a good strategy to reduce the severity of natural disasters and epidemics.

d. W-T

A weakness of Ricegreen is the numer of doubtful debts of up to 6%, higher than

expected. To limit this, Ricegreen should have contracts with customers to deal with

the debt more easily. Additionally, Ricegreen should also invest in training courses for

employees so that they can performance better and increase productivity.

Balanced Scorecard analysis

In general, Ricegreen's BSC is specific and uses data to set strategic goals, but the

criteria set are not enough. In the Finance section, setting a goal to increase profit by

measuring the profit increase from the price and the sale volume is reasonable because

this will help the company try to sell more. However, Ricegreen plan to minimize

costs because the material costs and the labor costs of the company are higher

compared to the budget. In the customer perspective, the company should divide the

market share in the domestic market and the international market because Ricegreen

mainly focuses on exporting rice. In addition, it is unreasonable to measure market

share by % of market share, the measure should be the total revenue or sales volume

because market share equals the business sales / the market sales (tutor2u, 2016).

Moreover, customer satisfaction should be a measure because it can measure customer

loyalty, then helps the company identify the reason to solve and increase revenue

(Lisa Copley, 2017). To plan the strategy for internal business, the management

accountant did well because the measures for each indicators are suitable. In learning

anđ growh section, the management account should set strategy to train professional

skills for employees because the quality of labor is low. The measure for increase in

labor's technical skills should be KPIs and productivity because it helps the company

to know whether the business is on the right track or not (Marr, 2012). In conclusion,

the BSC of Ricegreen should add some other objectives to make the strategy more

sufficient, then the company can solve their existing problems and increase the

revenue.

Moreover, customer satisfaction should be a measure because it can measure customer

loyalty, then helps the company identify the reason to solve and increase revenue

(Lisa Copley, 2017). To plan the strategy for internal business, the management

accountant did well because the measures for each indicators are suitable. In learning

anđ growh section, the management account should set strategy to train professional

skills for employees because the quality of labor is low. The measure for increase in

labor's technical skills should be KPIs and productivity because it helps the company

to know whether the business is on the right track or not (Marr, 2012). In conclusion,

the BSC of Ricegreen should add some other objectives to make the strategy more

sufficient, then the company can solve their existing problems and increase the

revenue.

