Audit, Assurance, and Compliance Review of Oz Minerals Ltd

VerifiedAdded on 2023/06/05

|16

|3886

|487

Report

AI Summary

This report examines the audit, assurance, and compliance practices at Oz Minerals, focusing on the auditor's role in enhancing audit report quality. It highlights KPMG's adherence to regulations and standards, the remuneration structure for audit and non-audit services, and key audit matters in Oz Minerals' financial operations. The analysis covers auditor independence, non-audit services provided by KPMG, and the audit committee's role in ensuring compliance. Key audit matters, such as PPE valuation and low-grade gold ore stockpiles, are assessed, detailing the procedures used by KPMG. The report also addresses material subsequent events and the auditors' handling of material information. Desklib offers this and other solved assignments for students.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Executive Summary

Different parts of the report inspect the role and responsibility of the auditor towards

enhancing the quality of audit report in Oz Minerals. The report sheds light on the fact that

KPMG has taken into consideration all the relevant regulations and standards in order to carry

on the audit procedures. This report also takes into consideration the remuneration structure

of the company of the auditor for both the audit and non-audit services. At the same time, the

report has assessed the key audit matters in the financial operations of Oz Minerals.

Executive Summary

Different parts of the report inspect the role and responsibility of the auditor towards

enhancing the quality of audit report in Oz Minerals. The report sheds light on the fact that

KPMG has taken into consideration all the relevant regulations and standards in order to carry

on the audit procedures. This report also takes into consideration the remuneration structure

of the company of the auditor for both the audit and non-audit services. At the same time, the

report has assessed the key audit matters in the financial operations of Oz Minerals.

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Introduction.....................................................................................................................................3

Adherence to the Auditors’ Independence Requirement...............................................................3

Non-Audit Services..........................................................................................................................4

Auditor’s Remuneration..................................................................................................................5

Key Audit Matters............................................................................................................................7

Audit Committee..............................................................................................................................9

Audit Opinion...................................................................................................................................9

Difference between Responsibilities.............................................................................................10

Material Subsequent Events..........................................................................................................10

Analysis of the Material Information by the Auditors...................................................................11

Material Information Missing........................................................................................................11

Follow-up Questions......................................................................................................................12

Conclusion......................................................................................................................................12

References.....................................................................................................................................13

Table of Contents

Introduction.....................................................................................................................................3

Adherence to the Auditors’ Independence Requirement...............................................................3

Non-Audit Services..........................................................................................................................4

Auditor’s Remuneration..................................................................................................................5

Key Audit Matters............................................................................................................................7

Audit Committee..............................................................................................................................9

Audit Opinion...................................................................................................................................9

Difference between Responsibilities.............................................................................................10

Material Subsequent Events..........................................................................................................10

Analysis of the Material Information by the Auditors...................................................................11

Material Information Missing........................................................................................................11

Follow-up Questions......................................................................................................................12

Conclusion......................................................................................................................................12

References.....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

Introduction

The process of auditing plays an integral parts for the investors and other users of the

financial reports in shoeing the fact that where the financial statements and reports of the

companies are free from material misstatements or not (Louwers et al. 2015). For this reason, it

is the responsibility on the auditor to provide the investors and other users with quality audit

report by considering all the material issue in the financial statements of the companies. In the

year 2016, it can be observed that the responsible audit authorities have taken some major

steps and initiatives for enhancing the quality of the audit process (Knechel and Salterio 2016).

Due to these initiatives, it has become necessary for the Australian Stock Exchange (ASX) listed

companies to disclose the information on the Key Audit Matters and implement the

mechanism for the effective communication of the material information in simple English. The

introduction of this new auditing standard has increased the responsibility of the auditors as it

has become necessary for auditors to report the identified key audit matters and they are also

required to disclose information on the applied substantive audit procedure in order to address

these risks. Hence, this has increased the responsibility of both the companies and the auditors

(Chan and Vasarhelyi 2018). This report aims to analyze and evaluate the section related to the

role of the auditors of one of the Australian companies, OZ Minerals.

