Management Accounting & Budgeting: A Case Study of Smart Looks Ltd

VerifiedAdded on 2023/04/04

|22

|4424

|319

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Smart Looks Limited, covering cost classification (variable, fixed, semi-variable), budgeting methods (zero-based, flexible, fixed), and inventory management techniques (LIFO, FIFO, weighted average). It calculates total and per-unit costs at different production levels, presents a cost of goods sold report, and uses graphical representations to interpret cost behaviors. The report also discusses the use of key performance indicators (KPIs) for assessing business performance, including balanced scorecards, quality metrics, and sales turnover, and proposes strategies for cost control and quality improvement within the company. The analysis aims to provide insights into effective financial management and operational efficiency for Smart Looks Limited.

MANAGEMENT

ACCOUNTING COSTING

AND BUDGETING

1

ACCOUNTING COSTING

AND BUDGETING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INTRODUCTION

The accounting process under which financial data are recorded, analysed and reviewed

by the managers of the company able to take internal business decisions is known as

management accounting. It considers in the business entity for manage the overall financials as

well as forecast for the upcoming times. In the current report Smart Looks Limited company is to

be taken into account for analsye and explain different concepts of the management accounting.

In this report, different kinds of costs are to be classified as per their criteria of segregation.

Different kinds of budgets like as sales, production, cash, overhead etc. are prepared and

reviewed here for the Smart Looks firm. In addition to this, at the current study there are

different kinds of budgeting methods such as zero based, flexible and fixed are to be explained

which supports to frame the budget statements. Moreover costs such as variable, fixed and semi

variable are analysed and after adding such all cost of total production and units expenses both

determined.

TASK 1

1.1 (A) Differentiate the costs and expenses

Variable cost and expenses Semi-variable cost and

expenditures

Fixed cost of production

Power for sewing machine

(level of power and

electricity changes as per the

units of production)

Deliver delivers pay

(In some situation cost of

deliver is fixed but due to

enhancing production by

high level then gets fluctuate

(Kaplan and Atkinson,

2015).)

Factory rent

(As per the signed agreements

between land lord and Smart

Looks rent of factory fixed)

Material for clothes

(when more number of cloths

produce then fabric and raw

materials also require in

more

quantity)

Factory heating

(Up to some extent heating

and fuel cost is fixed but

because of increasing

production at the higher level

then change)

Factory supervisor wages

(As per the signed contract

wages and salary fixed)

Packaging material Telephone charges (basic Office rates

3

The accounting process under which financial data are recorded, analysed and reviewed

by the managers of the company able to take internal business decisions is known as

management accounting. It considers in the business entity for manage the overall financials as

well as forecast for the upcoming times. In the current report Smart Looks Limited company is to

be taken into account for analsye and explain different concepts of the management accounting.

In this report, different kinds of costs are to be classified as per their criteria of segregation.

Different kinds of budgets like as sales, production, cash, overhead etc. are prepared and

reviewed here for the Smart Looks firm. In addition to this, at the current study there are

different kinds of budgeting methods such as zero based, flexible and fixed are to be explained

which supports to frame the budget statements. Moreover costs such as variable, fixed and semi

variable are analysed and after adding such all cost of total production and units expenses both

determined.

TASK 1

1.1 (A) Differentiate the costs and expenses

Variable cost and expenses Semi-variable cost and

expenditures

Fixed cost of production

Power for sewing machine

(level of power and

electricity changes as per the

units of production)

Deliver delivers pay

(In some situation cost of

deliver is fixed but due to

enhancing production by

high level then gets fluctuate

(Kaplan and Atkinson,

2015).)

