Management Accounting: Definition, Types, and Significance

VerifiedAdded on 2023/04/04

|18

|4455

|183

AI Summary

This document provides a comprehensive guide to management accounting. It covers the definition of management accounting and how it differs from financial accounting. It also explores the different types of management accounting information, such as cost accounting, inventory management, and job costing. Additionally, it discusses the advantages and disadvantages of different budgeting techniques, including incremental budgeting and zero-based budgeting. Perfect for students studying management accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a)c...........................................................................................................................................3

i. Definition of management accounting. How it differ from financial accounting...............3

ii. Significance of management accounting information........................................................5

b) Explain the different types of management accounting information.................................6

Task 3...............................................................................................................................................9

P4 Advantage and disadvantage of different types of budget................................................9

P5 Balance score card approach...........................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a)c...........................................................................................................................................3

i. Definition of management accounting. How it differ from financial accounting...............3

ii. Significance of management accounting information........................................................5

b) Explain the different types of management accounting information.................................6

Task 3...............................................................................................................................................9

P4 Advantage and disadvantage of different types of budget................................................9

P5 Balance score card approach...........................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INTRODUCTION

Management accounting plays a significant role for the manufacturing Company as the

manager can effectively day to day operations. It can be used for the purpose of forward looking

through get the statistical and financial information. The research project is context to the Imda

tech limited used the management accounting information that helps them in attaining its goals

and objectives effectively. There is a mainly discussion on the definition of management

accounting and the difference among the financial accounting and management accounting.

Furthermore, the management accounting information as a decisions tool which gives various

advantages are the Make or buy decisions, Product costing and budgets etc. Thereafter, income

statement prepared on the basis of Marginal and Absorption costing techniques. There is a study

on Advantage and disadvantage of different types of budget. The end portion in which there is

description on Balance scorecard is an approach which is used by entities for measuring their

overall performance (Klychova, Faskhutdinova and Sadrieva, 2014). It evaluates the working on

the bases of four criteria such as financial, internal process, customers and learning or growth. It

evaluates the efforts of firm for the future improvement of organizations

TASK 1

a)c

i. Definition of management accounting. How it differ from financial accounting

Management accounting can be define in that it is a procedure in which the useful

information can be identifying, analyzing, measuring, interpreting and transfer data of

accounting that attain the company to reach its goal in effective manner. Thus, it can be used by

the manager of Imda tech limited to make their day to day decisions of business so, they can

carry out all the function in smoothly (Setthasakko, 2010). It is highly by the management for the

purpose of looking forward and it is used by the internal affairs. Thus, management accounting is

the important part of business units. Firms have to manage their operations well so that it can

sustain in the corporate market for longer duration. Competition is very high to survive in such

environment it is necessary to prepare a good budget. It can be prepared by looking upon income

and cost of the organization in particular fiscal year. It is highly by the management for the

purpose of looking forward and it is used by the internal affairs. Though it is difficult task but

this can help in identifying the sales volume and income of the organization. By this way

Management accounting plays a significant role for the manufacturing Company as the

manager can effectively day to day operations. It can be used for the purpose of forward looking

through get the statistical and financial information. The research project is context to the Imda

tech limited used the management accounting information that helps them in attaining its goals

and objectives effectively. There is a mainly discussion on the definition of management

accounting and the difference among the financial accounting and management accounting.

Furthermore, the management accounting information as a decisions tool which gives various

advantages are the Make or buy decisions, Product costing and budgets etc. Thereafter, income

statement prepared on the basis of Marginal and Absorption costing techniques. There is a study

on Advantage and disadvantage of different types of budget. The end portion in which there is

description on Balance scorecard is an approach which is used by entities for measuring their

overall performance (Klychova, Faskhutdinova and Sadrieva, 2014). It evaluates the working on

the bases of four criteria such as financial, internal process, customers and learning or growth. It

evaluates the efforts of firm for the future improvement of organizations

TASK 1

a)c

i. Definition of management accounting. How it differ from financial accounting

Management accounting can be define in that it is a procedure in which the useful

information can be identifying, analyzing, measuring, interpreting and transfer data of

accounting that attain the company to reach its goal in effective manner. Thus, it can be used by

the manager of Imda tech limited to make their day to day decisions of business so, they can

carry out all the function in smoothly (Setthasakko, 2010). It is highly by the management for the

purpose of looking forward and it is used by the internal affairs. Thus, management accounting is

the important part of business units. Firms have to manage their operations well so that it can

sustain in the corporate market for longer duration. Competition is very high to survive in such

environment it is necessary to prepare a good budget. It can be prepared by looking upon income

and cost of the organization in particular fiscal year. It is highly by the management for the

purpose of looking forward and it is used by the internal affairs. Though it is difficult task but

this can help in identifying the sales volume and income of the organization. By this way

managers will be able to allocate the resources well. Zero based budgeting is effective tool, it is

not depended upon the assumptions so good results can be come out and organizations can

accomplish their objective easily. There is a vast difference among the financial and management