Adherence to the Auditors’ Independence Requirement

In order to enhance the quality of the audit operations and the audit report, the

responsibility of the auditors is to comply with all the requirements of auditor’s independence

(Guénin-Paracini, Malsch and Tremblay 2014). It need to be mentioned in this context that

Introduction

The process of auditing plays an integral parts for the investors and other users of the

financial reports in shoeing the fact that where the financial statements and reports of the

companies are free from material misstatements or not (Louwers et al. 2015). For this reason, it

is the responsibility on the auditor to provide the investors and other users with quality audit

report by considering all the material issue in the financial statements of the companies. In the

year 2016, it can be observed that the responsible audit authorities have taken some major

steps and initiatives for enhancing the quality of the audit process (Knechel and Salterio 2016).

Due to these initiatives, it has become necessary for the Australian Stock Exchange (ASX) listed

companies to disclose the information on the Key Audit Matters and implement the

mechanism for the effective communication of the material information in simple English. The

introduction of this new auditing standard has increased the responsibility of the auditors as it

has become necessary for auditors to report the identified key audit matters and they are also

required to disclose information on the applied substantive audit procedure in order to address

these risks. Hence, this has increased the responsibility of both the companies and the auditors

(Chan and Vasarhelyi 2018). This report aims to analyze and evaluate the section related to the

role of the auditors of one of the Australian companies, OZ Minerals.

Adherence to the Auditors’ Independence Requirement

In order to enhance the quality of the audit operations and the audit report, the

responsibility of the auditors is to comply with all the requirements of auditor’s independence

(Guénin-Paracini, Malsch and Tremblay 2014). It need to be mentioned in this context that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

KPMG was the audit partner of Oz Minerals for the year 2017. According to Auditor’s

Independence Declaration in 2017 Annual Report of Oz Minerals, the auditors of KPMG have

complied with the regulations and principles of Section 307C of the Corporations Act 2001.

They have also declared that there was not any contravention in the requirement of auditor’s

independence by KPMG. At the same time, there was not any contravention in the applicable

code of professional conduct by the auditors related to auditor’s independence

(Ozminerals.com 2018).

Non-Audit Services

Besides providing the audit and assurance related services, the auditors can be found in

providing some non-audit services to the audit clients (Svanström 2013). It can be seen from

the remuneration report of KPMG in the 2017 annual report of Oz Minerals that the company

has received two types of non-audit services from KPMG. They are Tax Compliance and Other

Tax Advisory Services and Other Non-audit Services. For receiving the services of tax advisory

and other taxation related services, Oz Minerals paid KPMG with $180,000 in 2017 and

$160,124 in 2016. For receiving the services for other services, KPMG received from Oz

Minerals worth $44,328 in 2017 and $5,125 in 2016 (Ozminerals.com 2018).

While receiving the non-audit services from KPMG, the Audit Committee of Oz Minerals

ensured the fact that they did not have any impact on the objectivity and integrity of the

external auditors (Koh, Rajgopal and Srinivasan 2013). The same committee also made ensure

on the fact that the auditors have provided Oz Minerals with the non-audit services by

complying with the general principles of independence for the auditors by Corporations Act

KPMG was the audit partner of Oz Minerals for the year 2017. According to Auditor’s

Independence Declaration in 2017 Annual Report of Oz Minerals, the auditors of KPMG have

complied with the regulations and principles of Section 307C of the Corporations Act 2001.

They have also declared that there was not any contravention in the requirement of auditor’s

independence by KPMG. At the same time, there was not any contravention in the applicable

code of professional conduct by the auditors related to auditor’s independence

(Ozminerals.com 2018).

Non-Audit Services

Besides providing the audit and assurance related services, the auditors can be found in

providing some non-audit services to the audit clients (Svanström 2013). It can be seen from

the remuneration report of KPMG in the 2017 annual report of Oz Minerals that the company

has received two types of non-audit services from KPMG. They are Tax Compliance and Other

Tax Advisory Services and Other Non-audit Services. For receiving the services of tax advisory

and other taxation related services, Oz Minerals paid KPMG with $180,000 in 2017 and

$160,124 in 2016. For receiving the services for other services, KPMG received from Oz

Minerals worth $44,328 in 2017 and $5,125 in 2016 (Ozminerals.com 2018).

While receiving the non-audit services from KPMG, the Audit Committee of Oz Minerals

ensured the fact that they did not have any impact on the objectivity and integrity of the

external auditors (Koh, Rajgopal and Srinivasan 2013). The same committee also made ensure

on the fact that the auditors have provided Oz Minerals with the non-audit services by

complying with the general principles of independence for the auditors by Corporations Act

5AUDIT, ASSURANCE AND COMPLIANCE

2001. It implies that the auditors neither did nor compromise the independence requirement

by the Corporations Act 2001 (Ozminerals.com 2018).