Factory rent

(As per the signed agreements

between land lord and Smart

Looks rent of factory fixed)

Material for clothes

(when more number of cloths

produce then fabric and raw

materials also require in

more

quantity)

Factory heating

(Up to some extent heating

and fuel cost is fixed but

because of increasing

production at the higher level

then change)

Factory supervisor wages

(As per the signed contract

wages and salary fixed)

Packaging material Telephone charges (basic Office rates

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Higher the number of cloths

lead to increase costs of

packaging and fewer units

incur low cost of packaging

the products)

cost and bills of the

telephone are fixed for each

month but as higher and

lower consuming lead to

increase and decline

respectively (Islam and Hu,

2012).)

(It is not related to the

production level and due to

this it remains same and not

varied)

1.1 (B) Other methods to segregate costs of the production

In the above section there are costs are to be segregated in basically three concepts which

are such fixed, variable as well as semi-variable expenses. Apart from this all there are other

ways on the basis of total expenses associated in the Smart Looks Limited. Varieties of the other

costs as well as expenses on the basis of which number of expenditures are classified are like as

prime costs, opportunity costs, sunk costs, conversion expenses etc. Furthermore, by considering

the direct as well as indirect costs and overheads expenses also total costs are classified at the

workplace. In addition to this, among the overheads also there are different expense comes which

are such as manufacturing, fixed as well as variable overheads (Hammad, Jusoh and Yen Nee

Oon, 2010).

1.2 Calculating the total expenses along with the unit cost

At the current task there are different kinds and varieties of costs comes under the

production and manufacturing process. After adding all types of expenses the company able to

assess the total cost of products which are stitched and manufactured in the firm of Smart Looks

Limited. Further, after consider the total cost as well as level of outputs the managers able to

assess cost and expense of every unit. Moreover, total and unit expenditure of the firm are stated

as below:

4

lead to increase costs of

packaging and fewer units

incur low cost of packaging

the products)

cost and bills of the

telephone are fixed for each

month but as higher and

lower consuming lead to

increase and decline

respectively (Islam and Hu,

2012).)

(It is not related to the

production level and due to

this it remains same and not

varied)

1.1 (B) Other methods to segregate costs of the production

In the above section there are costs are to be segregated in basically three concepts which

are such fixed, variable as well as semi-variable expenses. Apart from this all there are other

ways on the basis of total expenses associated in the Smart Looks Limited. Varieties of the other

costs as well as expenses on the basis of which number of expenditures are classified are like as

prime costs, opportunity costs, sunk costs, conversion expenses etc. Furthermore, by considering

the direct as well as indirect costs and overheads expenses also total costs are classified at the

workplace. In addition to this, among the overheads also there are different expense comes which

are such as manufacturing, fixed as well as variable overheads (Hammad, Jusoh and Yen Nee

Oon, 2010).

1.2 Calculating the total expenses along with the unit cost

At the current task there are different kinds and varieties of costs comes under the

production and manufacturing process. After adding all types of expenses the company able to

assess the total cost of products which are stitched and manufactured in the firm of Smart Looks

Limited. Further, after consider the total cost as well as level of outputs the managers able to

assess cost and expense of every unit. Moreover, total and unit expenditure of the firm are stated

