Financial Reporting Exam Solutions - Detailed Calculations Included

VerifiedAdded on 2022/12/28

|12

|2264

|31

Homework Assignment

AI Summary

This document contains comprehensive solutions to a Financial Reporting exam, covering multiple sections and questions. Section A includes detailed calculations for consolidation, focusing on group structures, consideration transfers, fair value adjustments, goodwill, and non-controlling interests. It analyzes the application of IFRS 10 regarding control components. Section B addresses statement of cash flows (IAS 7), contract accounting, and revenue recognition under IFRS 15. The solutions provide step-by-step calculations for cash flow statements, accounting for contract liabilities, commission, performance obligations, depreciation, and currency translation. The document offers practical advice on accounting treatments and currency selection, ensuring a thorough understanding of financial reporting concepts.

Feedback: Please see question 4 in section 2. Please go over

every calculation for every question so that they are all correct

and non is missing. Many Thanks

Online Exam (Financial

Reporting)

every calculation for every question so that they are all correct

and non is missing. Many Thanks

Online Exam (Financial

Reporting)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................6

SECTION B.....................................................................................................................................8

Question 4....................................................................................................................................8

Question 5..................................................................................................................................10

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................6

SECTION B.....................................................................................................................................8

Question 4....................................................................................................................................8

Question 5..................................................................................................................................10

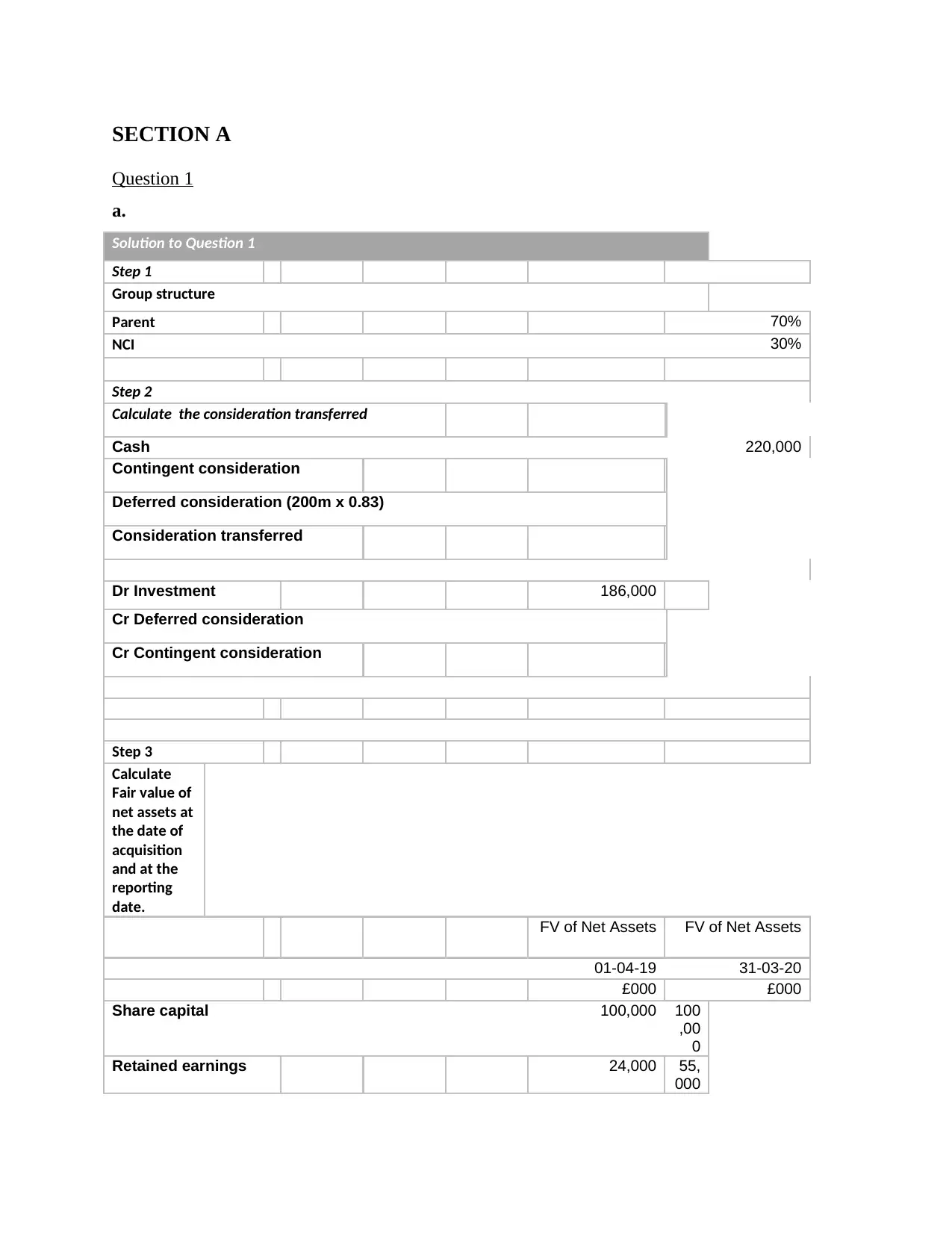

SECTION A

Question 1

a.

Solution to Question 1

Step 1

Group structure

Parent 70%

NCI 30%

Step 2

Calculate the consideration transferred

Cash 220,000

Contingent consideration

Deferred consideration (200m x 0.83)

Consideration transferred

Dr Investment 186,000

Cr Deferred consideration

Cr Contingent consideration

Step 3

Calculate

Fair value of

net assets at

the date of

acquisition

and at the

reporting

date.

FV of Net Assets FV of Net Assets

01-04-19 31-03-20

£000 £000

Share capital 100,000 100

,00

0

Retained earnings 24,000 55,

000

Question 1

a.

Solution to Question 1

Step 1

Group structure

Parent 70%

NCI 30%

Step 2

Calculate the consideration transferred

Cash 220,000

Contingent consideration

Deferred consideration (200m x 0.83)

Consideration transferred

Dr Investment 186,000

Cr Deferred consideration

Cr Contingent consideration

Step 3

Calculate

Fair value of

net assets at

the date of

acquisition

and at the

reporting

date.

