Desklib: SEO Optimization for Online Library Study Material

VerifiedAdded on 2023/05/29

|9

|2311

|305

AI Summary

This text discusses various economic concepts such as income elasticity, efficient scale, perfect competition, monopoly markets, and monopolistic competition. It also explains how these concepts apply to different scenarios and provides examples to help readers understand them better.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

International Economics

International Economics

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Problem set 1- Income Elasticity

According to Andreyeva, Long and Brownell (2010) income elasticity of demand can be referred

as the sensitivity of quantity demanded for the goods and services based on certain changes in

income of the consumers. According to the problem set, the consumers at similar price but at

different income levels demand two different quantities of motel rooms. When the income level

is increased the consumers tend to demand more rooms at the existing prices compared to its

initial income level. Therefore, it is clear that at high-income levels individuals tend to demand

more goods at similar price. However, the law of demand is maintained even at high levels of

income, which can be observed by the fact that at higher prices of the motel rooms the

individuals are demanding fewer rooms even at higher income levels. The income elasticity of

demand at price 20$ = percentage change in demand of goods / percentage change in income of

the consumers.

Percentage change in demand = initial demand – present demand /initial demand +present

demand /2

Percentage change in demand = 24 -34/ 24+34/2

Percentage change in demand = -10/58/2

Percentage change in demand = -10/29

Percentage in income = initial income –present income / initial income + present income /2

Percent change in income = 50,000- 60,000/50,000 + 60,000/2

Percent change in income = -10,000/1,10,000/2

Percentage change in income = -10,000/55000

Income Elasticity of demand at price $20 = -10/29÷ -10,000/55,000

Income Elasticity of demand = -10/29 × 55,000/-10,000

Income Elasticity of demand = 18.96

Problem set 1- Income Elasticity

According to Andreyeva, Long and Brownell (2010) income elasticity of demand can be referred

as the sensitivity of quantity demanded for the goods and services based on certain changes in

income of the consumers. According to the problem set, the consumers at similar price but at

different income levels demand two different quantities of motel rooms. When the income level

is increased the consumers tend to demand more rooms at the existing prices compared to its

initial income level. Therefore, it is clear that at high-income levels individuals tend to demand

more goods at similar price. However, the law of demand is maintained even at high levels of

income, which can be observed by the fact that at higher prices of the motel rooms the

individuals are demanding fewer rooms even at higher income levels. The income elasticity of

demand at price 20$ = percentage change in demand of goods / percentage change in income of

the consumers.

Percentage change in demand = initial demand – present demand /initial demand +present

demand /2

Percentage change in demand = 24 -34/ 24+34/2

Percentage change in demand = -10/58/2

Percentage change in demand = -10/29

Percentage in income = initial income –present income / initial income + present income /2

Percent change in income = 50,000- 60,000/50,000 + 60,000/2

Percent change in income = -10,000/1,10,000/2

Percentage change in income = -10,000/55000

Income Elasticity of demand at price $20 = -10/29÷ -10,000/55,000

Income Elasticity of demand = -10/29 × 55,000/-10,000

Income Elasticity of demand = 18.96

3

The elasticity of the motel rooms when the price is $120 is also calculated using the midpoint

formula. That is percentage change in demand ÷ percentage change in income. Therefore,

Income elasticity of demand at $120= -10/9 ÷ -10,000/55,000

= 6.11

b) it can be observed from the above results that the income elasticity at both the prices are

positive. Therefore, it can be said that the goods are normal, as in case of normal goods the

consumers tend to buy more goods and services with an increase in their income (Bilbiie, 2009).

c) It can be observed that the income elasticity in both the case is positive and greater than one,

which indicates that rooms are a luxury goods for the consumers. In case of necessary goods the

income elasticity is normally between 0 and less than 1 (Papacharissi, 2010)

Problem set 2- Assessment of efficient scale

A firm is recognized as an efficient producer when it minimizes its variable costs in order to

produce the same amount of products and services. According to the case provided the total cost

is given as TC = 588+3q2 , where 588 depicts the fixed cost and 3q2 depicts the variable cost

with q considered as the individual unit production.

