Impact of Modernization of Oil and Gas Reporting Requirement on Value Relevance of Financial Statements of US Oil and Gas Registrants

VerifiedAdded on 2023/06/15

|67

|20161

|65

AI Summary

This research study analyses the impact of modernization of the Oil and Gas Reporting Requirement on the value relevance of the financial statements of US Oil and Gas registrants. It includes a literature review, research methodology, data analysis, and recommendations for future research.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MSC OIL AND GAS ACCOUNTING

Msc Oil and Gas Accounting

Name of the student:

Name of the University:

Author note

Msc Oil and Gas Accounting

Name of the student:

Name of the University:

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MSC OIL AND GAS ACCOUNTING

Abstract:

This research was aimed to analyse the financial statement impact through the modernization

of the Oil and Gas Reporting Requirement which was proposed Rule and effective from the

January 1, 2010. In addition to this, the report has analysed the impact of the same on the

previously applicable rule. The report portrayed an in-depth literature review of the previous

researches regarding the performance and reason of the modernisation program brought in by

the SEC and next to this it has traced the various changes occurred due to the same. As per

the analysis it could be stated that during 2009, 2008 SEC issued the final rule revising the

requirement of disclosure related to the oil and gas reserves. As per the final rule, SEC

reflects consideration of comments received from the stakeholders in response to the

proposed rule brought in by the SEC. It has also been found that it is necessary to make

amendments in the financial reporting procedures for the US organizations to ensure

transparency in their disclosures. The oil and gas industry is not an exception to this regime,

as this sector carries numerous benefits for different groups of stakeholders, however during

the research only few firms operating and Oil and Gas sector in US has been chosen that

restricts the finding of the study.

Key words: SEC proposed rule, SEC proposed rule effective from 2010, Modernization of

the Oil and Gas Reporting Requirement, Value relevance of the financial statements of

United State Oil and Gas registrants

Abstract:

This research was aimed to analyse the financial statement impact through the modernization

of the Oil and Gas Reporting Requirement which was proposed Rule and effective from the

January 1, 2010. In addition to this, the report has analysed the impact of the same on the

previously applicable rule. The report portrayed an in-depth literature review of the previous

researches regarding the performance and reason of the modernisation program brought in by

the SEC and next to this it has traced the various changes occurred due to the same. As per

the analysis it could be stated that during 2009, 2008 SEC issued the final rule revising the

requirement of disclosure related to the oil and gas reserves. As per the final rule, SEC

reflects consideration of comments received from the stakeholders in response to the

proposed rule brought in by the SEC. It has also been found that it is necessary to make

amendments in the financial reporting procedures for the US organizations to ensure

transparency in their disclosures. The oil and gas industry is not an exception to this regime,

as this sector carries numerous benefits for different groups of stakeholders, however during

the research only few firms operating and Oil and Gas sector in US has been chosen that

restricts the finding of the study.

Key words: SEC proposed rule, SEC proposed rule effective from 2010, Modernization of

the Oil and Gas Reporting Requirement, Value relevance of the financial statements of

United State Oil and Gas registrants

2MSC OIL AND GAS ACCOUNTING

Table of Contents

CHAPTER 1: INTRODUCTION:.............................................................................................4

1. Introduction:.......................................................................................................................4

2. Background of the study:...................................................................................................5

3. Research aim and objective:...............................................................................................6

3.1 Research aim:...............................................................................................................6

3.1 Objective of the study:.................................................................................................7

3.2 Research question:.......................................................................................................7

4. Justification of the study:...................................................................................................7

5. Structure of the research:...................................................................................................8

6. Chapter summary:..............................................................................................................9

CHAPTER 2: LITERATURE REVIEW:..................................................................................9

1. Introduction........................................................................................................................9

2. A brief Overview:............................................................................................................10

3. The implications of the modernization:...........................................................................10

4. Some new rules under the amendment:...........................................................................11

5. Addition of new products:................................................................................................13

6. Communication with the SEC:.........................................................................................13

7. Impact on accounting literature:.......................................................................................14

8. Consistency with the rules of FASB and the IASB:........................................................14

8.1 Contradictory capitalisation approach between mining and oil and gas related activities:

..............................................................................................................................................15

8.2 Oil and Gas Reserves: Meaning and Importance...........................................................16

8.2.1 Types of Oil and Gas Reserves...............................................................................17

8.2.2 Oil and Gas Reserves in the contemporary period..................................................19

8.2.3 Importance of Oil and Gas Reserves.......................................................................21

8.3 Evolution of Reserves and their disclosure....................................................................23

8.4 Modernization of Oil and Gas Reporting: Reasons and Implications............................25

8.4.1 Reasons behind the Modernization of Oil and Gas Reporting................................25

8.4.2 SEC Modernization of Oil and Gas Reporting of 2009..........................................26

9. Road of modernization:....................................................................................................28

10. Role of Third Party Firm in oil and gas reserve modernization:....................................29

11. Conclusion:....................................................................................................................30

CHAPTER 3: RESEARCH METHODOLOGY:....................................................................31

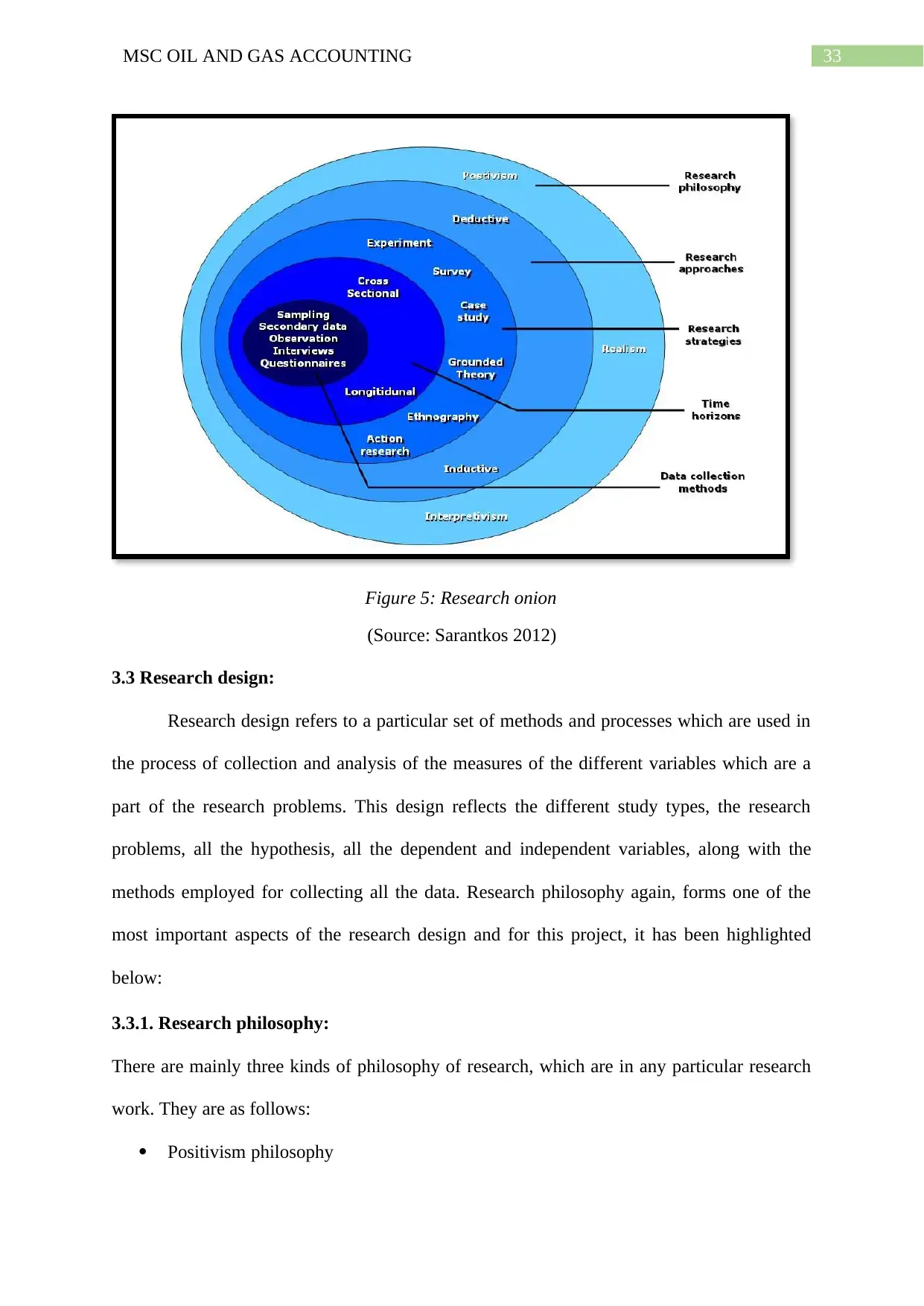

1. Introduction:.....................................................................................................................31

2. Research Onion:...............................................................................................................32

3. Research design:...............................................................................................................33

3.1. Research philosophy:................................................................................................33

3.2 Research approach:....................................................................................................35

4. Objectives of the research:...............................................................................................36

4.1 Research aim:.............................................................................................................36

4.2 Objective of the study:...............................................................................................36

4.3 Research question:.....................................................................................................37

Table of Contents

CHAPTER 1: INTRODUCTION:.............................................................................................4

1. Introduction:.......................................................................................................................4

2. Background of the study:...................................................................................................5

3. Research aim and objective:...............................................................................................6

3.1 Research aim:...............................................................................................................6

3.1 Objective of the study:.................................................................................................7

3.2 Research question:.......................................................................................................7

4. Justification of the study:...................................................................................................7

5. Structure of the research:...................................................................................................8

6. Chapter summary:..............................................................................................................9

CHAPTER 2: LITERATURE REVIEW:..................................................................................9

1. Introduction........................................................................................................................9

2. A brief Overview:............................................................................................................10

3. The implications of the modernization:...........................................................................10

4. Some new rules under the amendment:...........................................................................11

5. Addition of new products:................................................................................................13

6. Communication with the SEC:.........................................................................................13

7. Impact on accounting literature:.......................................................................................14

8. Consistency with the rules of FASB and the IASB:........................................................14

8.1 Contradictory capitalisation approach between mining and oil and gas related activities:

..............................................................................................................................................15

