Choosing between formal employment and self-employment

VerifiedAdded on 2023/04/07

|11

|1586

|300

AI Summary

This memo provides advice on choosing between formal employment and self-employment based on the tax burden and benefits associated with each option. It compares the income tax payable as an employee of Main Street Consultants Limited and the tax payable when self-employed. It also discusses the advantages of self-employment, such as the potential for business growth and tax relief options. The memo concludes that self-employment is more advantageous.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

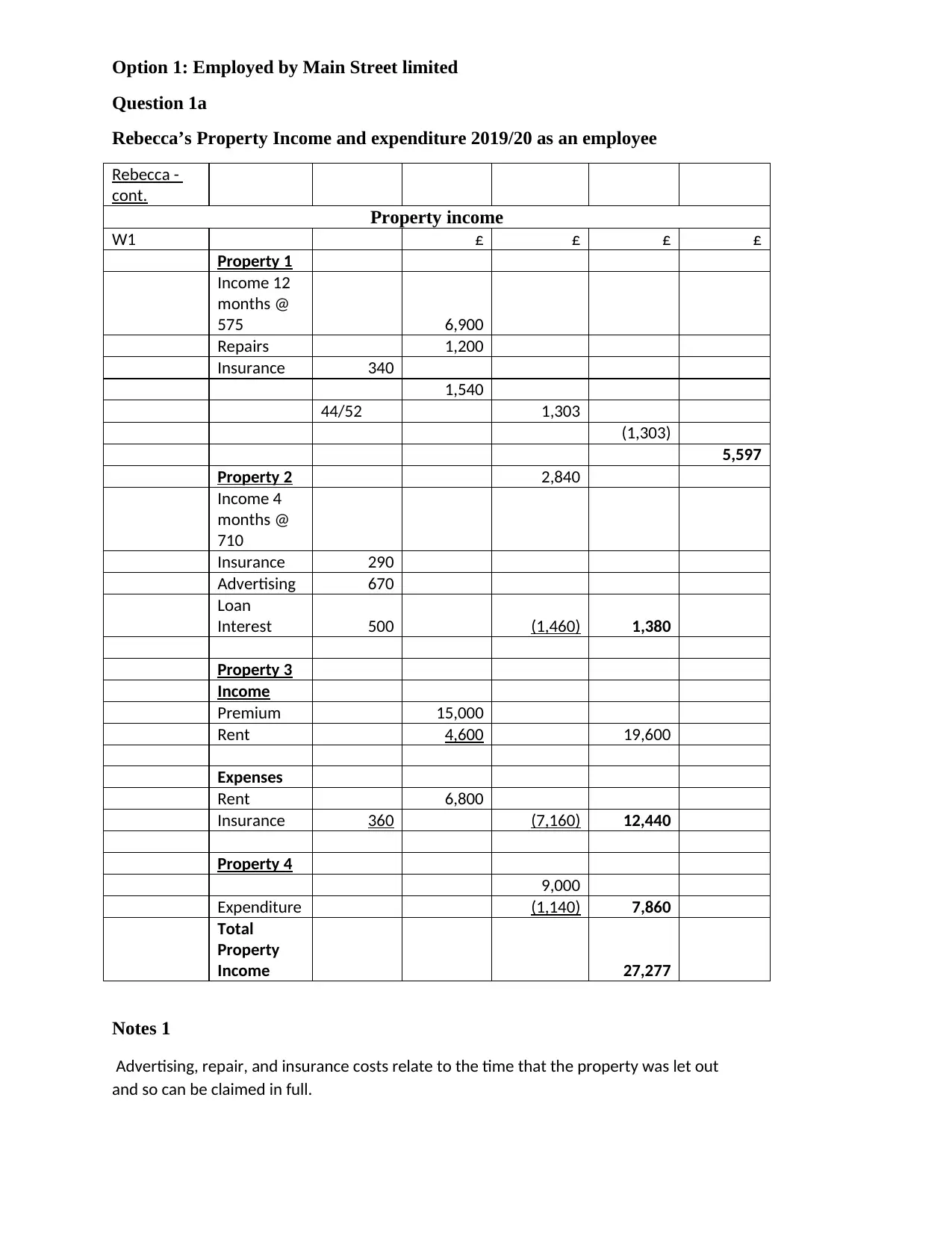

Option 1: Employed by Main Street limited

Question 1a

Rebecca’s Property Income and expenditure 2019/20 as an employee

Rebecca -

cont.

Property income

W1 £ £ £ £

Property 1

Income 12

months @

575 6,900

Repairs 1,200

Insurance 340

1,540

44/52 1,303

(1,303)

5,597

Property 2 2,840

Income 4

months @

710

Insurance 290

Advertising 670

Loan

Interest 500 (1,460) 1,380

Property 3

Income

Premium 15,000

Rent 4,600 19,600

Expenses

Rent 6,800

Insurance 360 (7,160) 12,440

Property 4

9,000

Expenditure (1,140) 7,860

Total

Property

Income 27,277

Notes 1

Advertising, repair, and insurance costs relate to the time that the property was let out

and so can be claimed in full.

Question 1a

Rebecca’s Property Income and expenditure 2019/20 as an employee

Rebecca -

cont.

