Management Accounting Report: Costing, Budgeting & Analysis

VerifiedAdded on 2023/04/04

|23

|4654

|63

Report

AI Summary

This management accounting report provides a detailed analysis of Smart Looks, a UK-based clothing retailer. It distinguishes various costs incurred by the company, categorizing them as fixed, semi-variable, or variable. The report calculates total and unit costs at different production levels, offering insights into cost behavior. Inventory valuation methods, including FIFO, LIFO, and average cost, are applied to determine the cost of goods sold. The report identifies critical success factors and performance indicators, such as customer experience, supplier relationships, and operational efficiency. Budgeting techniques are explored, including sales, production, raw material, labor, and overhead budgets. A cash budget is prepared and analyzed, and variance analysis is conducted to identify deviations from planned performance. Finally, the report suggests corrective actions for improvement, emphasizing the role of management accounting in enhancing the firm's growth and profitability. Desklib provides access to similar reports and study tools for students.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................................4

Question 1...............................................................................................................................................4

a. Distinguishing various costs incurred by Smart looks..........................................................................4

b. Presenting different types of cost related to clothing retail firm.........................................................4

Q.2...........................................................................................................................................................6

(A) Calculation of total cost (TC) and unit cost (UC).................................................................................6

(B) Cost data analysis...............................................................................................................................7

Q.3 Inventory valuation...........................................................................................................................8

(1) First-in, first-out.................................................................................................................................8

(2) Last-in, First-out.................................................................................................................................8

(3) Average costs.....................................................................................................................................9

Q.4. Calculation of cost of goods sold under FIFO, LIFO and average cost method...............................10

Question 5.............................................................................................................................................10

A. Identifying critical success factors and performance indicators........................................................10

B............................................................................................................................................................11

1. Identifying the ways through which cost level can be reduced.........................................................11

2. Assessing the manner in which quality can be enhanced..................................................................12

TASK 2........................................................................................................................................................12

Q.6.........................................................................................................................................................12

(A). Meaning of budget..........................................................................................................................12

(B). Purpose or objectives of budgetary planning..................................................................................12

(C) Different methods of budget prearation for Smart Looks................................................................13

Question7..............................................................................................................................................14

a. Sales budget.......................................................................................................................................14

b. Production budget.............................................................................................................................15

c. Raw material budgets........................................................................................................................15

d. Labor budgets....................................................................................................................................15

e. Total overhead budget......................................................................................................................16

Q.8. Preparing cash budget and its analysis..........................................................................................16

INTRODUCTION...........................................................................................................................................4

Question 1...............................................................................................................................................4

a. Distinguishing various costs incurred by Smart looks..........................................................................4

b. Presenting different types of cost related to clothing retail firm.........................................................4

Q.2...........................................................................................................................................................6

(A) Calculation of total cost (TC) and unit cost (UC).................................................................................6

(B) Cost data analysis...............................................................................................................................7

Q.3 Inventory valuation...........................................................................................................................8

(1) First-in, first-out.................................................................................................................................8

(2) Last-in, First-out.................................................................................................................................8

(3) Average costs.....................................................................................................................................9

Q.4. Calculation of cost of goods sold under FIFO, LIFO and average cost method...............................10

Question 5.............................................................................................................................................10

A. Identifying critical success factors and performance indicators........................................................10

B............................................................................................................................................................11

1. Identifying the ways through which cost level can be reduced.........................................................11

2. Assessing the manner in which quality can be enhanced..................................................................12

TASK 2........................................................................................................................................................12

Q.6.........................................................................................................................................................12

(A). Meaning of budget..........................................................................................................................12

(B). Purpose or objectives of budgetary planning..................................................................................12

(C) Different methods of budget prearation for Smart Looks................................................................13

Question7..............................................................................................................................................14

a. Sales budget.......................................................................................................................................14

b. Production budget.............................................................................................................................15

c. Raw material budgets........................................................................................................................15

d. Labor budgets....................................................................................................................................15

e. Total overhead budget......................................................................................................................16

Q.8. Preparing cash budget and its analysis..........................................................................................16

TASK 3........................................................................................................................................................18

Question 9.............................................................................................................................................18

a. Computation of planned margin for March 2017..............................................................................18

b. Calculation of actual profit................................................................................................................18

c. Computation of material and labor variances....................................................................................19

d. Preparing reconciliation profit...........................................................................................................20

Question 10...........................................................................................................................................20

Finding causes of deviations and taking correction actions for improvement.......................................20

CONCLUSION.............................................................................................................................................21

REFERENCES..............................................................................................................................................22

Question 9.............................................................................................................................................18

a. Computation of planned margin for March 2017..............................................................................18

b. Calculation of actual profit................................................................................................................18

c. Computation of material and labor variances....................................................................................19

d. Preparing reconciliation profit...........................................................................................................20

