Auditing & Control Online Exam Solution: BA7010, May 2021

VerifiedAdded on 2022/12/12

|13

|3800

|406

Homework Assignment

AI Summary

This document provides a detailed solution to an online exam for the BA7010 Auditing & Control course. The solution addresses several key aspects of auditing, including the responsibilities of auditors, the importance of audit evidence, and the factors that indicate going concern difficulties. It explores the concepts of sufficient and appropriate audit evidence, as defined by ISA 500, and outlines the reliability of different types of audit evidence. The solution also differentiates between external and internal audits, the requirements for appointing an internal auditor and the relationship between them. Furthermore, it includes audit procedures for inventory counting and the ascertainment of inventory value. The document is structured to provide a comprehensive understanding of auditing principles and practices, making it a valuable resource for students studying auditing and control.

Online exam BA7010-

Auditing & Control

Auditing & Control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question: 1.......................................................................................................................................2

QUESTION 2..................................................................................................................................4

(a).................................................................................................................................................4

(b).................................................................................................................................................5

(c) Procedure of obtaining audit evidence involves:...................................................................6

QUESTION 4..................................................................................................................................7

(a) Audit procedure for inventory counting.................................................................................7

b) Five audit procedure for carrying out the ascertainment of the value of CRV’s inventory....7

Question 5........................................................................................................................................8

Difference between external and internal audit...........................................................................8

Requirements to appoint internal auditor....................................................................................9

Internal auditor reply upon external auditor................................................................................9

REFERENCES..............................................................................................................................11

1

Question: 1.......................................................................................................................................2

QUESTION 2..................................................................................................................................4

(a).................................................................................................................................................4

(b).................................................................................................................................................5

(c) Procedure of obtaining audit evidence involves:...................................................................6

QUESTION 4..................................................................................................................................7

(a) Audit procedure for inventory counting.................................................................................7

b) Five audit procedure for carrying out the ascertainment of the value of CRV’s inventory....7

Question 5........................................................................................................................................8

Difference between external and internal audit...........................................................................8

Requirements to appoint internal auditor....................................................................................9

Internal auditor reply upon external auditor................................................................................9

REFERENCES..............................................................................................................................11

1

Question: 1

a)

To

The Audit Senior

From: Audit manager

Subject: Issues identified with regards to Auditor’s responsibility

Date: 6 May, 2021

The various responsibilities stated regarding auditor’s responsibility as an auditors has been

found out to be incorrect on certain ground and there are many issues related to these

mentioned auditor’s responsibilities in the draft audit report of Keynes Ltd has been identified.

First of all, as an auditors are not responsible for preparing financial statements for or of the

companies rather it is the duty of the management of the company to prepare the same, and

auditors are just responsible for presenting their opinion about the fairness of these financial

statements based on the evaluation done (Hajering, 2019).

Second, the statement stating that “our responsibility is to express an opinion on all pages of

the financial statement based on our audit” is found to be incomplete as auditor’s are

responsible for listing out all the components of the financial statement they have audited

which may be balance sheet, income statement, cash flow statement, accounting policies

followed and all other information forming part of the notes to the account (DeZoort and

Harrison, 2018).

Third, in the second responsibility mentioned in the draft audit report which says that most of

the international standards on auditing has been followed is incorrect as auditors are obliged to

comply with all ISAs and there is a need to state to state they all the ISAs has been followed.

Fourth, with regards to obtaining maximum assurance in order to ensure that the financial

statements are free from any kind misstatements is incorrect as it is not possible even for

auditors to provide maximum assurance and no clear cut confirmation can be given that the

financial statements are free from errors due to the reason that practically it is not possible for

auditors to test each and every transactions and balances. And only sample of transactions are

tested upon along with some of the material balances that the auditor thought to be important

and therefore able to give reasonable assurance related to financial statement that they free

from misstatements (Maroun, 2017).

2

a)

To

The Audit Senior

From: Audit manager

Subject: Issues identified with regards to Auditor’s responsibility

Date: 6 May, 2021

The various responsibilities stated regarding auditor’s responsibility as an auditors has been

found out to be incorrect on certain ground and there are many issues related to these

mentioned auditor’s responsibilities in the draft audit report of Keynes Ltd has been identified.

First of all, as an auditors are not responsible for preparing financial statements for or of the

companies rather it is the duty of the management of the company to prepare the same, and

auditors are just responsible for presenting their opinion about the fairness of these financial

statements based on the evaluation done (Hajering, 2019).

Second, the statement stating that “our responsibility is to express an opinion on all pages of

the financial statement based on our audit” is found to be incomplete as auditor’s are

responsible for listing out all the components of the financial statement they have audited

which may be balance sheet, income statement, cash flow statement, accounting policies

followed and all other information forming part of the notes to the account (DeZoort and

Harrison, 2018).

