Contemporary Issues in Financial Accounting: Online Exam

VerifiedAdded on 2022/11/30

|13

|2382

|134

AI Summary

This document is an online exam on contemporary issues in financial accounting. It includes sections on total comprehensive income, change in equity, financial position, revenue model, conceptual framework, accounting policy change, related party disclosures, and management commentary. The document provides detailed explanations and calculations for each section. It is a valuable resource for students studying financial accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ONLINE EXAM

CONTEMPORARY ISSUES

IN FINANCIAL

ACCOUNTING

CONTEMPORARY ISSUES

IN FINANCIAL

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Table of Contents

MAIN BODY..................................................................................................................................................3

SECTION- A ..................................................................................................................................................3

SECTION- B...................................................................................................................................................5

Question B1 ...........................................................................................................................................5

Question B2 ...........................................................................................................................................6

Question B3............................................................................................................................................6

Question B4 ...........................................................................................................................................7

Question B5............................................................................................................................................9

Question B6..........................................................................................................................................10

REFERENCES..............................................................................................................................................12

Table of Contents

MAIN BODY..................................................................................................................................................3

SECTION- A ..................................................................................................................................................3

SECTION- B...................................................................................................................................................5

Question B1 ...........................................................................................................................................5

Question B2 ...........................................................................................................................................6

Question B3............................................................................................................................................6

Question B4 ...........................................................................................................................................7

Question B5............................................................................................................................................9

Question B6..........................................................................................................................................10

REFERENCES..............................................................................................................................................12

