HI5020 Corporate Accounting: Financial Analysis of Orica Limited

VerifiedAdded on 2023/06/11

|8

|1665

|126

Report

AI Summary

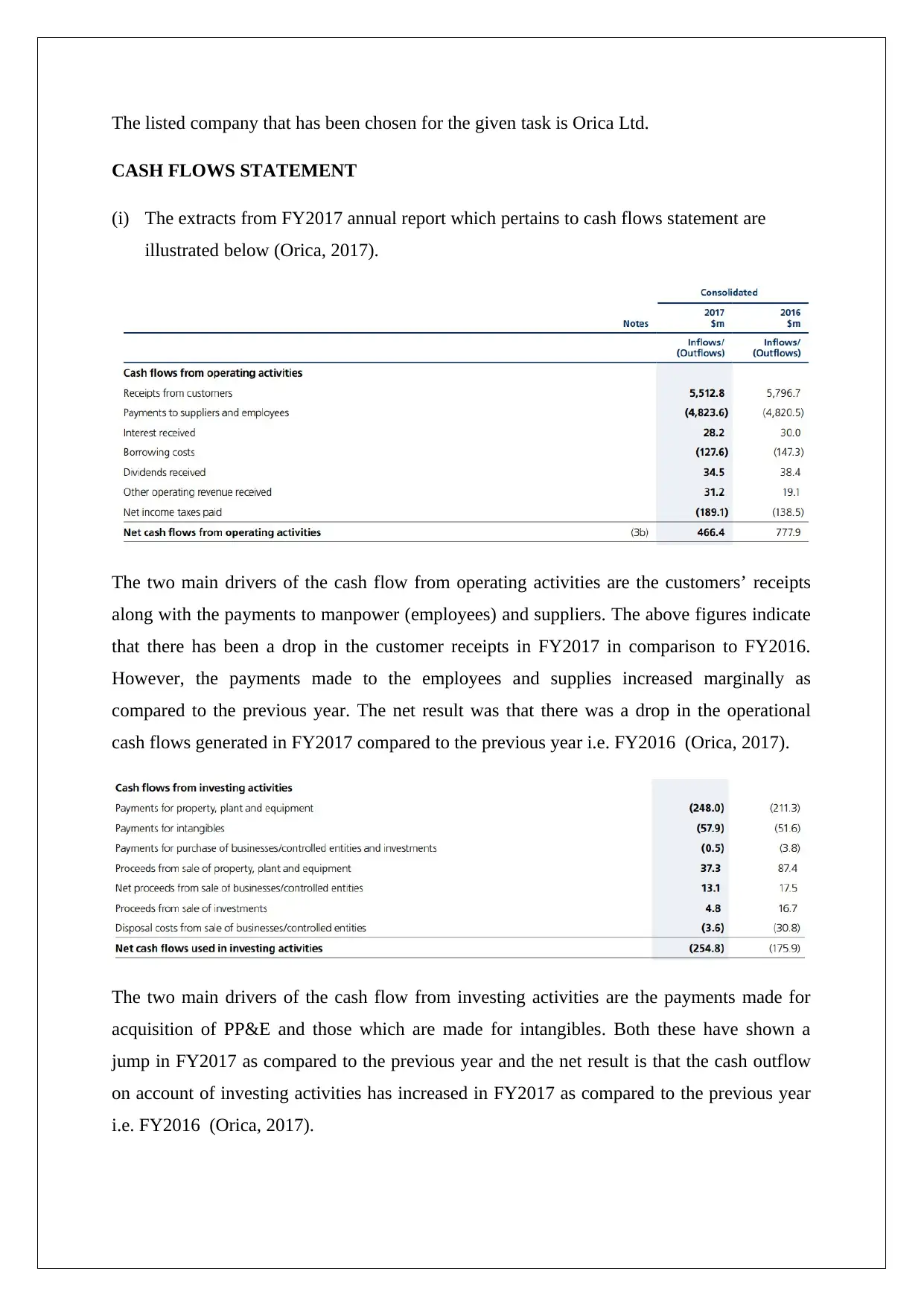

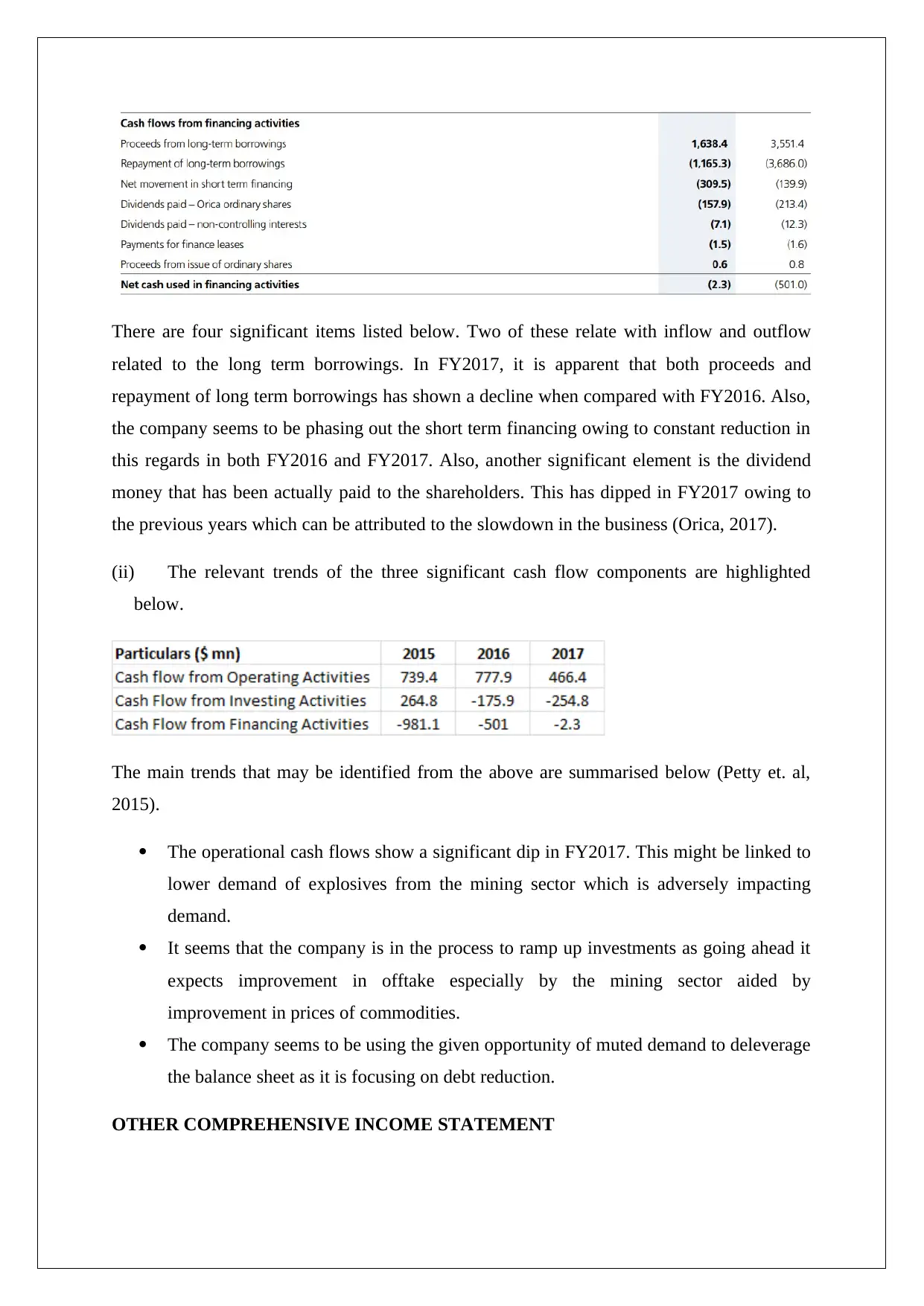

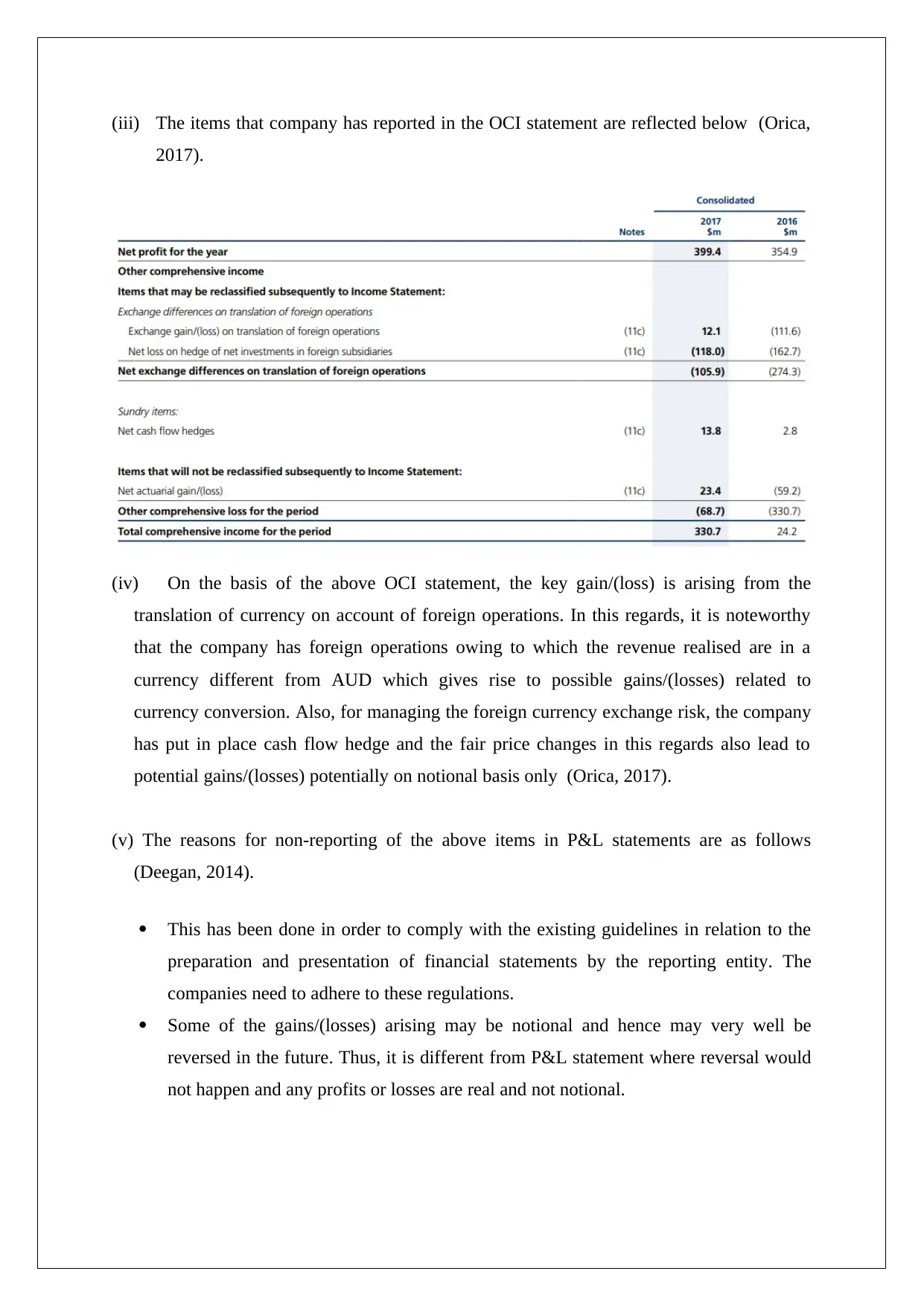

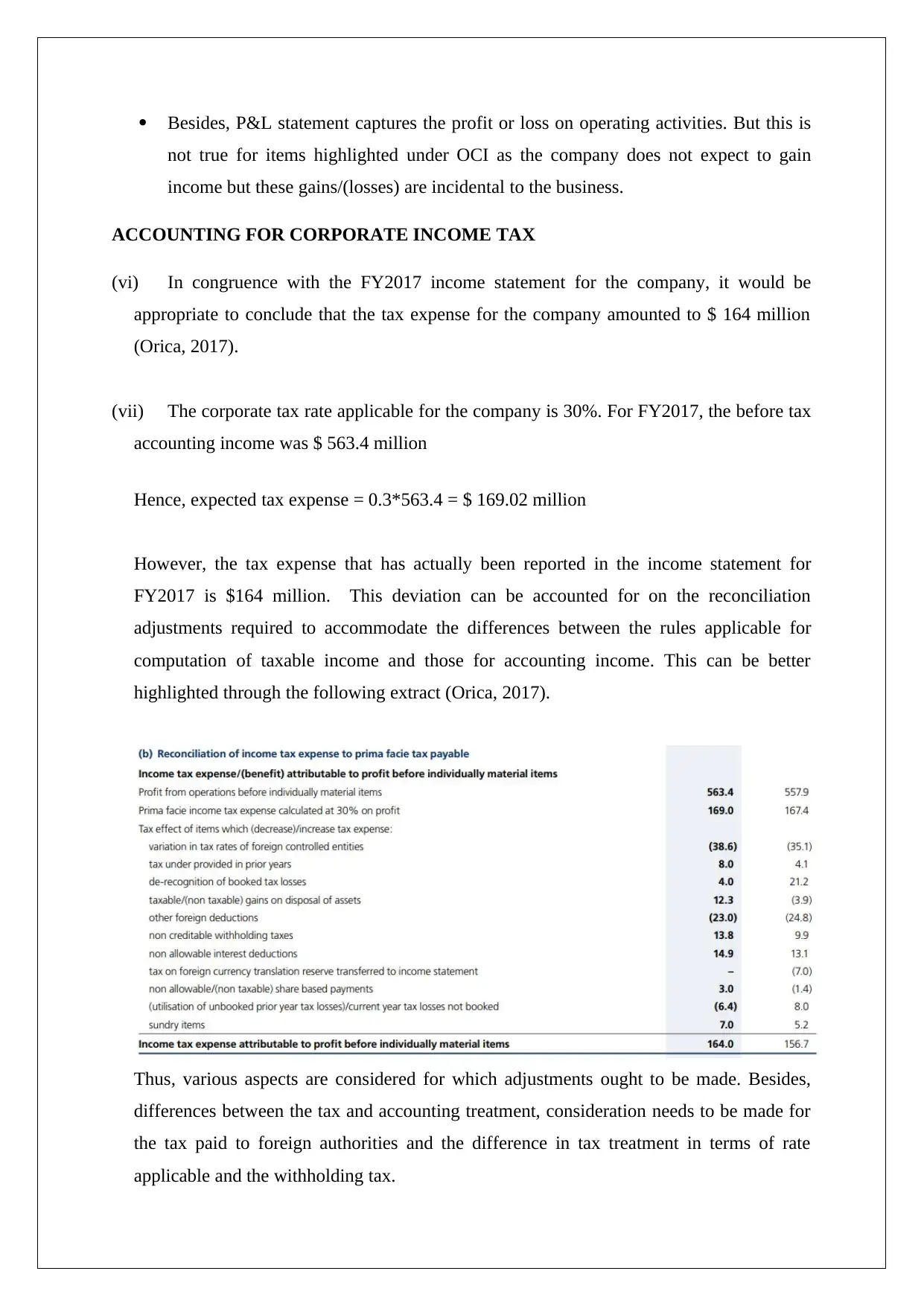

