University Assignment: Accounting, Finance, Investment and Taxation

VerifiedAdded on 2023/06/13

|15

|3018

|376

Homework Assignment

AI Summary

This assignment solution delves into various aspects of accounting and finance, starting with the calculation of present value for an investment opportunity involving future cash flows. It then addresses the computation of quarterly loan payments using the annuity formula and determines monthly payments from an investment's future value. The solution further analyzes the impact of the Australian government's corporate tax rate reduction on foreign investment and domestic shareholders, considering dividend imputation. Finally, it examines the monthly and annual returns of NAB, BHP, and AORD stocks, calculates standard deviation, beta, expected return, and plots the security market line to analyze investment risk and return. Desklib offers a wide array of such solved assignments and past papers to aid students in their academic pursuits.

Running head: ACCOUNTING AND FINANCE

Accounting and finance

Name of the University

Author Note

Accounting and finance

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................3

Part c:.....................................................................................................................................4

Answer to Question 2:................................................................................................................5

Part i:......................................................................................................................................5

Part ii:.....................................................................................................................................5

Answer to question 3:.................................................................................................................6

Answer to Question 4:................................................................................................................8

Part i:......................................................................................................................................8

Part ii:.....................................................................................................................................8

Part iii:....................................................................................................................................9

Part iv:..................................................................................................................................10

Part v:...................................................................................................................................10

Part vi:..................................................................................................................................10

Part vii:.................................................................................................................................11

Part viii:................................................................................................................................11

Part ix:..................................................................................................................................11

References list:.........................................................................................................................13

ACCOUNTING AND FINANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................3

Part c:.....................................................................................................................................4

Answer to Question 2:................................................................................................................5

Part i:......................................................................................................................................5

Part ii:.....................................................................................................................................5

Answer to question 3:.................................................................................................................6

Answer to Question 4:................................................................................................................8

Part i:......................................................................................................................................8

Part ii:.....................................................................................................................................8

Part iii:....................................................................................................................................9

Part iv:..................................................................................................................................10

Part v:...................................................................................................................................10

Part vi:..................................................................................................................................10

Part vii:.................................................................................................................................11

Part viii:................................................................................................................................11

Part ix:..................................................................................................................................11

References list:.........................................................................................................................13

2

ACCOUNTING AND FINANCE

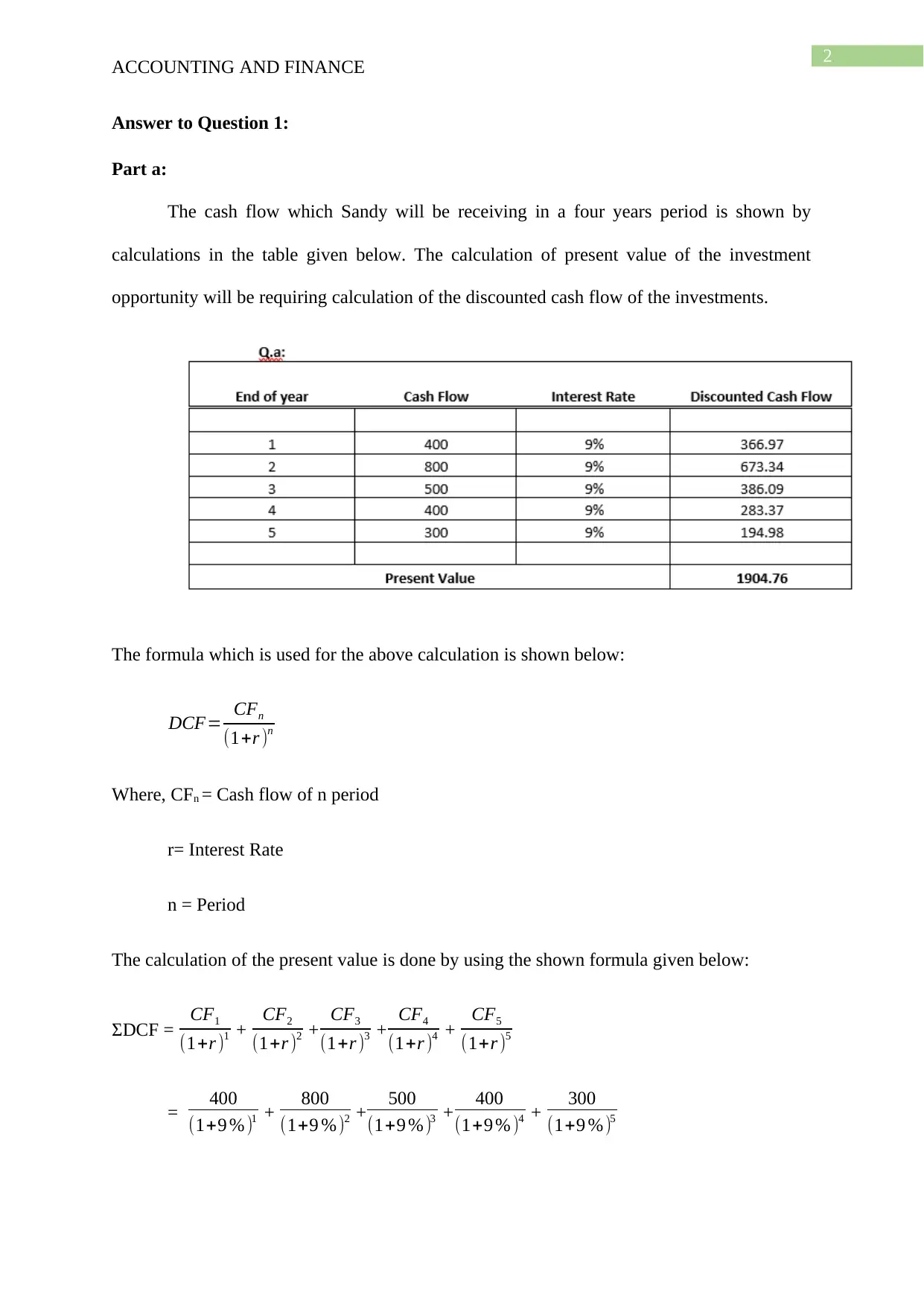

Answer to Question 1:

Part a:

The cash flow which Sandy will be receiving in a four years period is shown by

calculations in the table given below. The calculation of present value of the investment

opportunity will be requiring calculation of the discounted cash flow of the investments.

