Analyzing Glebe Farm's Financial Ratios and Business Performance

VerifiedAdded on 2023/06/12

|9

|3028

|346

Report

AI Summary

This report provides a comprehensive financial analysis of Glebe Farm, focusing on the years 2020 and 2021. It calculates and interprets key financial ratios such as the gearing ratio, interest coverage ratio, quick ratio, inventory days, and receivable days. The analysis identifies trends, discusses the implications of changes in these metrics, and assesses the overall financial health of the company. Furthermore, it advises the financial director on the sufficiency of the financial statements for a bank loan application and highlights the limitations of financial record analysis. The report also addresses operational aspects, examining demand variability sources at Glebe Farm and evaluating capacity management options like chase demand, level capacity, and demand management.

OPEN BOOK EXAM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

PART B...........................................................................................................................................3

Question 1....................................................................................................................................3

a) Define in relation with law of variability that rising variability always degrade the

performance of a delivery-based system. What are the sources of demand variability

applicable to Glebe farm and how they affect their related results?............................................3

b) Explain buffering mechanisms that are available for identified demand variabilities in Glebe

farm..............................................................................................................................................3

c) Examine which capacity option (chase demand, level capacity and demand management)

that could be and which cannot be an option in relation to reconcile capacity with demand

variation observed in Glebe farm................................................................................................4

d) What sort of factors must Glebe farm owner should consider while deciding the quantity of

flavours from 5-10.......................................................................................................................5

PART C: FINANCIAL MANAGEMENT......................................................................................6

Question 2....................................................................................................................................6

a) Calculate the following ratios for the years 2020 and 2021....................................................6

b) Comments should include whether each metric is improving or deteriorating versus prior

year and against the standard terms of business for the company if applicable. You should

identify the potential causes/implications of each change...........................................................7

C) You should give an overall opinion on the financial health of the company, based on your

analysis. Is there evidence that the company may not be a ‘going concern’?.............................9

D) Give advice to financial director whether financial statement is sufficient to apply for bank

loan and also describe the limitations of financial record analysis need to be considered:.........9

PART B...........................................................................................................................................3

Question 1....................................................................................................................................3

a) Define in relation with law of variability that rising variability always degrade the

performance of a delivery-based system. What are the sources of demand variability

applicable to Glebe farm and how they affect their related results?............................................3

b) Explain buffering mechanisms that are available for identified demand variabilities in Glebe

farm..............................................................................................................................................3

c) Examine which capacity option (chase demand, level capacity and demand management)

that could be and which cannot be an option in relation to reconcile capacity with demand

variation observed in Glebe farm................................................................................................4

d) What sort of factors must Glebe farm owner should consider while deciding the quantity of

flavours from 5-10.......................................................................................................................5

PART C: FINANCIAL MANAGEMENT......................................................................................6

Question 2....................................................................................................................................6

a) Calculate the following ratios for the years 2020 and 2021....................................................6

b) Comments should include whether each metric is improving or deteriorating versus prior

year and against the standard terms of business for the company if applicable. You should

identify the potential causes/implications of each change...........................................................7

C) You should give an overall opinion on the financial health of the company, based on your

analysis. Is there evidence that the company may not be a ‘going concern’?.............................9

D) Give advice to financial director whether financial statement is sufficient to apply for bank

loan and also describe the limitations of financial record analysis need to be considered:.........9

PART B

Question 1.

a) Define in relation with law of variability that rising variability always degrade the

performance of a delivery-based system. What are the sources of demand variability

applicable to Glebe farm and how they affect their related results?

Law of variability: It can be explained as a tool that helps to measure to what extent

demand would vary in associated business. It defines the difference between what one

expects to take place and what actually happens. There are many reasons that are

responsible for such variations and which contribute in degrading the functioning of a

system dealing in delivery as well. Sources of demand variability are described below:

Complexity: In Glebe farm case It can be justified as a complicated function that

takes in account whether what is being planned or predicted would give exact

results that are expected and thus what would be related measure that would help

to achieve such goals in area of ice cream and milking factory.

Uncertainty: It can be stated as a situation that is developed through force and

existence of external factors present in market and which would cause demand to

rise or fall unexpectedly. In Glebe farm area there are many local shops available

around that might attract consumer and thus is not necessary that the demand

would rise. In case of milking, it has to manage number of visitors and in case of

ice cream sales it has to increase number of flavours.

Volatility: It can be explained as a alternation and rapid change observed in rise of

unpredictable demand taking place in business related environment. In relation

with Glebe farm it is observed that the demand is expected to rise for certain

flavours that must be met by the business for smooth working and carrying out of

operations and for milking tour it must manage related space required for

increasing visitors.

b) Explain buffering mechanisms that are available for identified demand variabilities in Glebe

farm.