8.2 Oil and Gas Reserves: Meaning and Importance...........................................................16

8.2.1 Types of Oil and Gas Reserves...............................................................................17

8.2.2 Oil and Gas Reserves in the contemporary period..................................................19

8.2.3 Importance of Oil and Gas Reserves.......................................................................21

8.3 Evolution of Reserves and their disclosure....................................................................23

8.4 Modernization of Oil and Gas Reporting: Reasons and Implications............................25

8.4.1 Reasons behind the Modernization of Oil and Gas Reporting................................25

8.4.2 SEC Modernization of Oil and Gas Reporting of 2009..........................................26

9. Road of modernization:....................................................................................................28

10. Role of Third Party Firm in oil and gas reserve modernization:....................................29

11. Conclusion:....................................................................................................................30

CHAPTER 3: RESEARCH METHODOLOGY:....................................................................31

1. Introduction:.....................................................................................................................31

2. Research Onion:...............................................................................................................32

3. Research design:...............................................................................................................33

3.1. Research philosophy:................................................................................................33

3.2 Research approach:....................................................................................................35

4. Objectives of the research:...............................................................................................36

4.1 Research aim:.............................................................................................................36

4.2 Objective of the study:...............................................................................................36

4.3 Research question:.....................................................................................................37

3MSC OIL AND GAS ACCOUNTING

5. Data Collection:...............................................................................................................37

6. Sampling method:............................................................................................................40

7. Conclusion:......................................................................................................................41

CHAPTER 4: DATA ANALYSIS...........................................................................................41

1. Introduction:.....................................................................................................................41

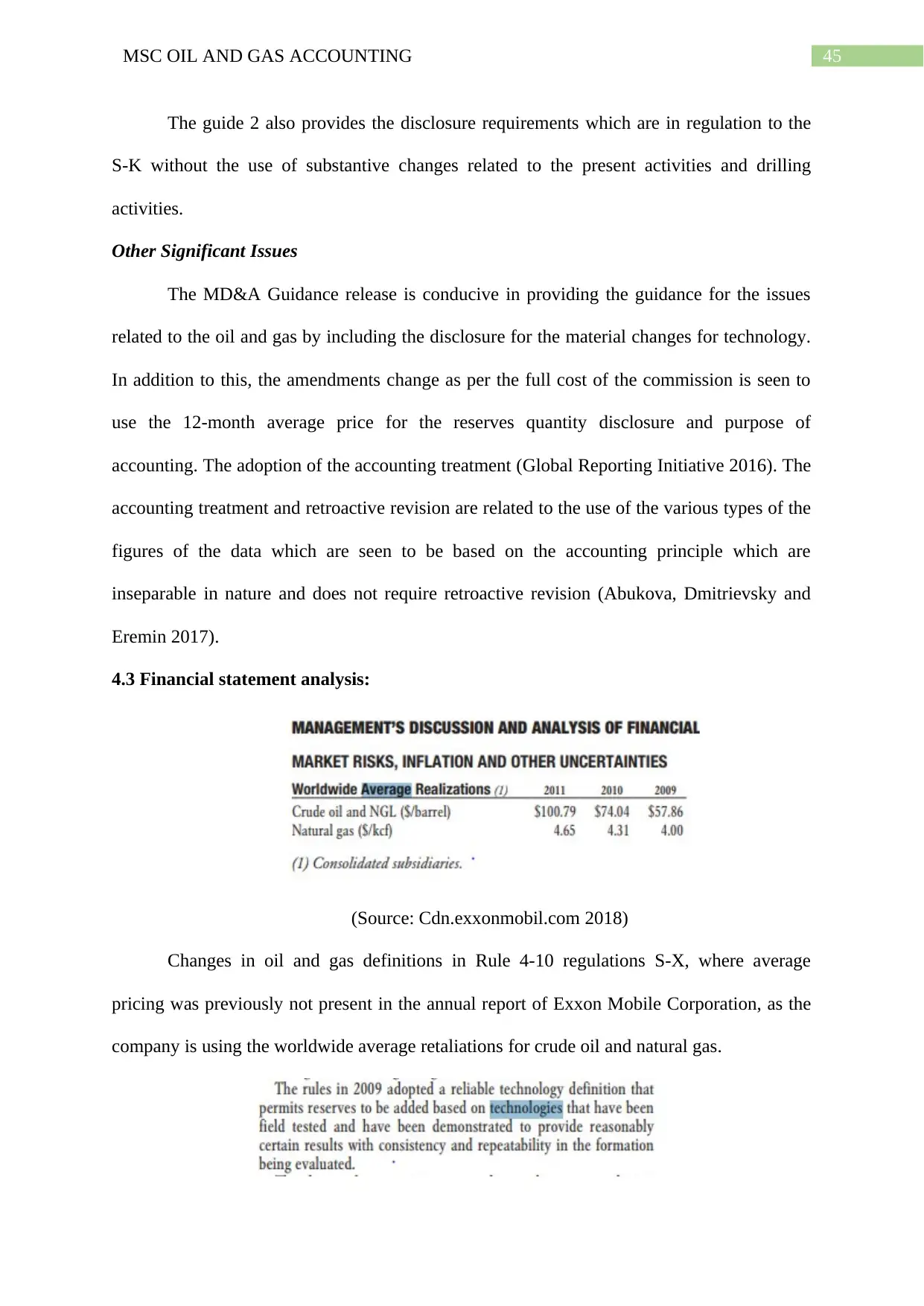

2. Deviations pertaining to the gas definitions in the Rule 4-10 of Regulation S-X............42

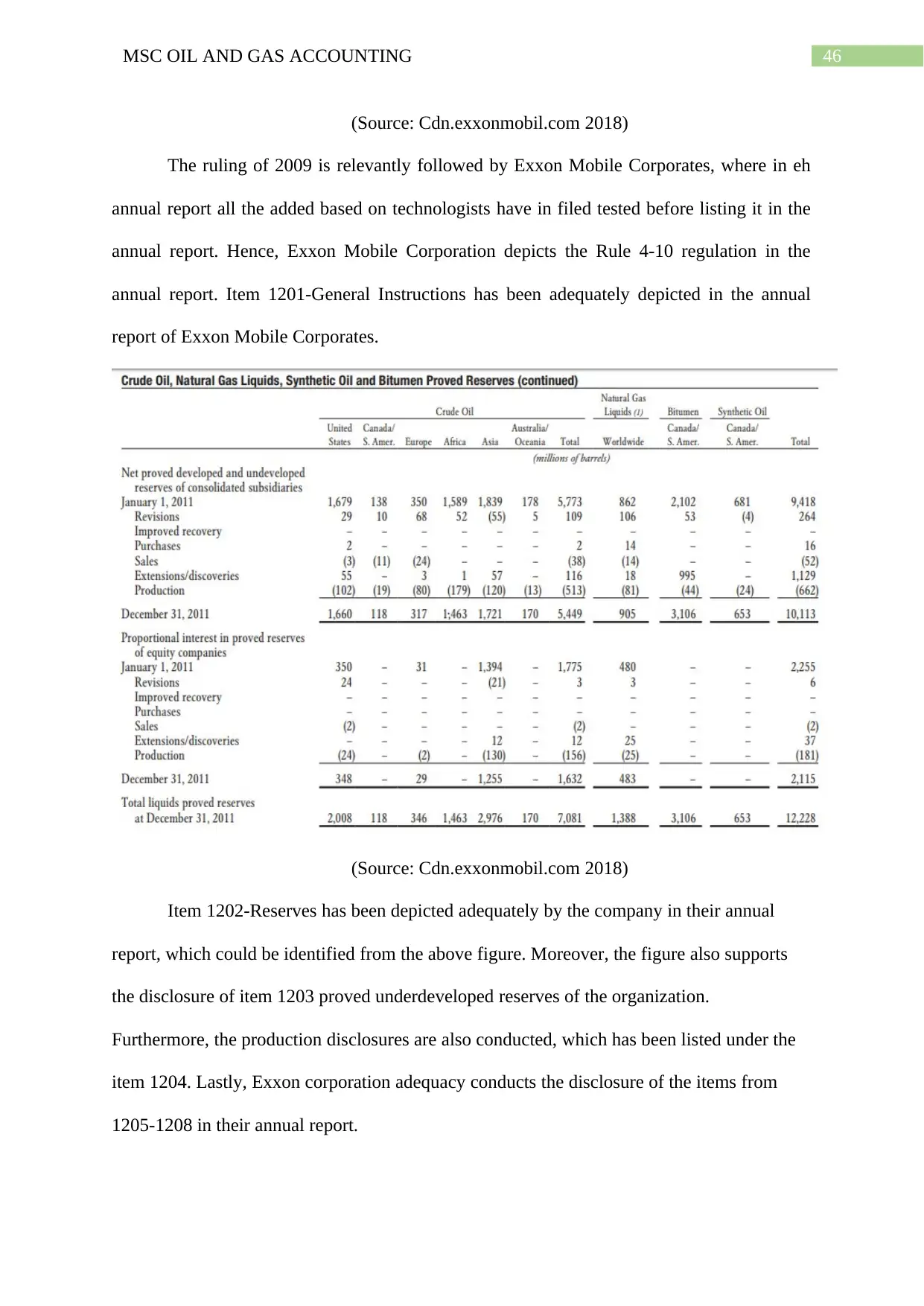

3. Financial statement analysis:............................................................................................45

4. Conclusion:......................................................................................................................48

CHAPTER 5: CONCLUSION AND RECOMMENDATION................................................48

1. Introduction......................................................................................................................48

2. Limitation of the research:...............................................................................................49

3. Findings:...........................................................................................................................50

4. Conclusion:......................................................................................................................52

5. Scopes for future research................................................................................................53

6. Recommendations............................................................................................................54

Reference:................................................................................................................................57

Table of figures

Figure 1: Different types of oil and gas reserves.....................................................................18

Figure 2: Share (In %) of World Gas Reserves (Continent-wise)...........................................20

Figure 3: Share (In %) of World Oil Reserves (Continent-wise).............................................20