MAIN BODY

SECTION- A

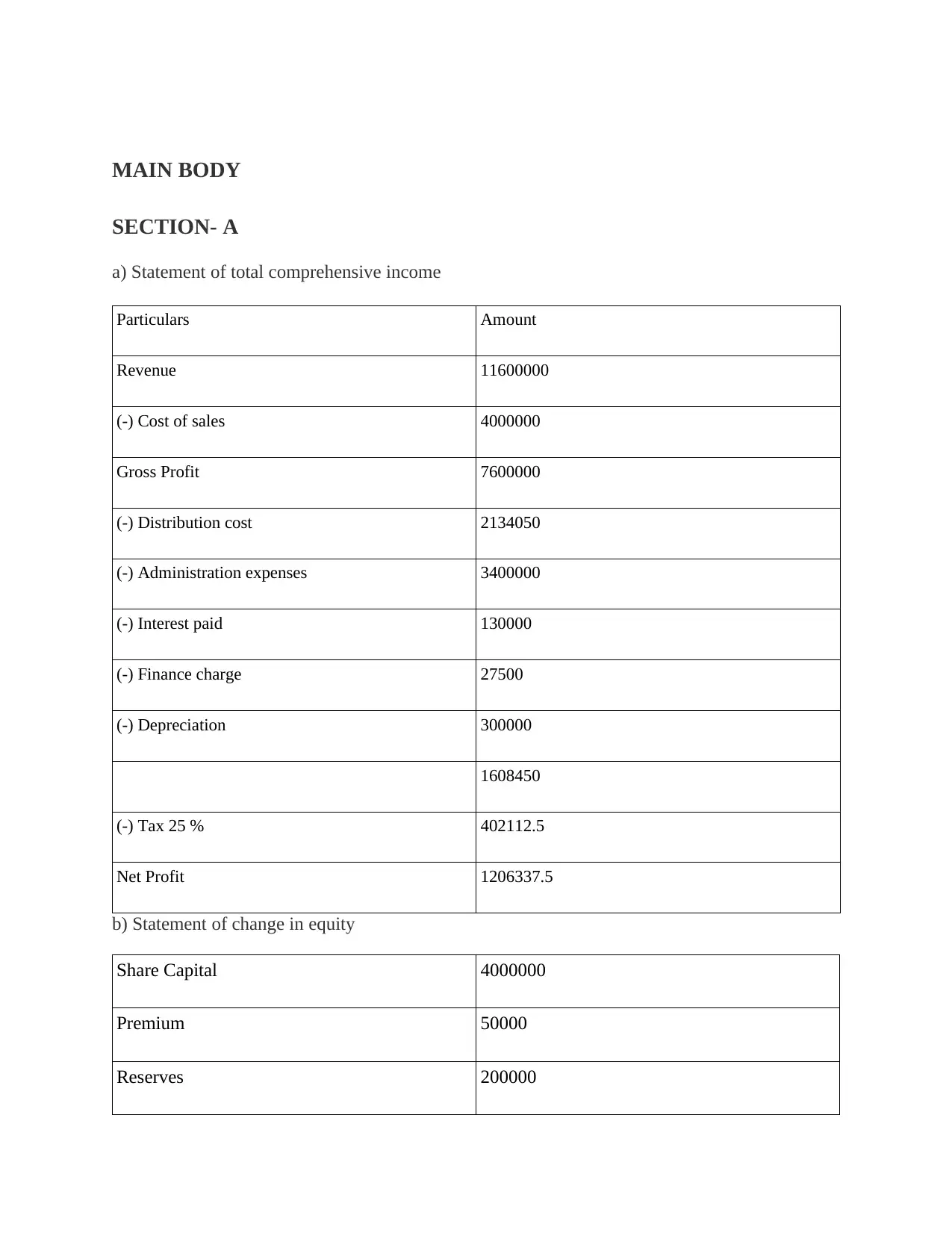

a) Statement of total comprehensive income

Particulars Amount

Revenue 11600000

(-) Cost of sales 4000000

Gross Profit 7600000

(-) Distribution cost 2134050

(-) Administration expenses 3400000

(-) Interest paid 130000

(-) Finance charge 27500

(-) Depreciation 300000

1608450

(-) Tax 25 % 402112.5

Net Profit 1206337.5

b) Statement of change in equity

Share Capital 4000000

Premium 50000

Reserves 200000

SECTION- A

a) Statement of total comprehensive income

Particulars Amount

Revenue 11600000

(-) Cost of sales 4000000

Gross Profit 7600000

(-) Distribution cost 2134050

(-) Administration expenses 3400000

(-) Interest paid 130000

(-) Finance charge 27500

(-) Depreciation 300000

1608450

(-) Tax 25 % 402112.5

Net Profit 1206337.5

b) Statement of change in equity

Share Capital 4000000

Premium 50000

Reserves 200000

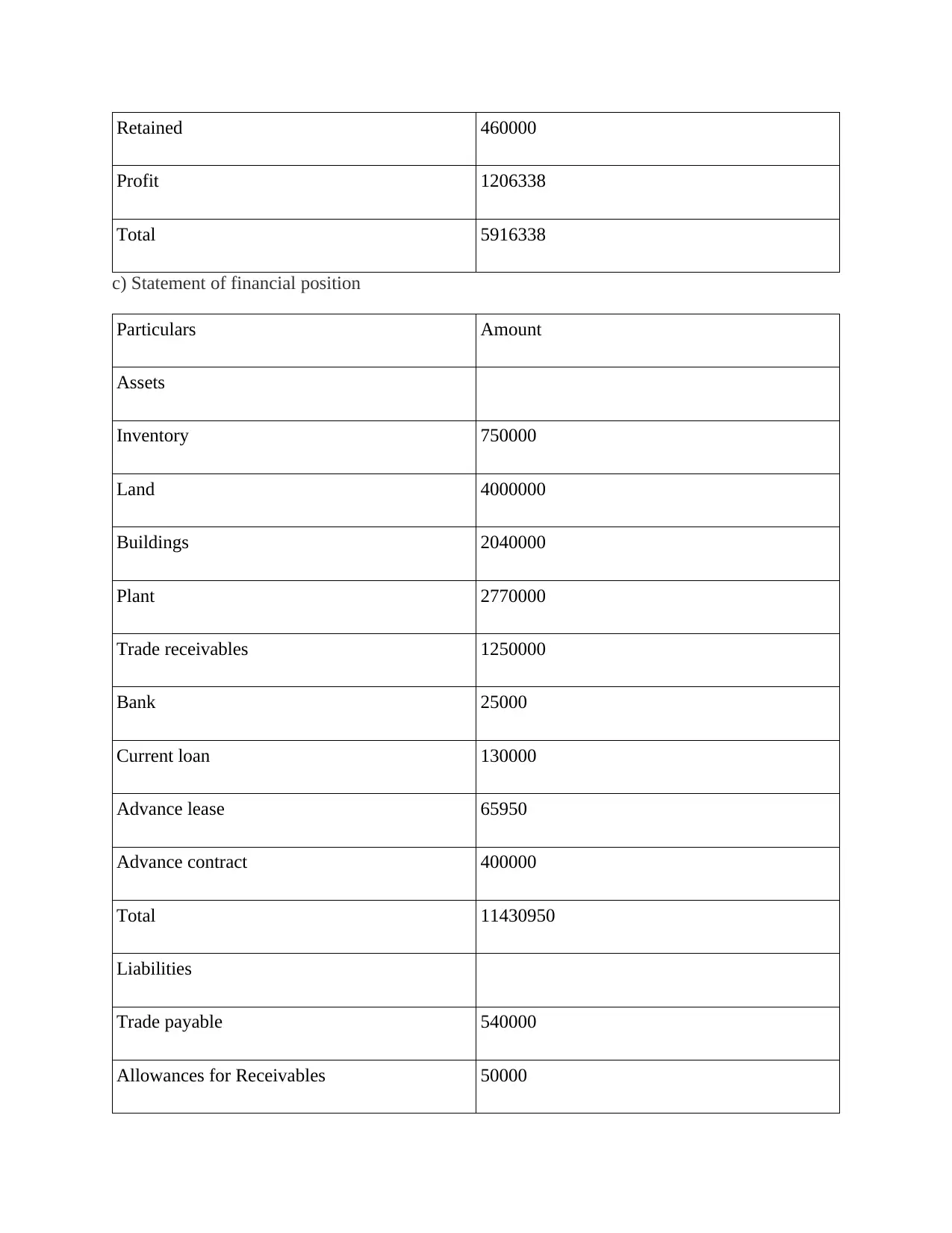

Retained 460000

Profit 1206338

Total 5916338

c) Statement of financial position

Particulars Amount

Assets

Inventory 750000

Land 4000000

Buildings 2040000

Plant 2770000

Trade receivables 1250000

Bank 25000

Current loan 130000

Advance lease 65950

Advance contract 400000

Total 11430950

Liabilities

Trade payable 540000

Allowances for Receivables 50000

Profit 1206338

Total 5916338

c) Statement of financial position

Particulars Amount

Assets

Inventory 750000

Land 4000000

Buildings 2040000

Plant 2770000

Trade receivables 1250000

Bank 25000

Current loan 130000

Advance lease 65950

Advance contract 400000

Total 11430950

Liabilities

Trade payable 540000

Allowances for Receivables 50000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

