Finance Sources, Implications, and Stock Listing for Milner Chemicals

VerifiedAdded on 2023/04/04

|26

|4570

|228

Report

AI Summary

This report provides a comprehensive financial analysis of Milner Chemicals Plc, examining various aspects of its financial strategy. It identifies and assesses different sources of finance, including internal and external options, and evaluates their implications for the company. The report delves into the advantages and disadvantages of obtaining a listing on the London Stock Exchange, along with the methods available for achieving this. Furthermore, it analyzes the cost of different types of capital, such as ordinary shares, preference shares, and debentures, and calculates the Weighted Average Cost of Capital (WACC). The report also addresses the importance of financial planning, the informational needs of different management levels, and the impact of finance on financial statements. Additionally, it includes calculations of production costs, prices, and profit, along with a production budget and the calculation of Payback Period (PBP), Accounting Rate of Return (ARR), and Net Present Value (NPV). The report concludes with a detailed assessment of the company's financial position and strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 01.............................................................................................................................................3

1.1 Identify different sources of finance..........................................................................................3

1.2 Assess the implications of the different sources........................................................................3

1.3 obtaining a listing in a stock exchanged....................................................................................3

1.4 methods of obtaining a listin......................................................................................................3

1.5 the methods of raising capital....................................................................................................3

Task 02.............................................................................................................................................3

2.1 Cost of Shares & Debt...............................................................................................................3

2.1 (a) Cost of Ordinary Share Capital............................................................................................3

2.1 (b) Cost of Preference share capital...........................................................................................3

2.1 (c) cost of debenture capital after tax........................................................................................3

2.1 (d) Calculating the Weighted Average Cost of Capital (WACC).............................................3

2.2 Importance of Financial Planning..............................................................................................3

2.3 Informational Needs of Directors, Senior Managers and Junior Managers..............................3

2.4 Impact of Finance on the Financial Statements.........................................................................3

Task 03.............................................................................................................................................3

2 | P a g e

Task 01.............................................................................................................................................3

1.1 Identify different sources of finance..........................................................................................3

1.2 Assess the implications of the different sources........................................................................3

1.3 obtaining a listing in a stock exchanged....................................................................................3

1.4 methods of obtaining a listin......................................................................................................3

1.5 the methods of raising capital....................................................................................................3

Task 02.............................................................................................................................................3

2.1 Cost of Shares & Debt...............................................................................................................3

2.1 (a) Cost of Ordinary Share Capital............................................................................................3

2.1 (b) Cost of Preference share capital...........................................................................................3

2.1 (c) cost of debenture capital after tax........................................................................................3

2.1 (d) Calculating the Weighted Average Cost of Capital (WACC).............................................3

2.2 Importance of Financial Planning..............................................................................................3

2.3 Informational Needs of Directors, Senior Managers and Junior Managers..............................3

2.4 Impact of Finance on the Financial Statements.........................................................................3

Task 03.............................................................................................................................................3

2 | P a g e

3.2 calculations of the production cost, price and profit..................................................................3

3.1 Production Budget.....................................................................................................................3

3.3 Calculation of the PBP, ARR &NPV........................................................................................3

References........................................................................................................................................3

Task 01

1.1 Identify different sources of finance available to Milner chemicals Plc.

As the Milner chemical is a Public Limited Company, it is capable of raising the capital from

two main sources such as internal sources or external sources. (Samuelson, 2006) So here the

internal sources are implying the capital which are generated from the insider of the organization

such as holding the profits of the organization other than dividing to the shareholders, reducing

the inventory level of the organization or delay the payments to its creditors etc. on the other

hand the Milner Plc is capable of going to external fund sources and there are three main types of

external finances such as short term, Medium term and long term. (Charles, 2004)

Here the short term financing sources are indicating the money market which is consisting of the

securities which are matured within one year period or less than one year like treasury bills,

commercial papers etc. and then the medium and the long term financing will indicate the capital

market which is comprising with the securities which are matured more than 5 years like treasury

bonds, bank loans, government bonds etc. so here the company should have to determine their

3 | P a g e

3.1 Production Budget.....................................................................................................................3

3.3 Calculation of the PBP, ARR &NPV........................................................................................3

References........................................................................................................................................3

Task 01

1.1 Identify different sources of finance available to Milner chemicals Plc.

As the Milner chemical is a Public Limited Company, it is capable of raising the capital from

two main sources such as internal sources or external sources. (Samuelson, 2006) So here the

internal sources are implying the capital which are generated from the insider of the organization

such as holding the profits of the organization other than dividing to the shareholders, reducing

the inventory level of the organization or delay the payments to its creditors etc. on the other

hand the Milner Plc is capable of going to external fund sources and there are three main types of

external finances such as short term, Medium term and long term. (Charles, 2004)

Here the short term financing sources are indicating the money market which is consisting of the

securities which are matured within one year period or less than one year like treasury bills,

commercial papers etc. and then the medium and the long term financing will indicate the capital

market which is comprising with the securities which are matured more than 5 years like treasury

bonds, bank loans, government bonds etc. so here the company should have to determine their

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fund requirements with the time framework and the expected future obligations in a cost

effective manner.