FV of Net Assets FV of Net Assets

01-04-19 31-03-20

£000 £000

Share capital 100,000 100

,00

0

Retained earnings 24,000 55,

000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

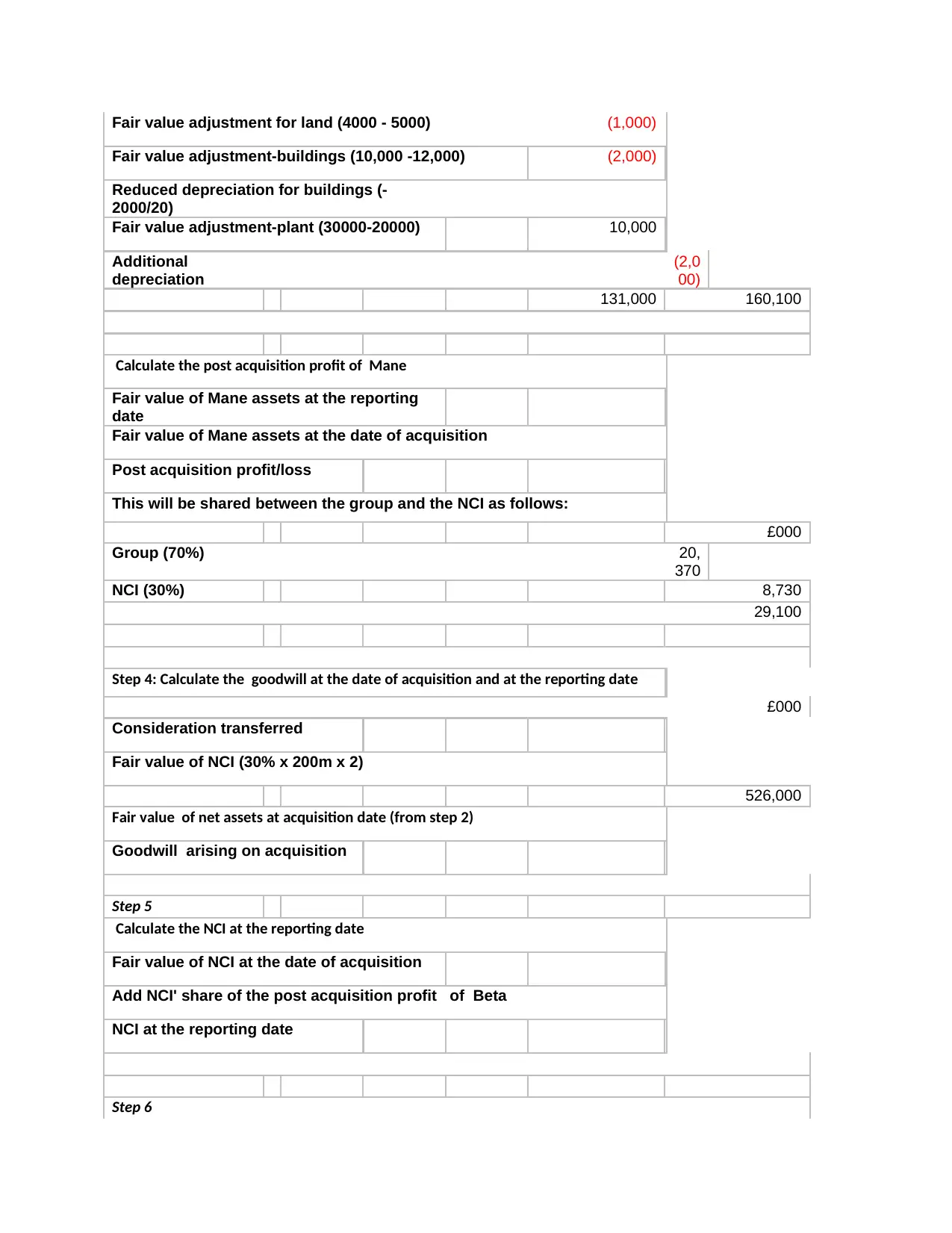

Fair value adjustment for land (4000 - 5000) (1,000)

Fair value adjustment-buildings (10,000 -12,000) (2,000)

Reduced depreciation for buildings (-

2000/20)

Fair value adjustment-plant (30000-20000) 10,000

Additional

depreciation

(2,0

00)

131,000 160,100

Calculate the post acquisition profit of Mane

Fair value of Mane assets at the reporting

date

Fair value of Mane assets at the date of acquisition

Post acquisition profit/loss

This will be shared between the group and the NCI as follows:

£000

Group (70%) 20,

370

NCI (30%) 8,730

29,100

Step 4: Calculate the goodwill at the date of acquisition and at the reporting date

£000

Consideration transferred

Fair value of NCI (30% x 200m x 2)

526,000

Fair value of net assets at acquisition date (from step 2)

Goodwill arising on acquisition

Step 5

Calculate the NCI at the reporting date

Fair value of NCI at the date of acquisition

Add NCI' share of the post acquisition profit of Beta

NCI at the reporting date

Step 6

Fair value adjustment-buildings (10,000 -12,000) (2,000)

Reduced depreciation for buildings (-

2000/20)

Fair value adjustment-plant (30000-20000) 10,000

Additional

depreciation

(2,0

00)

131,000 160,100

Calculate the post acquisition profit of Mane

Fair value of Mane assets at the reporting

date

Fair value of Mane assets at the date of acquisition

Post acquisition profit/loss

This will be shared between the group and the NCI as follows:

£000

Group (70%) 20,

370

NCI (30%) 8,730

29,100

Step 4: Calculate the goodwill at the date of acquisition and at the reporting date

£000

Consideration transferred

Fair value of NCI (30% x 200m x 2)

526,000

Fair value of net assets at acquisition date (from step 2)