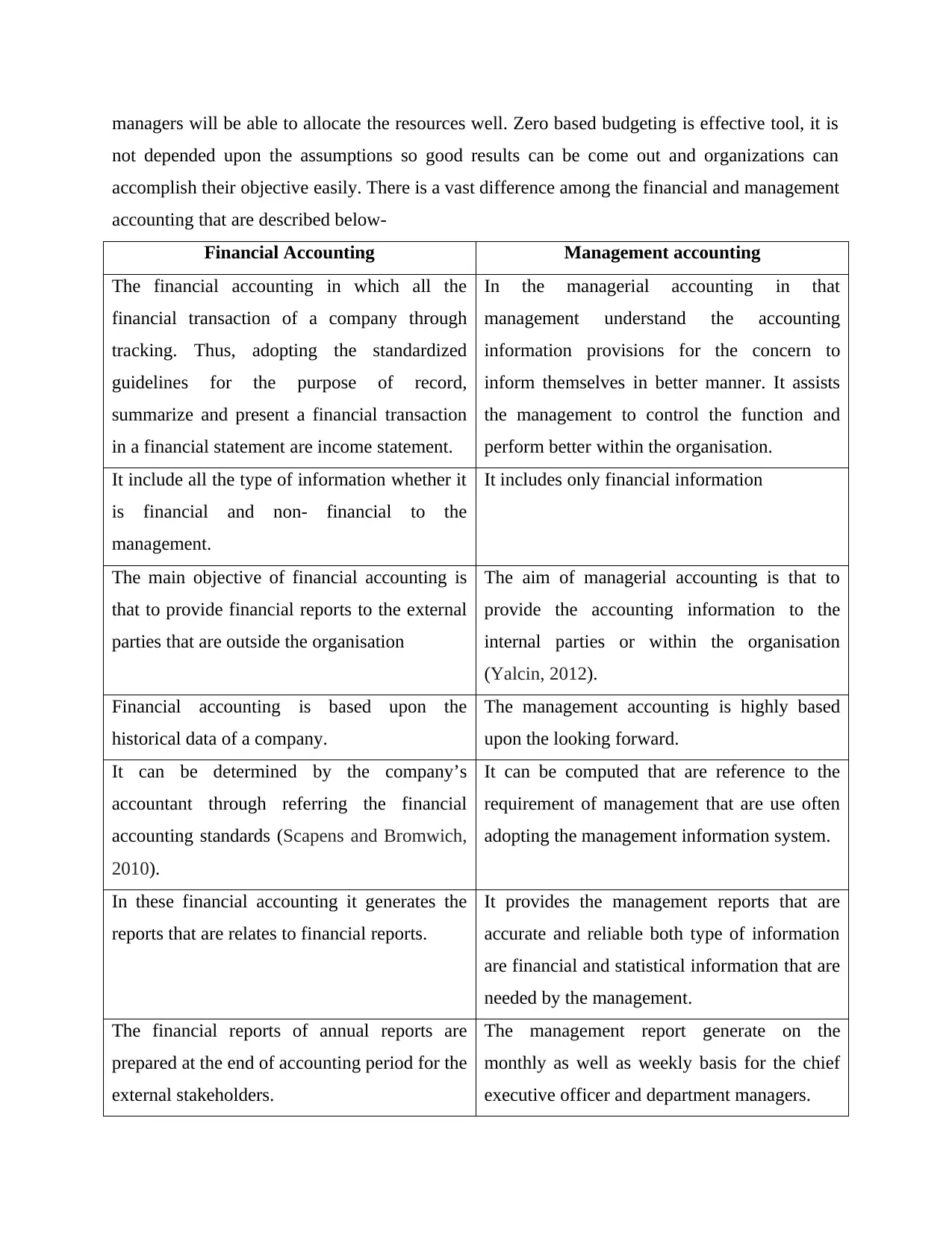

accounting that are described below-

Financial Accounting Management accounting

The financial accounting in which all the

financial transaction of a company through

tracking. Thus, adopting the standardized

guidelines for the purpose of record,

summarize and present a financial transaction

in a financial statement are income statement.

In the managerial accounting in that

management understand the accounting

information provisions for the concern to

inform themselves in better manner. It assists

the management to control the function and

perform better within the organisation.

It include all the type of information whether it

is financial and non- financial to the

management.

It includes only financial information

The main objective of financial accounting is

that to provide financial reports to the external

parties that are outside the organisation

The aim of managerial accounting is that to

provide the accounting information to the

internal parties or within the organisation

(Yalcin, 2012).

Financial accounting is based upon the

historical data of a company.

The management accounting is highly based

upon the looking forward.

It can be determined by the company’s

accountant through referring the financial

accounting standards (Scapens and Bromwich,

2010).

It can be computed that are reference to the

requirement of management that are use often

adopting the management information system.

In these financial accounting it generates the

reports that are relates to financial reports.

It provides the management reports that are

accurate and reliable both type of information

are financial and statistical information that are

needed by the management.

The financial reports of annual reports are

prepared at the end of accounting period for the

external stakeholders.

The management report generate on the

monthly as well as weekly basis for the chief

executive officer and department managers.

not depended upon the assumptions so good results can be come out and organizations can

accomplish their objective easily. There is a vast difference among the financial and management

accounting that are described below-

Financial Accounting Management accounting

The financial accounting in which all the

financial transaction of a company through

tracking. Thus, adopting the standardized

guidelines for the purpose of record,

summarize and present a financial transaction

in a financial statement are income statement.

In the managerial accounting in that

management understand the accounting

information provisions for the concern to

inform themselves in better manner. It assists

the management to control the function and

perform better within the organisation.

It include all the type of information whether it

is financial and non- financial to the

management.

It includes only financial information

The main objective of financial accounting is

that to provide financial reports to the external

parties that are outside the organisation

The aim of managerial accounting is that to

provide the accounting information to the

internal parties or within the organisation

(Yalcin, 2012).

Financial accounting is based upon the

historical data of a company.

The management accounting is highly based

upon the looking forward.

It can be determined by the company’s

accountant through referring the financial

accounting standards (Scapens and Bromwich,

2010).

It can be computed that are reference to the

requirement of management that are use often

adopting the management information system.

In these financial accounting it generates the

reports that are relates to financial reports.

It provides the management reports that are

accurate and reliable both type of information

are financial and statistical information that are

needed by the management.

The financial reports of annual reports are

prepared at the end of accounting period for the

external stakeholders.

The management report generate on the

monthly as well as weekly basis for the chief

executive officer and department managers.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

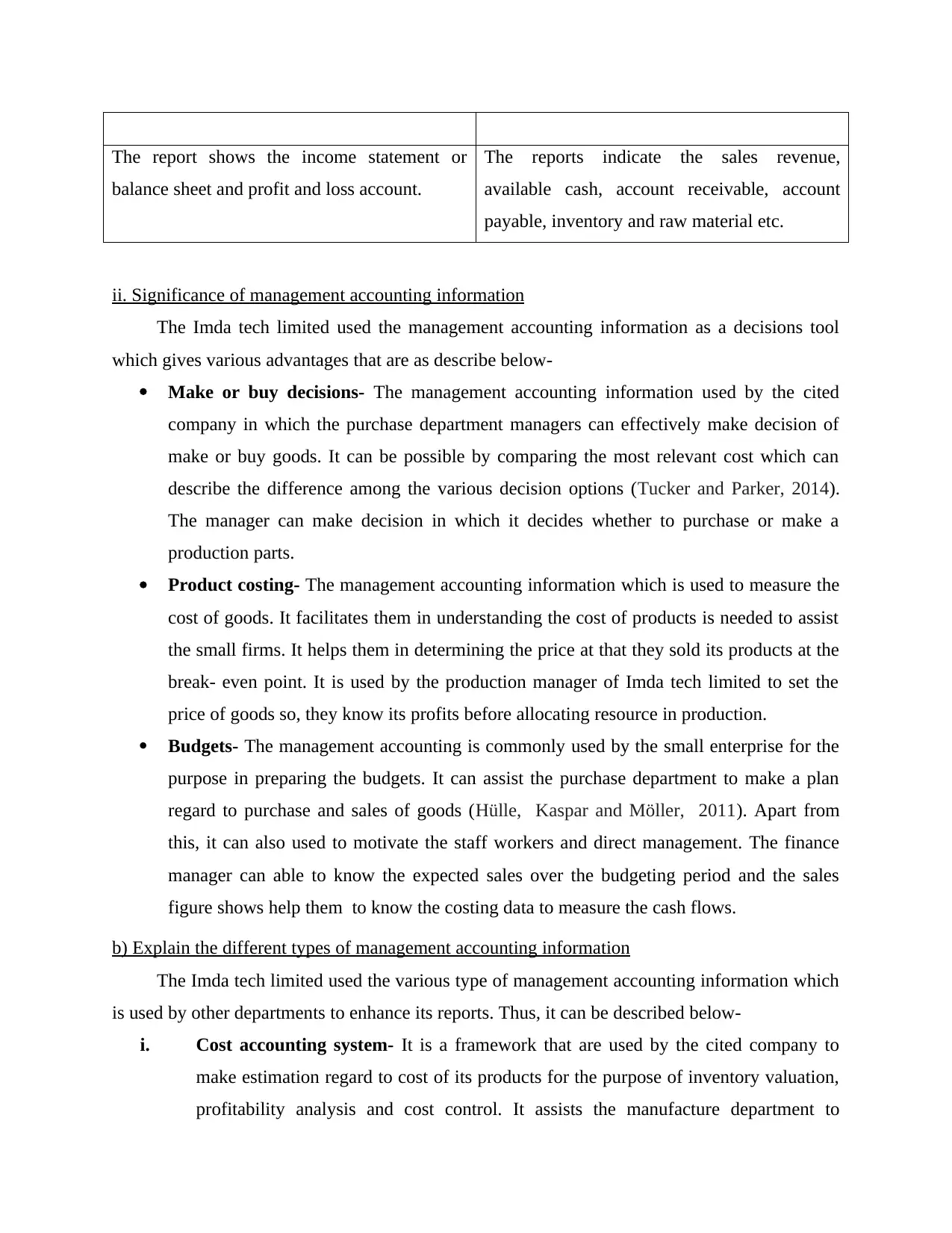

The report shows the income statement or

balance sheet and profit and loss account.