Here the trade credit, short term bank loans and the advances, overdrafts, cash credit, customer

advances, installment credit and loans from cooperatives etc. can be identified as short term

external finance sources. And then the medium term loans and the advances as well as the

medium term cash credits, medium term cooperative loans etc. can be considered as medium

term external financing sources to the Milner chemicals. Finally it can be recognized that there

are so many long term finance sources to Milner chemicals like loan finance or loan stocks such

as ordinary shares preference shares in stock market, debentures, long term bank loans,

convertibles debentures and convertibles loan stocks, mortgages, leasing, hire purchase, debt

factoring etc.( Crockford, 2006)

1.2 Assess the implications of the different sources.

When it comes to identify the implications of the internal financing sources of the Milner

chemicals, it can be identified that the internal financing has lesser cost than external fund

sources with raising the capital internally. And also it is not necessary to repaid and no interest is

payable for that as well. But there is a huge capital constraints regarding the amount of money

can be raised itself. (Berezin, M., 2005)

However when it comes to external financing, it may lead to arise a huge amount of money from

the capital markets and it will cause to enhance the financial leverage of the company and

thereby the enhancing the ROE as well. (Shapiro, 2008) Here the company should have assess its

funds requirements in terms of the short run, medium run or long run and the expected capital

structure of the company before going to select the financing resources internally or externally. If

the organization is willing to go for the financial leverage, then it would be better to go for the

debt financing options. (Samuelson, 2006) And also here the company should have to evaluate

their life cycle and place they are n currently, because the debt financing is suitable for the

growing or maturity level firm and unless otherwise it would better to go for equity fiancé with

the existing shareholders of the company and the operational leverage with lower level of debt or

4 | P a g e

effective manner.

Here the trade credit, short term bank loans and the advances, overdrafts, cash credit, customer

advances, installment credit and loans from cooperatives etc. can be identified as short term

external finance sources. And then the medium term loans and the advances as well as the

medium term cash credits, medium term cooperative loans etc. can be considered as medium

term external financing sources to the Milner chemicals. Finally it can be recognized that there

are so many long term finance sources to Milner chemicals like loan finance or loan stocks such

as ordinary shares preference shares in stock market, debentures, long term bank loans,

convertibles debentures and convertibles loan stocks, mortgages, leasing, hire purchase, debt

factoring etc.( Crockford, 2006)

1.2 Assess the implications of the different sources.

When it comes to identify the implications of the internal financing sources of the Milner

chemicals, it can be identified that the internal financing has lesser cost than external fund

sources with raising the capital internally. And also it is not necessary to repaid and no interest is

payable for that as well. But there is a huge capital constraints regarding the amount of money

can be raised itself. (Berezin, M., 2005)

However when it comes to external financing, it may lead to arise a huge amount of money from

the capital markets and it will cause to enhance the financial leverage of the company and

thereby the enhancing the ROE as well. (Shapiro, 2008) Here the company should have assess its

funds requirements in terms of the short run, medium run or long run and the expected capital

structure of the company before going to select the financing resources internally or externally. If

the organization is willing to go for the financial leverage, then it would be better to go for the

debt financing options. (Samuelson, 2006) And also here the company should have to evaluate

their life cycle and place they are n currently, because the debt financing is suitable for the

growing or maturity level firm and unless otherwise it would better to go for equity fiancé with

the existing shareholders of the company and the operational leverage with lower level of debt or

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

no debts within the capital structure of the company. So it is very much important to Milner

chemicals Plc to evaluate their existing capital structure and the expected capital structure before

going to select the options related to the debt financing or equity financing here. (Berezin, M.,

2005)

