MSc Financial Management: Ottava PLC US Expansion & Funding Analysis

VerifiedAdded on 2023/05/28

|10

|4203

|261

Report

AI Summary

This report provides a financial analysis of Ottava PLC, a UK-based electric vehicle manufacturer, as it considers expanding its operations into the United States. The analysis explores two primary expansion alternatives: establishing a production unit in the US and forming a joint venture with Fermata Inc. It assesses the feasibility of the US expansion project using Net Present Value (NPV) calculations, considering factors such as initial investment, sales forecasts, operating costs, marketing expenses, and working capital requirements. Sensitivity analysis is conducted to evaluate the impact of changing cash flows on the project's viability. The report also examines different funding strategies, including bank loans, debt securities, and convertible bonds, evaluating their market values and implications for Ottava PLC's capital structure. Furthermore, the report discusses the potential impact of trade barriers, such as tariffs, on the company's international trade activities. The analysis concludes with recommendations based on the NPV calculations, sensitivity analysis, and consideration of relevant market factors.

Msc Accounting and Finance

Table of content

Contents

Table of content....................................................................................................................................1

Introduction...........................................................................................................................................2

Analysis..............................................................................................................................................2

Appendix-1- Expansion into the United States..................................................................................2

Sensitivity Analysis.........................................................................................................................3

Appendix-2........................................................................................................................................5

New Cost of Equity and Weighted Average Cost of Capital...........................................................7

Appendix-3........................................................................................................................................8

Possibility of Joint Venture............................................................................................................9

Virtual Shared Service Centre........................................................................................................9

Business Partner Model to the Finance Function..........................................................................9

1

Table of content

Contents

Table of content....................................................................................................................................1

Introduction...........................................................................................................................................2

Analysis..............................................................................................................................................2

Appendix-1- Expansion into the United States..................................................................................2

Sensitivity Analysis.........................................................................................................................3

Appendix-2........................................................................................................................................5

New Cost of Equity and Weighted Average Cost of Capital...........................................................7

Appendix-3........................................................................................................................................8

Possibility of Joint Venture............................................................................................................9

Virtual Shared Service Centre........................................................................................................9

Business Partner Model to the Finance Function..........................................................................9

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Ottava PLC is a UK resident Company. The company specialised in manufacturing of electric vehicle.

The company was founded in 1990 and marks its presence in commercial vehicle space. It is the

largest manufacturer of UK in commercial space. The company has very less reliance on debt since

its very start of operation and has relied more on internal funds and shareholder’s equity for funding

of day to day operations of the company. Thus, company is compliant with pecking order theory. The

current share price of the company is Sterling 5.56 and is in a growth phase and expected to grow

continuously year on year basis.

The company is proposing to expand its operation in US via expanding its production unit in the

country itself as an alternative 1 and via a joint venture with Fermata Inc. in US as an alternative 2

and company is also thinking of modes of procuring fund from market via three strategies i.e namely

bank loan, debt instrument and convertible debt instrument.

For the purpose of above analysis, Ottava PLC has hired Marcato Consulting to advise on this matter,

The advise report has been detailed under three parts in accordance with Appendix presented in the

report.

Analysis

Appendix-1- Expansion into the United States

Under, the first analysis the company is seeking to expand it business operations in US while

maintaining its production base in the UK itself. The manufacture shall take place in Leeds. For the

purpose of conducting a feasibility analysis of the project, Net Present Value of the project has been

computed based on the following assumptions and facts:

(a) Cost of feasibility study has been considered a sunk cost. However, tax impact of the cost has

been considered;

(b) Cost of setting up new operations has been considered at 180 Million sterling out of which 50%

shall be eligible for tax deduction subject to a 25% diminishing balance deduction;

(c) The sales of vehicle has been forecasted at 1000 vehicles at a price of USD 2,50,000 which shall

increase by 10% and 3% respectively;

(d) The Scrap value of the depreciating asset shall be 10 Million Sterling while the balance of the

remaining non depreciable asset shall remain consistent at 90 Mio post 5 years of operations of

business;

(e) The cost of operations in US shall stand at Sterling 1,62,500/- which shall increase as per the rate

of inflation in UK which is 2% and the volume shall increase by 10% in terms of sales. Assuming

whatever produced is sold;

(f) The marketing cost shall stand at 90 Million USD and 20 Million USD for year 1 and 3 respectively;

(g) Incremental Fixed Cost shall stand at Sterling 7 Million and shall increase as per inflation rate of

UK which is 2%;

(h) Working Capital shall stand at 10% of Sales value and shall be realised at the end of the project

i.e. 5 years;

(i) Tax rate in UK has been taken at 20%;

(j) Exchange rate has been taken at 1 Sterling = 1.3 USD and shall change every year based on

inflation in terms of relative purchase power parity;

(k) Discount rate for the project has been taken at 9%

On the basis of above fact, the computation has been detailed here-in-below:

2

Ottava PLC is a UK resident Company. The company specialised in manufacturing of electric vehicle.

The company was founded in 1990 and marks its presence in commercial vehicle space. It is the

largest manufacturer of UK in commercial space. The company has very less reliance on debt since

its very start of operation and has relied more on internal funds and shareholder’s equity for funding

of day to day operations of the company. Thus, company is compliant with pecking order theory. The

current share price of the company is Sterling 5.56 and is in a growth phase and expected to grow

continuously year on year basis.

The company is proposing to expand its operation in US via expanding its production unit in the

country itself as an alternative 1 and via a joint venture with Fermata Inc. in US as an alternative 2

and company is also thinking of modes of procuring fund from market via three strategies i.e namely

bank loan, debt instrument and convertible debt instrument.

For the purpose of above analysis, Ottava PLC has hired Marcato Consulting to advise on this matter,

The advise report has been detailed under three parts in accordance with Appendix presented in the

report.

Analysis

Appendix-1- Expansion into the United States

Under, the first analysis the company is seeking to expand it business operations in US while

maintaining its production base in the UK itself. The manufacture shall take place in Leeds. For the

purpose of conducting a feasibility analysis of the project, Net Present Value of the project has been

computed based on the following assumptions and facts:

(a) Cost of feasibility study has been considered a sunk cost. However, tax impact of the cost has

been considered;

(b) Cost of setting up new operations has been considered at 180 Million sterling out of which 50%

shall be eligible for tax deduction subject to a 25% diminishing balance deduction;

(c) The sales of vehicle has been forecasted at 1000 vehicles at a price of USD 2,50,000 which shall

increase by 10% and 3% respectively;

(d) The Scrap value of the depreciating asset shall be 10 Million Sterling while the balance of the

remaining non depreciable asset shall remain consistent at 90 Mio post 5 years of operations of

business;

(e) The cost of operations in US shall stand at Sterling 1,62,500/- which shall increase as per the rate

of inflation in UK which is 2% and the volume shall increase by 10% in terms of sales. Assuming

whatever produced is sold;

(f) The marketing cost shall stand at 90 Million USD and 20 Million USD for year 1 and 3 respectively;

(g) Incremental Fixed Cost shall stand at Sterling 7 Million and shall increase as per inflation rate of

UK which is 2%;

(h) Working Capital shall stand at 10% of Sales value and shall be realised at the end of the project

i.e. 5 years;

(i) Tax rate in UK has been taken at 20%;

(j) Exchange rate has been taken at 1 Sterling = 1.3 USD and shall change every year based on

inflation in terms of relative purchase power parity;

(k) Discount rate for the project has been taken at 9%

On the basis of above fact, the computation has been detailed here-in-below:

2

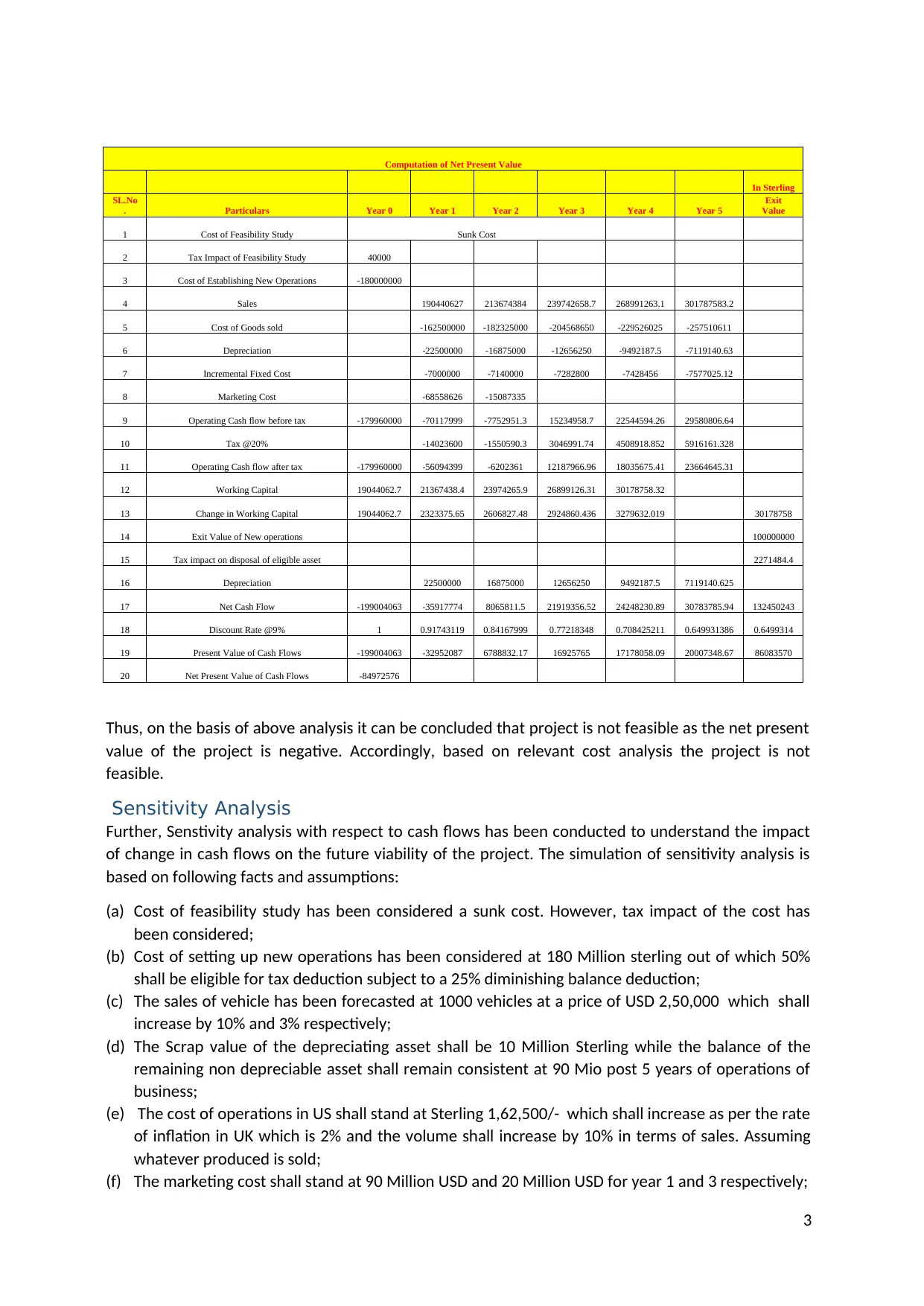

Computation of Net Present Value

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Exit

Value

1 Cost of Feasibility Study Sunk Cost

2 Tax Impact of Feasibility Study 40000

3 Cost of Establishing New Operations -180000000

4 Sales 190440627 213674384 239742658.7 268991263.1 301787583.2

5 Cost of Goods sold -162500000 -182325000 -204568650 -229526025 -257510611

6 Depreciation -22500000 -16875000 -12656250 -9492187.5 -7119140.63

7 Incremental Fixed Cost -7000000 -7140000 -7282800 -7428456 -7577025.12

8 Marketing Cost -68558626 -15087335

9 Operating Cash flow before tax -179960000 -70117999 -7752951.3 15234958.7 22544594.26 29580806.64

10 Tax @20% -14023600 -1550590.3 3046991.74 4508918.852 5916161.328

11 Operating Cash flow after tax -179960000 -56094399 -6202361 12187966.96 18035675.41 23664645.31

12 Working Capital 19044062.7 21367438.4 23974265.9 26899126.31 30178758.32

13 Change in Working Capital 19044062.7 2323375.65 2606827.48 2924860.436 3279632.019 30178758

14 Exit Value of New operations 100000000

15 Tax impact on disposal of eligible asset 2271484.4

16 Depreciation 22500000 16875000 12656250 9492187.5 7119140.625

17 Net Cash Flow -199004063 -35917774 8065811.5 21919356.52 24248230.89 30783785.94 132450243

18 Discount Rate @9% 1 0.91743119 0.84167999 0.77218348 0.708425211 0.649931386 0.6499314

19 Present Value of Cash Flows -199004063 -32952087 6788832.17 16925765 17178058.09 20007348.67 86083570

20 Net Present Value of Cash Flows -84972576

Thus, on the basis of above analysis it can be concluded that project is not feasible as the net present

value of the project is negative. Accordingly, based on relevant cost analysis the project is not

feasible.

Sensitivity Analysis

Further, Senstivity analysis with respect to cash flows has been conducted to understand the impact

of change in cash flows on the future viability of the project. The simulation of sensitivity analysis is

based on following facts and assumptions:

(a) Cost of feasibility study has been considered a sunk cost. However, tax impact of the cost has

been considered;

(b) Cost of setting up new operations has been considered at 180 Million sterling out of which 50%

shall be eligible for tax deduction subject to a 25% diminishing balance deduction;

(c) The sales of vehicle has been forecasted at 1000 vehicles at a price of USD 2,50,000 which shall

increase by 10% and 3% respectively;

(d) The Scrap value of the depreciating asset shall be 10 Million Sterling while the balance of the

remaining non depreciable asset shall remain consistent at 90 Mio post 5 years of operations of

business;

(e) The cost of operations in US shall stand at Sterling 1,62,500/- which shall increase as per the rate

of inflation in UK which is 2% and the volume shall increase by 10% in terms of sales. Assuming

whatever produced is sold;

(f) The marketing cost shall stand at 90 Million USD and 20 Million USD for year 1 and 3 respectively;

3

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Exit

Value

1 Cost of Feasibility Study Sunk Cost

2 Tax Impact of Feasibility Study 40000

3 Cost of Establishing New Operations -180000000

4 Sales 190440627 213674384 239742658.7 268991263.1 301787583.2

5 Cost of Goods sold -162500000 -182325000 -204568650 -229526025 -257510611

6 Depreciation -22500000 -16875000 -12656250 -9492187.5 -7119140.63

7 Incremental Fixed Cost -7000000 -7140000 -7282800 -7428456 -7577025.12

8 Marketing Cost -68558626 -15087335

9 Operating Cash flow before tax -179960000 -70117999 -7752951.3 15234958.7 22544594.26 29580806.64

10 Tax @20% -14023600 -1550590.3 3046991.74 4508918.852 5916161.328

11 Operating Cash flow after tax -179960000 -56094399 -6202361 12187966.96 18035675.41 23664645.31

12 Working Capital 19044062.7 21367438.4 23974265.9 26899126.31 30178758.32

13 Change in Working Capital 19044062.7 2323375.65 2606827.48 2924860.436 3279632.019 30178758

14 Exit Value of New operations 100000000

15 Tax impact on disposal of eligible asset 2271484.4

16 Depreciation 22500000 16875000 12656250 9492187.5 7119140.625

17 Net Cash Flow -199004063 -35917774 8065811.5 21919356.52 24248230.89 30783785.94 132450243

18 Discount Rate @9% 1 0.91743119 0.84167999 0.77218348 0.708425211 0.649931386 0.6499314

19 Present Value of Cash Flows -199004063 -32952087 6788832.17 16925765 17178058.09 20007348.67 86083570

20 Net Present Value of Cash Flows -84972576

Thus, on the basis of above analysis it can be concluded that project is not feasible as the net present

value of the project is negative. Accordingly, based on relevant cost analysis the project is not

feasible.