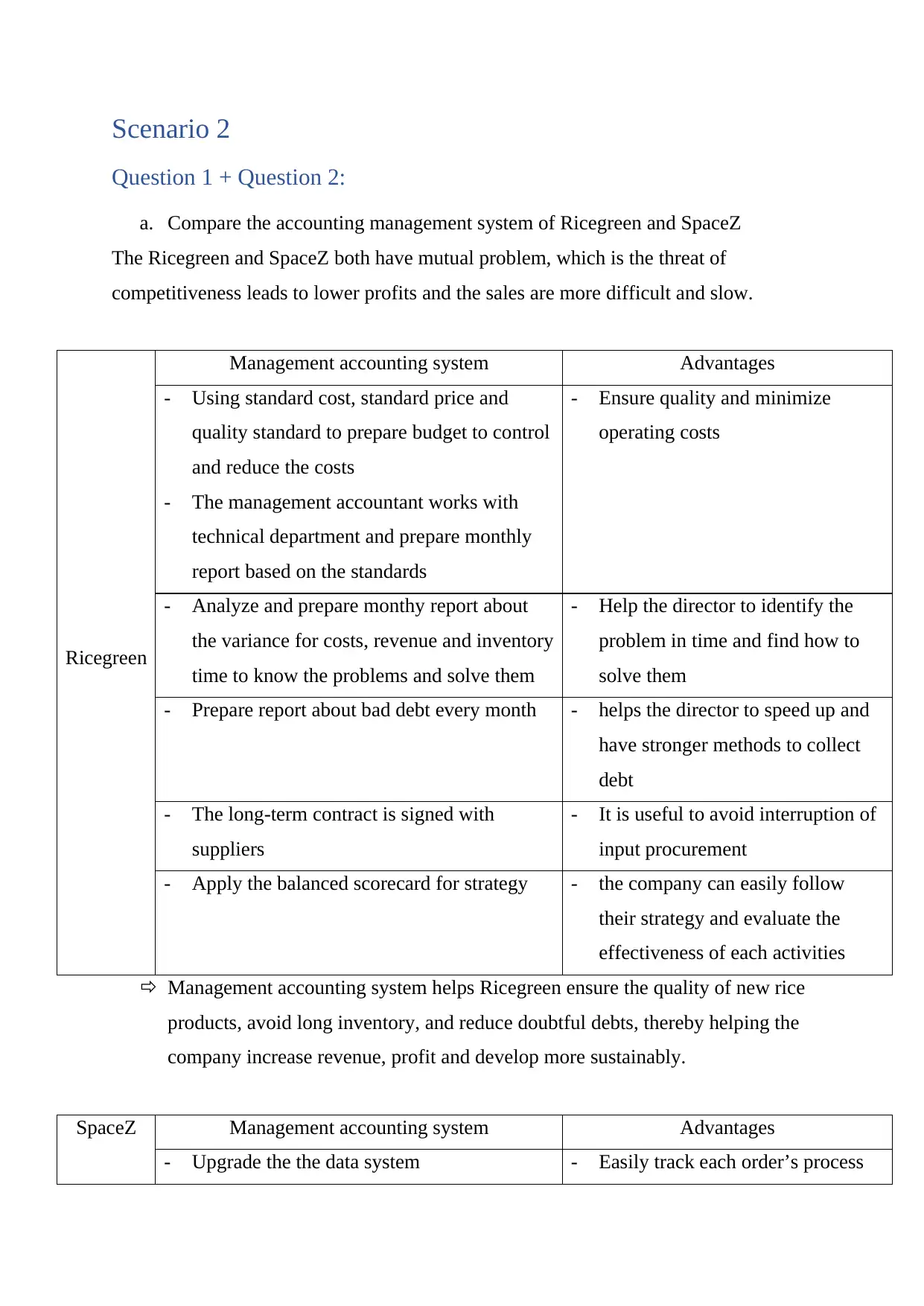

Scenario 2

Question 1 + Question 2:

a. Compare the accounting management system of Ricegreen and SpaceZ

The Ricegreen and SpaceZ both have mutual problem, which is the threat of

competitiveness leads to lower profits and the sales are more difficult and slow.

Ricegreen

Management accounting system Advantages

- Using standard cost, standard price and

quality standard to prepare budget to control

and reduce the costs

- The management accountant works with

technical department and prepare monthly

report based on the standards

- Ensure quality and minimize

operating costs

- Analyze and prepare monthy report about

the variance for costs, revenue and inventory

time to know the problems and solve them

- Help the director to identify the

problem in time and find how to

solve them

- Prepare report about bad debt every month - helps the director to speed up and

have stronger methods to collect

debt

- The long-term contract is signed with

suppliers

- It is useful to avoid interruption of

input procurement

- Apply the balanced scorecard for strategy - the company can easily follow

their strategy and evaluate the

effectiveness of each activities

Management accounting system helps Ricegreen ensure the quality of new rice

products, avoid long inventory, and reduce doubtful debts, thereby helping the

company increase revenue, profit and develop more sustainably.