Bank loans

Advantages Disadvantages

This is good for the budgeting of the company

as the repayments can be spread over the time

period easily

This can be more expensive as the interest

payments

Bank will require some securities for the long

term loans itself

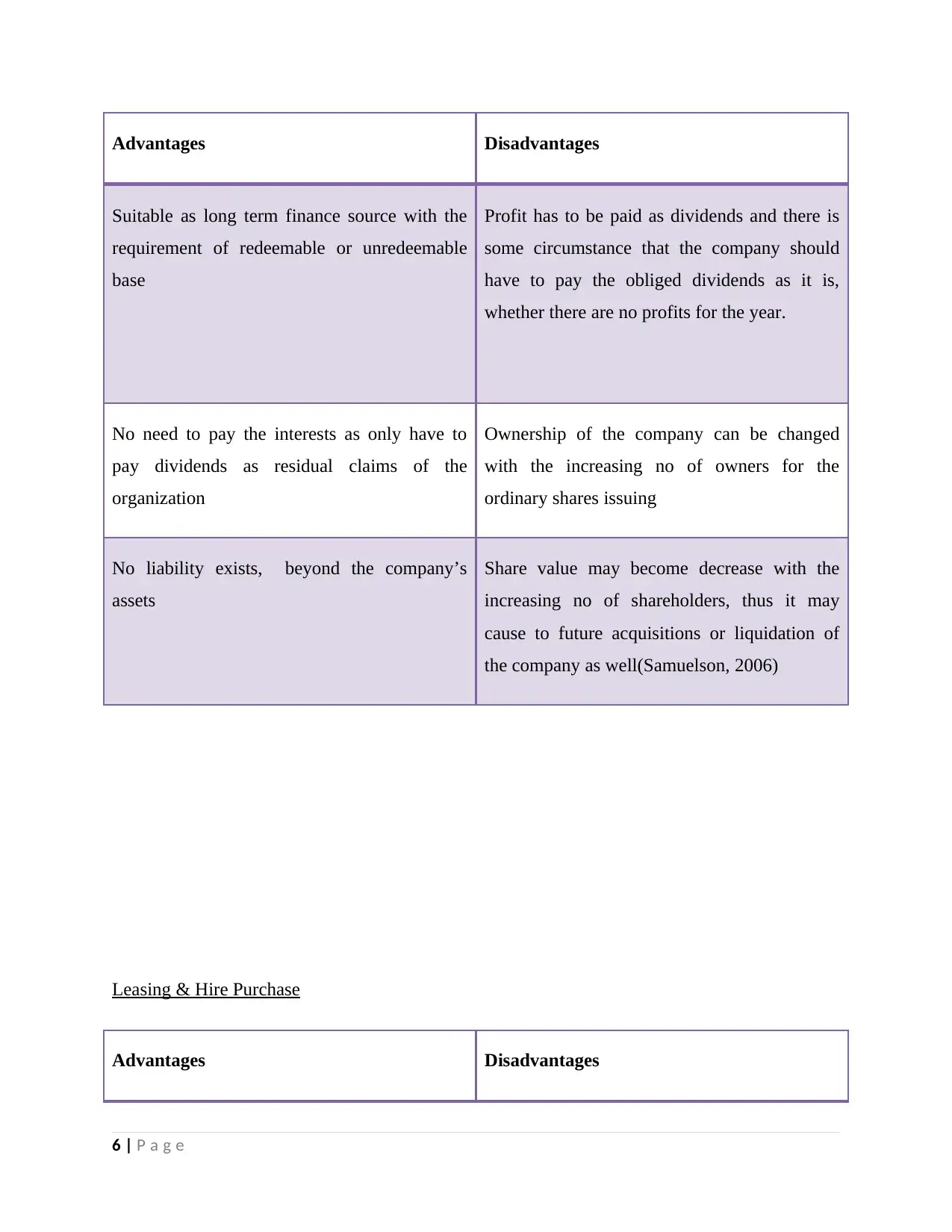

Share Capital (Ordinary Shares & Preference Shares)

5 | P a g e

chemicals Plc to evaluate their existing capital structure and the expected capital structure before

going to select the options related to the debt financing or equity financing here. (Berezin, M.,

2005)

Bank loans

Advantages Disadvantages

This is good for the budgeting of the company

as the repayments can be spread over the time

period easily

This can be more expensive as the interest

payments

Bank will require some securities for the long

term loans itself

Share Capital (Ordinary Shares & Preference Shares)

5 | P a g e

Advantages Disadvantages

Suitable as long term finance source with the

requirement of redeemable or unredeemable

base

Profit has to be paid as dividends and there is

some circumstance that the company should

have to pay the obliged dividends as it is,

whether there are no profits for the year.

No need to pay the interests as only have to

pay dividends as residual claims of the

organization

Ownership of the company can be changed

with the increasing no of owners for the

ordinary shares issuing

No liability exists, beyond the company’s

assets

Share value may become decrease with the

increasing no of shareholders, thus it may

cause to future acquisitions or liquidation of

the company as well(Samuelson, 2006)

Leasing & Hire Purchase

Advantages Disadvantages

6 | P a g e

Suitable as long term finance source with the

requirement of redeemable or unredeemable

base

Profit has to be paid as dividends and there is

some circumstance that the company should

have to pay the obliged dividends as it is,

whether there are no profits for the year.

