Optimal Investment Portfolio Analysis: Accounting 2 Project

VerifiedAdded on 2023/06/11

|11

|3323

|463

Report

AI Summary

This report presents an analysis of investment portfolios tailored for both risk-averse and high-risk tolerance investors, utilizing data from the UK market. It outlines the choices made in creating these portfolios, grounded in modern portfolio theory, and compares their performance based on risk and return. The report details the allocation strategies, with a risk-averse portfolio focusing on minimizing beta and a high-risk portfolio prioritizing return. Performance is evaluated using the Capital Asset Pricing Model (CAPM) to determine expected returns, highlighting the trade-offs between risk and return for each portfolio type. The analysis concludes with a recommendation based on investor preferences, emphasizing that risk-averse investors should prioritize the lower-risk portfolio despite its lower return, while risk-tolerant investors should opt for the higher-return portfolio despite its increased risk. Desklib offers a wealth of similar resources, including past papers and solved assignments, to support students in their studies.

Running Head: Accounting

1

Project Report: Accounting

1

Project Report: Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting

2

Contents

Introduction.......................................................................................................................3

Portfolio overview............................................................................................................3

Optimal portfolio and the performance of the portfolio...................................................5

Recommendation and conclusion.....................................................................................9

References.......................................................................................................................10

2

Contents

Introduction.......................................................................................................................3

Portfolio overview............................................................................................................3

Optimal portfolio and the performance of the portfolio...................................................5

Recommendation and conclusion.....................................................................................9

References.......................................................................................................................10

Accounting

3

Introduction:

Portfolio management is an art and science which is used to make decision about the

investment into few securities to manage the risk and return. This portfolio management

process is used to match the investment objective, asset allocation etc for institutions and

individuals and maintain the risk against performance. The overall aim of the portfolio

management is to determine strength, opportunities, threats and weakness of the debts,

equity, domestic shares, international shares, safety, growth etc to attempt to minimize the

risk and maximize the return (Zimmerman and Yahya-Zadeh, 2011).

In the report, the optimal portfolios have been prepared on the basis of the risk and

return. On the basis of the given data, 2 portfolios have been prepared. One portfolio focuses

on the risk-averse investors and other focuses on the high risk tolerance. In the given report,

the performance of both the portfolios has been measured to identify the position of the firms

and the overall returns from the portfolios. For evaluating the risk position and the return of

the assets, equity and debt, FTSE 250 index price has been taken into the concern.

Portfolio overview:

Portfolio is a collection of investment which is all owned by the same investor,

individual or an organization. Normally, these portfolios include stocks, bonds, investment in

individual businesses, government securities, mutual funds, debt etc to reduce the risk level

and manage the return from the overall investment of the individual (William et al, 2015). A

portfolio is prepared in such a way that if one stock is offering the negative result than other

stock, bond or other securities overcome that risk and loss of the individual.

The portfolio explains that all the amount must be invested into different securities so

that the risk could be diversified and a portfolio manger must assures that the investment is

done in the different venture. In the given case, the 3 different firms of UK market have been

taken for the purpose of portfolio. The risk and return of all the firms have been calculated

firstly to make an optimal capital structure for the risk-averse investors and other focuses on

the high risk tolerance.

The risk-averse investors are those individuals or the organization that prefer to take

lower return for the portfolio with known risk rather than taking the higher return from the

unknown risk. These kinds of investors play safe in the security market and invest in those

3

Introduction:

Portfolio management is an art and science which is used to make decision about the

investment into few securities to manage the risk and return. This portfolio management

process is used to match the investment objective, asset allocation etc for institutions and

individuals and maintain the risk against performance. The overall aim of the portfolio

management is to determine strength, opportunities, threats and weakness of the debts,

equity, domestic shares, international shares, safety, growth etc to attempt to minimize the

risk and maximize the return (Zimmerman and Yahya-Zadeh, 2011).

In the report, the optimal portfolios have been prepared on the basis of the risk and

return. On the basis of the given data, 2 portfolios have been prepared. One portfolio focuses

on the risk-averse investors and other focuses on the high risk tolerance. In the given report,

the performance of both the portfolios has been measured to identify the position of the firms

and the overall returns from the portfolios. For evaluating the risk position and the return of

the assets, equity and debt, FTSE 250 index price has been taken into the concern.

Portfolio overview:

Portfolio is a collection of investment which is all owned by the same investor,

individual or an organization. Normally, these portfolios include stocks, bonds, investment in

individual businesses, government securities, mutual funds, debt etc to reduce the risk level

and manage the return from the overall investment of the individual (William et al, 2015). A

portfolio is prepared in such a way that if one stock is offering the negative result than other

stock, bond or other securities overcome that risk and loss of the individual.