as below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

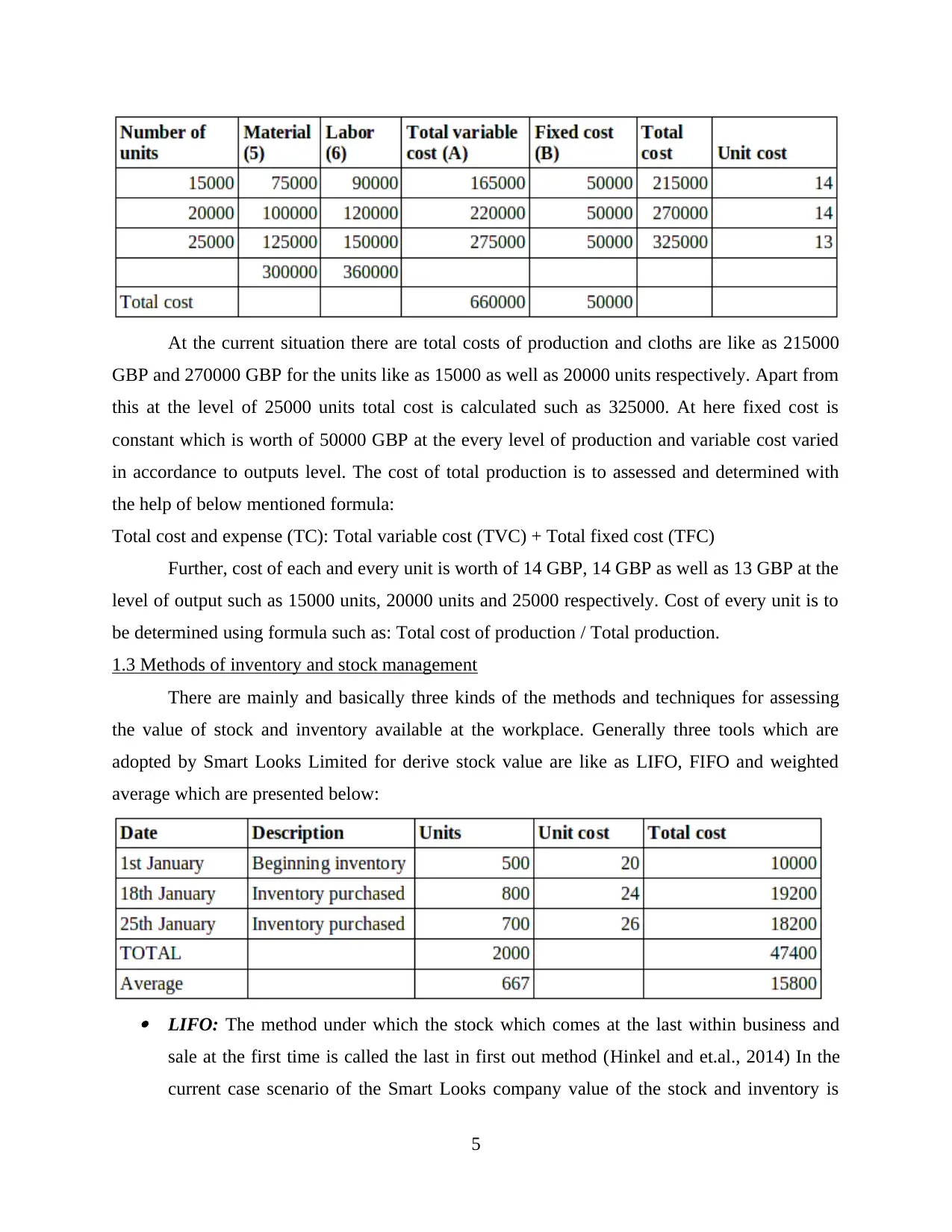

At the current situation there are total costs of production and cloths are like as 215000

GBP and 270000 GBP for the units like as 15000 as well as 20000 units respectively. Apart from

this at the level of 25000 units total cost is calculated such as 325000. At here fixed cost is

constant which is worth of 50000 GBP at the every level of production and variable cost varied

in accordance to outputs level. The cost of total production is to assessed and determined with

the help of below mentioned formula:

Total cost and expense (TC): Total variable cost (TVC) + Total fixed cost (TFC)

Further, cost of each and every unit is worth of 14 GBP, 14 GBP as well as 13 GBP at the

level of output such as 15000 units, 20000 units and 25000 respectively. Cost of every unit is to

be determined using formula such as: Total cost of production / Total production.