No need to pay the interests as only have to

pay dividends as residual claims of the

organization

Ownership of the company can be changed

with the increasing no of owners for the

ordinary shares issuing

No liability exists, beyond the company’s

assets

Share value may become decrease with the

increasing no of shareholders, thus it may

cause to future acquisitions or liquidation of

the company as well(Samuelson, 2006)

Leasing & Hire Purchase

Advantages Disadvantages

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

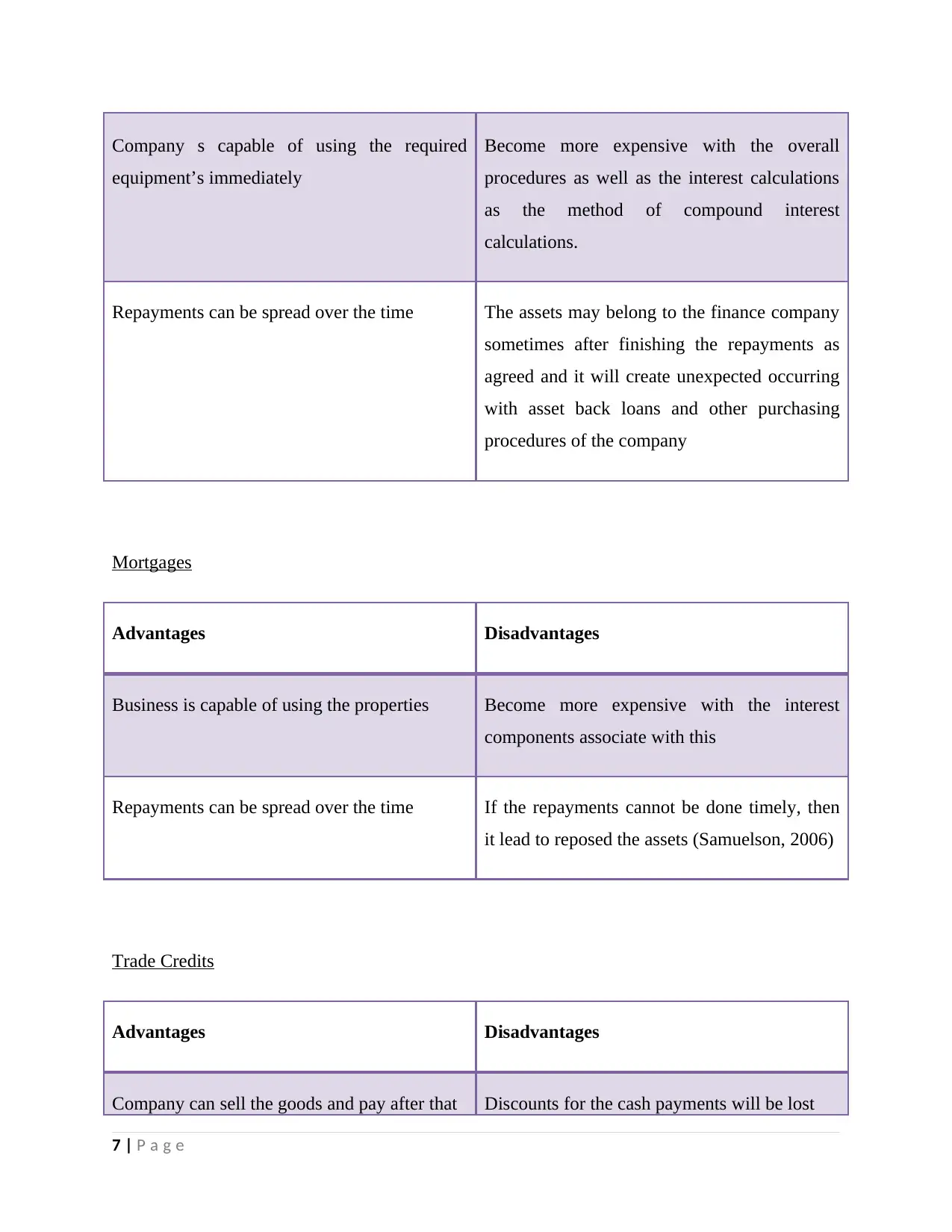

Company s capable of using the required

equipment’s immediately

Become more expensive with the overall

procedures as well as the interest calculations

as the method of compound interest

calculations.

Repayments can be spread over the time The assets may belong to the finance company

sometimes after finishing the repayments as

agreed and it will create unexpected occurring

with asset back loans and other purchasing

procedures of the company

Mortgages

Advantages Disadvantages

Business is capable of using the properties Become more expensive with the interest

components associate with this

Repayments can be spread over the time If the repayments cannot be done timely, then

it lead to reposed the assets (Samuelson, 2006)

Trade Credits

Advantages Disadvantages

Company can sell the goods and pay after that Discounts for the cash payments will be lost

7 | P a g e

equipment’s immediately

Become more expensive with the overall

procedures as well as the interest calculations

as the method of compound interest

calculations.