a) The average fixed cost can be calculated by dividing the total fixed cost with the number

of units produced by the firm. In this case the average fixed cost is = 588/q+3q. The

average variable cost is also calculated by diving the total variable cost by the number of

units produced by the firms. Therefore, the AVC = 3q. The marginal cost can be found by

differentiating the total cost function that is d/dq of 588+3q2 = 1+ 6q

b) According to Bikker, Shaffer and Spierdijk (2012) the average total cost curves are u

shaped in nature because with the increase in production levels the cost levels tends to

fall down and economies of scale is generated in the industry. The greater the units

produced the lower is the cost incurred for the firm. Therefore, when q is maximum the

average total cost is minimum.

c) Efficient scale of production is the situation when the firm is producing maximum

quantities with minimum costs. The condition of efficient production can take place when

the firm is increasing the number of produced goods at their existing cost.

The elasticity of the motel rooms when the price is $120 is also calculated using the midpoint

formula. That is percentage change in demand ÷ percentage change in income. Therefore,

Income elasticity of demand at $120= -10/9 ÷ -10,000/55,000

= 6.11

b) it can be observed from the above results that the income elasticity at both the prices are

positive. Therefore, it can be said that the goods are normal, as in case of normal goods the

consumers tend to buy more goods and services with an increase in their income (Bilbiie, 2009).

c) It can be observed that the income elasticity in both the case is positive and greater than one,

which indicates that rooms are a luxury goods for the consumers. In case of necessary goods the

income elasticity is normally between 0 and less than 1 (Papacharissi, 2010)

Problem set 2- Assessment of efficient scale

A firm is recognized as an efficient producer when it minimizes its variable costs in order to

produce the same amount of products and services. According to the case provided the total cost

is given as TC = 588+3q2 , where 588 depicts the fixed cost and 3q2 depicts the variable cost

with q considered as the individual unit production.

a) The average fixed cost can be calculated by dividing the total fixed cost with the number

of units produced by the firm. In this case the average fixed cost is = 588/q+3q. The

average variable cost is also calculated by diving the total variable cost by the number of

units produced by the firms. Therefore, the AVC = 3q. The marginal cost can be found by

differentiating the total cost function that is d/dq of 588+3q2 = 1+ 6q

b) According to Bikker, Shaffer and Spierdijk (2012) the average total cost curves are u

shaped in nature because with the increase in production levels the cost levels tends to

fall down and economies of scale is generated in the industry. The greater the units

produced the lower is the cost incurred for the firm. Therefore, when q is maximum the

average total cost is minimum.

c) Efficient scale of production is the situation when the firm is producing maximum

quantities with minimum costs. The condition of efficient production can take place when

the firm is increasing the number of produced goods at their existing cost.

4

Problem set 3- supply with perfect competition

1) In perfect competition, the price is always considered the marginal cost of producing the

goods. Therefore, in the short run when the number of firms is fixed the producers tend to

supply the quantity of output so that the marginal cost becomes equal to the price charged

from the consumers. When the price is equal to the marginal costs the producers tend to

earn profits as the price is above the total variable cost and equal to the marginal cost. In

this case, the cost curve acts as the supply curve for the fixed number of firms.

2) Equilibrium price and quantity are the set of price and quantity that are obtained in the

market when the buyer and sellers mutually agree to make a transaction by maximizing

their own utility. Therefore, when the price quoted by the seller maximizes the utility of

the consumer and vice versa, the price is said to be an equilibrium price where both party

gets benefited by the transaction. In this case, the equilibrium price and quantity can be

obtained when the market demand curve is equal to the market supply curve. Further, it is

already stated that the market supply curve is equal to the cost curve. Therefore, when the

supply curve is equated with the demand curve the equilibrium quantity and price is

ascertained. The demand function given as Q= 500-2P and the supply function would be

equal to the marginal cost of the firms operating in the market. That is C = 1 +6q. Now in

this case of equilibrium demand is equal to supply. Therefore, it can be written that

P=MC. The average price is considered as the demand curve in equilibrium condition.

