Operations Management: Bottom Up Pricing and Dynamic Pricing Methods

VerifiedAdded on 2023/06/15

|10

|2351

|449

AI Summary

This report discusses the bottom up pricing and dynamic pricing methods in operations management. It explains the steps involved in the bottom up pricing method and factors affecting it. It also compares the advantages and disadvantages of both methods. The report is relevant for students studying operations management and related courses. No specific course code, course name, or college/university is mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

LEVEL 2 UNIT 7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

Bottom up pricing techniques.................................................................................................................3

Factors affect to bottom up pricing.........................................................................................................4

PART B.........................................................................................................................................................5

Compare the advantages and disadvantages of the following approaches to setting room rates..........5

CONCLUSION...............................................................................................................................................8

REFERENCES................................................................................................................................................9

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

Bottom up pricing techniques.................................................................................................................3

Factors affect to bottom up pricing.........................................................................................................4

PART B.........................................................................................................................................................5

Compare the advantages and disadvantages of the following approaches to setting room rates..........5

CONCLUSION...............................................................................................................................................8

REFERENCES................................................................................................................................................9

INTRODUCTION

The administration of business activities to achieve the best degree of effectiveness feasible

inside an organisation is known as operations management (OM). It is focused with effectively

transforming factors of production into products or services in order to maximize a firm's profit

(Luengalongkot, 2021). The goal of operational top management is to produce the largest net

operational profit achievable by balancing expenses and income. In this report consist of bottom

up pricing method and dynamic pricing method with their advantage and disadvantage.

PART A

Bottom up pricing techniques

The average room rate can be worked given below:

Pricing rooms is done from the ground up. To establish the average rate per room, this method

takes into account operational costs, projected profits, and the expected number of rooms sold.

Since its first item – net income (profit) – shows at the bottom of the distribution, it is termed a

bottom-up strategy. There are following these steps for the proper calculation:

1. Calculate hotel desired profit by multiplying the desired rate of return by the owner’s

investment

= 18, 00,000 * 5%

= 90000

2. Calculate pretax profits by dividing desired profits by minus the hotel tax rate

= 90000 / 1-20%

= 90000 / 0.8

= 112500

3. Calculate fixed charges and management fees

The administration of business activities to achieve the best degree of effectiveness feasible

inside an organisation is known as operations management (OM). It is focused with effectively

transforming factors of production into products or services in order to maximize a firm's profit

(Luengalongkot, 2021). The goal of operational top management is to produce the largest net

operational profit achievable by balancing expenses and income. In this report consist of bottom

up pricing method and dynamic pricing method with their advantage and disadvantage.

PART A

Bottom up pricing techniques

The average room rate can be worked given below:

Pricing rooms is done from the ground up. To establish the average rate per room, this method

takes into account operational costs, projected profits, and the expected number of rooms sold.

Since its first item – net income (profit) – shows at the bottom of the distribution, it is termed a

bottom-up strategy. There are following these steps for the proper calculation:

1. Calculate hotel desired profit by multiplying the desired rate of return by the owner’s

investment

= 18, 00,000 * 5%

= 90000

2. Calculate pretax profits by dividing desired profits by minus the hotel tax rate

= 90000 / 1-20%

= 90000 / 0.8

= 112500

3. Calculate fixed charges and management fees

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

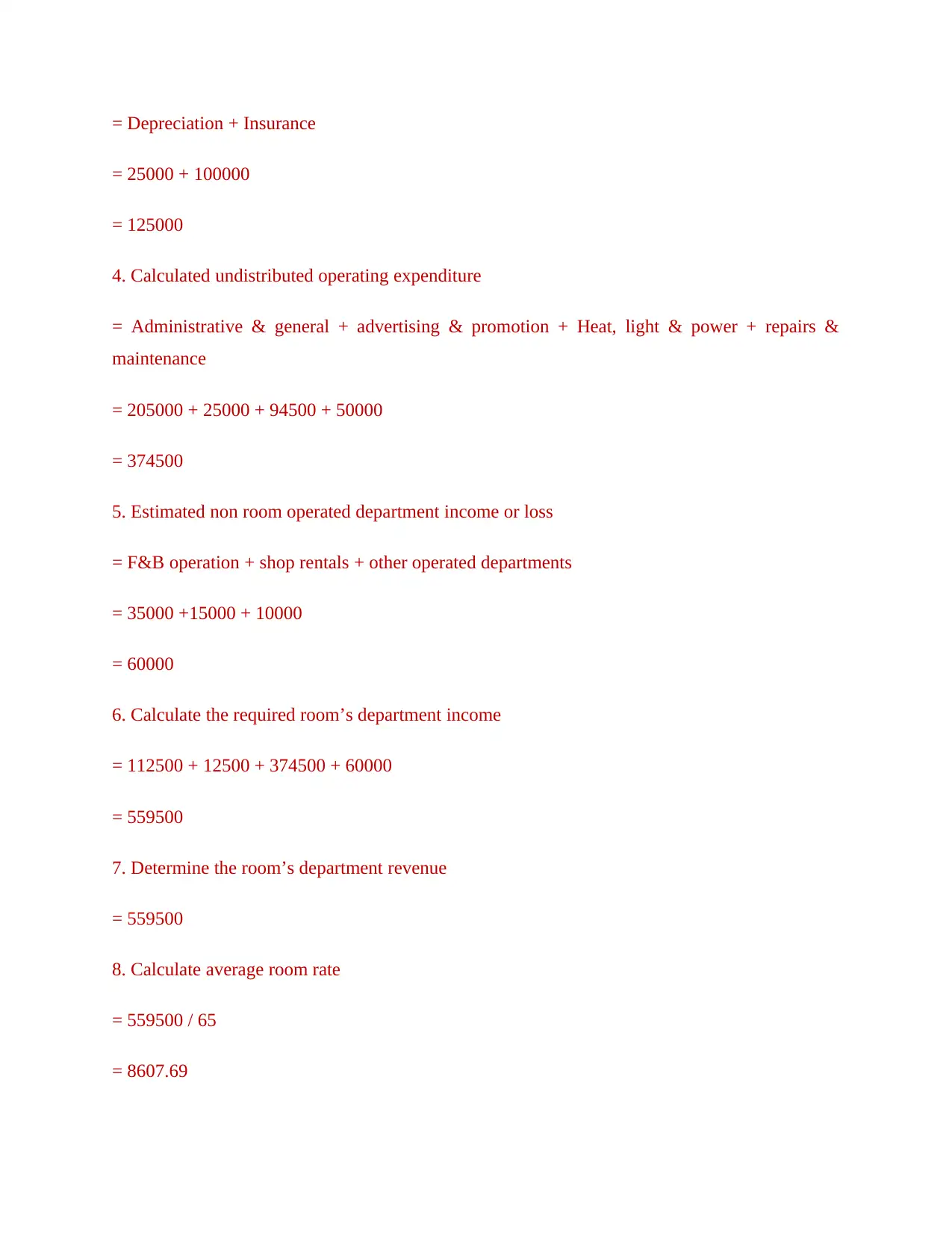

= Depreciation + Insurance

= 25000 + 100000

= 125000

4. Calculated undistributed operating expenditure

= Administrative & general + advertising & promotion + Heat, light & power + repairs &

maintenance

= 205000 + 25000 + 94500 + 50000

= 374500

5. Estimated non room operated department income or loss

= F&B operation + shop rentals + other operated departments

= 35000 +15000 + 10000

= 60000

6. Calculate the required room’s department income

= 112500 + 12500 + 374500 + 60000

= 559500

7. Determine the room’s department revenue

= 559500

8. Calculate average room rate

= 559500 / 65

= 8607.69

= 25000 + 100000

= 125000

4. Calculated undistributed operating expenditure

= Administrative & general + advertising & promotion + Heat, light & power + repairs &

maintenance

= 205000 + 25000 + 94500 + 50000

= 374500

5. Estimated non room operated department income or loss

= F&B operation + shop rentals + other operated departments

= 35000 +15000 + 10000

= 60000

6. Calculate the required room’s department income

= 112500 + 12500 + 374500 + 60000

= 559500

7. Determine the room’s department revenue

= 559500

8. Calculate average room rate

= 559500 / 65

= 8607.69

From the above calculation it is determined that there are different factors that affect to

bottom up pricing method like pretax profit, average room revenue, fixed charges and

management fees, undistributed operating expenses and many others.

Factors affect to bottom up pricing

Cost allocation: The cost allocation is one of the most difficult aspects of bottom-up pricing.