1.3 Methods of inventory and stock management

There are mainly and basically three kinds of the methods and techniques for assessing

the value of stock and inventory available at the workplace. Generally three tools which are

adopted by Smart Looks Limited for derive stock value are like as LIFO, FIFO and weighted

average which are presented below:

LIFO: The method under which the stock which comes at the last within business and

sale at the first time is called the last in first out method (Hinkel and et.al., 2014) In the

current case scenario of the Smart Looks company value of the stock and inventory is

5

GBP and 270000 GBP for the units like as 15000 as well as 20000 units respectively. Apart from

this at the level of 25000 units total cost is calculated such as 325000. At here fixed cost is

constant which is worth of 50000 GBP at the every level of production and variable cost varied

in accordance to outputs level. The cost of total production is to assessed and determined with

the help of below mentioned formula:

Total cost and expense (TC): Total variable cost (TVC) + Total fixed cost (TFC)

Further, cost of each and every unit is worth of 14 GBP, 14 GBP as well as 13 GBP at the

level of output such as 15000 units, 20000 units and 25000 respectively. Cost of every unit is to

be determined using formula such as: Total cost of production / Total production.

1.3 Methods of inventory and stock management

There are mainly and basically three kinds of the methods and techniques for assessing

the value of stock and inventory available at the workplace. Generally three tools which are

adopted by Smart Looks Limited for derive stock value are like as LIFO, FIFO and weighted

average which are presented below:

LIFO: The method under which the stock which comes at the last within business and

sale at the first time is called the last in first out method (Hinkel and et.al., 2014) In the

current case scenario of the Smart Looks company value of the stock and inventory is

5

worth of 10000 GBP as well as 19200 GBP which is for the units of 500 and 800

respectively. On the basis of current stock valuation technique the business able to

determine effectual and proper value and takes the business decisions in the proper way.

Further, old and higher inventory lead to reduce productivity and liquidity of the firm due

to which LIFO method is better. FIFO: Another method for valuing the level of inventory and stock is such as first in first

out under which beginning stock is to be sold at the earlier and preference to the new and

current inventory is to be given (Clinton and White, 2012). At this technique stock value

of the Smart Looks company is such as 18200 GBP which is lower as compare to above

mentioned method. Higher the value of stock is better and due to which cause the above

discussed method is more effectual. Apart from this, after adopting the existing stock

valuation way the company able cannot sale the old stock which lead to decrease its

efficiency for generating revenue in the textile industry.

Weighted Average: Combination as well as mixture of LIFO and FIFO both the methods

is known as weighted average technique where the firm can assess average value of the

overall stock (Eichfelder and Schorn, 2012). In the business entity Smart Looks average

value of the available stock comes worth of 15800 GBP which is lower from both the

tools. Hence, due to this overall stock valuation fall down this is not good for the firm as

compare to others. At this level of the stock value average production units are such as

667 units at the end of the financial year.

1.4 Analyse as well as interpret the costs using graphical representation

In the Smart Looks firm there are variable as well as fixed both kinds of costs associated

under stitching and producing cloths. After adding such both expenses total cost is to be

determined which shows and presented using the graphs stated below:

Total variable costs:

6

respectively. On the basis of current stock valuation technique the business able to

determine effectual and proper value and takes the business decisions in the proper way.

Further, old and higher inventory lead to reduce productivity and liquidity of the firm due

to which LIFO method is better. FIFO: Another method for valuing the level of inventory and stock is such as first in first

out under which beginning stock is to be sold at the earlier and preference to the new and

current inventory is to be given (Clinton and White, 2012). At this technique stock value

of the Smart Looks company is such as 18200 GBP which is lower as compare to above

mentioned method. Higher the value of stock is better and due to which cause the above

discussed method is more effectual. Apart from this, after adopting the existing stock

valuation way the company able cannot sale the old stock which lead to decrease its

efficiency for generating revenue in the textile industry.

Weighted Average: Combination as well as mixture of LIFO and FIFO both the methods

is known as weighted average technique where the firm can assess average value of the

overall stock (Eichfelder and Schorn, 2012). In the business entity Smart Looks average

value of the available stock comes worth of 15800 GBP which is lower from both the

tools. Hence, due to this overall stock valuation fall down this is not good for the firm as

compare to others. At this level of the stock value average production units are such as

667 units at the end of the financial year.