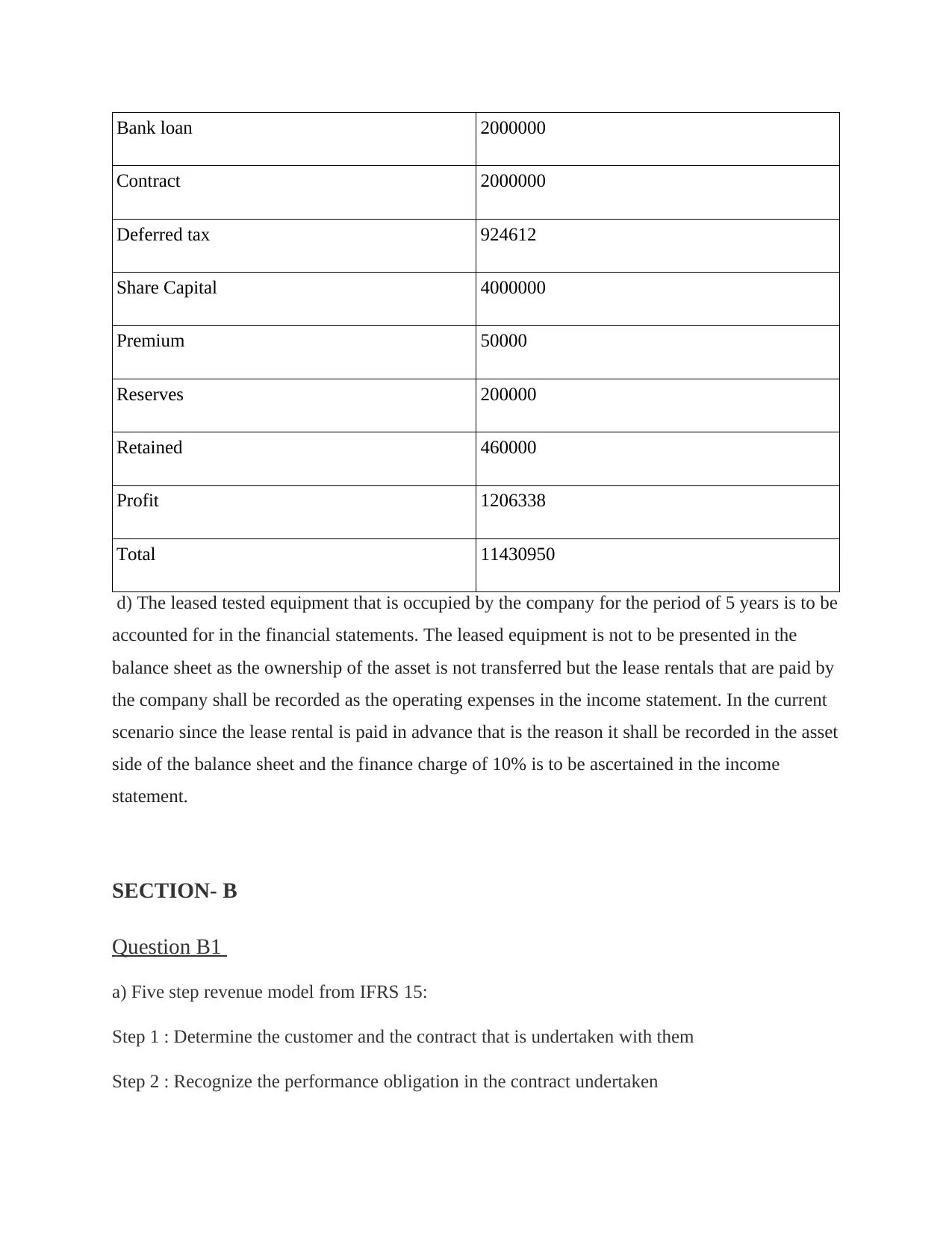

Bank loan 2000000

Contract 2000000

Deferred tax 924612

Share Capital 4000000

Premium 50000

Reserves 200000

Retained 460000

Profit 1206338

Total 11430950

d) The leased tested equipment that is occupied by the company for the period of 5 years is to be

accounted for in the financial statements. The leased equipment is not to be presented in the

balance sheet as the ownership of the asset is not transferred but the lease rentals that are paid by

the company shall be recorded as the operating expenses in the income statement. In the current

scenario since the lease rental is paid in advance that is the reason it shall be recorded in the asset

side of the balance sheet and the finance charge of 10% is to be ascertained in the income

statement.

SECTION- B

Question B1

a) Five step revenue model from IFRS 15:

Step 1 : Determine the customer and the contract that is undertaken with them

Step 2 : Recognize the performance obligation in the contract undertaken

Contract 2000000

Deferred tax 924612

Share Capital 4000000

Premium 50000

Reserves 200000

Retained 460000

Profit 1206338

Total 11430950

d) The leased tested equipment that is occupied by the company for the period of 5 years is to be

accounted for in the financial statements. The leased equipment is not to be presented in the

balance sheet as the ownership of the asset is not transferred but the lease rentals that are paid by

the company shall be recorded as the operating expenses in the income statement. In the current

scenario since the lease rental is paid in advance that is the reason it shall be recorded in the asset

side of the balance sheet and the finance charge of 10% is to be ascertained in the income

statement.

SECTION- B

Question B1

a) Five step revenue model from IFRS 15:

Step 1 : Determine the customer and the contract that is undertaken with them

Step 2 : Recognize the performance obligation in the contract undertaken

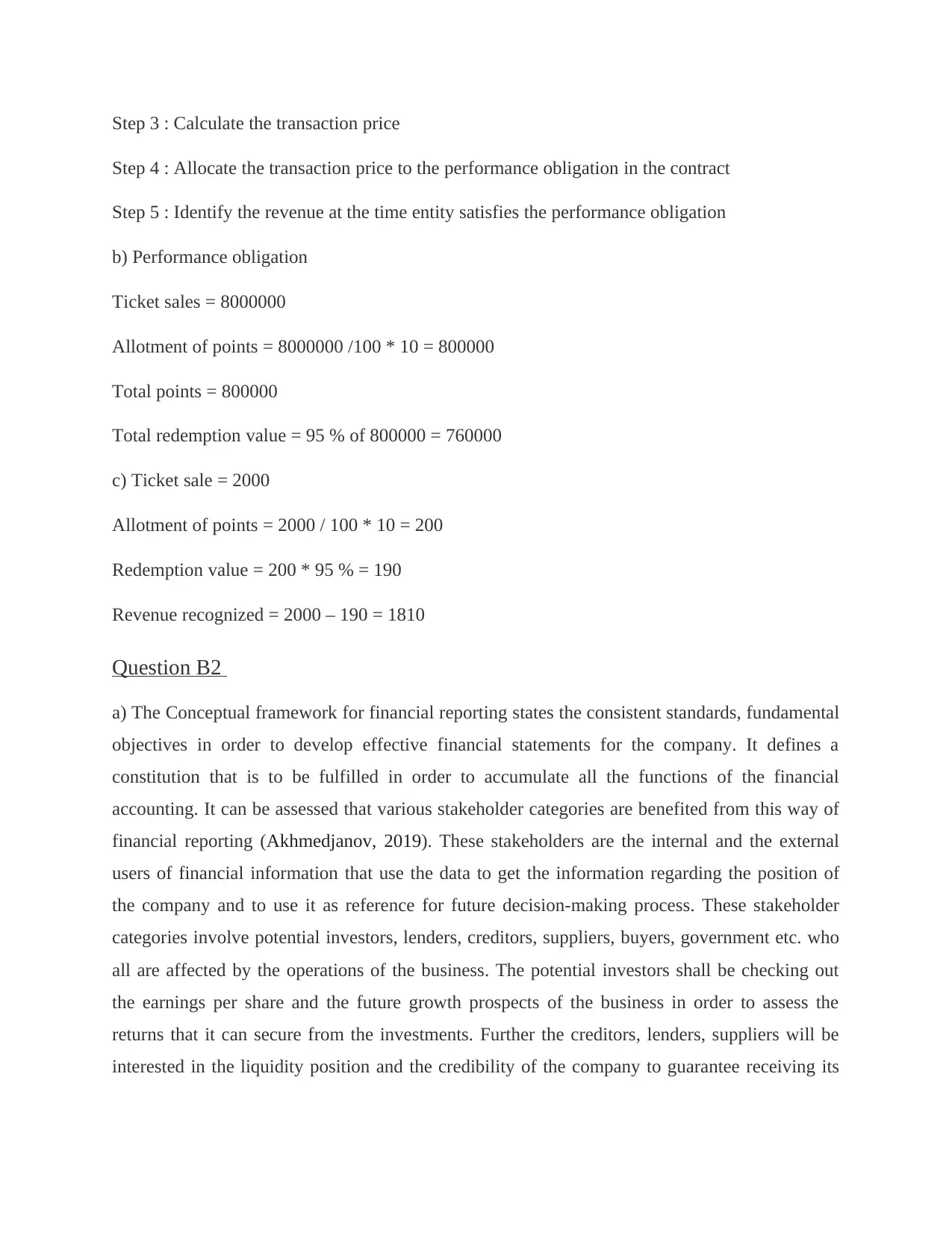

Step 3 : Calculate the transaction price

Step 4 : Allocate the transaction price to the performance obligation in the contract

Step 5 : Identify the revenue at the time entity satisfies the performance obligation

b) Performance obligation

Ticket sales = 8000000

Allotment of points = 8000000 /100 * 10 = 800000

Total points = 800000

Total redemption value = 95 % of 800000 = 760000

c) Ticket sale = 2000

Allotment of points = 2000 / 100 * 10 = 200

Redemption value = 200 * 95 % = 190

Revenue recognized = 2000 – 190 = 1810

Question B2

a) The Conceptual framework for financial reporting states the consistent standards, fundamental

objectives in order to develop effective financial statements for the company. It defines a

constitution that is to be fulfilled in order to accumulate all the functions of the financial

accounting. It can be assessed that various stakeholder categories are benefited from this way of

financial reporting (Akhmedjanov, 2019). These stakeholders are the internal and the external

users of financial information that use the data to get the information regarding the position of

the company and to use it as reference for future decision-making process. These stakeholder

categories involve potential investors, lenders, creditors, suppliers, buyers, government etc. who

all are affected by the operations of the business. The potential investors shall be checking out

the earnings per share and the future growth prospects of the business in order to assess the

returns that it can secure from the investments. Further the creditors, lenders, suppliers will be

interested in the liquidity position and the credibility of the company to guarantee receiving its

Step 4 : Allocate the transaction price to the performance obligation in the contract

Step 5 : Identify the revenue at the time entity satisfies the performance obligation

b) Performance obligation

Ticket sales = 8000000

Allotment of points = 8000000 /100 * 10 = 800000

Total points = 800000

Total redemption value = 95 % of 800000 = 760000

c) Ticket sale = 2000

Allotment of points = 2000 / 100 * 10 = 200

Redemption value = 200 * 95 % = 190

Revenue recognized = 2000 – 190 = 1810

Question B2

a) The Conceptual framework for financial reporting states the consistent standards, fundamental

objectives in order to develop effective financial statements for the company. It defines a

constitution that is to be fulfilled in order to accumulate all the functions of the financial

accounting. It can be assessed that various stakeholder categories are benefited from this way of

financial reporting (Akhmedjanov, 2019). These stakeholders are the internal and the external

users of financial information that use the data to get the information regarding the position of

the company and to use it as reference for future decision-making process. These stakeholder

categories involve potential investors, lenders, creditors, suppliers, buyers, government etc. who

all are affected by the operations of the business. The potential investors shall be checking out

the earnings per share and the future growth prospects of the business in order to assess the

returns that it can secure from the investments. Further the creditors, lenders, suppliers will be

interested in the liquidity position and the credibility of the company to guarantee receiving its

debts in future. This is how the various stakeholder categories make decision through the

financial reporting.

b) It can be advised to the uncle and to Wong Brothers Ltd that the financial accounting and

recording of the transaction is done in respect of the recognition concept as specified by the

Conceptual Framework. The recognition concept says that the income and expenses of the

business are to be recorded in the books of accounts at the time it has been accrued irrespective

of whether they are paid or not. So the transaction related to purchase of goods worth 300000 has

to be recorded on the date of transactions even though a 6 months credit period is offered by the

supplier.