The formula which is used for the above calculation is shown below:

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

The calculation of the present value is done by using the shown formula given below:

ΣDCF = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 400

(1+9 % )1 + 800

(1+9 %)2 + 500

(1+9 % )3 + 400

(1+9 % )4 + 300

(1+9 % )5

ACCOUNTING AND FINANCE

Answer to Question 1:

Part a:

The cash flow which Sandy will be receiving in a four years period is shown by

calculations in the table given below. The calculation of present value of the investment

opportunity will be requiring calculation of the discounted cash flow of the investments.

The formula which is used for the above calculation is shown below:

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

The calculation of the present value is done by using the shown formula given below:

ΣDCF = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 400

(1+9 % )1 + 800

(1+9 %)2 + 500

(1+9 % )3 + 400

(1+9 % )4 + 300

(1+9 % )5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING AND FINANCE

= 400

1.09 + 800

1.188 + 500

1.295 + 400

1.412 + 300

1.539

= 366.97+673.34 +386.09+283.37+194.98

= 1904.76

As per the above calculations, it can be confirmed that Sandy has to pay $1,904.76 for

the investment opportunity to earn the desired cash flow.

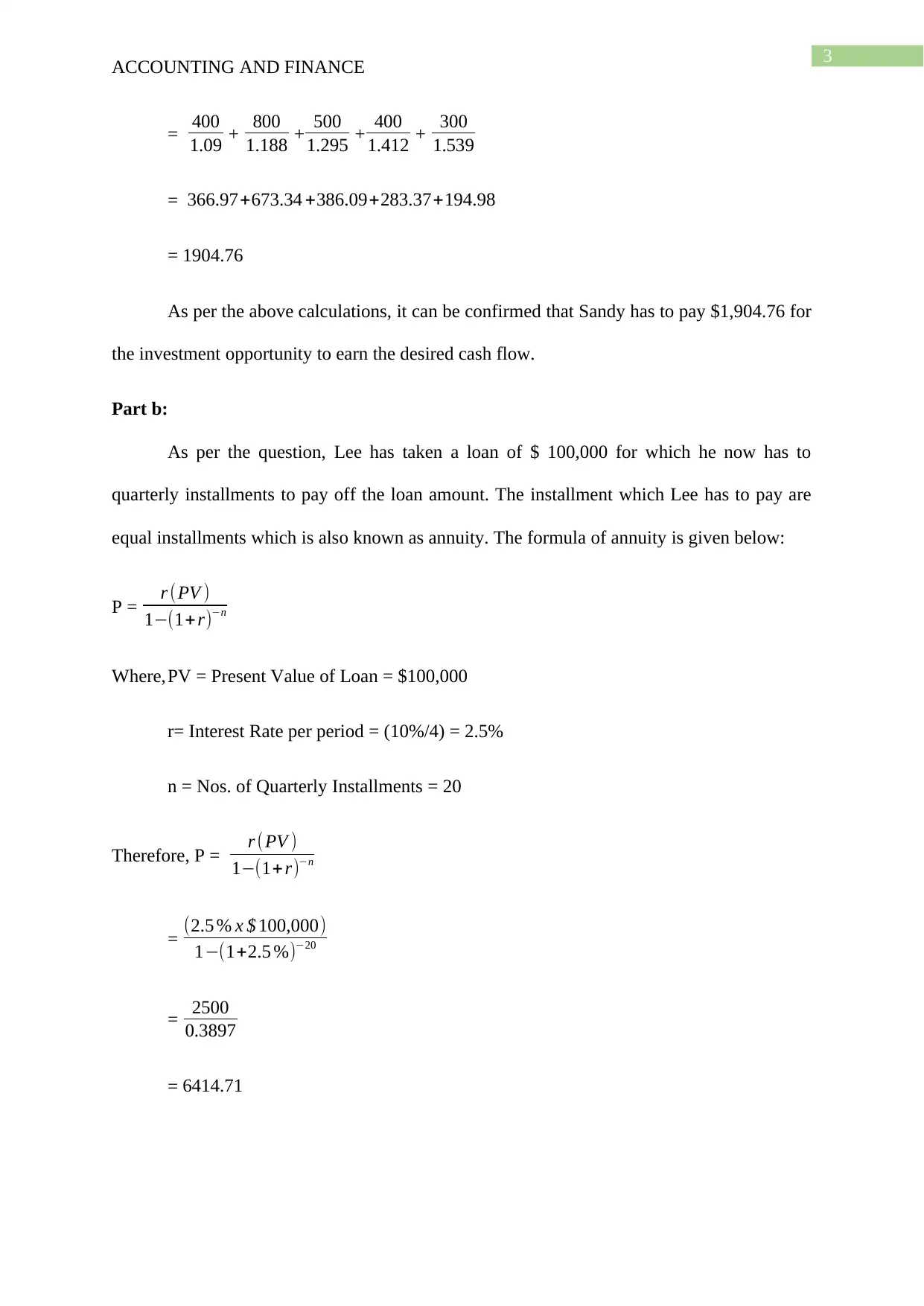

Part b:

As per the question, Lee has taken a loan of $ 100,000 for which he now has to

quarterly installments to pay off the loan amount. The installment which Lee has to pay are

equal installments which is also known as annuity. The formula of annuity is given below:

P = r (PV )

1−(1+r)−n

Where,PV = Present Value of Loan = $100,000

r= Interest Rate per period = (10%/4) = 2.5%

n = Nos. of Quarterly Installments = 20

Therefore, P = r (PV )

1−(1+ r)−n

= (2.5 % x $ 100,000)

1−(1+2.5 %)−20

= 2500

0.3897

= 6414.71

ACCOUNTING AND FINANCE

= 400

1.09 + 800

1.188 + 500

1.295 + 400

1.412 + 300

1.539

= 366.97+673.34 +386.09+283.37+194.98

= 1904.76

As per the above calculations, it can be confirmed that Sandy has to pay $1,904.76 for

the investment opportunity to earn the desired cash flow.