The variation in buffering recorded in delivery systems takes place because of mixtures of

inventory, capacity and time. The buffering here states the unpredictable increment or decrement

Question 1.

a) Define in relation with law of variability that rising variability always degrade the

performance of a delivery-based system. What are the sources of demand variability

applicable to Glebe farm and how they affect their related results?

Law of variability: It can be explained as a tool that helps to measure to what extent

demand would vary in associated business. It defines the difference between what one

expects to take place and what actually happens. There are many reasons that are

responsible for such variations and which contribute in degrading the functioning of a

system dealing in delivery as well. Sources of demand variability are described below:

Complexity: In Glebe farm case It can be justified as a complicated function that

takes in account whether what is being planned or predicted would give exact

results that are expected and thus what would be related measure that would help

to achieve such goals in area of ice cream and milking factory.

Uncertainty: It can be stated as a situation that is developed through force and

existence of external factors present in market and which would cause demand to

rise or fall unexpectedly. In Glebe farm area there are many local shops available

around that might attract consumer and thus is not necessary that the demand

would rise. In case of milking, it has to manage number of visitors and in case of

ice cream sales it has to increase number of flavours.

Volatility: It can be explained as a alternation and rapid change observed in rise of

unpredictable demand taking place in business related environment. In relation

with Glebe farm it is observed that the demand is expected to rise for certain

flavours that must be met by the business for smooth working and carrying out of

operations and for milking tour it must manage related space required for

increasing visitors.

b) Explain buffering mechanisms that are available for identified demand variabilities in Glebe

farm.

The variation in buffering recorded in delivery systems takes place because of mixtures of

inventory, capacity and time. The buffering here states the unpredictable increment or decrement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in demand are related to goods that can be captivated by keeping a hold of buffer or new quantity

of commodity. There are various kind of buffering mechanism explained as below:

Time buffering: It simply relates to queue of the related consumers and the visitors as well. It

primarily takes place when there is a occasion or at the time of holiday. The batch size restricts a

limited number of 12 persons for viewing the milking process of cows that results in generation

of inventory and production of stock as well. It can be substituted if frequency rate of batch is

limited and number of visitor gets increased to a level of 80 persons which are able to see cow

milking for a duration of one hour. It would be fruitful for corporate as well as for consumer

would be attracted and visitor will also rise in number. This would result in occupying 100%

capacity of visitors.

Capacity buffering: It hangs on buffering of inventory variation and as the decision expects to

generate more capacity of goods that depends on batch area which must be manufactured in a

larger quantity. The variability in quantity is related to buffering of inventory that states to ignore

capacity buffering, inventory should be at a reducing rate.

Inventory buffering: In area of Glebe farm, the buffering of inventory can be buffered with the

help of delivering raw material that must be processed so that demand of farm related products

could be matched. It can be achieved with the help of variation in internal result of work- in

progress of commodities. Capacity of inventory buffering can be predicted the reason being as

the material and production level can be carried out smoothly only if the required capacity is

met. From the given case study, it can be said that inventory buffering can be reduced by

possessing large amount of raw material and expecting that the number of customers during

holidays will increase according to required capacity and time set.

c) Examine which capacity option (chase demand, level capacity and demand management) that

could be and which cannot be an option in relation to reconcile capacity with demand

variation observed in Glebe farm.

Chase demand: It explains where the capacity is required to be adjusted according to

variation observed in demand cycle. It is useful mainly in service-related industries such

as construction or tourism. Thus, in case of Glebe farm products such as ice cream and

milk factories it is not a beneficial option that can be considered.

Level capacity: It is described as a situation where the decision maker has to decide ways

to meet requirements of consumers at the time of peak durations. Applying it in situation

of commodity. There are various kind of buffering mechanism explained as below:

Time buffering: It simply relates to queue of the related consumers and the visitors as well. It

primarily takes place when there is a occasion or at the time of holiday. The batch size restricts a

limited number of 12 persons for viewing the milking process of cows that results in generation

of inventory and production of stock as well. It can be substituted if frequency rate of batch is

limited and number of visitor gets increased to a level of 80 persons which are able to see cow

milking for a duration of one hour. It would be fruitful for corporate as well as for consumer

would be attracted and visitor will also rise in number. This would result in occupying 100%

capacity of visitors.

Capacity buffering: It hangs on buffering of inventory variation and as the decision expects to

generate more capacity of goods that depends on batch area which must be manufactured in a

larger quantity. The variability in quantity is related to buffering of inventory that states to ignore

capacity buffering, inventory should be at a reducing rate.