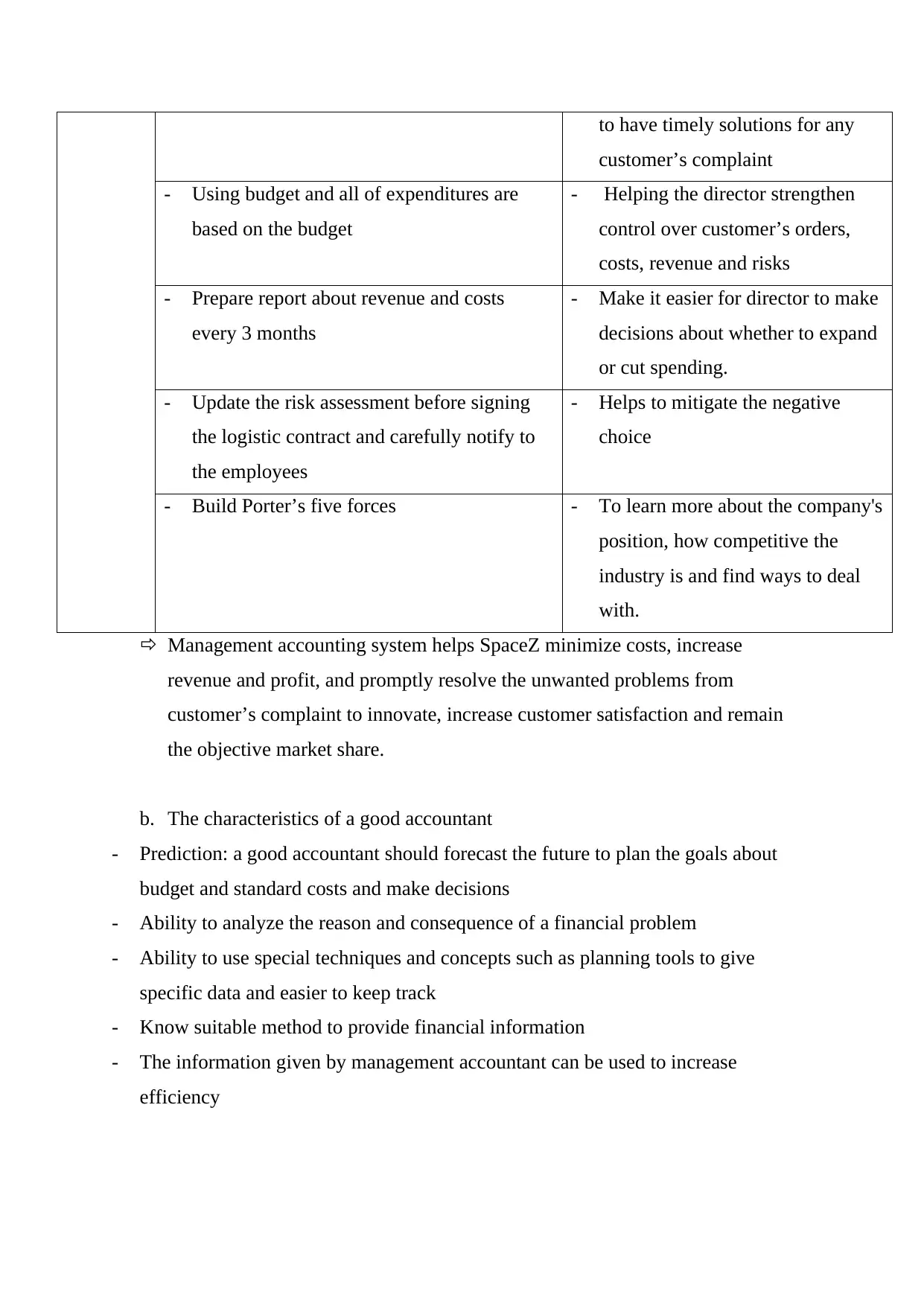

SpaceZ Management accounting system Advantages

- Upgrade the the data system - Easily track each order’s process

Question 1 + Question 2:

a. Compare the accounting management system of Ricegreen and SpaceZ

The Ricegreen and SpaceZ both have mutual problem, which is the threat of

competitiveness leads to lower profits and the sales are more difficult and slow.

Ricegreen

Management accounting system Advantages

- Using standard cost, standard price and

quality standard to prepare budget to control

and reduce the costs

- The management accountant works with

technical department and prepare monthly

report based on the standards

- Ensure quality and minimize

operating costs

- Analyze and prepare monthy report about

the variance for costs, revenue and inventory

time to know the problems and solve them

- Help the director to identify the

problem in time and find how to

solve them

- Prepare report about bad debt every month - helps the director to speed up and

have stronger methods to collect

debt

- The long-term contract is signed with

suppliers

- It is useful to avoid interruption of

input procurement

- Apply the balanced scorecard for strategy - the company can easily follow

their strategy and evaluate the

effectiveness of each activities

Management accounting system helps Ricegreen ensure the quality of new rice

products, avoid long inventory, and reduce doubtful debts, thereby helping the

company increase revenue, profit and develop more sustainably.

SpaceZ Management accounting system Advantages

- Upgrade the the data system - Easily track each order’s process

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to have timely solutions for any

customer’s complaint

- Using budget and all of expenditures are

based on the budget

- Helping the director strengthen

control over customer’s orders,

costs, revenue and risks

- Prepare report about revenue and costs

every 3 months

- Make it easier for director to make

decisions about whether to expand

or cut spending.

- Update the risk assessment before signing

the logistic contract and carefully notify to

the employees

- Helps to mitigate the negative

choice

- Build Porter’s five forces - To learn more about the company's

position, how competitive the

industry is and find ways to deal

with.

Management accounting system helps SpaceZ minimize costs, increase

revenue and profit, and promptly resolve the unwanted problems from

customer’s complaint to innovate, increase customer satisfaction and remain

the objective market share.

b. The characteristics of a good accountant

- Prediction: a good accountant should forecast the future to plan the goals about

budget and standard costs and make decisions

- Ability to analyze the reason and consequence of a financial problem

- Ability to use special techniques and concepts such as planning tools to give

specific data and easier to keep track

- Know suitable method to provide financial information

- The information given by management accountant can be used to increase

efficiency

customer’s complaint

- Using budget and all of expenditures are

based on the budget

- Helping the director strengthen

control over customer’s orders,

costs, revenue and risks

- Prepare report about revenue and costs

every 3 months

- Make it easier for director to make

decisions about whether to expand

or cut spending.

- Update the risk assessment before signing

the logistic contract and carefully notify to

the employees

- Helps to mitigate the negative

choice

- Build Porter’s five forces - To learn more about the company's

position, how competitive the

industry is and find ways to deal

with.

Management accounting system helps SpaceZ minimize costs, increase

revenue and profit, and promptly resolve the unwanted problems from

customer’s complaint to innovate, increase customer satisfaction and remain

the objective market share.

b. The characteristics of a good accountant

- Prediction: a good accountant should forecast the future to plan the goals about

budget and standard costs and make decisions

- Ability to analyze the reason and consequence of a financial problem

- Ability to use special techniques and concepts such as planning tools to give

specific data and easier to keep track

- Know suitable method to provide financial information

- The information given by management accountant can be used to increase

efficiency

Question 3:

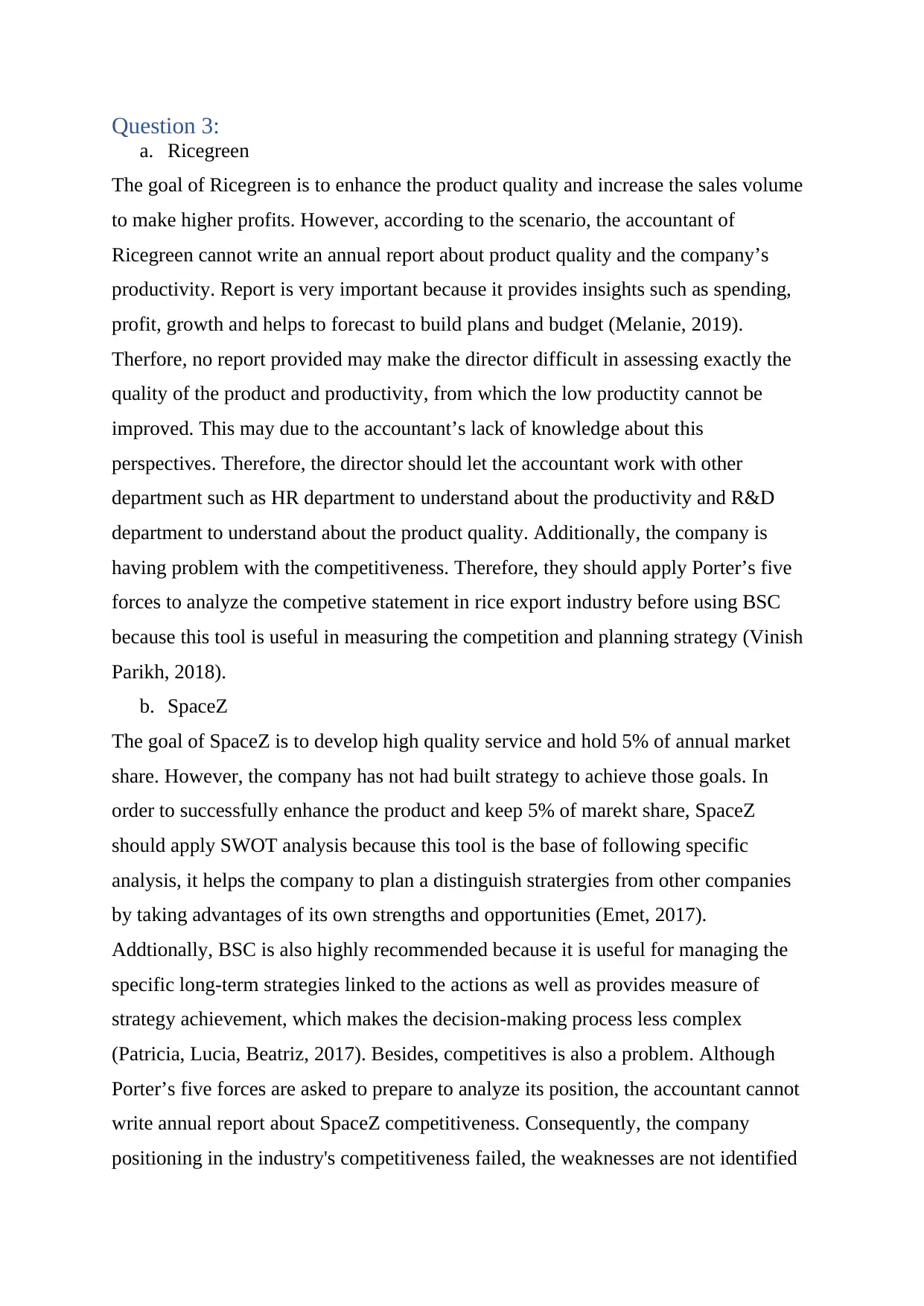

a. Ricegreen

The goal of Ricegreen is to enhance the product quality and increase the sales volume

to make higher profits. However, according to the scenario, the accountant of

Ricegreen cannot write an annual report about product quality and the company’s

productivity. Report is very important because it provides insights such as spending,

profit, growth and helps to forecast to build plans and budget (Melanie, 2019).

Therfore, no report provided may make the director difficult in assessing exactly the

quality of the product and productivity, from which the low productity cannot be

improved. This may due to the accountant’s lack of knowledge about this

perspectives. Therefore, the director should let the accountant work with other

department such as HR department to understand about the productivity and R&D

department to understand about the product quality. Additionally, the company is

having problem with the competitiveness. Therefore, they should apply Porter’s five

forces to analyze the competive statement in rice export industry before using BSC

because this tool is useful in measuring the competition and planning strategy (Vinish

Parikh, 2018).

b. SpaceZ

The goal of SpaceZ is to develop high quality service and hold 5% of annual market

share. However, the company has not had built strategy to achieve those goals. In

order to successfully enhance the product and keep 5% of marekt share, SpaceZ

should apply SWOT analysis because this tool is the base of following specific

analysis, it helps the company to plan a distinguish stratergies from other companies

by taking advantages of its own strengths and opportunities (Emet, 2017).