Part b:

As per the question, Lee has taken a loan of $ 100,000 for which he now has to

quarterly installments to pay off the loan amount. The installment which Lee has to pay are

equal installments which is also known as annuity. The formula of annuity is given below:

P = r (PV )

1−(1+r)−n

Where,PV = Present Value of Loan = $100,000

r= Interest Rate per period = (10%/4) = 2.5%

n = Nos. of Quarterly Installments = 20

Therefore, P = r (PV )

1−(1+ r)−n

= (2.5 % x $ 100,000)

1−(1+2.5 %)−20

= 2500

0.3897

= 6414.71

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING AND FINANCE

As per the calculations which is shown above, the quarterly payment of Lee will

amount to $ 6,414.71. The table which shows the calculation is given below:

Part c:

Dianne would receive the monthly payments after two years of investment. The

investment value for the next two year needs to be calculated. The future value of the

investment can be computed by using the following formula:

FV = PV x (1+r )n

Where, PV = Present value of investment = $200,000

r= Interest Rate per compounding periods = (10%/12 months) = 0.83%

n = Nos. of Compounding Periods = (2 yrs. X12 months) = 24

Hence, FV = 200,000 x (1+ 0.83 %)24

= 200,000 x 1.220391

= 2,44,078.19

The amount Dianne would be receiving through 150 equal monthly installments is

$2,44,078.19. The formula used for calculating the monthly payments is as follows:

ACCOUNTING AND FINANCE

As per the calculations which is shown above, the quarterly payment of Lee will

amount to $ 6,414.71. The table which shows the calculation is given below:

Part c:

Dianne would receive the monthly payments after two years of investment. The

investment value for the next two year needs to be calculated. The future value of the

investment can be computed by using the following formula:

FV = PV x (1+r )n

Where, PV = Present value of investment = $200,000

r= Interest Rate per compounding periods = (10%/12 months) = 0.83%

n = Nos. of Compounding Periods = (2 yrs. X12 months) = 24

Hence, FV = 200,000 x (1+ 0.83 %)24

= 200,000 x 1.220391

= 2,44,078.19

The amount Dianne would be receiving through 150 equal monthly installments is

$2,44,078.19. The formula used for calculating the monthly payments is as follows:

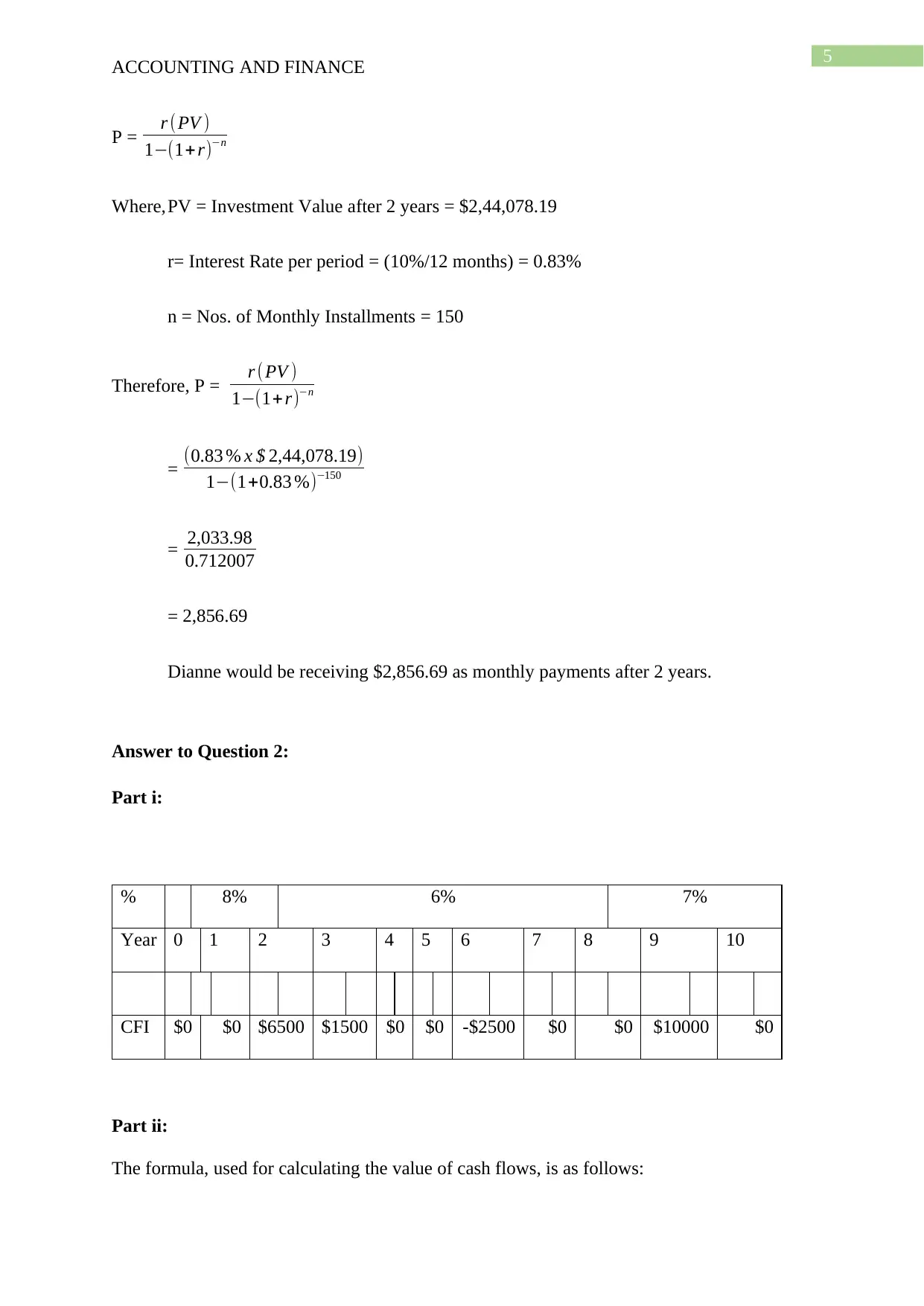

5

ACCOUNTING AND FINANCE

P = r (PV )

1−(1+r)−n

Where,PV = Investment Value after 2 years = $2,44,078.19

r= Interest Rate per period = (10%/12 months) = 0.83%

n = Nos. of Monthly Installments = 150

Therefore, P = r (PV )

1−(1+ r)−n

= (0.83 % x $ 2,44,078.19)

1−(1+0.83 %)−150

= 2,033.98

0.712007

= 2,856.69

Dianne would be receiving $2,856.69 as monthly payments after 2 years.