Third, in the second responsibility mentioned in the draft audit report which says that most of

the international standards on auditing has been followed is incorrect as auditors are obliged to

comply with all ISAs and there is a need to state to state they all the ISAs has been followed.

Fourth, with regards to obtaining maximum assurance in order to ensure that the financial

statements are free from any kind misstatements is incorrect as it is not possible even for

auditors to provide maximum assurance and no clear cut confirmation can be given that the

financial statements are free from errors due to the reason that practically it is not possible for

auditors to test each and every transactions and balances. And only sample of transactions are

tested upon along with some of the material balances that the auditor thought to be important

and therefore able to give reasonable assurance related to financial statement that they free

from misstatements (Maroun, 2017).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fifth, auditor is not in anyways responsible for preventing and detecting frauds and errors as

the same is the responsibility of the management and thus auditors are responsible just for

detecting material misstatements either caused due to fraud or errors.

Sixth, a statement saying that auditors has nothing to do with the presentation of the financial

statements as the same is the duty of the management of the company is not true as auditors

are also responsible for ensuring that the presentation of financial statements is in accordance

with the relevant accounting standards and thus in line with the findings of their auditing.

b) Ten factors indicating that the company has a going concern difficulties are as follows:

Significant reduction in the sales revenue of the business indicates that the business is not

doing well. The decreased sales always leads to reduction in the overall profitability of

the business and profitability is necessary for any business to ensure long term survival.

Huge amount due on account of debt and interest payable thereon indicates that there is

financial problems with the company and management needs to resort to bank for the

loans. Such problems may arise on account of operating losses and poor cash flows. A

huge debt and interest payable thereon is a major indicator of business’s going concern as

sometimes financial crisis leads to the closure of the business.

Due to lack of cash flows there may be large amount of overdrafts and the same may

leads to the more cash outflows in the form of higher interest payable on such overdraft

amounts. And resorting to overdraft in itself is not a good option as bank may anytime

stop extending financial support in the form of overdraft which leads to negative impact

on the business operations. So, this may affect the going concern of the businesses (Chen,

Eshleman and Soileau, 2017).

Key management of the business when lost to competitors is considered to be a big threat

on the survival of the business as ordinary leaving of key management is also considered

as a negative sign of the company in the market and generally leads to the loss of

customer base too and thus affect the going concern of the business.

Cash flow problems with the business indicating through its cash flow statements,

balance sheet and liquidity ratios are a major concern for the business management team

as it too indicates going concern objective of the business.

When some major projects of the business are lost in the hand of the competitors then it

might create a problem for the business going concern as continuous loss of projects may

lead to the closure of the business (Näsman, 2019).

When businesses reliance on excessive short term borrowing for financing its long term

projects is the indicator of business going concern difficulties.

When there is a withdrawal from financial institutions, banks and creditors from lending

any additional finance to the business indicates that the business is facing an issue of

ensuring its going concern.

Adversity depicted by company’s financial ratios is a key indicators of business’s going

concern difficulties.

3

the same is the responsibility of the management and thus auditors are responsible just for

detecting material misstatements either caused due to fraud or errors.

Sixth, a statement saying that auditors has nothing to do with the presentation of the financial

statements as the same is the duty of the management of the company is not true as auditors

are also responsible for ensuring that the presentation of financial statements is in accordance

with the relevant accounting standards and thus in line with the findings of their auditing.

b) Ten factors indicating that the company has a going concern difficulties are as follows:

Significant reduction in the sales revenue of the business indicates that the business is not

doing well. The decreased sales always leads to reduction in the overall profitability of

the business and profitability is necessary for any business to ensure long term survival.

Huge amount due on account of debt and interest payable thereon indicates that there is

financial problems with the company and management needs to resort to bank for the

loans. Such problems may arise on account of operating losses and poor cash flows. A

huge debt and interest payable thereon is a major indicator of business’s going concern as

sometimes financial crisis leads to the closure of the business.

Due to lack of cash flows there may be large amount of overdrafts and the same may

leads to the more cash outflows in the form of higher interest payable on such overdraft

amounts. And resorting to overdraft in itself is not a good option as bank may anytime

stop extending financial support in the form of overdraft which leads to negative impact

on the business operations. So, this may affect the going concern of the businesses (Chen,

Eshleman and Soileau, 2017).

Key management of the business when lost to competitors is considered to be a big threat

on the survival of the business as ordinary leaving of key management is also considered

as a negative sign of the company in the market and generally leads to the loss of

customer base too and thus affect the going concern of the business.

Cash flow problems with the business indicating through its cash flow statements,

balance sheet and liquidity ratios are a major concern for the business management team

as it too indicates going concern objective of the business.