Sensitivity Analysis

Further, Senstivity analysis with respect to cash flows has been conducted to understand the impact

of change in cash flows on the future viability of the project. The simulation of sensitivity analysis is

based on following facts and assumptions:

(a) Cost of feasibility study has been considered a sunk cost. However, tax impact of the cost has

been considered;

(b) Cost of setting up new operations has been considered at 180 Million sterling out of which 50%

shall be eligible for tax deduction subject to a 25% diminishing balance deduction;

(c) The sales of vehicle has been forecasted at 1000 vehicles at a price of USD 2,50,000 which shall

increase by 10% and 3% respectively;

(d) The Scrap value of the depreciating asset shall be 10 Million Sterling while the balance of the

remaining non depreciable asset shall remain consistent at 90 Mio post 5 years of operations of

business;

(e) The cost of operations in US shall stand at Sterling 1,62,500/- which shall increase as per the rate

of inflation in UK which is 2% and the volume shall increase by 10% in terms of sales. Assuming

whatever produced is sold;

(f) The marketing cost shall stand at 90 Million USD and 20 Million USD for year 1 and 3 respectively;

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

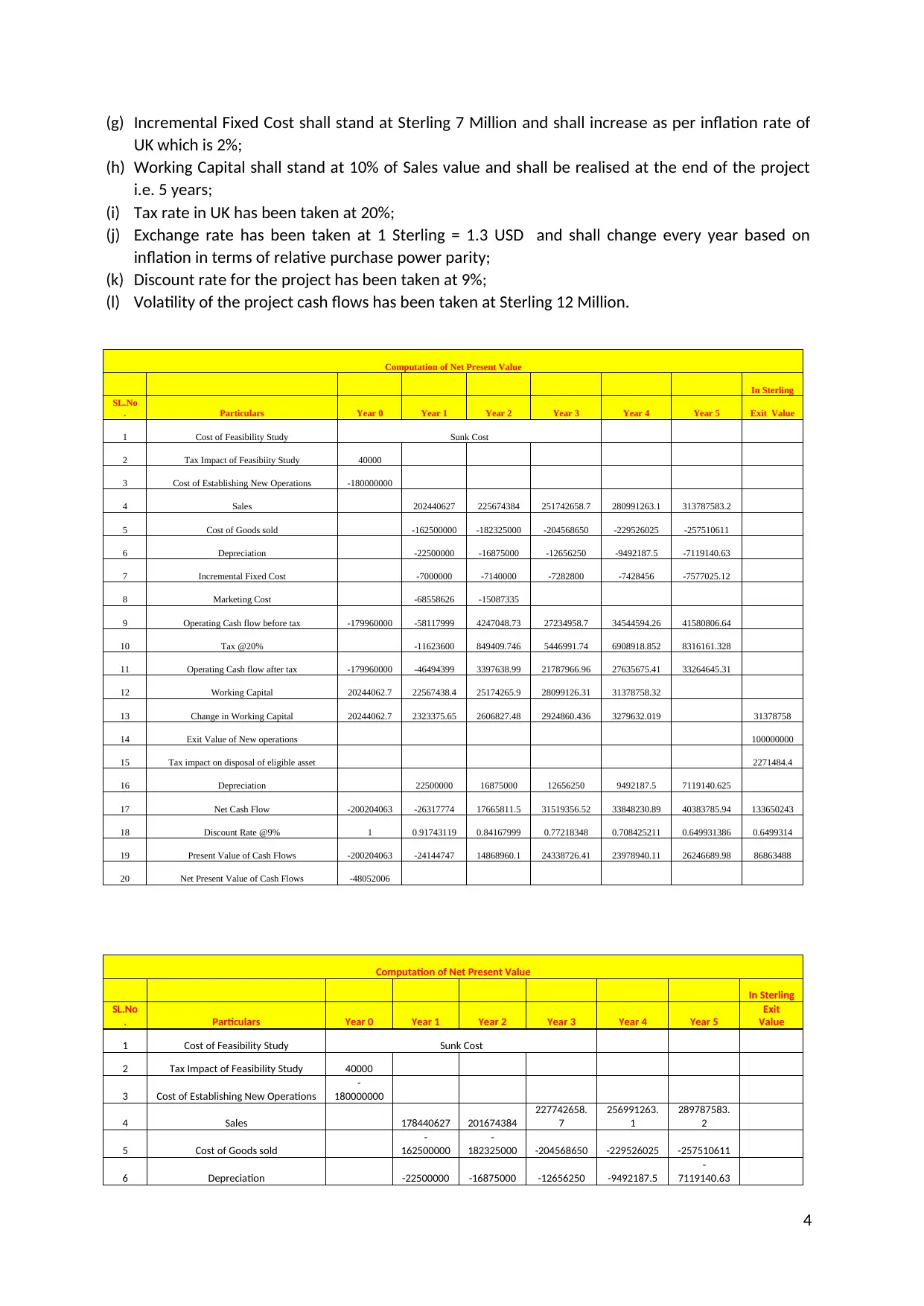

(g) Incremental Fixed Cost shall stand at Sterling 7 Million and shall increase as per inflation rate of

UK which is 2%;

(h) Working Capital shall stand at 10% of Sales value and shall be realised at the end of the project

i.e. 5 years;

(i) Tax rate in UK has been taken at 20%;

(j) Exchange rate has been taken at 1 Sterling = 1.3 USD and shall change every year based on

inflation in terms of relative purchase power parity;

(k) Discount rate for the project has been taken at 9%;

(l) Volatility of the project cash flows has been taken at Sterling 12 Million.

Computation of Net Present Value

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Exit Value

1 Cost of Feasibility Study Sunk Cost

2 Tax Impact of Feasibiity Study 40000

3 Cost of Establishing New Operations -180000000

4 Sales 202440627 225674384 251742658.7 280991263.1 313787583.2

5 Cost of Goods sold -162500000 -182325000 -204568650 -229526025 -257510611

6 Depreciation -22500000 -16875000 -12656250 -9492187.5 -7119140.63

7 Incremental Fixed Cost -7000000 -7140000 -7282800 -7428456 -7577025.12

8 Marketing Cost -68558626 -15087335

9 Operating Cash flow before tax -179960000 -58117999 4247048.73 27234958.7 34544594.26 41580806.64

10 Tax @20% -11623600 849409.746 5446991.74 6908918.852 8316161.328

11 Operating Cash flow after tax -179960000 -46494399 3397638.99 21787966.96 27635675.41 33264645.31

12 Working Capital 20244062.7 22567438.4 25174265.9 28099126.31 31378758.32

13 Change in Working Capital 20244062.7 2323375.65 2606827.48 2924860.436 3279632.019 31378758

14 Exit Value of New operations 100000000

15 Tax impact on disposal of eligible asset 2271484.4

16 Depreciation 22500000 16875000 12656250 9492187.5 7119140.625

17 Net Cash Flow -200204063 -26317774 17665811.5 31519356.52 33848230.89 40383785.94 133650243

18 Discount Rate @9% 1 0.91743119 0.84167999 0.77218348 0.708425211 0.649931386 0.6499314

19 Present Value of Cash Flows -200204063 -24144747 14868960.1 24338726.41 23978940.11 26246689.98 86863488

20 Net Present Value of Cash Flows -48052006

Computation of Net Present Value

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Exit

Value

1 Cost of Feasibility Study Sunk Cost

2 Tax Impact of Feasibility Study 40000

3 Cost of Establishing New Operations

-

180000000

4 Sales 178440627 201674384

227742658.