There are a few expenses that are not borne by the people who pay for the things or service. In

such circumstances, rather of using a straight line technique in which all expenses are evenly

distributed across all programmes, the corporation uses a more sophisticated strategy in which

costs are allocated correctly to various programmers and persons. The drawback of this method

is that these additional activities, which may help the community, often die out because they are

unable to recoup their costs. Not only for the programme, but bottom-up charging in general isn't

always a smart idea in terms of cost-recovery when compared to top-down pricing (Endiana and

et.al, 2020).

Cost structure: Every business has a unique cost structure depending on the various aspects

involved, such as labour, administration, marketing expenses, and paper products. All expenses

are first categorised as overhead expenses, after which the value of each element is computed.

First from sum of the foregoing, the entire cost is determined and translated to an unit price. The

intended profit is then applied to the entire cost, yielding the final number, which is the amount

that the customer will pay. In this approach, meticulously assessing expenses will reveal what

costs to cut while prices are low, allowing the price to be adjusted constantly.

PART B

Compare the advantages and disadvantages of the following approaches to setting room rates

Bottom up pricing using a cost base: Cost-based pricing is a tried-and-true method of earning

consistent revenue. This model is used by businesses to increase their bottom line and distinguish

oneself, and it is effective. For example, Everlane employs a cost-based pricing approach to set

itself apart from its competition, and its income has increased year after year with no signs of

slowing down. The simplest approach to figure out how much a thing should cost is to use price

pricing. There are two types of full-cost pricing: full-cost high prices and straightforward sales

prices. Variable and fixed costs, as well as a percent markup, are all factored into full cost price.

bottom up pricing method like pretax profit, average room revenue, fixed charges and

management fees, undistributed operating expenses and many others.

Factors affect to bottom up pricing

Cost allocation: The cost allocation is one of the most difficult aspects of bottom-up pricing.

There are a few expenses that are not borne by the people who pay for the things or service. In

such circumstances, rather of using a straight line technique in which all expenses are evenly

distributed across all programmes, the corporation uses a more sophisticated strategy in which

costs are allocated correctly to various programmers and persons. The drawback of this method

is that these additional activities, which may help the community, often die out because they are

unable to recoup their costs. Not only for the programme, but bottom-up charging in general isn't

always a smart idea in terms of cost-recovery when compared to top-down pricing (Endiana and

et.al, 2020).

Cost structure: Every business has a unique cost structure depending on the various aspects

involved, such as labour, administration, marketing expenses, and paper products. All expenses

are first categorised as overhead expenses, after which the value of each element is computed.

First from sum of the foregoing, the entire cost is determined and translated to an unit price. The

intended profit is then applied to the entire cost, yielding the final number, which is the amount

that the customer will pay. In this approach, meticulously assessing expenses will reveal what

costs to cut while prices are low, allowing the price to be adjusted constantly.

PART B

Compare the advantages and disadvantages of the following approaches to setting room rates

Bottom up pricing using a cost base: Cost-based pricing is a tried-and-true method of earning

consistent revenue. This model is used by businesses to increase their bottom line and distinguish

oneself, and it is effective. For example, Everlane employs a cost-based pricing approach to set

itself apart from its competition, and its income has increased year after year with no signs of

slowing down. The simplest approach to figure out how much a thing should cost is to use price

pricing. There are two types of full-cost pricing: full-cost high prices and straightforward sales

prices. Variable and fixed costs, as well as a percent markup, are all factored into full cost price.

Variable expenses plus a percent markup make up straightforward prices. Cost-plus pricing is a

profit-maximizing pricing strategy employed by businesses. The enterprises achieve their profit

maximization goal by raising output until marginal income matches marginal cost, after which

they charge a price specified by the quantity demanded. Cost-plus pricing is popular since it is

simple to compute and needs minimal data (Zawawi and Hoque, 2020).

Advantage:

Predict earnings: One of the main benefits of the lowest pricing is that it enables the

company to forecast revenues from good or service transactions. Because the selling cost

of a good or service is controlled by the profit margin, users can simply predict however

much money they will make and adjust their calculations. However, enterprises must

guarantee that its product satisfies sales goals in order to generate the profitability.