Question 10...........................................................................................................................................20

Finding causes of deviations and taking correction actions for improvement.......................................20

CONCLUSION.............................................................................................................................................21

REFERENCES..............................................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting includes several tools and techniques which in turn help in

preparing suitable reports for decision making. In the present times, each business unit lays

emphasis on employing varied tools for getting information about the extent to which each

business unit is performing in a well manner. Moreover, managerial reporting provides deeper

insight to the firm about the area which requires improvement. Thus, management accounting

system aids in the growth and profitability aspect of firm to a great extent. The present report is

based on Smart Looks which is the clothing retailer of UK. It provides customers with high

quality fashion apparel at affordable prices. In this, report will furnish information regarding the

different types of cost associated with the manufacturing of clothes. Further, it will also provide

understanding about the manner in which suitable plan can be developed in monetary terms.

Besides this, report will help in understanding the manner in which variance analysis technique

helps in taking strategic action for the purpose of improvement.

Question 1

a. Distinguishing various costs incurred by Smart looks

Cited case situation presents that Smart Looks has incurred following expenses which fall

in the category of either fixed, semi-variable or variable. Hence, category of cost incurred is

enumerated below:

Material for clothes: Variable cost

Factory rent: Fixed cost

Power of sewing machines: Semi-variable cost

Telephone expenses: semi-variable cost

Office rates: Fixed cost

Delivery drivers: Semi-variable cost

Factory heating: Variable cost

b. Presenting different types of cost related to clothing retail firm

Cost may be defined as a sum of all the expenses which are incurred by firm to

manufacture clothes. In the business organization, firm has to incur several costs which in turn

Management accounting includes several tools and techniques which in turn help in

preparing suitable reports for decision making. In the present times, each business unit lays

emphasis on employing varied tools for getting information about the extent to which each

business unit is performing in a well manner. Moreover, managerial reporting provides deeper

insight to the firm about the area which requires improvement. Thus, management accounting

system aids in the growth and profitability aspect of firm to a great extent. The present report is

based on Smart Looks which is the clothing retailer of UK. It provides customers with high

quality fashion apparel at affordable prices. In this, report will furnish information regarding the

different types of cost associated with the manufacturing of clothes. Further, it will also provide

understanding about the manner in which suitable plan can be developed in monetary terms.

Besides this, report will help in understanding the manner in which variance analysis technique

helps in taking strategic action for the purpose of improvement.

Question 1

a. Distinguishing various costs incurred by Smart looks

Cited case situation presents that Smart Looks has incurred following expenses which fall

in the category of either fixed, semi-variable or variable. Hence, category of cost incurred is

enumerated below:

Material for clothes: Variable cost

Factory rent: Fixed cost

Power of sewing machines: Semi-variable cost

Telephone expenses: semi-variable cost

Office rates: Fixed cost

Delivery drivers: Semi-variable cost

Factory heating: Variable cost

b. Presenting different types of cost related to clothing retail firm

Cost may be defined as a sum of all the expenses which are incurred by firm to

manufacture clothes. In the business organization, firm has to incur several costs which in turn