The reports indicate the sales revenue,

available cash, account receivable, account

payable, inventory and raw material etc.

ii. Significance of management accounting information

The Imda tech limited used the management accounting information as a decisions tool

which gives various advantages that are as describe below-

Make or buy decisions- The management accounting information used by the cited

company in which the purchase department managers can effectively make decision of

make or buy goods. It can be possible by comparing the most relevant cost which can

describe the difference among the various decision options (Tucker and Parker, 2014).

The manager can make decision in which it decides whether to purchase or make a

production parts.

Product costing- The management accounting information which is used to measure the

cost of goods. It facilitates them in understanding the cost of products is needed to assist

the small firms. It helps them in determining the price at that they sold its products at the

break- even point. It is used by the production manager of Imda tech limited to set the

price of goods so, they know its profits before allocating resource in production.

Budgets- The management accounting is commonly used by the small enterprise for the

purpose in preparing the budgets. It can assist the purchase department to make a plan

regard to purchase and sales of goods (Hülle, Kaspar and Möller, 2011). Apart from

this, it can also used to motivate the staff workers and direct management. The finance

manager can able to know the expected sales over the budgeting period and the sales

figure shows help them to know the costing data to measure the cash flows.

b) Explain the different types of management accounting information

The Imda tech limited used the various type of management accounting information which

is used by other departments to enhance its reports. Thus, it can be described below-

i. Cost accounting system- It is a framework that are used by the cited company to

make estimation regard to cost of its products for the purpose of inventory valuation,

profitability analysis and cost control. It assists the manufacture department to

balance sheet and profit and loss account.

The reports indicate the sales revenue,

available cash, account receivable, account

payable, inventory and raw material etc.

ii. Significance of management accounting information

The Imda tech limited used the management accounting information as a decisions tool

which gives various advantages that are as describe below-

Make or buy decisions- The management accounting information used by the cited

company in which the purchase department managers can effectively make decision of

make or buy goods. It can be possible by comparing the most relevant cost which can

describe the difference among the various decision options (Tucker and Parker, 2014).

The manager can make decision in which it decides whether to purchase or make a

production parts.

Product costing- The management accounting information which is used to measure the

cost of goods. It facilitates them in understanding the cost of products is needed to assist

the small firms. It helps them in determining the price at that they sold its products at the

break- even point. It is used by the production manager of Imda tech limited to set the

price of goods so, they know its profits before allocating resource in production.

Budgets- The management accounting is commonly used by the small enterprise for the

purpose in preparing the budgets. It can assist the purchase department to make a plan

regard to purchase and sales of goods (Hülle, Kaspar and Möller, 2011). Apart from

this, it can also used to motivate the staff workers and direct management. The finance

manager can able to know the expected sales over the budgeting period and the sales

figure shows help them to know the costing data to measure the cash flows.

b) Explain the different types of management accounting information

The Imda tech limited used the various type of management accounting information which

is used by other departments to enhance its reports. Thus, it can be described below-

i. Cost accounting system- It is a framework that are used by the cited company to

make estimation regard to cost of its products for the purpose of inventory valuation,

profitability analysis and cost control. It assists the manufacture department to

estimate the reliable cost of products so, can able to know which products give them

profits or not (Ambe, 2016). It can be used for the preparation the financial statements

it aid them to estimate the closing value of material stock, WIP and finished stock

inventory.

ii. Inventory management system- The Company can used the inventory management

system for the purpose of maintaining the inventory or stock. It is an element of

supply chain management in which it majorly includes the elements like overseeing

and controlling ordering stock, also controlling amount of goods for sale and storage

of stock. It helps the management accountant to store the day to day operation of

business regard to maintaining the inventory (Tucker and Parker, 2014). It facilitates

them to take new orders from the clients and it able the company to keep track all of

its stock, vendors, orders and more. Thus, there are various software through which

inventory can managed its stock level and also reduce the wastage of resources.

iii. Job costing system- The cited company adopts the job costing system in which there

is a procedure of obtaining the information regard to cost and it is used in assigning

stock that are manufactured products. Thus, this system is used to track cost of

material that which are used course of job (Setthasakko, 2010). Therefore, it includes

three types of information are the direct materials, labour and overhead etc. it can be

used for the purpose of tracking the cost as well as revenues that able to produced the

standardised reports of profitability through job.