When some major projects of the business are lost in the hand of the competitors then it

might create a problem for the business going concern as continuous loss of projects may

lead to the closure of the business (Näsman, 2019).

When businesses reliance on excessive short term borrowing for financing its long term

projects is the indicator of business going concern difficulties.

When there is a withdrawal from financial institutions, banks and creditors from lending

any additional finance to the business indicates that the business is facing an issue of

ensuring its going concern.

Adversity depicted by company’s financial ratios is a key indicators of business’s going

concern difficulties.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Discontinuance in paying dividends and making arrears in paying back creditors on due

dates.

QUESTION 2

(a)

As per ISA 500 “Audit Evidence”, it refers to the evidence the external and independent

auditors acquire from the internal and external sources of the organization in order to provide

opinion on the financial statement of the business. The evidence that the auditor acquire must be

relevant and reliable which help the auditor in reflecting true and fair opinion on the financial

information.

Sufficient Audit Evidence

As per the standard, the audit evidence must meet the criteria of sufficient and appropriateness.

The sufficiency of audit evidence is measure in the term of quantity and describe that as

measuring the evidence in volume is subjective so the auditor needs to use their professional

judgement for this purpose. The standard also reflect that the sufficiency of audit evidence is also

depends upon the procedure of the audit which must be appropriate as per the circumstances. For

example: Documentation and Inspection (Lessambo, 2018).

Appropriate Audit Evidence

As sufficiency is measured in quantity the appropriateness is measured in quality as describe in

the standard. This means that the quality of the information must be consider by the independent

auditor at the time of conducting audit of the company. The standard defines that to measure the

appropriateness of audit evidence the auditor needs to check reliability and relevance of audit

evidence. For example: Analytical procedure and external confirmation.

Relevance of audit evidence: The purpose of audit procedure by the auditor is the base

which defines that whether the evidence is relevant or not. The direction of testing the

evidence is important for defining the relevance of the evidences. For example;

inspection of fixed assets is relevant for the purpose of auditing, verifying the existence

of plants and equipment is also relevant evidence etc.

Reliability of audit evidence: The reliability of evidence is depending upon the source,

nature and circumstance of the auditor while receiving audit evidences. As per standard,

these all three factors are play crucial role is measuring the reliability of any sources and

4

dates.

QUESTION 2

(a)

As per ISA 500 “Audit Evidence”, it refers to the evidence the external and independent

auditors acquire from the internal and external sources of the organization in order to provide

opinion on the financial statement of the business. The evidence that the auditor acquire must be

relevant and reliable which help the auditor in reflecting true and fair opinion on the financial

information.

Sufficient Audit Evidence

As per the standard, the audit evidence must meet the criteria of sufficient and appropriateness.

The sufficiency of audit evidence is measure in the term of quantity and describe that as

measuring the evidence in volume is subjective so the auditor needs to use their professional

judgement for this purpose. The standard also reflect that the sufficiency of audit evidence is also

depends upon the procedure of the audit which must be appropriate as per the circumstances. For

example: Documentation and Inspection (Lessambo, 2018).

Appropriate Audit Evidence

As sufficiency is measured in quantity the appropriateness is measured in quality as describe in

the standard. This means that the quality of the information must be consider by the independent

auditor at the time of conducting audit of the company. The standard defines that to measure the

appropriateness of audit evidence the auditor needs to check reliability and relevance of audit

evidence. For example: Analytical procedure and external confirmation.

Relevance of audit evidence: The purpose of audit procedure by the auditor is the base

which defines that whether the evidence is relevant or not. The direction of testing the

evidence is important for defining the relevance of the evidences. For example;

inspection of fixed assets is relevant for the purpose of auditing, verifying the existence

of plants and equipment is also relevant evidence etc.

Reliability of audit evidence: The reliability of evidence is depending upon the source,

nature and circumstance of the auditor while receiving audit evidences. As per standard,

these all three factors are play crucial role is measuring the reliability of any sources and

4

evidences. For example: external evidence is more reliable than the internal evidence

(LU, and Hai, 2021).

(b)

As per the ISA 500, the reliability of audit evidence is depending upon the following factors:

Audit evidence obtained from independent sources are more reliable than the evidence

obtained from internal and dependent sources.

The direct involvement of auditor while collecting audit evidence is more reliable that not

having any direct involvement in collecting audit evidence.

Audit evidence in written form is more reliable than the evidence in oral form.

The original document of evidences is more reliable as compared to evidences in the

photocopy form.

The control and circumstance matter a lot when the audit evidence comes or generates

from the clients and company (Aouira and et.al., 2020).

(1) Bank reconciliation statement is the reliable audit evidence as per the ISA 500 because it is

basically prepared by the bank accountant which reflect that this particular source of evidences is

external to the company and reliable. The auditor can also use the cash book and pass book of

the clients in order to check the exact difference and figures of the cash and bank balance.