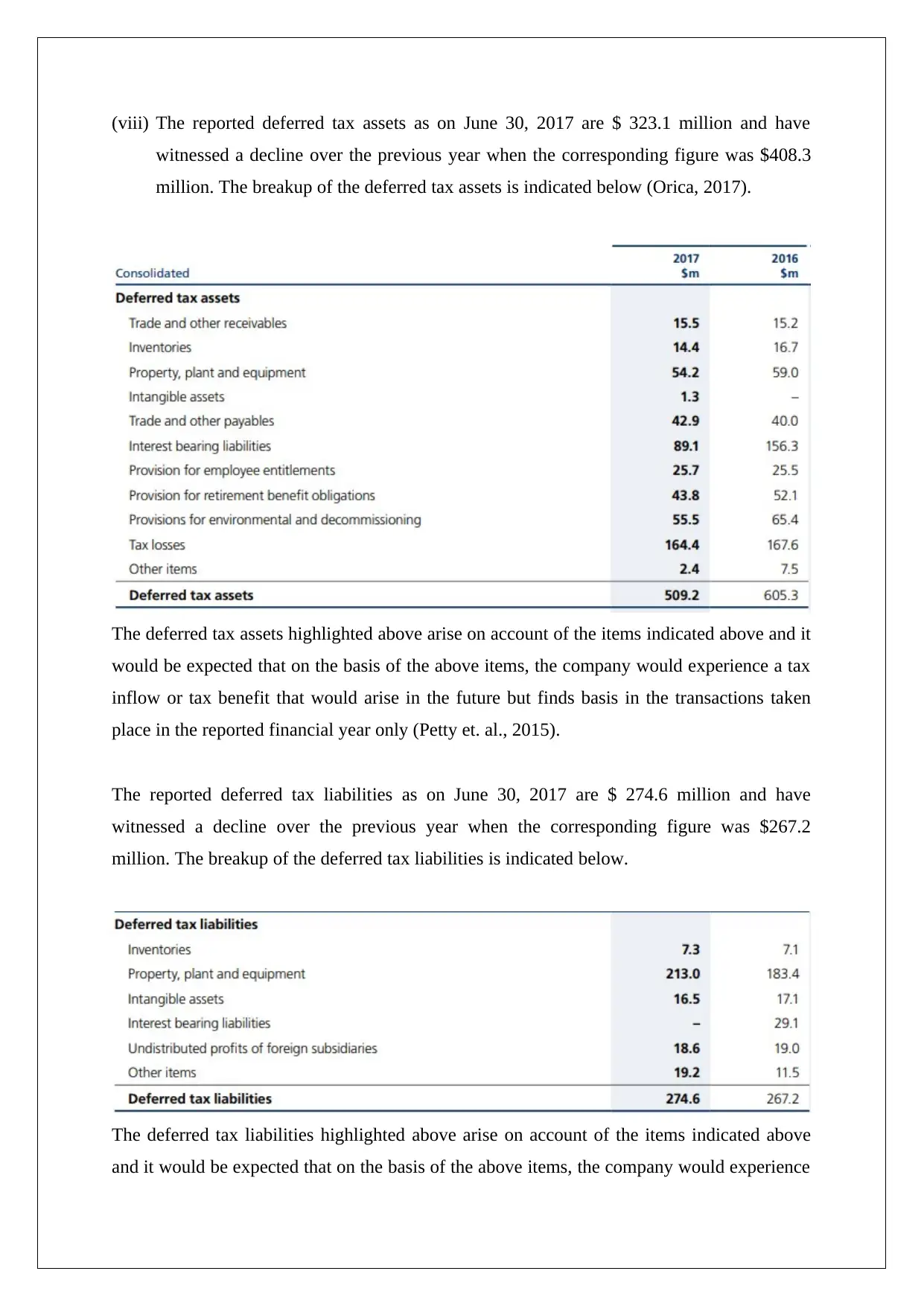

This report provides a comprehensive analysis of Orica Limited's corporate accounting practices, focusing on the company's cash flow statement, other comprehensive income (OCI) statement, and accounting for corporate income tax based on their annual reports. The analysis of the cash flow statement identifies key drivers such as customer receipts, payments to employees and suppliers, and investments in property, plant, and equipment (PP&E). It also highlights trends in operational cash flows, investment strategies, and debt management. The OCI statement analysis explains the impact of foreign currency translations and cash flow hedges on the company's financial performance. Furthermore, the report reconciles the differences between the reported tax expense and the expected tax expense, considering adjustments for taxable income and accounting income differences, foreign tax payments, and withholding tax. Deferred tax assets and liabilities are also examined, along with a discussion on the differences between tax expense and tax paid. The report concludes with a reflection on the complexities of deferred tax assets and liabilities.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.