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

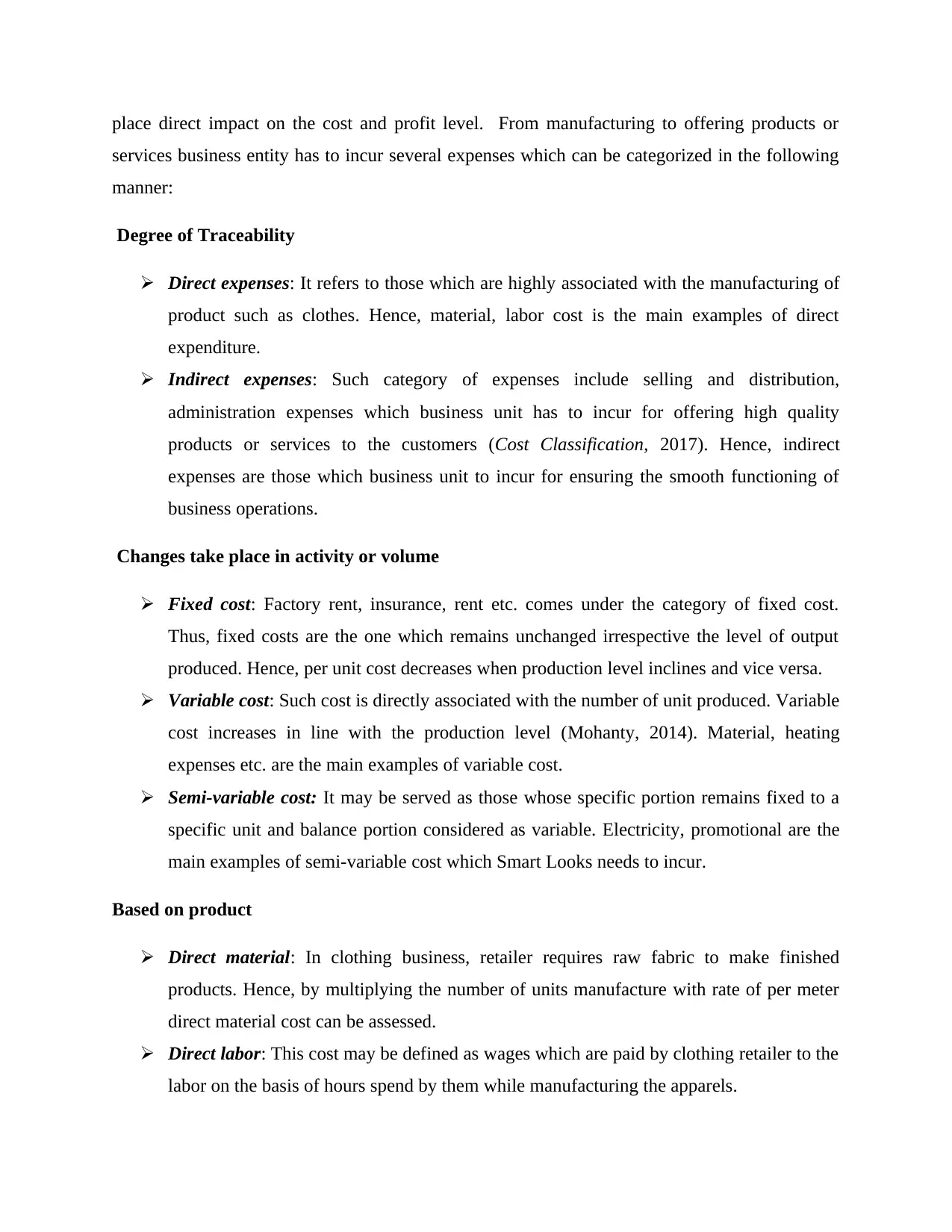

place direct impact on the cost and profit level. From manufacturing to offering products or

services business entity has to incur several expenses which can be categorized in the following

manner:

Degree of Traceability

Direct expenses: It refers to those which are highly associated with the manufacturing of

product such as clothes. Hence, material, labor cost is the main examples of direct

expenditure.

Indirect expenses: Such category of expenses include selling and distribution,

administration expenses which business unit has to incur for offering high quality

products or services to the customers (Cost Classification, 2017). Hence, indirect

expenses are those which business unit to incur for ensuring the smooth functioning of

business operations.

Changes take place in activity or volume

Fixed cost: Factory rent, insurance, rent etc. comes under the category of fixed cost.

Thus, fixed costs are the one which remains unchanged irrespective the level of output

produced. Hence, per unit cost decreases when production level inclines and vice versa.

Variable cost: Such cost is directly associated with the number of unit produced. Variable

cost increases in line with the production level (Mohanty, 2014). Material, heating

expenses etc. are the main examples of variable cost.

Semi-variable cost: It may be served as those whose specific portion remains fixed to a

specific unit and balance portion considered as variable. Electricity, promotional are the

main examples of semi-variable cost which Smart Looks needs to incur.

Based on product

Direct material: In clothing business, retailer requires raw fabric to make finished

products. Hence, by multiplying the number of units manufacture with rate of per meter

direct material cost can be assessed.

Direct labor: This cost may be defined as wages which are paid by clothing retailer to the

labor on the basis of hours spend by them while manufacturing the apparels.

services business entity has to incur several expenses which can be categorized in the following

manner:

Degree of Traceability

Direct expenses: It refers to those which are highly associated with the manufacturing of

product such as clothes. Hence, material, labor cost is the main examples of direct

expenditure.

Indirect expenses: Such category of expenses include selling and distribution,

administration expenses which business unit has to incur for offering high quality

products or services to the customers (Cost Classification, 2017). Hence, indirect

expenses are those which business unit to incur for ensuring the smooth functioning of

business operations.

Changes take place in activity or volume

Fixed cost: Factory rent, insurance, rent etc. comes under the category of fixed cost.

Thus, fixed costs are the one which remains unchanged irrespective the level of output

produced. Hence, per unit cost decreases when production level inclines and vice versa.

Variable cost: Such cost is directly associated with the number of unit produced. Variable

cost increases in line with the production level (Mohanty, 2014). Material, heating

expenses etc. are the main examples of variable cost.

Semi-variable cost: It may be served as those whose specific portion remains fixed to a

specific unit and balance portion considered as variable. Electricity, promotional are the

main examples of semi-variable cost which Smart Looks needs to incur.