7

256991263.

1

289787583.

2

5 Cost of Goods sold

-

162500000

-

182325000 -204568650 -229526025 -257510611

6 Depreciation -22500000 -16875000 -12656250 -9492187.5

-

7119140.63

4

UK which is 2%;

(h) Working Capital shall stand at 10% of Sales value and shall be realised at the end of the project

i.e. 5 years;

(i) Tax rate in UK has been taken at 20%;

(j) Exchange rate has been taken at 1 Sterling = 1.3 USD and shall change every year based on

inflation in terms of relative purchase power parity;

(k) Discount rate for the project has been taken at 9%;

(l) Volatility of the project cash flows has been taken at Sterling 12 Million.

Computation of Net Present Value

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Exit Value

1 Cost of Feasibility Study Sunk Cost

2 Tax Impact of Feasibiity Study 40000

3 Cost of Establishing New Operations -180000000

4 Sales 202440627 225674384 251742658.7 280991263.1 313787583.2

5 Cost of Goods sold -162500000 -182325000 -204568650 -229526025 -257510611

6 Depreciation -22500000 -16875000 -12656250 -9492187.5 -7119140.63

7 Incremental Fixed Cost -7000000 -7140000 -7282800 -7428456 -7577025.12

8 Marketing Cost -68558626 -15087335

9 Operating Cash flow before tax -179960000 -58117999 4247048.73 27234958.7 34544594.26 41580806.64

10 Tax @20% -11623600 849409.746 5446991.74 6908918.852 8316161.328

11 Operating Cash flow after tax -179960000 -46494399 3397638.99 21787966.96 27635675.41 33264645.31

12 Working Capital 20244062.7 22567438.4 25174265.9 28099126.31 31378758.32

13 Change in Working Capital 20244062.7 2323375.65 2606827.48 2924860.436 3279632.019 31378758

14 Exit Value of New operations 100000000

15 Tax impact on disposal of eligible asset 2271484.4

16 Depreciation 22500000 16875000 12656250 9492187.5 7119140.625

17 Net Cash Flow -200204063 -26317774 17665811.5 31519356.52 33848230.89 40383785.94 133650243

18 Discount Rate @9% 1 0.91743119 0.84167999 0.77218348 0.708425211 0.649931386 0.6499314

19 Present Value of Cash Flows -200204063 -24144747 14868960.1 24338726.41 23978940.11 26246689.98 86863488

20 Net Present Value of Cash Flows -48052006

Computation of Net Present Value

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Exit

Value

1 Cost of Feasibility Study Sunk Cost

2 Tax Impact of Feasibility Study 40000

3 Cost of Establishing New Operations

-

180000000

4 Sales 178440627 201674384

227742658.

7

256991263.

1

289787583.

2

5 Cost of Goods sold

-

162500000

-

182325000 -204568650 -229526025 -257510611

6 Depreciation -22500000 -16875000 -12656250 -9492187.5

-

7119140.63

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Computation of Net Present Value

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Exit

Value

7 Incremental Fixed Cost -7000000 -7140000 -7282800 -7428456

-

7577025.12

8 Marketing Cost -68558626 -15087335

9 Operating Cash flow before tax

-

179960000 -82117999 -19752951

3234958.70

1

10544594.2

6

17580806.6

4

10 Tax @20% -16423600

-

3950590.3

646991.740

1

2108918.85

2

3516161.32

8

11 Operating Cash flow after tax

-

179960000 -65694399 -15802361 2587966.96 8435675.41

14064645.3

1

12 Working Capital

17844062.

7

20167438.

4

22774265.

9

25699126.3

1

28978758.3

2

13 Change in Working Capital

17844062.

7

2323375.6

5

2606827.4

8

2924860.43

6

3279632.01

9 28978758

14 Exit Value of New operations

10000000

0

15

Tax impact on disposal of eligible

asset 2271484.4

16 Depreciation 22500000 16875000 12656250 9492187.5

7119140.62

5

17 Net Cash Flow

-

197804063 -45517774

-

1534188.5

12319356.5

2

14648230.8

9

21183785.9

4

13125024

3

18 Discount Rate @9% 1

0.9174311

9

0.8416799

9 0.77218348

0.70842521

1

0.64993138

6 0.6499314

19 Present Value of Cash Flows

-

197804063 -41759426

-

1291295.8

9512803.59

3

10377176.0

6

13768007.3

6 85303652

20 Net Present Value of Cash Flows

-

121893145

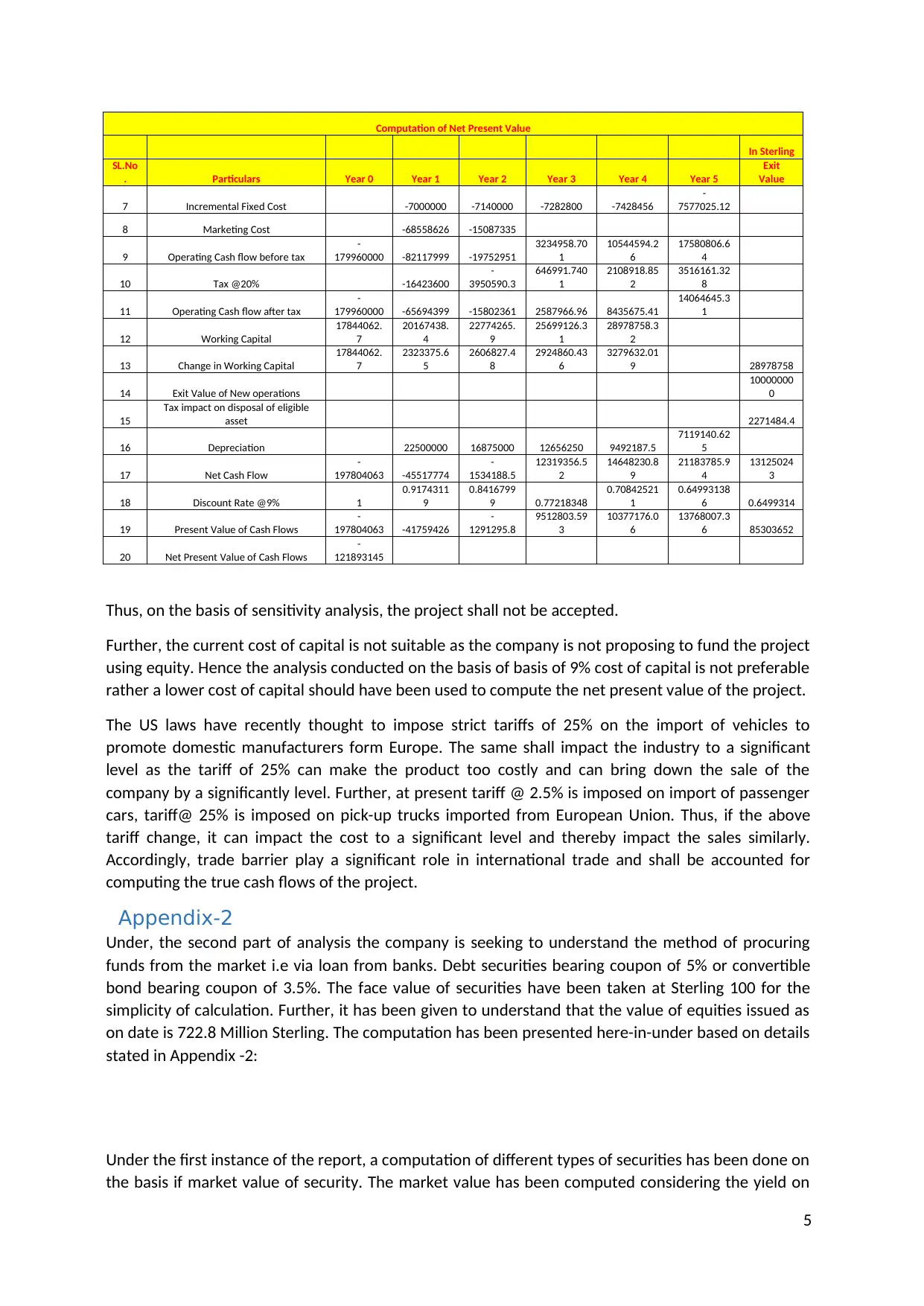

Thus, on the basis of sensitivity analysis, the project shall not be accepted.