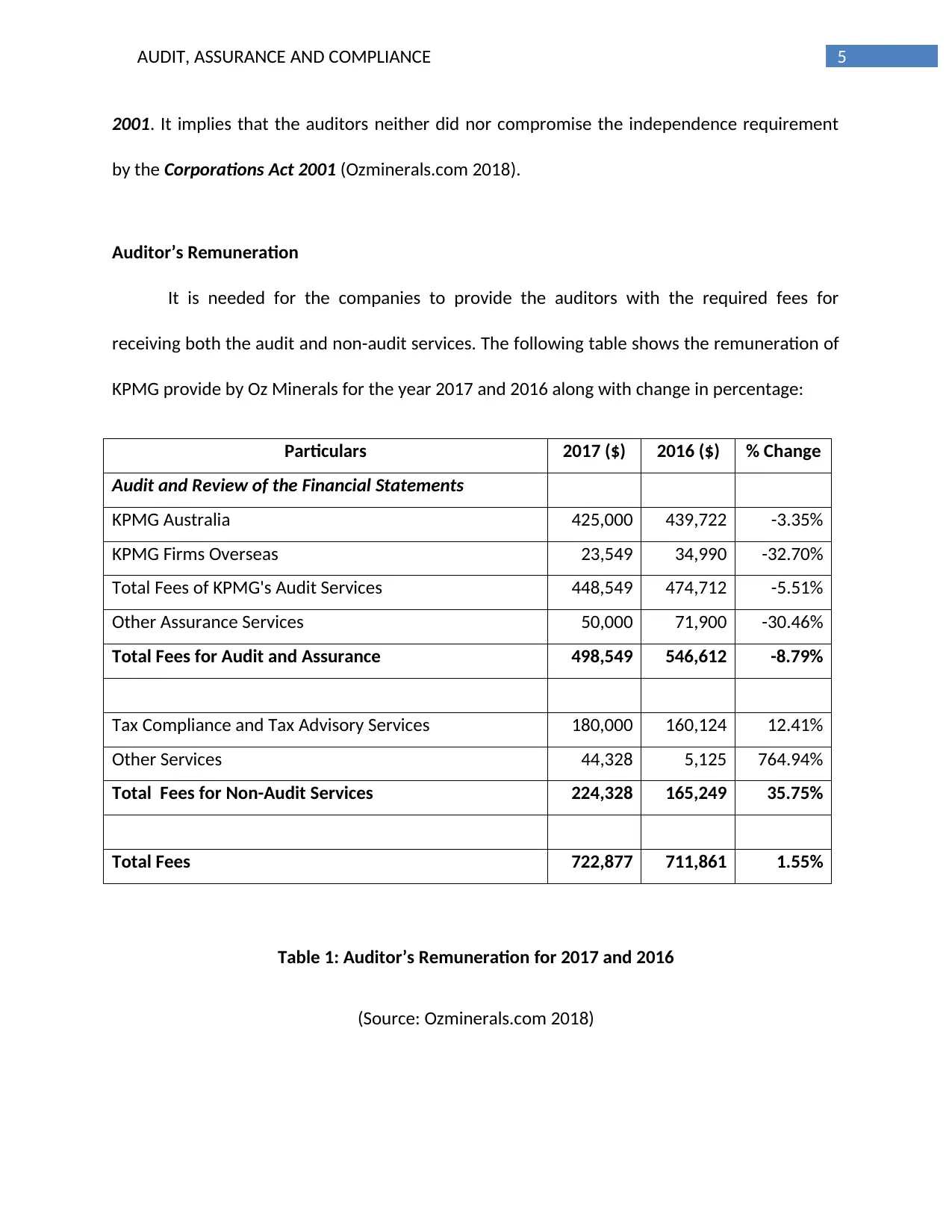

Auditor’s Remuneration

It is needed for the companies to provide the auditors with the required fees for

receiving both the audit and non-audit services. The following table shows the remuneration of

KPMG provide by Oz Minerals for the year 2017 and 2016 along with change in percentage:

Particulars 2017 ($) 2016 ($) % Change

Audit and Review of the Financial Statements

KPMG Australia 425,000 439,722 -3.35%

KPMG Firms Overseas 23,549 34,990 -32.70%

Total Fees of KPMG's Audit Services 448,549 474,712 -5.51%

Other Assurance Services 50,000 71,900 -30.46%

Total Fees for Audit and Assurance 498,549 546,612 -8.79%

Tax Compliance and Tax Advisory Services 180,000 160,124 12.41%

Other Services 44,328 5,125 764.94%

Total Fees for Non-Audit Services 224,328 165,249 35.75%

Total Fees 722,877 711,861 1.55%

Table 1: Auditor’s Remuneration for 2017 and 2016

(Source: Ozminerals.com 2018)

2001. It implies that the auditors neither did nor compromise the independence requirement

by the Corporations Act 2001 (Ozminerals.com 2018).