(2) A payables confirmation letter is considered as external confirmation is reliable audit

evidence as per the Indian accounting standards. Along with that such confirmation letter is in

written form which increases their reliability and relevance. But for this the additionally the

auditor also has to ask the suppliers orally about their concern and issues via phone or personal

visit.

(3) The copy of article is a not a reliable source because it is not an original document as defined

by the standard. So, to obtain reliable audit evidence the auditor needs to ask for the original

article because articles always reflect correct information because it is available to public for

access purpose. The auditor can also analyse the performance of the company which are acquired

by the superb lift plc.

5

(LU, and Hai, 2021).

(b)

As per the ISA 500, the reliability of audit evidence is depending upon the following factors:

Audit evidence obtained from independent sources are more reliable than the evidence

obtained from internal and dependent sources.

The direct involvement of auditor while collecting audit evidence is more reliable that not

having any direct involvement in collecting audit evidence.

Audit evidence in written form is more reliable than the evidence in oral form.

The original document of evidences is more reliable as compared to evidences in the

photocopy form.

The control and circumstance matter a lot when the audit evidence comes or generates

from the clients and company (Aouira and et.al., 2020).

(1) Bank reconciliation statement is the reliable audit evidence as per the ISA 500 because it is

basically prepared by the bank accountant which reflect that this particular source of evidences is

external to the company and reliable. The auditor can also use the cash book and pass book of

the clients in order to check the exact difference and figures of the cash and bank balance.

(2) A payables confirmation letter is considered as external confirmation is reliable audit

evidence as per the Indian accounting standards. Along with that such confirmation letter is in

written form which increases their reliability and relevance. But for this the additionally the

auditor also has to ask the suppliers orally about their concern and issues via phone or personal

visit.

(3) The copy of article is a not a reliable source because it is not an original document as defined

by the standard. So, to obtain reliable audit evidence the auditor needs to ask for the original

article because articles always reflect correct information because it is available to public for

access purpose. The auditor can also analyse the performance of the company which are acquired

by the superb lift plc.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(4) As per the factors of the reliability it is clear that if the auditor involves personally in the

auditing process via inspection and observation than such audit evidence must be considered as

reliable. So, in this case inspection of registration document of directors’ car is reliable audit

evidence as per the standard guild lines and provision (Appelbaum, Kogan and Vasarhelyi,

2017).

(5) Accounts receivable confirmation letter is a reliable audit evidence as per the accounting

standard 500 because it is not only reflecting the external confirmation but it also involves

auditor in to the auditing process. It is because the auditors select particular customers having

high amount of outstanding and ask them for their total amount of accounts receivables in order

to match it with the amount reflect by company’s books.

(6) Photocopy of title deed is not reliable audit evidence because it is not an original document

which do not meet the criteria of the reliable audit evidence. For this the auditor need to adopt

original deed because they have right to access the deed in order to give opinion on the true and

fair view of financial statement (Kokina and Davenport, 2017).

(c) Procedure of obtaining audit evidence involves:

Audit inquiry: In order to obtain understanding audit evidence and to confirm some

related issues and assertion the auditor have to inquires the management of the company

on certain business transaction and events.

Analytical observation: This is the procedure have to followed by the auditor for the

purpose of obtaining sufficient and appropriate audit evidence. The need to observe the

way through which the controls is related to the performance of the financial reporting.

Audit Inspection: The auditor has to inspect certain document and evidences of the

company which required attention of the stakeholders of the company. For example:

inspection of plants and assets, inspection of provision is made by the company or not in

case of any uncertainty.

6

auditing process via inspection and observation than such audit evidence must be considered as

reliable. So, in this case inspection of registration document of directors’ car is reliable audit

evidence as per the standard guild lines and provision (Appelbaum, Kogan and Vasarhelyi,

2017).

(5) Accounts receivable confirmation letter is a reliable audit evidence as per the accounting

standard 500 because it is not only reflecting the external confirmation but it also involves

auditor in to the auditing process. It is because the auditors select particular customers having

high amount of outstanding and ask them for their total amount of accounts receivables in order

to match it with the amount reflect by company’s books.

(6) Photocopy of title deed is not reliable audit evidence because it is not an original document

which do not meet the criteria of the reliable audit evidence. For this the auditor need to adopt

original deed because they have right to access the deed in order to give opinion on the true and

fair view of financial statement (Kokina and Davenport, 2017).

(c) Procedure of obtaining audit evidence involves:

Audit inquiry: In order to obtain understanding audit evidence and to confirm some

related issues and assertion the auditor have to inquires the management of the company

on certain business transaction and events.

