Financial Reporting Exam Solution: Alpha Group and Firmino

VerifiedAdded on 2022/12/28

|10

|2152

|2

Homework Assignment

AI Summary

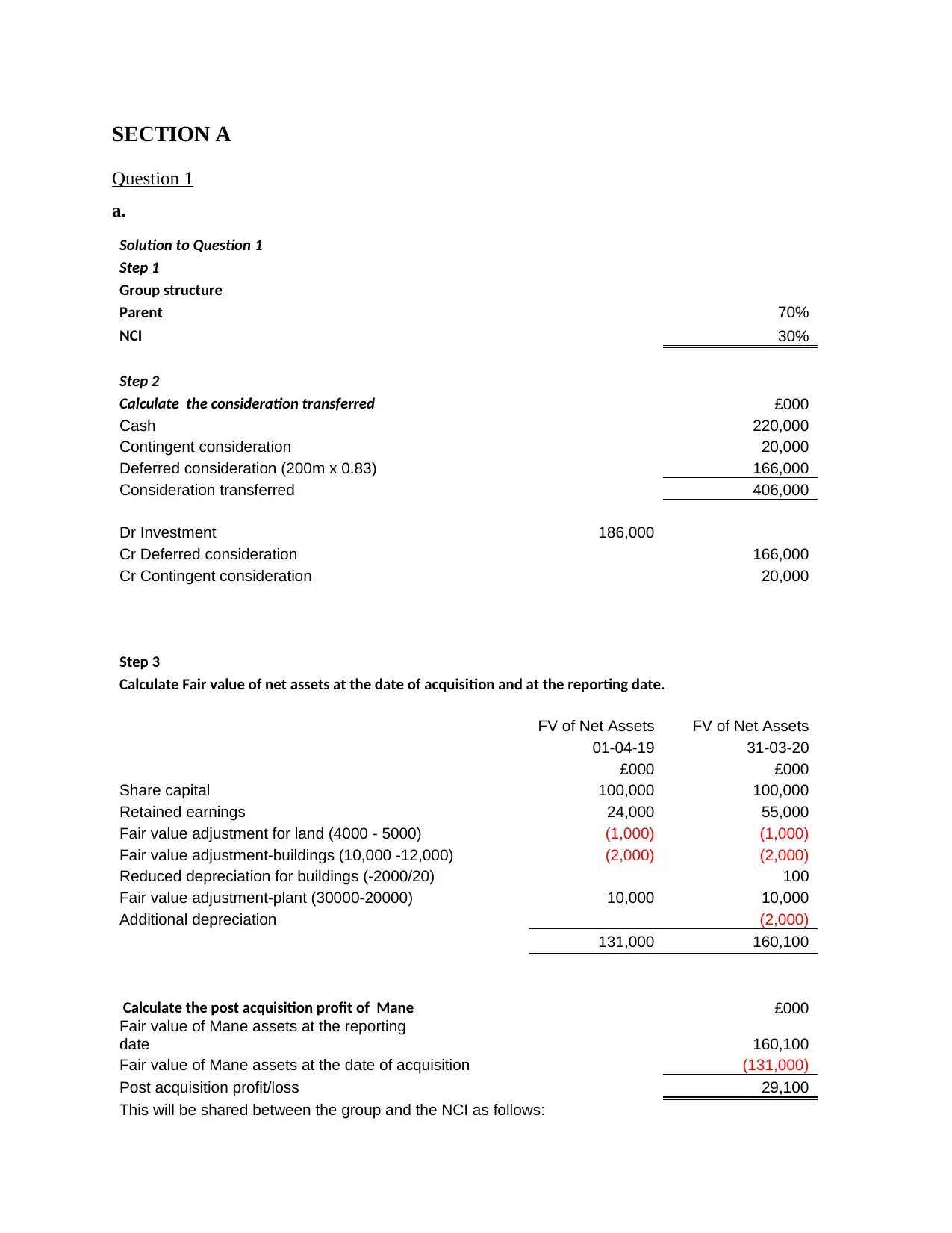

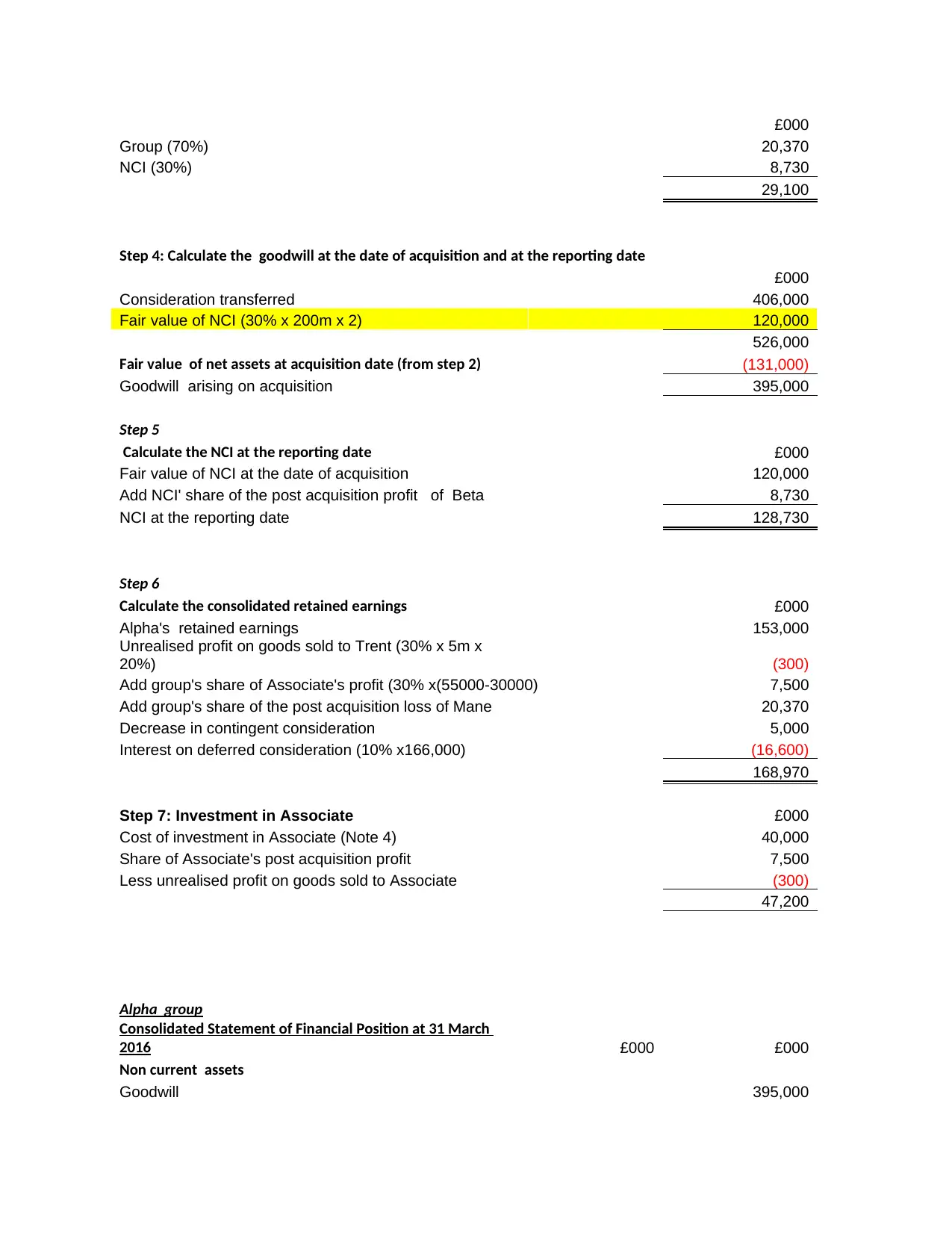

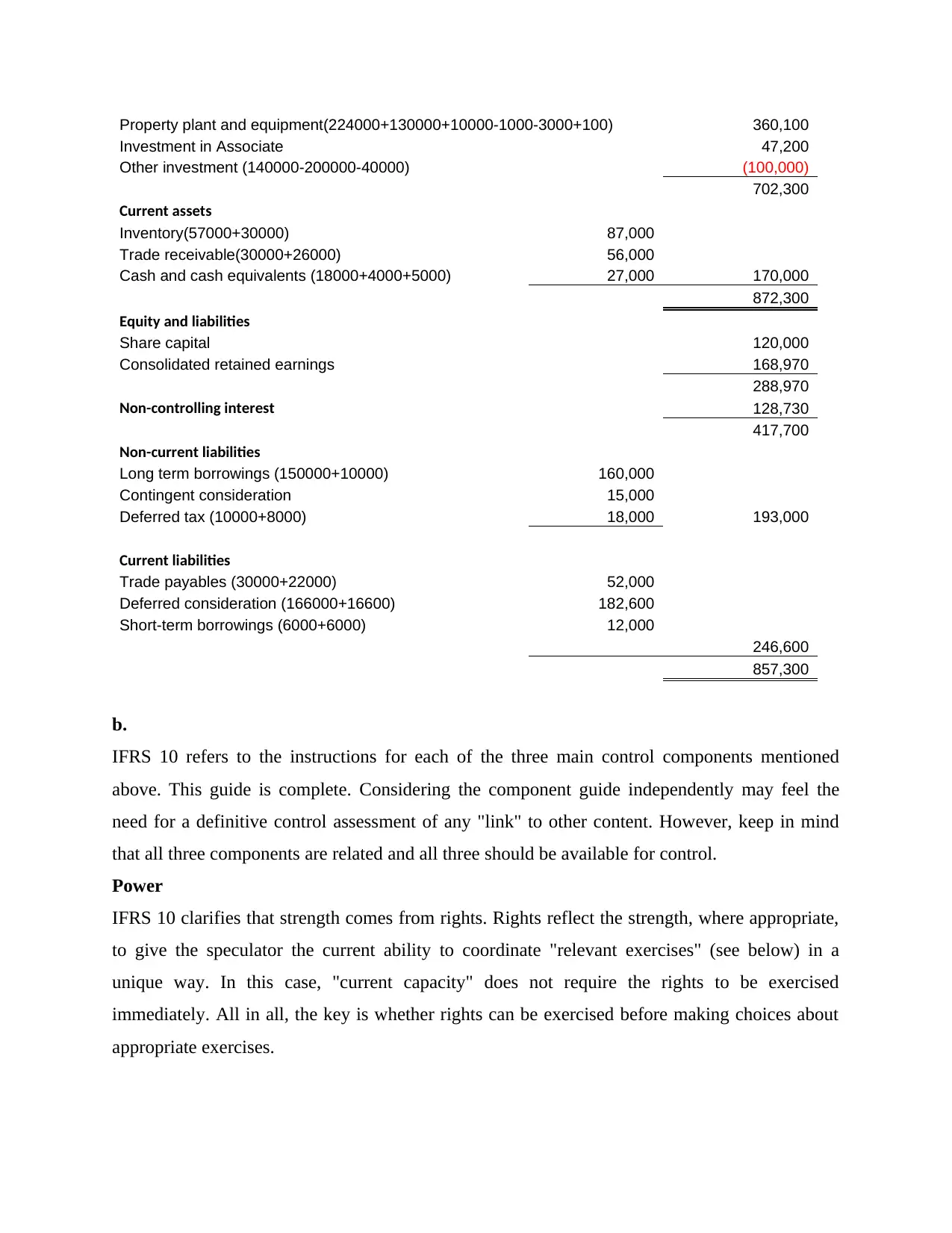