The portfolio explains that all the amount must be invested into different securities so

that the risk could be diversified and a portfolio manger must assures that the investment is

done in the different venture. In the given case, the 3 different firms of UK market have been

taken for the purpose of portfolio. The risk and return of all the firms have been calculated

firstly to make an optimal capital structure for the risk-averse investors and other focuses on

the high risk tolerance.

The risk-averse investors are those individuals or the organization that prefer to take

lower return for the portfolio with known risk rather than taking the higher return from the

unknown risk. These kinds of investors play safe in the security market and invest in those

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting

4

securities which are associated with lower risk (Nobes and Parker, 2008). On the other hand,

high risk tolerance investors are those individuals which mainly focus on the higher return.

No matter, how much risk is associated with the portfolio, they only focuses on the higher

returns from the portfolio. The risk-averse investors and the high risk tolerance explain that

the choices of an individual are always different while preparing a portfolio. Some only

focuses on the risk whereas some focuses on the return of the company.

Along with the investment in each security or stock, the risk and return is essential. A

few reasons due to which portfolio is prepared by the investors are:

Risk of losing the money

With the volatility in the price, the worth of the total investment could be lower at the

time of need (Weygandt et al, 2009).

The changes into the growth or the competition level could affect the stock price of an

organization.

Or the changes into a particular industry could also affect the investment of an

individual.

Thus, an investor has to be sure that the investment has to be done in different

organization from different industry and in government bonds and the debts so that the level

of the risk could be minimized (Phillips and Stawarski, 2016). A portfolio could be

diversified in many ways to manage the risk and return of an organization. An investor could

follow the different methods to manage and prepare a portfolio such as:

Diversification of investment through investing into the stocks, currencies, real estate

investment, convertible securities etc.

Investment into the different countries so that the economic fluctuation could not

impact on the return.

Investment into the different market to save from currency fluctuations and other

factors (Niu, 2006).

Investment into the different industry to reduce the industry risk.

Different market optimization

Investment companies with different market share

4

securities which are associated with lower risk (Nobes and Parker, 2008). On the other hand,

high risk tolerance investors are those individuals which mainly focus on the higher return.

No matter, how much risk is associated with the portfolio, they only focuses on the higher

returns from the portfolio. The risk-averse investors and the high risk tolerance explain that

the choices of an individual are always different while preparing a portfolio. Some only

focuses on the risk whereas some focuses on the return of the company.

Along with the investment in each security or stock, the risk and return is essential. A

few reasons due to which portfolio is prepared by the investors are:

Risk of losing the money

With the volatility in the price, the worth of the total investment could be lower at the

time of need (Weygandt et al, 2009).

The changes into the growth or the competition level could affect the stock price of an

organization.

Or the changes into a particular industry could also affect the investment of an

individual.

Thus, an investor has to be sure that the investment has to be done in different

organization from different industry and in government bonds and the debts so that the level

of the risk could be minimized (Phillips and Stawarski, 2016). A portfolio could be

diversified in many ways to manage the risk and return of an organization. An investor could

follow the different methods to manage and prepare a portfolio such as:

Diversification of investment through investing into the stocks, currencies, real estate

investment, convertible securities etc.

Investment into the different countries so that the economic fluctuation could not

impact on the return.

Investment into the different market to save from currency fluctuations and other

factors (Niu, 2006).

Investment into the different industry to reduce the industry risk.

Different market optimization

Investment companies with different market share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting

5

Rate of return

Investment style

Holding period of the portfolio

Holding period of cash (Moles, Parrino and Kidwekk, 2011).

Above all are few methods which could be applied by the portfolio manager or the

individuals on the basis of the choice and the demands to make a better portfolio. The main

benefits of the portfolio management are as follows:

Better decision making

Risk management

Faster project turn times

Increase project delivery success

Streamline data and increment in the collaboration (Needles, Powers and Crosson,

2013)

On the basis of it, it has been found that the portfolio is one of the best choices for the

purpose of investment as it helps an organization or the individual to manage the overall

performance of the investment amount.

Optimal portfolio and the performance of the portfolio:

An efficient portfolio is the portfolio in which the return and risk are combined in a

way that it maximizes the return in anticipated and the current circumstances. Optimal

portfolio could be prepared on the basis of the efficient portfolio and the modern portfolio

theory (Bromwich and Bhimani, 2005). Modern portfolio theory is an optimal portfolio

strategy which constructs an optimal portfolio through considering various figures such as

beta, alpha and R-squared. The theory explains that the risk of a stock could be evaluated on

the basis of the fluctuations in the total stock price of an individual security on the basis of

the index stock price.