1.4 Analyse as well as interpret the costs using graphical representation

In the Smart Looks firm there are variable as well as fixed both kinds of costs associated

under stitching and producing cloths. After adding such both expenses total cost is to be

determined which shows and presented using the graphs stated below:

Total variable costs:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

165000

220000

275000

In the firm cost of variable improves as level of production which is such as 165000

GBP, 220000 GBP and 275000 GBP for the cloth units like 15000, 20000 and 25000 units

respectively.

Fixed costs:

15000 20000 25000

0

10000

20000

30000

40000

50000

60000

50000 50000 50000

The cost which always remains same as well as constant even number of the cloths

changes and increase or decline is called as fixed expense. At this such kind of expenditure is

such as 50000 GBP.

Total cost of production:

7

0

50000

100000

150000

200000

250000

300000

165000

220000

275000

In the firm cost of variable improves as level of production which is such as 165000

GBP, 220000 GBP and 275000 GBP for the cloth units like 15000, 20000 and 25000 units

respectively.

Fixed costs:

15000 20000 25000

0

10000

20000

30000

40000

50000

60000

50000 50000 50000

The cost which always remains same as well as constant even number of the cloths

changes and increase or decline is called as fixed expense. At this such kind of expenditure is

such as 50000 GBP.

Total cost of production:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

Graphical representation of all costs:

1 2 3

0

50000

100000

150000

200000

250000

300000

350000

Total variable cost (A)

Fixed cost (B)

Total cost

On the basis of the above graphs it can be analysed that total cost of production is

different at the various level of production. The graph clearly states that as level of the output

enhances then total cost also give response in same direction (Otley, 2016). Here when the

production is at the 15000 units then total expense is worth of 215000 GBP and by increasing

number of cloth up to 20000 units then expenditures as well which are up to 270000 GBP. Apart

from this, at the level of production improves from 20000 to 25000 then the cost is worth of

325000 GBP. Hence, it has been reflected that as Smart Looks produce and manufacture more

units of cloth then total expenditures also improves.

8

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

Graphical representation of all costs:

1 2 3

0

50000

100000

150000

200000

250000

300000

350000

Total variable cost (A)

Fixed cost (B)

Total cost

On the basis of the above graphs it can be analysed that total cost of production is

different at the various level of production. The graph clearly states that as level of the output

enhances then total cost also give response in same direction (Otley, 2016). Here when the

production is at the 15000 units then total expense is worth of 215000 GBP and by increasing

number of cloth up to 20000 units then expenditures as well which are up to 270000 GBP. Apart

from this, at the level of production improves from 20000 to 25000 then the cost is worth of

325000 GBP. Hence, it has been reflected that as Smart Looks produce and manufacture more

units of cloth then total expenditures also improves.

8

TASK 2

2.1 Report to the management of Smart Looks for the cost of goods sold

To,

Board of Director,

Smart Looks Limited,

Date: 28th April 2017.

In the company such as Smart Looks Limited there are several kinds of costs and

expenses comes which are like as variable, fixed semi-variable etc. Further cost which

associated for selling the cloths are provided In the below stated table:

Particulars Number of units Cost of each unit Total expenses

Inventory at the

beginning

500 20 10000

First purchase 800 24 19200

Second purchase 700 26 18200

Total goods and units

available for sale

2000 70 47400

Less: Inventory at the

end (500+800+7000-

1400)

600 26 (15600)

COGS 1400 44 61600

By considering the above table of cost of goods sold it can be said that in the company

there are total units and cloths which are sold at the end are such as 1400 units. At this level of

production units there are cost of each and every product and cloths comes is such as 44 GBP.

In the company total units which are the company going to sale are 2000 units but from it

closing stock is to be subtracted. Hence, the costs which incur at the workplace of Smart Looks

for selling in the market is worth of 61600 GBP which is derived by multiplying two values

such as cost of one unit and total outputs.