Addtionally, BSC is also highly recommended because it is useful for managing the

specific long-term strategies linked to the actions as well as provides measure of

strategy achievement, which makes the decision-making process less complex

(Patricia, Lucia, Beatriz, 2017). Besides, competitives is also a problem. Although

Porter’s five forces are asked to prepare to analyze its position, the accountant cannot

write annual report about SpaceZ competitiveness. Consequently, the company

positioning in the industry's competitiveness failed, the weaknesses are not identified

a. Ricegreen

The goal of Ricegreen is to enhance the product quality and increase the sales volume

to make higher profits. However, according to the scenario, the accountant of

Ricegreen cannot write an annual report about product quality and the company’s

productivity. Report is very important because it provides insights such as spending,

profit, growth and helps to forecast to build plans and budget (Melanie, 2019).

Therfore, no report provided may make the director difficult in assessing exactly the

quality of the product and productivity, from which the low productity cannot be

improved. This may due to the accountant’s lack of knowledge about this

perspectives. Therefore, the director should let the accountant work with other

department such as HR department to understand about the productivity and R&D

department to understand about the product quality. Additionally, the company is

having problem with the competitiveness. Therefore, they should apply Porter’s five

forces to analyze the competive statement in rice export industry before using BSC

because this tool is useful in measuring the competition and planning strategy (Vinish

Parikh, 2018).

b. SpaceZ

The goal of SpaceZ is to develop high quality service and hold 5% of annual market

share. However, the company has not had built strategy to achieve those goals. In

order to successfully enhance the product and keep 5% of marekt share, SpaceZ

should apply SWOT analysis because this tool is the base of following specific

analysis, it helps the company to plan a distinguish stratergies from other companies

by taking advantages of its own strengths and opportunities (Emet, 2017).

Addtionally, BSC is also highly recommended because it is useful for managing the

specific long-term strategies linked to the actions as well as provides measure of

strategy achievement, which makes the decision-making process less complex

(Patricia, Lucia, Beatriz, 2017). Besides, competitives is also a problem. Although

Porter’s five forces are asked to prepare to analyze its position, the accountant cannot

write annual report about SpaceZ competitiveness. Consequently, the company

positioning in the industry's competitiveness failed, the weaknesses are not identified

to be improved and the strengths are unknown to take advantage of, then leading to

slow sales and decreased profits. The reason for this problem may be because the

accountant does not know how to analyze company’s competitiveness. Therefore, the

accountant should join the Porter’s five forces analyzing process with MCKinsey

Vietnam to gain more experience.

slow sales and decreased profits. The reason for this problem may be because the

accountant does not know how to analyze company’s competitiveness. Therefore, the

accountant should join the Porter’s five forces analyzing process with MCKinsey

Vietnam to gain more experience.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