TASK 2

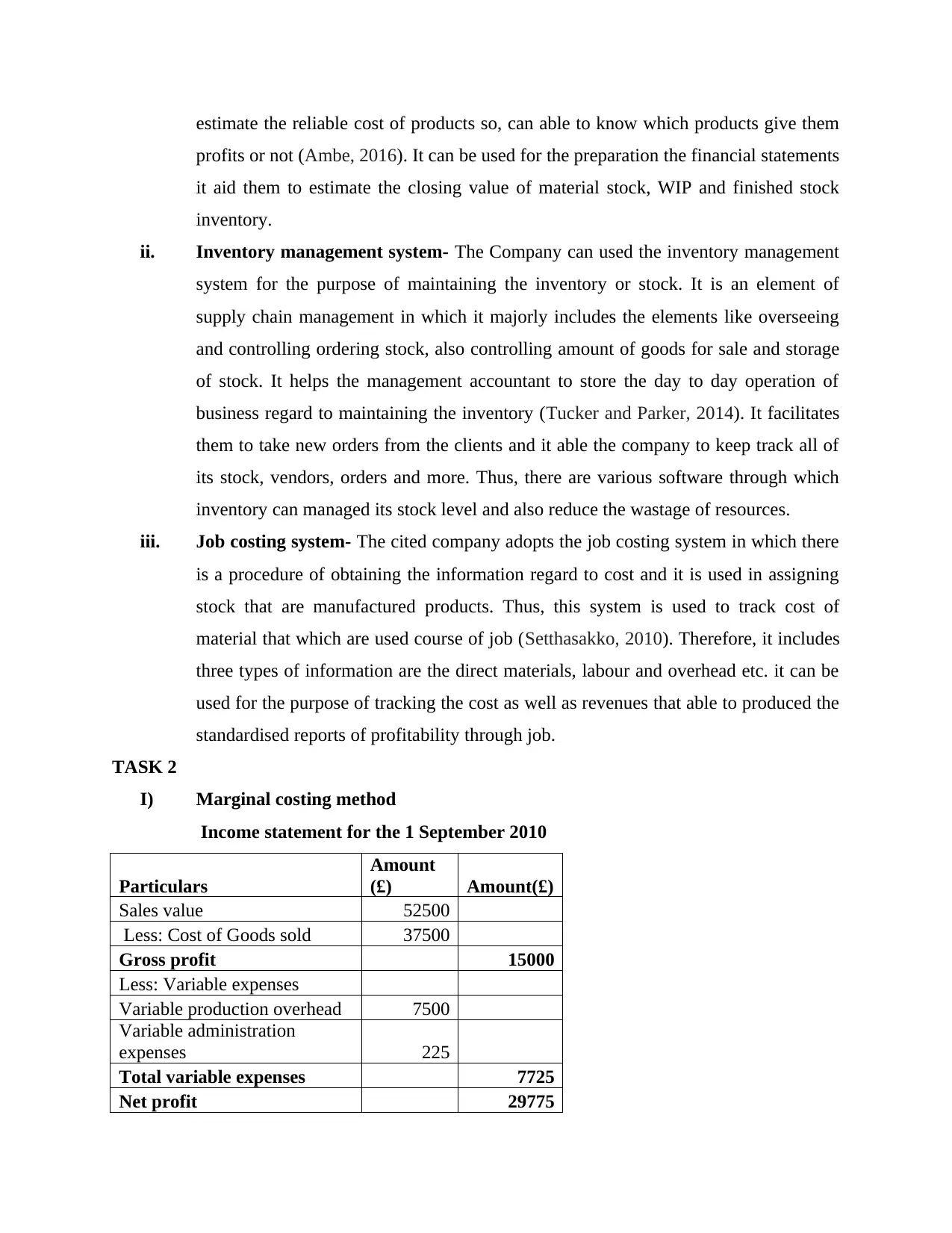

I) Marginal costing method

Income statement for the 1 September 2010

Particulars

Amount

(£) Amount(£)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Net profit 29775

profits or not (Ambe, 2016). It can be used for the preparation the financial statements

it aid them to estimate the closing value of material stock, WIP and finished stock

inventory.

ii. Inventory management system- The Company can used the inventory management

system for the purpose of maintaining the inventory or stock. It is an element of

supply chain management in which it majorly includes the elements like overseeing

and controlling ordering stock, also controlling amount of goods for sale and storage

of stock. It helps the management accountant to store the day to day operation of

business regard to maintaining the inventory (Tucker and Parker, 2014). It facilitates

them to take new orders from the clients and it able the company to keep track all of

its stock, vendors, orders and more. Thus, there are various software through which

inventory can managed its stock level and also reduce the wastage of resources.

iii. Job costing system- The cited company adopts the job costing system in which there

is a procedure of obtaining the information regard to cost and it is used in assigning

stock that are manufactured products. Thus, this system is used to track cost of

material that which are used course of job (Setthasakko, 2010). Therefore, it includes

three types of information are the direct materials, labour and overhead etc. it can be

used for the purpose of tracking the cost as well as revenues that able to produced the

standardised reports of profitability through job.

TASK 2

I) Marginal costing method

Income statement for the 1 September 2010

Particulars

Amount

(£) Amount(£)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Net profit 29775

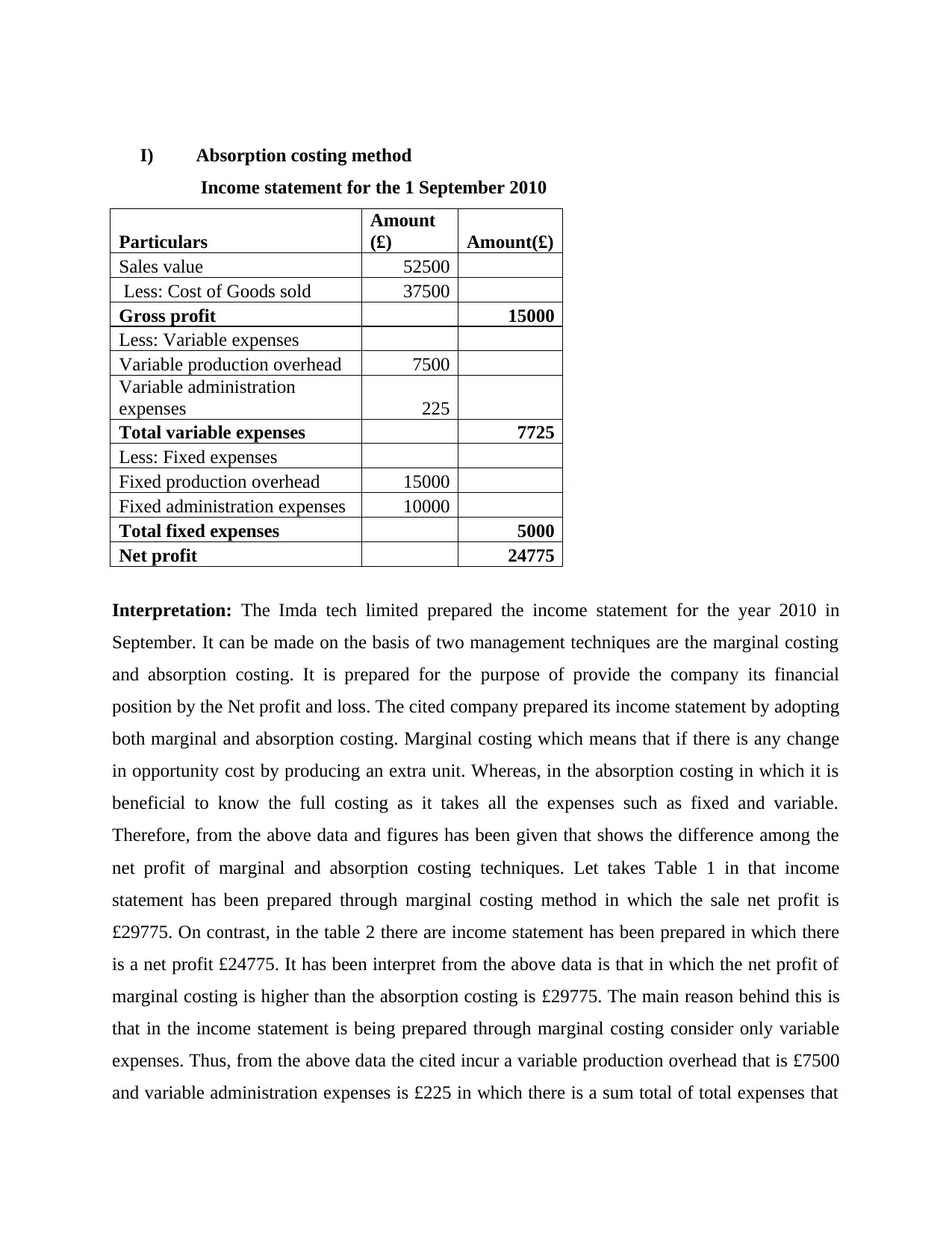

I) Absorption costing method

Income statement for the 1 September 2010

Particulars

Amount

(£) Amount(£)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Less: Fixed expenses

Fixed production overhead 15000

Fixed administration expenses 10000

Total fixed expenses 5000

Net profit 24775

Interpretation: The Imda tech limited prepared the income statement for the year 2010 in

September. It can be made on the basis of two management techniques are the marginal costing

and absorption costing. It is prepared for the purpose of provide the company its financial

position by the Net profit and loss. The cited company prepared its income statement by adopting

both marginal and absorption costing. Marginal costing which means that if there is any change

in opportunity cost by producing an extra unit. Whereas, in the absorption costing in which it is

beneficial to know the full costing as it takes all the expenses such as fixed and variable.