9

2.1 Report to the management of Smart Looks for the cost of goods sold

To,

Board of Director,

Smart Looks Limited,

Date: 28th April 2017.

In the company such as Smart Looks Limited there are several kinds of costs and

expenses comes which are like as variable, fixed semi-variable etc. Further cost which

associated for selling the cloths are provided In the below stated table:

Particulars Number of units Cost of each unit Total expenses

Inventory at the

beginning

500 20 10000

First purchase 800 24 19200

Second purchase 700 26 18200

Total goods and units

available for sale

2000 70 47400

Less: Inventory at the

end (500+800+7000-

1400)

600 26 (15600)

COGS 1400 44 61600

By considering the above table of cost of goods sold it can be said that in the company

there are total units and cloths which are sold at the end are such as 1400 units. At this level of

production units there are cost of each and every product and cloths comes is such as 44 GBP.

In the company total units which are the company going to sale are 2000 units but from it

closing stock is to be subtracted. Hence, the costs which incur at the workplace of Smart Looks

for selling in the market is worth of 61600 GBP which is derived by multiplying two values

such as cost of one unit and total outputs.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Use of key performance indicators in order to assess business performance

It is highly compulsory to determine that in which way the company performing in the

industry of clothing and textiles. To assess performance and presentation of the company there

are different kinds of indicators and methods are used by the management. Among all key

performance indicators are the highly useful under which balanced scorecard, quality, sales and

turnover, performance appraisal etc. taken into account. On the basis of the quality if the

company such as Smart Looks enhance and improve level of the quality of cloths then it can be

said that it performs well in the industry (Boyns and Edwards, 2013). The balanced scorecard is

method under which four concepts and aspects are to be reviewed which are highly significant

for the overall firm. Further, main and key concept are like as learning and growth, customers

and buyers, financial performance as well as internal business process perspectives. Apart from

this, when firm found that consumers are more satisfied by consuming its cloths and garments

and increasing level of customer satisfaction reflect that its performance improves in the overall

industry.

2.3 Strategies and method for control costs as well as improve quality of products

In the company controlling and managing cost take one of the most significant place along

with improving level of the quality of fabrics and cloths. For this the management of Smart

Looks company needs to analyse and review the financial statements like as profit and loss

account. By this the firm assess that up to which extent expenses incur at the workplace. Further,

it requires to forecast the financial data using cash and sales budget and on the basis of that

strategies are framed. While talking about the quality aspect then Smart Looks should apply

TQM approach as well as six sigma and lean production (Seal, 2012). From this all, the firm

supportive for reducing the wastage materials and eliminated defective cloth pieces. In this

regards, there are total quality management supports to the managers in order to enhance quality

of the products. Further, six sigma is a concept under which percentage of defective items is such

as 0.06% behind total 100o units. Hence, as improving quality cost reduce and ultimately more

customers attract which is indication of enhancing revenue.

10

It is highly compulsory to determine that in which way the company performing in the

industry of clothing and textiles. To assess performance and presentation of the company there

are different kinds of indicators and methods are used by the management. Among all key

performance indicators are the highly useful under which balanced scorecard, quality, sales and

turnover, performance appraisal etc. taken into account. On the basis of the quality if the

company such as Smart Looks enhance and improve level of the quality of cloths then it can be

said that it performs well in the industry (Boyns and Edwards, 2013). The balanced scorecard is

method under which four concepts and aspects are to be reviewed which are highly significant

for the overall firm. Further, main and key concept are like as learning and growth, customers

and buyers, financial performance as well as internal business process perspectives. Apart from

this, when firm found that consumers are more satisfied by consuming its cloths and garments

and increasing level of customer satisfaction reflect that its performance improves in the overall

industry.