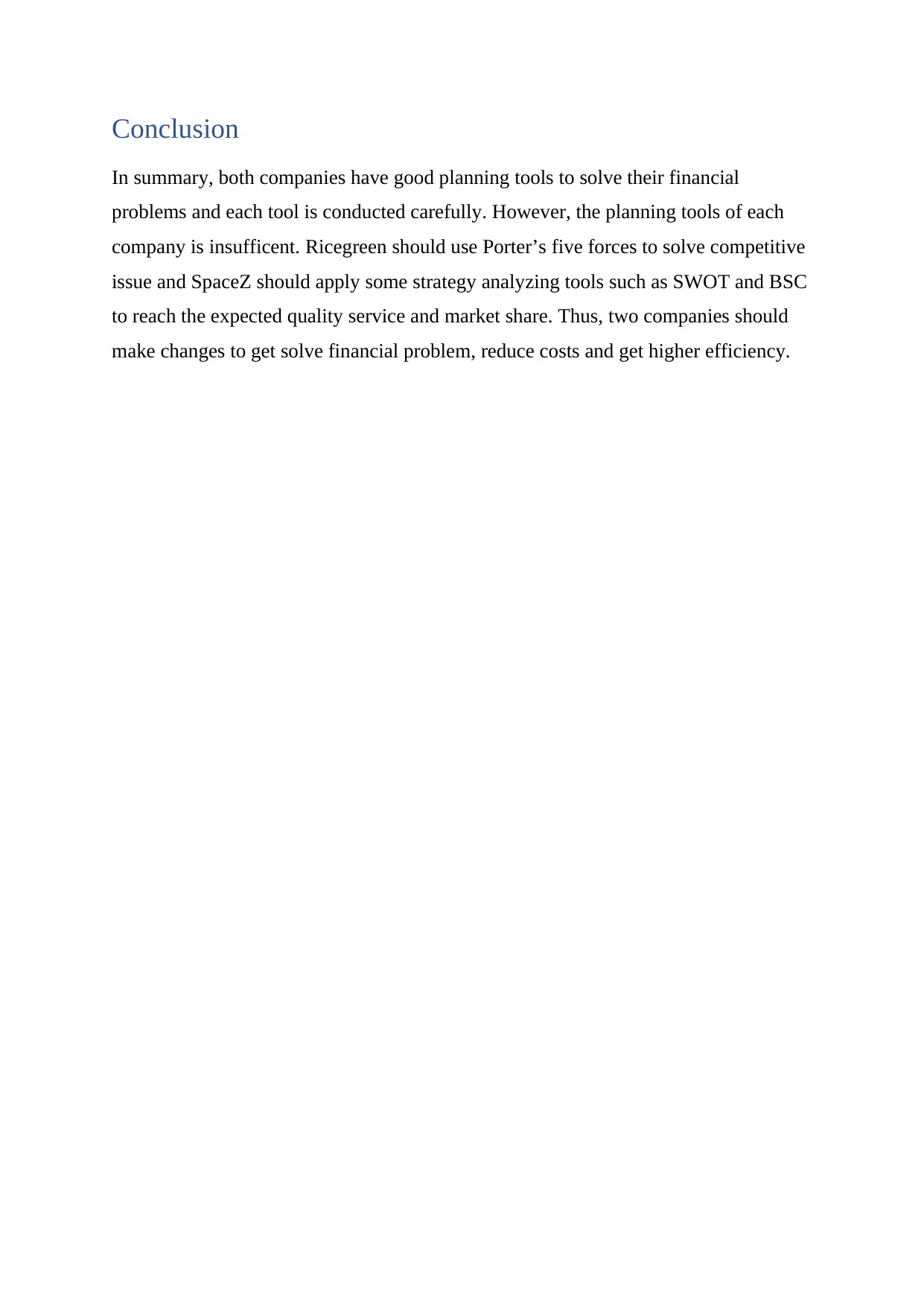

Conclusion

In summary, both companies have good planning tools to solve their financial

problems and each tool is conducted carefully. However, the planning tools of each

company is insufficent. Ricegreen should use Porter’s five forces to solve competitive

issue and SpaceZ should apply some strategy analyzing tools such as SWOT and BSC

to reach the expected quality service and market share. Thus, two companies should

make changes to get solve financial problem, reduce costs and get higher efficiency.

In summary, both companies have good planning tools to solve their financial

problems and each tool is conducted carefully. However, the planning tools of each

company is insufficent. Ricegreen should use Porter’s five forces to solve competitive

issue and SpaceZ should apply some strategy analyzing tools such as SWOT and BSC

to reach the expected quality service and market share. Thus, two companies should

make changes to get solve financial problem, reduce costs and get higher efficiency.

References

1. baodientu.chinhphu.vn. 2020. Lúa, Gạo Ở ĐBSCL Cùng Tăng Giá Vào Cuối

Vụ. [online] Available at: <http://baochinhphu.vn/Kinh-te/Lua-gao-o-DBSCL-

cung-tang-gia-vao-cuoi-vu/405238.vgp> [Accessed 9 December 2020].

2. Bragg, S., 2019. Standard Costing — Accountingtools. [online]

AccountingTools. Available at:

<https://www.accountingtools.com/articles/2017/5/14/standard-costing>

[Accessed 9 December 2020].

3. Emet, G., 2017. SWOT ANALYSIS: A THEORETICAL REVIEW. Journal of

International Social Research, [online] 10(51), pp.997-1000. Available at:

<http://researchgate.net/publication/319367788_SWOT_ANALYSIS_A_THE

ORETICAL_REVIEW> [Accessed 9 December 2020].

4. Harold, A., n.d. What Is A Budget? | Accountingcoach. [online]

AccountingCoach.com. Available at:

<https://www.accountingcoach.com/blog/what-is-a-budget-2#:~:text=A

%20budget%20is%20a%20financial,capital%20expenditures%20budget%2C

%20and%20others> [Accessed 9 December 2020].

5. Hydra.cloud. 2020. 5 Common Resource Planning Problems And How To

Solve Them. [online] Available at:

<https://www.hydra.cloud/en/resources/blog/131-5-common-resource-

planning-problems-and-how-to-solve-them> [Accessed 9 December 2020].

6. Lisa, C., 2017. 6 Reasons Why Customer Satisfaction Is Important. [online]

Allaboutcalls.co.uk. Available at: <https://www.allaboutcalls.co.uk/the-call-

takers-blog/6-reasons-why-customer-satisfaction-is-

important#:~:text=Customer%20satisfaction%20plays%20an

%20important,customers%20in%20competitive%20business

%20environments> [Accessed 9 December 2020].

7. Long, N., 2020. "Bắt Mạch" Tỷ Giá USD/VND Cuối Năm 202. [online]

TapChiTaiChinh. Available at: <http://tapchitaichinh.vn/ngan-hang/bat-mach-

ty-gia-usdvnd-cuoi-nam-2020-328745.html> [Accessed 6 December 2020].

1. baodientu.chinhphu.vn. 2020. Lúa, Gạo Ở ĐBSCL Cùng Tăng Giá Vào Cuối

Vụ. [online] Available at: <http://baochinhphu.vn/Kinh-te/Lua-gao-o-DBSCL-

cung-tang-gia-vao-cuoi-vu/405238.vgp> [Accessed 9 December 2020].

2. Bragg, S., 2019. Standard Costing — Accountingtools. [online]

AccountingTools. Available at:

<https://www.accountingtools.com/articles/2017/5/14/standard-costing>

[Accessed 9 December 2020].