Goodwill arising on acquisition

Step 5

Calculate the NCI at the reporting date

Fair value of NCI at the date of acquisition

Add NCI' share of the post acquisition profit of Beta

NCI at the reporting date

Step 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

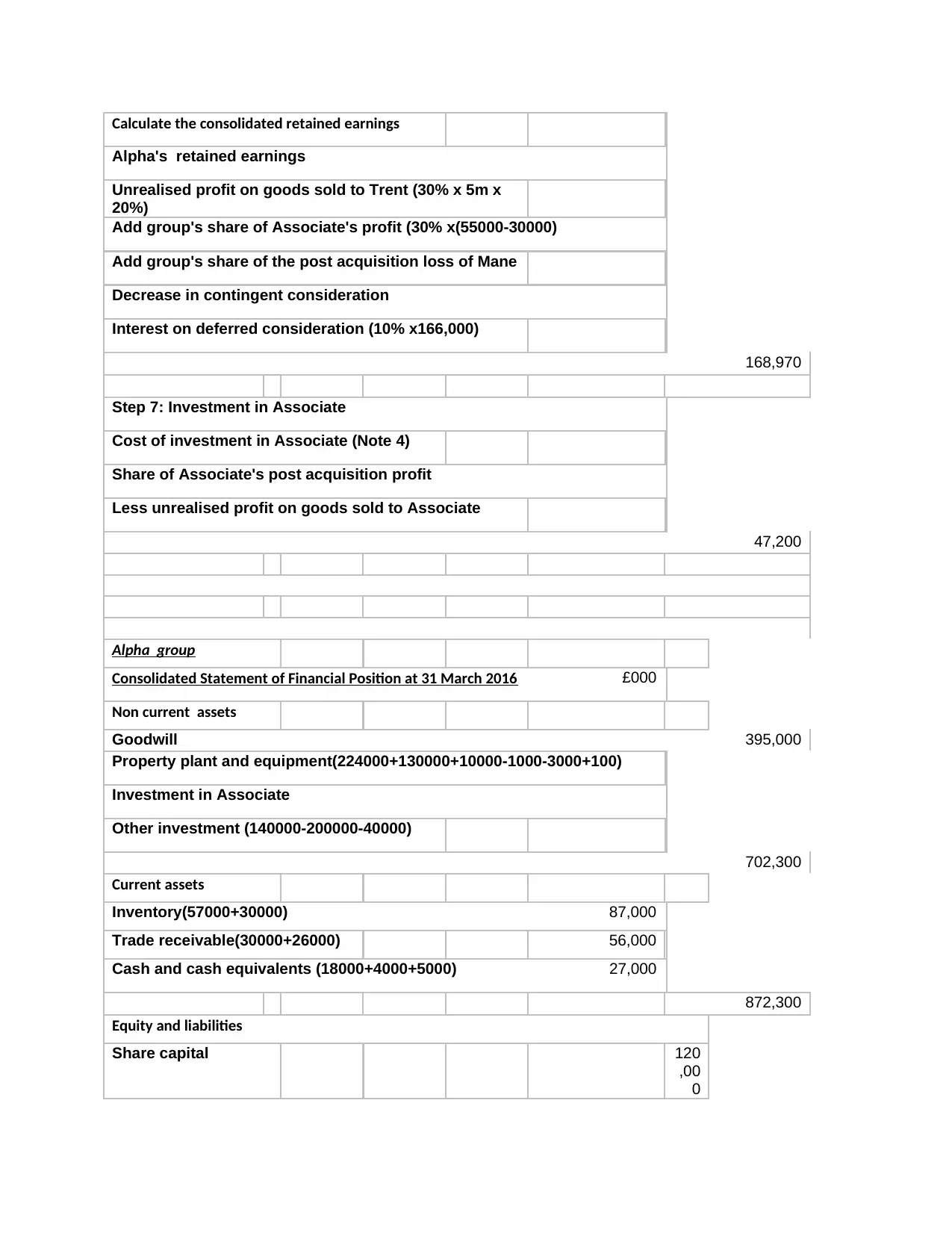

Calculate the consolidated retained earnings

Alpha's retained earnings

Unrealised profit on goods sold to Trent (30% x 5m x

20%)

Add group's share of Associate's profit (30% x(55000-30000)

Add group's share of the post acquisition loss of Mane

Decrease in contingent consideration

Interest on deferred consideration (10% x166,000)

168,970

Step 7: Investment in Associate

Cost of investment in Associate (Note 4)

Share of Associate's post acquisition profit

Less unrealised profit on goods sold to Associate

47,200

Alpha group

Consolidated Statement of Financial Position at 31 March 2016 £000

Non current assets

Goodwill 395,000

Property plant and equipment(224000+130000+10000-1000-3000+100)

Investment in Associate

Other investment (140000-200000-40000)

702,300

Current assets

Inventory(57000+30000) 87,000

Trade receivable(30000+26000) 56,000

Cash and cash equivalents (18000+4000+5000) 27,000

872,300

Equity and liabilities

Share capital 120

,00

0

Alpha's retained earnings

Unrealised profit on goods sold to Trent (30% x 5m x

20%)

Add group's share of Associate's profit (30% x(55000-30000)

Add group's share of the post acquisition loss of Mane

Decrease in contingent consideration

Interest on deferred consideration (10% x166,000)

168,970

Step 7: Investment in Associate

Cost of investment in Associate (Note 4)

Share of Associate's post acquisition profit

Less unrealised profit on goods sold to Associate

47,200

Alpha group

Consolidated Statement of Financial Position at 31 March 2016 £000

Non current assets

Goodwill 395,000

Property plant and equipment(224000+130000+10000-1000-3000+100)

Investment in Associate

Other investment (140000-200000-40000)