Answer to Question 2:

Part i:

% 8% 6% 7%

Year 0 1 2 3 4 5 6 7 8 9 10

CFI $0 $0 $6500 $1500 $0 $0 -$2500 $0 $0 $10000 $0

Part ii:

The formula, used for calculating the value of cash flows, is as follows:

ACCOUNTING AND FINANCE

P = r (PV )

1−(1+r)−n

Where,PV = Investment Value after 2 years = $2,44,078.19

r= Interest Rate per period = (10%/12 months) = 0.83%

n = Nos. of Monthly Installments = 150

Therefore, P = r (PV )

1−(1+ r)−n

= (0.83 % x $ 2,44,078.19)

1−(1+0.83 %)−150

= 2,033.98

0.712007

= 2,856.69

Dianne would be receiving $2,856.69 as monthly payments after 2 years.

Answer to Question 2:

Part i:

% 8% 6% 7%

Year 0 1 2 3 4 5 6 7 8 9 10

CFI $0 $0 $6500 $1500 $0 $0 -$2500 $0 $0 $10000 $0

Part ii:

The formula, used for calculating the value of cash flows, is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

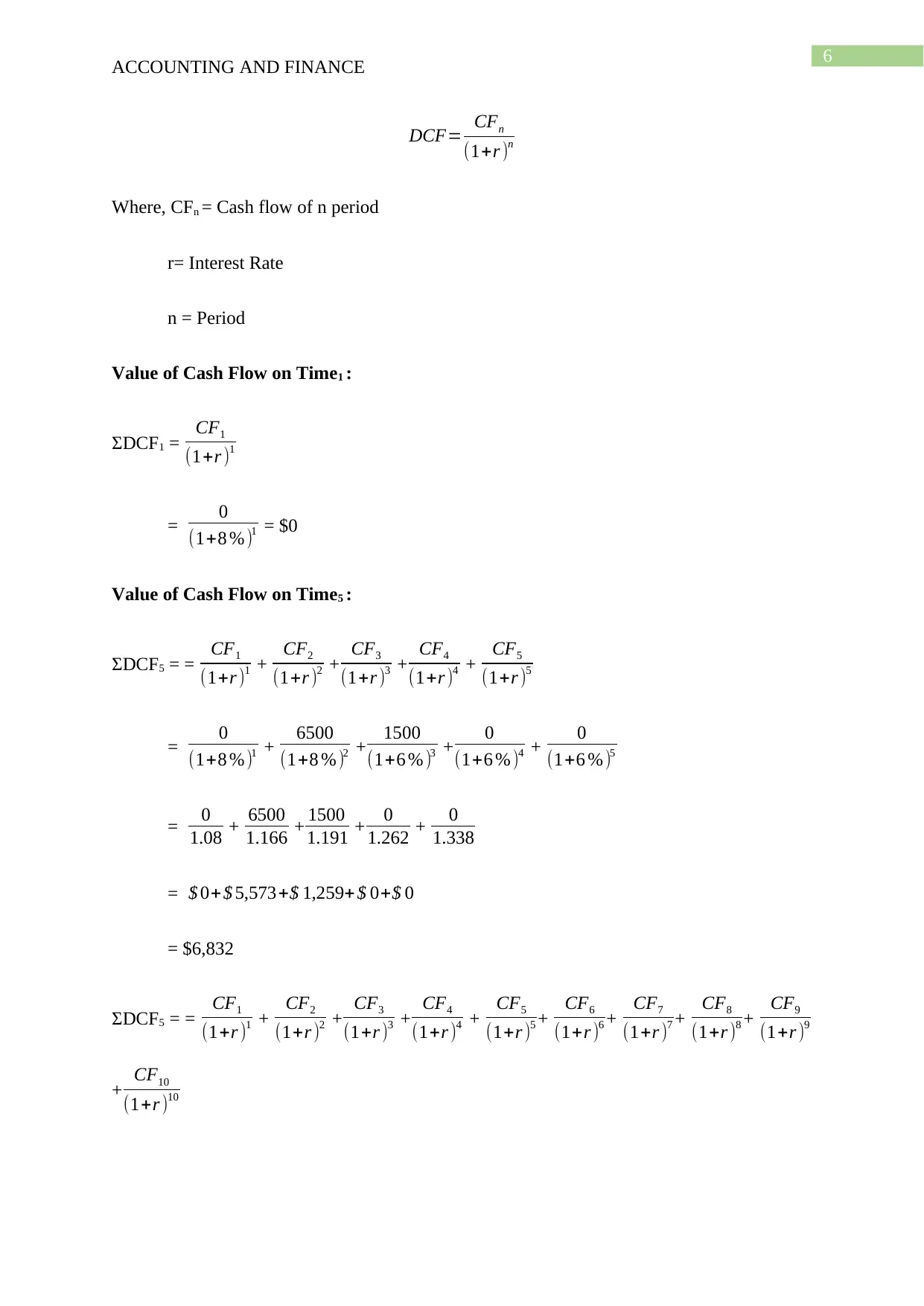

ACCOUNTING AND FINANCE

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

Value of Cash Flow on Time1 :

ΣDCF1 = CF1

(1+r )1

= 0

(1+8 % )1 = $0

Value of Cash Flow on Time5 :

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 0

(1+8 % )1 + 6500

(1+8 % )2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 % )5

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338

= $ 0+$ 5,573+$ 1,259+ $ 0+$ 0

= $6,832

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5 + CF6

(1+r )6 + CF7

(1+r )7 + CF8

(1+r )8 + CF9

(1+r )9

+ CF10

(1+r )10

ACCOUNTING AND FINANCE

DCF= CFn

(1+r )n

Where, CFn = Cash flow of n period

r= Interest Rate

n = Period

Value of Cash Flow on Time1 :

ΣDCF1 = CF1

(1+r )1

= 0

(1+8 % )1 = $0

Value of Cash Flow on Time5 :