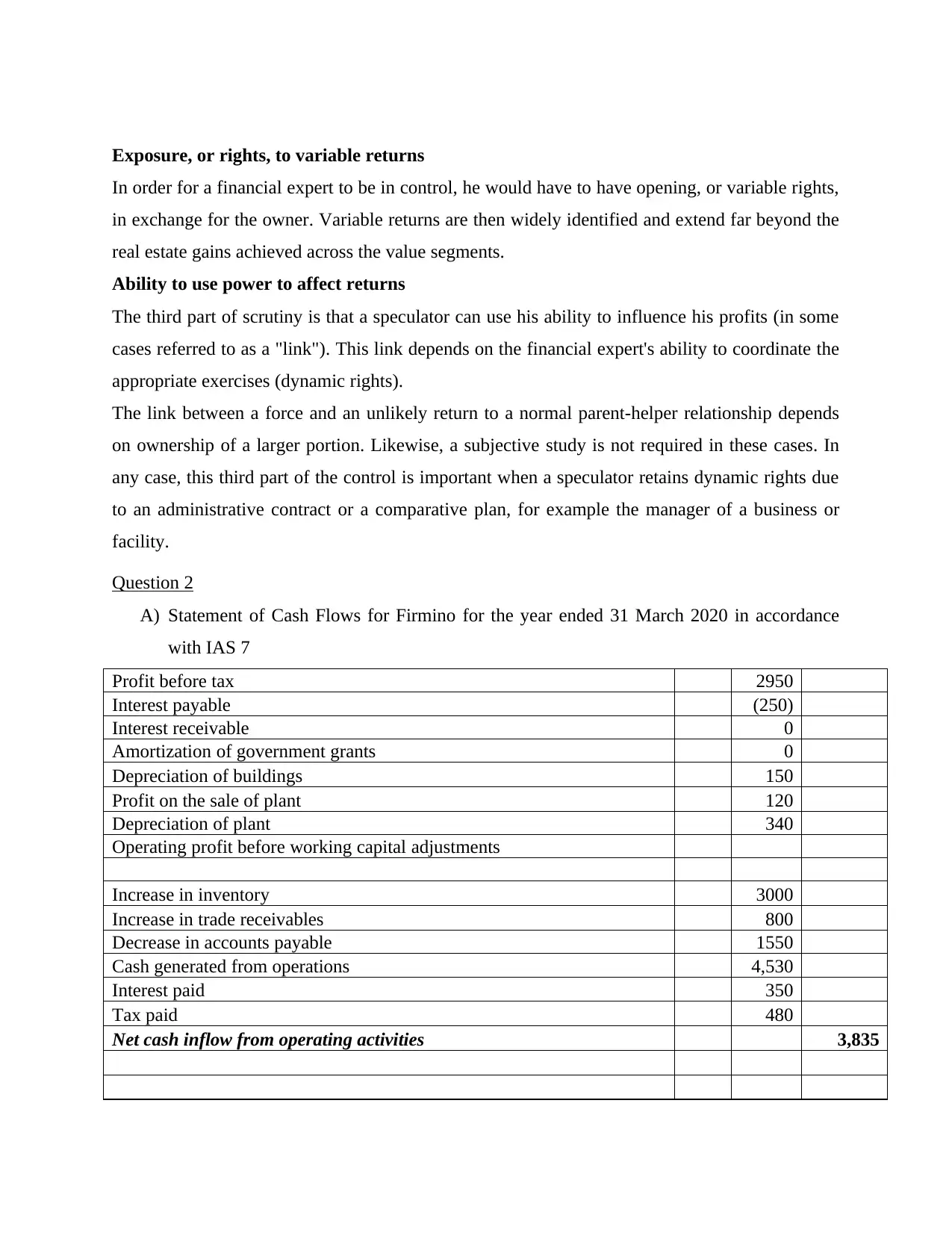

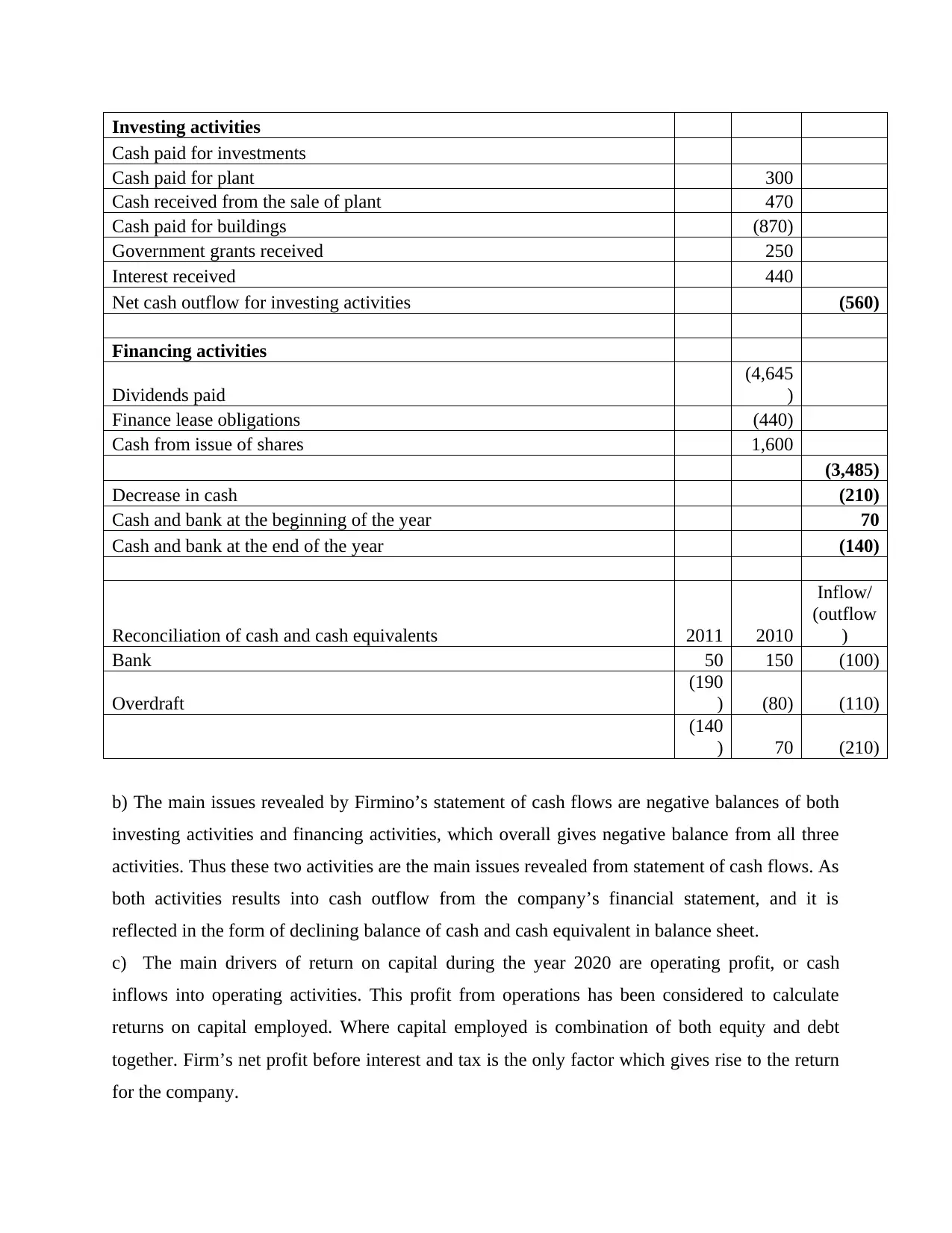

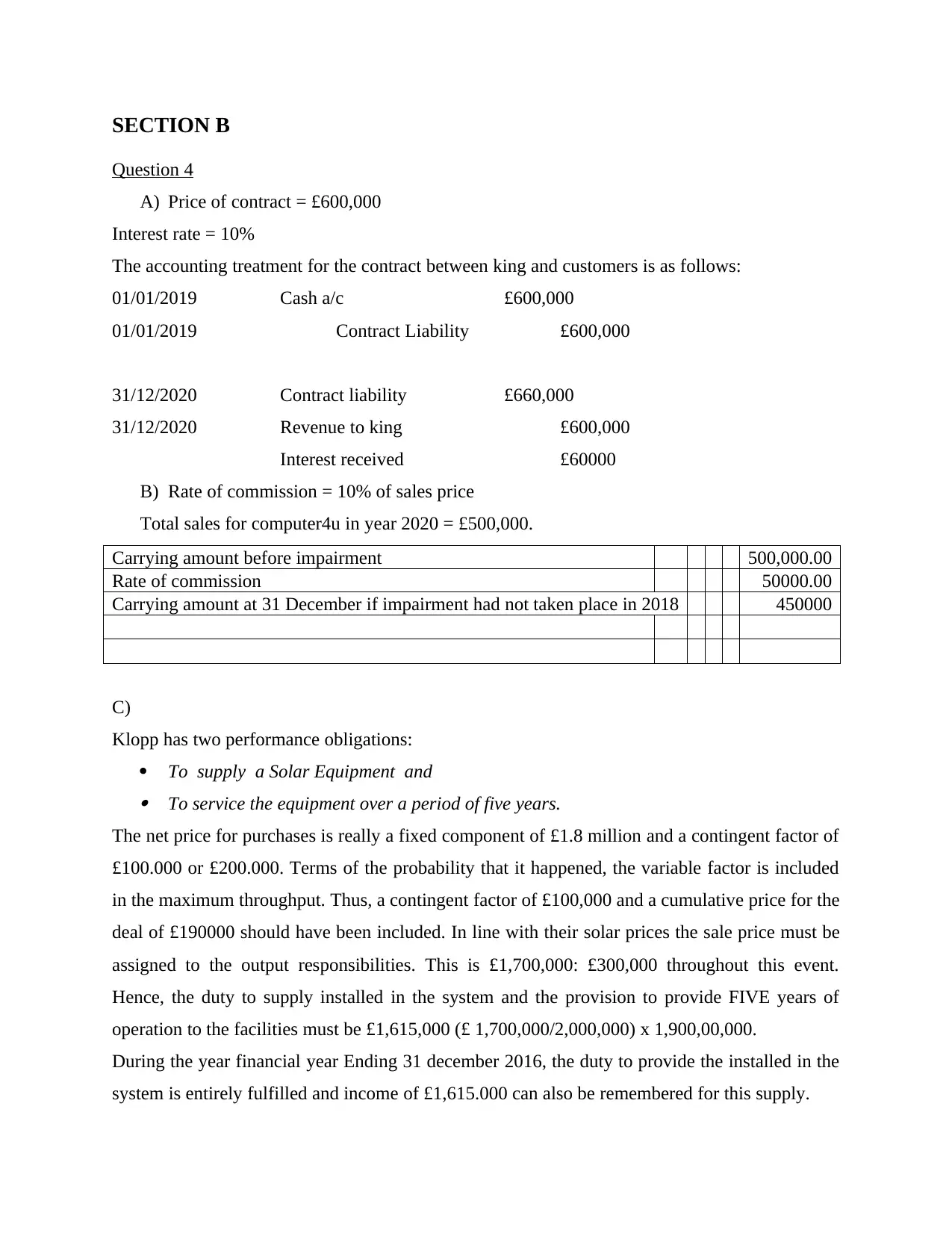

This document presents a detailed solution to a Financial Reporting exam, covering various aspects of financial accounting. Section A includes solutions to questions on group structure, consideration transferred, fair value of net assets, goodwill calculation, and non-controlling interest (NCI) at both acquisition and reporting dates. It also explains the accounting treatment for investment in associates, consolidated retained earnings, and provides a consolidated statement of financial position. Section B analyzes a statement of cash flows for Firmino, addressing negative balances in investing and financing activities and identifying the main drivers of return on capital. Further, the solution provides accounting treatments for contracts, commission calculations, and revenue recognition for performance obligations, along with advice on currency utilization and accounting for various transactions, including building depreciation and patent accounting. The solution is comprehensive and provides a detailed breakdown of each question, making it a useful resource for students studying financial reporting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.