Auditor’s Remuneration

It is needed for the companies to provide the auditors with the required fees for

receiving both the audit and non-audit services. The following table shows the remuneration of

KPMG provide by Oz Minerals for the year 2017 and 2016 along with change in percentage:

Particulars 2017 ($) 2016 ($) % Change

Audit and Review of the Financial Statements

KPMG Australia 425,000 439,722 -3.35%

KPMG Firms Overseas 23,549 34,990 -32.70%

Total Fees of KPMG's Audit Services 448,549 474,712 -5.51%

Other Assurance Services 50,000 71,900 -30.46%

Total Fees for Audit and Assurance 498,549 546,612 -8.79%

Tax Compliance and Tax Advisory Services 180,000 160,124 12.41%

Other Services 44,328 5,125 764.94%

Total Fees for Non-Audit Services 224,328 165,249 35.75%

Total Fees 722,877 711,861 1.55%

Table 1: Auditor’s Remuneration for 2017 and 2016

(Source: Ozminerals.com 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

KPMG has provided Oz Minerals with both the audit and non-audit services. It can be

seen from the above table that there is decrease in the fees of every service KPMG has

provided to Oz Minerals in the year 2017 as compared to 2016. Due to this, there is a decrease

in the total payment of the fees to the auditors in the year 2017 as compared to 2016. It can be

seen that there is a 3.35% decrease in the fees paid to KPMG Australia; there is 32.70%

decrease in the fees paid to KPMG oversees firms and there is 30.46% decrease in the payment

of other assurance services. Due to all these, there is 8.79% decrease in the total fees paid to

KPMG in the year 2017 as compared to 2016 (Chambers 2014).

However, the opposite aspect can be noticed in case of non-audit services as there is

increase in the payment to KPMG to give the non-audit services in the year 2017 as compared

to 2016. The above table shows an increase of 12.41% in the provide non-audit services for tax

compliance and other taxation advisory services (Ozminerals.com 2018). After that, there is

764.94% increase in the other non-audit service fees to KPMG in the year 2017 as compared to

2016. There is a 35.75% increase in the payment of total non-audit services to KPMG for the

year 2017 as compared to 2016. In this context, it needs to be mentioned that there is an

overall increase in the total audit fees paid to KPMG by Oz Minerals in the year 2017 for 1.55%

as compared to 2016 and this increase in total audit fees can be considered as a result for the

increase in the payment of the non-audit services (Leung, Richardson and Jaggi 2014).

KPMG has provided Oz Minerals with both the audit and non-audit services. It can be

seen from the above table that there is decrease in the fees of every service KPMG has

provided to Oz Minerals in the year 2017 as compared to 2016. Due to this, there is a decrease

in the total payment of the fees to the auditors in the year 2017 as compared to 2016. It can be

seen that there is a 3.35% decrease in the fees paid to KPMG Australia; there is 32.70%

decrease in the fees paid to KPMG oversees firms and there is 30.46% decrease in the payment

of other assurance services. Due to all these, there is 8.79% decrease in the total fees paid to

KPMG in the year 2017 as compared to 2016 (Chambers 2014).

However, the opposite aspect can be noticed in case of non-audit services as there is

increase in the payment to KPMG to give the non-audit services in the year 2017 as compared

to 2016. The above table shows an increase of 12.41% in the provide non-audit services for tax

compliance and other taxation advisory services (Ozminerals.com 2018). After that, there is

764.94% increase in the other non-audit service fees to KPMG in the year 2017 as compared to

2016. There is a 35.75% increase in the payment of total non-audit services to KPMG for the

year 2017 as compared to 2016. In this context, it needs to be mentioned that there is an

overall increase in the total audit fees paid to KPMG by Oz Minerals in the year 2017 for 1.55%

as compared to 2016 and this increase in total audit fees can be considered as a result for the

increase in the payment of the non-audit services (Leung, Richardson and Jaggi 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