For finding the price the demand function can be used Q = 500-2P

2P = Q+500

P = Q/2 +250

MC = 1+6q

If P=MC is applied then

Q/2+250 = 1+6q

Q/2-6q = 1-250

-5q = -498

Q = 99.6

If the value of q is substituted in the demand function we get the equilibrium price. That

is P = 99/2 + 250

P = 299.5

Problem set 3- supply with perfect competition

1) In perfect competition, the price is always considered the marginal cost of producing the

goods. Therefore, in the short run when the number of firms is fixed the producers tend to

supply the quantity of output so that the marginal cost becomes equal to the price charged

from the consumers. When the price is equal to the marginal costs the producers tend to

earn profits as the price is above the total variable cost and equal to the marginal cost. In

this case, the cost curve acts as the supply curve for the fixed number of firms.

2) Equilibrium price and quantity are the set of price and quantity that are obtained in the

market when the buyer and sellers mutually agree to make a transaction by maximizing

their own utility. Therefore, when the price quoted by the seller maximizes the utility of

the consumer and vice versa, the price is said to be an equilibrium price where both party

gets benefited by the transaction. In this case, the equilibrium price and quantity can be

obtained when the market demand curve is equal to the market supply curve. Further, it is

already stated that the market supply curve is equal to the cost curve. Therefore, when the

supply curve is equated with the demand curve the equilibrium quantity and price is

ascertained. The demand function given as Q= 500-2P and the supply function would be

equal to the marginal cost of the firms operating in the market. That is C = 1 +6q. Now in

this case of equilibrium demand is equal to supply. Therefore, it can be written that

P=MC. The average price is considered as the demand curve in equilibrium condition.

For finding the price the demand function can be used Q = 500-2P

2P = Q+500

P = Q/2 +250

MC = 1+6q

If P=MC is applied then

Q/2+250 = 1+6q

Q/2-6q = 1-250

-5q = -498

Q = 99.6

If the value of q is substituted in the demand function we get the equilibrium price. That

is P = 99/2 + 250

P = 299.5

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

3) According to Weimer and Vining (2017) consumer surplus is the situation when the

consumers are actually paying less than they are prepared to pay for any goods or

services. On the other hand, producer surplus is the situation where producers are gaining

maximum profit from the price at which they are actually supplying than to a lower price

at which they would have supplied in the market. In case of market equilibrium the

consumer and producer is gaining surplus and is benefitted the most from the transaction.

The amount of surplus is illustrated with a simple diagram

The diagram depicts both the consumer and producer surplus and it can be easily

understood that in case of equilibrium, the consumer is gaining a surplus of the area ABP

and the producer is gaining a surplus of PBE.

Problem set 4- supply with monopoly markets

a) The profit maximizing quantity of the monopolist is determined by two measures of the

market they are marginal revenue and marginal cost. When the marginal revenue is equal

to marginal cost the monopolist tend to make profits, below the marginal cost the

monopolist will make loss hence it is advisable not to operate below the marginal cost. In

order to attain the profit maximizing output the condition used in monopoly market is

MR =MC. In order to get the marginal revenue we double the slope of the demand curve

MR = 360/2-Q

MC = 1 + 4q

3) According to Weimer and Vining (2017) consumer surplus is the situation when the

consumers are actually paying less than they are prepared to pay for any goods or

services. On the other hand, producer surplus is the situation where producers are gaining

maximum profit from the price at which they are actually supplying than to a lower price

at which they would have supplied in the market. In case of market equilibrium the

consumer and producer is gaining surplus and is benefitted the most from the transaction.

The amount of surplus is illustrated with a simple diagram

The diagram depicts both the consumer and producer surplus and it can be easily

understood that in case of equilibrium, the consumer is gaining a surplus of the area ABP

and the producer is gaining a surplus of PBE.

Problem set 4- supply with monopoly markets

a) The profit maximizing quantity of the monopolist is determined by two measures of the

market they are marginal revenue and marginal cost. When the marginal revenue is equal

to marginal cost the monopolist tend to make profits, below the marginal cost the

monopolist will make loss hence it is advisable not to operate below the marginal cost. In

order to attain the profit maximizing output the condition used in monopoly market is

MR =MC. In order to get the marginal revenue we double the slope of the demand curve

MR = 360/2-Q

MC = 1 + 4q

6

MR =MC

360/2 – Q = 1 + 4Q

Q = 35

Now if the value of q is substituted in he inverse demand function we get the price charged by

the monopolist.