Inventory buffering: In area of Glebe farm, the buffering of inventory can be buffered with the

help of delivering raw material that must be processed so that demand of farm related products

could be matched. It can be achieved with the help of variation in internal result of work- in

progress of commodities. Capacity of inventory buffering can be predicted the reason being as

the material and production level can be carried out smoothly only if the required capacity is

met. From the given case study, it can be said that inventory buffering can be reduced by

possessing large amount of raw material and expecting that the number of customers during

holidays will increase according to required capacity and time set.

c) Examine which capacity option (chase demand, level capacity and demand management) that

could be and which cannot be an option in relation to reconcile capacity with demand

variation observed in Glebe farm.

Chase demand: It explains where the capacity is required to be adjusted according to

variation observed in demand cycle. It is useful mainly in service-related industries such

as construction or tourism. Thus, in case of Glebe farm products such as ice cream and

milk factories it is not a beneficial option that can be considered.

Level capacity: It is described as a situation where the decision maker has to decide ways

to meet requirements of consumers at the time of peak durations. Applying it in situation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of Glebe farm it would prove to be fruitful as Gill has to manage visitor place of 80 in

peak hours at peak days and produce more number of flavours for expected rise in scale

of consumers & to increase profit, sale. Thus, it can be considered as an better option that

would help in reconciling capacity in relation with demand variation. It would help to

engage more customers in other areas as well and attract them for increasing profitability

of the business.

Demand management: It is helpful where the demand deals in seasonal products such as

ice cream flavours being produced in Glebe farm that would help to manage demand &

balance its associated customers. Whereas in case of Milking area Gill is expected to

make best use of available resources and manage increasing visitors in peak hours for the

milking tour. It would be helpful in long run and to better fulfil unpredictable needs and

expectations of consumers. Demand can be managed by proper planning and production

in the factory and making best use of available resources.

d) What sort of factors must Glebe farm owner should consider while deciding the quantity of

flavours from 5-10.

While raising the quantity of ice cream flavour for promoting sale is a good idea, the amount

of every flavour to be created is uncertain, and also if or not is of comparable amounts related to

all varieties must be produced. For that concern Glebe farm must understand buying patterns of

customers and how they can be met if an unexpected rise is observed. If in the near future any

new demand for a related product seems to rise and which is not available with them to be

offered to customer it would lead to dissatisfaction and bad impact. It is possible that Glebe farm

records more amount of losses if it produces flavours that are not frequently demanded and are

produced more in quantity. Another hurdle that might affect the farm is whether they have

enough workforce for production and enough funds for carrying out increased operations.

Finally, it can be said that if the demand does not increase, it won’t improve sales and profits will

not rise and inventory might go wasted for a longer duration. Hence, it is necessary for Glebe

farm to plan and handle the idea to increase the quantity of variety carefully that requires only

the investment of ingredients flavoured and no increased staff. It would be helpful if farm

focuses more on making best use of available resources and funds & not increase expense of

carrying out additional operations.

peak hours at peak days and produce more number of flavours for expected rise in scale

of consumers & to increase profit, sale. Thus, it can be considered as an better option that

would help in reconciling capacity in relation with demand variation. It would help to

engage more customers in other areas as well and attract them for increasing profitability

of the business.

Demand management: It is helpful where the demand deals in seasonal products such as

ice cream flavours being produced in Glebe farm that would help to manage demand &

balance its associated customers. Whereas in case of Milking area Gill is expected to

make best use of available resources and manage increasing visitors in peak hours for the

milking tour. It would be helpful in long run and to better fulfil unpredictable needs and

expectations of consumers. Demand can be managed by proper planning and production

in the factory and making best use of available resources.

d) What sort of factors must Glebe farm owner should consider while deciding the quantity of

flavours from 5-10.

While raising the quantity of ice cream flavour for promoting sale is a good idea, the amount

of every flavour to be created is uncertain, and also if or not is of comparable amounts related to

all varieties must be produced. For that concern Glebe farm must understand buying patterns of

customers and how they can be met if an unexpected rise is observed. If in the near future any

new demand for a related product seems to rise and which is not available with them to be

offered to customer it would lead to dissatisfaction and bad impact. It is possible that Glebe farm

records more amount of losses if it produces flavours that are not frequently demanded and are

produced more in quantity. Another hurdle that might affect the farm is whether they have

enough workforce for production and enough funds for carrying out increased operations.

Finally, it can be said that if the demand does not increase, it won’t improve sales and profits will

not rise and inventory might go wasted for a longer duration. Hence, it is necessary for Glebe

farm to plan and handle the idea to increase the quantity of variety carefully that requires only

the investment of ingredients flavoured and no increased staff. It would be helpful if farm

focuses more on making best use of available resources and funds & not increase expense of

carrying out additional operations.