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5

= 0

(1+8 % )1 + 6500

(1+8 % )2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 % )5

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338

= $ 0+$ 5,573+$ 1,259+ $ 0+$ 0

= $6,832

ΣDCF5 = = CF1

(1+r )1 + CF2

(1+r )2 + CF3

(1+r )3 + CF4

(1+r )4 + CF5

(1+r )5 + CF6

(1+r )6 + CF7

(1+r )7 + CF8

(1+r )8 + CF9

(1+r )9

+ CF10

(1+r )10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

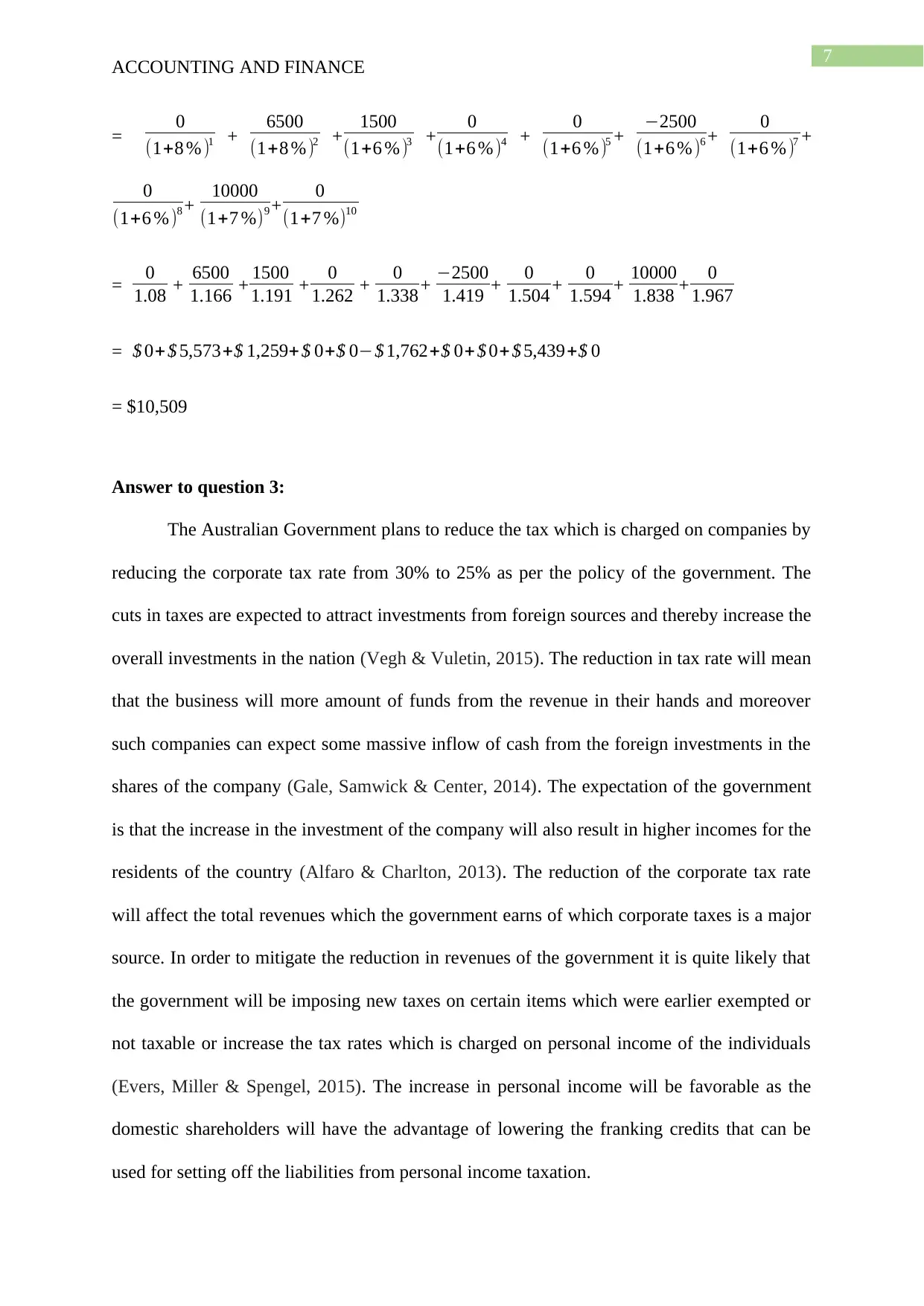

ACCOUNTING AND FINANCE

= 0

(1+8 % )1 + 6500

(1+8 % )2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 % )5 + −2500

(1+6 % )6 + 0

(1+6 % )7 +

0

(1+6 %)8 + 10000

(1+7 %)9 + 0

(1+7 %)10

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338+ −2500

1.419 + 0

1.504 + 0

1.594 + 10000

1.838 + 0

1.967

= $ 0+ $ 5,573+$ 1,259+$ 0+$ 0−$ 1,762+$ 0+ $ 0+ $ 5,439+$ 0

= $10,509

Answer to question 3:

The Australian Government plans to reduce the tax which is charged on companies by

reducing the corporate tax rate from 30% to 25% as per the policy of the government. The

cuts in taxes are expected to attract investments from foreign sources and thereby increase the

overall investments in the nation (Vegh & Vuletin, 2015). The reduction in tax rate will mean

that the business will more amount of funds from the revenue in their hands and moreover

such companies can expect some massive inflow of cash from the foreign investments in the

shares of the company (Gale, Samwick & Center, 2014). The expectation of the government

is that the increase in the investment of the company will also result in higher incomes for the

residents of the country (Alfaro & Charlton, 2013). The reduction of the corporate tax rate

will affect the total revenues which the government earns of which corporate taxes is a major

source. In order to mitigate the reduction in revenues of the government it is quite likely that

the government will be imposing new taxes on certain items which were earlier exempted or

not taxable or increase the tax rates which is charged on personal income of the individuals

(Evers, Miller & Spengel, 2015). The increase in personal income will be favorable as the

domestic shareholders will have the advantage of lowering the franking credits that can be

used for setting off the liabilities from personal income taxation.