2P = 360- 35

P = 162

Solving the above equation, we get the profit maximizing quantity of the monopolist. Moreover,

the price charged by the monopolist in the market is always above the marginal cost and the

average cost but the monopolist in general try to take the highest price the consumers agrees to

pay. In the perfect competitive market the price charged from the consumers is always equal to

the marginal revenue which is again equal to the marginal cost P=MR=MC. In case of monopoly

markets, the price is always greater than the marginal revenue and marginal cost. That is P>MR

=MC (Jensen, 2010). The profit level that is being obtained by the monopolist is the

b) The economic profit of the monopolist can be measured by taking a difference between

the price charged by the monopolist minus the average total cost. In this case the price

charged by the monopolist is 162 and the average total cost is 141. Therefore, the

economic profit is around 21.

c) In case of the monopoly market their occurs deadweight loss which not beneficial either

for the consumer and the producer. The deadweight loss depicts a social welfare loss for

the economy. Both the measures that is consumer surplus and producer surplus is

decreased in a imperfect competition market or in monopoly market. The following

diagram depicts the deadweight loss

MR =MC

360/2 – Q = 1 + 4Q

Q = 35

Now if the value of q is substituted in he inverse demand function we get the price charged by

the monopolist.

2P = 360- 35

P = 162

Solving the above equation, we get the profit maximizing quantity of the monopolist. Moreover,

the price charged by the monopolist in the market is always above the marginal cost and the

average cost but the monopolist in general try to take the highest price the consumers agrees to

pay. In the perfect competitive market the price charged from the consumers is always equal to

the marginal revenue which is again equal to the marginal cost P=MR=MC. In case of monopoly

markets, the price is always greater than the marginal revenue and marginal cost. That is P>MR

=MC (Jensen, 2010). The profit level that is being obtained by the monopolist is the

b) The economic profit of the monopolist can be measured by taking a difference between

the price charged by the monopolist minus the average total cost. In this case the price

charged by the monopolist is 162 and the average total cost is 141. Therefore, the

economic profit is around 21.