Therefore, from the above data and figures has been given that shows the difference among the

net profit of marginal and absorption costing techniques. Let takes Table 1 in that income

statement has been prepared through marginal costing method in which the sale net profit is

£29775. On contrast, in the table 2 there are income statement has been prepared in which there

is a net profit £24775. It has been interpret from the above data is that in which the net profit of

marginal costing is higher than the absorption costing is £29775. The main reason behind this is

that in the income statement is being prepared through marginal costing consider only variable

expenses. Thus, from the above data the cited incur a variable production overhead that is £7500

and variable administration expenses is £225 in which there is a sum total of total expenses that

Income statement for the 1 September 2010

Particulars

Amount

(£) Amount(£)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Less: Fixed expenses

Fixed production overhead 15000

Fixed administration expenses 10000

Total fixed expenses 5000

Net profit 24775

Interpretation: The Imda tech limited prepared the income statement for the year 2010 in

September. It can be made on the basis of two management techniques are the marginal costing

and absorption costing. It is prepared for the purpose of provide the company its financial

position by the Net profit and loss. The cited company prepared its income statement by adopting

both marginal and absorption costing. Marginal costing which means that if there is any change

in opportunity cost by producing an extra unit. Whereas, in the absorption costing in which it is

beneficial to know the full costing as it takes all the expenses such as fixed and variable.

Therefore, from the above data and figures has been given that shows the difference among the

net profit of marginal and absorption costing techniques. Let takes Table 1 in that income

statement has been prepared through marginal costing method in which the sale net profit is

£29775. On contrast, in the table 2 there are income statement has been prepared in which there

is a net profit £24775. It has been interpret from the above data is that in which the net profit of

marginal costing is higher than the absorption costing is £29775. The main reason behind this is

that in the income statement is being prepared through marginal costing consider only variable

expenses. Thus, from the above data the cited incur a variable production overhead that is £7500

and variable administration expenses is £225 in which there is a sum total of total expenses that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is £7725. On contrast to this, the cited firm adopts the absorption costing methods in which it

consider both type of expenses are the fixed and variable expenses. Thus, from the above data

the total fixed expenses it takes that is £ and the total variable expenses £7725 for which there is

a total expenses is £5000. The main difference among net profit in the marginal costing and

absorption costing technique that are explained further. Thus, from the above data table 1 and

table 2 in that the calculation of net profit by using marginal costing in which sales revenue is

minus total variable expenses. Therefore, sales revenue is £52500 minus total variable expenses

is £7725 in which the net profit obtains from this value is £29775. On contrast to this, from the

table 2 there is a calculation of net profit is £24775 that are come from sales revenue £52500

minus total expenses is £5000.

consider both type of expenses are the fixed and variable expenses. Thus, from the above data

the total fixed expenses it takes that is £ and the total variable expenses £7725 for which there is

a total expenses is £5000. The main difference among net profit in the marginal costing and

absorption costing technique that are explained further. Thus, from the above data table 1 and

table 2 in that the calculation of net profit by using marginal costing in which sales revenue is

minus total variable expenses. Therefore, sales revenue is £52500 minus total variable expenses

is £7725 in which the net profit obtains from this value is £29775. On contrast to this, from the

table 2 there is a calculation of net profit is £24775 that are come from sales revenue £52500

minus total expenses is £5000.

Task 3

P4 Advantage and disadvantage of different types of budget

A) Budget is one of the important part of business operations. Proper and accurate budget

can help in gaining high profit to the organization. In the management meeting it was

discussed by Imda Tech Limited that all department managers have to be involved in

budget preparation (Rosentreter Singh and Schönbohm, 2013)

There are several types of the budget which can be used by cited firm, these are

discussed as below:

Incremental budgeting

It is one of the important tool which explains that by making small changes in existing

budget firms can prepare a new budget (Noordin, 2016)

. They have to add incremental amount in the new budget. There is no single formula for

preparing incremental budget but there is approach of assumption that can help in preparing this

financial budget. Expenses of last year will be starting point of this year.

Advantage:

it is very simple process and easily to implement. It does not involve complex

calculations (Lay, 2016). In such type of budget managers of Imda Tech Limited need

not to do detail analyses of each activity.

It ensures continuity of cash inflow so issues like shortage of funds do not take place. It is beneficial tool in which impact of changes are immediately seen .

Disadvantage:

This budget is based on assumption and if assumptions are wrong then overall result will

be negative (Gibassier, 2017).

It encourages higher spending for maintaining budget of next year.

Budgetary slack is one of the major drawback of this budget in this company will earn

lower revenue and will spend high amount.

Zero-based budgeting

It is another type of budget which can be used by Imda Tech Limited. In this method, all

expenditures are needed to be justified for new financial year (BAHRI and REZAIE, 2016)

P4 Advantage and disadvantage of different types of budget

A) Budget is one of the important part of business operations. Proper and accurate budget

can help in gaining high profit to the organization. In the management meeting it was

discussed by Imda Tech Limited that all department managers have to be involved in

budget preparation (Rosentreter Singh and Schönbohm, 2013)

There are several types of the budget which can be used by cited firm, these are

discussed as below:

Incremental budgeting

It is one of the important tool which explains that by making small changes in existing

budget firms can prepare a new budget (Noordin, 2016)

. They have to add incremental amount in the new budget. There is no single formula for

preparing incremental budget but there is approach of assumption that can help in preparing this

financial budget. Expenses of last year will be starting point of this year.

Advantage:

it is very simple process and easily to implement. It does not involve complex

calculations (Lay, 2016). In such type of budget managers of Imda Tech Limited need

not to do detail analyses of each activity.

It ensures continuity of cash inflow so issues like shortage of funds do not take place. It is beneficial tool in which impact of changes are immediately seen .

Disadvantage:

This budget is based on assumption and if assumptions are wrong then overall result will

be negative (Gibassier, 2017).

It encourages higher spending for maintaining budget of next year.

Budgetary slack is one of the major drawback of this budget in this company will earn

lower revenue and will spend high amount.

Zero-based budgeting

It is another type of budget which can be used by Imda Tech Limited. In this method, all

expenditures are needed to be justified for new financial year (BAHRI and REZAIE, 2016)

. It starts with zero base in which managers have to identify objectives then they have to evaluate

alternative methods and in the last phase of budget preparation they have to allocate resource

according to priorities (Klychova, Faskhutdinova and Sadrieva, 2014).

Advantage:

Alternative analyses is major advantage of this budgeting in which manager find out

alternative ways to get profit through budget.

In zero based budgeting managers look upon the effectiveness of activities and eliminate

non key activities (Taipaleenmäki, 2014).