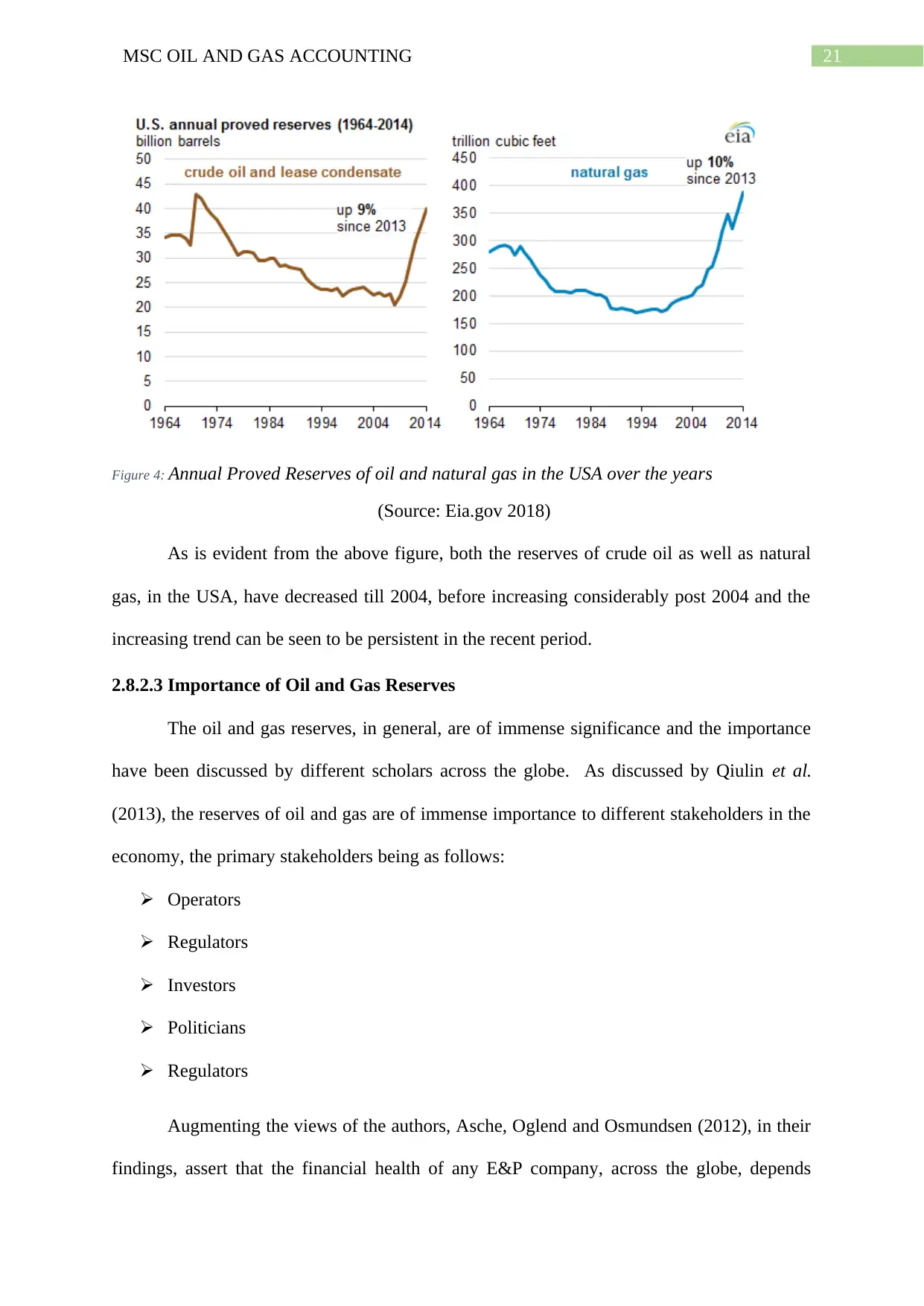

Figure 4: Annual Proved Reserves of oil and natural gas in the USA over the years.............21

Figure 5: Research onion.........................................................................................................32

Figure 6: types of research philosophies..................................................................................34

Figure 7types of research approach..........................................................................................35

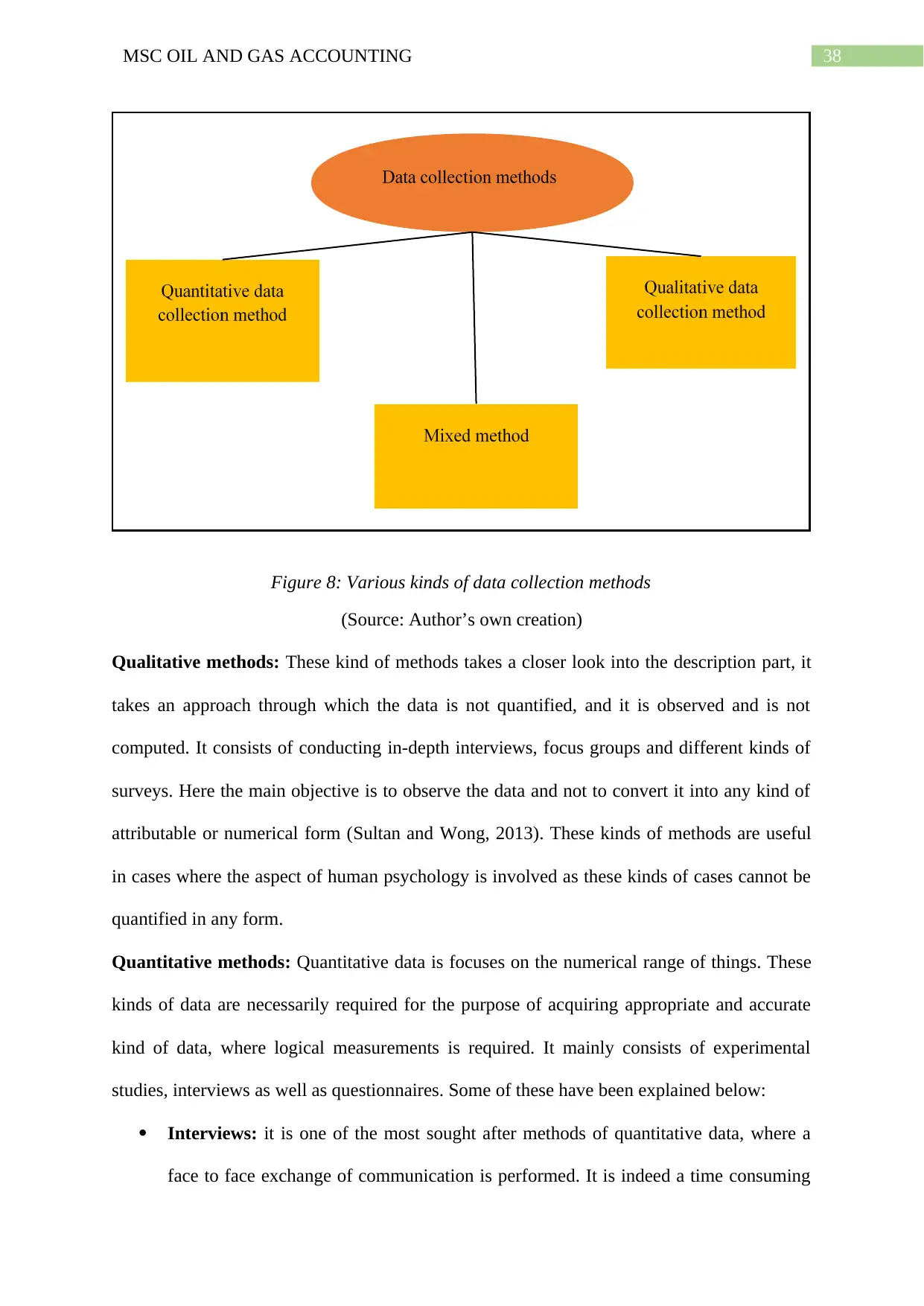

Figure 8: Various kinds of data collection methods.................................................................38

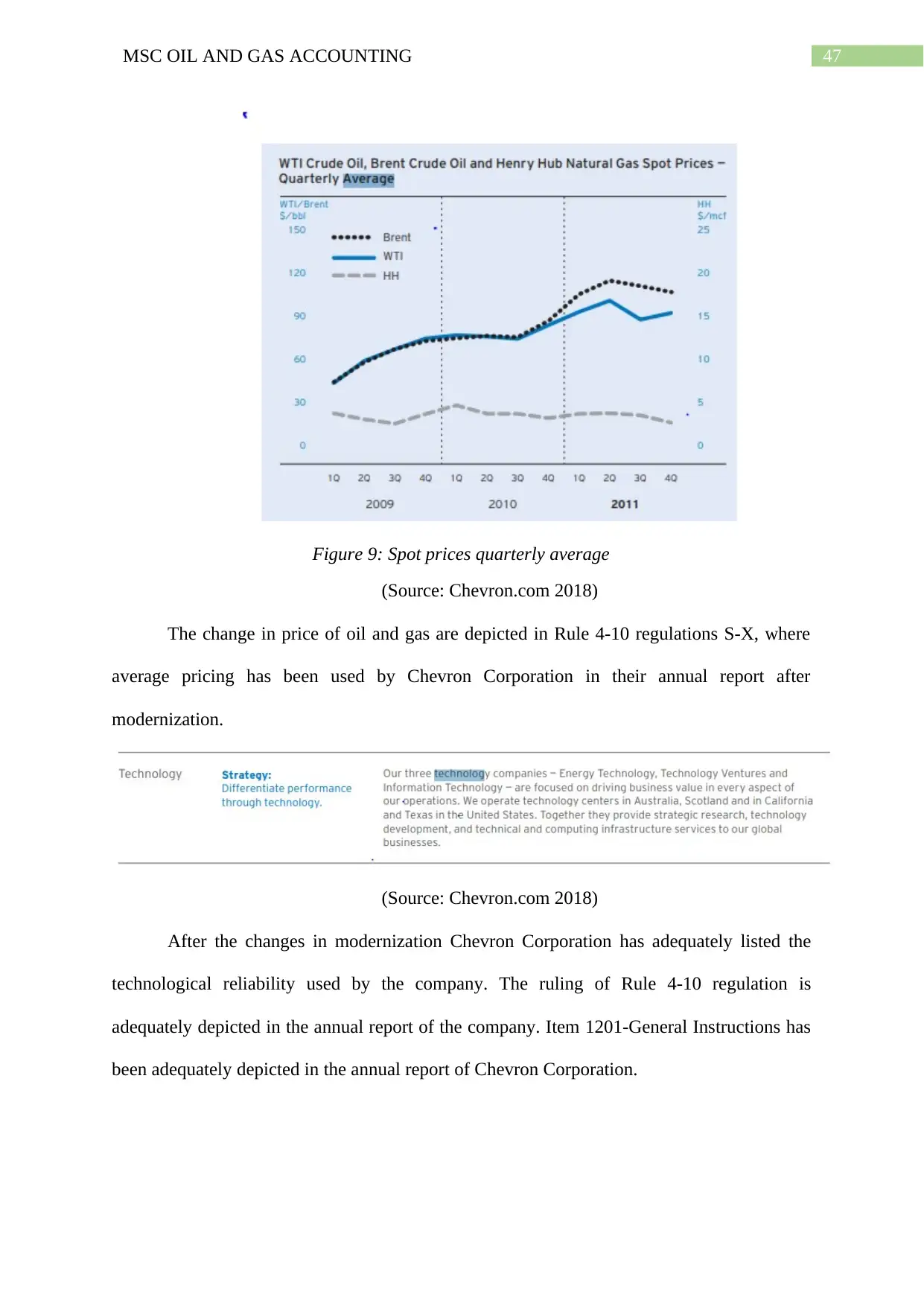

Figure 9: Spot prices quarterly average...................................................................................47