PART C: FINANCIAL MANAGEMENT

Question 2

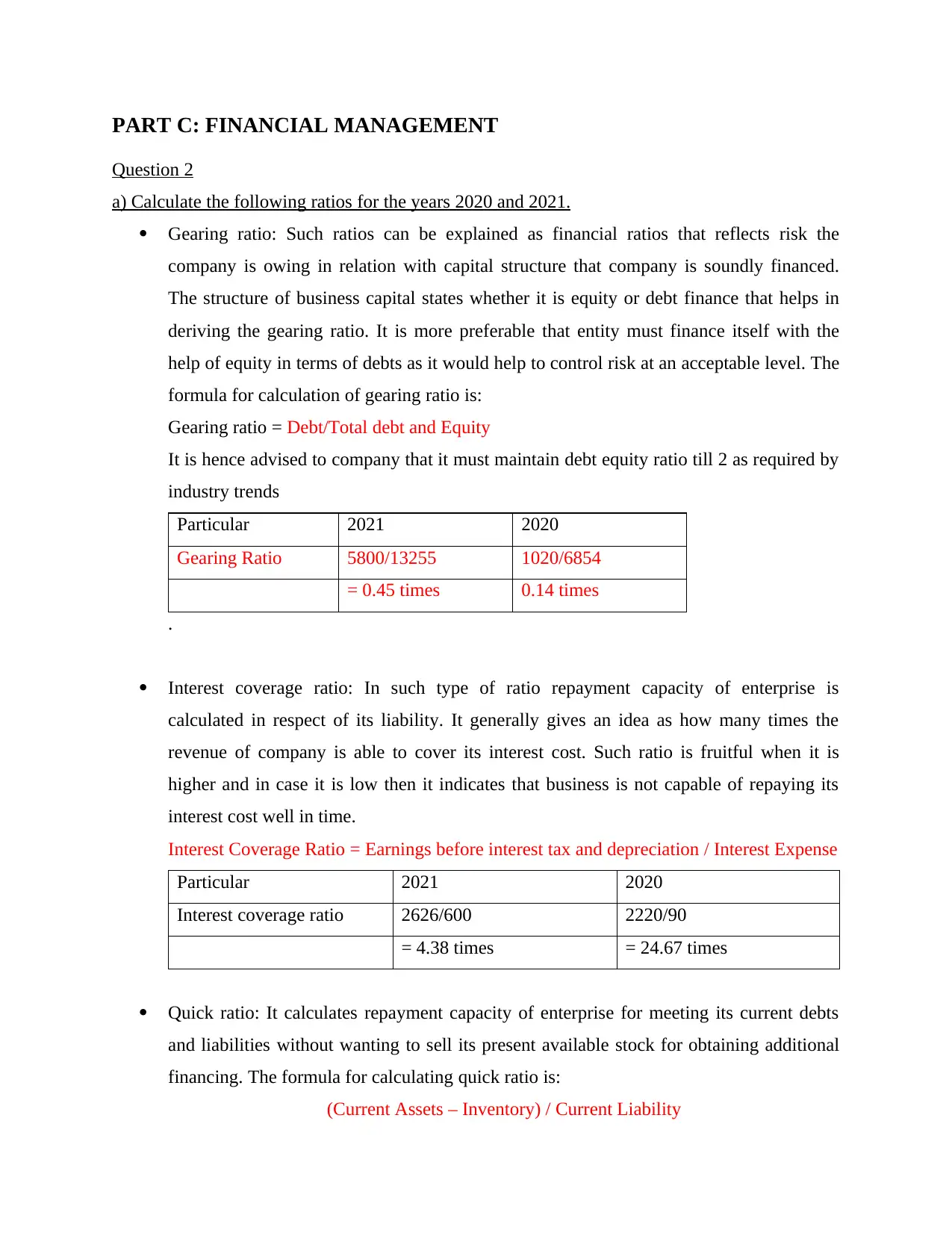

a) Calculate the following ratios for the years 2020 and 2021.

Gearing ratio: Such ratios can be explained as financial ratios that reflects risk the

company is owing in relation with capital structure that company is soundly financed.

The structure of business capital states whether it is equity or debt finance that helps in

deriving the gearing ratio. It is more preferable that entity must finance itself with the

help of equity in terms of debts as it would help to control risk at an acceptable level. The

formula for calculation of gearing ratio is:

Gearing ratio = Debt/Total debt and Equity

It is hence advised to company that it must maintain debt equity ratio till 2 as required by

industry trends

Particular 2021 2020

Gearing Ratio 5800/13255 1020/6854

= 0.45 times 0.14 times

.

Interest coverage ratio: In such type of ratio repayment capacity of enterprise is

calculated in respect of its liability. It generally gives an idea as how many times the

revenue of company is able to cover its interest cost. Such ratio is fruitful when it is

higher and in case it is low then it indicates that business is not capable of repaying its

interest cost well in time.