With the help of this tool redundancy can be identified by the managers so such type of

activities can be reduced. Resources are all being allocated as per the mission and objective of organization so cited

firm will be able to accomplish its goal significantly.If Imda Tech Limited uses zero

based budgeting method then it will help in reviewing the all aspects periodically

(Bebbington, Unerman and O'Dwyer, 2014)

Disadvantage:

For preparing this budget high level of efforts are required. Because close investigation is

required for each department activities.

Bureaucracy is another drawback of this type of budget and to manage it organization

will require additional staff members.

For preparing zero based budgeting company will have to train its staff members which

will be time consuming.

Fixed budgeting

It is the final financial plan which cannot be changed by the entities. It is an essential tool

through which success of small firms can be measured easily (Rosentreter Singh and

Schönbohm, 2013).

Advantage:

With the help of this method company like Imda Tech Limited can measure short term and long

term profit of the organization. In this, same amount is allotted in all months thus, performance

of the company can be measured effectively (Lay, 2016).

alternative methods and in the last phase of budget preparation they have to allocate resource

according to priorities (Klychova, Faskhutdinova and Sadrieva, 2014).

Advantage:

Alternative analyses is major advantage of this budgeting in which manager find out

alternative ways to get profit through budget.

In zero based budgeting managers look upon the effectiveness of activities and eliminate

non key activities (Taipaleenmäki, 2014).

With the help of this tool redundancy can be identified by the managers so such type of

activities can be reduced. Resources are all being allocated as per the mission and objective of organization so cited

firm will be able to accomplish its goal significantly.If Imda Tech Limited uses zero

based budgeting method then it will help in reviewing the all aspects periodically

(Bebbington, Unerman and O'Dwyer, 2014)

Disadvantage:

For preparing this budget high level of efforts are required. Because close investigation is

required for each department activities.

Bureaucracy is another drawback of this type of budget and to manage it organization

will require additional staff members.

For preparing zero based budgeting company will have to train its staff members which

will be time consuming.

Fixed budgeting

It is the final financial plan which cannot be changed by the entities. It is an essential tool

through which success of small firms can be measured easily (Rosentreter Singh and

Schönbohm, 2013).

Advantage:

With the help of this method company like Imda Tech Limited can measure short term and long

term profit of the organization. In this, same amount is allotted in all months thus, performance

of the company can be measured effectively (Lay, 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

In this type of budgeting method, finance manager focus on reducing cost. Company

strict to its financial limits and financial discipline has to be maintained by all level

persons.

Disadvantage:

Lack of flexibility is the major drawback of this budgeting system. Once company has set

a budget on the bases of sales volume then it cannot allocate additional resources if sales

get increased (Bebbington, Unerman and O'Dwyer, 2014).

It is useful only such places where companies are highly predictable for its sales volume.

B) Process of preparing budget

Preparation of final budget is the crucial task for the organizations, they have to compare

the report with last year and have to make assumption for future. Process of preparing budget are

described as below:

Gather information: It is the first step in which managers have to collect all relevant

information such as sales, cost etc. On the basis of these details final budget is prepared.

Record all income source: In this phase Imda Tech Limited will have to look upon

income sources so that estimation of cash inflow can be done. Accordingly cited firm can

allocate resources to each activity (Gibassier, 2017).

Create list of expenses: Once income is identified then organization will have to look

upon the expenditures which are going to incurred in this financial year.

Breaking of expenses is the next phase in which all fixed and variable cost are to be

separated.

Total income can expenses are assumed by the managers of Imda Tech Limited now they

have to make adjustments (BAHRI and REZAIE, 2016).

Unnecessary expenses need to be cut down so that resources can be used effectively.

Once it is done then managers have to review the budget monthly so that actual results

can be find out.

C) Pricing strategies

Price is the major factor that can influence mind of consumers. Effective pricing

strategies help in enhancing market share, increasing profit and gaining competitive advantage

(Taipaleenmäki, 2014).

Cost-based pricing

strict to its financial limits and financial discipline has to be maintained by all level

persons.

Disadvantage:

Lack of flexibility is the major drawback of this budgeting system. Once company has set

a budget on the bases of sales volume then it cannot allocate additional resources if sales

get increased (Bebbington, Unerman and O'Dwyer, 2014).

It is useful only such places where companies are highly predictable for its sales volume.

B) Process of preparing budget

Preparation of final budget is the crucial task for the organizations, they have to compare

the report with last year and have to make assumption for future. Process of preparing budget are

described as below:

Gather information: It is the first step in which managers have to collect all relevant

information such as sales, cost etc. On the basis of these details final budget is prepared.

Record all income source: In this phase Imda Tech Limited will have to look upon

income sources so that estimation of cash inflow can be done. Accordingly cited firm can

allocate resources to each activity (Gibassier, 2017).

Create list of expenses: Once income is identified then organization will have to look

upon the expenditures which are going to incurred in this financial year.

Breaking of expenses is the next phase in which all fixed and variable cost are to be

separated.

Total income can expenses are assumed by the managers of Imda Tech Limited now they

have to make adjustments (BAHRI and REZAIE, 2016).

Unnecessary expenses need to be cut down so that resources can be used effectively.

Once it is done then managers have to review the budget monthly so that actual results

can be find out.

C) Pricing strategies

Price is the major factor that can influence mind of consumers. Effective pricing

strategies help in enhancing market share, increasing profit and gaining competitive advantage

(Taipaleenmäki, 2014).

Cost-based pricing

It is important pricing strategy in which Imda Tech Limited can include all costs and can add

company’s profit in it to get the price. By this way cited firm will be able to get desired profit

percentage. It will help in increasing profit of the firm to great extent. It long term profit earning

strategies that can help cited firm in accomplishing its goal soon (Gibassier, 2017).

Marginal cost plus pricing

It is another type of strategy which is used for short term profit earning. In this Imda Tech

Limited can offer consumers discounts or buy products on reduced price. It is less appropriate

because fixed cost can not be recovered by the organization with this strategy (Rosentreter Singh

and Schönbohm, 2013).

Competitive pricing:

In this Imda Tech Limited can use competitor prices for selling its products. If

competitors are offering same quality, size products then cited firm can use this strategy. That

would help in sustaining in competitive market for longer duration (Gibassier, 2017).

Price skimming

It is the strategy in which Imda Tech Limited can charge extra ordinary high prices with

consumers. It can be applied if cited firm offer innovative and luxury products to customers. By

this way organization will be able to recover its development expenses soon.

P5 Balance score card approach

Earlier firms were using traditional methods to evaluate their last year performances but

now there are many tools that can help in measuring performance of the organizations. Balance

scorecard is an approach which is used by entities for measuring their overall performance

(Klychova, Faskhutdinova and Sadrieva, 2014). It evaluates the working on the bases of four

criteria such as financial, internal process, customers and learning or growth. It evaluates the

efforts of firm for the future improvement of organizations.

It not only focuses on financial performance of Balance Score Card approach but also

consider the non-financial perspectives too (BAHRI and REZAIE, 2016). Financial perspective: Balance score card pay attention on cash flow, sales growth,

income, equity etc. If the cash inflow has been increased that means cited firm has earned

profit and it has performed well in the financial year (Bebbington, Unerman and

O'Dwyer, 2014).

company’s profit in it to get the price. By this way cited firm will be able to get desired profit

percentage. It will help in increasing profit of the firm to great extent. It long term profit earning

strategies that can help cited firm in accomplishing its goal soon (Gibassier, 2017).