According to the given data in the case, two portfolios have been prepared on the

basis of the overall risk and return of the security. Firstly, a portfolio has been made for the

risk-averse investors and it has been found that the total risk of the firm 1, firm 2 and firm 3

are 0.10, 0.11 and 0.03. At the same time, the market risk premium and risk free rate of UK is

5

Rate of return

Investment style

Holding period of the portfolio

Holding period of cash (Moles, Parrino and Kidwekk, 2011).

Above all are few methods which could be applied by the portfolio manager or the

individuals on the basis of the choice and the demands to make a better portfolio. The main

benefits of the portfolio management are as follows:

Better decision making

Risk management

Faster project turn times

Increase project delivery success

Streamline data and increment in the collaboration (Needles, Powers and Crosson,

2013)

On the basis of it, it has been found that the portfolio is one of the best choices for the

purpose of investment as it helps an organization or the individual to manage the overall

performance of the investment amount.

Optimal portfolio and the performance of the portfolio:

An efficient portfolio is the portfolio in which the return and risk are combined in a

way that it maximizes the return in anticipated and the current circumstances. Optimal

portfolio could be prepared on the basis of the efficient portfolio and the modern portfolio

theory (Bromwich and Bhimani, 2005). Modern portfolio theory is an optimal portfolio

strategy which constructs an optimal portfolio through considering various figures such as

beta, alpha and R-squared. The theory explains that the risk of a stock could be evaluated on

the basis of the fluctuations in the total stock price of an individual security on the basis of

the index stock price.

According to the given data in the case, two portfolios have been prepared on the

basis of the overall risk and return of the security. Firstly, a portfolio has been made for the

risk-averse investors and it has been found that the total risk of the firm 1, firm 2 and firm 3

are 0.10, 0.11 and 0.03. At the same time, the market risk premium and risk free rate of UK is