Interest Coverage Ratio = Earnings before interest tax and depreciation / Interest Expense

Particular 2021 2020

Interest coverage ratio 2626/600 2220/90

= 4.38 times = 24.67 times

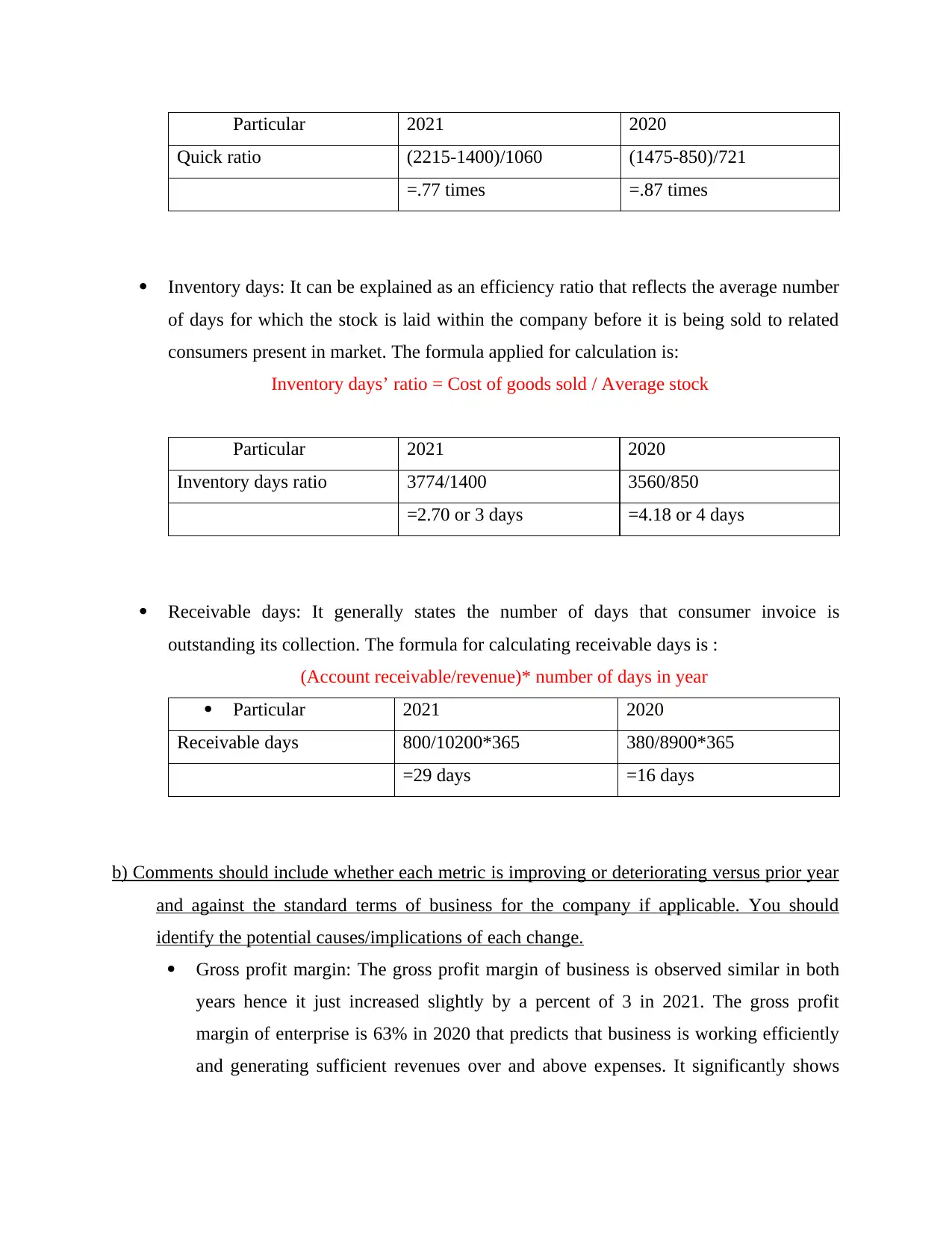

Quick ratio: It calculates repayment capacity of enterprise for meeting its current debts

and liabilities without wanting to sell its present available stock for obtaining additional

financing. The formula for calculating quick ratio is:

(Current Assets – Inventory) / Current Liability

Question 2

a) Calculate the following ratios for the years 2020 and 2021.

Gearing ratio: Such ratios can be explained as financial ratios that reflects risk the

company is owing in relation with capital structure that company is soundly financed.