Key Audit Matters

According to the earlier discussion, it is the responsibility of the auditors to report about

the key audit matters of the business organizations and there is nor any exception of this fat in

the case of Oz Minerals. The following discussion shows the key audit matters of Oz Minerals:

Key Audit Matter 1: PPE’s carrying Value of Prominent Hill

KPMG has considered the carrying value of the PPE of Prominent Hill as a key audit

matter as the auditors have to put major effort in order to assess the fact there is not any

indication of impairment related to the PPE of Prominent Hill. The presence of some important

factors can be seen in this situation. One major issue include in the assessment of this situation

that the presence of any kind of impairment indicator would lead to the analysis of the

recoverable amount from Prominent Hill. At the same time, another major aspect was the

historic sensatory of the modeling of the company for external as well as internal conditions. At

the time of the assessment, the auditors of KPMG have analyzed some major aspects like

commodity price, foreign exchange rate, and production level for the metals, capital

expenditures and operating costs (Ozminerals.com 2018).

KPMG has used some analytical techniques for addressing this issue. The auditors have

undertaken the testing of the internal control of Oz Minerals related to operational plan and

budget for Prominent Hill PPE for the assessment of the primary indicators for impairments.

After this, the auditors have assessed the key forecast units such as metal production level,

capital expenditures against the historical costs and the operating costs. At the same time, the

auditors have undertaken the assessment of the relevant rate of discount sourced from the

Key Audit Matters

According to the earlier discussion, it is the responsibility of the auditors to report about

the key audit matters of the business organizations and there is nor any exception of this fat in

the case of Oz Minerals. The following discussion shows the key audit matters of Oz Minerals:

Key Audit Matter 1: PPE’s carrying Value of Prominent Hill

KPMG has considered the carrying value of the PPE of Prominent Hill as a key audit

matter as the auditors have to put major effort in order to assess the fact there is not any

indication of impairment related to the PPE of Prominent Hill. The presence of some important

factors can be seen in this situation. One major issue include in the assessment of this situation

that the presence of any kind of impairment indicator would lead to the analysis of the

recoverable amount from Prominent Hill. At the same time, another major aspect was the

historic sensatory of the modeling of the company for external as well as internal conditions. At

the time of the assessment, the auditors of KPMG have analyzed some major aspects like

commodity price, foreign exchange rate, and production level for the metals, capital

expenditures and operating costs (Ozminerals.com 2018).

KPMG has used some analytical techniques for addressing this issue. The auditors have

undertaken the testing of the internal control of Oz Minerals related to operational plan and

budget for Prominent Hill PPE for the assessment of the primary indicators for impairments.

After this, the auditors have assessed the key forecast units such as metal production level,

capital expenditures against the historical costs and the operating costs. At the same time, the

auditors have undertaken the assessment of the relevant rate of discount sourced from the

8AUDIT, ASSURANCE AND COMPLIANCE

comparable market rates. Apart from this, KPMG has also made the comparison between the

forecast commodity prices and the foreign exchange rates. Thus, the classification of these

procedures can be done as tests of controls and substantive tests of details (Brasel et al. 2016).

Key Audit Matter 2: Low Grade Gold Ore Stockpiles Valuation

The auditors of KPMG have considered the valuation of low grade gold ore stockpile as a

key audit matter due to the presence of significant judgment by the auditors at the time of the

evaluation of the assessment of the value. The assessment of the company is dependent on the

estimates that include in estimation of future revenues that are expected to be derived from

the low grade ore. In this process, the auditors have put major focus on some of the key

judgments like the future metal level of production, cost of future processing cost, future

commodity prices and the timing of production (Christensen, Glover and Wolfe 2014).

It needs to be mentioned that the auditors of KPMG have undertaken certain

procedures in order to address this key audit matter. The auditors have undertaken the testing

of control related to the valuation mechanism of the company’s low grade gold ore stockpiles

that include key of board authorization and the process of Oz Minerals’ to record and monitor

the volumes and grades of stockpiles. After that, the auditors have also assessed the

methodology adopted by the company for the determination of the value of low grade gold

ore. Moreover, the company has also assessed some of the major assumptions related to the

valuation of low grade gold ore such as comparison of the forecast processing cost, assessment

of the forecast selling cost, assessment of the commodity price along with the foreign exchange

rates and others (Keddie 2013).

comparable market rates. Apart from this, KPMG has also made the comparison between the

forecast commodity prices and the foreign exchange rates. Thus, the classification of these

procedures can be done as tests of controls and substantive tests of details (Brasel et al. 2016).