Analytical observation: This is the procedure have to followed by the auditor for the

purpose of obtaining sufficient and appropriate audit evidence. The need to observe the

way through which the controls is related to the performance of the financial reporting.

Audit Inspection: The auditor has to inspect certain document and evidences of the

company which required attention of the stakeholders of the company. For example:

inspection of plants and assets, inspection of provision is made by the company or not in

case of any uncertainty.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 4

(a) Audit procedure for inventory counting

Cut-off analysis: This involves the examination of the procedure of halting of any further

receiving and shipment of inventory in the organization by the auditors. The auditor

needs to record the time of shipment of the inventory and match it with the physical

inventory time. So, that any extra time will be excluded from the inventory record

keeping (Buyurgan, Zhang and Okyay, 2019).

Observe the physical inventory count: For taking appropriate audit evidence and

providing true and fair opinion to the company on their financial statement the auditor

has to physical observe all the inventory by themselves. To make it more reliable and

relevant auditor also need to test, count and trace some of the inventory by themselves.

Reconcile the inventory count to the general ledger: After analysing and observing all

the inventory physically, the auditor has to match the inventory count with the general

ledger book which is prepared by the company. If they do not have any difference than

auditor must give them clear opinion but in case if any difference arises the auditor must

apply analytical procedure.

Test inventory in transit: The auditor also needs to adopt the information regarding the

inventory which are in transit and yet not received by the company. Because it helps them

in analysing the figure of closing inventory which must include inventory in transit

because of accrual accounting.

Finished goods cost analysis: This is another procedure the auditor has to do in order to

analyse the cost of the good that is actually available to sale. This helps the auditor in

comparing the cost with the selling price so that they can identify the profit percentage of

the company (Han, Bae and Lee, 2018).

b) Five audit procedure for carrying out the ascertainment of the value of CRV’s inventory

First procedure towards valuing inventory is to confirm the existence of inventory

through physical verification and the auditor can do so by joining year-end inventory

count or perform their own with the help of sampling. Physical verification does not only

ensures the existence but also confirms on the condition of the inventories. The procedure

of inventory count is helpful in identifying errors related to the quantity of inventory

reported in the balance sheet by the client.

7

(a) Audit procedure for inventory counting

Cut-off analysis: This involves the examination of the procedure of halting of any further

receiving and shipment of inventory in the organization by the auditors. The auditor

needs to record the time of shipment of the inventory and match it with the physical

inventory time. So, that any extra time will be excluded from the inventory record

keeping (Buyurgan, Zhang and Okyay, 2019).

Observe the physical inventory count: For taking appropriate audit evidence and

providing true and fair opinion to the company on their financial statement the auditor

has to physical observe all the inventory by themselves. To make it more reliable and

relevant auditor also need to test, count and trace some of the inventory by themselves.

Reconcile the inventory count to the general ledger: After analysing and observing all

the inventory physically, the auditor has to match the inventory count with the general

ledger book which is prepared by the company. If they do not have any difference than

auditor must give them clear opinion but in case if any difference arises the auditor must

apply analytical procedure.

Test inventory in transit: The auditor also needs to adopt the information regarding the

inventory which are in transit and yet not received by the company. Because it helps them

in analysing the figure of closing inventory which must include inventory in transit

because of accrual accounting.

Finished goods cost analysis: This is another procedure the auditor has to do in order to

analyse the cost of the good that is actually available to sale. This helps the auditor in

comparing the cost with the selling price so that they can identify the profit percentage of

the company (Han, Bae and Lee, 2018).

b) Five audit procedure for carrying out the ascertainment of the value of CRV’s inventory

First procedure towards valuing inventory is to confirm the existence of inventory

through physical verification and the auditor can do so by joining year-end inventory

count or perform their own with the help of sampling. Physical verification does not only

ensures the existence but also confirms on the condition of the inventories. The procedure

of inventory count is helpful in identifying errors related to the quantity of inventory

reported in the balance sheet by the client.

7

Second procedure involves reviewing the ownership of the client over the inventories by

checking quotations, invoices, contracts and delivery notes. Terms and conditions

mentioned in the contracts so audited by the auditor is very useful in determining the

ownership of the inventory.

Third procedure involves assessment of the value of the inventory. As per the IAS and

IFRS standards related to inventory valuation, it allows for measuring inventories on

lowest of cost or net value that could be realized from its sale. The auditor here is

responsible for reviewing the method of costing and policy of accounting that has been

followed by the company in valuing its inventories (Mitra, 2017). For the inventories of

WIP and finished goods, review of cost of conversion must be done that leads to the

conversion of raw material to WIP and WIP to finished goods. And at last review must be

done on account of identifying any unnecessary costs or cost not allowed by IAS2 are

included in the inventory’s cost.