Repayments can be spread over the time The assets may belong to the finance company

sometimes after finishing the repayments as

agreed and it will create unexpected occurring

with asset back loans and other purchasing

procedures of the company

Mortgages

Advantages Disadvantages

Business is capable of using the properties Become more expensive with the interest

components associate with this

Repayments can be spread over the time If the repayments cannot be done timely, then

it lead to reposed the assets (Samuelson, 2006)

Trade Credits

Advantages Disadvantages

Company can sell the goods and pay after that Discounts for the cash payments will be lost

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Suitable for the cash flows of the company Ned to be more careful about the liquidity of

the company as the debt id due to pay

No need to pay interest if it has paid within the

agreed time period

There should be a better liquidity within the

organization and it will lead to reduce the

profitability as well.

1.3 What are the advantages and disadvantages of obtaining a listing in a stock exchanged like the

London Stock Exchange

Advantages Disadvantages

Milner chemicals can increase their capital as

expectedly

This is an expensive process to the firm with

huge legal expenses, underwriter’s expenses

etc.

It leads to place a value to the company’s

stocks

Have to operate under the closet scrutiny

It gives the permission to access to the capital

market in future financing needs too

Decision making process may become more

formal and low flexible

8 | P a g e

the company as the debt id due to pay

No need to pay interest if it has paid within the

agreed time period

There should be a better liquidity within the

organization and it will lead to reduce the

profitability as well.

1.3 What are the advantages and disadvantages of obtaining a listing in a stock exchanged like the

London Stock Exchange

Advantages Disadvantages

Milner chemicals can increase their capital as

expectedly

This is an expensive process to the firm with

huge legal expenses, underwriter’s expenses

etc.

It leads to place a value to the company’s

stocks

Have to operate under the closet scrutiny

It gives the permission to access to the capital

market in future financing needs too

Decision making process may become more

formal and low flexible

8 | P a g e

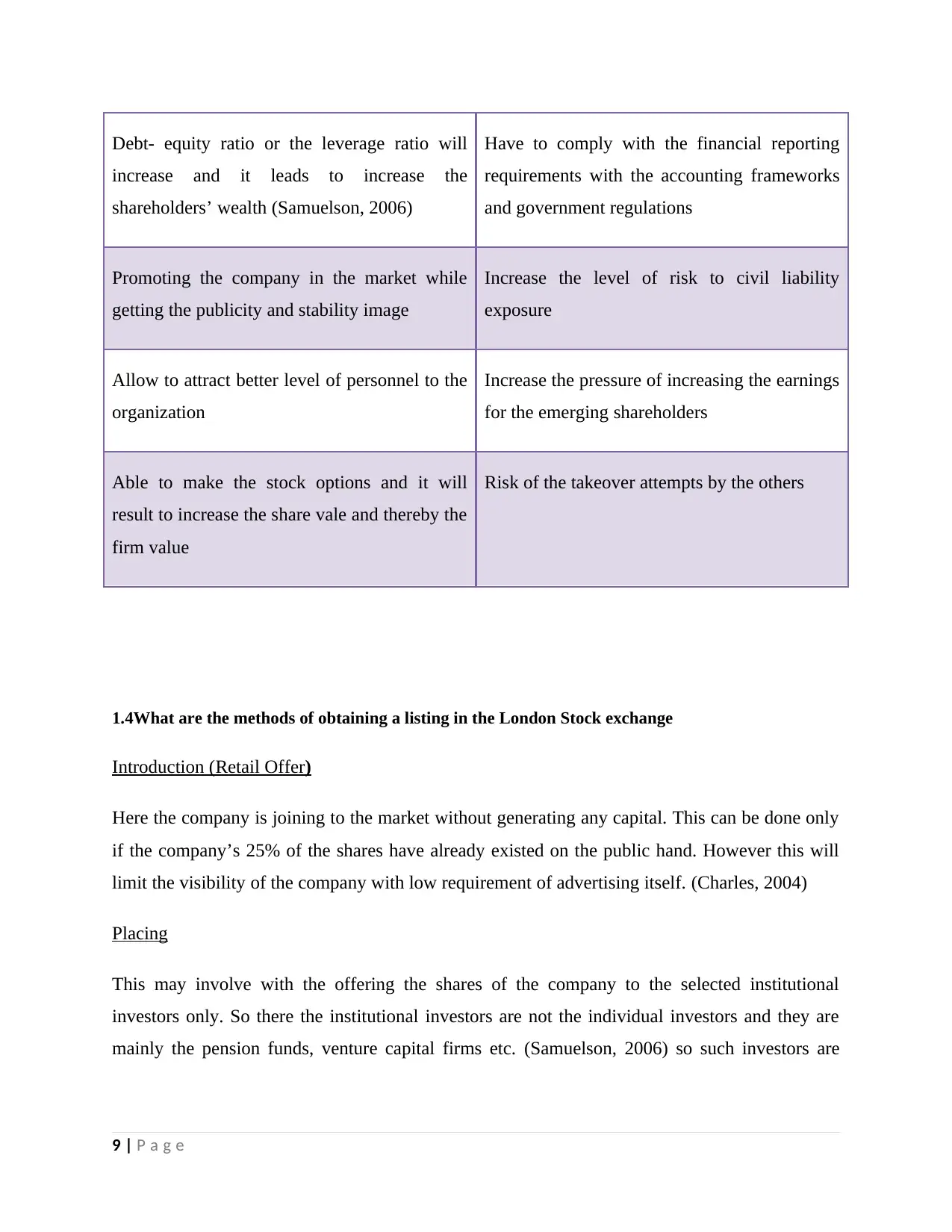

Debt- equity ratio or the leverage ratio will

increase and it leads to increase the

shareholders’ wealth (Samuelson, 2006)