5. Data Collection:...............................................................................................................37

6. Sampling method:............................................................................................................40

7. Conclusion:......................................................................................................................41

CHAPTER 4: DATA ANALYSIS...........................................................................................41

1. Introduction:.....................................................................................................................41

2. Deviations pertaining to the gas definitions in the Rule 4-10 of Regulation S-X............42

3. Financial statement analysis:............................................................................................45

4. Conclusion:......................................................................................................................48

CHAPTER 5: CONCLUSION AND RECOMMENDATION................................................48

1. Introduction......................................................................................................................48

2. Limitation of the research:...............................................................................................49

3. Findings:...........................................................................................................................50

4. Conclusion:......................................................................................................................52

5. Scopes for future research................................................................................................53

6. Recommendations............................................................................................................54

Reference:................................................................................................................................57

Table of figures

Figure 1: Different types of oil and gas reserves.....................................................................18

Figure 2: Share (In %) of World Gas Reserves (Continent-wise)...........................................20

Figure 3: Share (In %) of World Oil Reserves (Continent-wise).............................................20

Figure 4: Annual Proved Reserves of oil and natural gas in the USA over the years.............21

Figure 5: Research onion.........................................................................................................32

Figure 6: types of research philosophies..................................................................................34

Figure 7types of research approach..........................................................................................35

Figure 8: Various kinds of data collection methods.................................................................38

Figure 9: Spot prices quarterly average...................................................................................47

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MSC OIL AND GAS ACCOUNTING

CHAPTER 1: INTRODUCTION:

1.1 Introduction:

During 2009, Securities and Exchange (SEC) a proposed amendment to the disclosure

requirement of the oil and gas companies. It was aimed to encompass the issues that are

previously addressed to source the commission more general revelation of the disclosure

requirement to the firms. New amendment were proposed depending upon the continuing

review of the disclosure that shareholders receive in case they are enquire to make a decision

through voting decision and by the process followed in case those votes are lobbied.

Considering this fact, during 2008 SEC issued the final rule revising the requirement of

disclosure related to the oil and gas reserves. As per the final rule, SEC reflects consideration

of comments received from the stakeholders in response to the proposed rule brought in by

the SEC. as per the official notification of the SECC amendment, it can be seen that,

amendments were aimed to update and modernize the oil and gas disclosure requirements,

specifically in the case of item 102Regulation S-K, Industry Guide 2 and Rule 4-10 of

Regulation S-X in order to align them as per the current industry practices so as to adapt the

changes in technology.

This report is aimed to analyse the financial statement impact through the

modernization of the Oil and Gas Reporting Requirement which was proposed Rule and

effective from the January 1, 2010. In addition to this, the report will analyse and impact of

the same on the previously applicable rule. This section of the report will portray the research

aim, objective and questions and subsequently it will be analysed where it will depict the

target of the researcher. Moving forward, it will portray the structure of the research and

depict the desired finding of the same.

CHAPTER 1: INTRODUCTION:

1.1 Introduction:

During 2009, Securities and Exchange (SEC) a proposed amendment to the disclosure

requirement of the oil and gas companies. It was aimed to encompass the issues that are

previously addressed to source the commission more general revelation of the disclosure

requirement to the firms. New amendment were proposed depending upon the continuing

review of the disclosure that shareholders receive in case they are enquire to make a decision

through voting decision and by the process followed in case those votes are lobbied.

Considering this fact, during 2008 SEC issued the final rule revising the requirement of

disclosure related to the oil and gas reserves. As per the final rule, SEC reflects consideration

of comments received from the stakeholders in response to the proposed rule brought in by

the SEC. as per the official notification of the SECC amendment, it can be seen that,

amendments were aimed to update and modernize the oil and gas disclosure requirements,

specifically in the case of item 102Regulation S-K, Industry Guide 2 and Rule 4-10 of

Regulation S-X in order to align them as per the current industry practices so as to adapt the

changes in technology.

This report is aimed to analyse the financial statement impact through the

modernization of the Oil and Gas Reporting Requirement which was proposed Rule and

effective from the January 1, 2010. In addition to this, the report will analyse and impact of

the same on the previously applicable rule. This section of the report will portray the research

aim, objective and questions and subsequently it will be analysed where it will depict the

target of the researcher. Moving forward, it will portray the structure of the research and

depict the desired finding of the same.

5MSC OIL AND GAS ACCOUNTING

1.2 Background of the study:

Oil and gas reserves are one of the most vital assets for the oil and gas enterprises.

One of the source of confusions for the investors in the oil enterprise is that the quantities of

reserves and its values are of uncertain estimates. The reserves are mainly classified based on

chance of recovery from the underground reservoirs. The SPE (Society of Petroleum

Engineers) first implemented definitions for the proved reserves in the year 1964. The Energy

policy conservation Act was passed in the year 1975, which in turn led to the definitions for

the proved reserves from SEC in 1978. The SEC has various investigative procedure, rules

and enforcement process unlike other enterprises involved with Oil and Gas sector.

According to the recent definition of SEC, the oil and gas reserves are the measured

remaining quantities of oil and gas and its related substances that is presumed to be

producible economically by the implementation of development projects to the known

accumulations (Davis 2012). The changes that have been occurred since the year 1978

includes- significant advancement in recovery and hydrocarbons characterization, growth as

well as improvement of spot markets and transportation for both oil and gas, establishment of

the economic production from the non- traditional resources. The reserves volumes as well

as values of traded oil and gas enterprise are not directly given on the balance sheet of the

company and therefore is attached to financial statements. The petroleum resources of the

companies in underground reservoirs cannot be counted in an asset. Only recoverable

amounts has been monetized to future cash flows and thus is considered as inventory.

Recoverability of the reserves is considered as the function of numerous variables involving

geology, feasible technology and those that are connected with uncertainty. The SPE

categorizes the reserves into various groups based on uncertainty as well as maturity of

recoverable volumes. Even the total volumes that are recoverable are uncertain but measures

future production under specified conditions. These conditions include- the economic

1.2 Background of the study:

Oil and gas reserves are one of the most vital assets for the oil and gas enterprises.

One of the source of confusions for the investors in the oil enterprise is that the quantities of

reserves and its values are of uncertain estimates. The reserves are mainly classified based on

chance of recovery from the underground reservoirs. The SPE (Society of Petroleum

Engineers) first implemented definitions for the proved reserves in the year 1964. The Energy

policy conservation Act was passed in the year 1975, which in turn led to the definitions for

the proved reserves from SEC in 1978. The SEC has various investigative procedure, rules

and enforcement process unlike other enterprises involved with Oil and Gas sector.

According to the recent definition of SEC, the oil and gas reserves are the measured

remaining quantities of oil and gas and its related substances that is presumed to be

producible economically by the implementation of development projects to the known

accumulations (Davis 2012). The changes that have been occurred since the year 1978

includes- significant advancement in recovery and hydrocarbons characterization, growth as

well as improvement of spot markets and transportation for both oil and gas, establishment of

the economic production from the non- traditional resources. The reserves volumes as well

as values of traded oil and gas enterprise are not directly given on the balance sheet of the

company and therefore is attached to financial statements. The petroleum resources of the

companies in underground reservoirs cannot be counted in an asset. Only recoverable

amounts has been monetized to future cash flows and thus is considered as inventory.

Recoverability of the reserves is considered as the function of numerous variables involving

geology, feasible technology and those that are connected with uncertainty. The SPE

categorizes the reserves into various groups based on uncertainty as well as maturity of

recoverable volumes. Even the total volumes that are recoverable are uncertain but measures

future production under specified conditions. These conditions include- the economic

6MSC OIL AND GAS ACCOUNTING

conditions including commodity prices, completion as well as extracting resources,

geological information. Some of the US oil and gas companies such as Exxon and Chevron

have lowered their total reserve amounts owing to low prices. Since the reserve amount

estimation is not always done with proper objectivity, it can be showcase broad aspect of this

field.

The commission has been proposing revision to the reporting requirements of oil and

gas that exists in the present form in Regulation S-K as well as Regulation- S-X under the

Securities Act of 1934 and Securities Act 1933. This revision are mainly intended in

providing investors with comprehensive understanding of the oil and gas reserves that might

help investors in evaluating value of the oil and gas enterprise. In the past three decades

which have passed since implementation of these needs, there have been huge changes in oil

and gas sector. Moreover, these proposed amendments are mainly designed to update as well

as modernize oil and gas disclosure needs for aligning them with present practice as well as

changes in technology (Gipper, Lombardi and Skinner 2013). In addition to this, amendments

also simultaneously align full cost rules of accounting with revised disclosures. These

amendments also revise as well as codify the sector guide in the regulation S-K. Furthermore,

this harmonize the disclosures of oil and gas by the private issuers with disclosures for the

domestic issuers. After the initial implementation of oil and gas disclosure needs in the year

1978 and 1982, huge changes have occurred in this oil and gas sector. These changes include-

advancement in technology and huge changes in different kinds of projects where oil and gas

companies invest the capital. This study mainly reflects on and effect of modernization of oil

and gas reporting requirement on value relevance of financial statement of the US Oil and

Gas enterprises (Leuz and Wysocki 2016).

conditions including commodity prices, completion as well as extracting resources,

geological information. Some of the US oil and gas companies such as Exxon and Chevron

have lowered their total reserve amounts owing to low prices. Since the reserve amount

estimation is not always done with proper objectivity, it can be showcase broad aspect of this

field.

