Accounting Solutions: Income Tax, Journal Entries, Financial Leases

VerifiedAdded on 2023/06/18

|11

|1223

|281

Homework Assignment

AI Summary

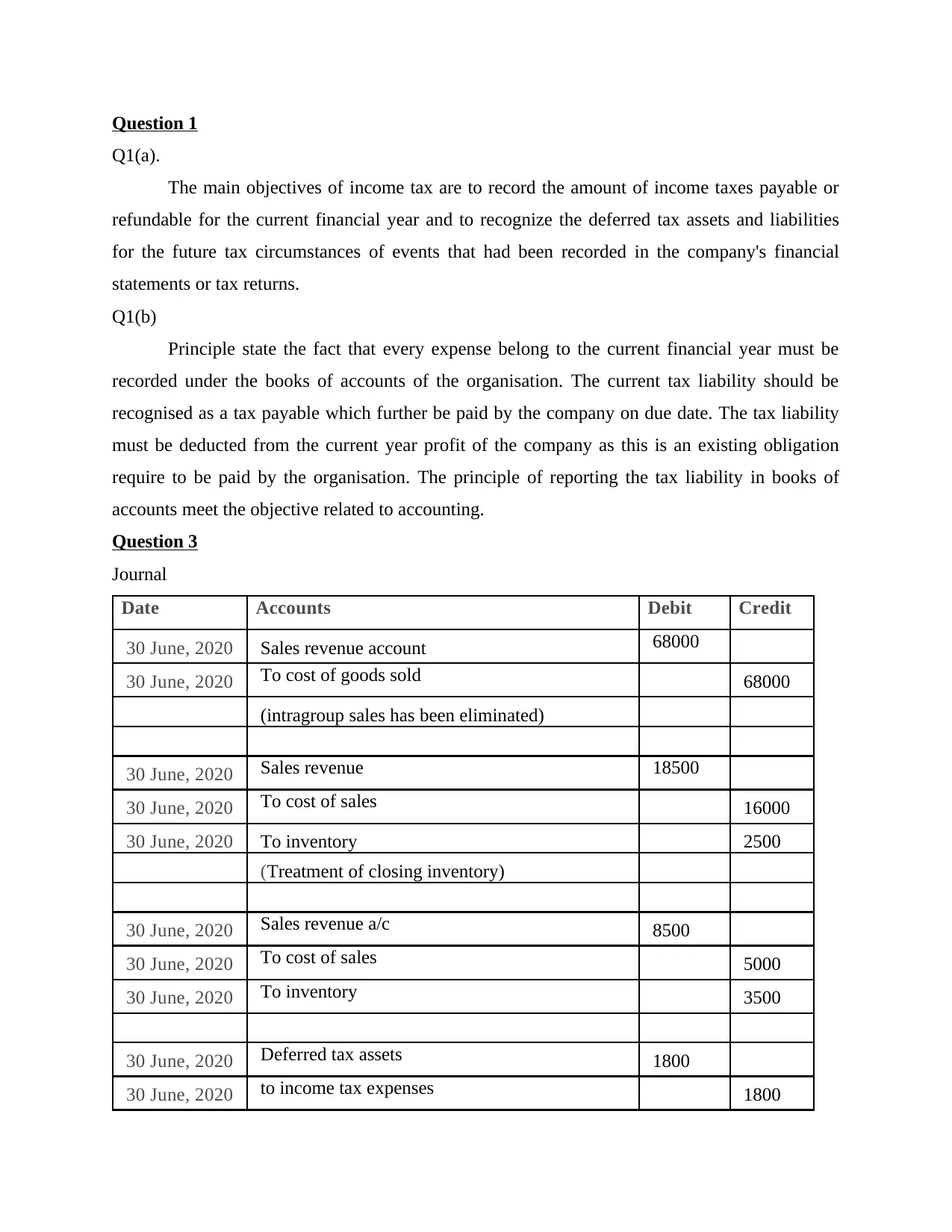

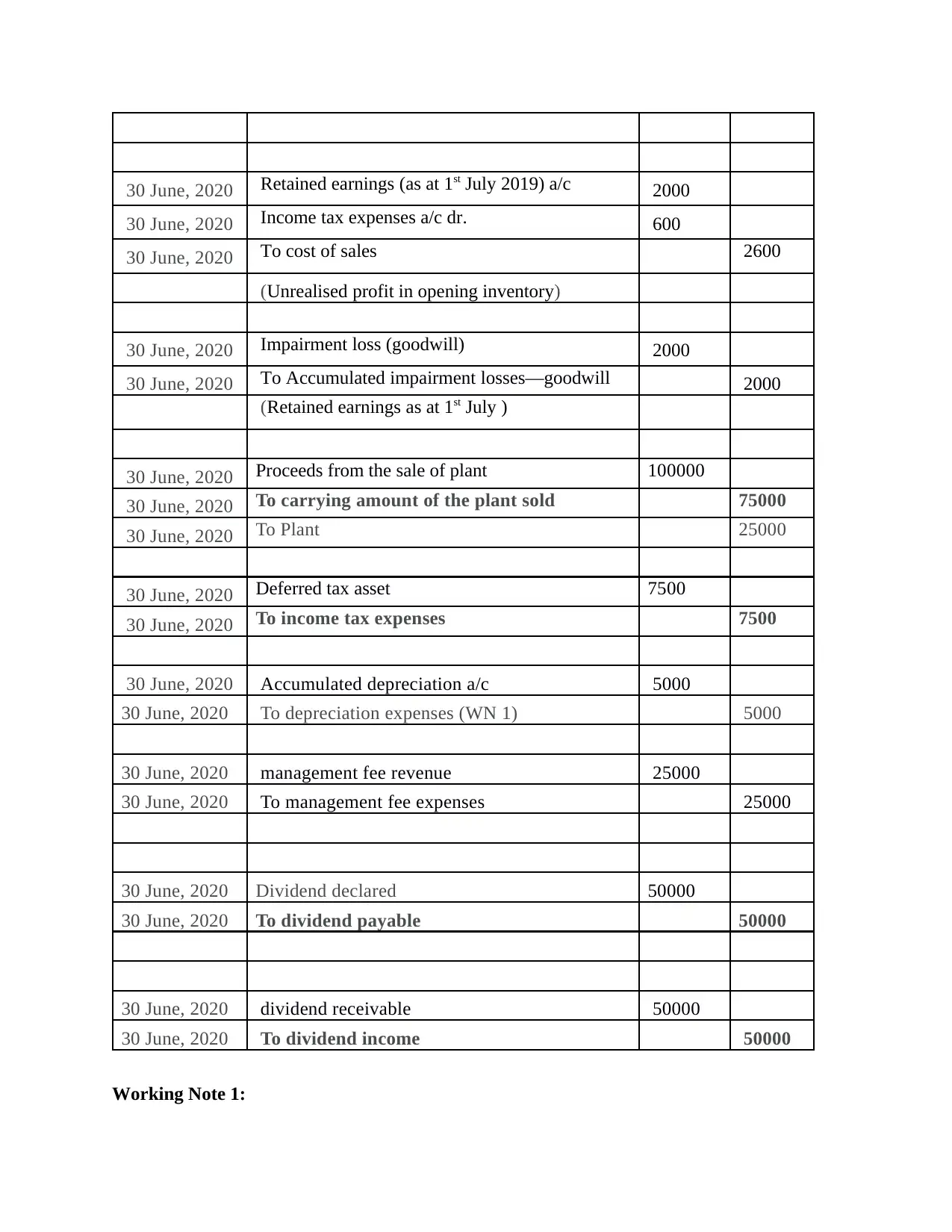

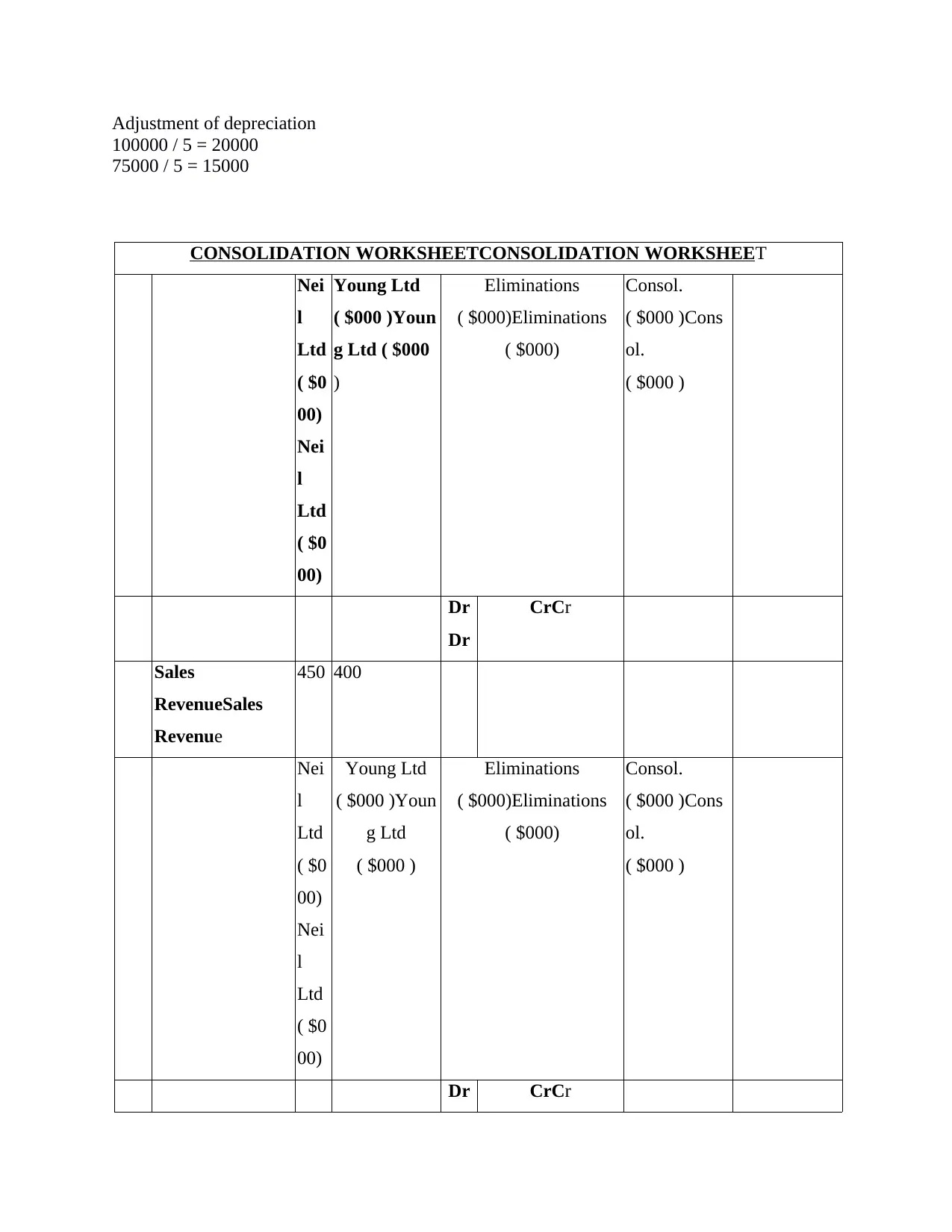

This accounting assignment solution provides detailed answers to various accounting problems. It includes calculating income tax, preparing journal entries for intragroup sales, unrealized profits, and deferred tax assets. It also covers the creation of a consolidation worksheet, including eliminations for intragroup transactions. Furthermore, the solution addresses the calculation of capital gains, income tax liabilities, and the accounting treatment for financial leases, including the present value calculation and lease payment schedule. Finally, it discusses the accounting standard for proposed dividends and their treatment as contingent liabilities. Desklib offers this and many other solved assignments for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.