2.3 Strategies and method for control costs as well as improve quality of products

In the company controlling and managing cost take one of the most significant place along

with improving level of the quality of fabrics and cloths. For this the management of Smart

Looks company needs to analyse and review the financial statements like as profit and loss

account. By this the firm assess that up to which extent expenses incur at the workplace. Further,

it requires to forecast the financial data using cash and sales budget and on the basis of that

strategies are framed. While talking about the quality aspect then Smart Looks should apply

TQM approach as well as six sigma and lean production (Seal, 2012). From this all, the firm

supportive for reducing the wastage materials and eliminated defective cloth pieces. In this

regards, there are total quality management supports to the managers in order to enhance quality

of the products. Further, six sigma is a concept under which percentage of defective items is such

as 0.06% behind total 100o units. Hence, as improving quality cost reduce and ultimately more

customers attract which is indication of enhancing revenue.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK3

3.1 Budgets and purpose

Budget is the one of the main statement that is used to make project the cash inflow and

outflow that can take place in the business. There are number of methods that are used to prepare

the budget. It depend on the firm that which approach it find appropriate to prepare the budget.

Budget can be prepared for any time period whether it may be for two to six months. It is very

important to make accurate prediction because if same will be made then only budget can be

prepared accurately. It is possible that wrong prediction can be made by the managers. If same

will be done then in that case wrong values will be predicted and firm will take decision in

wrong direction. Purpose due to which budget is prepared by the most firms is explained below. Use of budget for short term target setting: Budget is the statement that is used to set

short term target for the business. Budget can be prepared for 3 to 9 months’ time period.

In the budget cash inflow and outflow is projected and accordingly for each month step

by step targets can be determined (Callahan, Stetz. and Brooks, 2011). Thus, it can be

said that budget is the one of the main tool that is used to set short term target in the

business. There is a huge significance of the budget for the business firms. Monitoring of firm performance: Monitoring of the firm performance is another main

objective behind preparation of budget. Under this projection is made about cash inflow

and outflow in the business and same is compared time to time with the budgeted values.

By doing so firm performance is monitored on monthly basis. Control function: Control function is also performed by using budget and under this if on

comparison it is identified that actual performance is below projected performance then

in that case corrective action is taken to improve firm performance (Mat, Smith and

Djajadikerta, 2010). It can be said that there is a huge importance of the budget for the

firms. Motivating employees: Employee motivation is another objective for preparation of

budget. In order to achieve overall target for each employee target is determined. Setting

of target motivate employees to achieve something on job. It can be said that budget help

firms in making effective use of its workforce.

11

3.1 Budgets and purpose

Budget is the one of the main statement that is used to make project the cash inflow and

outflow that can take place in the business. There are number of methods that are used to prepare

the budget. It depend on the firm that which approach it find appropriate to prepare the budget.

Budget can be prepared for any time period whether it may be for two to six months. It is very

important to make accurate prediction because if same will be made then only budget can be

prepared accurately. It is possible that wrong prediction can be made by the managers. If same

will be done then in that case wrong values will be predicted and firm will take decision in

wrong direction. Purpose due to which budget is prepared by the most firms is explained below. Use of budget for short term target setting: Budget is the statement that is used to set

short term target for the business. Budget can be prepared for 3 to 9 months’ time period.

In the budget cash inflow and outflow is projected and accordingly for each month step

by step targets can be determined (Callahan, Stetz. and Brooks, 2011). Thus, it can be

said that budget is the one of the main tool that is used to set short term target in the

business. There is a huge significance of the budget for the business firms. Monitoring of firm performance: Monitoring of the firm performance is another main

objective behind preparation of budget. Under this projection is made about cash inflow

and outflow in the business and same is compared time to time with the budgeted values.