The structure of business capital states whether it is equity or debt finance that helps in

deriving the gearing ratio. It is more preferable that entity must finance itself with the

help of equity in terms of debts as it would help to control risk at an acceptable level. The

formula for calculation of gearing ratio is:

Gearing ratio = Debt/Total debt and Equity

It is hence advised to company that it must maintain debt equity ratio till 2 as required by

industry trends

Particular 2021 2020

Gearing Ratio 5800/13255 1020/6854

= 0.45 times 0.14 times

.

Interest coverage ratio: In such type of ratio repayment capacity of enterprise is

calculated in respect of its liability. It generally gives an idea as how many times the

revenue of company is able to cover its interest cost. Such ratio is fruitful when it is

higher and in case it is low then it indicates that business is not capable of repaying its

interest cost well in time.

Interest Coverage Ratio = Earnings before interest tax and depreciation / Interest Expense

Particular 2021 2020

Interest coverage ratio 2626/600 2220/90

= 4.38 times = 24.67 times

Quick ratio: It calculates repayment capacity of enterprise for meeting its current debts

and liabilities without wanting to sell its present available stock for obtaining additional

financing. The formula for calculating quick ratio is:

(Current Assets – Inventory) / Current Liability

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particular 2021 2020

Quick ratio (2215-1400)/1060 (1475-850)/721

=.77 times =.87 times

Inventory days: It can be explained as an efficiency ratio that reflects the average number

of days for which the stock is laid within the company before it is being sold to related

consumers present in market. The formula applied for calculation is:

Inventory days’ ratio = Cost of goods sold / Average stock

Particular 2021 2020

Inventory days ratio 3774/1400 3560/850

=2.70 or 3 days =4.18 or 4 days

Receivable days: It generally states the number of days that consumer invoice is

outstanding its collection. The formula for calculating receivable days is :

(Account receivable/revenue)* number of days in year

Particular 2021 2020

Receivable days 800/10200*365 380/8900*365

=29 days =16 days

b) Comments should include whether each metric is improving or deteriorating versus prior year

and against the standard terms of business for the company if applicable. You should

identify the potential causes/implications of each change.

Gross profit margin: The gross profit margin of business is observed similar in both

years hence it just increased slightly by a percent of 3 in 2021. The gross profit

margin of enterprise is 63% in 2020 that predicts that business is working efficiently

and generating sufficient revenues over and above expenses. It significantly shows

Quick ratio (2215-1400)/1060 (1475-850)/721

=.77 times =.87 times

Inventory days: It can be explained as an efficiency ratio that reflects the average number

of days for which the stock is laid within the company before it is being sold to related

consumers present in market. The formula applied for calculation is:

Inventory days’ ratio = Cost of goods sold / Average stock

Particular 2021 2020

Inventory days ratio 3774/1400 3560/850

=2.70 or 3 days =4.18 or 4 days

Receivable days: It generally states the number of days that consumer invoice is

outstanding its collection. The formula for calculating receivable days is :

(Account receivable/revenue)* number of days in year

Particular 2021 2020

Receivable days 800/10200*365 380/8900*365

=29 days =16 days

b) Comments should include whether each metric is improving or deteriorating versus prior year

and against the standard terms of business for the company if applicable. You should

identify the potential causes/implications of each change.

Gross profit margin: The gross profit margin of business is observed similar in both

years hence it just increased slightly by a percent of 3 in 2021. The gross profit

margin of enterprise is 63% in 2020 that predicts that business is working efficiently

and generating sufficient revenues over and above expenses. It significantly shows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