The commission has been proposing revision to the reporting requirements of oil and

gas that exists in the present form in Regulation S-K as well as Regulation- S-X under the

Securities Act of 1934 and Securities Act 1933. This revision are mainly intended in

providing investors with comprehensive understanding of the oil and gas reserves that might

help investors in evaluating value of the oil and gas enterprise. In the past three decades

which have passed since implementation of these needs, there have been huge changes in oil

and gas sector. Moreover, these proposed amendments are mainly designed to update as well

as modernize oil and gas disclosure needs for aligning them with present practice as well as

changes in technology (Gipper, Lombardi and Skinner 2013). In addition to this, amendments

also simultaneously align full cost rules of accounting with revised disclosures. These

amendments also revise as well as codify the sector guide in the regulation S-K. Furthermore,

this harmonize the disclosures of oil and gas by the private issuers with disclosures for the

domestic issuers. After the initial implementation of oil and gas disclosure needs in the year

1978 and 1982, huge changes have occurred in this oil and gas sector. These changes include-

advancement in technology and huge changes in different kinds of projects where oil and gas

companies invest the capital. This study mainly reflects on and effect of modernization of oil

and gas reporting requirement on value relevance of financial statement of the US Oil and

Gas enterprises (Leuz and Wysocki 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MSC OIL AND GAS ACCOUNTING

1.3 Research aim and objective:

1.3.1 Research aim:

This research work has the following aims:

To understand how the fluctuation in the different factors provided in the treatment in

the final rule of SEC can affect the financial statement of the oil and gas companies

and how it can impact the value relevance of the same.

1.3.2 Objective of the study:

The object of the study are as follows:

Examine how the changes and factors, from the prescribed treatment in the final rule,

have affected the financial statements of oil and gas companies and whether this has

led to an improvement in their value relevance

1.3.3 Research question:

To identify impact of the modernization of the Oil and Gas Reporting Requirement on the

value relevance of the financial statement of the US Oil and Gas registrants.

1.4 Justification of the study:

The modernization of the disclosures in the annual report helps in depicting the clear

valuation such as previously only one value was taken for identifying relevant revenues

generated by the company by selling oil (Kim 2013). However, now average valuation has

been taken to depict the actual value of the revenues that is generated during the year and the

research study has been done in order to provide knowledge to the corporate managers and

investors about the issues with the present financial accounting standards during the 2009

(Libby 2017). Some of the problems faced by these enterprises include- tax issues, contract

management, issues regarding technologies and so on. The oil and gas companies having

facing these problems over the years, which in turn affected their financial performance. This

research study will help the sharehlders of these oil and gas companies to address results of

1.3 Research aim and objective:

1.3.1 Research aim:

This research work has the following aims:

To understand how the fluctuation in the different factors provided in the treatment in

the final rule of SEC can affect the financial statement of the oil and gas companies

and how it can impact the value relevance of the same.

1.3.2 Objective of the study:

The object of the study are as follows:

Examine how the changes and factors, from the prescribed treatment in the final rule,

have affected the financial statements of oil and gas companies and whether this has

led to an improvement in their value relevance

1.3.3 Research question:

To identify impact of the modernization of the Oil and Gas Reporting Requirement on the

value relevance of the financial statement of the US Oil and Gas registrants.

1.4 Justification of the study:

The modernization of the disclosures in the annual report helps in depicting the clear

valuation such as previously only one value was taken for identifying relevant revenues

generated by the company by selling oil (Kim 2013). However, now average valuation has

been taken to depict the actual value of the revenues that is generated during the year and the

research study has been done in order to provide knowledge to the corporate managers and

investors about the issues with the present financial accounting standards during the 2009

(Libby 2017). Some of the problems faced by these enterprises include- tax issues, contract

management, issues regarding technologies and so on. The oil and gas companies having

facing these problems over the years, which in turn affected their financial performance. This

research study will help the sharehlders of these oil and gas companies to address results of

8MSC OIL AND GAS ACCOUNTING

pre-tax differences between the IFRS and GAAP (Macve 2015). Moreover, it will help to

revaluate existing tax accounting methods. In addition to this, this study will also help the

shareholders to combat issues regarding existing contracts. Furthermore, the managers of

these oil and gas enterprise will also able to identify their technology issues and take action

accordingly (Alazzani and Wan-Hussin 2013).

1.5 Structure of the research:

In order to effectively undertake this research project, the whole thesis has been

divided into five chapters. The first chapter of the research study focuses on the background

of the research topic, research aims and objectives, justification of the research study and

structure of the research. The second chapter highlights on the review of literature relating to

the research topic that aligns with impact of the modernization of the Oil and Gas Reporting

Requirement on the value relevance of the financial statement of the US Oil and Gas

registrants. The next section of the research study will portray on the methods that had been

used while conducting the research study. The methods include- research philosophy,

research approach, research design, data collection method, data analysis, sampling design,

sampling technique and ethical considerations. The next section of this research study focuses

on the data analysis in which the data that are collected while conducting this research are

analysed by using few tools. The last section of this study focuses on the conclusion that is

drawn after conducting the reseach study. Furthermore, in this chapter the recommendations

are also provided to the managers and investors of these companies relating to the above-

mentioned problems.

1.6 Chapter summary:

From the above discussion it can be found that the research is aimed to identify

impact of the modernization of the Oil and Gas Reporting Requirement on the value

relevance of the financial statement of the US Oil and Gas registrants. For this purpose, in

pre-tax differences between the IFRS and GAAP (Macve 2015). Moreover, it will help to

revaluate existing tax accounting methods. In addition to this, this study will also help the

shareholders to combat issues regarding existing contracts. Furthermore, the managers of

these oil and gas enterprise will also able to identify their technology issues and take action

accordingly (Alazzani and Wan-Hussin 2013).

1.5 Structure of the research:

In order to effectively undertake this research project, the whole thesis has been

divided into five chapters. The first chapter of the research study focuses on the background

of the research topic, research aims and objectives, justification of the research study and

structure of the research. The second chapter highlights on the review of literature relating to

the research topic that aligns with impact of the modernization of the Oil and Gas Reporting

Requirement on the value relevance of the financial statement of the US Oil and Gas

registrants. The next section of the research study will portray on the methods that had been

used while conducting the research study. The methods include- research philosophy,

research approach, research design, data collection method, data analysis, sampling design,

sampling technique and ethical considerations. The next section of this research study focuses

on the data analysis in which the data that are collected while conducting this research are

analysed by using few tools. The last section of this study focuses on the conclusion that is

drawn after conducting the reseach study. Furthermore, in this chapter the recommendations

are also provided to the managers and investors of these companies relating to the above-

mentioned problems.

1.6 Chapter summary:

From the above discussion it can be found that the research is aimed to identify

impact of the modernization of the Oil and Gas Reporting Requirement on the value

relevance of the financial statement of the US Oil and Gas registrants. For this purpose, in

9MSC OIL AND GAS ACCOUNTING

this section it has portrayed the research aim, objective and the questions that the researcher

wanted to research and it has provided a brief overview of the process utilising which the

project work will proceed further.

CHAPTER 2: LITERATURE REVIEW:

2.1 Introduction

The oil and gas industry being one of the crucial industries in the contemporary

framework, as discussed in the above section and the same having huge implications on other

industries across the globe, it becomes considerably important to have a robust accounting

and reporting model for the purpose of accounting the exploration as well as production

activities in the oil and gas market, in order to ensure transparency, efficiency and facilitation

of investment and economic decisions in the concerned field (Libby 2017).

There have been considerable debates, in this context, over the years, regarding the

appropriate accounting model in the aspects of the accounting regulation which

comprehensively captures the different transactions which take place in the oil and gas

industry across the globe, due to the existence of faults and limitations in the traditional

accounting practices used in this domain in the earlier times (Olah, Goeppert and Prakash

2011). There exist huge literary and empirical evidences regarding the different accounting

models and their evolution, benefits and limitations in the aspect of oil and gas accounting, in

the global framework, with the same getting developed and more inclusive with time.

Keeping this into consideration, the concerned section of the thesis tries to conduct an

extensive review of the literatures and scholarly evidences, present in the global scenario

regarding these aspects, with emphasis on the oil and gas reserves in the contemporary

period, especially in the domain of the United States of America.

this section it has portrayed the research aim, objective and the questions that the researcher

wanted to research and it has provided a brief overview of the process utilising which the

project work will proceed further.

CHAPTER 2: LITERATURE REVIEW:

2.1 Introduction

The oil and gas industry being one of the crucial industries in the contemporary

framework, as discussed in the above section and the same having huge implications on other

industries across the globe, it becomes considerably important to have a robust accounting

and reporting model for the purpose of accounting the exploration as well as production

activities in the oil and gas market, in order to ensure transparency, efficiency and facilitation

of investment and economic decisions in the concerned field (Libby 2017).

There have been considerable debates, in this context, over the years, regarding the

appropriate accounting model in the aspects of the accounting regulation which

comprehensively captures the different transactions which take place in the oil and gas

industry across the globe, due to the existence of faults and limitations in the traditional

accounting practices used in this domain in the earlier times (Olah, Goeppert and Prakash

2011). There exist huge literary and empirical evidences regarding the different accounting

models and their evolution, benefits and limitations in the aspect of oil and gas accounting, in

the global framework, with the same getting developed and more inclusive with time.

Keeping this into consideration, the concerned section of the thesis tries to conduct an

extensive review of the literatures and scholarly evidences, present in the global scenario

regarding these aspects, with emphasis on the oil and gas reserves in the contemporary

period, especially in the domain of the United States of America.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MSC OIL AND GAS ACCOUNTING

2.2 A brief Overview:

Reserves disclosures are going to undergo a vast amount of change because of the

introduction of the Securities and Exchange Commission of the Oil and Gas Requirements.

There are a variety of changes, which were initially expected, as this change was announced.