Property income

W1 £ £ £ £

Property 1

Income 12

months @

575 6,900

Repairs 1,200

Insurance 340

1,540

44/52 1,303

(1,303)

5,597

Property 2 2,840

Income 4

months @

710

Insurance 290

Advertising 670

Loan

Interest 500 (1,460) 1,380

Property 3

Income

Premium 15,000

Rent 4,600 19,600

Expenses

Rent 6,800

Insurance 360 (7,160) 12,440

Property 4

9,000

Expenditure (1,140) 7,860

Total

Property

Income 27,277

Notes 1

Advertising, repair, and insurance costs relate to the time that the property was let out

and so can be claimed in full.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

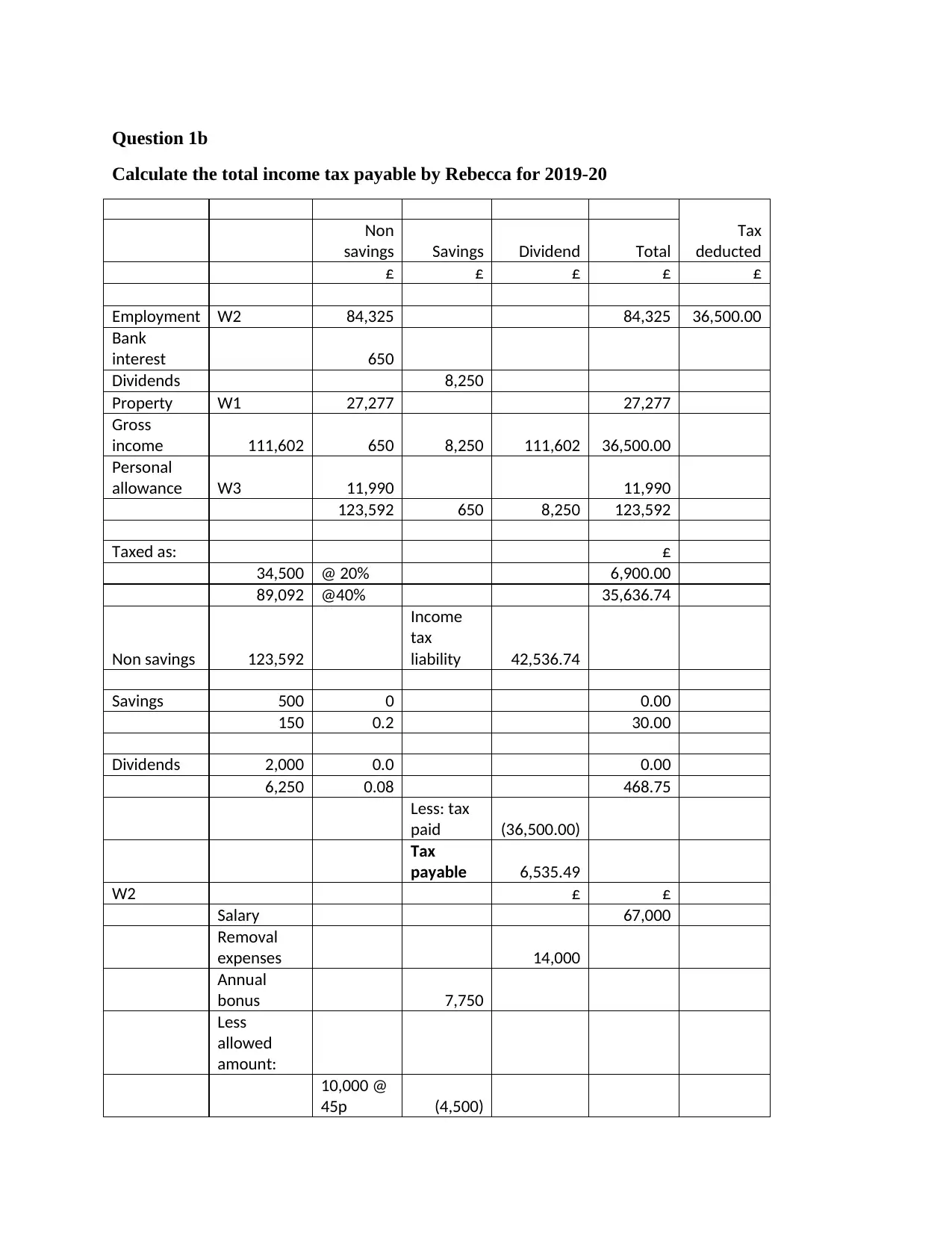

Question 1b

Calculate the total income tax payable by Rebecca for 2019-20

Tax

deducted

Non

savings Savings Dividend Total

£ £ £ £ £

Employment W2 84,325 84,325 36,500.00

Bank

interest 650

Dividends 8,250

Property W1 27,277 27,277

Gross

income 111,602 650 8,250 111,602 36,500.00

Personal

allowance W3 11,990 11,990

123,592 650 8,250 123,592

Taxed as: £

34,500 @ 20% 6,900.00

89,092 @40% 35,636.74

Non savings 123,592

Income

tax

liability 42,536.74

Savings 500 0 0.00

150 0.2 30.00

Dividends 2,000 0.0 0.00

6,250 0.08 468.75

Less: tax

paid (36,500.00)

Tax

payable 6,535.49

W2 £ £

Salary 67,000

Removal

expenses 14,000

Annual

bonus 7,750

Less

allowed

amount:

10,000 @

45p (4,500)