Fourth procedure involves review of cut off. Cut off can be best reviewed through

shipping documents and any more documents that depicts and prove the delivery and

receive dates. This helps auditors in ensuring that the inventories are being recorded in

the period from which it is belonging to (Safonova and Alekseenko, 2019).

Analytical review is the fifth procedure to determine any kind of unreasonable events and

transactions related to the inventory. Analytical review allows for reducing risk related to

inventory more efficiently. Trends in revenue from sales and COGS is the best way to

determine what happens to the inventory during the accounting period, so that better

understanding can be developed by the auditor related to the valuation of inventory.

Question 5

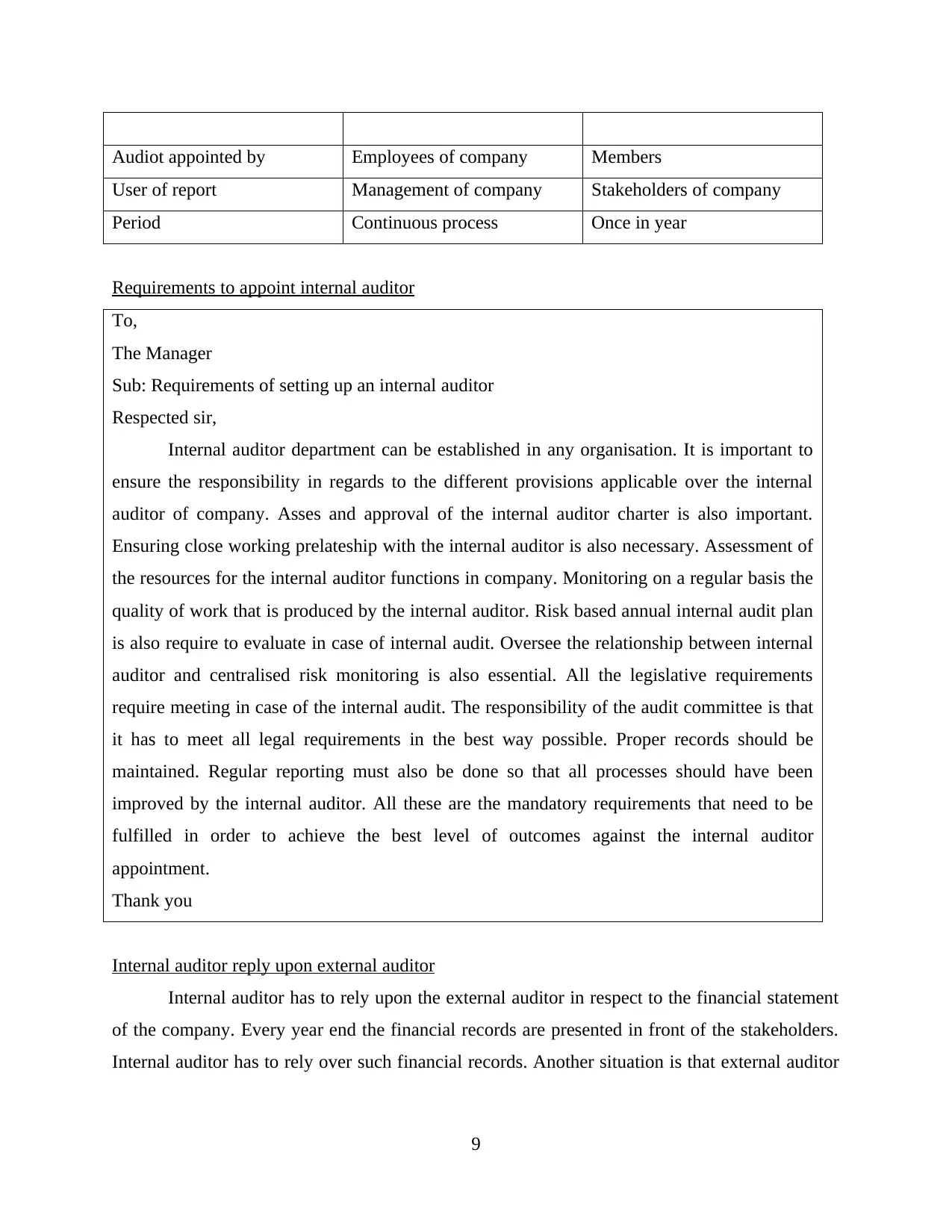

Difference between external and internal audit

Point of difference Internal audit External audit

Objectives Review the routine activates

and provides suggestion of

improvement.

Analysis and evaluate the

financial statement of the

business entity.

Conducted by Employees of company Third part

8

checking quotations, invoices, contracts and delivery notes. Terms and conditions

mentioned in the contracts so audited by the auditor is very useful in determining the

ownership of the inventory.