Marginal cost plus pricing

It is another type of strategy which is used for short term profit earning. In this Imda Tech

Limited can offer consumers discounts or buy products on reduced price. It is less appropriate

because fixed cost can not be recovered by the organization with this strategy (Rosentreter Singh

and Schönbohm, 2013).

Competitive pricing:

In this Imda Tech Limited can use competitor prices for selling its products. If

competitors are offering same quality, size products then cited firm can use this strategy. That

would help in sustaining in competitive market for longer duration (Gibassier, 2017).

Price skimming

It is the strategy in which Imda Tech Limited can charge extra ordinary high prices with

consumers. It can be applied if cited firm offer innovative and luxury products to customers. By

this way organization will be able to recover its development expenses soon.

P5 Balance score card approach

Earlier firms were using traditional methods to evaluate their last year performances but

now there are many tools that can help in measuring performance of the organizations. Balance

scorecard is an approach which is used by entities for measuring their overall performance

(Klychova, Faskhutdinova and Sadrieva, 2014). It evaluates the working on the bases of four

criteria such as financial, internal process, customers and learning or growth. It evaluates the

efforts of firm for the future improvement of organizations.

It not only focuses on financial performance of Balance Score Card approach but also

consider the non-financial perspectives too (BAHRI and REZAIE, 2016). Financial perspective: Balance score card pay attention on cash flow, sales growth,

income, equity etc. If the cash inflow has been increased that means cited firm has earned

profit and it has performed well in the financial year (Bebbington, Unerman and

O'Dwyer, 2014).

Customers: it is another area that helps to measure the performance of Balance Score

Card approach. It includes consumer’s satisfaction, retention, market share etc. It can be

evaluated on the bases of all these areas. For instance, in the fiscal year Balance Score

Card approach has increased number of consumers that means clients are satisfied with

the products and they will be connected with the brand for longer duration (BAHRI and

REZAIE, 2016). On the basis on this aspect it can be evaluated that cited firm is offering

quality products and services to its users and people are very satisfied. Increased retention

rate of customers show that organization is able to gain competitive advantage that would

help in sustaining in the corporate market for longer period. Internal process: It includes procurement, production etc. On the bases of these areas

performance of Balance Score Card approach can be measured.

Learning & growth perspective: It includes employee’s satisfaction, retention rate of

workers, skills sets etc. For instance, if company is performing well then workers will

like the workplace because they will find career opportunity in the cited firm. By this way

skilled persons will stay in the organization for longer duration. That shows that company

is performing well and it can earn high profit as well (Gibassier, 2017).

Balance score card is a beneficial tool that supports Balance Score Card approach in

identifying and respond to financial problems. With the help of this techniques cited firm can

measure its performance and can identify its lacking points. By this way managers of cited firm

will be able to make effective strategies that can support in reducing economic problems of the

organization (Bebbington, Unerman and O'Dwyer, 2014). As financial performance can be

measured through sales volume, equity return, income growth etc. if sales is lower than its

expectation then organization will be able to find out the root cause of the problems and will find

suitable solution to resolve this issue. In the business planning managers of Balance Score Card

approach set long term business objectives. In order to achieve these goal management level

persons, take strategic initiatives and allocate resources. If consumers are satisfied that means

faster payment will be collected that means high income or cash inflow (Gibassier, 2017).

Customer based and internal process perspectives are important tools through which

performance of company can be measured easily. Through this cited firm can identify its

problems and managers can work to improve it. For instance, if in the Imda Tech Limited there

are high employees turn over that shows that cited firm is not treating its workers well or staff

Card approach. It includes consumer’s satisfaction, retention, market share etc. It can be

evaluated on the bases of all these areas. For instance, in the fiscal year Balance Score

Card approach has increased number of consumers that means clients are satisfied with

the products and they will be connected with the brand for longer duration (BAHRI and

REZAIE, 2016). On the basis on this aspect it can be evaluated that cited firm is offering

quality products and services to its users and people are very satisfied. Increased retention

rate of customers show that organization is able to gain competitive advantage that would

help in sustaining in the corporate market for longer period. Internal process: It includes procurement, production etc. On the bases of these areas

performance of Balance Score Card approach can be measured.

Learning & growth perspective: It includes employee’s satisfaction, retention rate of

workers, skills sets etc. For instance, if company is performing well then workers will

like the workplace because they will find career opportunity in the cited firm. By this way

skilled persons will stay in the organization for longer duration. That shows that company

is performing well and it can earn high profit as well (Gibassier, 2017).

Balance score card is a beneficial tool that supports Balance Score Card approach in

identifying and respond to financial problems. With the help of this techniques cited firm can

measure its performance and can identify its lacking points. By this way managers of cited firm

will be able to make effective strategies that can support in reducing economic problems of the

organization (Bebbington, Unerman and O'Dwyer, 2014). As financial performance can be

measured through sales volume, equity return, income growth etc. if sales is lower than its

expectation then organization will be able to find out the root cause of the problems and will find

suitable solution to resolve this issue. In the business planning managers of Balance Score Card

approach set long term business objectives. In order to achieve these goal management level

persons, take strategic initiatives and allocate resources. If consumers are satisfied that means

faster payment will be collected that means high income or cash inflow (Gibassier, 2017).

Customer based and internal process perspectives are important tools through which

performance of company can be measured easily. Through this cited firm can identify its

problems and managers can work to improve it. For instance, if in the Imda Tech Limited there

are high employees turn over that shows that cited firm is not treating its workers well or staff

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are not getting growth opportunity in the organization (Taipaleenmäki, 2014). On other hand if

company is suffering from financial problems of cash inflow is the problems then it shows

consumers are not satisfied. By this way cited firm can make effective strategy that can support

in improving its economic condition. Management can change their pricing strategies and can

improve quality of products (Rosentreter Singh and Schönbohm, 2013). By this way more people

will get attracted towards the brand and issues of cash flow will get minimized significantly.

Conclusion

From the above report, it can be concluded that management accounting is the important

part of business units. Firms have to manage their operations well so that it can sustain in the

corporate market for longer duration. Competition is very high to survive in such environment it

is necessary to prepare a good budget. It can be prepared by looking upon income and cost of the

organization in particular fiscal year. Management accounting can be define in that it is a

procedure in which the useful information can be identifying, analyzing, measuring, interpreting

and transfer data of accounting that attain the company to reach its goal in effective manner.

Thus, it can be used by the manager of Imda tech limited to make their day to day decisions of

business so, they can carry out all the function in smoothly. It is highly by the management for

the purpose of looking forward and it is used by the internal affairs. Though it is difficult task but

this can help in identifying the sales volume and income of the organization. By this way

managers will be able to allocate the resources well. Zero based budgeting is effective tool, it is

not depended upon the assumptions so good results can be come out and organizations can

accomplish their objective easily. Report has discussed about balance score card. It can be

articulate that it is the technique through which companies can manage their operations well.