Key Audit Matter 2: Low Grade Gold Ore Stockpiles Valuation

The auditors of KPMG have considered the valuation of low grade gold ore stockpile as a

key audit matter due to the presence of significant judgment by the auditors at the time of the

evaluation of the assessment of the value. The assessment of the company is dependent on the

estimates that include in estimation of future revenues that are expected to be derived from

the low grade ore. In this process, the auditors have put major focus on some of the key

judgments like the future metal level of production, cost of future processing cost, future

commodity prices and the timing of production (Christensen, Glover and Wolfe 2014).

It needs to be mentioned that the auditors of KPMG have undertaken certain

procedures in order to address this key audit matter. The auditors have undertaken the testing

of control related to the valuation mechanism of the company’s low grade gold ore stockpiles

that include key of board authorization and the process of Oz Minerals’ to record and monitor

the volumes and grades of stockpiles. After that, the auditors have also assessed the

methodology adopted by the company for the determination of the value of low grade gold

ore. Moreover, the company has also assessed some of the major assumptions related to the

valuation of low grade gold ore such as comparison of the forecast processing cost, assessment

of the forecast selling cost, assessment of the commodity price along with the foreign exchange

rates and others (Keddie 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

Audit Committee

As per the latest annual report of Oz Minerals company has an Audit Committee within

the organization and the main function of this committee is to provide assistance to the board

in discharging their duties and responsibilities related to financial reporting properly (Badolato,

Donelson and Ege 2014). It needs to be mentioned that Peter Wasow, a non-executive director

of Oz Minerals, will be the Chainman of the Audit Committee.

As per the latest annual report of Oz Minerals that the company has an Audit

Committee Charter within the organizations and this committee has certain policies and

standards. The first policy is the Governance and Risk Policy that ensures the use of ethical

business processes for corporate governance standards (Ozminerals.com 2018). The second

policy is the Market Dividend Policy that ensures fair trading of the securities of Oz Minerals.

The third policy is Finance and Accounting Policy that ensures the compliance of Oz Minerals

with all the required financial and accounting disclosures. The fourth policy is the Securities

Trading Policies that involves in setting out necessary policies for employees, directors and

others (Contessotto and Moroney 2014).

Audit Opinion

As per the Independent Auditor’s Report, the auditors of KPMG have provide the

opinion that the financial statements of Oz Minerals have been prepared as per the regulations

of Corporations Act 2001 and this compliance has ensured the true and fair view of the

financial position of Oz Minerals for that particular period (Ozminerals.com 2018). The auditors

Audit Committee

As per the latest annual report of Oz Minerals company has an Audit Committee within

the organization and the main function of this committee is to provide assistance to the board

in discharging their duties and responsibilities related to financial reporting properly (Badolato,

Donelson and Ege 2014). It needs to be mentioned that Peter Wasow, a non-executive director

of Oz Minerals, will be the Chainman of the Audit Committee.

As per the latest annual report of Oz Minerals that the company has an Audit

Committee Charter within the organizations and this committee has certain policies and

standards. The first policy is the Governance and Risk Policy that ensures the use of ethical

business processes for corporate governance standards (Ozminerals.com 2018). The second

policy is the Market Dividend Policy that ensures fair trading of the securities of Oz Minerals.

The third policy is Finance and Accounting Policy that ensures the compliance of Oz Minerals

with all the required financial and accounting disclosures. The fourth policy is the Securities

Trading Policies that involves in setting out necessary policies for employees, directors and

others (Contessotto and Moroney 2014).

Audit Opinion

As per the Independent Auditor’s Report, the auditors of KPMG have provide the

opinion that the financial statements of Oz Minerals have been prepared as per the regulations

of Corporations Act 2001 and this compliance has ensured the true and fair view of the

financial position of Oz Minerals for that particular period (Ozminerals.com 2018). The auditors

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

have also opined that the company has complied with the Australian Accounting Standards

and Corporations Regulations 2001 in the process of financial reporting (Newton et al. 2015).

Difference between Responsibilities

According to the Auditor’s Report in 2017 Annual Report of Oz Minerals, the prime

responsibilities of the directors are the preparation of financial reports as per Australian

Accounting Standards and Corporations Act 2001 with the aim to provide true and fair view;

the implementation of necessary internal control in the aspect of financial reporting; and the

assessment of the Consolidated Entity’s ability for continuing as a going concern

(Ozminerals.com 2018).