Third procedure involves assessment of the value of the inventory. As per the IAS and

IFRS standards related to inventory valuation, it allows for measuring inventories on

lowest of cost or net value that could be realized from its sale. The auditor here is

responsible for reviewing the method of costing and policy of accounting that has been

followed by the company in valuing its inventories (Mitra, 2017). For the inventories of

WIP and finished goods, review of cost of conversion must be done that leads to the

conversion of raw material to WIP and WIP to finished goods. And at last review must be

done on account of identifying any unnecessary costs or cost not allowed by IAS2 are

included in the inventory’s cost.

Fourth procedure involves review of cut off. Cut off can be best reviewed through

shipping documents and any more documents that depicts and prove the delivery and

receive dates. This helps auditors in ensuring that the inventories are being recorded in

the period from which it is belonging to (Safonova and Alekseenko, 2019).

Analytical review is the fifth procedure to determine any kind of unreasonable events and

transactions related to the inventory. Analytical review allows for reducing risk related to

inventory more efficiently. Trends in revenue from sales and COGS is the best way to

determine what happens to the inventory during the accounting period, so that better

understanding can be developed by the auditor related to the valuation of inventory.

Question 5

Difference between external and internal audit

Point of difference Internal audit External audit

Objectives Review the routine activates

and provides suggestion of

improvement.

Analysis and evaluate the

financial statement of the

business entity.

Conducted by Employees of company Third part

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audiot appointed by Employees of company Members

User of report Management of company Stakeholders of company

Period Continuous process Once in year

Requirements to appoint internal auditor

To,

The Manager

Sub: Requirements of setting up an internal auditor

Respected sir,

Internal auditor department can be established in any organisation. It is important to

ensure the responsibility in regards to the different provisions applicable over the internal

auditor of company. Asses and approval of the internal auditor charter is also important.

Ensuring close working prelateship with the internal auditor is also necessary. Assessment of

the resources for the internal auditor functions in company. Monitoring on a regular basis the

quality of work that is produced by the internal auditor. Risk based annual internal audit plan

is also require to evaluate in case of internal audit. Oversee the relationship between internal

auditor and centralised risk monitoring is also essential. All the legislative requirements

require meeting in case of the internal audit. The responsibility of the audit committee is that

it has to meet all legal requirements in the best way possible. Proper records should be

maintained. Regular reporting must also be done so that all processes should have been

improved by the internal auditor. All these are the mandatory requirements that need to be

fulfilled in order to achieve the best level of outcomes against the internal auditor

appointment.

Thank you

Internal auditor reply upon external auditor

Internal auditor has to rely upon the external auditor in respect to the financial statement

of the company. Every year end the financial records are presented in front of the stakeholders.

Internal auditor has to rely over such financial records. Another situation is that external auditor

9

User of report Management of company Stakeholders of company

Period Continuous process Once in year

Requirements to appoint internal auditor

To,

The Manager

Sub: Requirements of setting up an internal auditor

Respected sir,

Internal auditor department can be established in any organisation. It is important to

ensure the responsibility in regards to the different provisions applicable over the internal

auditor of company. Asses and approval of the internal auditor charter is also important.

Ensuring close working prelateship with the internal auditor is also necessary. Assessment of

the resources for the internal auditor functions in company. Monitoring on a regular basis the

quality of work that is produced by the internal auditor. Risk based annual internal audit plan

is also require to evaluate in case of internal audit. Oversee the relationship between internal

auditor and centralised risk monitoring is also essential. All the legislative requirements

require meeting in case of the internal audit. The responsibility of the audit committee is that

it has to meet all legal requirements in the best way possible. Proper records should be

maintained. Regular reporting must also be done so that all processes should have been

improved by the internal auditor. All these are the mandatory requirements that need to be

fulfilled in order to achieve the best level of outcomes against the internal auditor

appointment.

Thank you

Internal auditor reply upon external auditor

Internal auditor has to rely upon the external auditor in respect to the financial statement

of the company. Every year end the financial records are presented in front of the stakeholders.

Internal auditor has to rely over such financial records. Another situation is that external auditor

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

present the audit report demonstrate the position of business in the auditor report. Internal auditor

also has to rely over all such factors external auditor demonstrates in its audit report.

10

also has to rely over all such factors external auditor demonstrates in its audit report.

10

REFERENCES

Books and journals

Lessambo, F. I., 2018. Audit Evidence and Documentation. In Auditing, Assurance Services, and

Forensics (pp. 155-182). Palgrave Macmillan, Cham.

LU, H. and Hai, L.U., 2021. Structural analysis of audit evidence using belief functions.

(2002). Fuzzy Set and Systems. 131(1). pp.107-120.