Question B3

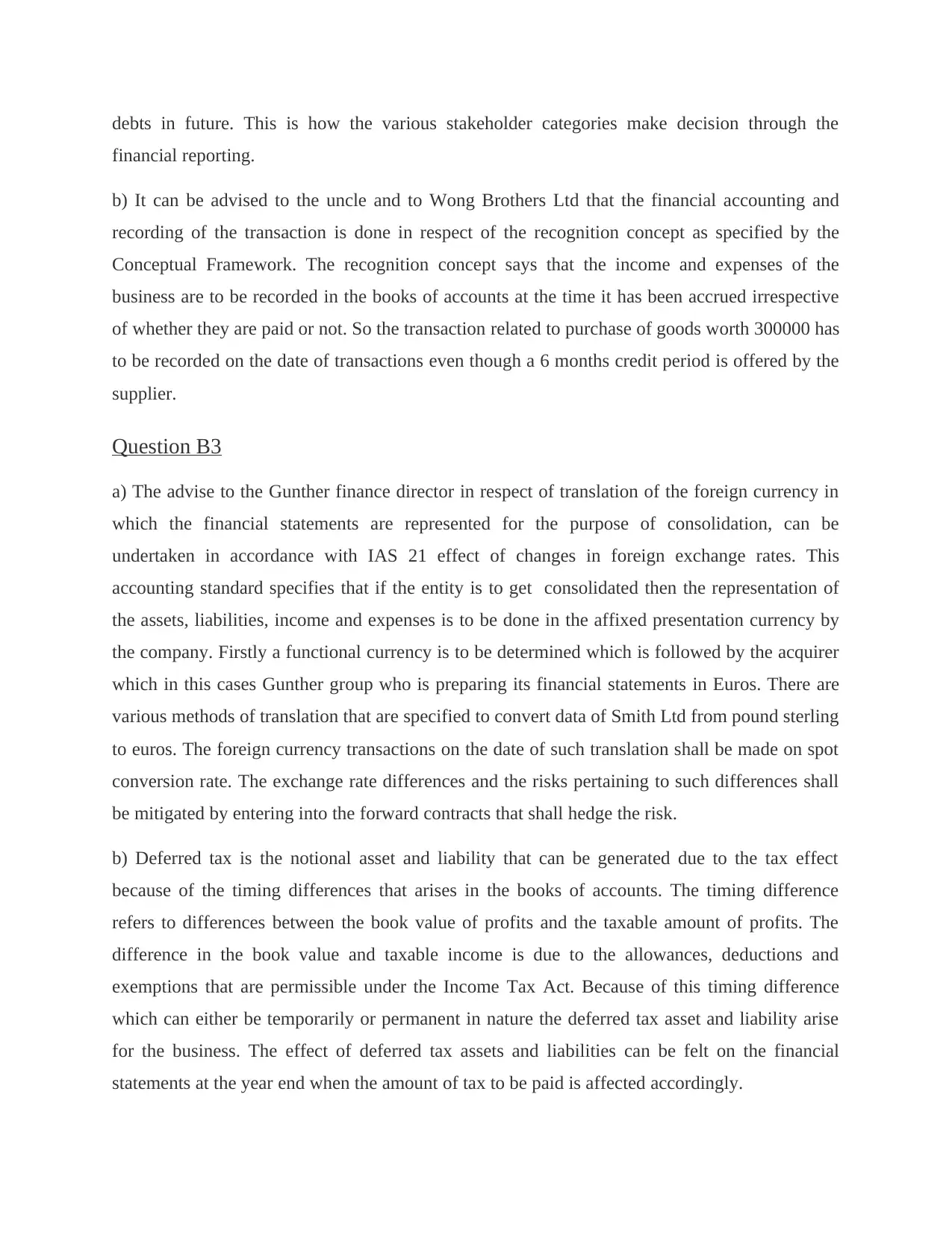

a) The advise to the Gunther finance director in respect of translation of the foreign currency in

which the financial statements are represented for the purpose of consolidation, can be

undertaken in accordance with IAS 21 effect of changes in foreign exchange rates. This

accounting standard specifies that if the entity is to get consolidated then the representation of

the assets, liabilities, income and expenses is to be done in the affixed presentation currency by

the company. Firstly a functional currency is to be determined which is followed by the acquirer

which in this cases Gunther group who is preparing its financial statements in Euros. There are

various methods of translation that are specified to convert data of Smith Ltd from pound sterling

to euros. The foreign currency transactions on the date of such translation shall be made on spot

conversion rate. The exchange rate differences and the risks pertaining to such differences shall

be mitigated by entering into the forward contracts that shall hedge the risk.

b) Deferred tax is the notional asset and liability that can be generated due to the tax effect

because of the timing differences that arises in the books of accounts. The timing difference

refers to differences between the book value of profits and the taxable amount of profits. The

difference in the book value and taxable income is due to the allowances, deductions and

exemptions that are permissible under the Income Tax Act. Because of this timing difference

which can either be temporarily or permanent in nature the deferred tax asset and liability arise

for the business. The effect of deferred tax assets and liabilities can be felt on the financial

statements at the year end when the amount of tax to be paid is affected accordingly.

financial reporting.

b) It can be advised to the uncle and to Wong Brothers Ltd that the financial accounting and

recording of the transaction is done in respect of the recognition concept as specified by the

Conceptual Framework. The recognition concept says that the income and expenses of the

business are to be recorded in the books of accounts at the time it has been accrued irrespective

of whether they are paid or not. So the transaction related to purchase of goods worth 300000 has

to be recorded on the date of transactions even though a 6 months credit period is offered by the

supplier.