Have to comply with the financial reporting

requirements with the accounting frameworks

and government regulations

Promoting the company in the market while

getting the publicity and stability image

Increase the level of risk to civil liability

exposure

Allow to attract better level of personnel to the

organization

Increase the pressure of increasing the earnings

for the emerging shareholders

Able to make the stock options and it will

result to increase the share vale and thereby the

firm value

Risk of the takeover attempts by the others

1.4What are the methods of obtaining a listing in the London Stock exchange

Introduction (Retail Offer)

Here the company is joining to the market without generating any capital. This can be done only

if the company’s 25% of the shares have already existed on the public hand. However this will

limit the visibility of the company with low requirement of advertising itself. (Charles, 2004)

Placing

This may involve with the offering the shares of the company to the selected institutional

investors only. So there the institutional investors are not the individual investors and they are

mainly the pension funds, venture capital firms etc. (Samuelson, 2006) so such investors are

9 | P a g e

increase and it leads to increase the

shareholders’ wealth (Samuelson, 2006)

Have to comply with the financial reporting

requirements with the accounting frameworks

and government regulations

Promoting the company in the market while

getting the publicity and stability image

Increase the level of risk to civil liability

exposure

Allow to attract better level of personnel to the

organization

Increase the pressure of increasing the earnings

for the emerging shareholders

Able to make the stock options and it will

result to increase the share vale and thereby the

firm value

Risk of the takeover attempts by the others

1.4What are the methods of obtaining a listing in the London Stock exchange

Introduction (Retail Offer)

Here the company is joining to the market without generating any capital. This can be done only

if the company’s 25% of the shares have already existed on the public hand. However this will

limit the visibility of the company with low requirement of advertising itself. (Charles, 2004)

Placing

This may involve with the offering the shares of the company to the selected institutional

investors only. So there the institutional investors are not the individual investors and they are

mainly the pension funds, venture capital firms etc. (Samuelson, 2006) so such investors are

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

having high level of influence to the performance of the company in the future as well. However

this leads to narrow the shareholder base with lower liquidity needs. (Shapiro, 2008)

Initial public offering (IPO)-(Offer to Intermediaries)

This is the first time of offering the shares to the public and with the underwritten as well.

However this is more expensive route, but it can raise substantial amount of capital for the

Milner chemicals as well. Here the company is capable of enhancing their capital as expected

manner and expected amount as there the company will have direct cash flow itself. However

there are some associated huge costs with the brokerage fees and the legal proceedings of the

entire process if IPO as well. (Crockford, 2006)

1.5What are the methods of raising capital in the London Stock Exchange

There are some methods of raising the capital in the London Stock Exchange as follows;

Issue the equity securities as an IPO or secondary issue

Issue the depository receipts

Issue the debt securities like bonds. (Samuelson, 2006)

Here the company is capable of issuing their ordinary shares as an initial public offering or

secondary offering within the market in order to raise the expected capital form the market. On

the other hand the company is possible to issue some kind of depository receipts like the

commercial papers within the market in order to gather the money from the public to expand

their business furthermore. But here the company should have to consider about their future

obligations with repayment of the capital and interest portion for the debt holders or the security

holders itself. And finally the company is also possible to raise their required capital from the

debt securities in the market like mortgages, treasury bonds, government bonds etc. And also

here the company should have to evaluate their life cycle and place they are n currently, because

the debt financing is suitable for the growing or maturity level firm and unless otherwise it would

better to go for equity fiancé with the existing shareholders of the company and the operational

leverage with lower level of debt or no debts within the capital structure of the company.

Likewise the Milner Plc is capable of going for any method of raising funds from the London

10 | P a g e

this leads to narrow the shareholder base with lower liquidity needs. (Shapiro, 2008)

Initial public offering (IPO)-(Offer to Intermediaries)

This is the first time of offering the shares to the public and with the underwritten as well.