With the help of this tool problems will be identified and management will be able to make plan

to resolve such issues. It has been also analysed from the above data is that in which the net

profit of marginal costing is higher than the absorption costing is £29775. The main reason

behind this is that in the income statement is being prepared through marginal costing consider

only variable expenses.

company is suffering from financial problems of cash inflow is the problems then it shows

consumers are not satisfied. By this way cited firm can make effective strategy that can support

in improving its economic condition. Management can change their pricing strategies and can

improve quality of products (Rosentreter Singh and Schönbohm, 2013). By this way more people

will get attracted towards the brand and issues of cash flow will get minimized significantly.

Conclusion

From the above report, it can be concluded that management accounting is the important

part of business units. Firms have to manage their operations well so that it can sustain in the

corporate market for longer duration. Competition is very high to survive in such environment it

is necessary to prepare a good budget. It can be prepared by looking upon income and cost of the

organization in particular fiscal year. Management accounting can be define in that it is a

procedure in which the useful information can be identifying, analyzing, measuring, interpreting

and transfer data of accounting that attain the company to reach its goal in effective manner.

Thus, it can be used by the manager of Imda tech limited to make their day to day decisions of

business so, they can carry out all the function in smoothly. It is highly by the management for

the purpose of looking forward and it is used by the internal affairs. Though it is difficult task but

this can help in identifying the sales volume and income of the organization. By this way

managers will be able to allocate the resources well. Zero based budgeting is effective tool, it is

not depended upon the assumptions so good results can be come out and organizations can

accomplish their objective easily. Report has discussed about balance score card. It can be

articulate that it is the technique through which companies can manage their operations well.

With the help of this tool problems will be identified and management will be able to make plan

to resolve such issues. It has been also analysed from the above data is that in which the net

profit of marginal costing is higher than the absorption costing is £29775. The main reason

behind this is that in the income statement is being prepared through marginal costing consider

only variable expenses.

References

Books and Journals

Rosentreter, S.J., Singh, P. and Schönbohm, A., 2013. Research output of management

accounting academics at Universities of Applied Sciences in Germany and Universities of

Technology in South Africa: a comparative study of input determinants (No. 77). Working

Papers of the Institute of Management Berlin at the Berlin School of Economics and Law

(HWR Berlin).

Noordin, R., 2016. Strategic management accounting information elements: Malaysian

evidence. Asia-Pacific Management Accounting Journal. 4(1).

Lay, T. A., 2016. Business Strategy, Strategic Role of Accountant, Strategic Management

Accounting and their Links to Firm Performance: An Exploratory Study of Manufacturing

Companies in Malaysia. Asia-Pacific Management Accounting Journal. 7(1).

BAHRI, S. J. and REZAIE, F., 2016. AN INTEGRATED APPROACH TO GREEN DESIGN,

PRODUCT LIFE CYCLE, AHP FUZZY AND ENVIRONMENTAL MANAGEMENT

ACCOUNTING (CASE STUDY: WIRE AND CABLE MANUFACTURING

COMPANY OF TABRIZ).

Gibassier, D., 2017. From écobilan to LCA: the elite’s institutional work in the creation of an

environmental management accounting tool. Critical Perspectives on Accounting. 42.

pp.36-58.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E. R., 2014. Budget efficiency for cost

control purposes in management accounting system.Mediterranean Journal of Social

Sciences. 5(24). pp.79.

Taipaleenmäki, J., 2014. Absence and variant modes of presence of management accounting in

new product development–theoretical refinement and some empirical evidence. European

Accounting Review. 23(2). pp.291-334.

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Lowe, A. and De Loo, I., 2014. The existential perversity of management accounting and

control. In Management Control and Uncertainty (pp. 239-254). Palgrave Macmillan UK.

Books and Journals

Rosentreter, S.J., Singh, P. and Schönbohm, A., 2013. Research output of management

accounting academics at Universities of Applied Sciences in Germany and Universities of

Technology in South Africa: a comparative study of input determinants (No. 77). Working

Papers of the Institute of Management Berlin at the Berlin School of Economics and Law

(HWR Berlin).

Noordin, R., 2016. Strategic management accounting information elements: Malaysian

evidence. Asia-Pacific Management Accounting Journal. 4(1).

Lay, T. A., 2016. Business Strategy, Strategic Role of Accountant, Strategic Management

Accounting and their Links to Firm Performance: An Exploratory Study of Manufacturing

Companies in Malaysia. Asia-Pacific Management Accounting Journal. 7(1).

BAHRI, S. J. and REZAIE, F., 2016. AN INTEGRATED APPROACH TO GREEN DESIGN,

PRODUCT LIFE CYCLE, AHP FUZZY AND ENVIRONMENTAL MANAGEMENT

ACCOUNTING (CASE STUDY: WIRE AND CABLE MANUFACTURING

COMPANY OF TABRIZ).

Gibassier, D., 2017. From écobilan to LCA: the elite’s institutional work in the creation of an

environmental management accounting tool. Critical Perspectives on Accounting. 42.

pp.36-58.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E. R., 2014. Budget efficiency for cost

control purposes in management accounting system.Mediterranean Journal of Social

Sciences. 5(24). pp.79.

Taipaleenmäki, J., 2014. Absence and variant modes of presence of management accounting in

new product development–theoretical refinement and some empirical evidence. European

Accounting Review. 23(2). pp.291-334.

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Lowe, A. and De Loo, I., 2014. The existential perversity of management accounting and

control. In Management Control and Uncertainty (pp. 239-254). Palgrave Macmillan UK.

Setthasakko, W., 2010. Barriers to the development of environmental management accounting:

An exploratory study of pulp and paper companies in Thailand. EuroMed Journal of

Business, 5(3), pp.315-331.

Scapens, R.W. and Bromwich, M., 2010. Practice, theory and paradigms.

Yalcin, S., 2012. Adoption and benefits of management accounting practices: an inter-country

comparison. Accounting in Europe, 9(1), pp.95-110.

Tucker, B. and Parker, L., 2014. In our ivory towers? The research-practice gap in management

accounting. Accounting and Business Research, 44(2), pp.104-143.

Hülle, J., Kaspar, R. and Möller, K., 2011. Multiple Criteria Decision‐Making in Management

Accounting and Control‐State of the Art and Research Perspectives Based on a

Bibliometric Study. Journal of Multi

‐Criteria Decision Analysis, 18(5-6), pp.253-265.

Ambe, C.M., 2016. Environmental management accounting in South Africa: Status, challenges

and implementation framework.

An exploratory study of pulp and paper companies in Thailand. EuroMed Journal of

Business, 5(3), pp.315-331.

Scapens, R.W. and Bromwich, M., 2010. Practice, theory and paradigms.

Yalcin, S., 2012. Adoption and benefits of management accounting practices: an inter-country

comparison. Accounting in Europe, 9(1), pp.95-110.

Tucker, B. and Parker, L., 2014. In our ivory towers? The research-practice gap in management

accounting. Accounting and Business Research, 44(2), pp.104-143.

Hülle, J., Kaspar, R. and Möller, K., 2011. Multiple Criteria Decision‐Making in Management

Accounting and Control‐State of the Art and Research Perspectives Based on a

Bibliometric Study. Journal of Multi

‐Criteria Decision Analysis, 18(5-6), pp.253-265.

Ambe, C.M., 2016. Environmental management accounting in South Africa: Status, challenges

and implementation framework.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.