Accounting

6

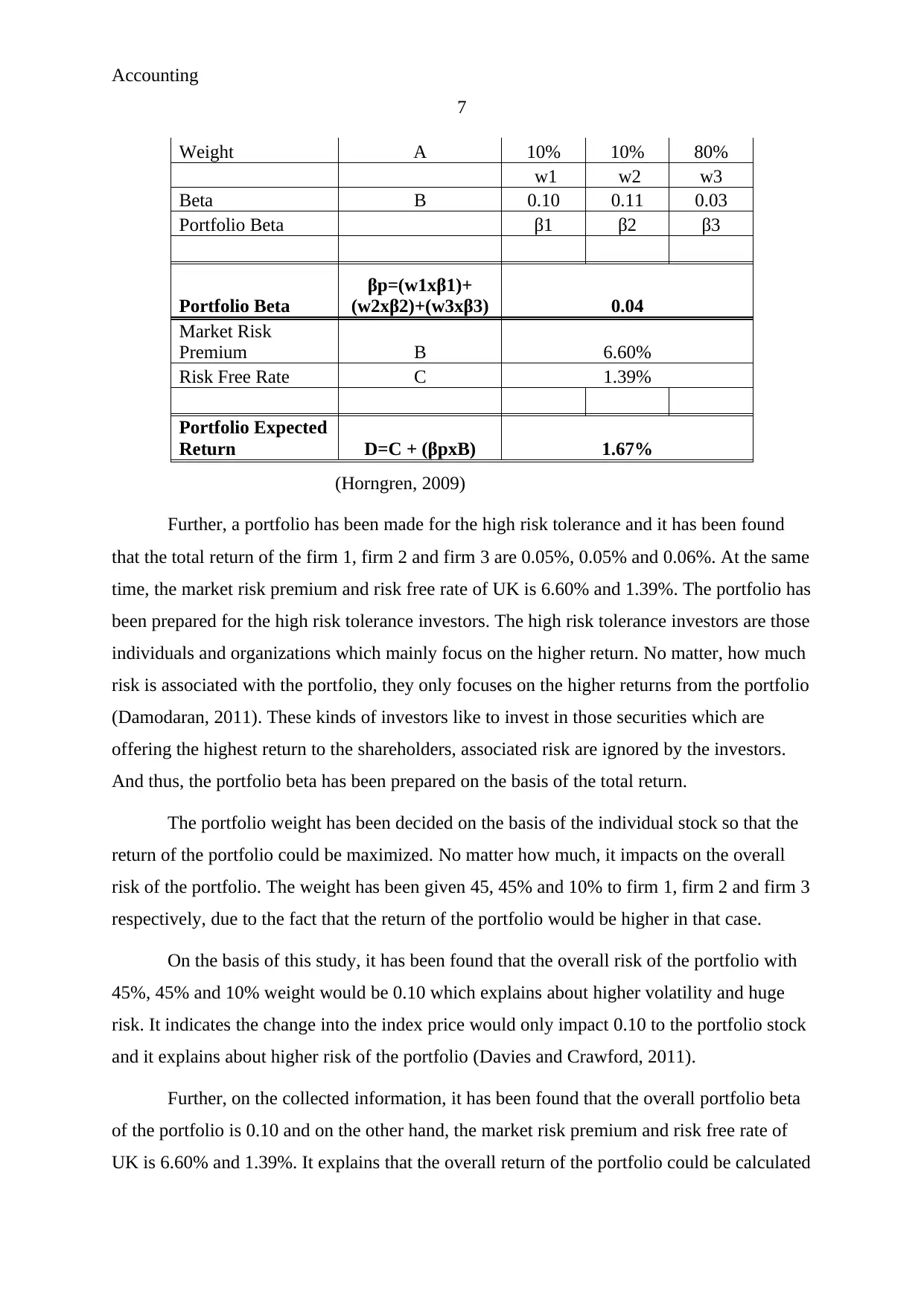

6.60% and 1.39% (Bloomberg, 2018). The portfolio has been prepared for the risk-averse

investors. The risk-averse investors are those individuals or the organization that prefer to

take lower return for the portfolio with known risk rather than taking the higher return from

the unknown risk. These kinds of investors play safe in the security market and invest in

those securities which are associated with lower risk. And thus, the portfolio beta has been

prepared on the basis of the risk (Bromwich and Bhimani, 2005).

The portfolio weight has been decided on the basis of the individual stock so that the

beta (risk) of the portfolio could be minimized. No matter how much, it impacts on the

overall return of the portfolio. The weight has been given 10%, 10% and 80% to firm 1, firm

2 and firm 3 respectively, due to the fact that the beta of firm 1 and firm 2 is 0.10 and 0.11

which is quite higher than the beta of firm 3. The beta of firm 3 is 0.03 which is lowest and

thus the rest fraction which is 80% has been given to the Firm 3.

On the basis of this study, it has been found that the overall risk of the portfolio with

10%, 10% and 80% weight would be 0.04 which explains about lower volatility and lesser

risk. It indicates the change into the index price would only impact 0.04 to the portfolio stock

and it explains about lower risk of the portfolio (Travlos et al, 2015).

Further, on the collected information, it has been found that the overall portfolio beta

of the portfolio is 0.04 and on the other hand, the market risk premium and risk free rate of

UK is 6.60% and 1.39% (Market premia, 2018). It explains that the overall return of the

portfolio could be calculated through capital asset pricing model. The capital asset pricing

model explains that the overall return from the portfolio would be 1.67%.

On the basis of the below given table, it has been recognized that the overall risk of

the portfolio is 0.04 and the return from the portfolio is 1.67%. It explains that the associated

risk with the portfolio is lower and thus it is better option for the risk-adverse investors.

However, it has also been found through this portfolio that overall return of the portfolio is

also lower (Thanatawee, 2013). But the risk-averse investor only focuses on the lower risk;

return does not matter that much to them.

Thus, this portfolio is one of the better option for the risk averse investor and if an

investor wants to face lowest risk than he should invest into the portfolio for sure.

Particulars Firm 1 Firm 2 Firm 3

6

6.60% and 1.39% (Bloomberg, 2018). The portfolio has been prepared for the risk-averse

investors. The risk-averse investors are those individuals or the organization that prefer to

take lower return for the portfolio with known risk rather than taking the higher return from

the unknown risk. These kinds of investors play safe in the security market and invest in

those securities which are associated with lower risk. And thus, the portfolio beta has been

prepared on the basis of the risk (Bromwich and Bhimani, 2005).

The portfolio weight has been decided on the basis of the individual stock so that the

beta (risk) of the portfolio could be minimized. No matter how much, it impacts on the

overall return of the portfolio. The weight has been given 10%, 10% and 80% to firm 1, firm

2 and firm 3 respectively, due to the fact that the beta of firm 1 and firm 2 is 0.10 and 0.11

which is quite higher than the beta of firm 3. The beta of firm 3 is 0.03 which is lowest and

thus the rest fraction which is 80% has been given to the Firm 3.

On the basis of this study, it has been found that the overall risk of the portfolio with

10%, 10% and 80% weight would be 0.04 which explains about lower volatility and lesser

risk. It indicates the change into the index price would only impact 0.04 to the portfolio stock

and it explains about lower risk of the portfolio (Travlos et al, 2015).