Work Engagement: One of the advantages of the low-cost approach is work

engagement. Because employee pay is clearly linked to product or service sales, it will

interest workers with the brand and generate additional selling. This will maintain

personnel on line and revenues moving forward. Whenever a good or brand generates

highly engaged and pleasure from the ground up, it will keep the business alive again for

long haul and produce revenues (Diab, 2021).

Disadvantage:

Initial investment: Just like any other firm, entrepreneurs must make an initial

investment to get their venture off the ground. However, if they intend to use the bottom-

up technique, they must guarantee that the good or brand can generate sufficient revenues

and profits. If the expected sales are not achieved, the firm may suffer a loss.

Generating selling - For the lowest pricing, it's critical to make sales according to the

strategy. As previously said, significant money was invested in product development; yet,

if the expected sales numbers are not attained, the firm may suffer a setback. Particularly

whenever the corporation is providing a consumer incentive, such as a free product. As a

result, before implementing the cheapest pricing plan, the company must first determine

whether it is possible (Makvandi and Amirnejad, 2021).

profit-maximizing pricing strategy employed by businesses. The enterprises achieve their profit

maximization goal by raising output until marginal income matches marginal cost, after which

they charge a price specified by the quantity demanded. Cost-plus pricing is popular since it is

simple to compute and needs minimal data (Zawawi and Hoque, 2020).

Advantage:

Predict earnings: One of the main benefits of the lowest pricing is that it enables the

company to forecast revenues from good or service transactions. Because the selling cost

of a good or service is controlled by the profit margin, users can simply predict however

much money they will make and adjust their calculations. However, enterprises must

guarantee that its product satisfies sales goals in order to generate the profitability.

Work Engagement: One of the advantages of the low-cost approach is work

engagement. Because employee pay is clearly linked to product or service sales, it will

interest workers with the brand and generate additional selling. This will maintain

personnel on line and revenues moving forward. Whenever a good or brand generates

highly engaged and pleasure from the ground up, it will keep the business alive again for

long haul and produce revenues (Diab, 2021).

Disadvantage:

Initial investment: Just like any other firm, entrepreneurs must make an initial

investment to get their venture off the ground. However, if they intend to use the bottom-

up technique, they must guarantee that the good or brand can generate sufficient revenues

and profits. If the expected sales are not achieved, the firm may suffer a loss.

Generating selling - For the lowest pricing, it's critical to make sales according to the

strategy. As previously said, significant money was invested in product development; yet,

if the expected sales numbers are not attained, the firm may suffer a setback. Particularly

whenever the corporation is providing a consumer incentive, such as a free product. As a

result, before implementing the cheapest pricing plan, the company must first determine

whether it is possible (Makvandi and Amirnejad, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dynamic based pricing based what the market will bear: Dynamic pricing is a sort of

differential pricing that strives to identify the best price level at any given time. Price fluctuations

can be influenced by a consumer point of view of how much they are prepared to spend for a

product at a given moment, better price, as well as other factors. Dynamic pricing, also known as

higher fares, demanding pricing, or time-based selling prices, is a valuation approach in which

companies establish variable pricing for account of growing demand on market requirements.

Advantage:

Higher profile and sales: Dynamic pricing is extremely beneficial since it includes

additional more as offering more. They may utilize pricing structure to raise prices on

items where desire has increased, resulting in greater profitability. This, however, is the

best use, and pricing structure may effectively improve either profitability or revenue.

Adjusting the competition: Dynamic pricing can let effortlessly outperform the

competitors. Because of price changes, it may consider their consumers' buying habits

into account to give a great service at a reduced price than their competition. It involves

bringing in almost just clients; it also enhances revenue, especially when there are many

rivals in the marketplace (Adiputra and Sujana, 2021).

Flexibility: Firm will benefit from dynamic pricing since it will maintain profitability.

This offers the ability and flexibility to concentrate on other elements of their

organization. Dynamic pricing concentrates on diverse revenue streams while also

making even through the worst of circumstances. Such mobility and independence may

often make or destroy a company's operations.

Better inventory management: Dynamic pricing aids indirectly inventory tracking by

allowing businesses to offer reductions for oversupplied materials in order to reduce their

quantities, or to make a lot more money for higher need commodities in order to keep the

distribution network running whilst generating more money. This aids in sustaining stock

levels under the most difficult of circumstances (Plaskova, Prodanova and Reshetov,

2020).