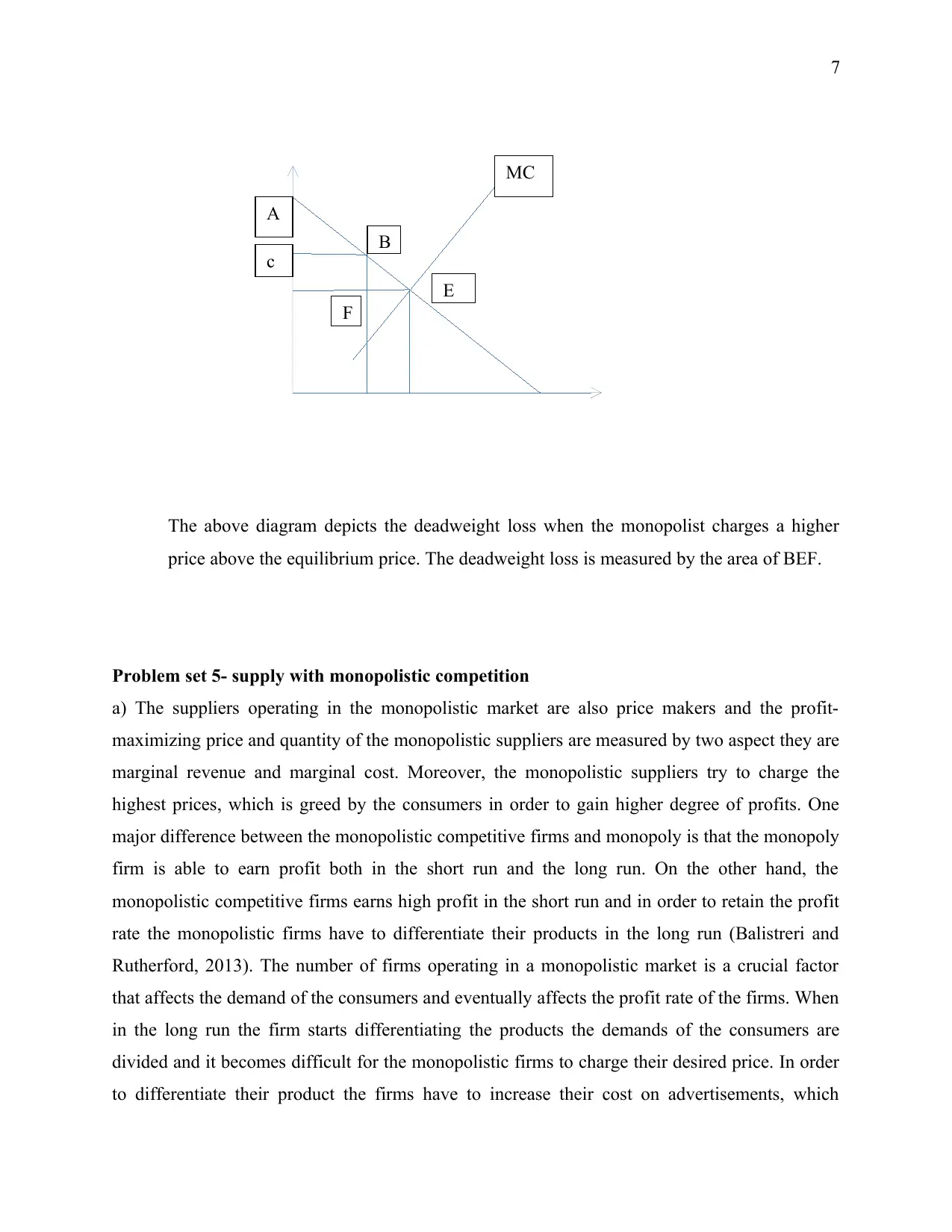

c) In case of the monopoly market their occurs deadweight loss which not beneficial either

for the consumer and the producer. The deadweight loss depicts a social welfare loss for

the economy. Both the measures that is consumer surplus and producer surplus is

decreased in a imperfect competition market or in monopoly market. The following

diagram depicts the deadweight loss

A

B

c

E

F

MC

7

The above diagram depicts the deadweight loss when the monopolist charges a higher

price above the equilibrium price. The deadweight loss is measured by the area of BEF.

Problem set 5- supply with monopolistic competition

a) The suppliers operating in the monopolistic market are also price makers and the profit-

maximizing price and quantity of the monopolistic suppliers are measured by two aspect they are

marginal revenue and marginal cost. Moreover, the monopolistic suppliers try to charge the

highest prices, which is greed by the consumers in order to gain higher degree of profits. One

major difference between the monopolistic competitive firms and monopoly is that the monopoly

firm is able to earn profit both in the short run and the long run. On the other hand, the

monopolistic competitive firms earns high profit in the short run and in order to retain the profit

rate the monopolistic firms have to differentiate their products in the long run (Balistreri and

Rutherford, 2013). The number of firms operating in a monopolistic market is a crucial factor

that affects the demand of the consumers and eventually affects the profit rate of the firms. When

in the long run the firm starts differentiating the products the demands of the consumers are

divided and it becomes difficult for the monopolistic firms to charge their desired price. In order

to differentiate their product the firms have to increase their cost on advertisements, which

B

c

E

F

MC

7

The above diagram depicts the deadweight loss when the monopolist charges a higher

price above the equilibrium price. The deadweight loss is measured by the area of BEF.

Problem set 5- supply with monopolistic competition

a) The suppliers operating in the monopolistic market are also price makers and the profit-

maximizing price and quantity of the monopolistic suppliers are measured by two aspect they are

marginal revenue and marginal cost. Moreover, the monopolistic suppliers try to charge the

highest prices, which is greed by the consumers in order to gain higher degree of profits. One

major difference between the monopolistic competitive firms and monopoly is that the monopoly

firm is able to earn profit both in the short run and the long run. On the other hand, the

monopolistic competitive firms earns high profit in the short run and in order to retain the profit

rate the monopolistic firms have to differentiate their products in the long run (Balistreri and