Calculate the total income tax payable by Rebecca for 2019-20

Tax

deducted

Non

savings Savings Dividend Total

£ £ £ £ £

Employment W2 84,325 84,325 36,500.00

Bank

interest 650

Dividends 8,250

Property W1 27,277 27,277

Gross

income 111,602 650 8,250 111,602 36,500.00

Personal

allowance W3 11,990 11,990

123,592 650 8,250 123,592

Taxed as: £

34,500 @ 20% 6,900.00

89,092 @40% 35,636.74

Non savings 123,592

Income

tax

liability 42,536.74

Savings 500 0 0.00

150 0.2 30.00

Dividends 2,000 0.0 0.00

6,250 0.08 468.75

Less: tax

paid (36,500.00)

Tax

payable 6,535.49

W2 £ £

Salary 67,000

Removal

expenses 14,000

Annual

bonus 7,750

Less

allowed

amount:

10,000 @

45p (4,500)

4,100 @

25p (1,025)

2,225

Golf club

Subscription 1,000

Loan 12

000×(4%-

1.5%)×4/12 100

84,325

W3

Total

income

exceeds

£100,000,

so personal

allowance

is abated.

£

PA 11,850

Less:

(107,415 -

100,000) / 2 (5,801)

6,049

Notes 2

PSA is £500 because Rebecca is a higher rate taxpayer.

The £2,000 dividend allowance is available to all taxpayers.

Question 1c

National Insurance Contribution Payable by Rebecca

£

Property 1 insurance 340

Property 2 insurance 290

Property 3 insurance 360

Property 4 insurance 1140

Total 2130

Question1d

National Insurance Contribution payable by Main Street Consultants Limited.

Monthly pay £ 5583.33

25p (1,025)

2,225

Golf club

Subscription 1,000

Loan 12

000×(4%-

1.5%)×4/12 100

84,325

W3

Total

income

exceeds

£100,000,

so personal

allowance

is abated.

£

PA 11,850

Less:

(107,415 -

100,000) / 2 (5,801)

6,049

Notes 2

PSA is £500 because Rebecca is a higher rate taxpayer.

The £2,000 dividend allowance is available to all taxpayers.

Question 1c

National Insurance Contribution Payable by Rebecca

£

Property 1 insurance 340

Property 2 insurance 290

Property 3 insurance 360

Property 4 insurance 1140

Total 2130

Question1d

National Insurance Contribution payable by Main Street Consultants Limited.