Further, on the collected information, it has been found that the overall portfolio beta

of the portfolio is 0.04 and on the other hand, the market risk premium and risk free rate of

UK is 6.60% and 1.39% (Market premia, 2018). It explains that the overall return of the

portfolio could be calculated through capital asset pricing model. The capital asset pricing

model explains that the overall return from the portfolio would be 1.67%.

On the basis of the below given table, it has been recognized that the overall risk of

the portfolio is 0.04 and the return from the portfolio is 1.67%. It explains that the associated

risk with the portfolio is lower and thus it is better option for the risk-adverse investors.

However, it has also been found through this portfolio that overall return of the portfolio is

also lower (Thanatawee, 2013). But the risk-averse investor only focuses on the lower risk;

return does not matter that much to them.

Thus, this portfolio is one of the better option for the risk averse investor and if an

investor wants to face lowest risk than he should invest into the portfolio for sure.

Particulars Firm 1 Firm 2 Firm 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting

7

Weight A 10% 10% 80%

w1 w2 w3

Beta B 0.10 0.11 0.03

Portfolio Beta β1 β2 β3

Portfolio Beta

βp=(w1xβ1)+

(w2xβ2)+(w3xβ3) 0.04

Market Risk

Premium B 6.60%

Risk Free Rate C 1.39%

Portfolio Expected

Return D=C + (βpxB) 1.67%

(Horngren, 2009)