However this is more expensive route, but it can raise substantial amount of capital for the

Milner chemicals as well. Here the company is capable of enhancing their capital as expected

manner and expected amount as there the company will have direct cash flow itself. However

there are some associated huge costs with the brokerage fees and the legal proceedings of the

entire process if IPO as well. (Crockford, 2006)

1.5What are the methods of raising capital in the London Stock Exchange

There are some methods of raising the capital in the London Stock Exchange as follows;

Issue the equity securities as an IPO or secondary issue

Issue the depository receipts

Issue the debt securities like bonds. (Samuelson, 2006)

Here the company is capable of issuing their ordinary shares as an initial public offering or

secondary offering within the market in order to raise the expected capital form the market. On

the other hand the company is possible to issue some kind of depository receipts like the

commercial papers within the market in order to gather the money from the public to expand

their business furthermore. But here the company should have to consider about their future

obligations with repayment of the capital and interest portion for the debt holders or the security

holders itself. And finally the company is also possible to raise their required capital from the

debt securities in the market like mortgages, treasury bonds, government bonds etc. And also

here the company should have to evaluate their life cycle and place they are n currently, because

the debt financing is suitable for the growing or maturity level firm and unless otherwise it would

better to go for equity fiancé with the existing shareholders of the company and the operational

leverage with lower level of debt or no debts within the capital structure of the company.

Likewise the Milner Plc is capable of going for any method of raising funds from the London

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stock Exchange according to their main capital requirements and the main goal of expanding its

business furthermore. (Berezin, M., 2005)

Task 02

2.1 Cost of Shares & Debt

2.1 (a) Cost of Ordinary Share Capital

Calculation of cost of equity share capital: it is calculated via Expected dividend/ current market price of

the share+ growth rate of shares. Here, company paid dividend 10p which is going to grow by 8% in the

next year. So the expected dividend= 10+8%= £0.108, and the value of the current ordinary share was

£2. so the cost of equity would be:

.108/ £2+8%*100 = 5.832%

2.1 (b) Cost of Preference share capital

Cost of preference shares shall be calculated as: dividend or return on preference shares/ price of the

preference shares. Here,

Dividend on preference shares was 12% on value on the preference shares. i.e 1.2*12%= 0.144 would be

the dividend amount. Market price of the shares is £1.2. hence, cost of preference shares =

0.144/1.2*100= 12%

2.1 (c) cost of debenture capital after tax

Company’s cost of debenture is calculated as: interest rate*(1-tax rate)/market price of debenture.

Here, the data has been provided that the tax rate is 20% and market price of debenture is £120 and

10% interest rate is given. so it is easy to calculate the cost of debenture by putting the values in the

formula:

10(1-0.20)/120*100= 6.67%

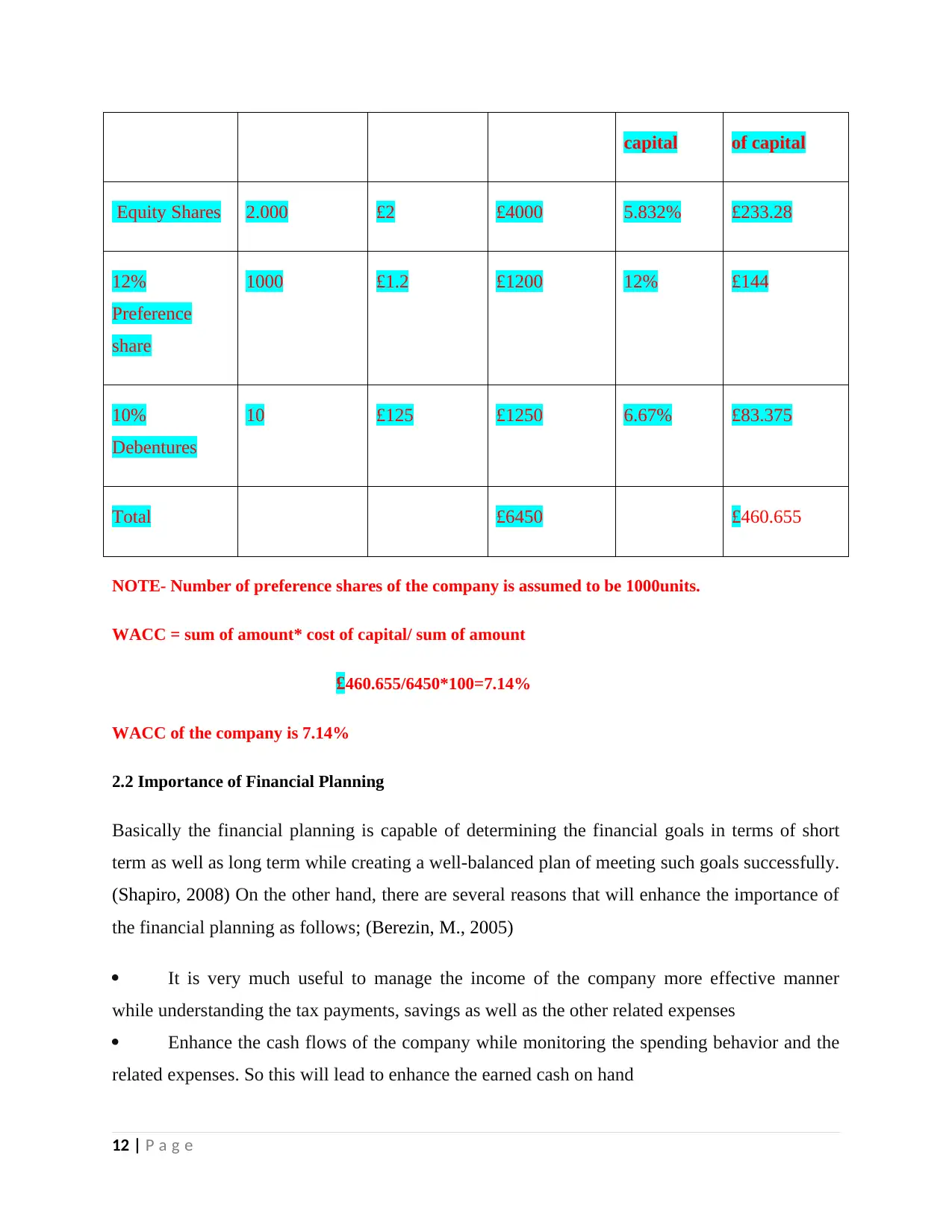

2.1 (d) Calculating the Weighted Average Cost of Capital (WACC) as per market value

(£000)

Sources quantitiy price Amount Cost of Amount*cost

11 | P a g e

business furthermore. (Berezin, M., 2005)

Task 02

2.1 Cost of Shares & Debt

2.1 (a) Cost of Ordinary Share Capital

Calculation of cost of equity share capital: it is calculated via Expected dividend/ current market price of

the share+ growth rate of shares. Here, company paid dividend 10p which is going to grow by 8% in the

next year. So the expected dividend= 10+8%= £0.108, and the value of the current ordinary share was

£2. so the cost of equity would be:

.108/ £2+8%*100 = 5.832%

2.1 (b) Cost of Preference share capital

Cost of preference shares shall be calculated as: dividend or return on preference shares/ price of the

preference shares. Here,

Dividend on preference shares was 12% on value on the preference shares. i.e 1.2*12%= 0.144 would be

the dividend amount. Market price of the shares is £1.2. hence, cost of preference shares =

0.144/1.2*100= 12%

2.1 (c) cost of debenture capital after tax

Company’s cost of debenture is calculated as: interest rate*(1-tax rate)/market price of debenture.

Here, the data has been provided that the tax rate is 20% and market price of debenture is £120 and

10% interest rate is given. so it is easy to calculate the cost of debenture by putting the values in the

formula:

10(1-0.20)/120*100= 6.67%

2.1 (d) Calculating the Weighted Average Cost of Capital (WACC) as per market value

(£000)

Sources quantitiy price Amount Cost of Amount*cost

11 | P a g e

capital of capital

Equity Shares 2.000 £2 £4000 5.832% £233.28

12%

Preference

share

1000 £1.2 £1200 12% £144

10%

Debentures

10 £125 £1250 6.67% £83.375

Total £6450 £460.655

NOTE- Number of preference shares of the company is assumed to be 1000units.

WACC = sum of amount* cost of capital/ sum of amount

£460.655/6450*100=7.14%

WACC of the company is 7.14%

2.2 Importance of Financial Planning

Basically the financial planning is capable of determining the financial goals in terms of short

term as well as long term while creating a well-balanced plan of meeting such goals successfully.

(Shapiro, 2008) On the other hand, there are several reasons that will enhance the importance of

the financial planning as follows; (Berezin, M., 2005)

It is very much useful to manage the income of the company more effective manner

while understanding the tax payments, savings as well as the other related expenses

Enhance the cash flows of the company while monitoring the spending behavior and the

related expenses. So this will lead to enhance the earned cash on hand

12 | P a g e

Equity Shares 2.000 £2 £4000 5.832% £233.28

12%

Preference

share

1000 £1.2 £1200 12% £144

10%

Debentures

10 £125 £1250 6.67% £83.375

Total £6450 £460.655

NOTE- Number of preference shares of the company is assumed to be 1000units.

WACC = sum of amount* cost of capital/ sum of amount

£460.655/6450*100=7.14%

WACC of the company is 7.14%

2.2 Importance of Financial Planning

Basically the financial planning is capable of determining the financial goals in terms of short

term as well as long term while creating a well-balanced plan of meeting such goals successfully.

(Shapiro, 2008) On the other hand, there are several reasons that will enhance the importance of

the financial planning as follows; (Berezin, M., 2005)

It is very much useful to manage the income of the company more effective manner

while understanding the tax payments, savings as well as the other related expenses

Enhance the cash flows of the company while monitoring the spending behavior and the

related expenses. So this will lead to enhance the earned cash on hand

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.