Further, the current cost of capital is not suitable as the company is not proposing to fund the project

using equity. Hence the analysis conducted on the basis of basis of 9% cost of capital is not preferable

rather a lower cost of capital should have been used to compute the net present value of the project.

The US laws have recently thought to impose strict tariffs of 25% on the import of vehicles to

promote domestic manufacturers form Europe. The same shall impact the industry to a significant

level as the tariff of 25% can make the product too costly and can bring down the sale of the

company by a significantly level. Further, at present tariff @ 2.5% is imposed on import of passenger

cars, tariff@ 25% is imposed on pick-up trucks imported from European Union. Thus, if the above

tariff change, it can impact the cost to a significant level and thereby impact the sales similarly.

Accordingly, trade barrier play a significant role in international trade and shall be accounted for

computing the true cash flows of the project.

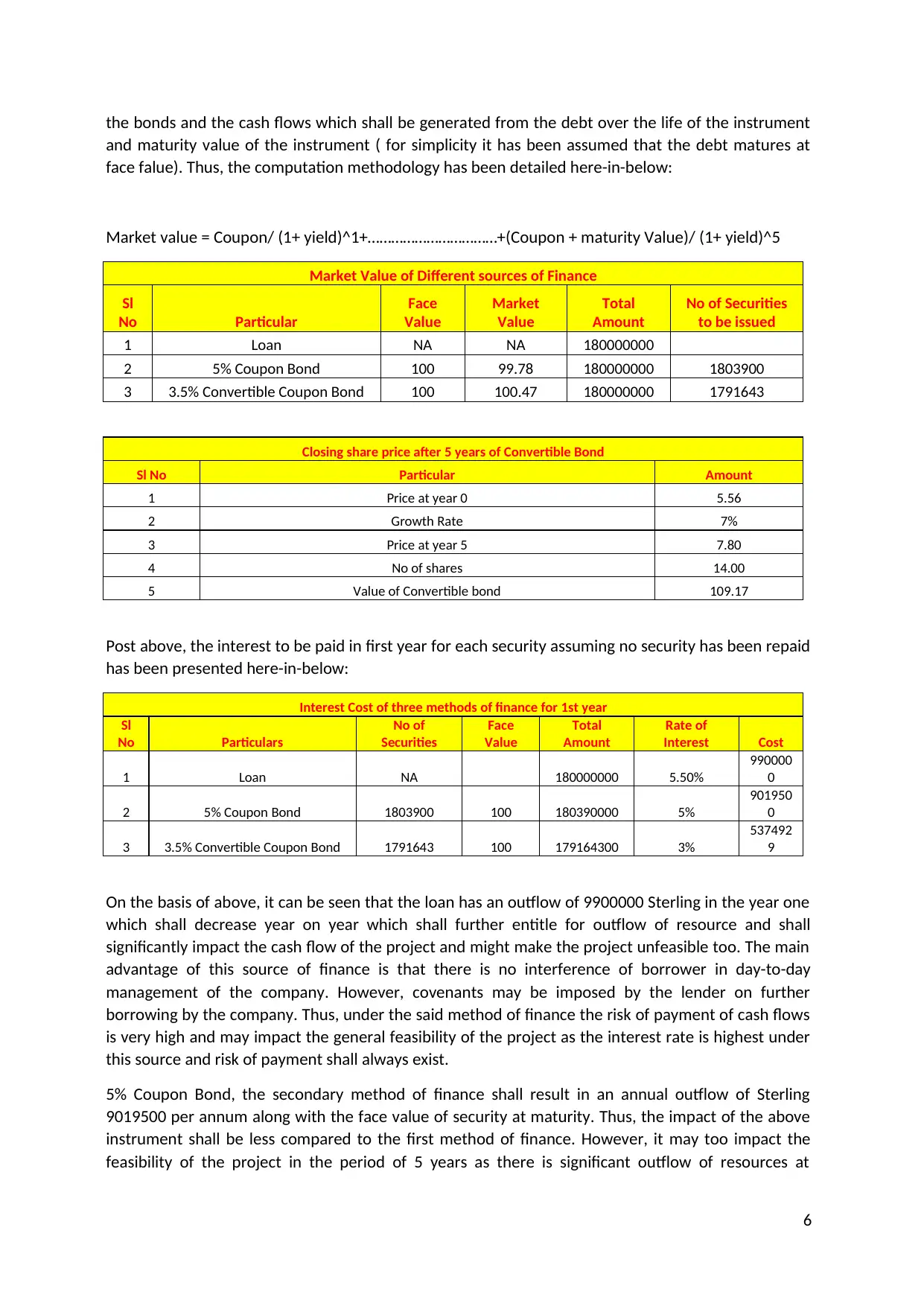

Appendix-2

Under, the second part of analysis the company is seeking to understand the method of procuring

funds from the market i.e via loan from banks. Debt securities bearing coupon of 5% or convertible

bond bearing coupon of 3.5%. The face value of securities have been taken at Sterling 100 for the

simplicity of calculation. Further, it has been given to understand that the value of equities issued as

on date is 722.8 Million Sterling. The computation has been presented here-in-under based on details

stated in Appendix -2:

Under the first instance of the report, a computation of different types of securities has been done on

the basis if market value of security. The market value has been computed considering the yield on

5

In Sterling

SL.No

. Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Exit

Value

7 Incremental Fixed Cost -7000000 -7140000 -7282800 -7428456

-

7577025.12

8 Marketing Cost -68558626 -15087335

9 Operating Cash flow before tax

-

179960000 -82117999 -19752951

3234958.70

1

10544594.2

6

17580806.6

4

10 Tax @20% -16423600

-

3950590.3

646991.740

1

2108918.85

2

3516161.32

8

11 Operating Cash flow after tax

-

179960000 -65694399 -15802361 2587966.96 8435675.41

14064645.3

1

12 Working Capital

17844062.

7

20167438.

4

22774265.

9

25699126.3

1

28978758.3

2

13 Change in Working Capital

17844062.

7

2323375.6

5

2606827.4

8

2924860.43

6

3279632.01

9 28978758

14 Exit Value of New operations

10000000

0

15

Tax impact on disposal of eligible

asset 2271484.4

16 Depreciation 22500000 16875000 12656250 9492187.5

7119140.62

5

17 Net Cash Flow

-

197804063 -45517774

-

1534188.5

12319356.5

2

14648230.8

9

21183785.9

4

13125024

3

18 Discount Rate @9% 1

0.9174311

9

0.8416799

9 0.77218348

0.70842521

1

0.64993138

6 0.6499314

19 Present Value of Cash Flows

-

197804063 -41759426

-

1291295.8

9512803.59

3

10377176.0

6

13768007.3

6 85303652

20 Net Present Value of Cash Flows

-

121893145

Thus, on the basis of sensitivity analysis, the project shall not be accepted.

Further, the current cost of capital is not suitable as the company is not proposing to fund the project

using equity. Hence the analysis conducted on the basis of basis of 9% cost of capital is not preferable

rather a lower cost of capital should have been used to compute the net present value of the project.

The US laws have recently thought to impose strict tariffs of 25% on the import of vehicles to

promote domestic manufacturers form Europe. The same shall impact the industry to a significant

level as the tariff of 25% can make the product too costly and can bring down the sale of the

company by a significantly level. Further, at present tariff @ 2.5% is imposed on import of passenger

cars, tariff@ 25% is imposed on pick-up trucks imported from European Union. Thus, if the above

tariff change, it can impact the cost to a significant level and thereby impact the sales similarly.