Question B3

a) The advise to the Gunther finance director in respect of translation of the foreign currency in

which the financial statements are represented for the purpose of consolidation, can be

undertaken in accordance with IAS 21 effect of changes in foreign exchange rates. This

accounting standard specifies that if the entity is to get consolidated then the representation of

the assets, liabilities, income and expenses is to be done in the affixed presentation currency by

the company. Firstly a functional currency is to be determined which is followed by the acquirer

which in this cases Gunther group who is preparing its financial statements in Euros. There are

various methods of translation that are specified to convert data of Smith Ltd from pound sterling

to euros. The foreign currency transactions on the date of such translation shall be made on spot

conversion rate. The exchange rate differences and the risks pertaining to such differences shall

be mitigated by entering into the forward contracts that shall hedge the risk.

b) Deferred tax is the notional asset and liability that can be generated due to the tax effect

because of the timing differences that arises in the books of accounts. The timing difference

refers to differences between the book value of profits and the taxable amount of profits. The

difference in the book value and taxable income is due to the allowances, deductions and

exemptions that are permissible under the Income Tax Act. Because of this timing difference

which can either be temporarily or permanent in nature the deferred tax asset and liability arise

for the business. The effect of deferred tax assets and liabilities can be felt on the financial

statements at the year end when the amount of tax to be paid is affected accordingly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

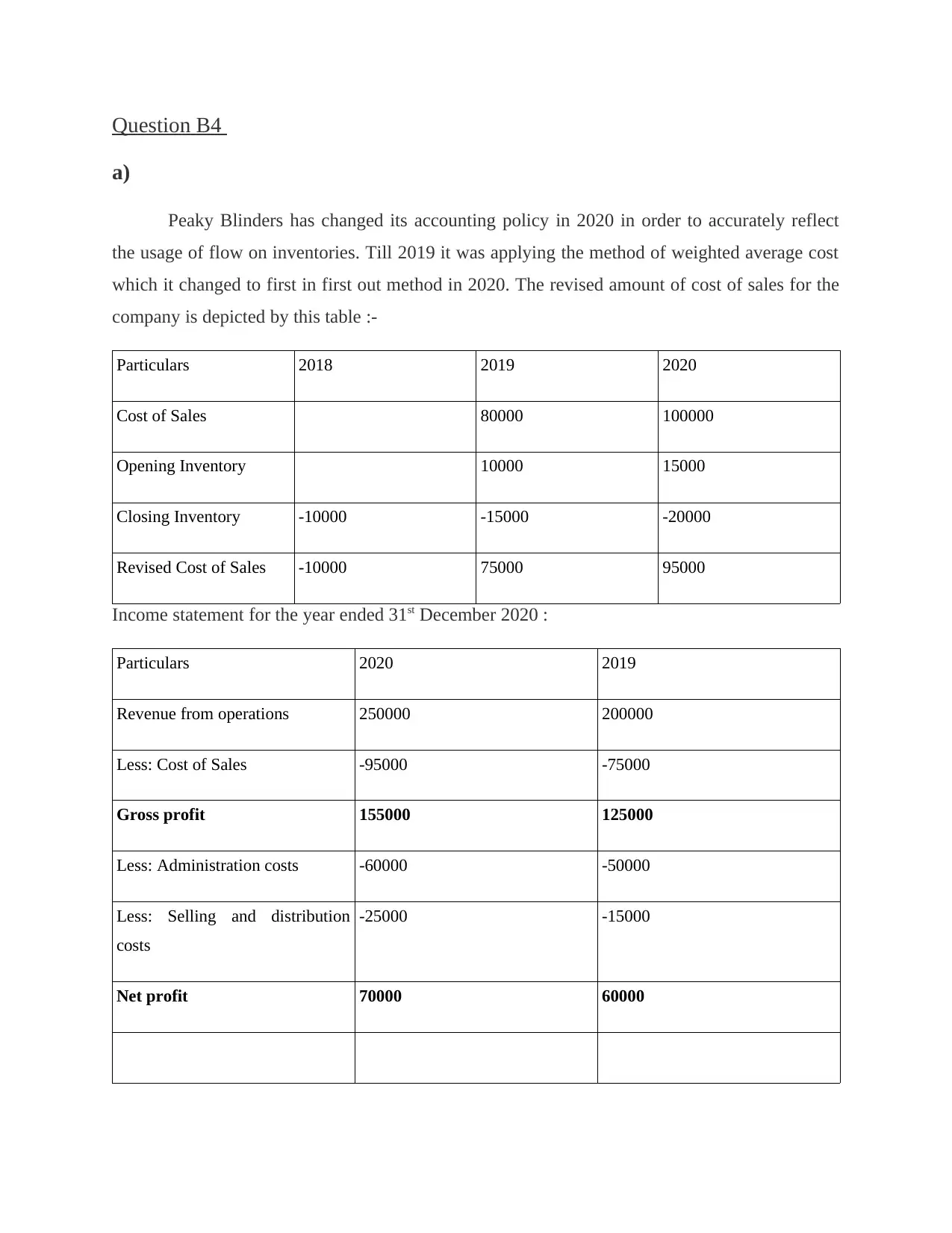

Question B4

a)