3. Emet, G., 2017. SWOT ANALYSIS: A THEORETICAL REVIEW. Journal of

International Social Research, [online] 10(51), pp.997-1000. Available at:

<http://researchgate.net/publication/319367788_SWOT_ANALYSIS_A_THE

ORETICAL_REVIEW> [Accessed 9 December 2020].

4. Harold, A., n.d. What Is A Budget? | Accountingcoach. [online]

AccountingCoach.com. Available at:

<https://www.accountingcoach.com/blog/what-is-a-budget-2#:~:text=A

%20budget%20is%20a%20financial,capital%20expenditures%20budget%2C

%20and%20others> [Accessed 9 December 2020].

5. Hydra.cloud. 2020. 5 Common Resource Planning Problems And How To

Solve Them. [online] Available at:

<https://www.hydra.cloud/en/resources/blog/131-5-common-resource-

planning-problems-and-how-to-solve-them> [Accessed 9 December 2020].

6. Lisa, C., 2017. 6 Reasons Why Customer Satisfaction Is Important. [online]

Allaboutcalls.co.uk. Available at: <https://www.allaboutcalls.co.uk/the-call-

takers-blog/6-reasons-why-customer-satisfaction-is-

important#:~:text=Customer%20satisfaction%20plays%20an

%20important,customers%20in%20competitive%20business

%20environments> [Accessed 9 December 2020].

7. Long, N., 2020. "Bắt Mạch" Tỷ Giá USD/VND Cuối Năm 202. [online]

TapChiTaiChinh. Available at: <http://tapchitaichinh.vn/ngan-hang/bat-mach-

ty-gia-usdvnd-cuoi-nam-2020-328745.html> [Accessed 6 December 2020].

8. Mariana, Z., 2015. The pros and cons of budgeting system within economic

entities. Transilvania University of Braşov, [online] 8(57), pp.187-189.

Available at: <http://webbut.unitbv.ro/BU2015/Series%20V/BULETIN%20I

%20PDF/22_Zamfir_M.pdf> [Accessed 9 December 2020].

9. Marr, B., 2012. Key Performance Indicators. Harlow, England [etc]: Pearson

Education

10. Melanie, 2019. Why Business Reporting Is Important For Business Success -

Unleashed Software. [online] Unleashed Software. Available at:

<https://www.unleashedsoftware.com/blog/why-business-reporting-is-

important-for-business-success> [Accessed 9 December 2020].

11. Nam Khánh, 2020. Hạn Chế Xuất Khẩu Gạo: Doanh Nghiệp Rơi Cảnh Tiến

Thoái Lưỡng Nan. [online] vietnambiz. Available at:

<https://vietnambiz.vn/han-che-xuat-khau-gao-doanh-nghiep-roi-canh-tien-

thoai-luong-nan-20200410071149592.htm> [Accessed 9 December 2020].

12. Nhat Linh, 2018. Phó Thủ Tướng: Việt Nam Ủng Hộ Hợp Tác Quốc Tế Về Sản

Xuất, Thương Mại Gạo. [online] thoibaokinhdoanh.vn. Available at:

<https://thoibaokinhdoanh.vn/viet-nam/pho-thu-tuong-viet-nam-ung-ho-hop-

tac-quoc-te-ve-san-xuat-thuong-mai-gao-1051466.html> [Accessed 9

December 2020].

13. Parikh, V., 2018. Porter Five Forces Model Advantages And Disadvantages.

[online] Letslearnfinance.com. Available at:

<https://www.letslearnfinance.com/porter-five-forces-model-advantages-and-

disadvantages.html> [Accessed 9 December 2020].

14. Paul, E., 2016. IMPLICATIONS OF STANDARD COSTING SYSTEM IN

MANUFACTURING: A CASE STUDY. [online] 5(3), pp.162-164. Available

at:

<https://www.researchgate.net/publication/306446664_IMPLICATIONS_OF_

STANDARD_COSTING_SYSTEM_IN_MANUFACTURING_A_CASE_ST

UDY> [Accessed 9 December 2020].

15. Salem, M., Hasnan, N. and Nor, H., 2012. BALANCED SCORECARD:

WEAKNESSES, STRENGTHS, and ITS ABILITY as PERFORMANCE

entities. Transilvania University of Braşov, [online] 8(57), pp.187-189.

Available at: <http://webbut.unitbv.ro/BU2015/Series%20V/BULETIN%20I

%20PDF/22_Zamfir_M.pdf> [Accessed 9 December 2020].

9. Marr, B., 2012. Key Performance Indicators. Harlow, England [etc]: Pearson

Education

10. Melanie, 2019. Why Business Reporting Is Important For Business Success -

Unleashed Software. [online] Unleashed Software. Available at:

<https://www.unleashedsoftware.com/blog/why-business-reporting-is-

important-for-business-success> [Accessed 9 December 2020].

11. Nam Khánh, 2020. Hạn Chế Xuất Khẩu Gạo: Doanh Nghiệp Rơi Cảnh Tiến

Thoái Lưỡng Nan. [online] vietnambiz. Available at:

<https://vietnambiz.vn/han-che-xuat-khau-gao-doanh-nghiep-roi-canh-tien-

thoai-luong-nan-20200410071149592.htm> [Accessed 9 December 2020].

