Accounting Fundamentals: Break-Even Point and Management Accounting

VerifiedAdded on 2023/06/18

|7

|1426

|336

Homework Assignment

AI Summary

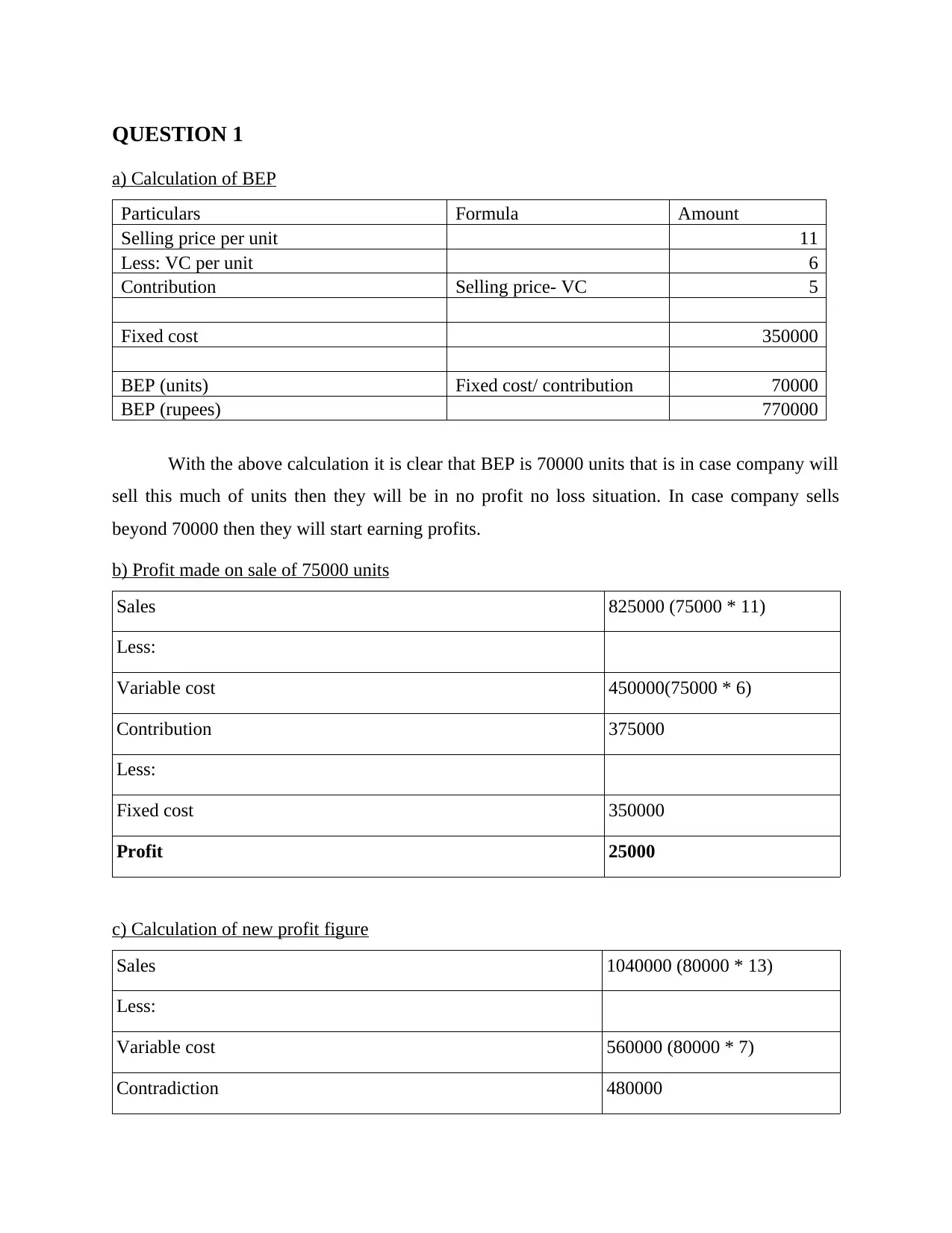

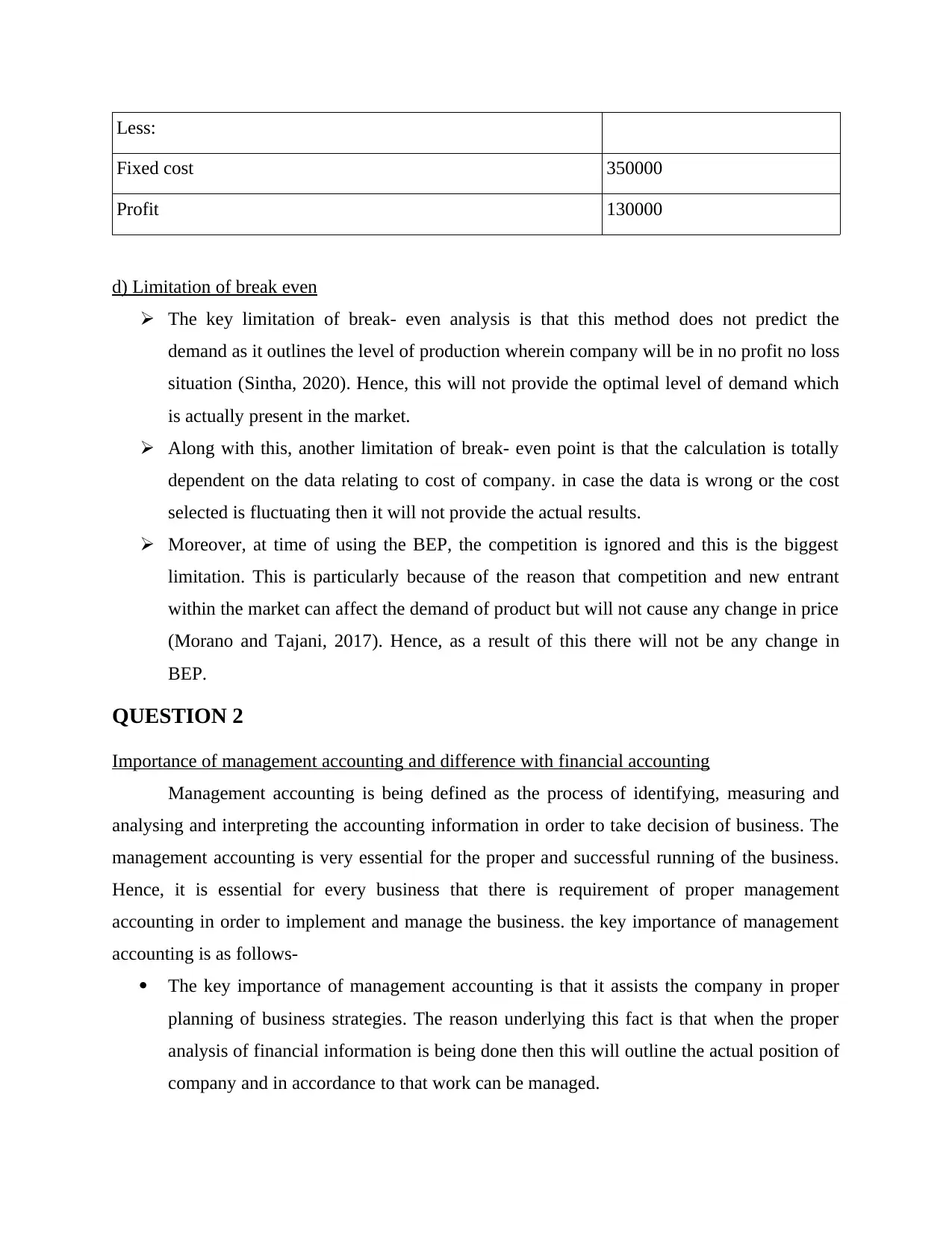

This document provides solutions to an accounting fundamentals exam, covering key concepts such as break-even point (BEP) calculation and the importance of management accounting. The BEP is calculated in units and rupees, and its limitations are discussed. The importance of management accounting is highlighted, along with the differences between management and financial accounting. Furthermore, the document outlines three techniques through which management accountants can achieve organizational objectives: budgetary control, financial statement analysis, and trend analysis and forecasting. These techniques aid in planning, decision-making, and identifying potential problems within the business. Desklib offers a platform for students to access similar solved assignments and study tools.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.