702,300

Current assets

Inventory(57000+30000) 87,000

Trade receivable(30000+26000) 56,000

Cash and cash equivalents (18000+4000+5000) 27,000

872,300

Equity and liabilities

Share capital 120

,00

0

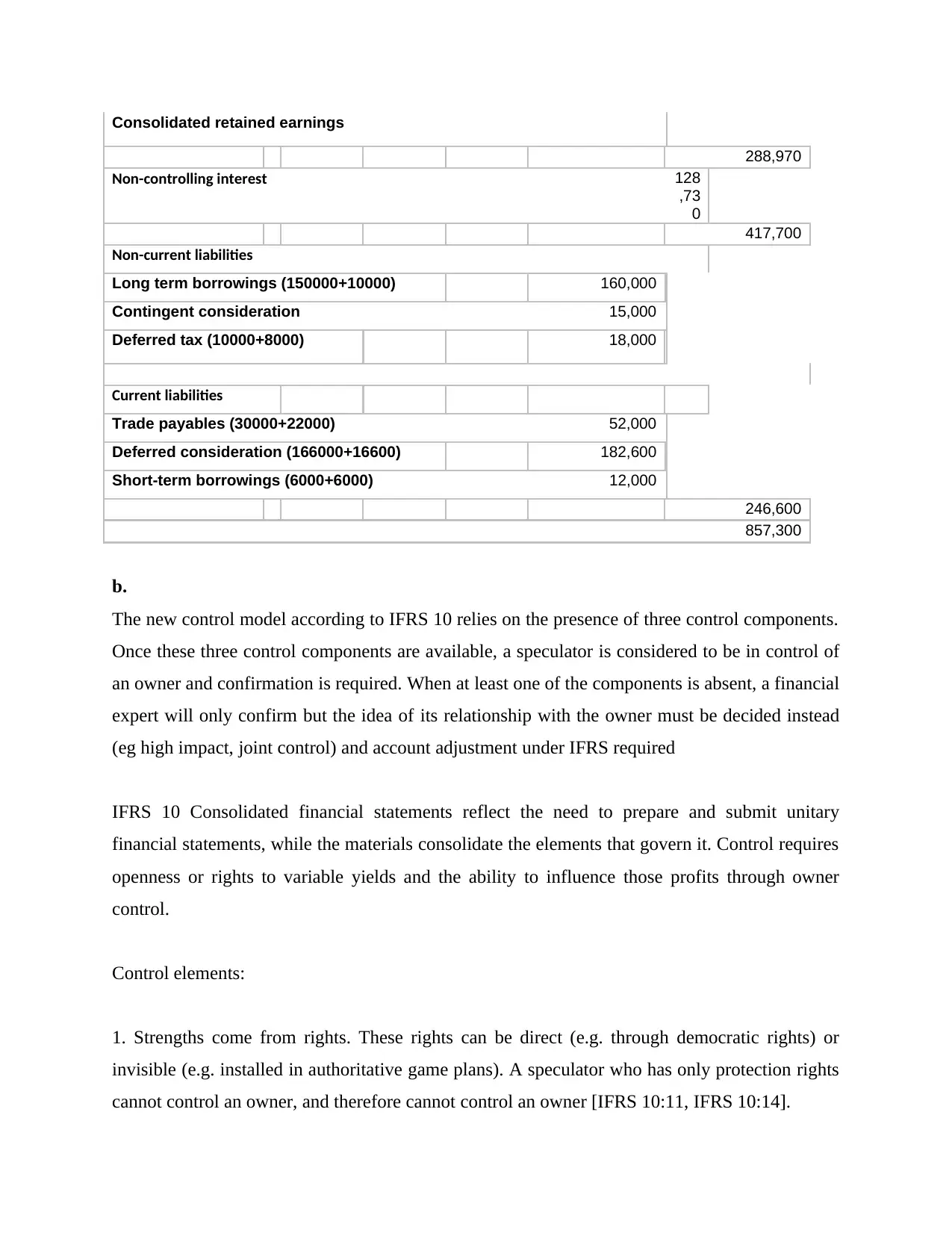

Consolidated retained earnings

288,970

Non-controlling interest 128

,73

0

417,700

Non-current liabilities

Long term borrowings (150000+10000) 160,000

Contingent consideration 15,000

Deferred tax (10000+8000) 18,000

Current liabilities

Trade payables (30000+22000) 52,000

Deferred consideration (166000+16600) 182,600

Short-term borrowings (6000+6000) 12,000

246,600

857,300

b.

The new control model according to IFRS 10 relies on the presence of three control components.

Once these three control components are available, a speculator is considered to be in control of

an owner and confirmation is required. When at least one of the components is absent, a financial

expert will only confirm but the idea of its relationship with the owner must be decided instead

(eg high impact, joint control) and account adjustment under IFRS required

IFRS 10 Consolidated financial statements reflect the need to prepare and submit unitary

financial statements, while the materials consolidate the elements that govern it. Control requires

openness or rights to variable yields and the ability to influence those profits through owner

control.

Control elements:

1. Strengths come from rights. These rights can be direct (e.g. through democratic rights) or

invisible (e.g. installed in authoritative game plans). A speculator who has only protection rights

cannot control an owner, and therefore cannot control an owner [IFRS 10:11, IFRS 10:14].

288,970

Non-controlling interest 128

,73

0

417,700

Non-current liabilities

Long term borrowings (150000+10000) 160,000

Contingent consideration 15,000

Deferred tax (10000+8000) 18,000

Current liabilities

Trade payables (30000+22000) 52,000

Deferred consideration (166000+16600) 182,600

Short-term borrowings (6000+6000) 12,000

246,600

857,300

b.

The new control model according to IFRS 10 relies on the presence of three control components.

Once these three control components are available, a speculator is considered to be in control of

an owner and confirmation is required. When at least one of the components is absent, a financial

expert will only confirm but the idea of its relationship with the owner must be decided instead

(eg high impact, joint control) and account adjustment under IFRS required

IFRS 10 Consolidated financial statements reflect the need to prepare and submit unitary

financial statements, while the materials consolidate the elements that govern it. Control requires

openness or rights to variable yields and the ability to influence those profits through owner

control.

Control elements:

1. Strengths come from rights. These rights can be direct (e.g. through democratic rights) or

invisible (e.g. installed in authoritative game plans). A speculator who has only protection rights

cannot control an owner, and therefore cannot control an owner [IFRS 10:11, IFRS 10:14].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