Monthly pay £ 5583.33

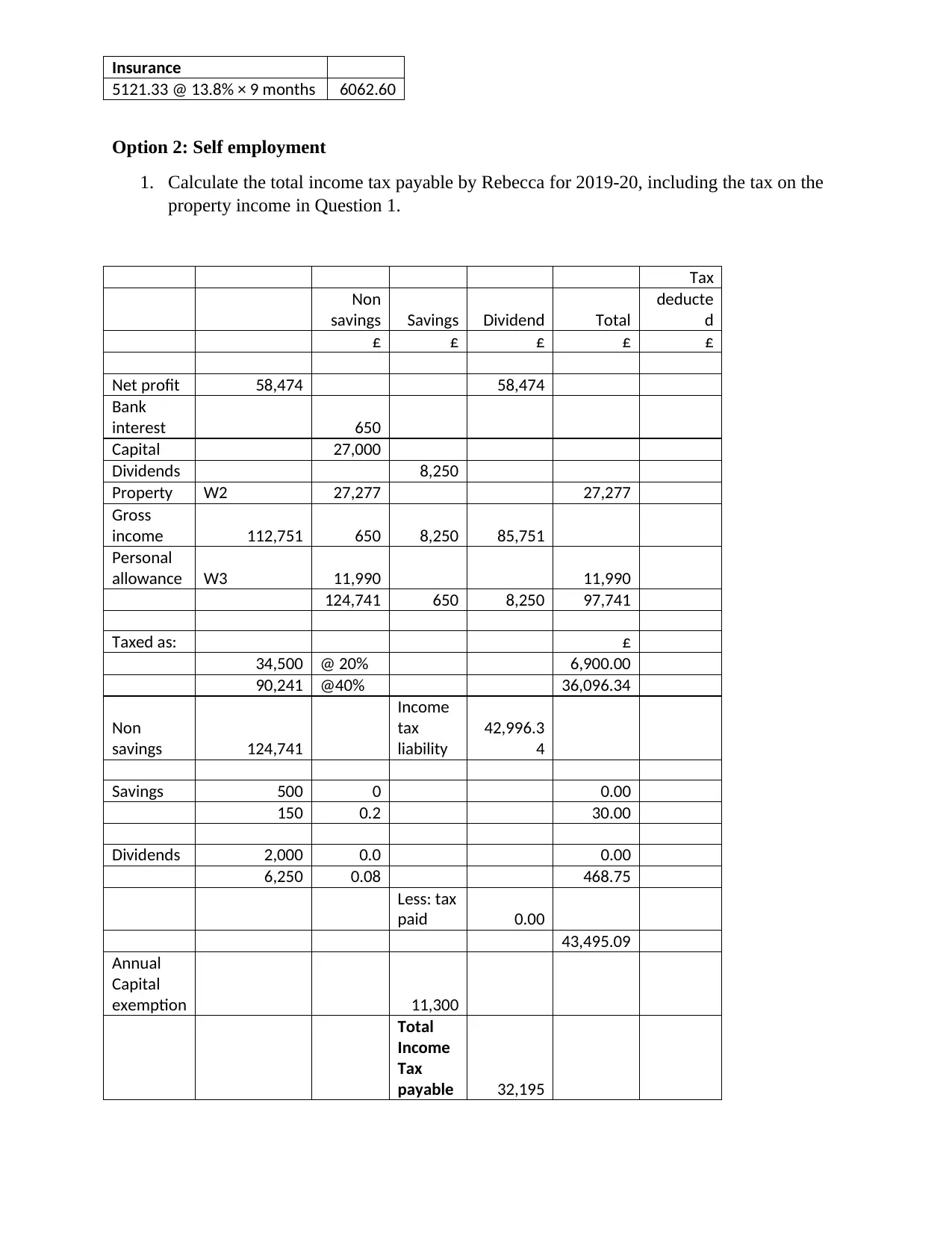

Insurance

5121.33 @ 13.8% × 9 months 6062.60

Option 2: Self employment

1. Calculate the total income tax payable by Rebecca for 2019-20, including the tax on the

property income in Question 1.

Tax

Non

savings Savings Dividend Total

deducte

d

£ £ £ £ £

Net profit 58,474 58,474

Bank

interest 650

Capital 27,000

Dividends 8,250

Property W2 27,277 27,277

Gross

income 112,751 650 8,250 85,751

Personal

allowance W3 11,990 11,990

124,741 650 8,250 97,741

Taxed as: £

34,500 @ 20% 6,900.00

90,241 @40% 36,096.34

Non

savings 124,741

Income

tax

liability

42,996.3

4

Savings 500 0 0.00

150 0.2 30.00

Dividends 2,000 0.0 0.00

6,250 0.08 468.75

Less: tax

paid 0.00

43,495.09

Annual

Capital

exemption 11,300

Total

Income

Tax

payable 32,195

5121.33 @ 13.8% × 9 months 6062.60

Option 2: Self employment

1. Calculate the total income tax payable by Rebecca for 2019-20, including the tax on the

property income in Question 1.