Disadvantage:

differential pricing that strives to identify the best price level at any given time. Price fluctuations

can be influenced by a consumer point of view of how much they are prepared to spend for a

product at a given moment, better price, as well as other factors. Dynamic pricing, also known as

higher fares, demanding pricing, or time-based selling prices, is a valuation approach in which

companies establish variable pricing for account of growing demand on market requirements.

Advantage:

Higher profile and sales: Dynamic pricing is extremely beneficial since it includes

additional more as offering more. They may utilize pricing structure to raise prices on

items where desire has increased, resulting in greater profitability. This, however, is the

best use, and pricing structure may effectively improve either profitability or revenue.

Adjusting the competition: Dynamic pricing can let effortlessly outperform the

competitors. Because of price changes, it may consider their consumers' buying habits

into account to give a great service at a reduced price than their competition. It involves

bringing in almost just clients; it also enhances revenue, especially when there are many

rivals in the marketplace (Adiputra and Sujana, 2021).

Flexibility: Firm will benefit from dynamic pricing since it will maintain profitability.

This offers the ability and flexibility to concentrate on other elements of their

organization. Dynamic pricing concentrates on diverse revenue streams while also

making even through the worst of circumstances. Such mobility and independence may

often make or destroy a company's operations.

Better inventory management: Dynamic pricing aids indirectly inventory tracking by

allowing businesses to offer reductions for oversupplied materials in order to reduce their

quantities, or to make a lot more money for higher need commodities in order to keep the

distribution network running whilst generating more money. This aids in sustaining stock

levels under the most difficult of circumstances (Plaskova, Prodanova and Reshetov,

2020).

Disadvantage:

Customer dissatisfaction: People who buy a same thing at random times end up having to

pay more than another, thanks to dynamic pricing on items. Consumers who have to pay

a greater price are usually irritated by this. Dynamic pricing has two sides: the client who

received the identical goods for a lower price may start trusting their brand. However,

individuals on the opposite end of the spectrum may become antagonistic to their

organisation, lowering your brand's reputation and image.

Loss of sales: Although dynamic pricing might help them to increase profitability and

growing sales, it can also result in the loss of revenue and consumers though not handled

effectively. They will not benefit from adopting dynamic pricing if a buyer comes across

the equivalent job but priced much lower by some other vendor (Pattnaik and et.al, 2020).

Gaming the system: Consumers are more technologically sophisticated than ever before.

They've devised techniques and tools to assist people cope with fluctuating pricing the

services and applications present buyers with a list of costs for the same goods from

several merchants. This allows consumers to discover the best discounts and undermines

all of the measures in place for client retention because they don't care about just the

product anymore - only the price. Customers know that corporations utilize variable

pricing systems to establish their prices; therefore they employ inventive techniques

including such utilizing private websites for market work to reduce the quantity of data

acquired. This aids in the rejection of variable pricing systems, which function by rising

prices on things as search volume increases (Thottoli, 2020).

CONCLUSION

The use of resources such as people, resources, technology, and technologies is part of

operations management. Management teams buy, create, and supply items to customers

depending on the demands of the customer and the company's capabilities. Operations

management is responsible for a wide range of strategic concerns, such as defining the size of

production facilities, program standard operating procedures, and the layout of information

systems. Additional operational concerns include stock control, particularly employment and raw

material levels.

pay more than another, thanks to dynamic pricing on items. Consumers who have to pay

a greater price are usually irritated by this. Dynamic pricing has two sides: the client who

received the identical goods for a lower price may start trusting their brand. However,

individuals on the opposite end of the spectrum may become antagonistic to their

organisation, lowering your brand's reputation and image.

Loss of sales: Although dynamic pricing might help them to increase profitability and

growing sales, it can also result in the loss of revenue and consumers though not handled

effectively. They will not benefit from adopting dynamic pricing if a buyer comes across

the equivalent job but priced much lower by some other vendor (Pattnaik and et.al, 2020).

Gaming the system: Consumers are more technologically sophisticated than ever before.

They've devised techniques and tools to assist people cope with fluctuating pricing the

services and applications present buyers with a list of costs for the same goods from

several merchants. This allows consumers to discover the best discounts and undermines

all of the measures in place for client retention because they don't care about just the

product anymore - only the price. Customers know that corporations utilize variable

pricing systems to establish their prices; therefore they employ inventive techniques

including such utilizing private websites for market work to reduce the quantity of data

acquired. This aids in the rejection of variable pricing systems, which function by rising

prices on things as search volume increases (Thottoli, 2020).