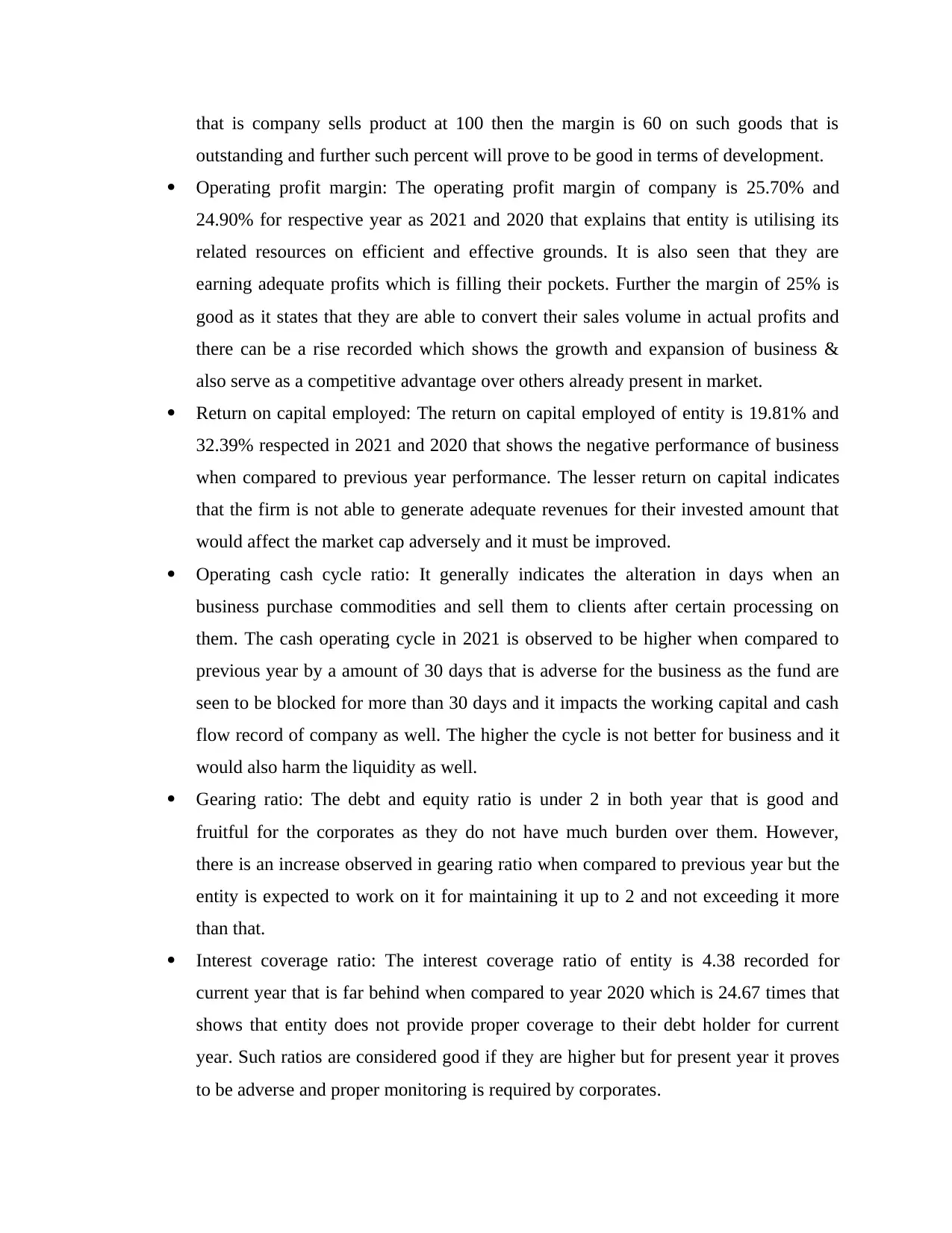

that is company sells product at 100 then the margin is 60 on such goods that is

outstanding and further such percent will prove to be good in terms of development.

Operating profit margin: The operating profit margin of company is 25.70% and

24.90% for respective year as 2021 and 2020 that explains that entity is utilising its

related resources on efficient and effective grounds. It is also seen that they are

earning adequate profits which is filling their pockets. Further the margin of 25% is

good as it states that they are able to convert their sales volume in actual profits and

there can be a rise recorded which shows the growth and expansion of business &

also serve as a competitive advantage over others already present in market.

Return on capital employed: The return on capital employed of entity is 19.81% and

32.39% respected in 2021 and 2020 that shows the negative performance of business

when compared to previous year performance. The lesser return on capital indicates

that the firm is not able to generate adequate revenues for their invested amount that

would affect the market cap adversely and it must be improved.

Operating cash cycle ratio: It generally indicates the alteration in days when an

business purchase commodities and sell them to clients after certain processing on

them. The cash operating cycle in 2021 is observed to be higher when compared to

previous year by a amount of 30 days that is adverse for the business as the fund are

seen to be blocked for more than 30 days and it impacts the working capital and cash

flow record of company as well. The higher the cycle is not better for business and it

would also harm the liquidity as well.

Gearing ratio: The debt and equity ratio is under 2 in both year that is good and

fruitful for the corporates as they do not have much burden over them. However,

there is an increase observed in gearing ratio when compared to previous year but the

entity is expected to work on it for maintaining it up to 2 and not exceeding it more

than that.

Interest coverage ratio: The interest coverage ratio of entity is 4.38 recorded for

current year that is far behind when compared to year 2020 which is 24.67 times that

shows that entity does not provide proper coverage to their debt holder for current

year. Such ratios are considered good if they are higher but for present year it proves

to be adverse and proper monitoring is required by corporates.

outstanding and further such percent will prove to be good in terms of development.

Operating profit margin: The operating profit margin of company is 25.70% and

24.90% for respective year as 2021 and 2020 that explains that entity is utilising its

related resources on efficient and effective grounds. It is also seen that they are

earning adequate profits which is filling their pockets. Further the margin of 25% is

good as it states that they are able to convert their sales volume in actual profits and

there can be a rise recorded which shows the growth and expansion of business &

also serve as a competitive advantage over others already present in market.