Accordingly, trade barrier play a significant role in international trade and shall be accounted for

computing the true cash flows of the project.

Appendix-2

Under, the second part of analysis the company is seeking to understand the method of procuring

funds from the market i.e via loan from banks. Debt securities bearing coupon of 5% or convertible

bond bearing coupon of 3.5%. The face value of securities have been taken at Sterling 100 for the

simplicity of calculation. Further, it has been given to understand that the value of equities issued as

on date is 722.8 Million Sterling. The computation has been presented here-in-under based on details

stated in Appendix -2:

Under the first instance of the report, a computation of different types of securities has been done on

the basis if market value of security. The market value has been computed considering the yield on

5

the bonds and the cash flows which shall be generated from the debt over the life of the instrument

and maturity value of the instrument ( for simplicity it has been assumed that the debt matures at

face falue). Thus, the computation methodology has been detailed here-in-below:

Market value = Coupon/ (1+ yield)^1+……………………………+(Coupon + maturity Value)/ (1+ yield)^5

Market Value of Different sources of Finance

Sl

No Particular

Face

Value

Market

Value

Total

Amount

No of Securities

to be issued

1 Loan NA NA 180000000

2 5% Coupon Bond 100 99.78 180000000 1803900

3 3.5% Convertible Coupon Bond 100 100.47 180000000 1791643

Closing share price after 5 years of Convertible Bond

Sl No Particular Amount

1 Price at year 0 5.56

2 Growth Rate 7%

3 Price at year 5 7.80

4 No of shares 14.00

5 Value of Convertible bond 109.17

Post above, the interest to be paid in first year for each security assuming no security has been repaid

has been presented here-in-below:

Interest Cost of three methods of finance for 1st year

Sl

No Particulars

No of

Securities

Face

Value

Total

Amount

Rate of

Interest Cost

1 Loan NA 180000000 5.50%

990000

0

2 5% Coupon Bond 1803900 100 180390000 5%

901950

0

3 3.5% Convertible Coupon Bond 1791643 100 179164300 3%

537492

9

On the basis of above, it can be seen that the loan has an outflow of 9900000 Sterling in the year one

which shall decrease year on year which shall further entitle for outflow of resource and shall

significantly impact the cash flow of the project and might make the project unfeasible too. The main

advantage of this source of finance is that there is no interference of borrower in day-to-day

management of the company. However, covenants may be imposed by the lender on further

borrowing by the company. Thus, under the said method of finance the risk of payment of cash flows

is very high and may impact the general feasibility of the project as the interest rate is highest under

this source and risk of payment shall always exist.

5% Coupon Bond, the secondary method of finance shall result in an annual outflow of Sterling

9019500 per annum along with the face value of security at maturity. Thus, the impact of the above

instrument shall be less compared to the first method of finance. However, it may too impact the

feasibility of the project in the period of 5 years as there is significant outflow of resources at

6

and maturity value of the instrument ( for simplicity it has been assumed that the debt matures at

face falue). Thus, the computation methodology has been detailed here-in-below:

Market value = Coupon/ (1+ yield)^1+……………………………+(Coupon + maturity Value)/ (1+ yield)^5

Market Value of Different sources of Finance

Sl

No Particular

Face

Value

Market

Value

Total

Amount

No of Securities

to be issued

1 Loan NA NA 180000000

2 5% Coupon Bond 100 99.78 180000000 1803900

3 3.5% Convertible Coupon Bond 100 100.47 180000000 1791643

Closing share price after 5 years of Convertible Bond

Sl No Particular Amount

1 Price at year 0 5.56

2 Growth Rate 7%

3 Price at year 5 7.80

4 No of shares 14.00

5 Value of Convertible bond 109.17

Post above, the interest to be paid in first year for each security assuming no security has been repaid

has been presented here-in-below:

Interest Cost of three methods of finance for 1st year

Sl

No Particulars

No of

Securities

Face

Value

Total

Amount

Rate of

Interest Cost

1 Loan NA 180000000 5.50%

990000

0

2 5% Coupon Bond 1803900 100 180390000 5%

901950

0

3 3.5% Convertible Coupon Bond 1791643 100 179164300 3%

537492

9

On the basis of above, it can be seen that the loan has an outflow of 9900000 Sterling in the year one

which shall decrease year on year which shall further entitle for outflow of resource and shall

significantly impact the cash flow of the project and might make the project unfeasible too. The main

advantage of this source of finance is that there is no interference of borrower in day-to-day

management of the company. However, covenants may be imposed by the lender on further

borrowing by the company. Thus, under the said method of finance the risk of payment of cash flows

is very high and may impact the general feasibility of the project as the interest rate is highest under

this source and risk of payment shall always exist.

5% Coupon Bond, the secondary method of finance shall result in an annual outflow of Sterling

9019500 per annum along with the face value of security at maturity. Thus, the impact of the above

instrument shall be less compared to the first method of finance. However, it may too impact the

feasibility of the project in the period of 5 years as there is significant outflow of resources at

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maturity of the project. However, in case of the said method there is not interference of bond

holders in day-to-day management of the company and there is no dilution of equity post completion

of project. Thus, the said method is better than first method of finance but has its drawback similar to

that of bank loan as there is high coupon rate and involves significant outflow of resources in the life

of the project.

3.5% Coupon Convertible Bond, the third method of finance shall result in an annual outflow of

Sterling 5374929 per annum along with the convertible option of bonds to 14 shares of the company.

Under the said method, since the value of shares at maturity shall be greater than face value of

maturity of debt it is assumed that investor shall be prudent to convert the same into equity. The

computation of value of equity at 7% growth year on year has been presented here-in-below:

Closing share price after 5 years of Convertible Bond

Sl. No Particular Amount

1 Price at year 0 5.56

2 Growth Rate 7%

3 Price at year 5 7.80

4 No of shares 14.00

5 Value of Convertible bond 109.17

On the basis of above, it can be seen that the value of convertible bond shall be 109.17 and shall be

converted into share thus the risk of significant outflow of resource is minimised. Accordingly, the

cash out flow under the said method is minimum. Further, the major drawback of this method is that

there is interference in day-to day management of the company and dilution of equity post 5 years of

project.

All the three methods of finance are encompassed with the benefit of trading on equity for the life

of project along with the deduction of interest for computation of tax liability.

New Cost of Equity and Weighted Average Cost of Capital

The new cost of equity under debt of 5% and 3.5% along with the weighted average cost of capital

has been presented here-in-below:

When Coupon is 5%

Sl No Particular Brief

1 Ungeared Cost of Equity 9%

2 Value of Equity 722.8

3 Value of Debt 180

4 Cost of Debt 5%

5 Levered Equity 9.8%

6 WACC 8.84%

7

holders in day-to-day management of the company and there is no dilution of equity post completion

of project. Thus, the said method is better than first method of finance but has its drawback similar to

that of bank loan as there is high coupon rate and involves significant outflow of resources in the life

of the project.

3.5% Coupon Convertible Bond, the third method of finance shall result in an annual outflow of

Sterling 5374929 per annum along with the convertible option of bonds to 14 shares of the company.

Under the said method, since the value of shares at maturity shall be greater than face value of

maturity of debt it is assumed that investor shall be prudent to convert the same into equity. The

computation of value of equity at 7% growth year on year has been presented here-in-below:

Closing share price after 5 years of Convertible Bond

Sl. No Particular Amount

1 Price at year 0 5.56

2 Growth Rate 7%

3 Price at year 5 7.80

4 No of shares 14.00

5 Value of Convertible bond 109.17

On the basis of above, it can be seen that the value of convertible bond shall be 109.17 and shall be

converted into share thus the risk of significant outflow of resource is minimised. Accordingly, the

cash out flow under the said method is minimum. Further, the major drawback of this method is that

there is interference in day-to day management of the company and dilution of equity post 5 years of

project.