Some of the doubts were raised about the implications of this change in the form of

calculation under new requirements, impact on the volumes, whether there will be a decrease

or increase, or if the adoption of the change would be sudden, resulting in a fast pace shifting

or would it be slow and gradual process. All these various kinds of issues were important

from the perspective this change would be bringing.

2.3 The implications of the modernization:

The Securities and Exchange Commission had adopted a range of revisions to its oil and gas

reporting disclosure procedures, which were previously disseminated in Regulations S-K,

Regulation S-X and as well as Industry Guide 2. The recent amendments have been followed

in the Rule 4-to of Regulation S-X. The recent amendments have also updated the

Commission’s disclosure needs for the oil and gas manufacturing companies and classify

them into a new sub head 1200 to Regulation S-K. It would be necessary on the part of the oil

and gas companies of presenting disclosures to the new rules in registration statements and

annual reports which have been ending on after 31st December, 2009.

One of the most important and primary reasons for this amendment is to provide the investors

with a more expressive and inclusive understanding of the oil and gas reserves. This would

assist the investors in estimating the rightful value of these oil and gas reserves. This

amendment has been designed in order to modernise and update the oil and gas disclosures

needs for aligning them with the existent practices and changes in technology.

As the implications of these kind of new rules are so enormous, it was a sigh of relief for the

oil and gas companies, when it was announced that the companies will be required to report

2.2 A brief Overview:

Reserves disclosures are going to undergo a vast amount of change because of the

introduction of the Securities and Exchange Commission of the Oil and Gas Requirements.

There are a variety of changes, which were initially expected, as this change was announced.

Some of the doubts were raised about the implications of this change in the form of

calculation under new requirements, impact on the volumes, whether there will be a decrease

or increase, or if the adoption of the change would be sudden, resulting in a fast pace shifting

or would it be slow and gradual process. All these various kinds of issues were important

from the perspective this change would be bringing.

2.3 The implications of the modernization:

The Securities and Exchange Commission had adopted a range of revisions to its oil and gas

reporting disclosure procedures, which were previously disseminated in Regulations S-K,

Regulation S-X and as well as Industry Guide 2. The recent amendments have been followed

in the Rule 4-to of Regulation S-X. The recent amendments have also updated the

Commission’s disclosure needs for the oil and gas manufacturing companies and classify

them into a new sub head 1200 to Regulation S-K. It would be necessary on the part of the oil

and gas companies of presenting disclosures to the new rules in registration statements and

annual reports which have been ending on after 31st December, 2009.

One of the most important and primary reasons for this amendment is to provide the investors

with a more expressive and inclusive understanding of the oil and gas reserves. This would

assist the investors in estimating the rightful value of these oil and gas reserves. This

amendment has been designed in order to modernise and update the oil and gas disclosures

needs for aligning them with the existent practices and changes in technology.

As the implications of these kind of new rules are so enormous, it was a sigh of relief for the

oil and gas companies, when it was announced that the companies will be required to report

11MSC OIL AND GAS ACCOUNTING

all the information about their oil and gas operations, including their oil and gas revenues, as

per the old rules and regulations, until the new ones are put into force (Qp.gov.sk.ca, 2018).

This will ensure comparability among the different kinds of disclosers, among the different

companies.

2.4 Some new rules under the amendment:

Changes of oil and gas related definitions: Under the new rules, some of the terms

and definitions of the oil and gas related items have been revised in accordance new

amendment specifically in the Rule 4 to 10 of the Regulation S to X, in the prescribed

manner, given below:

Average price: One of the major implication of the new amendment is the is the

usage of the 12 month average price instead of the current standard of a single day

price for the purpose of calculating reserves, which will ensure comparability of the

reserves.

Dependable Technologies: the new amendment has made some significant changes

in the use of technologies in the arena of oil and gas, where as per the new

amendment it is required to make use of dependable, reliable and consistent

technologies, instead of the erstwhile field tests, which used to take place earlier.

Modern resources: in accordance with the new rule, it is necessary for the companies

that all the non-traditional resources such as bitumen, shale and oil sands must be

included in the oil and gas reserves because of the fact that all the products of these

resources are produced from the using traditional resources only.

Supporting definitions: The rules under the new amendment have added a lot of new

provisions, with regards to the addition of new kind of definitions to the various

supporting terms of the oil and gas industry. It includes new definitions of probable,

proved and possible reserves, along with a new definition of ‘reserves’.

all the information about their oil and gas operations, including their oil and gas revenues, as

per the old rules and regulations, until the new ones are put into force (Qp.gov.sk.ca, 2018).

This will ensure comparability among the different kinds of disclosers, among the different

companies.

2.4 Some new rules under the amendment:

Changes of oil and gas related definitions: Under the new rules, some of the terms

and definitions of the oil and gas related items have been revised in accordance new

amendment specifically in the Rule 4 to 10 of the Regulation S to X, in the prescribed

manner, given below:

Average price: One of the major implication of the new amendment is the is the

usage of the 12 month average price instead of the current standard of a single day

price for the purpose of calculating reserves, which will ensure comparability of the

reserves.

Dependable Technologies: the new amendment has made some significant changes

in the use of technologies in the arena of oil and gas, where as per the new

amendment it is required to make use of dependable, reliable and consistent

technologies, instead of the erstwhile field tests, which used to take place earlier.

Modern resources: in accordance with the new rule, it is necessary for the companies

that all the non-traditional resources such as bitumen, shale and oil sands must be

included in the oil and gas reserves because of the fact that all the products of these

resources are produced from the using traditional resources only.

Supporting definitions: The rules under the new amendment have added a lot of new

provisions, with regards to the addition of new kind of definitions to the various

supporting terms of the oil and gas industry. It includes new definitions of probable,

proved and possible reserves, along with a new definition of ‘reserves’.

12MSC OIL AND GAS ACCOUNTING

Compounding of Disclosure requirements: The new amendment has brought a

series of changes in the industry specific disclosure needs and requirements. It has

been included in a new sub head known as Subpart 1200 in Regulation S to K. This

was previously seen in item number 102 of Regulation S to K (Kaiser and Yu 2012).

The new sub head includes the following items:

Item number 1202: This includes Non-traditional resources as part of oil and gas

reserves, those kinds of technologies which are used to establish new or additional

reserves of oil and gas, different kinds of third party reports. In addition to this, the

new amendment does not require disclosures of the probable and potential reserves of

the company and as well as sensitivity of the prices of the reserves, which allows the

oil companies to show different approximations based on the future activities and

prices or the calculated prices of the company’s management.

Various other important issues: There are a host of other issues which are taken

care of by the new amendment, some of which have been given below:

Management Discussions and Analysis: the new amendment also takes into account

and includes all the guidance and necessary points regarding the different types of

issues, oil and Gas Company could face while preparing its management discussions

and analysis. It includes disclosures regarding technology, prices and allowance

conditions.

Limitation of ceiling test for capitalised nature goods: The new alterations in the

rules also have an impact on the ceiling tests for the capitalised nature of goods.

Under the new amendment, the commission’s full cost method has been replaced by a

12 month average pricing method (Etherington, 2009). This was particularly done for

the disclosures of reserves quantity and for other accounting purposes.

Compounding of Disclosure requirements: The new amendment has brought a

series of changes in the industry specific disclosure needs and requirements. It has

been included in a new sub head known as Subpart 1200 in Regulation S to K. This

was previously seen in item number 102 of Regulation S to K (Kaiser and Yu 2012).

The new sub head includes the following items:

Item number 1202: This includes Non-traditional resources as part of oil and gas

reserves, those kinds of technologies which are used to establish new or additional

reserves of oil and gas, different kinds of third party reports. In addition to this, the

new amendment does not require disclosures of the probable and potential reserves of

the company and as well as sensitivity of the prices of the reserves, which allows the

oil companies to show different approximations based on the future activities and

prices or the calculated prices of the company’s management.

Various other important issues: There are a host of other issues which are taken

care of by the new amendment, some of which have been given below:

Management Discussions and Analysis: the new amendment also takes into account

and includes all the guidance and necessary points regarding the different types of

issues, oil and Gas Company could face while preparing its management discussions

and analysis. It includes disclosures regarding technology, prices and allowance

conditions.

Limitation of ceiling test for capitalised nature goods: The new alterations in the

rules also have an impact on the ceiling tests for the capitalised nature of goods.

Under the new amendment, the commission’s full cost method has been replaced by a

12 month average pricing method (Etherington, 2009). This was particularly done for

the disclosures of reserves quantity and for other accounting purposes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MSC OIL AND GAS ACCOUNTING

Accounting treatment and absence of retroactive revisions: As per the new

amendment, there are accounting guidelines for stating any kind of changes in the

accounting figures which results from the amendments, which is considered as

indivisible from any kind of change in the accounting principle, which does not

necessarily require any kind of retroactive revision.

2.5 Addition of new products:

As per the new amendments there have been an addition of new varieties of products

compared to that of the previous products of oil and gas. There have been significant amount

of additions, under this arena and they have been classified under the head of the non-

traditional resources. These non-traditional resources include bitumen, oil and gas shale’s,

coal and gas hydrates (Grubert, 2012). The range of products also include non-renewable

natural resources which are to be upgraded into synthetic oil and gas. This has helped in

further classification of the products produced by the oil and gas companies. This

classification of the new variety of products would help in efficient reporting of the

happenings of the working of these kinds of oil and gas companies.

2.6 Communication with the SEC:

The new rules and guidelines regarding the various kinds of changes brought about by

the new provisions would require companies to know all the ins and outs of each of them. In

order to ensure smooth transition from the old laws to the new ones and their requirements,

the SEC and his or her office is always available, in order to quell any kind of doubts about

any of the provisions (Devold, 2013). In this regard, the SEC’s division office of corporation

of finance and the office of its Chief Accountant are always available to all the small,

medium and other companies for quelling their doubts about the different requirements

presented under the latest amendment.

Accounting treatment and absence of retroactive revisions: As per the new

amendment, there are accounting guidelines for stating any kind of changes in the

accounting figures which results from the amendments, which is considered as

indivisible from any kind of change in the accounting principle, which does not

necessarily require any kind of retroactive revision.