Peaky Blinders has changed its accounting policy in 2020 in order to accurately reflect

the usage of flow on inventories. Till 2019 it was applying the method of weighted average cost

which it changed to first in first out method in 2020. The revised amount of cost of sales for the

company is depicted by this table :-

Particulars 2018 2019 2020

Cost of Sales 80000 100000

Opening Inventory 10000 15000

Closing Inventory -10000 -15000 -20000

Revised Cost of Sales -10000 75000 95000

Income statement for the year ended 31st December 2020 :

Particulars 2020 2019

Revenue from operations 250000 200000

Less: Cost of Sales -95000 -75000

Gross profit 155000 125000

Less: Administration costs -60000 -50000

Less: Selling and distribution

costs

-25000 -15000

Net profit 70000 60000

a)

Peaky Blinders has changed its accounting policy in 2020 in order to accurately reflect

the usage of flow on inventories. Till 2019 it was applying the method of weighted average cost

which it changed to first in first out method in 2020. The revised amount of cost of sales for the

company is depicted by this table :-

Particulars 2018 2019 2020

Cost of Sales 80000 100000

Opening Inventory 10000 15000

Closing Inventory -10000 -15000 -20000

Revised Cost of Sales -10000 75000 95000

Income statement for the year ended 31st December 2020 :

Particulars 2020 2019

Revenue from operations 250000 200000

Less: Cost of Sales -95000 -75000

Gross profit 155000 125000

Less: Administration costs -60000 -50000

Less: Selling and distribution

costs

-25000 -15000

Net profit 70000 60000

The revised net profit for Peaky Blinders post the change of accounting policy from

weighted average cost to first in first out, its 70000 in 2020 and 60000 in 2019. This is due to the

revaluation of inventories that are possessed by the company.

b) Circumstances for change of accounting policy :-

The change in accounting policy can be viable if it is in order to enhance the relevance

and reliability of the financial statement pertaining to the organization.

It may be done as a result of change in the International Financial Reporting Standards

(Mongrut and Winkelried, 2019).

The change in the accounting policies of the company can be a voluntary decision by the

management in order to achieve better representation of the financial data or to facilitate

comparison

As per the IAS 8 the changes in accounting policy proper accounting treatment has to be

done in respect of the accounting policy that has been changed by the company. All the

correction of errors that have taken place with the change in the accounting policy are to be

retrospectively accounted for in the financial statements and the disclosures are to be made in

respect of it. Apart from that the accounting estimates are generally accounted for on prospective

basis.

For the new policy that is not addressed by IASB the management needs to make a

judgment and for that it has to consider the similar and related issues that are provided for in the

IASB standards. Apart from that the definition, recognition criteria and the measurement

concepts can be referred from the framework.

Question B5

a) As per the applicability of the IFRS and the IAS 24 which is associated with the related party

disclosures it can be assessed that some of the key disclosures are to be made by the company in

the preparation of its financial statements as these shall be helping the users to ascertain the

actual position of the company and its future growth prospects:-

weighted average cost to first in first out, its 70000 in 2020 and 60000 in 2019. This is due to the

revaluation of inventories that are possessed by the company.

b) Circumstances for change of accounting policy :-

The change in accounting policy can be viable if it is in order to enhance the relevance

and reliability of the financial statement pertaining to the organization.

It may be done as a result of change in the International Financial Reporting Standards

(Mongrut and Winkelried, 2019).

The change in the accounting policies of the company can be a voluntary decision by the

management in order to achieve better representation of the financial data or to facilitate

comparison

As per the IAS 8 the changes in accounting policy proper accounting treatment has to be

done in respect of the accounting policy that has been changed by the company. All the

correction of errors that have taken place with the change in the accounting policy are to be

retrospectively accounted for in the financial statements and the disclosures are to be made in

respect of it. Apart from that the accounting estimates are generally accounted for on prospective

basis.

For the new policy that is not addressed by IASB the management needs to make a

judgment and for that it has to consider the similar and related issues that are provided for in the

IASB standards. Apart from that the definition, recognition criteria and the measurement

concepts can be referred from the framework.

Question B5

a) As per the applicability of the IFRS and the IAS 24 which is associated with the related party

disclosures it can be assessed that some of the key disclosures are to be made by the company in

the preparation of its financial statements as these shall be helping the users to ascertain the

actual position of the company and its future growth prospects:-

The compensation and the remuneration that is paid to the chief executive officer is

considered to be the key management personnel and because of this reason the

disclosures in respect of annual salary, share based payments, contributions to the

retirement benefit plan and the reimbursements of his travel expenses.

The information as to the subsidiary and the controlling authority is to be specified in the

financial statements of the company. Ted Inc information is to be disclosed (Kieso,

Weygandt and Warfield, 2020).

Footnote:-

A sum of £2 million is paid to the chief executive officer in the form of annual salary.

Also the sum of £1 million is paid in the form of share based payments. An amount of £1

million is in the form of contributions to the retirement plan.

b) The major disclosure requirements under the IAS 24 are:-

The first and foremost disclosure is associated with the relationship of the parent and the

subsidiary company. It is mandatory for every entity to disclose the name of its parent

company or the controlling authority thereby indulged in producing the financial

statements to the public at large.

The next major disclosure is related to the compensation that is provided to the key

management personnel’s in the form of short term, long term, termination = and shared

employee benefits. The key management personnel of the company are the directors or

the executives who are playing major role in the planning and controlling the activities of

the business.

Lastly the disclosure in respect of the related party transactions of the entity, their

amounts, outstanding balances and the effect on the financial statements of the business.