Based on product

Direct material: In clothing business, retailer requires raw fabric to make finished

products. Hence, by multiplying the number of units manufacture with rate of per meter

direct material cost can be assessed.

Direct labor: This cost may be defined as wages which are paid by clothing retailer to the

labor on the basis of hours spend by them while manufacturing the apparels.

Overhead cost: Cost which is incurred by Smart Looks other than material and labor is

considered as overhead (Mungal and Garbharran, 2014). Hence, selling, administration

etc. are recognized as overhead cost that is vital for the business organization.

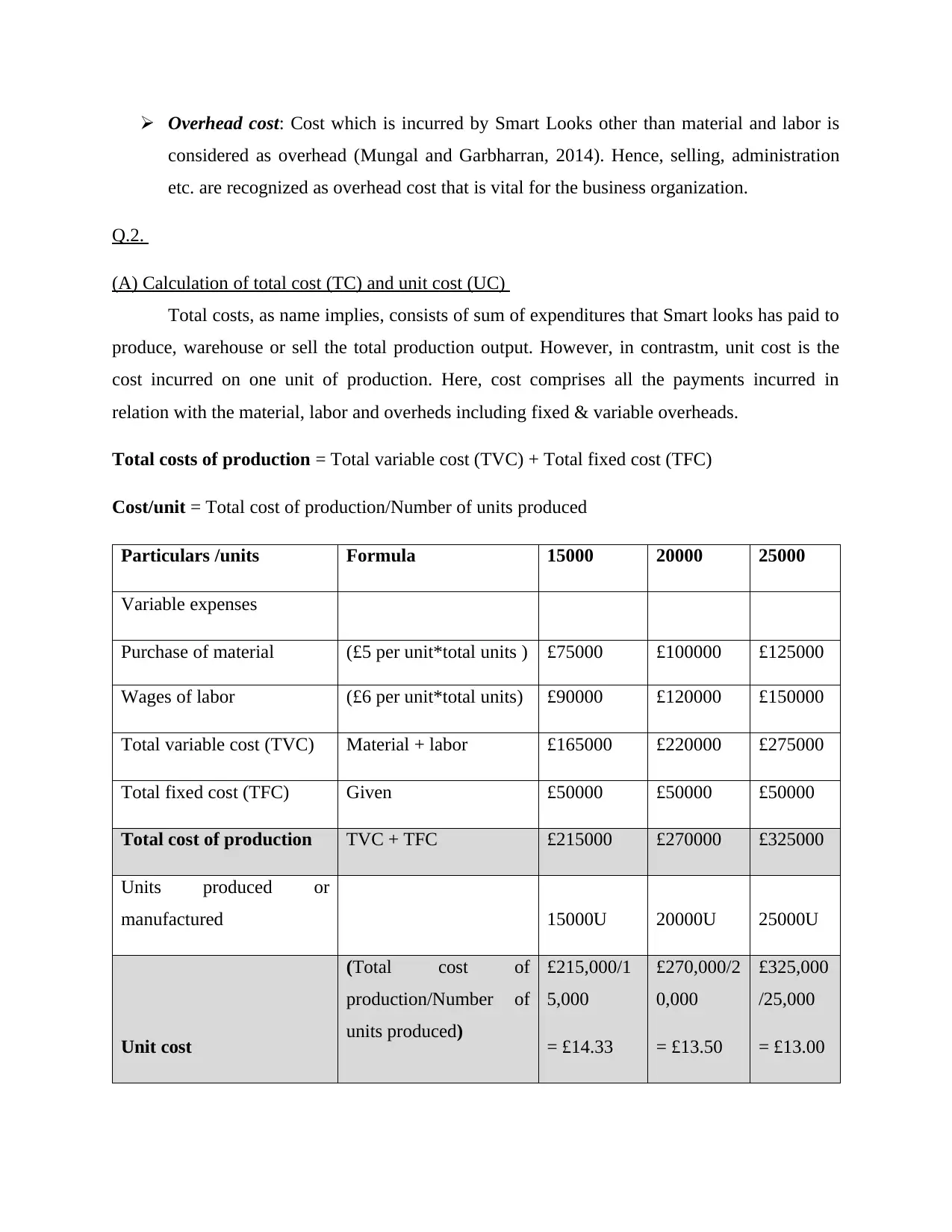

Q.2.

(A) Calculation of total cost (TC) and unit cost (UC)

Total costs, as name implies, consists of sum of expenditures that Smart looks has paid to

produce, warehouse or sell the total production output. However, in contrastm, unit cost is the

cost incurred on one unit of production. Here, cost comprises all the payments incurred in

relation with the material, labor and overheds including fixed & variable overheads.