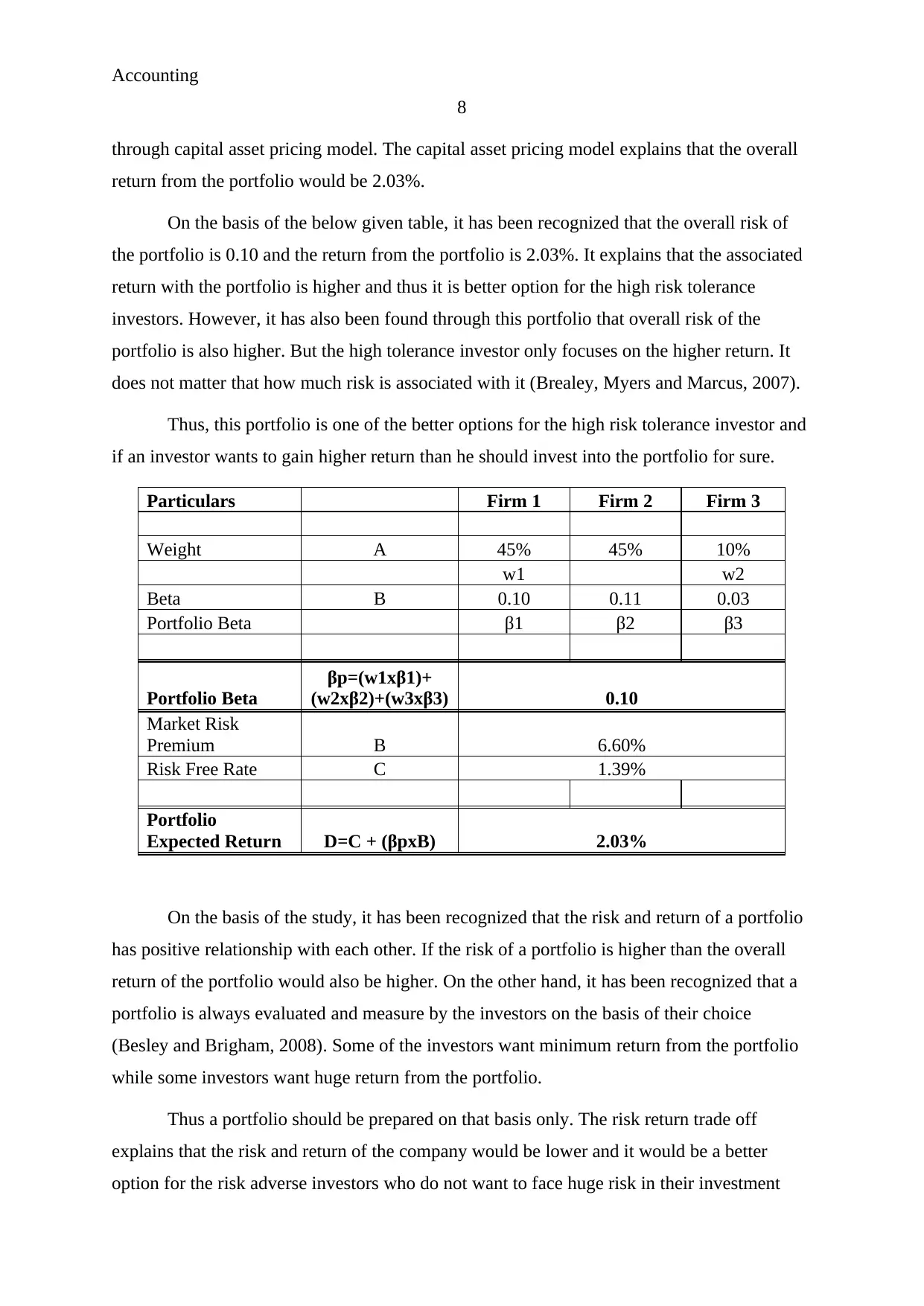

Further, a portfolio has been made for the high risk tolerance and it has been found

that the total return of the firm 1, firm 2 and firm 3 are 0.05%, 0.05% and 0.06%. At the same

time, the market risk premium and risk free rate of UK is 6.60% and 1.39%. The portfolio has

been prepared for the high risk tolerance investors. The high risk tolerance investors are those

individuals and organizations which mainly focus on the higher return. No matter, how much

risk is associated with the portfolio, they only focuses on the higher returns from the portfolio

(Damodaran, 2011). These kinds of investors like to invest in those securities which are

offering the highest return to the shareholders, associated risk are ignored by the investors.

And thus, the portfolio beta has been prepared on the basis of the total return.

The portfolio weight has been decided on the basis of the individual stock so that the

return of the portfolio could be maximized. No matter how much, it impacts on the overall

risk of the portfolio. The weight has been given 45, 45% and 10% to firm 1, firm 2 and firm 3

respectively, due to the fact that the return of the portfolio would be higher in that case.

On the basis of this study, it has been found that the overall risk of the portfolio with

45%, 45% and 10% weight would be 0.10 which explains about higher volatility and huge

risk. It indicates the change into the index price would only impact 0.10 to the portfolio stock

and it explains about higher risk of the portfolio (Davies and Crawford, 2011).

Further, on the collected information, it has been found that the overall portfolio beta

of the portfolio is 0.10 and on the other hand, the market risk premium and risk free rate of

UK is 6.60% and 1.39%. It explains that the overall return of the portfolio could be calculated

7

Weight A 10% 10% 80%

w1 w2 w3

Beta B 0.10 0.11 0.03

Portfolio Beta β1 β2 β3

Portfolio Beta

βp=(w1xβ1)+

(w2xβ2)+(w3xβ3) 0.04

Market Risk

Premium B 6.60%

Risk Free Rate C 1.39%

Portfolio Expected

Return D=C + (βpxB) 1.67%

(Horngren, 2009)

Further, a portfolio has been made for the high risk tolerance and it has been found

that the total return of the firm 1, firm 2 and firm 3 are 0.05%, 0.05% and 0.06%. At the same

time, the market risk premium and risk free rate of UK is 6.60% and 1.39%. The portfolio has

been prepared for the high risk tolerance investors. The high risk tolerance investors are those

individuals and organizations which mainly focus on the higher return. No matter, how much

risk is associated with the portfolio, they only focuses on the higher returns from the portfolio

(Damodaran, 2011). These kinds of investors like to invest in those securities which are

offering the highest return to the shareholders, associated risk are ignored by the investors.

And thus, the portfolio beta has been prepared on the basis of the total return.

The portfolio weight has been decided on the basis of the individual stock so that the

return of the portfolio could be maximized. No matter how much, it impacts on the overall

risk of the portfolio. The weight has been given 45, 45% and 10% to firm 1, firm 2 and firm 3

respectively, due to the fact that the return of the portfolio would be higher in that case.

On the basis of this study, it has been found that the overall risk of the portfolio with

45%, 45% and 10% weight would be 0.10 which explains about higher volatility and huge

risk. It indicates the change into the index price would only impact 0.10 to the portfolio stock

and it explains about higher risk of the portfolio (Davies and Crawford, 2011).

Further, on the collected information, it has been found that the overall portfolio beta

of the portfolio is 0.10 and on the other hand, the market risk premium and risk free rate of

UK is 6.60% and 1.39%. It explains that the overall return of the portfolio could be calculated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting

8

through capital asset pricing model. The capital asset pricing model explains that the overall

return from the portfolio would be 2.03%.

On the basis of the below given table, it has been recognized that the overall risk of

the portfolio is 0.10 and the return from the portfolio is 2.03%. It explains that the associated

return with the portfolio is higher and thus it is better option for the high risk tolerance

investors. However, it has also been found through this portfolio that overall risk of the

portfolio is also higher. But the high tolerance investor only focuses on the higher return. It

does not matter that how much risk is associated with it (Brealey, Myers and Marcus, 2007).