CONCLUSION

The use of resources such as people, resources, technology, and technologies is part of

operations management. Management teams buy, create, and supply items to customers

depending on the demands of the customer and the company's capabilities. Operations

management is responsible for a wide range of strategic concerns, such as defining the size of

production facilities, program standard operating procedures, and the layout of information

systems. Additional operational concerns include stock control, particularly employment and raw

material levels.

REFERENCES

Books and Journal

Luengalongkot, P., 2021. FACTORS RELATED TO ACHIEVEMENT OF THE

OPERATIONAL GOALS. Academy of Accounting and Financial Studies Journal. 25.

pp.1-11.

Endiana, I. and et.al, 2020. The effect of green accounting on corporate sustainability and

financial performance. The Journal Of Asian Finance, Economics, And Business. 7(12).

pp.731-738.

Zawawi, N. H. M. and Hoque, Z., 2020. Network control and balanced scorecard as inscriptions

in purchaser–provider arrangements: insights from a hybrid government

agency. Accounting, Auditing & Accountability Journal.

Diab, A. A., 2021. The appearance of community logics in management accounting and control:

Evidence from an Egyptian sugar beet village. Critical Perspectives on Accounting. 79.

p.102084.

Makvandi, F. and Amirnejad, G., 2021. Designing a coaching model for operational managers of

Persian Gulf Petrochemical Company in order to motivate human resources. Quarterly

Journal of Training and Development of Human Resources. 29(29). p.0.

Adiputra, I. M. P. and Sujana, E., 2021. Management Control Systems, Organizational Culture

and Village Credit Institution Financial Performance. The Indonesian Journal of

Accounting Research. 24(1).

Plaskova, N. S., Prodanova, N. A. and Reshetov, K. Y., 2020. Dealing operations as a means of

improving the efficiency of the financial management of a production company.

In Complex Systems: Innovation and Sustainability in the Digital Age (pp. 61-70).

Springer, Cham.

Pattnaik, D. and et.al, 2020. Trade credit research before and after the global financial crisis of

2008–A bibliometric overview. Research in International Business and Finance,

p.101287.

Thottoli, M. M., 2020. Knowledge and use of accounting software: evidence from

Oman. Journal of Industry-University Collaboration.

Books and Journal

Luengalongkot, P., 2021. FACTORS RELATED TO ACHIEVEMENT OF THE

OPERATIONAL GOALS. Academy of Accounting and Financial Studies Journal. 25.

pp.1-11.

Endiana, I. and et.al, 2020. The effect of green accounting on corporate sustainability and

financial performance. The Journal Of Asian Finance, Economics, And Business. 7(12).

pp.731-738.

Zawawi, N. H. M. and Hoque, Z., 2020. Network control and balanced scorecard as inscriptions

in purchaser–provider arrangements: insights from a hybrid government

agency. Accounting, Auditing & Accountability Journal.

Diab, A. A., 2021. The appearance of community logics in management accounting and control:

Evidence from an Egyptian sugar beet village. Critical Perspectives on Accounting. 79.

p.102084.

Makvandi, F. and Amirnejad, G., 2021. Designing a coaching model for operational managers of

Persian Gulf Petrochemical Company in order to motivate human resources. Quarterly

Journal of Training and Development of Human Resources. 29(29). p.0.

Adiputra, I. M. P. and Sujana, E., 2021. Management Control Systems, Organizational Culture

and Village Credit Institution Financial Performance. The Indonesian Journal of

Accounting Research. 24(1).

Plaskova, N. S., Prodanova, N. A. and Reshetov, K. Y., 2020. Dealing operations as a means of

improving the efficiency of the financial management of a production company.

In Complex Systems: Innovation and Sustainability in the Digital Age (pp. 61-70).

Springer, Cham.

Pattnaik, D. and et.al, 2020. Trade credit research before and after the global financial crisis of

2008–A bibliometric overview. Research in International Business and Finance,

p.101287.

Thottoli, M. M., 2020. Knowledge and use of accounting software: evidence from

Oman. Journal of Industry-University Collaboration.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.