Total costs of production = Total variable cost (TVC) + Total fixed cost (TFC)

Cost/unit = Total cost of production/Number of units produced

Particulars /units Formula 15000 20000 25000

Variable expenses

Purchase of material (£5 per unit*total units ) £75000 £100000 £125000

Wages of labor (£6 per unit*total units) £90000 £120000 £150000

Total variable cost (TVC) Material + labor £165000 £220000 £275000

Total fixed cost (TFC) Given £50000 £50000 £50000

Total cost of production TVC + TFC £215000 £270000 £325000

Units produced or

manufactured 15000U 20000U 25000U

Unit cost

(Total cost of

production/Number of

units produced)

£215,000/1

5,000

= £14.33

£270,000/2

0,000

= £13.50

£325,000

/25,000

= £13.00

considered as overhead (Mungal and Garbharran, 2014). Hence, selling, administration

etc. are recognized as overhead cost that is vital for the business organization.

Q.2.

(A) Calculation of total cost (TC) and unit cost (UC)

Total costs, as name implies, consists of sum of expenditures that Smart looks has paid to

produce, warehouse or sell the total production output. However, in contrastm, unit cost is the

cost incurred on one unit of production. Here, cost comprises all the payments incurred in

relation with the material, labor and overheds including fixed & variable overheads.

Total costs of production = Total variable cost (TVC) + Total fixed cost (TFC)

Cost/unit = Total cost of production/Number of units produced

Particulars /units Formula 15000 20000 25000

Variable expenses

Purchase of material (£5 per unit*total units ) £75000 £100000 £125000

Wages of labor (£6 per unit*total units) £90000 £120000 £150000

Total variable cost (TVC) Material + labor £165000 £220000 £275000

Total fixed cost (TFC) Given £50000 £50000 £50000

Total cost of production TVC + TFC £215000 £270000 £325000

Units produced or

manufactured 15000U 20000U 25000U

Unit cost

(Total cost of

production/Number of

units produced)