By doing so firm performance is monitored on monthly basis. Control function: Control function is also performed by using budget and under this if on

comparison it is identified that actual performance is below projected performance then

in that case corrective action is taken to improve firm performance (Mat, Smith and

Djajadikerta, 2010). It can be said that there is a huge importance of the budget for the

firms. Motivating employees: Employee motivation is another objective for preparation of

budget. In order to achieve overall target for each employee target is determined. Setting

of target motivate employees to achieve something on job. It can be said that budget help

firms in making effective use of its workforce.

11

3.2 Methods for preparing budget

There are number of methods that are used to prepare budget and some of them are

explained below.

Incremental budget: Incremental budget is the one of the budget that is prepared by the

firm in its business. Under incremental budget past month’s budget values are taken in to

consideration percentage is added to past values in order to prepare budget for the

upcoming months. There are some advantages and disadvantage s of this budget. Main

merit of the budget is that with increase in business operations revenue and cost increased

(Lukka and Vinnari, 2014). Thus, incremental budget approach help one in preparing

budget in proper manner. The main disadvantage of budget is that one can make wrong

estimation about percentage increase in income and expenses and due to this reason

budget can be prepared in wrong manner. Zero based budget: Zero base budget is another method that is used to make projection

by the business firms. Under this approach first of all departments prepare budget on their

own level and by considering all department budgets final budget is prepared for an

organization. The main advantage of the zero based budget is that it is prepared in

accurate manner because department managers better knows the expenditure that can be

made by the department in the upcoming time period. Hence, estimation of expenditures

is made by the managers accurately. The disadvantage of zero based budget is that

process is very lightly and time consuming (Hammad, Jusoh. and Yen Nee Oon, 2010). Fixed budget: Fixed budget is another sort of budget that is prepared by the firms in their

business. Under fixed budget fixed values are determined for all months. It can be said

that there is significant importance of the fixed budget for the business firm. This is

because every month expenses cannot be changed at fast pace. Thus, preparation of fixed

budget save lots of time of the business firm. Disadvantage of fixed budget is that in case

business conditions changed at fast pace than in that situation by using fixed budget

accurate decisions cannot be taken by the firm in its business.

3.3 Budget for the business firms

Sales budget: Sales budget is the one of the budget that is used to make projection about

the sales revenue in the business. In order to prepare the sales budget product sales price

12

There are number of methods that are used to prepare budget and some of them are

explained below.

Incremental budget: Incremental budget is the one of the budget that is prepared by the

firm in its business. Under incremental budget past month’s budget values are taken in to

consideration percentage is added to past values in order to prepare budget for the

upcoming months. There are some advantages and disadvantage s of this budget. Main

merit of the budget is that with increase in business operations revenue and cost increased

(Lukka and Vinnari, 2014). Thus, incremental budget approach help one in preparing

budget in proper manner. The main disadvantage of budget is that one can make wrong

estimation about percentage increase in income and expenses and due to this reason

budget can be prepared in wrong manner. Zero based budget: Zero base budget is another method that is used to make projection

by the business firms. Under this approach first of all departments prepare budget on their

own level and by considering all department budgets final budget is prepared for an

organization. The main advantage of the zero based budget is that it is prepared in

accurate manner because department managers better knows the expenditure that can be

made by the department in the upcoming time period. Hence, estimation of expenditures

is made by the managers accurately. The disadvantage of zero based budget is that

process is very lightly and time consuming (Hammad, Jusoh. and Yen Nee Oon, 2010). Fixed budget: Fixed budget is another sort of budget that is prepared by the firms in their

business. Under fixed budget fixed values are determined for all months. It can be said

that there is significant importance of the fixed budget for the business firm. This is

because every month expenses cannot be changed at fast pace. Thus, preparation of fixed

budget save lots of time of the business firm. Disadvantage of fixed budget is that in case

business conditions changed at fast pace than in that situation by using fixed budget

accurate decisions cannot be taken by the firm in its business.

3.3 Budget for the business firms

Sales budget: Sales budget is the one of the budget that is used to make projection about

the sales revenue in the business. In order to prepare the sales budget product sales price

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.