ACCOUNTING AND FINANCE

= 0

(1+8 % )1 + 6500

(1+8 % )2 + 1500

(1+6 % )3 + 0

(1+6 % )4 + 0

(1+6 % )5 + −2500

(1+6 % )6 + 0

(1+6 % )7 +

0

(1+6 %)8 + 10000

(1+7 %)9 + 0

(1+7 %)10

= 0

1.08 + 6500

1.166 + 1500

1.191 + 0

1.262 + 0

1.338+ −2500

1.419 + 0

1.504 + 0

1.594 + 10000

1.838 + 0

1.967

= $ 0+ $ 5,573+$ 1,259+$ 0+$ 0−$ 1,762+$ 0+ $ 0+ $ 5,439+$ 0

= $10,509

Answer to question 3:

The Australian Government plans to reduce the tax which is charged on companies by

reducing the corporate tax rate from 30% to 25% as per the policy of the government. The

cuts in taxes are expected to attract investments from foreign sources and thereby increase the

overall investments in the nation (Vegh & Vuletin, 2015). The reduction in tax rate will mean

that the business will more amount of funds from the revenue in their hands and moreover

such companies can expect some massive inflow of cash from the foreign investments in the

shares of the company (Gale, Samwick & Center, 2014). The expectation of the government

is that the increase in the investment of the company will also result in higher incomes for the

residents of the country (Alfaro & Charlton, 2013). The reduction of the corporate tax rate

will affect the total revenues which the government earns of which corporate taxes is a major

source. In order to mitigate the reduction in revenues of the government it is quite likely that

the government will be imposing new taxes on certain items which were earlier exempted or

not taxable or increase the tax rates which is charged on personal income of the individuals

(Evers, Miller & Spengel, 2015). The increase in personal income will be favorable as the

domestic shareholders will have the advantage of lowering the franking credits that can be

used for setting off the liabilities from personal income taxation.

8

ACCOUNTING AND FINANCE

The system of Australia allows the residents with a unique system of Dividend

imputation which helps in effectively reducing the tax rate as it provides the domestic

companies with an opportunity of franking credits which means if the company is paying

higher taxes then the investors do not have pay such high taxes (Siau, Sault & Warren, 2015).

Dividend imputation is basically a method which can help the residents in acquiring some tax

payer’s credits for tax that is deemed to have been paid on behalf of company. Dividends are

attached to the franking credits are the actual mechanisms for making delivery of tax credits

to residents (Vo et al., 2013). Therefore, the impact of tax reduction on the economy of

Australia is quite different in comparison with other countries (Dixon & Nassios, 2016).

However, the main advantages lie with the foreign investors as the tax reduction will attract

new investors in the Australian market. The lower tax rates will also facilitate higher returns

on the investments made by foreign investors which will keep them engaged in further

investments in the country (Bergmann, 2016). Moreover, there is also an advantage of

lowering the tax rate from the view point of global markets as it is said that higher tax rates

discourage potential investors of global markets.

Another significant advantage associated with the lowering of tax rate is that the as

the tax expenses of a company which is regraded as a normal cost reduces, the overall cost of

production will also decrease and therefore the companies will be able to provide the

products manufactured at a lower cost to the residents. The residents will have access to

products at a lower which will reduce their consumption expenditure and thereby allowing

them to make savings. In other words, it will be providing the residents of the country with

better standard of living and also lead to overall development of the country as a whole.

ACCOUNTING AND FINANCE

The system of Australia allows the residents with a unique system of Dividend

imputation which helps in effectively reducing the tax rate as it provides the domestic

companies with an opportunity of franking credits which means if the company is paying

higher taxes then the investors do not have pay such high taxes (Siau, Sault & Warren, 2015).

Dividend imputation is basically a method which can help the residents in acquiring some tax

payer’s credits for tax that is deemed to have been paid on behalf of company. Dividends are

attached to the franking credits are the actual mechanisms for making delivery of tax credits

to residents (Vo et al., 2013). Therefore, the impact of tax reduction on the economy of

Australia is quite different in comparison with other countries (Dixon & Nassios, 2016).

However, the main advantages lie with the foreign investors as the tax reduction will attract

new investors in the Australian market. The lower tax rates will also facilitate higher returns

on the investments made by foreign investors which will keep them engaged in further

investments in the country (Bergmann, 2016). Moreover, there is also an advantage of

lowering the tax rate from the view point of global markets as it is said that higher tax rates

discourage potential investors of global markets.

Another significant advantage associated with the lowering of tax rate is that the as

the tax expenses of a company which is regraded as a normal cost reduces, the overall cost of

production will also decrease and therefore the companies will be able to provide the

products manufactured at a lower cost to the residents. The residents will have access to

products at a lower which will reduce their consumption expenditure and thereby allowing

them to make savings. In other words, it will be providing the residents of the country with

better standard of living and also lead to overall development of the country as a whole.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING AND FINANCE

Answer to Question 4:

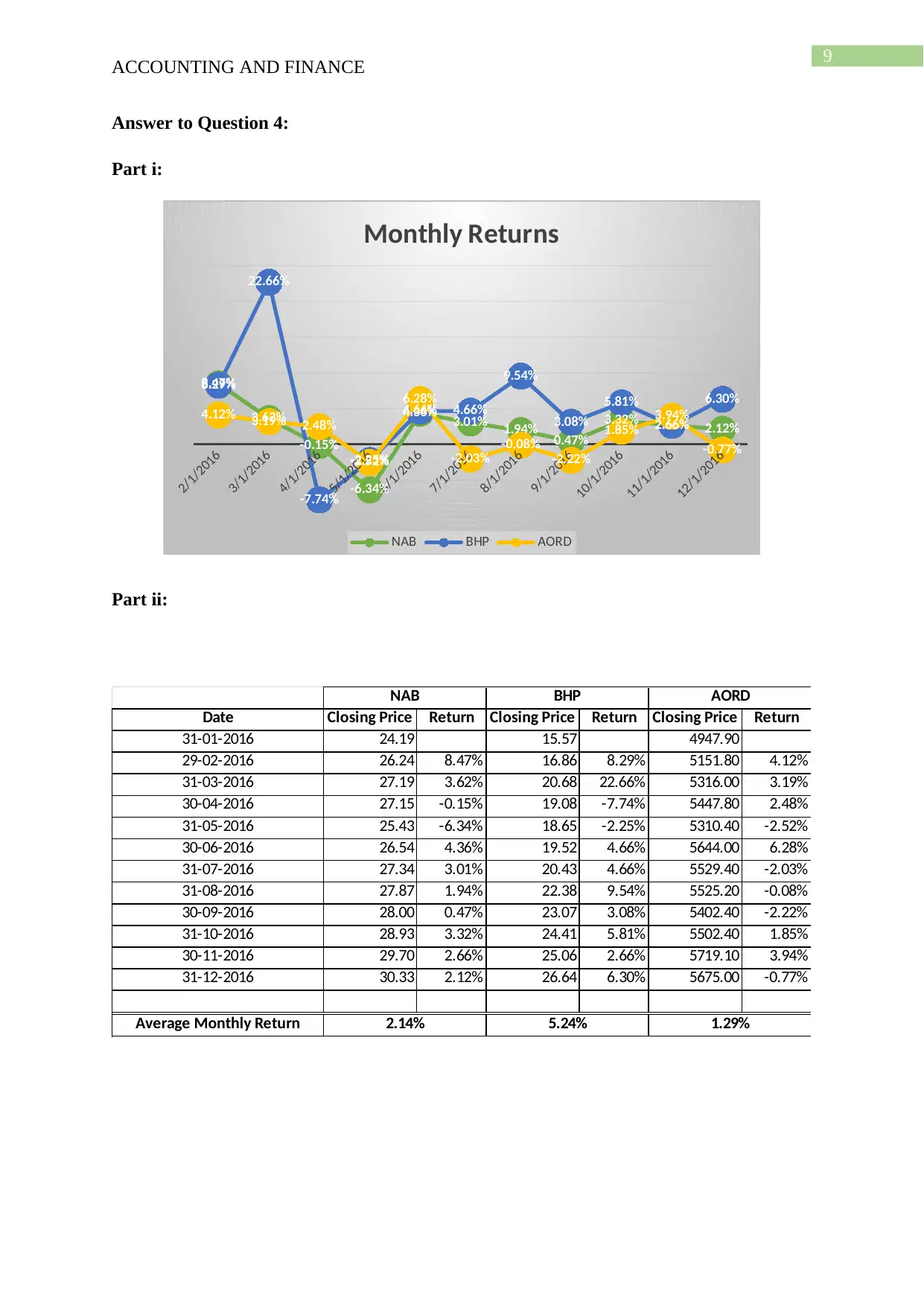

Part i:

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

8.47%

3.62%

-0.15%

-6.34%

4.36% 3.01% 1.94% 0.47%

3.32% 2.66% 2.12%

8.29%

22.66%

-7.74%

-2.25%

4.66% 4.66%

9.54%

3.08%

5.81%

2.66%

6.30%

4.12% 3.19% 2.48%

-2.52%

6.28%

-2.03%

-0.08%

-2.22%

1.85%

3.94%

-0.77%

Monthly Returns

NAB BHP AORD

Part ii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return

NAB BHP AORD

2.14% 1.29%5.24%

ACCOUNTING AND FINANCE

Answer to Question 4:

Part i:

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

8.47%

3.62%

-0.15%

-6.34%

4.36% 3.01% 1.94% 0.47%

3.32% 2.66% 2.12%

8.29%

22.66%

-7.74%

-2.25%

4.66% 4.66%

9.54%

3.08%

5.81%

2.66%

6.30%

4.12% 3.19% 2.48%

-2.52%

6.28%

-2.03%

-0.08%

-2.22%

1.85%

3.94%

-0.77%

Monthly Returns

NAB BHP AORD

Part ii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Average Monthly Return

NAB BHP AORD

2.14% 1.29%5.24%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING AND FINANCE

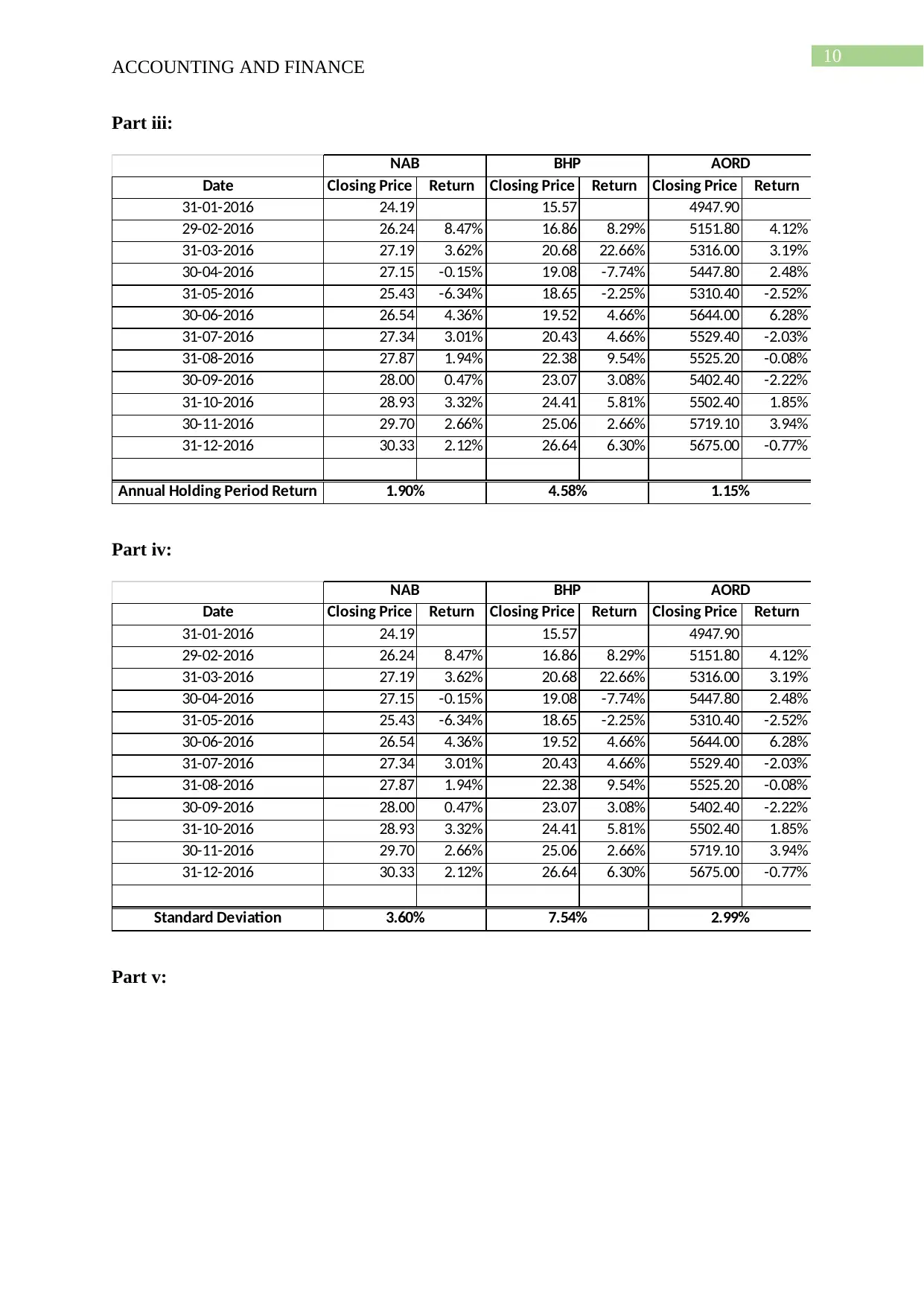

Part iii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period Return

NAB BHP AORD

1.90% 1.15%4.58%

Part iv:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation

NAB BHP AORD

3.60% 2.99%7.54%

Part v:

ACCOUNTING AND FINANCE

Part iii:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Annual Holding Period Return

NAB BHP AORD

1.90% 1.15%4.58%

Part iv:

Date Closing Price Return Closing Price Return Closing Price Return

31-01-2016 24.19 15.57 4947.90

29-02-2016 26.24 8.47% 16.86 8.29% 5151.80 4.12%

31-03-2016 27.19 3.62% 20.68 22.66% 5316.00 3.19%

30-04-2016 27.15 -0.15% 19.08 -7.74% 5447.80 2.48%

31-05-2016 25.43 -6.34% 18.65 -2.25% 5310.40 -2.52%

30-06-2016 26.54 4.36% 19.52 4.66% 5644.00 6.28%

31-07-2016 27.34 3.01% 20.43 4.66% 5529.40 -2.03%

31-08-2016 27.87 1.94% 22.38 9.54% 5525.20 -0.08%

30-09-2016 28.00 0.47% 23.07 3.08% 5402.40 -2.22%

31-10-2016 28.93 3.32% 24.41 5.81% 5502.40 1.85%

30-11-2016 29.70 2.66% 25.06 2.66% 5719.10 3.94%

31-12-2016 30.33 2.12% 26.64 6.30% 5675.00 -0.77%

Standard Deviation

NAB BHP AORD

3.60% 2.99%7.54%

Part v:

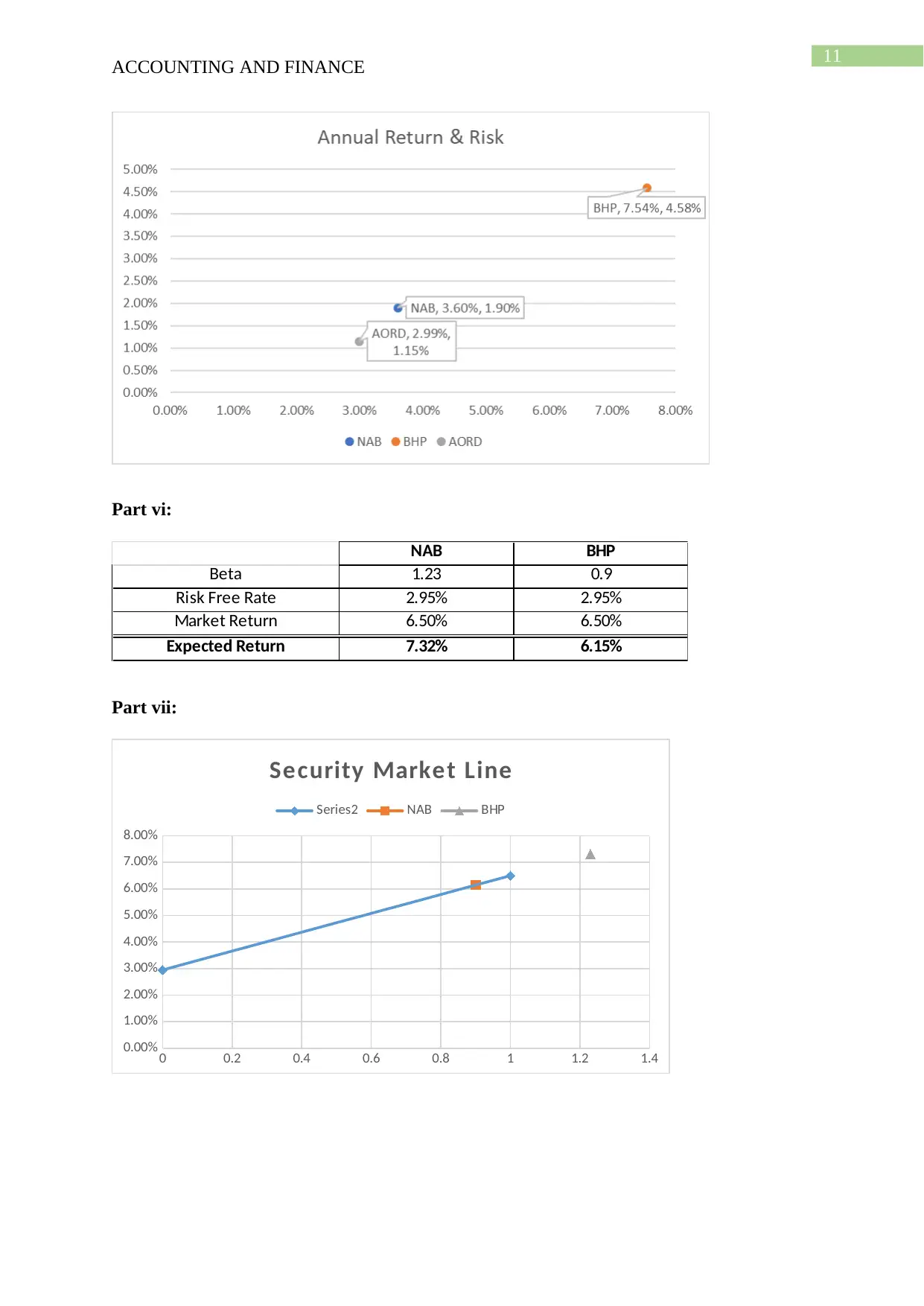

11

ACCOUNTING AND FINANCE

Part vi:

Beta

Risk Free Rate

Market Return

Expected Return

NAB BHP

1.23

2.95%

6.50%

7.32%

0.9

2.95%

6.50%

6.15%

Part vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Security Market Line

Series2 NAB BHP

ACCOUNTING AND FINANCE

Part vi:

Beta

Risk Free Rate

Market Return

Expected Return

NAB BHP

1.23

2.95%

6.50%

7.32%

0.9

2.95%

6.50%

6.15%

Part vii:

0 0.2 0.4 0.6 0.8 1 1.2 1.4

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Security Market Line

Series2 NAB BHP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.