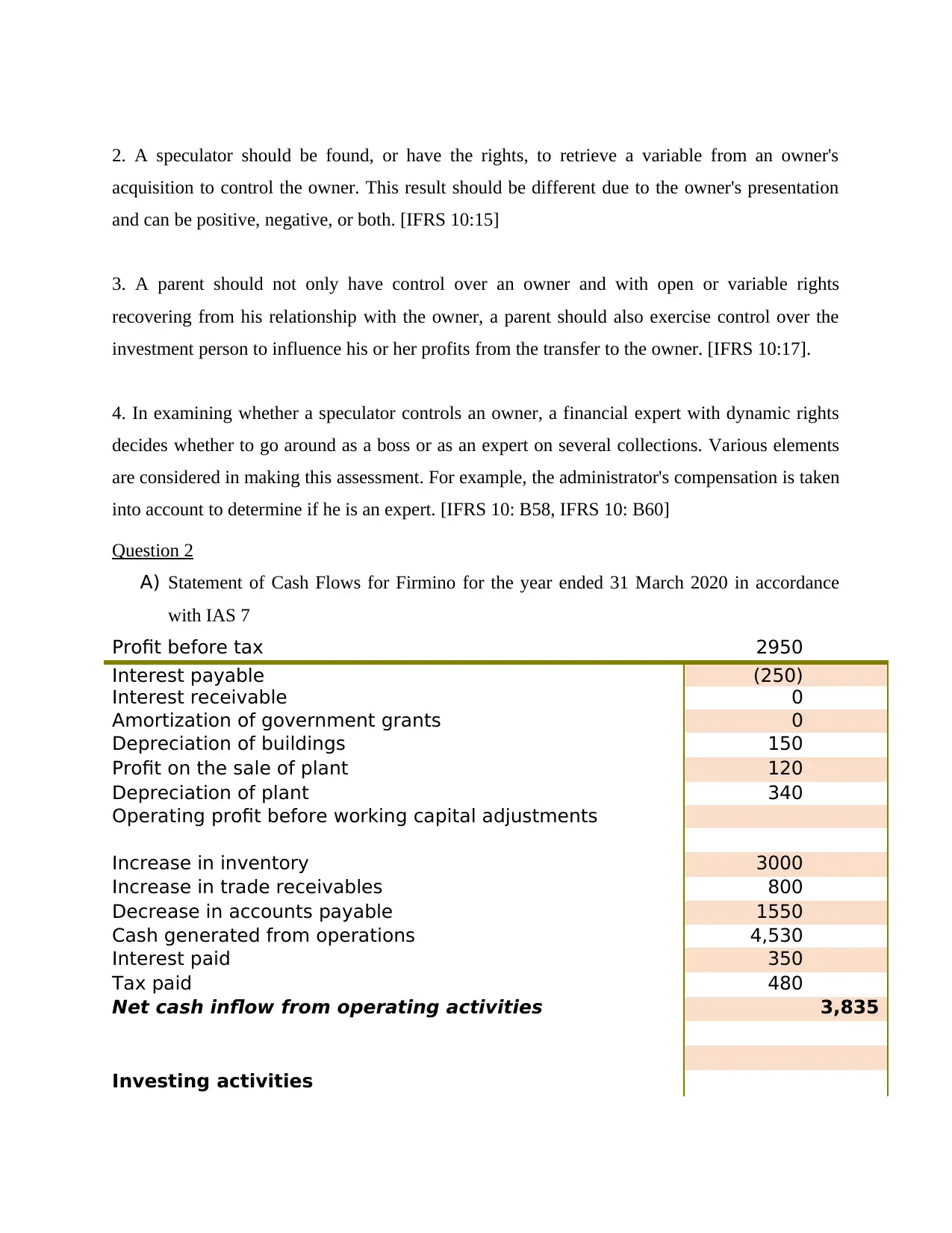

2. A speculator should be found, or have the rights, to retrieve a variable from an owner's

acquisition to control the owner. This result should be different due to the owner's presentation

and can be positive, negative, or both. [IFRS 10:15]

3. A parent should not only have control over an owner and with open or variable rights

recovering from his relationship with the owner, a parent should also exercise control over the

investment person to influence his or her profits from the transfer to the owner. [IFRS 10:17].

4. In examining whether a speculator controls an owner, a financial expert with dynamic rights

decides whether to go around as a boss or as an expert on several collections. Various elements

are considered in making this assessment. For example, the administrator's compensation is taken

into account to determine if he is an expert. [IFRS 10: B58, IFRS 10: B60]

Question 2

A) Statement of Cash Flows for Firmino for the year ended 31 March 2020 in accordance

with IAS 7

Profit before tax 2950

Interest payable (250)

Interest receivable 0

Amortization of government grants 0

Depreciation of buildings 150

Profit on the sale of plant 120

Depreciation of plant 340

Operating profit before working capital adjustments

Increase in inventory 3000

Increase in trade receivables 800

Decrease in accounts payable 1550

Cash generated from operations 4,530

Interest paid 350

Tax paid 480

Net cash inflow from operating activities 3,835

Investing activities

acquisition to control the owner. This result should be different due to the owner's presentation

and can be positive, negative, or both. [IFRS 10:15]

3. A parent should not only have control over an owner and with open or variable rights

recovering from his relationship with the owner, a parent should also exercise control over the

investment person to influence his or her profits from the transfer to the owner. [IFRS 10:17].

4. In examining whether a speculator controls an owner, a financial expert with dynamic rights

decides whether to go around as a boss or as an expert on several collections. Various elements

are considered in making this assessment. For example, the administrator's compensation is taken

into account to determine if he is an expert. [IFRS 10: B58, IFRS 10: B60]

Question 2

A) Statement of Cash Flows for Firmino for the year ended 31 March 2020 in accordance

with IAS 7

Profit before tax 2950

Interest payable (250)

Interest receivable 0

Amortization of government grants 0

Depreciation of buildings 150

Profit on the sale of plant 120

Depreciation of plant 340

Operating profit before working capital adjustments

Increase in inventory 3000

Increase in trade receivables 800

Decrease in accounts payable 1550

Cash generated from operations 4,530

Interest paid 350

Tax paid 480

Net cash inflow from operating activities 3,835

Investing activities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash paid for investments

Cash paid for plant 250

Cash received from the sale of plant 120

Cash paid for buildings (870)

Government grants received 250

Interest received 440

Net cash outflow for investing activities 190

Financing activities

Dividends paid (4,64

5)

Finance lease obligations -340

Cash from issue of shares 1,600

-

3585

Decrease in cash (210)

Cash and bank at the beginning of the year 70

Cash and bank at the end of the year (140)

Reconciliation of cash and cash equivalents 201

1

2010 Inflow

/

(outfl

ow)

Bank 50 150 (100)

Overdraft (19

0)

(80) (110)

(14

0)

70 (210)

b) The main issues highlighted in Firmino’s income statement are negative changes in both the

grant and funding years, which usually result in a negative balance from each of the three years.