12. Nhat Linh, 2018. Phó Thủ Tướng: Việt Nam Ủng Hộ Hợp Tác Quốc Tế Về Sản

Xuất, Thương Mại Gạo. [online] thoibaokinhdoanh.vn. Available at:

<https://thoibaokinhdoanh.vn/viet-nam/pho-thu-tuong-viet-nam-ung-ho-hop-

tac-quoc-te-ve-san-xuat-thuong-mai-gao-1051466.html> [Accessed 9

December 2020].

13. Parikh, V., 2018. Porter Five Forces Model Advantages And Disadvantages.

[online] Letslearnfinance.com. Available at:

<https://www.letslearnfinance.com/porter-five-forces-model-advantages-and-

disadvantages.html> [Accessed 9 December 2020].

14. Paul, E., 2016. IMPLICATIONS OF STANDARD COSTING SYSTEM IN

MANUFACTURING: A CASE STUDY. [online] 5(3), pp.162-164. Available

at:

<https://www.researchgate.net/publication/306446664_IMPLICATIONS_OF_

STANDARD_COSTING_SYSTEM_IN_MANUFACTURING_A_CASE_ST

UDY> [Accessed 9 December 2020].

15. Salem, M., Hasnan, N. and Nor, H., 2012. BALANCED SCORECARD:

WEAKNESSES, STRENGTHS, and ITS ABILITY as PERFORMANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT SYSTEM VERSUS OTHER PERFORMANCE

MANAGEMENT SYSTEMS. Journal of Environment and Earth Science,

[online] 2(9), pp.6,7. Available at:

<https://www.researchgate.net/publication/308118049_BALANCED_SCORE

CARD_WEAKNESSES_STRENGTHS_and_ITS_ABILITY_as_PERFORMA

NCE_MANAGEMENT_SYSTEM_VERSUS_OTHER_PERFORMANCE_M

ANAGEMENT_SYSTEMS> [Accessed 9 December 2020].

16. Ted, J., n.d. What Is A Balanced Scorecard? (A Definition). [online] ClearPoint

Strategy. Available at: <https://www.clearpointstrategy.com/what-is-a-

balanced-scorecard-definition/> [Accessed 9 December 2020].

17. Thi Lan, N., 2019. Nghiên Cứu Ảnh Hưởng Của Biến Đổi Khí Hậu Tới Kinh

Tế Nông Nghiệp Việt Nam. [online] TapChiTaiChinh. Available at:

<http://tapchitaichinh.vn/nghien-cuu-trao-doi/nghien-cuu-anh-huong-cua-bien-

doi-khi-hau-toi-kinh-te-nong-nghiep-viet-nam-313379.html> [Accessed 9

December 2020].

18. Tradingeconomics.com. 2020. Vietnam GDP Annual Growth Rate | 2000-2020

Data | 2021-2022 Forecast | Calendar. [online] Available at:

<https://tradingeconomics.com/vietnam/gdp-growth-annual> [Accessed 5

December 2020].

19. tutor2u, 2016. Marketing: Calculating Market Share. [video] Available at:

<https://www.youtube.com/watch?v=7XifAlvu7-k> [Accessed 9 December

2020].

MANAGEMENT SYSTEMS. Journal of Environment and Earth Science,

[online] 2(9), pp.6,7. Available at:

<https://www.researchgate.net/publication/308118049_BALANCED_SCORE

CARD_WEAKNESSES_STRENGTHS_and_ITS_ABILITY_as_PERFORMA

NCE_MANAGEMENT_SYSTEM_VERSUS_OTHER_PERFORMANCE_M

ANAGEMENT_SYSTEMS> [Accessed 9 December 2020].

16. Ted, J., n.d. What Is A Balanced Scorecard? (A Definition). [online] ClearPoint

Strategy. Available at: <https://www.clearpointstrategy.com/what-is-a-

balanced-scorecard-definition/> [Accessed 9 December 2020].

17. Thi Lan, N., 2019. Nghiên Cứu Ảnh Hưởng Của Biến Đổi Khí Hậu Tới Kinh

Tế Nông Nghiệp Việt Nam. [online] TapChiTaiChinh. Available at:

<http://tapchitaichinh.vn/nghien-cuu-trao-doi/nghien-cuu-anh-huong-cua-bien-

doi-khi-hau-toi-kinh-te-nong-nghiep-viet-nam-313379.html> [Accessed 9

December 2020].

18. Tradingeconomics.com. 2020. Vietnam GDP Annual Growth Rate | 2000-2020

Data | 2021-2022 Forecast | Calendar. [online] Available at:

<https://tradingeconomics.com/vietnam/gdp-growth-annual> [Accessed 5

December 2020].

19. tutor2u, 2016. Marketing: Calculating Market Share. [video] Available at:

<https://www.youtube.com/watch?v=7XifAlvu7-k> [Accessed 9 December

2020].

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.