£215,000/1

5,000

= £14.33

£270,000/2

0,000

= £13.50

£325,000

/25,000

= £13.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

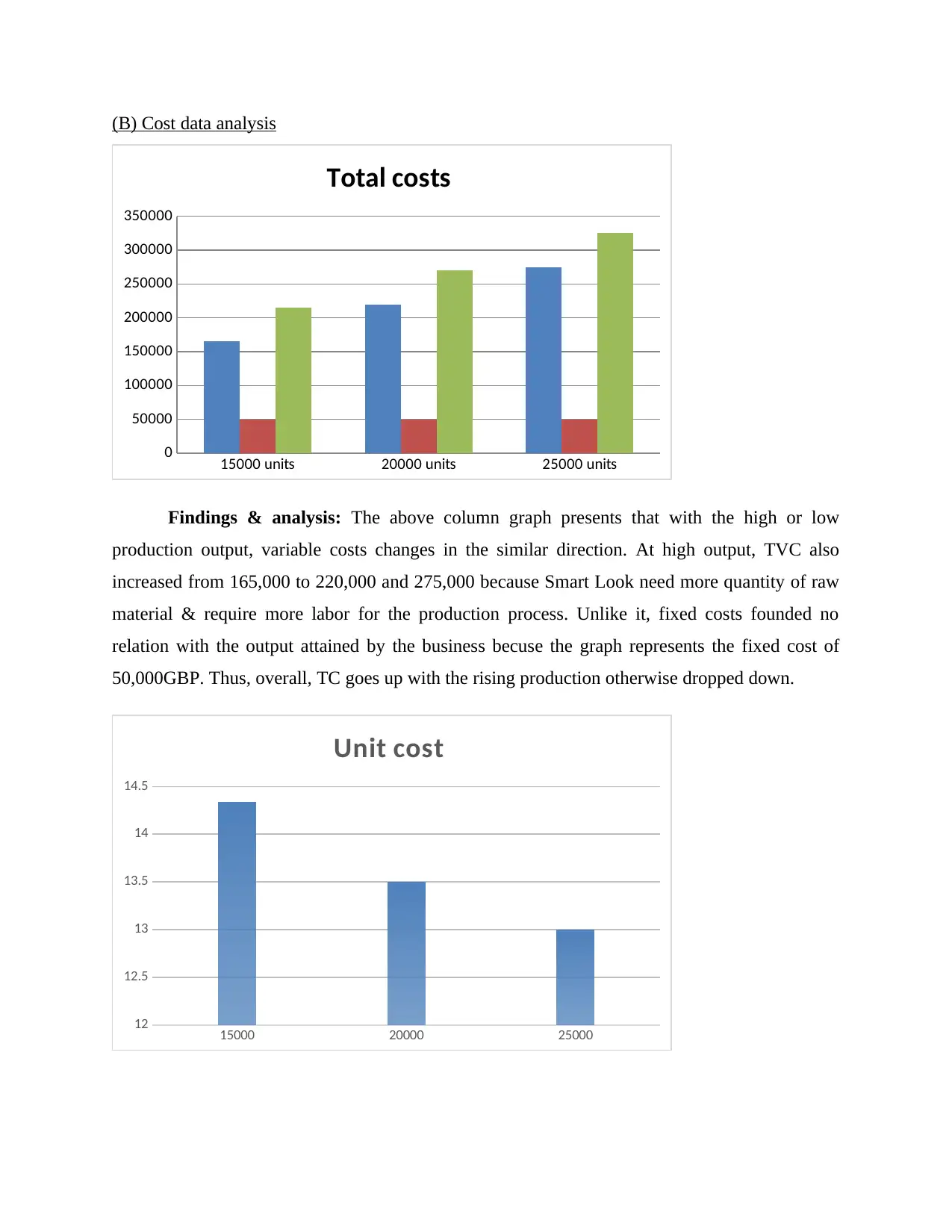

(B) Cost data analysis

15000 units 20000 units 25000 units

0

50000

100000

150000

200000

250000

300000

350000

Total costs

Findings & analysis: The above column graph presents that with the high or low

production output, variable costs changes in the similar direction. At high output, TVC also

increased from 165,000 to 220,000 and 275,000 because Smart Look need more quantity of raw

material & require more labor for the production process. Unlike it, fixed costs founded no

relation with the output attained by the business becuse the graph represents the fixed cost of

50,000GBP. Thus, overall, TC goes up with the rising production otherwise dropped down.

15000 20000 25000

12

12.5

13

13.5

14

14.5

Unit cost

15000 units 20000 units 25000 units

0

50000

100000

150000

200000

250000

300000

350000

Total costs

Findings & analysis: The above column graph presents that with the high or low

production output, variable costs changes in the similar direction. At high output, TVC also

increased from 165,000 to 220,000 and 275,000 because Smart Look need more quantity of raw

material & require more labor for the production process. Unlike it, fixed costs founded no

relation with the output attained by the business becuse the graph represents the fixed cost of

50,000GBP. Thus, overall, TC goes up with the rising production otherwise dropped down.

15000 20000 25000

12

12.5

13

13.5

14

14.5

Unit cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Findings & analysis: Unit costs at 15000 units is figured to 14.33 GBP which came

downward to 13.5 and 13 GBP at 20,000 & 25000 units of output. The reason is that TFC of

50,000 is allocated and spreaded to more number of units which resulted less cost each unit.