Tax

Non

savings Savings Dividend Total

deducte

d

£ £ £ £ £

Net profit 58,474 58,474

Bank

interest 650

Capital 27,000

Dividends 8,250

Property W2 27,277 27,277

Gross

income 112,751 650 8,250 85,751

Personal

allowance W3 11,990 11,990

124,741 650 8,250 97,741

Taxed as: £

34,500 @ 20% 6,900.00

90,241 @40% 36,096.34

Non

savings 124,741

Income

tax

liability

42,996.3

4

Savings 500 0 0.00

150 0.2 30.00

Dividends 2,000 0.0 0.00

6,250 0.08 468.75

Less: tax

paid 0.00

43,495.09

Annual

Capital

exemption 11,300

Total

Income

Tax

payable 32,195

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

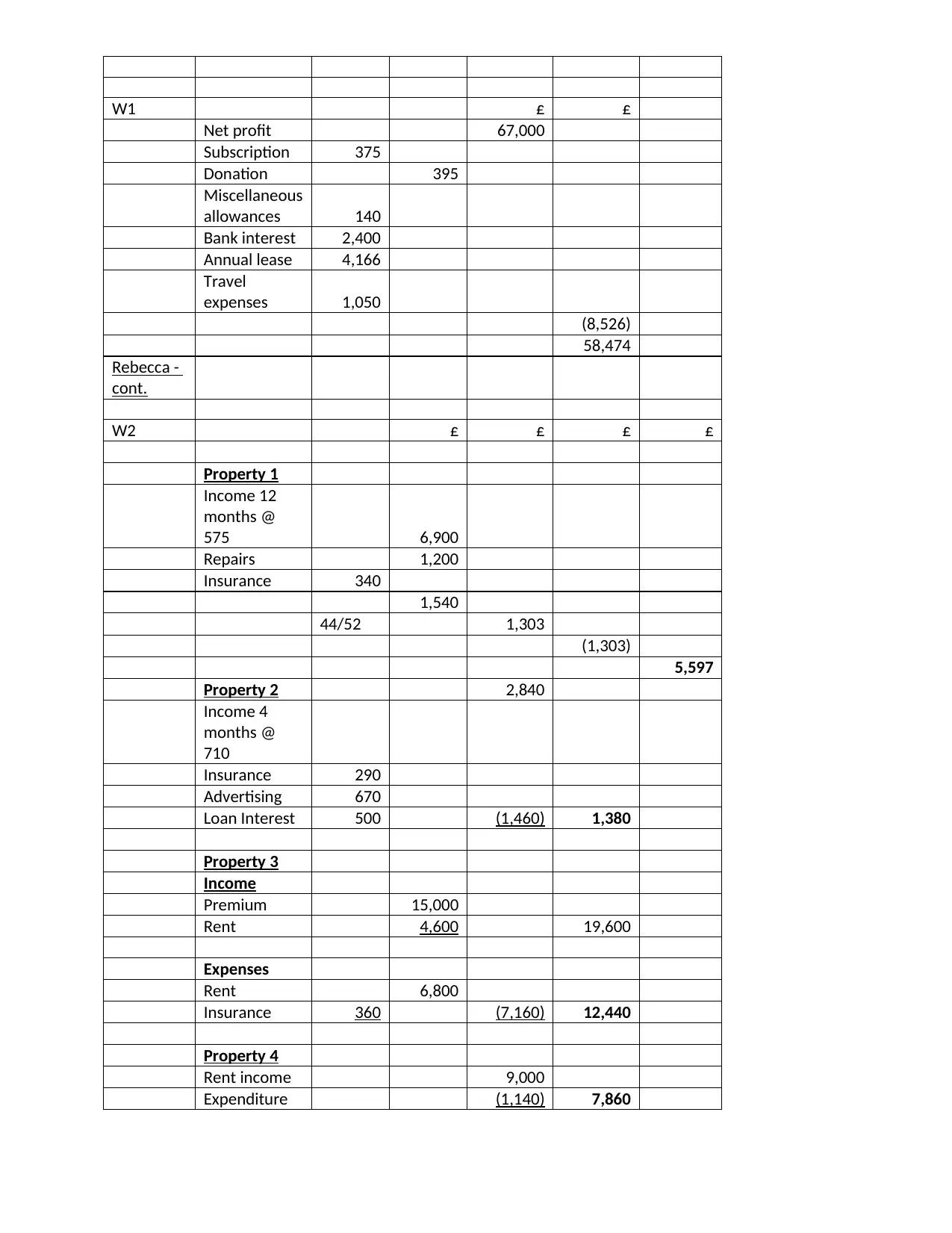

W1 £ £

Net profit 67,000

Subscription 375

Donation 395

Miscellaneous

allowances 140

Bank interest 2,400

Annual lease 4,166

Travel

expenses 1,050

(8,526)

58,474

Rebecca -

cont.

W2 £ £ £ £

Property 1

Income 12

months @

575 6,900

Repairs 1,200

Insurance 340

1,540

44/52 1,303

(1,303)

5,597

Property 2 2,840

Income 4

months @

710

Insurance 290

Advertising 670

Loan Interest 500 (1,460) 1,380

Property 3

Income

Premium 15,000

Rent 4,600 19,600

Expenses

Rent 6,800

Insurance 360 (7,160) 12,440

Property 4

Rent income 9,000

Expenditure (1,140) 7,860

Net profit 67,000

Subscription 375

Donation 395

Miscellaneous

allowances 140

Bank interest 2,400

Annual lease 4,166

Travel

expenses 1,050

(8,526)

58,474

Rebecca -

cont.

W2 £ £ £ £

Property 1

Income 12

months @

575 6,900

Repairs 1,200

Insurance 340

1,540

44/52 1,303

(1,303)