In this way, both of these exercises are the key issues found in income generation. Because both

exercises lead to an increase in cash from the ratio of the balance sheet of the organization, and is

reflected by a decreasing balance of money and equal cash in the cash register.

c) The main drivers of profit for capital in the year 2020 are labour benefits or cash inflows in

business years. This asset gain was considered to determine the return on capital employed.

Where the capital is used there is a mixture of value and connection. The company's net profit on

interest and valuation is the only factor driving a return to the company.

Cash paid for plant 250

Cash received from the sale of plant 120

Cash paid for buildings (870)

Government grants received 250

Interest received 440

Net cash outflow for investing activities 190

Financing activities

Dividends paid (4,64

5)

Finance lease obligations -340

Cash from issue of shares 1,600

-

3585

Decrease in cash (210)

Cash and bank at the beginning of the year 70

Cash and bank at the end of the year (140)

Reconciliation of cash and cash equivalents 201

1

2010 Inflow

/

(outfl

ow)

Bank 50 150 (100)

Overdraft (19

0)

(80) (110)

(14

0)

70 (210)

b) The main issues highlighted in Firmino’s income statement are negative changes in both the

grant and funding years, which usually result in a negative balance from each of the three years.

In this way, both of these exercises are the key issues found in income generation. Because both

exercises lead to an increase in cash from the ratio of the balance sheet of the organization, and is

reflected by a decreasing balance of money and equal cash in the cash register.

c) The main drivers of profit for capital in the year 2020 are labour benefits or cash inflows in

business years. This asset gain was considered to determine the return on capital employed.

Where the capital is used there is a mixture of value and connection. The company's net profit on

interest and valuation is the only factor driving a return to the company.

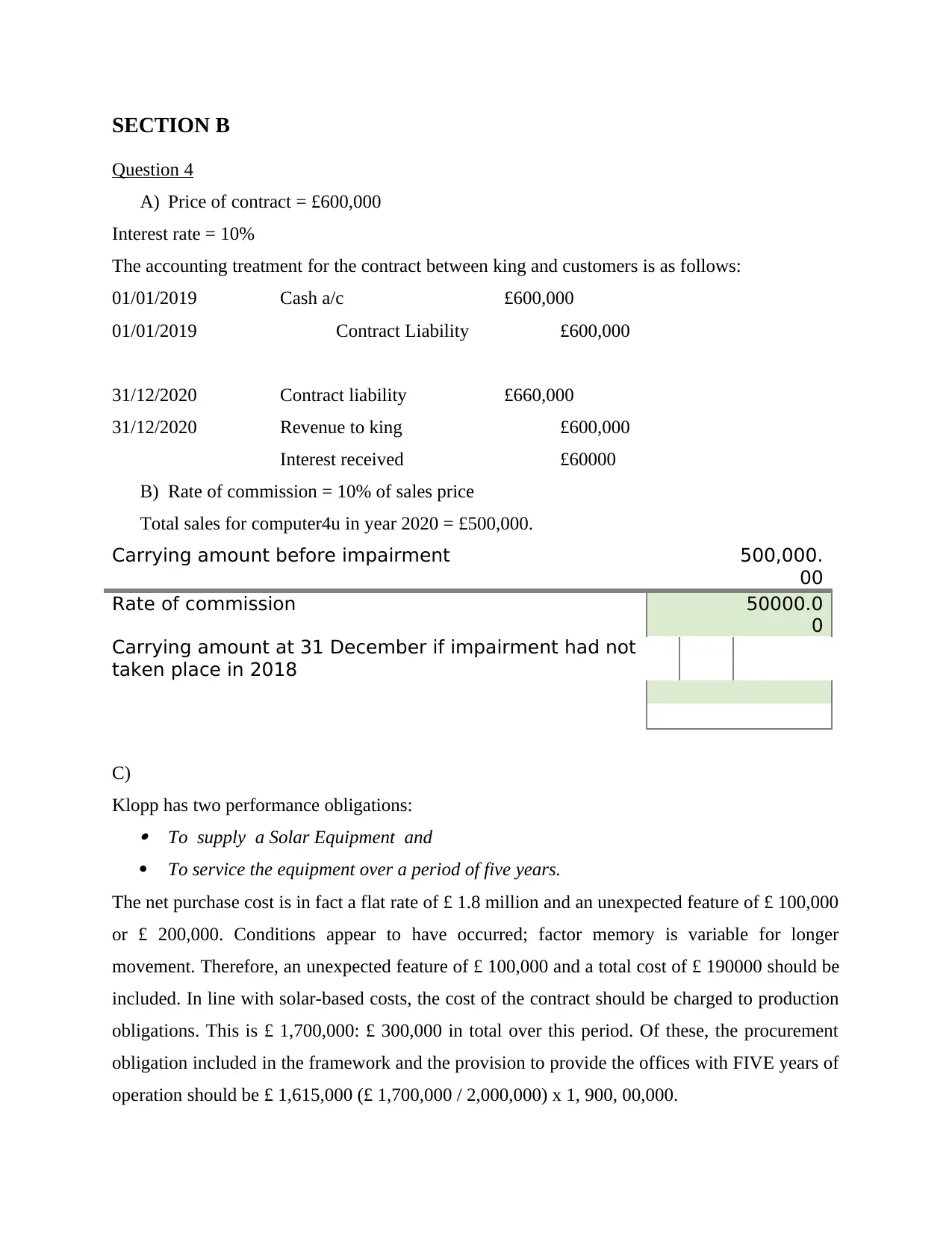

SECTION B

Question 4

A) Price of contract = £600,000

Interest rate = 10%

The accounting treatment for the contract between king and customers is as follows:

01/01/2019 Cash a/c £600,000

01/01/2019 Contract Liability £600,000

31/12/2020 Contract liability £660,000

31/12/2020 Revenue to king £600,000

Interest received £60000

B) Rate of commission = 10% of sales price

Total sales for computer4u in year 2020 = £500,000.

Carrying amount before impairment 500,000.

00

Rate of commission 50000.0

0

Carrying amount at 31 December if impairment had not

taken place in 2018

C)

Klopp has two performance obligations: To supply a Solar Equipment and

To service the equipment over a period of five years.