Thus, this portfolio is one of the better options for the high risk tolerance investor and

if an investor wants to gain higher return than he should invest into the portfolio for sure.

Particulars Firm 1 Firm 2 Firm 3

Weight A 45% 45% 10%

w1 w2

Beta B 0.10 0.11 0.03

Portfolio Beta β1 β2 β3

Portfolio Beta

βp=(w1xβ1)+

(w2xβ2)+(w3xβ3) 0.10

Market Risk

Premium B 6.60%

Risk Free Rate C 1.39%

Portfolio

Expected Return D=C + (βpxB) 2.03%

On the basis of the study, it has been recognized that the risk and return of a portfolio

has positive relationship with each other. If the risk of a portfolio is higher than the overall

return of the portfolio would also be higher. On the other hand, it has been recognized that a

portfolio is always evaluated and measure by the investors on the basis of their choice

(Besley and Brigham, 2008). Some of the investors want minimum return from the portfolio

while some investors want huge return from the portfolio.

Thus a portfolio should be prepared on that basis only. The risk return trade off

explains that the risk and return of the company would be lower and it would be a better

option for the risk adverse investors who do not want to face huge risk in their investment

8

through capital asset pricing model. The capital asset pricing model explains that the overall

return from the portfolio would be 2.03%.

On the basis of the below given table, it has been recognized that the overall risk of

the portfolio is 0.10 and the return from the portfolio is 2.03%. It explains that the associated

return with the portfolio is higher and thus it is better option for the high risk tolerance

investors. However, it has also been found through this portfolio that overall risk of the

portfolio is also higher. But the high tolerance investor only focuses on the higher return. It

does not matter that how much risk is associated with it (Brealey, Myers and Marcus, 2007).

Thus, this portfolio is one of the better options for the high risk tolerance investor and

if an investor wants to gain higher return than he should invest into the portfolio for sure.

Particulars Firm 1 Firm 2 Firm 3

Weight A 45% 45% 10%

w1 w2

Beta B 0.10 0.11 0.03

Portfolio Beta β1 β2 β3

Portfolio Beta

βp=(w1xβ1)+

(w2xβ2)+(w3xβ3) 0.10

Market Risk

Premium B 6.60%

Risk Free Rate C 1.39%

Portfolio

Expected Return D=C + (βpxB) 2.03%

On the basis of the study, it has been recognized that the risk and return of a portfolio

has positive relationship with each other. If the risk of a portfolio is higher than the overall

return of the portfolio would also be higher. On the other hand, it has been recognized that a

portfolio is always evaluated and measure by the investors on the basis of their choice

(Besley and Brigham, 2008). Some of the investors want minimum return from the portfolio

while some investors want huge return from the portfolio.

Thus a portfolio should be prepared on that basis only. The risk return trade off

explains that the risk and return of the company would be lower and it would be a better

option for the risk adverse investors who do not want to face huge risk in their investment

Accounting

9

whereas the risk and return of the company would be higher and it would be a better option

for the high risk tolerance investors who wants to earn higher return from their investment

(Bierman, 2010). It explains that an investor is required to evaluate all the related topics

while making a decision about the overall performance of the company.

Recommendation and conclusion:

On the basis of the study on the portfolio management, benefits of portfolio

management etc. it has been found that the portfolio is among the better choices of an

organization or an individual to make investments. If an investor is focusing on the risk only

and he wants to invest into those portfolio from where the risk is minimum than the portfolio

one is the better option for the investor and if an investor wants to face lowest risk than he

should invest into the portfolio for sure. On the other hand, it has been found that if an

investor is focusing on the return only and he wants to invest into those portfolio from where

the highest revenue could be earn than the portfolio two is the better option for the investor.

And if an investor wants to generate higher profit then he should invest into the portfolio for

sure.

To conclude, the portfolio management process is quite crucial for an organization

and the individual to manage the overall position and the performance of an organization.

The overall aim of the portfolio management is to determine strength, opportunities, threats

and weakness of the debts, equity, domestic shares, international shares, safety, growth etc to

attempt to minimize the risk and maximize the return.

9

whereas the risk and return of the company would be higher and it would be a better option

for the high risk tolerance investors who wants to earn higher return from their investment

(Bierman, 2010). It explains that an investor is required to evaluate all the related topics

while making a decision about the overall performance of the company.