5,597

Property 2 2,840

Income 4

months @

710

Insurance 290

Advertising 670

Loan Interest 500 (1,460) 1,380

Property 3

Income

Premium 15,000

Rent 4,600 19,600

Expenses

Rent 6,800

Insurance 360 (7,160) 12,440

Property 4

Rent income 9,000

Expenditure (1,140) 7,860

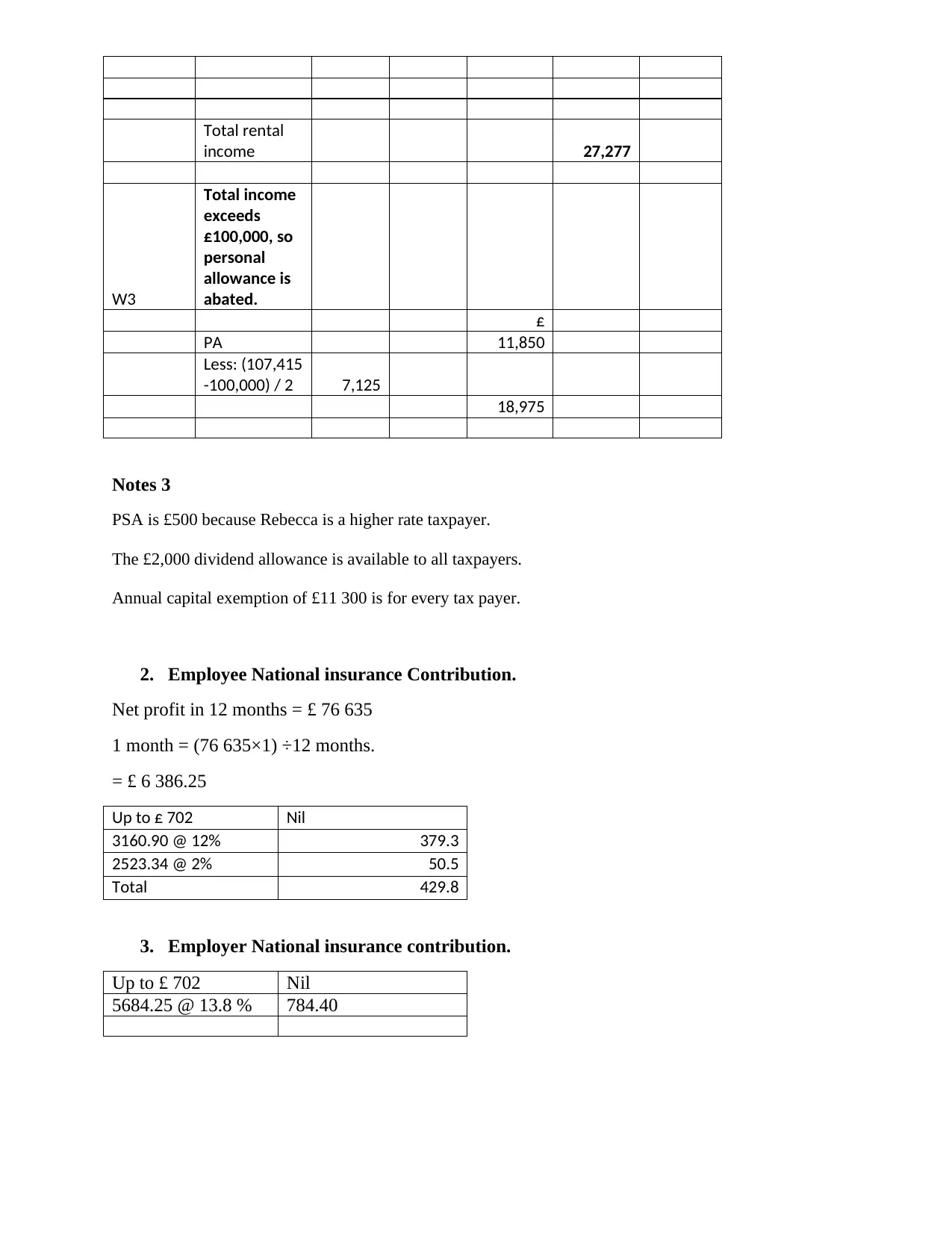

Total rental

income 27,277

W3

Total income

exceeds

£100,000, so

personal

allowance is

abated.

£

PA 11,850

Less: (107,415

-100,000) / 2 7,125

18,975

Notes 3

PSA is £500 because Rebecca is a higher rate taxpayer.

The £2,000 dividend allowance is available to all taxpayers.

Annual capital exemption of £11 300 is for every tax payer.

2. Employee National insurance Contribution.

Net profit in 12 months = £ 76 635

1 month = (76 635×1) ÷12 months.

= £ 6 386.25

Up to £ 702 Nil

3160.90 @ 12% 379.3

2523.34 @ 2% 50.5

Total 429.8

3. Employer National insurance contribution.

Up to £ 702 Nil

5684.25 @ 13.8 % 784.40

income 27,277

W3

Total income

exceeds

£100,000, so

personal

allowance is

abated.

£

PA 11,850

Less: (107,415

-100,000) / 2 7,125

18,975

Notes 3

PSA is £500 because Rebecca is a higher rate taxpayer.

The £2,000 dividend allowance is available to all taxpayers.

Annual capital exemption of £11 300 is for every tax payer.

2. Employee National insurance Contribution.

Net profit in 12 months = £ 76 635

1 month = (76 635×1) ÷12 months.

= £ 6 386.25

Up to £ 702 Nil

3160.90 @ 12% 379.3

2523.34 @ 2% 50.5

Total 429.8

3. Employer National insurance contribution.

Up to £ 702 Nil

5684.25 @ 13.8 % 784.40

SECTION B: BUSINESS MEMORANDUM

Office of Tax consultant

Internal Revenue Service

Memorandum

Number: 201903111

Release Date: 17/3/2019

Address:

UILC: 8501.02-02

Date: March 17, 2019

To: Rebecca Oliver

Retail Analyst

From: Name:

Tax Consultant

(Chartered Accountants, Harrison & Hawes LLP)

Subject: Choosing between formal employment and being self-employed.

The advice herein is a response to your request for help dated January 4, 2019. Please

Note that the advice given in this memorandum cannot be cited or used for any other

justification purposes.

Office of Tax consultant

Internal Revenue Service

Memorandum

Number: 201903111

Release Date: 17/3/2019

Address:

UILC: 8501.02-02

Date: March 17, 2019

To: Rebecca Oliver

Retail Analyst

From: Name:

Tax Consultant

(Chartered Accountants, Harrison & Hawes LLP)

Subject: Choosing between formal employment and being self-employed.

The advice herein is a response to your request for help dated January 4, 2019. Please

Note that the advice given in this memorandum cannot be cited or used for any other