The net purchase cost is in fact a flat rate of £ 1.8 million and an unexpected feature of £ 100,000

or £ 200,000. Conditions appear to have occurred; factor memory is variable for longer

movement. Therefore, an unexpected feature of £ 100,000 and a total cost of £ 190000 should be

included. In line with solar-based costs, the cost of the contract should be charged to production

obligations. This is £ 1,700,000: £ 300,000 in total over this period. Of these, the procurement

obligation included in the framework and the provision to provide the offices with FIVE years of

operation should be £ 1,615,000 (£ 1,700,000 / 2,000,000) x 1, 900, 00,000.

Question 4

A) Price of contract = £600,000

Interest rate = 10%

The accounting treatment for the contract between king and customers is as follows:

01/01/2019 Cash a/c £600,000

01/01/2019 Contract Liability £600,000

31/12/2020 Contract liability £660,000

31/12/2020 Revenue to king £600,000

Interest received £60000

B) Rate of commission = 10% of sales price

Total sales for computer4u in year 2020 = £500,000.

Carrying amount before impairment 500,000.

00

Rate of commission 50000.0

0

Carrying amount at 31 December if impairment had not

taken place in 2018

C)

Klopp has two performance obligations: To supply a Solar Equipment and

To service the equipment over a period of five years.

The net purchase cost is in fact a flat rate of £ 1.8 million and an unexpected feature of £ 100,000

or £ 200,000. Conditions appear to have occurred; factor memory is variable for longer

movement. Therefore, an unexpected feature of £ 100,000 and a total cost of £ 190000 should be

included. In line with solar-based costs, the cost of the contract should be charged to production

obligations. This is £ 1,700,000: £ 300,000 in total over this period. Of these, the procurement

obligation included in the framework and the provision to provide the offices with FIVE years of

operation should be £ 1,615,000 (£ 1,700,000 / 2,000,000) x 1, 900, 00,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

During the cash flow year ending 31 December 2016, the obligation to enter the framework is

fully satisfied and a payment of £ 1,615,000 may be associated with this investment.

Notice and in the cash flow year Ended December 31, 2016, 7/60 (December 1 to December 31

seven months) was certainly satisfied with a duty obligation, so it would be possible to recognize

an income as a result of these transfers of £ 33,250 (£ 285,000 x 7/60).

As of 1st June 2016, Klopp will recognize the payment of £ 1,900,000 subject to an appropriate

assessment of the situation. Klopp's total benefits of £ 251,750 (€ 1,900,000,000 - £ 1,615,000 -

33250) were written off as of 31 December 2016. The current liability would be £ 57,000 (£ 251,

750 x 12/53). The absent pledge is the balance of £ 194,750 (£ 251,750-57000).

53 = 60 months without seven months (from 1 June 2016 to 31 December 2016 there is a period

of 7 months).

b) As this number is determined in detail, the contracts would be valued and the total income

would be determined at £ 4,320,000 (90% 800x £ 6,000). The trade is known as credits for £

4,800,000 (800 x £ 6,000). How did you get the 800?

The repayment obligation is £ 480,000 (£ 48,000 - £ 4320000). Is the obligation a negative

figure? This appears to be a current commitment. The total cost was £ 2,800,000 for products

sold (800 x £ 3,500). Only £ 2,520,000 of the total will be included as cost of sale (90% x 800x £

3,500). The remaining £ 280,000 is seen as a right to return existing assets (£ 2,800,000 - £

2,520,000). Can you please finalise question4(A) answer as the following: the

above transaction should be accounted for in the financial statements of King

for the financial years ended 31 December 2019 and 2020

………………………….

fully satisfied and a payment of £ 1,615,000 may be associated with this investment.

Notice and in the cash flow year Ended December 31, 2016, 7/60 (December 1 to December 31

seven months) was certainly satisfied with a duty obligation, so it would be possible to recognize

an income as a result of these transfers of £ 33,250 (£ 285,000 x 7/60).

As of 1st June 2016, Klopp will recognize the payment of £ 1,900,000 subject to an appropriate

assessment of the situation. Klopp's total benefits of £ 251,750 (€ 1,900,000,000 - £ 1,615,000 -

33250) were written off as of 31 December 2016. The current liability would be £ 57,000 (£ 251,

750 x 12/53). The absent pledge is the balance of £ 194,750 (£ 251,750-57000).

53 = 60 months without seven months (from 1 June 2016 to 31 December 2016 there is a period

of 7 months).

b) As this number is determined in detail, the contracts would be valued and the total income

would be determined at £ 4,320,000 (90% 800x £ 6,000). The trade is known as credits for £

4,800,000 (800 x £ 6,000). How did you get the 800?

The repayment obligation is £ 480,000 (£ 48,000 - £ 4320000). Is the obligation a negative

figure? This appears to be a current commitment. The total cost was £ 2,800,000 for products

sold (800 x £ 3,500). Only £ 2,520,000 of the total will be included as cost of sale (90% x 800x £

3,500). The remaining £ 280,000 is seen as a right to return existing assets (£ 2,800,000 - £

2,520,000). Can you please finalise question4(A) answer as the following: the

above transaction should be accounted for in the financial statements of King

for the financial years ended 31 December 2019 and 2020

………………………….

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Can you please label question 4 properly? E.G. Where is question 4(Ci &

Cii)?