2.5 Addition of new products:

As per the new amendments there have been an addition of new varieties of products

compared to that of the previous products of oil and gas. There have been significant amount

of additions, under this arena and they have been classified under the head of the non-

traditional resources. These non-traditional resources include bitumen, oil and gas shale’s,

coal and gas hydrates (Grubert, 2012). The range of products also include non-renewable

natural resources which are to be upgraded into synthetic oil and gas. This has helped in

further classification of the products produced by the oil and gas companies. This

classification of the new variety of products would help in efficient reporting of the

happenings of the working of these kinds of oil and gas companies.

2.6 Communication with the SEC:

The new rules and guidelines regarding the various kinds of changes brought about by

the new provisions would require companies to know all the ins and outs of each of them. In

order to ensure smooth transition from the old laws to the new ones and their requirements,

the SEC and his or her office is always available, in order to quell any kind of doubts about

any of the provisions (Devold, 2013). In this regard, the SEC’s division office of corporation

of finance and the office of its Chief Accountant are always available to all the small,

medium and other companies for quelling their doubts about the different requirements

presented under the latest amendment.

14MSC OIL AND GAS ACCOUNTING

2.7 Impact on accounting literature:

The impact of the modernization of the oil and gas requirements upon the accounting

literature is as follows:

Prices used for accounting purposes: In the proposed rule, in the regulation S to X, the SEC

had planned for retaining the usage of a single-day, year-end price for different kinds of

accounting needs and requirements. This application, would have easily needed companies to

efficiently calculate reserves a total of two times, by using two diverse pricing assumptions

one for the purpose of disclosures and one for the different accounting purposes was

consistently opposed by critiques (Kaiser, 2013). Critiques have recommended that the

Commission synchronize equivalent rule changes both with the FASB and IASB for the

purpose of ensuring uniformity of the rules of the new amendment. Some critiques have

commented that the IASB is presently considering creation of a group of strategies for oil and

gas extraction activities, together with an explanation and definition of oil and gas reserves,

and has also suggested that the Commission line up its rules along those guidelines.

2.8 Consistency with the rules of FASB and the IASB:

The Staffs of the Securities and Exchange Commission is in the process of communicating

with the different staffs of the FASB in order to bring into line the standards used in FASB

proclamations with the Final Rule of the new amendment (Kan and Tomson, 2012). The SEC

will eventually introspect the matter of considering whether to delay the conformity date of

the Final Rule amendments on the basis of the progress of its negotiations with the two

premier financial regulation bodies, the FASB and IASB.

2.8.1 Contradictory capitalisation approach between mining and oil and gas related

activities:

In accordance with the present U.S. accounting guidelines, costs associated with proven

along with probable mining reserves may be capitalized for the purpose of conducting

2.7 Impact on accounting literature:

The impact of the modernization of the oil and gas requirements upon the accounting

literature is as follows:

Prices used for accounting purposes: In the proposed rule, in the regulation S to X, the SEC

had planned for retaining the usage of a single-day, year-end price for different kinds of

accounting needs and requirements. This application, would have easily needed companies to

efficiently calculate reserves a total of two times, by using two diverse pricing assumptions

one for the purpose of disclosures and one for the different accounting purposes was

consistently opposed by critiques (Kaiser, 2013). Critiques have recommended that the

Commission synchronize equivalent rule changes both with the FASB and IASB for the

purpose of ensuring uniformity of the rules of the new amendment. Some critiques have

commented that the IASB is presently considering creation of a group of strategies for oil and

gas extraction activities, together with an explanation and definition of oil and gas reserves,

and has also suggested that the Commission line up its rules along those guidelines.

2.8 Consistency with the rules of FASB and the IASB:

The Staffs of the Securities and Exchange Commission is in the process of communicating

with the different staffs of the FASB in order to bring into line the standards used in FASB

proclamations with the Final Rule of the new amendment (Kan and Tomson, 2012). The SEC

will eventually introspect the matter of considering whether to delay the conformity date of

the Final Rule amendments on the basis of the progress of its negotiations with the two

premier financial regulation bodies, the FASB and IASB.

2.8.1 Contradictory capitalisation approach between mining and oil and gas related

activities:

In accordance with the present U.S. accounting guidelines, costs associated with proven

along with probable mining reserves may be capitalized for the purpose of conducting

15MSC OIL AND GAS ACCOUNTING

operations which includes extracting products through different kinds of mining methods,

like bitumen. As per the Final Rule, extraction of bitumen and all those activities which are

used for the purpose of producing oil and gas through the various mining procedures would

be incorporated under oil and gas accounting set of laws, which only authorize capitalization

of costs related with proved reserves (Weijermars, 2012). In addition to all this, the

guidelines related to mining activities have failed to provide any particular percentages for

creation of levels of certainty for proven or probable reserves for mining activities.

1.8 In-depth implication of modernization:

The new guidelines are considered more flexible , when compared to the previous

standards, for instance, operators can now book PUD locations which are larger than a single

well spacing from producing well. In addition to this, the new technologies make room for

the use of consistent and reliable technologies. The new rules and regulations are more of a

principle based nature, than the ones, which were previously used by the commission (Gong,

2013). While more regulation could lead to more demanding standards and regulations, but

this has not been the case with modernisation. However, there have been some flaws in the

new rules and regulations too, which have been overlooked by the Securities and Exchange

Commission. Some of these limitations are ignorance of rules, weak internal controls and

biased behaviour towards humans. There can be issues cropping up regarding the flouting of

rules by the companies, by taking undue advantage of the new flexible norms and the reliable

technologies. There might be cases, where people inadvertently make use of the technologies,

without having any kind of knowledge about the same, which might not be good for the

ensuring an effective performance.

1.9 Major changes at a glance:

There have been a range of changes in the new modernization of the oil and gas

company’s requirements. This includes definition of the current prices, non-traditional

operations which includes extracting products through different kinds of mining methods,

like bitumen. As per the Final Rule, extraction of bitumen and all those activities which are

used for the purpose of producing oil and gas through the various mining procedures would

be incorporated under oil and gas accounting set of laws, which only authorize capitalization

of costs related with proved reserves (Weijermars, 2012). In addition to all this, the

guidelines related to mining activities have failed to provide any particular percentages for

creation of levels of certainty for proven or probable reserves for mining activities.

1.8 In-depth implication of modernization:

The new guidelines are considered more flexible , when compared to the previous

standards, for instance, operators can now book PUD locations which are larger than a single

well spacing from producing well. In addition to this, the new technologies make room for

the use of consistent and reliable technologies. The new rules and regulations are more of a

principle based nature, than the ones, which were previously used by the commission (Gong,

2013). While more regulation could lead to more demanding standards and regulations, but

this has not been the case with modernisation. However, there have been some flaws in the

new rules and regulations too, which have been overlooked by the Securities and Exchange

Commission. Some of these limitations are ignorance of rules, weak internal controls and

biased behaviour towards humans. There can be issues cropping up regarding the flouting of

rules by the companies, by taking undue advantage of the new flexible norms and the reliable

technologies. There might be cases, where people inadvertently make use of the technologies,

without having any kind of knowledge about the same, which might not be good for the

ensuring an effective performance.

1.9 Major changes at a glance:

There have been a range of changes in the new modernization of the oil and gas

company’s requirements. This includes definition of the current prices, non-traditional

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MSC OIL AND GAS ACCOUNTING

resources extraction has been considered and as well as included in the category of oil and

gas activities. There have been an increased use of the modern technology, with the new

requirements making use of the new technologies which are more reliable by nature. In

addition to all this, there has been an additional option of disclosing the probable and possible

reserves which have been allowed.

2.8.2 Oil and Gas Reserves: Meaning and Importance

There exist different assertions and perceptions regarding the term “oil and gas

reserves” and various scholars have tried to define the same from varied perspectives. In this

context, one of the most comprehensive definitions can be seen to be provided in the work of

Owen, Inderwildi and King (2010). Referring to the SEC definition, the authors highlight oil

and gas reserves to be the estimated quantities of oil, gas as well as related products to be

remaining, which are anticipated to be producible economically, at a particular point of time,

by applying development projects to the accumulations which are known (Sec.gov 2018).

This definition is augmented by Lee and Sidle (2010), according to whom, for any oil or gas

deposit to be considered as a reserve, some extent of commercial and technical certainty

regarding the extraction of such deposits has to be established, with the help of the existing

technologies in this domain.

