Investments: Portfolio Analysis, CAPM and Fama-French Report

VerifiedAdded on 2022/09/28

|6

|1070

|24

Report

AI Summary

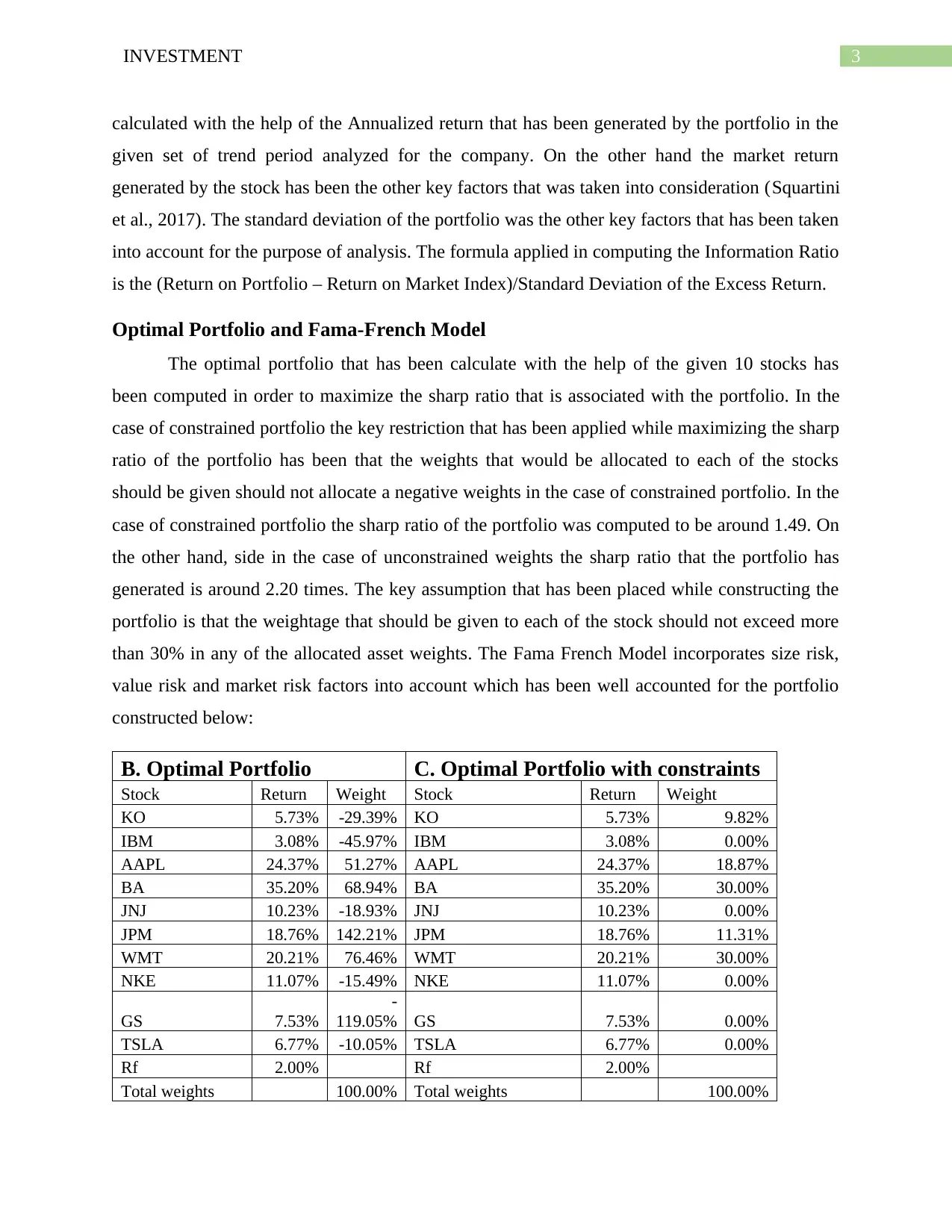

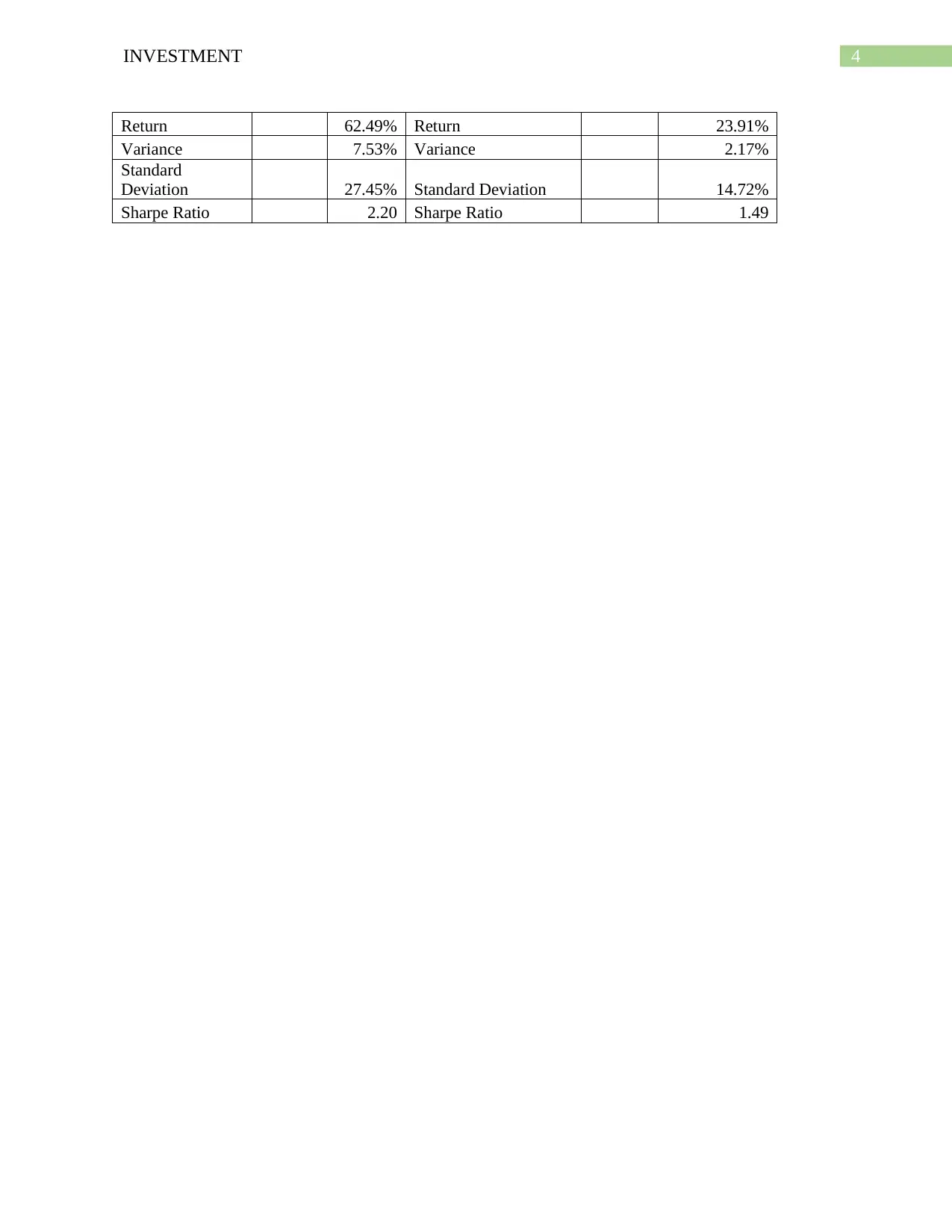

This report provides a comprehensive analysis of an investment portfolio, addressing the key aspects of portfolio construction and optimization. It begins with an overview of the Capital Asset Pricing Model (CAPM) and its application in determining the expected rate of return for stocks. The report then delves into the construction of an optimal portfolio, emphasizing the importance of weight allocation and the maximization of the Sharpe ratio. The analysis includes the construction of portfolios with and without constraints, considering factors such as risk and return, and incorporating the Fama-French model to account for size, value, and market risk factors. The report presents the optimal portfolio weights and returns, along with a comparative analysis of constrained and unconstrained portfolios, providing valuable insights into investment strategies and portfolio management.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.