Return on capital employed: The return on capital employed of entity is 19.81% and

32.39% respected in 2021 and 2020 that shows the negative performance of business

when compared to previous year performance. The lesser return on capital indicates

that the firm is not able to generate adequate revenues for their invested amount that

would affect the market cap adversely and it must be improved.

Operating cash cycle ratio: It generally indicates the alteration in days when an

business purchase commodities and sell them to clients after certain processing on

them. The cash operating cycle in 2021 is observed to be higher when compared to

previous year by a amount of 30 days that is adverse for the business as the fund are

seen to be blocked for more than 30 days and it impacts the working capital and cash

flow record of company as well. The higher the cycle is not better for business and it

would also harm the liquidity as well.

Gearing ratio: The debt and equity ratio is under 2 in both year that is good and

fruitful for the corporates as they do not have much burden over them. However,

there is an increase observed in gearing ratio when compared to previous year but the

entity is expected to work on it for maintaining it up to 2 and not exceeding it more

than that.

Interest coverage ratio: The interest coverage ratio of entity is 4.38 recorded for

current year that is far behind when compared to year 2020 which is 24.67 times that

shows that entity does not provide proper coverage to their debt holder for current

year. Such ratios are considered good if they are higher but for present year it proves

to be adverse and proper monitoring is required by corporates.

Quick Ratio: In 2021 and 2020, the company quick ratio will be 0.77 and 0.87 times,

respectively, implying essentially identical profitability in both years. If it is less than

working capital, it simply signifies that assets are not dependent on stocks and that

the company is spending its spare money in more income-generating sources.

Inventory Ratio: Businesses should keep their inventory as low as possible. It

basically means that the company will transfer its shares on a regular basis. In the

example above, inventory turnover is 3 and 4, which is advantageous to the entity's

welfare and therefore should be kept as low as reasonably achievable.

Receivable Days: The trade receivables in 2021 and 2020 are 29 and 16, respectively,

showing that revenues received by the firm are taking longer this year, impacting its

liquid assets in comparison to previous years, which must be addressed given the

company's prior performance.

C) You should give an overall opinion on the financial health of the company, based on your

analysis. Is there evidence that the company may not be a ‘going concern’?

The health of the company can be predicted better and sound that can be improved because

from the analysis of above defined ratios the gearing ratio can be said to be under control that

simply indicates that company does not have enough liability and debt the reason being they are

sound and have equity finance on a large scale. Further, the profitability and liquidity of

corporates can be seen improving and in a good manner that helps to understand that company at

given point of time is working well.

D) Give advice to financial director whether financial statement is sufficient to apply for bank

loan and also describe the limitations of financial record analysis need to be considered:

From the above analysis of profitability and examining performance of organisation it

can be said that entity can easily apply and receive loan amount from banks/ financial

institutions. The reason behind is that their gearing and liquidity ratio are in enough amount for

processing of loan. The limitation of financial statements is:

It is prepared on historical cost basis and exact value cannot be calculated.

It ignores the effect of all non-monetary related aspects.

They do not give any correct positioning of business in market point of view.

respectively, implying essentially identical profitability in both years. If it is less than

working capital, it simply signifies that assets are not dependent on stocks and that

the company is spending its spare money in more income-generating sources.

Inventory Ratio: Businesses should keep their inventory as low as possible. It

basically means that the company will transfer its shares on a regular basis. In the

example above, inventory turnover is 3 and 4, which is advantageous to the entity's

welfare and therefore should be kept as low as reasonably achievable.

Receivable Days: The trade receivables in 2021 and 2020 are 29 and 16, respectively,

showing that revenues received by the firm are taking longer this year, impacting its

liquid assets in comparison to previous years, which must be addressed given the

company's prior performance.

C) You should give an overall opinion on the financial health of the company, based on your

analysis. Is there evidence that the company may not be a ‘going concern’?

The health of the company can be predicted better and sound that can be improved because

from the analysis of above defined ratios the gearing ratio can be said to be under control that

simply indicates that company does not have enough liability and debt the reason being they are

sound and have equity finance on a large scale. Further, the profitability and liquidity of

corporates can be seen improving and in a good manner that helps to understand that company at

given point of time is working well.

D) Give advice to financial director whether financial statement is sufficient to apply for bank

loan and also describe the limitations of financial record analysis need to be considered:

From the above analysis of profitability and examining performance of organisation it

can be said that entity can easily apply and receive loan amount from banks/ financial

institutions. The reason behind is that their gearing and liquidity ratio are in enough amount for

processing of loan. The limitation of financial statements is:

It is prepared on historical cost basis and exact value cannot be calculated.

It ignores the effect of all non-monetary related aspects.

They do not give any correct positioning of business in market point of view.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.