2.8.2.1 Types of Oil and Gas Reserves

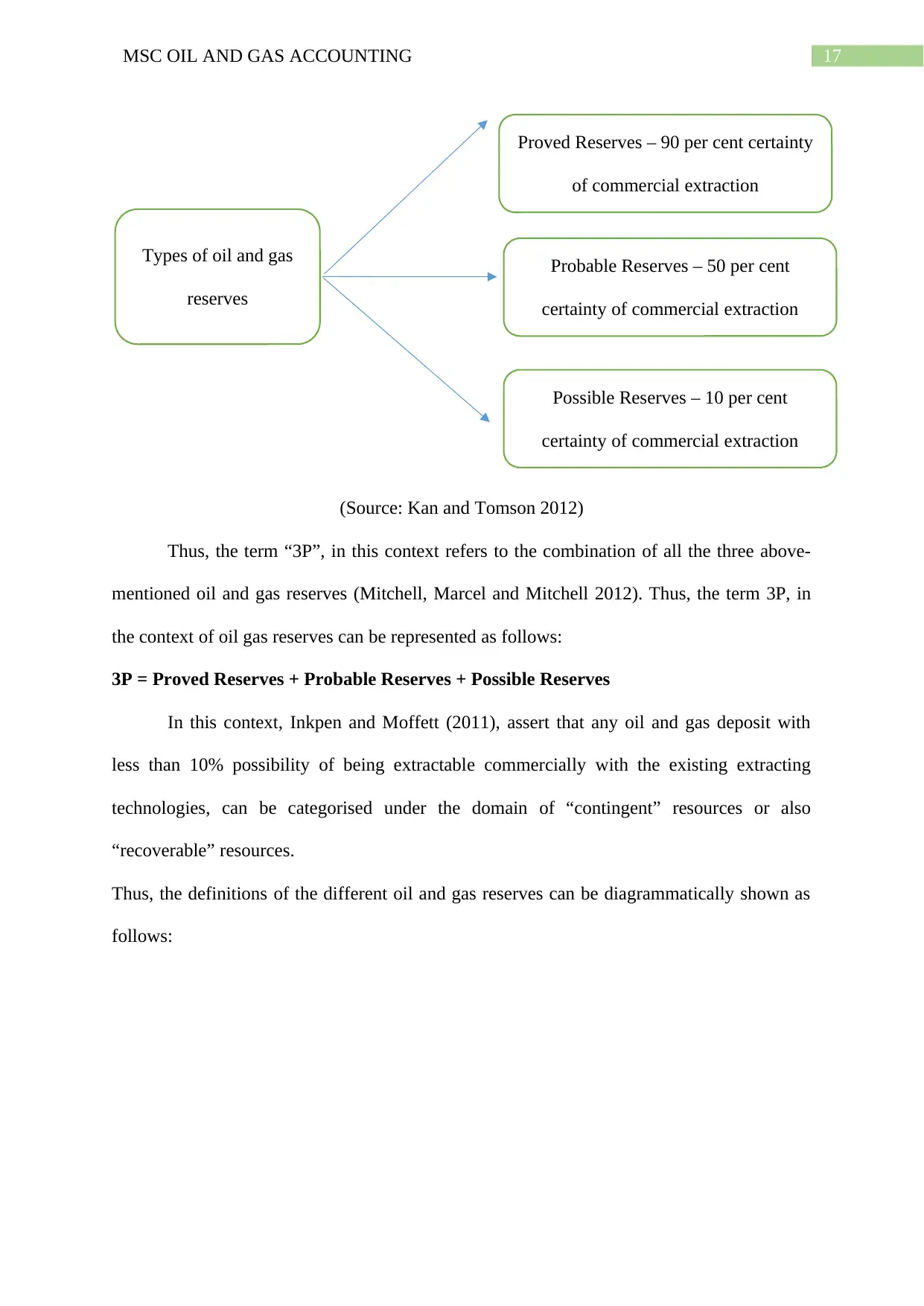

In this context, as Rui et al. (2017), highlights in their paper, the oil and gas reserves,

in the global framework, are usually classified into three broad categories, based on the

probable levels or certainty of their commercial extraction, the categories being as follows:

resources extraction has been considered and as well as included in the category of oil and

gas activities. There have been an increased use of the modern technology, with the new

requirements making use of the new technologies which are more reliable by nature. In

addition to all this, there has been an additional option of disclosing the probable and possible

reserves which have been allowed.

2.8.2 Oil and Gas Reserves: Meaning and Importance

There exist different assertions and perceptions regarding the term “oil and gas

reserves” and various scholars have tried to define the same from varied perspectives. In this

context, one of the most comprehensive definitions can be seen to be provided in the work of

Owen, Inderwildi and King (2010). Referring to the SEC definition, the authors highlight oil

and gas reserves to be the estimated quantities of oil, gas as well as related products to be

remaining, which are anticipated to be producible economically, at a particular point of time,

by applying development projects to the accumulations which are known (Sec.gov 2018).

This definition is augmented by Lee and Sidle (2010), according to whom, for any oil or gas

deposit to be considered as a reserve, some extent of commercial and technical certainty

regarding the extraction of such deposits has to be established, with the help of the existing

technologies in this domain.

2.8.2.1 Types of Oil and Gas Reserves

In this context, as Rui et al. (2017), highlights in their paper, the oil and gas reserves,

in the global framework, are usually classified into three broad categories, based on the

probable levels or certainty of their commercial extraction, the categories being as follows:

17MSC OIL AND GAS ACCOUNTING

(Source: Kan and Tomson 2012)

Thus, the term “3P”, in this context refers to the combination of all the three above-

mentioned oil and gas reserves (Mitchell, Marcel and Mitchell 2012). Thus, the term 3P, in

the context of oil gas reserves can be represented as follows:

3P = Proved Reserves + Probable Reserves + Possible Reserves

In this context, Inkpen and Moffett (2011), assert that any oil and gas deposit with

less than 10% possibility of being extractable commercially with the existing extracting

technologies, can be categorised under the domain of “contingent” resources or also

“recoverable” resources.

Thus, the definitions of the different oil and gas reserves can be diagrammatically shown as

follows:

Types of oil and gas

reserves

Proved Reserves – 90 per cent certainty

of commercial extraction

Probable Reserves – 50 per cent

certainty of commercial extraction

Possible Reserves – 10 per cent

certainty of commercial extraction

(Source: Kan and Tomson 2012)

Thus, the term “3P”, in this context refers to the combination of all the three above-

mentioned oil and gas reserves (Mitchell, Marcel and Mitchell 2012). Thus, the term 3P, in

the context of oil gas reserves can be represented as follows:

3P = Proved Reserves + Probable Reserves + Possible Reserves

In this context, Inkpen and Moffett (2011), assert that any oil and gas deposit with

less than 10% possibility of being extractable commercially with the existing extracting

technologies, can be categorised under the domain of “contingent” resources or also

“recoverable” resources.

Thus, the definitions of the different oil and gas reserves can be diagrammatically shown as

follows:

Types of oil and gas

reserves

Proved Reserves – 90 per cent certainty

of commercial extraction

Probable Reserves – 50 per cent

certainty of commercial extraction

Possible Reserves – 10 per cent

certainty of commercial extraction

18MSC OIL AND GAS ACCOUNTING

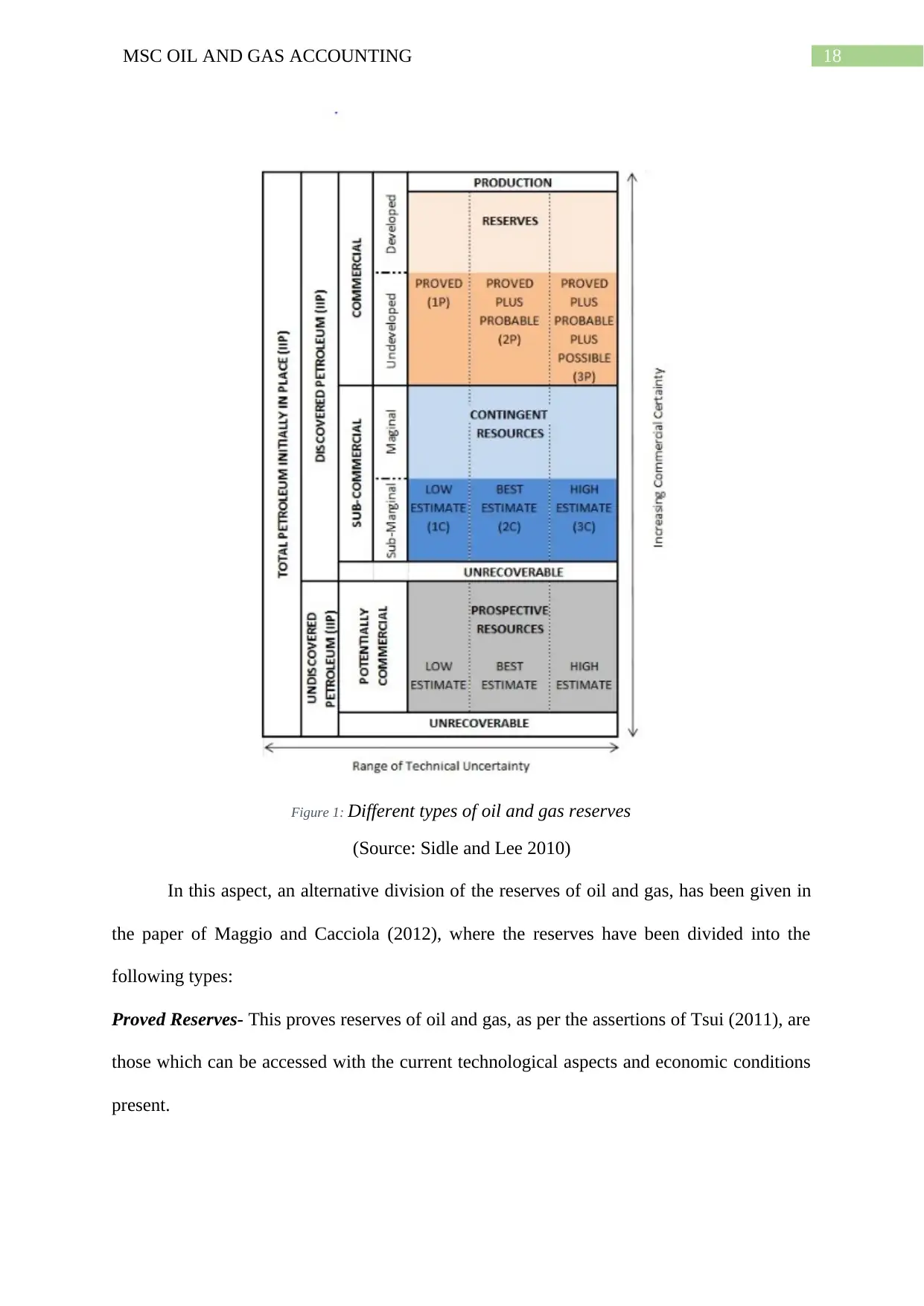

Figure 1: Different types of oil and gas reserves

(Source: Sidle and Lee 2010)

In this aspect, an alternative division of the reserves of oil and gas, has been given in

the paper of Maggio and Cacciola (2012), where the reserves have been divided into the

following types:

Proved Reserves- This proves reserves of oil and gas, as per the assertions of Tsui (2011), are

those which can be accessed with the current technological aspects and economic conditions

present.

Figure 1: Different types of oil and gas reserves

(Source: Sidle and Lee 2010)

In this aspect, an alternative division of the reserves of oil and gas, has been given in

the paper of Maggio and Cacciola (2012), where the reserves have been divided into the

following types:

Proved Reserves- This proves reserves of oil and gas, as per the assertions of Tsui (2011), are

those which can be accessed with the current technological aspects and economic conditions

present.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MSC OIL AND GAS ACCOUNTING

Total Technically Recoverable Resources (TTR)- These are the total amount of oil and gas

reserves which can be extracted with the help of the technologies which exist in the current

framework, irrespective of the presence or absence of financial sense in doing so (Othman

and Jafari 2012).

Unproved Reserves- The authors define this as follows:

Unproved Reserves = TTR – Proved Reserves

These are those reserves which can be extracted, but with more improved technology