However, the responsibilities of the auditors are different from the director for financial

reporting. The prime responsibilities of the auditors are to obtain reasonable assurance on the

fact that whether there is any material misstatements in the financial reports due to fraud and

errors and to issue the appropriate audit report that includes the audit opinion (DeZoort and

Harrison 2018).

Material Subsequent Events

The annual report for the year 2017 of Oz Minerals shows that the board of the

company was involved in payment of 14% fully franked dividend on 26 March 2018 and the

entitled record date of this was 12 March 2018. For this reason, the company has not

recognized the amount of the payment of dividend worth $41.8 million in the Consolidated

Financial Statements for the year ended 31 December 2017. Apart from this, the auditors have

have also opined that the company has complied with the Australian Accounting Standards

and Corporations Regulations 2001 in the process of financial reporting (Newton et al. 2015).

Difference between Responsibilities

According to the Auditor’s Report in 2017 Annual Report of Oz Minerals, the prime

responsibilities of the directors are the preparation of financial reports as per Australian

Accounting Standards and Corporations Act 2001 with the aim to provide true and fair view;

the implementation of necessary internal control in the aspect of financial reporting; and the

assessment of the Consolidated Entity’s ability for continuing as a going concern

(Ozminerals.com 2018).

However, the responsibilities of the auditors are different from the director for financial

reporting. The prime responsibilities of the auditors are to obtain reasonable assurance on the

fact that whether there is any material misstatements in the financial reports due to fraud and

errors and to issue the appropriate audit report that includes the audit opinion (DeZoort and

Harrison 2018).

Material Subsequent Events

The annual report for the year 2017 of Oz Minerals shows that the board of the

company was involved in payment of 14% fully franked dividend on 26 March 2018 and the

entitled record date of this was 12 March 2018. For this reason, the company has not

recognized the amount of the payment of dividend worth $41.8 million in the Consolidated

Financial Statements for the year ended 31 December 2017. Apart from this, the auditors have

11AUDIT, ASSURANCE AND COMPLIANCE

not considered any event as material subsequent for Oz Minerals in 2017 (Ruhnke and Schmidt

2014).

Analysis of the Material Information by the Auditors

From the above discussion of the relevant areas of audit in the annual report of Oz

Minerals, it is evident that the auditors of KPMG have efficiently assessed all the material audit

events in the financial statements of Oz Minerals. At the same time, clear communication of

these audit material issue in simple English can be seen in the audit report by the auditors. With

the help of this analysis, the auditors have identified two key audit matters in the financial

statements of Oz Minerals. All these aspects indicate towards the effective assessment of the

material issue in the financial statements of Oz Minerals (Czerney, Schmidt and Thompson

2014).

Material Information Missing

It can be seen from the above discussion that the auditors of KPMG has undertaken the

assessment of all the financial statements of the company by complying with all the required

standards and regulations of auditing. With the help of this assessment, they have found two

major key audit matters that they have addressed with the help of the required substantive

audit procedures. At the same time, they have provided their opinion in all the required areas

in the material issue. Hence, there is not any missing or partly reported material information in

the company (Brasel et al. 2016).

not considered any event as material subsequent for Oz Minerals in 2017 (Ruhnke and Schmidt

2014).

Analysis of the Material Information by the Auditors

From the above discussion of the relevant areas of audit in the annual report of Oz

Minerals, it is evident that the auditors of KPMG have efficiently assessed all the material audit

events in the financial statements of Oz Minerals. At the same time, clear communication of

these audit material issue in simple English can be seen in the audit report by the auditors. With

the help of this analysis, the auditors have identified two key audit matters in the financial

statements of Oz Minerals. All these aspects indicate towards the effective assessment of the

material issue in the financial statements of Oz Minerals (Czerney, Schmidt and Thompson

2014).

Material Information Missing

It can be seen from the above discussion that the auditors of KPMG has undertaken the

assessment of all the financial statements of the company by complying with all the required

standards and regulations of auditing. With the help of this assessment, they have found two

major key audit matters that they have addressed with the help of the required substantive

audit procedures. At the same time, they have provided their opinion in all the required areas

in the material issue. Hence, there is not any missing or partly reported material information in

the company (Brasel et al. 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.