All the three methods of finance are encompassed with the benefit of trading on equity for the life

of project along with the deduction of interest for computation of tax liability.

New Cost of Equity and Weighted Average Cost of Capital

The new cost of equity under debt of 5% and 3.5% along with the weighted average cost of capital

has been presented here-in-below:

When Coupon is 5%

Sl No Particular Brief

1 Ungeared Cost of Equity 9%

2 Value of Equity 722.8

3 Value of Debt 180

4 Cost of Debt 5%

5 Levered Equity 9.8%

6 WACC 8.84%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

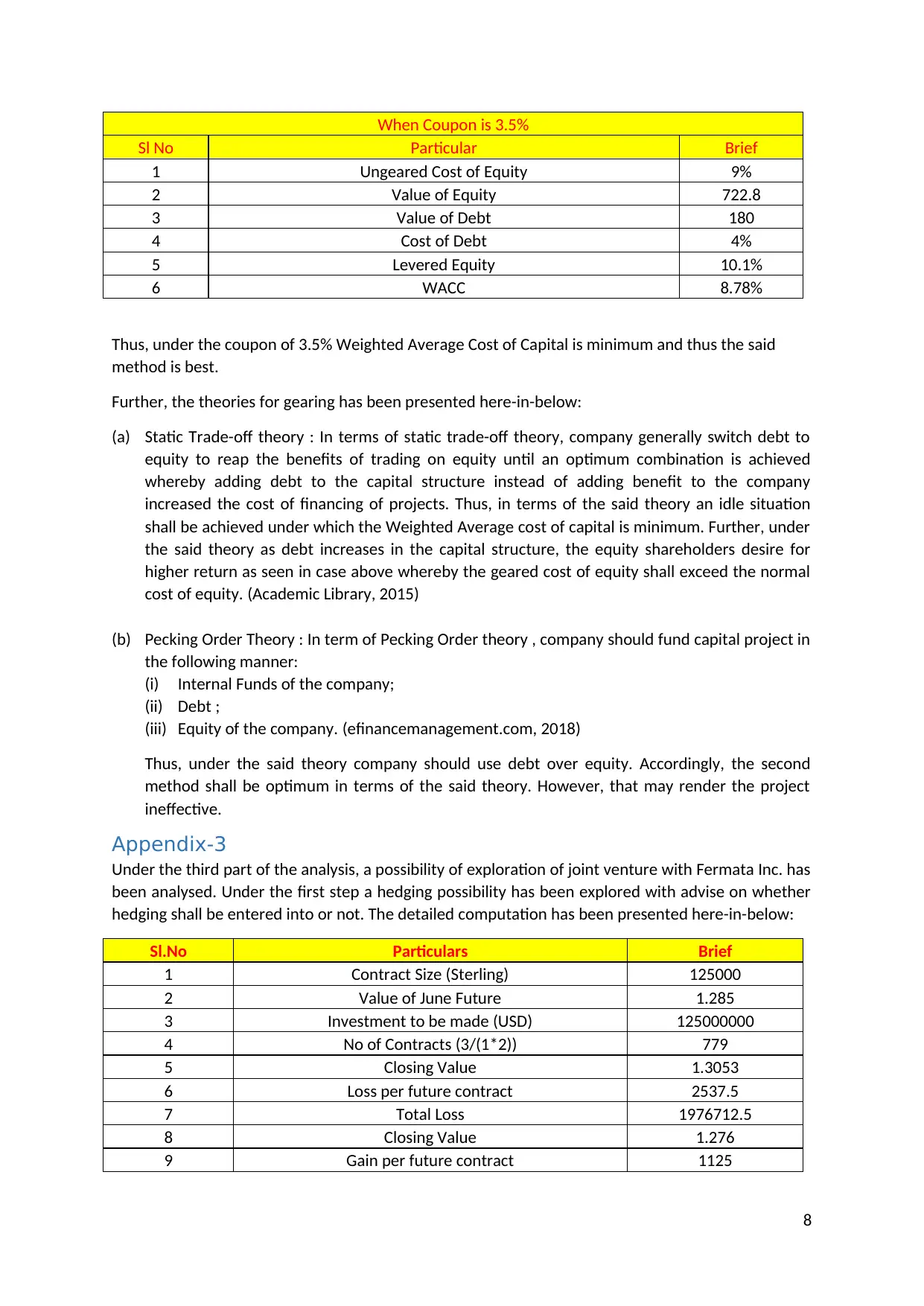

When Coupon is 3.5%

Sl No Particular Brief

1 Ungeared Cost of Equity 9%

2 Value of Equity 722.8

3 Value of Debt 180

4 Cost of Debt 4%

5 Levered Equity 10.1%

6 WACC 8.78%

Thus, under the coupon of 3.5% Weighted Average Cost of Capital is minimum and thus the said

method is best.

Further, the theories for gearing has been presented here-in-below:

(a) Static Trade-off theory : In terms of static trade-off theory, company generally switch debt to

equity to reap the benefits of trading on equity until an optimum combination is achieved

whereby adding debt to the capital structure instead of adding benefit to the company

increased the cost of financing of projects. Thus, in terms of the said theory an idle situation

shall be achieved under which the Weighted Average cost of capital is minimum. Further, under

the said theory as debt increases in the capital structure, the equity shareholders desire for

higher return as seen in case above whereby the geared cost of equity shall exceed the normal

cost of equity. (Academic Library, 2015)

(b) Pecking Order Theory : In term of Pecking Order theory , company should fund capital project in

the following manner:

(i) Internal Funds of the company;

(ii) Debt ;

(iii) Equity of the company. (efinancemanagement.com, 2018)

Thus, under the said theory company should use debt over equity. Accordingly, the second

method shall be optimum in terms of the said theory. However, that may render the project

ineffective.

Appendix-3

Under the third part of the analysis, a possibility of exploration of joint venture with Fermata Inc. has

been analysed. Under the first step a hedging possibility has been explored with advise on whether

hedging shall be entered into or not. The detailed computation has been presented here-in-below:

Sl.No Particulars Brief

1 Contract Size (Sterling) 125000

2 Value of June Future 1.285

3 Investment to be made (USD) 125000000

4 No of Contracts (3/(1*2)) 779

5 Closing Value 1.3053

6 Loss per future contract 2537.5

7 Total Loss 1976712.5

8 Closing Value 1.276

9 Gain per future contract 1125

8

Sl No Particular Brief

1 Ungeared Cost of Equity 9%

2 Value of Equity 722.8

3 Value of Debt 180

4 Cost of Debt 4%

5 Levered Equity 10.1%

6 WACC 8.78%

Thus, under the coupon of 3.5% Weighted Average Cost of Capital is minimum and thus the said

method is best.

Further, the theories for gearing has been presented here-in-below:

(a) Static Trade-off theory : In terms of static trade-off theory, company generally switch debt to

equity to reap the benefits of trading on equity until an optimum combination is achieved

whereby adding debt to the capital structure instead of adding benefit to the company

increased the cost of financing of projects. Thus, in terms of the said theory an idle situation

shall be achieved under which the Weighted Average cost of capital is minimum. Further, under

the said theory as debt increases in the capital structure, the equity shareholders desire for

higher return as seen in case above whereby the geared cost of equity shall exceed the normal

cost of equity. (Academic Library, 2015)

(b) Pecking Order Theory : In term of Pecking Order theory , company should fund capital project in

the following manner:

(i) Internal Funds of the company;

(ii) Debt ;

(iii) Equity of the company. (efinancemanagement.com, 2018)

Thus, under the said theory company should use debt over equity. Accordingly, the second

method shall be optimum in terms of the said theory. However, that may render the project

ineffective.