Rutherford, 2013). The number of firms operating in a monopolistic market is a crucial factor

that affects the demand of the consumers and eventually affects the profit rate of the firms. When

in the long run the firm starts differentiating the products the demands of the consumers are

divided and it becomes difficult for the monopolistic firms to charge their desired price. In order

to differentiate their product the firms have to increase their cost on advertisements, which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

further increases the cost of the firms and reduces the profit rate. Therefore, there are two major

effects for the firms that are they are producing surplus goods for the market and secondly, the

firms are not able to earn high profit rate and only survives in the break-even point.

b) As it is already discussed that the number of firms influences the profit rate in monopolistic

competitive firms. Therefore, the number of units produced by a single monopolistic firm will

depend on the N that I number of firms. If there are large, number of firms then in the long run

each firm have to produce more goods compared to the short run.

c) In the long run those firms will exist who will be able to compete with each other after

breaking even in the market. The firms that are able to absorb the breakeven point and produce

more differentiated goods will exist and other firm will stop operating in the market.

further increases the cost of the firms and reduces the profit rate. Therefore, there are two major

effects for the firms that are they are producing surplus goods for the market and secondly, the

firms are not able to earn high profit rate and only survives in the break-even point.

b) As it is already discussed that the number of firms influences the profit rate in monopolistic

competitive firms. Therefore, the number of units produced by a single monopolistic firm will

depend on the N that I number of firms. If there are large, number of firms then in the long run

each firm have to produce more goods compared to the short run.

c) In the long run those firms will exist who will be able to compete with each other after

breaking even in the market. The firms that are able to absorb the breakeven point and produce

more differentiated goods will exist and other firm will stop operating in the market.

9

References

Andreyeva, T., Long, M.W. and Brownell, K.D., 2010. The impact of food prices on

consumption: a systematic review of research on the price elasticity of demand for

food. American journal of public health, 100(2), pp.216-222.

Bilbiie, F.O., 2009. Nonseparable preferences, fiscal policy puzzles, and inferior goods. Journal

of Money, Credit and Banking, 41(2 3), pp.443-450.‐

Papacharissi, Z., 2010. Privacy as a luxury commodity. First Monday, 15(8), pp. 56-67.

Bikker, J.A., Shaffer, S. and Spierdijk, L., 2012. Assessing competition with the Panzar-Rosse

model: The role of scale, costs, and equilibrium. Review of Economics and Statistics, 94(4),

pp.1025-1044.

Weimer, D.L. and Vining, A.R., 2017. Policy analysis: Concepts and practice. 7th ed. Abingdon:

Routledge.

Balistreri, E.J. and Rutherford, T.F., 2013. Computing general equilibrium theories of

monopolistic competition and heterogeneous firms. 7th ed. London: Elsevier.

Jensen, M.C., 2010. Value maximization, stakeholder theory, and the corporate objective

function. Journal of applied corporate finance, 22(1), pp.32-42.

References

Andreyeva, T., Long, M.W. and Brownell, K.D., 2010. The impact of food prices on

consumption: a systematic review of research on the price elasticity of demand for

food. American journal of public health, 100(2), pp.216-222.

Bilbiie, F.O., 2009. Nonseparable preferences, fiscal policy puzzles, and inferior goods. Journal

of Money, Credit and Banking, 41(2 3), pp.443-450.‐

Papacharissi, Z., 2010. Privacy as a luxury commodity. First Monday, 15(8), pp. 56-67.

Bikker, J.A., Shaffer, S. and Spierdijk, L., 2012. Assessing competition with the Panzar-Rosse

model: The role of scale, costs, and equilibrium. Review of Economics and Statistics, 94(4),

pp.1025-1044.

Weimer, D.L. and Vining, A.R., 2017. Policy analysis: Concepts and practice. 7th ed. Abingdon:

Routledge.

Balistreri, E.J. and Rutherford, T.F., 2013. Computing general equilibrium theories of

monopolistic competition and heterogeneous firms. 7th ed. London: Elsevier.

Jensen, M.C., 2010. Value maximization, stakeholder theory, and the corporate objective

function. Journal of applied corporate finance, 22(1), pp.32-42.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.