Aouira, N. and et.al., 2020. Paper based vs. electronic records for clinical audit: Evidence of

documentation of medication safety monitoring in youth prescribed

antipsychotics. Children and Youth Services Review. 109. p.104666.

Appelbaum, D., Kogan, A. and Vasarhelyi, M. A., 2017. Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory. 36(4).

pp.1-27.

Kokina, J. and Davenport, T. H., 2017. The emergence of artificial intelligence: How automation

is changing auditing. Journal of emerging technologies in accounting. 14(1). pp.115-122.

Buyurgan, N., Zhang, S. and Okyay, H. K., 2019. Methodical analysis of inventory discrepancy

under conditions of uncertainty in supply chain management. International Journal of

Logistics Systems and Management. 32(2). pp.272-290.

Han, K. H., Bae, S. M. and Lee, W., 2018, March. Integrated inventory management system for

outdoors stocks based on small UAV and Beacon. In World Conference on Information

Systems and Technologies (pp. 533-541). Springer, Cham.

Maroun, W., 2017. Assuring the integrated report: Insights and recommendations from auditors

and preparers. The British Accounting Review, 49(3), pp.329-346.

DeZoort, F. T. and Harrison, P. D., 2018. Understanding auditors’ sense of responsibility for

detecting fraud within organizations. Journal of Business Ethics, 149(4), pp.857-874.

Hajering, M. S., 2019. Moderating Ethics Auditors Influence of Competence, Accountability on

Audit Quality. Jurnal Akuntansi, 23(3), pp.468-481.

Mitra, U. P., 2017. Inventory management process and internal audit procedure of Square

Toiletries Ltd.

Safonova, M. and Alekseenko, A., 2019, November. Information and analytical support for

internal audit of inventories. In International Conference on Sustainable Development of

Cross-Border Regions: Economic, Social and Security Challenges (ICSDCBR 2019) (pp.

49-53). Atlantis Press.

Näsman, L., 2019. A Qualitative Look into Going Concern Reports: From the Auditor's

Perspective.

Chen, Y., Eshleman, J. D. and Soileau, J. S., 2017. Business strategy and auditor

reporting. Auditing: A Journal of Practice & Theory, 36(2), pp.63-86.

11

Books and journals

Lessambo, F. I., 2018. Audit Evidence and Documentation. In Auditing, Assurance Services, and

Forensics (pp. 155-182). Palgrave Macmillan, Cham.

LU, H. and Hai, L.U., 2021. Structural analysis of audit evidence using belief functions.

(2002). Fuzzy Set and Systems. 131(1). pp.107-120.

Aouira, N. and et.al., 2020. Paper based vs. electronic records for clinical audit: Evidence of

documentation of medication safety monitoring in youth prescribed

antipsychotics. Children and Youth Services Review. 109. p.104666.

Appelbaum, D., Kogan, A. and Vasarhelyi, M. A., 2017. Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory. 36(4).

pp.1-27.

Kokina, J. and Davenport, T. H., 2017. The emergence of artificial intelligence: How automation

is changing auditing. Journal of emerging technologies in accounting. 14(1). pp.115-122.

Buyurgan, N., Zhang, S. and Okyay, H. K., 2019. Methodical analysis of inventory discrepancy

under conditions of uncertainty in supply chain management. International Journal of

Logistics Systems and Management. 32(2). pp.272-290.

Han, K. H., Bae, S. M. and Lee, W., 2018, March. Integrated inventory management system for

outdoors stocks based on small UAV and Beacon. In World Conference on Information

Systems and Technologies (pp. 533-541). Springer, Cham.

Maroun, W., 2017. Assuring the integrated report: Insights and recommendations from auditors

and preparers. The British Accounting Review, 49(3), pp.329-346.

DeZoort, F. T. and Harrison, P. D., 2018. Understanding auditors’ sense of responsibility for

detecting fraud within organizations. Journal of Business Ethics, 149(4), pp.857-874.

Hajering, M. S., 2019. Moderating Ethics Auditors Influence of Competence, Accountability on

Audit Quality. Jurnal Akuntansi, 23(3), pp.468-481.

Mitra, U. P., 2017. Inventory management process and internal audit procedure of Square

Toiletries Ltd.

Safonova, M. and Alekseenko, A., 2019, November. Information and analytical support for

internal audit of inventories. In International Conference on Sustainable Development of

Cross-Border Regions: Economic, Social and Security Challenges (ICSDCBR 2019) (pp.

49-53). Atlantis Press.

Näsman, L., 2019. A Qualitative Look into Going Concern Reports: From the Auditor's

Perspective.

Chen, Y., Eshleman, J. D. and Soileau, J. S., 2017. Business strategy and auditor

reporting. Auditing: A Journal of Practice & Theory, 36(2), pp.63-86.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.