justification purposes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

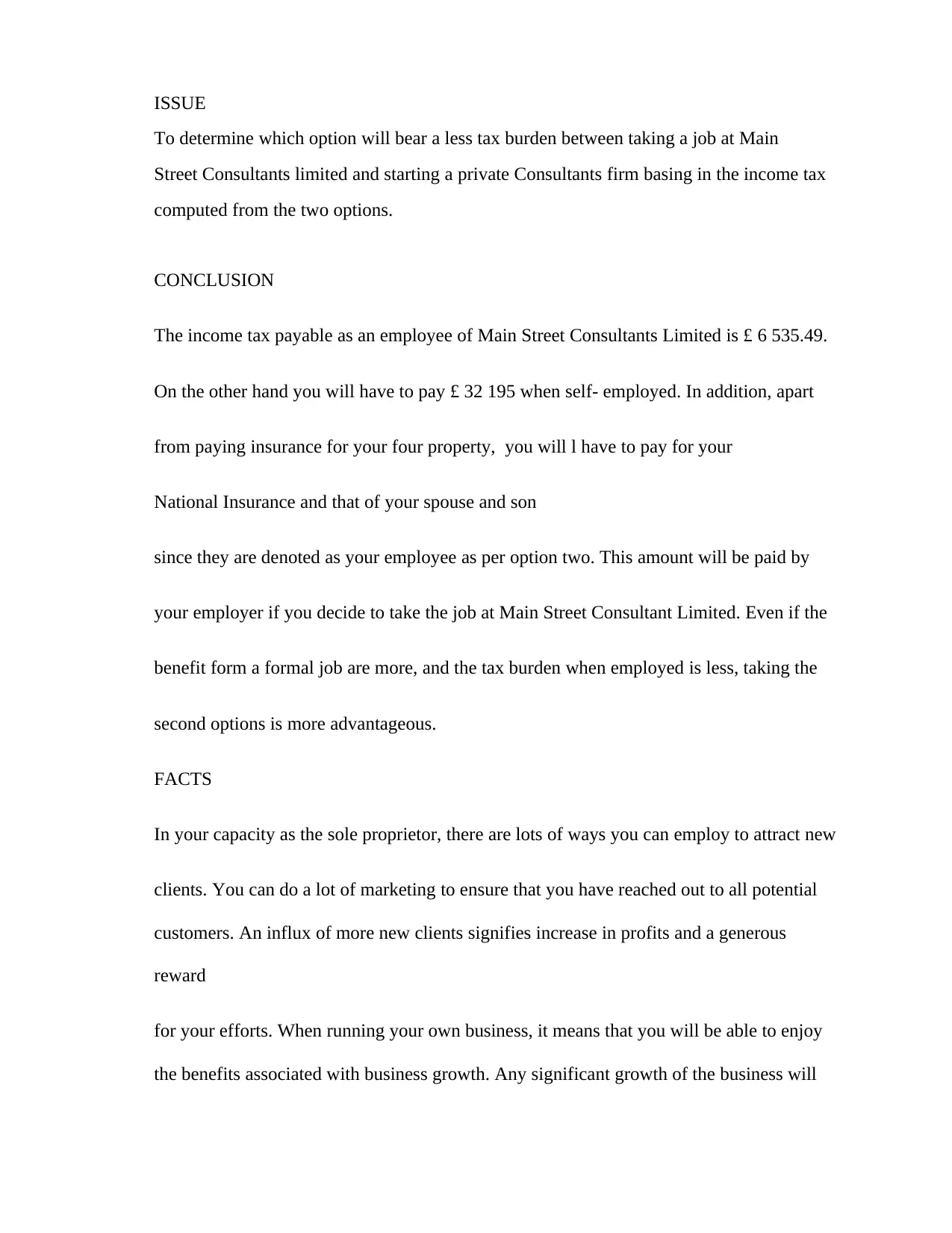

ISSUE

To determine which option will bear a less tax burden between taking a job at Main

Street Consultants limited and starting a private Consultants firm basing in the income tax

computed from the two options.

CONCLUSION

The income tax payable as an employee of Main Street Consultants Limited is £ 6 535.49.

On the other hand you will have to pay £ 32 195 when self- employed. In addition, apart

from paying insurance for your four property, you will l have to pay for your

National Insurance and that of your spouse and son

since they are denoted as your employee as per option two. This amount will be paid by

your employer if you decide to take the job at Main Street Consultant Limited. Even if the

benefit form a formal job are more, and the tax burden when employed is less, taking the

second options is more advantageous.

FACTS

In your capacity as the sole proprietor, there are lots of ways you can employ to attract new

clients. You can do a lot of marketing to ensure that you have reached out to all potential

customers. An influx of more new clients signifies increase in profits and a generous

reward

for your efforts. When running your own business, it means that you will be able to enjoy

the benefits associated with business growth. Any significant growth of the business will

To determine which option will bear a less tax burden between taking a job at Main

Street Consultants limited and starting a private Consultants firm basing in the income tax

computed from the two options.

CONCLUSION

The income tax payable as an employee of Main Street Consultants Limited is £ 6 535.49.

On the other hand you will have to pay £ 32 195 when self- employed. In addition, apart

from paying insurance for your four property, you will l have to pay for your

National Insurance and that of your spouse and son

since they are denoted as your employee as per option two. This amount will be paid by

your employer if you decide to take the job at Main Street Consultant Limited. Even if the

benefit form a formal job are more, and the tax burden when employed is less, taking the

second options is more advantageous.

FACTS

In your capacity as the sole proprietor, there are lots of ways you can employ to attract new

clients. You can do a lot of marketing to ensure that you have reached out to all potential

customers. An influx of more new clients signifies increase in profits and a generous

reward

for your efforts. When running your own business, it means that you will be able to enjoy

the benefits associated with business growth. Any significant growth of the business will

mean an increase in profit and thus increase in your income. This is contrary to the

employment whereas irrespective of how hard you work; your annual salaries will remain

the same even when there is an improvement in the annual profits of the business. No

reward for any extra efforts (Izawa, R. 2015).

Furthermore, since your business is a sole proprietor, there are few formalities required to

start the business as for sole proprietor, the business and the owner are not viewed as

separate entities and thus the liability of the owner to the business is unlimited. On the side

of taxes, only liable income tax will be

taxed. There are no other taxes such Pay As You Earn as compared to formally employed

people. You won’t be taxes on your personal dividends, loan or bond interests, and savings

accounts

As a way of minimizing your tax liability even further, you can use the following legal

Mean of tax relief

Capital Allowances. Capital allowance is a kind of tax relief that is claimed on

capital assets such as machinery, fixtures and fittings, and cars. In your capacity

as a sole proprietor you can claim up to one hundred percent of the taxable

expenditure. Capital allowances claims should be optimized in any manner

possible claiming all available allowances. The area where you can maximize

capital allowances include sales, purchases, repair and new business investments.