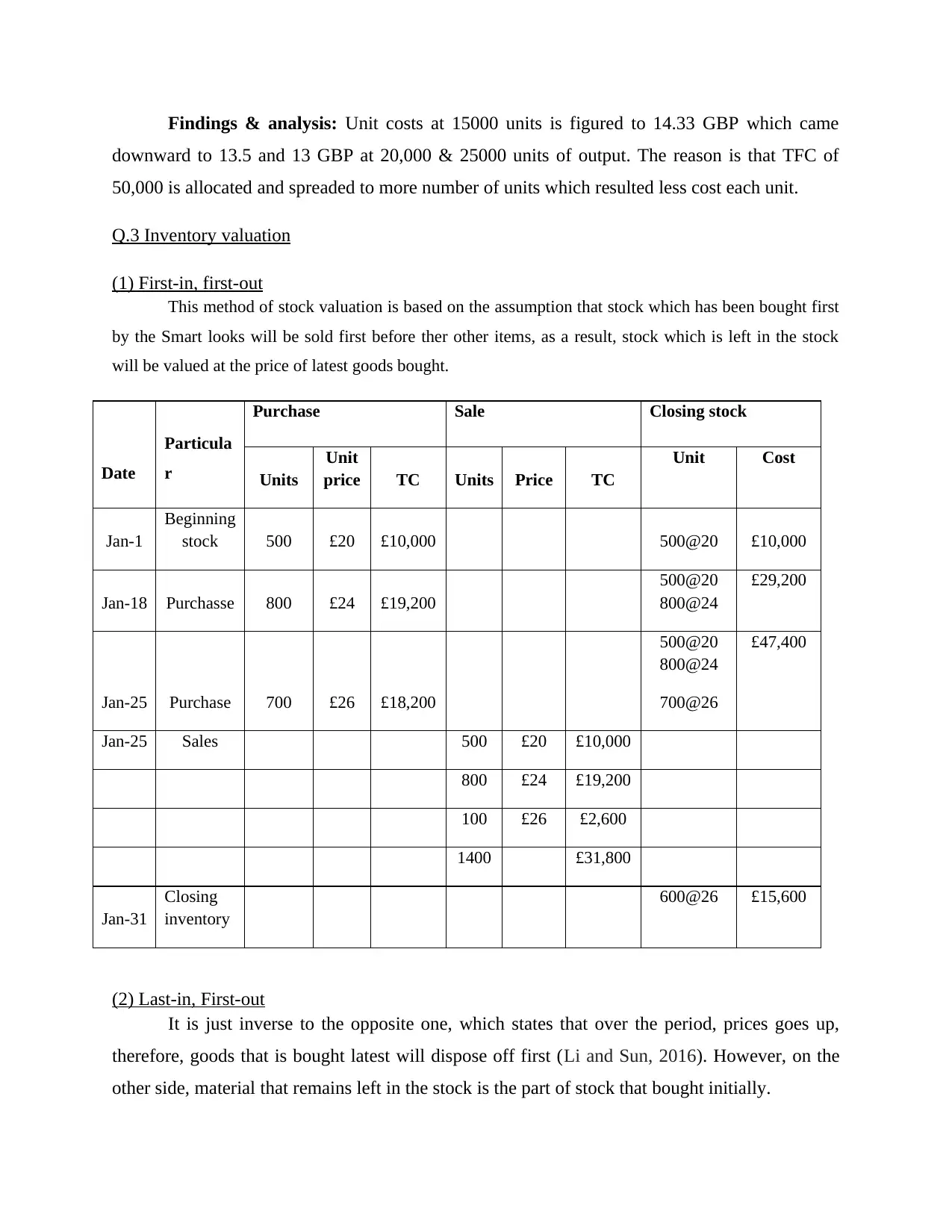

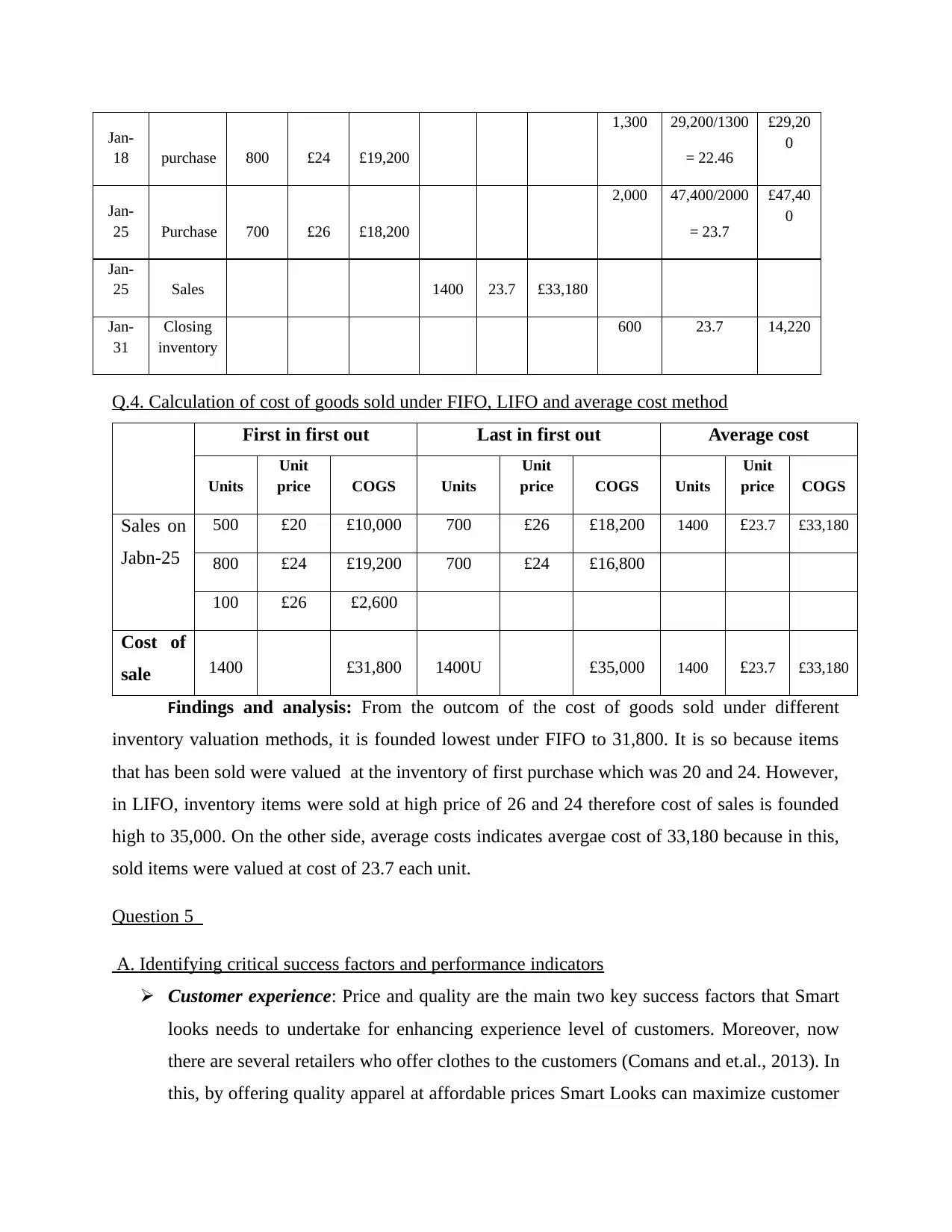

Q.3 Inventory valuation

(1) First-in, first-out

This method of stock valuation is based on the assumption that stock which has been bought first

by the Smart looks will be sold first before ther other items, as a result, stock which is left in the stock

will be valued at the price of latest goods bought.

Date

Particula

r

Purchase Sale Closing stock

Units

Unit

price TC Units Price TC

Unit Cost

Jan-1

Beginning

stock 500 £20 £10,000 500@20 £10,000

Jan-18 Purchasse 800 £24 £19,200

500@20

800@24

£29,200

Jan-25 Purchase 700 £26 £18,200

500@20

800@24

700@26

£47,400

Jan-25 Sales 500 £20 £10,000

800 £24 £19,200

100 £26 £2,600

1400 £31,800

Jan-31

Closing

inventory

600@26 £15,600

(2) Last-in, First-out

It is just inverse to the opposite one, which states that over the period, prices goes up,

therefore, goods that is bought latest will dispose off first (Li and Sun, 2016). However, on the

other side, material that remains left in the stock is the part of stock that bought initially.

downward to 13.5 and 13 GBP at 20,000 & 25000 units of output. The reason is that TFC of

50,000 is allocated and spreaded to more number of units which resulted less cost each unit.

Q.3 Inventory valuation

(1) First-in, first-out

This method of stock valuation is based on the assumption that stock which has been bought first

by the Smart looks will be sold first before ther other items, as a result, stock which is left in the stock

will be valued at the price of latest goods bought.

Date

Particula

r

Purchase Sale Closing stock

Units

Unit

price TC Units Price TC

Unit Cost

Jan-1

Beginning

stock 500 £20 £10,000 500@20 £10,000

Jan-18 Purchasse 800 £24 £19,200

500@20

800@24

£29,200

Jan-25 Purchase 700 £26 £18,200

500@20

800@24

700@26

£47,400

Jan-25 Sales 500 £20 £10,000