This can be related to the debtors the amount of transactions in the particular financial

year, the sum pertaining to the bad and doubtful debts and the provisions made in respect

of bad and doubtful debts of the company.

considered to be the key management personnel and because of this reason the

disclosures in respect of annual salary, share based payments, contributions to the

retirement benefit plan and the reimbursements of his travel expenses.

The information as to the subsidiary and the controlling authority is to be specified in the

financial statements of the company. Ted Inc information is to be disclosed (Kieso,

Weygandt and Warfield, 2020).

Footnote:-

A sum of £2 million is paid to the chief executive officer in the form of annual salary.

Also the sum of £1 million is paid in the form of share based payments. An amount of £1

million is in the form of contributions to the retirement plan.

b) The major disclosure requirements under the IAS 24 are:-

The first and foremost disclosure is associated with the relationship of the parent and the

subsidiary company. It is mandatory for every entity to disclose the name of its parent

company or the controlling authority thereby indulged in producing the financial

statements to the public at large.

The next major disclosure is related to the compensation that is provided to the key

management personnel’s in the form of short term, long term, termination = and shared

employee benefits. The key management personnel of the company are the directors or

the executives who are playing major role in the planning and controlling the activities of

the business.

Lastly the disclosure in respect of the related party transactions of the entity, their

amounts, outstanding balances and the effect on the financial statements of the business.

This can be related to the debtors the amount of transactions in the particular financial

year, the sum pertaining to the bad and doubtful debts and the provisions made in respect

of bad and doubtful debts of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question B6

a) No, I do not agree with the following statement that IFRS Practice Statement- Management

commentary falls under the scope of International Financial Reporting Standards. Also, I

disagree that it is mandatory for the companies who have adopted the IFRS to comply with the

practice statement policy (HAMEEDI and et.al., 2021). As per what is prescribed by the

International Accounting Standards Board (IASB) and the IFRS foundation it can be assessed

that both the IFRS and the practice statements are separate which that the neither practice

statements can replace the IFRS nor the IFRS is equivalent to the practice statements of the

management. Entities have to mandatorily prepare its financial statements using IFRS but

consequently they are not necessarily required to comply with framing the practice statements

unless it is required by their own jurisdiction. The practice statement is just the historical

explanations that are provided by the management of the company to its stakeholders or users of

the financial information in relation to the elements that are included in the financial statement of

the organization.

b) Yes, I agree that there are similarities in the UK guidance on the strategic report and the

practice statements that are prepared for the management commentary. The major similarity is

that they are prepared for communicating the business performance in their perspective,

strategies, implementations, business model, profitability position and the developmental and

future growth prospects of the business. These both statements are not mandatorily framed but

are preferred by the management in order to facilitate the better communication to the users and

stakeholders who are interested in the financial statements. They are given the idea regarding the

financial health and well-being of the organization and on the basis of that the users shall be

formulating the investment decisions in respect of the organization under consideration.

a) No, I do not agree with the following statement that IFRS Practice Statement- Management

commentary falls under the scope of International Financial Reporting Standards. Also, I

disagree that it is mandatory for the companies who have adopted the IFRS to comply with the

practice statement policy (HAMEEDI and et.al., 2021). As per what is prescribed by the

International Accounting Standards Board (IASB) and the IFRS foundation it can be assessed

that both the IFRS and the practice statements are separate which that the neither practice

statements can replace the IFRS nor the IFRS is equivalent to the practice statements of the

management. Entities have to mandatorily prepare its financial statements using IFRS but

consequently they are not necessarily required to comply with framing the practice statements

unless it is required by their own jurisdiction. The practice statement is just the historical

explanations that are provided by the management of the company to its stakeholders or users of

the financial information in relation to the elements that are included in the financial statement of

the organization.

b) Yes, I agree that there are similarities in the UK guidance on the strategic report and the

practice statements that are prepared for the management commentary. The major similarity is

that they are prepared for communicating the business performance in their perspective,

strategies, implementations, business model, profitability position and the developmental and

future growth prospects of the business. These both statements are not mandatorily framed but

are preferred by the management in order to facilitate the better communication to the users and

stakeholders who are interested in the financial statements. They are given the idea regarding the

financial health and well-being of the organization and on the basis of that the users shall be

formulating the investment decisions in respect of the organization under consideration.

REFERENCES

HAMEEDI, K. S. and et.al., 2021. Financial Performance Reporting, IFRS Implementation, and

Accounting Information: Evidence from Iraqi Banking Sector. The Journal of Asian

Finance, Economics and Business. 8(3). pp.1083-1094.

HAMEEDI, K. S. and et.al., 2021. Financial Performance Reporting, IFRS Implementation, and

Accounting Information: Evidence from Iraqi Banking Sector. The Journal of Asian

Finance, Economics and Business. 8(3). pp.1083-1094.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2020. Intermediate accounting IFRS. John

Wiley & Sons.

Mongrut, S. and Winkelried, D., 2019. Unintended effects of IFRS adoption on earnings

management: The case of Latin America. Emerging Markets Review. 38. pp.377-388.

Akhmedjanov, K., 2019. ACCOUNTANCY REFORM AND PREREQUISITES FOR THE

PREPARING OF FINANCIAL STATEMENTS UNDER IFRS IN THE REPUBLIC

OF UZBEKISTAN. Theoretical & Applied Science. (7). pp.86-92.

Wiley & Sons.

Mongrut, S. and Winkelried, D., 2019. Unintended effects of IFRS adoption on earnings

management: The case of Latin America. Emerging Markets Review. 38. pp.377-388.

Akhmedjanov, K., 2019. ACCOUNTANCY REFORM AND PREREQUISITES FOR THE

PREPARING OF FINANCIAL STATEMENTS UNDER IFRS IN THE REPUBLIC

OF UZBEKISTAN. Theoretical & Applied Science. (7). pp.86-92.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.