Business Property Relief (BPR). BPR is has the potential to remove the whole

value of business in terms of tax relief. Every business owner is eligible for this

employment whereas irrespective of how hard you work; your annual salaries will remain

the same even when there is an improvement in the annual profits of the business. No

reward for any extra efforts (Izawa, R. 2015).

Furthermore, since your business is a sole proprietor, there are few formalities required to

start the business as for sole proprietor, the business and the owner are not viewed as

separate entities and thus the liability of the owner to the business is unlimited. On the side

of taxes, only liable income tax will be

taxed. There are no other taxes such Pay As You Earn as compared to formally employed

people. You won’t be taxes on your personal dividends, loan or bond interests, and savings

accounts

As a way of minimizing your tax liability even further, you can use the following legal

Mean of tax relief

Capital Allowances. Capital allowance is a kind of tax relief that is claimed on

capital assets such as machinery, fixtures and fittings, and cars. In your capacity

as a sole proprietor you can claim up to one hundred percent of the taxable

expenditure. Capital allowances claims should be optimized in any manner

possible claiming all available allowances. The area where you can maximize

capital allowances include sales, purchases, repair and new business investments.

Business Property Relief (BPR). BPR is has the potential to remove the whole

value of business in terms of tax relief. Every business owner is eligible for this

type of relief. However, some conditions like disclosure of startup capital have to

be met before you fully qualify for this kind of relief.

Nevertheless, you will still have to pay property tax on your four apartments. The reason

for this is because you they are personal premises not business inventories. Other

additional taxes that you will have to pay are sales taxes and excise taxes. The rates at

which you will pay these taxes will depend on your level of revenue and how you use

commodities that \re levied with taxes.

Despite the advice in this memorandum, there some unforeseen contingency that you will

have to bear with. Some of these uncertainties include changes in tax rates, change in

regulations relating to tax. The other uncertainty is that this memorandum is written on

the assumption that you do not have any pending tax liability. Accrued taxes attract high

fines and penalties.

My final advice will be you consider self-employment because it comes with so many

other benefits. You will enjoy the freedom of being your own boss and you would suffer

the stress of employment pressure. You will be able to employ some people as the

business grows and thus help in creation of employment. When you run your own

business, You will earn profit and not salary. Profit is not constant since it will grow with

the growth of the business and the earnings will not be like salary which might remain

constant even the company you are serving is making super normal profits (Billings, M.,

& Oats, L. 2014)

Finally, after the comparison of the two options, please go for self-employment.

be met before you fully qualify for this kind of relief.

Nevertheless, you will still have to pay property tax on your four apartments. The reason

for this is because you they are personal premises not business inventories. Other

additional taxes that you will have to pay are sales taxes and excise taxes. The rates at

which you will pay these taxes will depend on your level of revenue and how you use

commodities that \re levied with taxes.

Despite the advice in this memorandum, there some unforeseen contingency that you will

have to bear with. Some of these uncertainties include changes in tax rates, change in

regulations relating to tax. The other uncertainty is that this memorandum is written on

the assumption that you do not have any pending tax liability. Accrued taxes attract high

fines and penalties.

My final advice will be you consider self-employment because it comes with so many

other benefits. You will enjoy the freedom of being your own boss and you would suffer

the stress of employment pressure. You will be able to employ some people as the

business grows and thus help in creation of employment. When you run your own

business, You will earn profit and not salary. Profit is not constant since it will grow with

the growth of the business and the earnings will not be like salary which might remain

constant even the company you are serving is making super normal profits (Billings, M.,

& Oats, L. 2014)

Finally, after the comparison of the two options, please go for self-employment.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

Billings, M., & Oats, L. (2014). Innovation and pragmatism in tax design: Excess

Profits Duty in the UK during the First World War. Accounting History

Review, 24(2-3), 83-101.

Izawa, R. (2015). The Formation of Companies for Tax Avoidance: The

Relationship between UK Multinationals and International Double Taxation in the

Interwar Period. In Business History Conference. Business and Economic History

On-line: Papers Presented at the BHC Annual Meeting (Vol. 13, p. 1). Business

History Conference.

Ivanova, M. (2018). The Multilateral Instrument: Avoidance of Permanent

Establishment Status and the Reservations on behalf of Australia and the

UK. Revenue Law Journal, 25(1).

Billings, M., & Oats, L. (2014). Innovation and pragmatism in tax design: Excess

Profits Duty in the UK during the First World War. Accounting History

Review, 24(2-3), 83-101.

Izawa, R. (2015). The Formation of Companies for Tax Avoidance: The

Relationship between UK Multinationals and International Double Taxation in the

Interwar Period. In Business History Conference. Business and Economic History

On-line: Papers Presented at the BHC Annual Meeting (Vol. 13, p. 1). Business

History Conference.

Ivanova, M. (2018). The Multilateral Instrument: Avoidance of Permanent

Establishment Status and the Reservations on behalf of Australia and the

UK. Revenue Law Journal, 25(1).

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.