Recommendation and conclusion:

On the basis of the study on the portfolio management, benefits of portfolio

management etc. it has been found that the portfolio is among the better choices of an

organization or an individual to make investments. If an investor is focusing on the risk only

and he wants to invest into those portfolio from where the risk is minimum than the portfolio

one is the better option for the investor and if an investor wants to face lowest risk than he

should invest into the portfolio for sure. On the other hand, it has been found that if an

investor is focusing on the return only and he wants to invest into those portfolio from where

the highest revenue could be earn than the portfolio two is the better option for the investor.

And if an investor wants to generate higher profit then he should invest into the portfolio for

sure.

To conclude, the portfolio management process is quite crucial for an organization

and the individual to manage the overall position and the performance of an organization.

The overall aim of the portfolio management is to determine strength, opportunities, threats

and weakness of the debts, equity, domestic shares, international shares, safety, growth etc to

attempt to minimize the risk and maximize the return.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting

10

References:

Besley, S. and Brigham, E.F., 2008. Essentials of managerial finance. Thomson South-

Western.

Bierman, H., 2010. An introduction to accounting and managerial finance: a merger of

equals. World Scientific.

Bloomberg. 2018. Rates and bonds. (online). Available at:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/uk (accessed 11/6/18).

Borio, C., 2014. The financial cycle and macroeconomics: What have we learnt?. Journal of

Banking & Finance, 45, pp.182-198.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. FundamentalsofCorporate Finance. Mc

Graw Hill, New York.

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Damodaran, A, 2011, Applied corporate finance,3rd edition, John Wiley & sons, USA.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Market risk premia. 2018. Market return. (online). Available at http://www.market-risk-

premia.com/gb.html (accessed 11/6/18).

Moles, P. Parrino, R & Kidwekk, D,.2011, Corporate finance, European edition, John Wiley

&sons, United Kingdom

Needles, B., Powers, M. and Crosson, S., 2013. Financial and managerial accounting. Nelson

Education.

Niu, F.F., 2006. Corporate governance and the quality of accounting earnings: a Canadian

perspective. International Journal of Managerial Finance, 2(4), pp.302-327.

Nobes, C. and Parker, R.H., 2008. Comparative international accounting. Pearson Education.

10

References:

Besley, S. and Brigham, E.F., 2008. Essentials of managerial finance. Thomson South-

Western.

Bierman, H., 2010. An introduction to accounting and managerial finance: a merger of

equals. World Scientific.

Bloomberg. 2018. Rates and bonds. (online). Available at:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/uk (accessed 11/6/18).

Borio, C., 2014. The financial cycle and macroeconomics: What have we learnt?. Journal of

Banking & Finance, 45, pp.182-198.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. FundamentalsofCorporate Finance. Mc

Graw Hill, New York.

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Damodaran, A, 2011, Applied corporate finance,3rd edition, John Wiley & sons, USA.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Market risk premia. 2018. Market return. (online). Available at http://www.market-risk-

premia.com/gb.html (accessed 11/6/18).

Moles, P. Parrino, R & Kidwekk, D,.2011, Corporate finance, European edition, John Wiley

&sons, United Kingdom

Needles, B., Powers, M. and Crosson, S., 2013. Financial and managerial accounting. Nelson

Education.

Niu, F.F., 2006. Corporate governance and the quality of accounting earnings: a Canadian

perspective. International Journal of Managerial Finance, 2(4), pp.302-327.

Nobes, C. and Parker, R.H., 2008. Comparative international accounting. Pearson Education.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting

11

Phillips, P.P. and Stawarski, C.A. 2016. Data Collection: Planning for and Collecting All

Types of Data. John Wiley & Sons.

Thanatawee, Y., 2013. Ownership structure and dividend policy: Evidence from Thailand.

Travlos, N.G., Trigeorgis, L. and Vafeas, N., 2015. Shareholder wealth effects of dividend

policy changes in an emerging stock market: The case of Cyprus.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2009. Managerial accounting: tools for

business decision making. John Wiley & Sons.

Williams, J.R., Haka, S.F., Bettner, M.S. and Carcello, J.V., 2005. Financial and managerial

accounting. China Machine Press.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

11

Phillips, P.P. and Stawarski, C.A. 2016. Data Collection: Planning for and Collecting All

Types of Data. John Wiley & Sons.

Thanatawee, Y., 2013. Ownership structure and dividend policy: Evidence from Thailand.

Travlos, N.G., Trigeorgis, L. and Vafeas, N., 2015. Shareholder wealth effects of dividend

policy changes in an emerging stock market: The case of Cyprus.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2009. Managerial accounting: tools for

business decision making. John Wiley & Sons.

Williams, J.R., Haka, S.F., Bettner, M.S. and Carcello, J.V., 2005. Financial and managerial

accounting. China Machine Press.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.