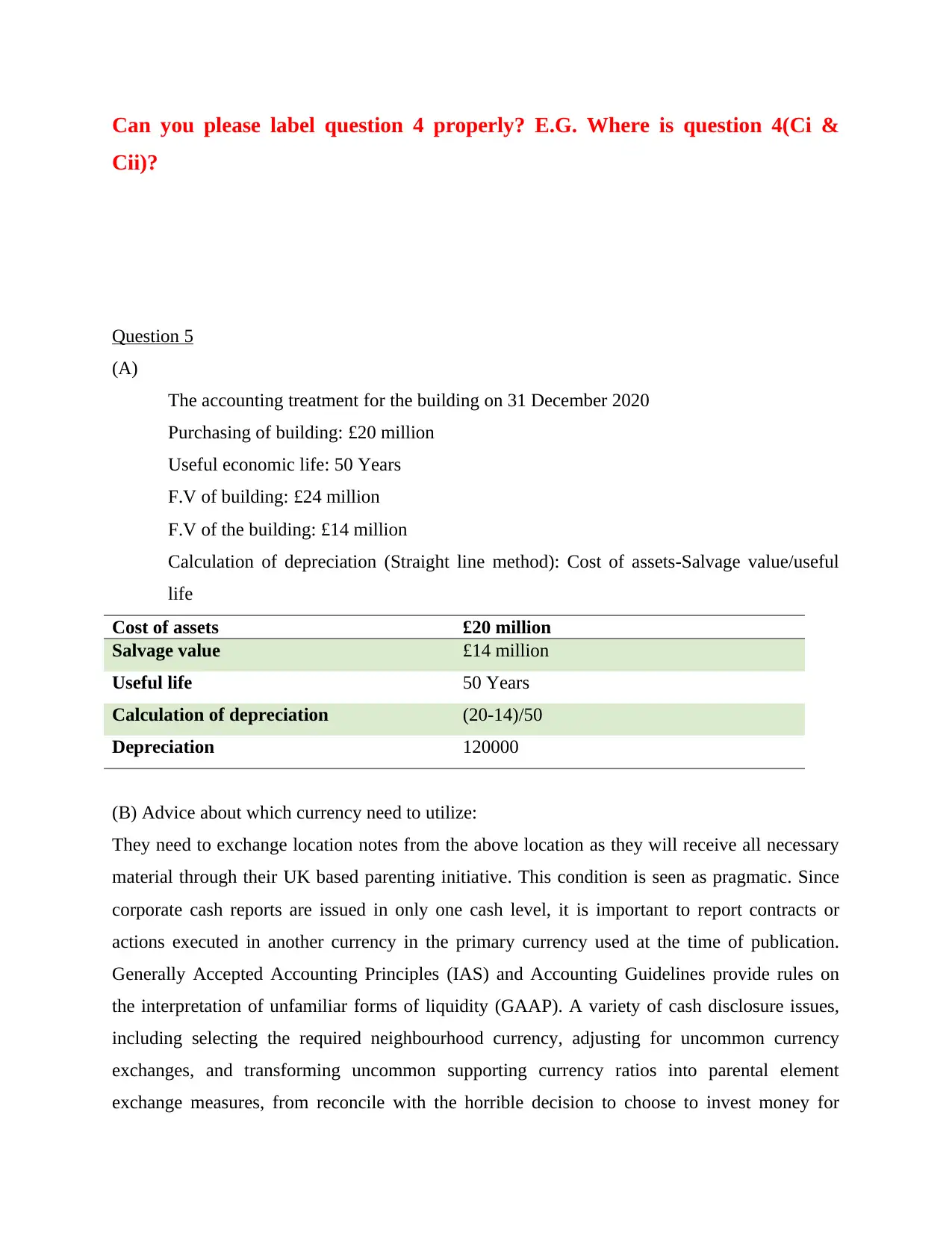

Question 5

(A)

The accounting treatment for the building on 31 December 2020

Purchasing of building: £20 million

Useful economic life: 50 Years

F.V of building: £24 million

F.V of the building: £14 million

Calculation of depreciation (Straight line method): Cost of assets-Salvage value/useful

life

Cost of assets £20 million

Salvage value £14 million

Useful life 50 Years

Calculation of depreciation (20-14)/50

Depreciation 120000

(B) Advice about which currency need to utilize:

They need to exchange location notes from the above location as they will receive all necessary

material through their UK based parenting initiative. This condition is seen as pragmatic. Since

corporate cash reports are issued in only one cash level, it is important to report contracts or

actions executed in another currency in the primary currency used at the time of publication.

Generally Accepted Accounting Principles (IAS) and Accounting Guidelines provide rules on

the interpretation of unfamiliar forms of liquidity (GAAP). A variety of cash disclosure issues,

including selecting the required neighbourhood currency, adjusting for uncommon currency

exchanges, and transforming uncommon supporting currency ratios into parental element

exchange measures, from reconcile with the horrible decision to choose to invest money for

Cii)?

Question 5

(A)

The accounting treatment for the building on 31 December 2020

Purchasing of building: £20 million

Useful economic life: 50 Years

F.V of building: £24 million

F.V of the building: £14 million

Calculation of depreciation (Straight line method): Cost of assets-Salvage value/useful

life

Cost of assets £20 million

Salvage value £14 million

Useful life 50 Years

Calculation of depreciation (20-14)/50

Depreciation 120000

(B) Advice about which currency need to utilize:

They need to exchange location notes from the above location as they will receive all necessary

material through their UK based parenting initiative. This condition is seen as pragmatic. Since

corporate cash reports are issued in only one cash level, it is important to report contracts or

actions executed in another currency in the primary currency used at the time of publication.

Generally Accepted Accounting Principles (IAS) and Accounting Guidelines provide rules on

the interpretation of unfamiliar forms of liquidity (GAAP). A variety of cash disclosure issues,

including selecting the required neighbourhood currency, adjusting for uncommon currency

exchanges, and transforming uncommon supporting currency ratios into parental element

exchange measures, from reconcile with the horrible decision to choose to invest money for

stocks around the world. (C) Advise the directors of Jack on to how to account for the above

transactions.

Date Particulars DR CR

1 January

2020

Patent account DR

To cash a/c

40

40

1 January

2020

Land a/c DR

Depreciation a/c DR

To cash a/c

16

4

20

1 January

2020

Accounts receivables a/c DR (3*2)

To sales

6

6

1 November

2020

Land a/c DR

Depreciation a/c DR

To cash a/c

100

50

150

1 January

2020

Accounts receivables a/c DR (9*1.5)

To sales

13.5

13.5

transactions.

Date Particulars DR CR

1 January

2020

Patent account DR

To cash a/c

40

40

1 January

2020

Land a/c DR

Depreciation a/c DR

To cash a/c

16

4

20

1 January

2020

Accounts receivables a/c DR (3*2)

To sales

6

6

1 November

2020

Land a/c DR

Depreciation a/c DR

To cash a/c

100

50

150

1 January

2020

Accounts receivables a/c DR (9*1.5)

To sales

13.5

13.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.