Appendix-3

Under the third part of the analysis, a possibility of exploration of joint venture with Fermata Inc. has

been analysed. Under the first step a hedging possibility has been explored with advise on whether

hedging shall be entered into or not. The detailed computation has been presented here-in-below:

Sl.No Particulars Brief

1 Contract Size (Sterling) 125000

2 Value of June Future 1.285

3 Investment to be made (USD) 125000000

4 No of Contracts (3/(1*2)) 779

5 Closing Value 1.3053

6 Loss per future contract 2537.5

7 Total Loss 1976712.5

8 Closing Value 1.276

9 Gain per future contract 1125

8

10 Total Gain 876375

Under, the present circumstance, it can be seen that total gain that can be made out of hedging is

lower than the loss that can be incurred out of hedging. Hence the company shall avoid the hedging

strategy as the currency shall be expected to increase over the period. Thus, avoiding hedging

strategy shall be better. Further, no data has been provided regarding the cost of future contract.

Accordingly, the same has not been considered for analysis.

Possibility of Joint Venture

Joint Venture is one of the most attractive solution for expanding in the different territory and has

lot of advantages and disadvantages associated with it. Further, the joint venture is liaised with the

following opportunities:

(a) Growth of the company shall be faster as the venturing company shall have better contacts in

the domestic market;

(b) It shall provide Ottava to step its foot in the US Market and shall help to gain market image and

share;

(c) It shall help Ottava to increase distribution networks;

(d) Increased profits on account of cost control technologies of Fermata;

(e) Sharing of risk of the company;

(f) Access to greater resources like staff, technology etc;

(g) Shared responsibility and cost optimisation. (Businessinfo.co.uk, 2018)

This are the advantages against the Sheffield wherein company has to bear the entire risk and has

to employ 100% capital and bear the loss entirely. Further, there shall be import duty on

manufacturing in UK. Accordingly, joint venture shall be a better looked option.

Virtual Shared Service Centre

The concept has been recently popularised whereby designated business function of the entity are

carried out at a different location on shared basis. This is generally done in order to reduce the

administration cost, increase the quality of work and efficiency of the project. The following are the

functions which are generally outsourced:

(a) Core Treasury Activity;

(b) Tax, Accounting and Finance Activity;

(c) General Corporate Activity.

The virtual shared Service Centre shall help company to centralise its finance function of the Joint

Venture at a single place whereby all the finance activities shall be maintained at a single unit and

control over the project shall be complete. The above step shall render the following advantages to

the company:

Reduction in operating cost on account of centralisation of operation;

Increase in efficiency;

Improved Control;

Performance Measurement; (Treasry Today, 2009)

Economies of Scale.

On the basis of above, the idea shall be suitable.

Business Partner Model to the Finance Function

The business partner model to the finance function refers to the model whereby there shall be active,

real time support both in relation to operation and management. The role shall encompass real time

9

Under, the present circumstance, it can be seen that total gain that can be made out of hedging is

lower than the loss that can be incurred out of hedging. Hence the company shall avoid the hedging

strategy as the currency shall be expected to increase over the period. Thus, avoiding hedging

strategy shall be better. Further, no data has been provided regarding the cost of future contract.

Accordingly, the same has not been considered for analysis.

Possibility of Joint Venture

Joint Venture is one of the most attractive solution for expanding in the different territory and has

lot of advantages and disadvantages associated with it. Further, the joint venture is liaised with the

following opportunities:

(a) Growth of the company shall be faster as the venturing company shall have better contacts in

the domestic market;

(b) It shall provide Ottava to step its foot in the US Market and shall help to gain market image and

share;

(c) It shall help Ottava to increase distribution networks;

(d) Increased profits on account of cost control technologies of Fermata;

(e) Sharing of risk of the company;

(f) Access to greater resources like staff, technology etc;

(g) Shared responsibility and cost optimisation. (Businessinfo.co.uk, 2018)

This are the advantages against the Sheffield wherein company has to bear the entire risk and has

to employ 100% capital and bear the loss entirely. Further, there shall be import duty on

manufacturing in UK. Accordingly, joint venture shall be a better looked option.

Virtual Shared Service Centre

The concept has been recently popularised whereby designated business function of the entity are

carried out at a different location on shared basis. This is generally done in order to reduce the

administration cost, increase the quality of work and efficiency of the project. The following are the

functions which are generally outsourced:

(a) Core Treasury Activity;

(b) Tax, Accounting and Finance Activity;

(c) General Corporate Activity.

The virtual shared Service Centre shall help company to centralise its finance function of the Joint

Venture at a single place whereby all the finance activities shall be maintained at a single unit and

control over the project shall be complete. The above step shall render the following advantages to

the company:

Reduction in operating cost on account of centralisation of operation;

Increase in efficiency;

Improved Control;

Performance Measurement; (Treasry Today, 2009)

Economies of Scale.

On the basis of above, the idea shall be suitable.

Business Partner Model to the Finance Function

The business partner model to the finance function refers to the model whereby there shall be active,

real time support both in relation to operation and management. The role shall encompass real time

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

support and analysis of the project. It enhances the decision making process. The following are the

advantages associated with the said model:

(a) Active help in decision making and part in day-to day activity of the company;

(b) They serve as interface between finance and operations;

(c) Future oriented management;

(d) Expertise in finance and operations and helps in better analysis of projects; (Chartered Accountas

Ireland, 2017)

(e) It is a way of thinking at the heart of which is problem solving.

On the basis of above, it shall be appropriate for the project.

Conclusion

On the basis of above, it can be seen that joint venture shall be the best possibility for the company

to explore project overseas and expand its business internationally.

References:

Academic Library, 2015. The Trade-off theory of capital structure. [Online]

Available at: https://ebrary.net/735/business_finance/trade-off_theory_capital_structure

[Accessed 31 December 2018].

Businessinfo.co.uk, 2018. Joint ventures and business partnerships. [Online]

Available at: https://www.nibusinessinfo.co.uk/content/joint-venture-benefits-and-risks

[Accessed 31 December 2018].

Chartered Accountas Ireland, 2017. Professional Development. [Online]

Available at: https://www.charteredaccountants.ie/professional-development/specialist-

qualifications/Diploma-in-Strategic-Finance--Analytics/What-is-a-finance-business-partner

[Accessed 31 December 2018].

efinancemanagement.com, 2018. Pecking Order Theory. [Online]

Available at: https://efinancemanagement.com/financial-leverage/pecking-order-theory

[Accessed 31 December 2018].

Treasry Today, 2009. Setting up a shared service centre. [Online]

Available at: http://treasurytoday.com/2009/04/setting-up-a-shared-service-centre

[Accessed 31 December 2018].

10

advantages associated with the said model:

(a) Active help in decision making and part in day-to day activity of the company;

(b) They serve as interface between finance and operations;

(c) Future oriented management;

(d) Expertise in finance and operations and helps in better analysis of projects; (Chartered Accountas

Ireland, 2017)

(e) It is a way of thinking at the heart of which is problem solving.

On the basis of above, it shall be appropriate for the project.

Conclusion

On the basis of above, it can be seen that joint venture shall be the best possibility for the company

to explore project overseas and expand its business internationally.

References:

Academic Library, 2015. The Trade-off theory of capital structure. [Online]

Available at: https://ebrary.net/735/business_finance/trade-off_theory_capital_structure

[Accessed 31 December 2018].

Businessinfo.co.uk, 2018. Joint ventures and business partnerships. [Online]

Available at: https://www.nibusinessinfo.co.uk/content/joint-venture-benefits-and-risks

[Accessed 31 December 2018].

Chartered Accountas Ireland, 2017. Professional Development. [Online]

Available at: https://www.charteredaccountants.ie/professional-development/specialist-

qualifications/Diploma-in-Strategic-Finance--Analytics/What-is-a-finance-business-partner

[Accessed 31 December 2018].

efinancemanagement.com, 2018. Pecking Order Theory. [Online]

Available at: https://efinancemanagement.com/financial-leverage/pecking-order-theory

[Accessed 31 December 2018].

Treasry Today, 2009. Setting up a shared service centre. [Online]

Available at: http://treasurytoday.com/2009/04/setting-up-a-shared-service-centre

[Accessed 31 December 2018].

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.