800 £24 £19,200

100 £26 £2,600

1400 £31,800

Jan-31

Closing

inventory

600@26 £15,600

(2) Last-in, First-out

It is just inverse to the opposite one, which states that over the period, prices goes up,

therefore, goods that is bought latest will dispose off first (Li and Sun, 2016). However, on the

other side, material that remains left in the stock is the part of stock that bought initially.

Date

Particul

ar

Purchase Sale Closing stock

Units

Unit

price

Total

cost Units

Unit

price

Total

cost

Unit with

rate

Total

cost

Jan-1

Beginning

stock 500 £20 £10,000 500@20 £10,000

Jan-18 Purchase 800 £24 £19,200

500@20

800@24

£29,200

Jan-25 Purchase 700 £26 £18,200

500 units

at 20

800 units

at 24

700 units

at 26

£47,400

Jan-25 Sales 700 £26 £18,200

700 £24 £16,800

1400 £35,000

Jan-31

Closing

stock

100 at 24

500 at 20

£12,400

(3) Average costs

This method is a mid-way between both the approaches which use average prices for the

inventory sales and closing stock valuation as well (Harris and Harris, 2017). The average price

of the stock is computed by applying the following formula, presented below:

Averrage price = Total costs of material / total number of units

Date Items

Purchase Sale Closing stock

Units

Unit

price

Total

cost

Unit

s

Uni

t

pric

e

Total

cost Units

Unit

price

Total

cost

Jan-1

Beginnin

g stock 500 £20 £10,000 500 20

£10,00

0

Particul

ar

Purchase Sale Closing stock

Units

Unit

price

Total

cost Units

Unit

price

Total

cost

Unit with

rate

Total

cost

Jan-1

Beginning

stock 500 £20 £10,000 500@20 £10,000

Jan-18 Purchase 800 £24 £19,200

500@20

800@24

£29,200

Jan-25 Purchase 700 £26 £18,200

500 units

at 20

800 units

at 24

700 units

at 26

£47,400

Jan-25 Sales 700 £26 £18,200

700 £24 £16,800

1400 £35,000

Jan-31

Closing

stock

100 at 24

500 at 20

£12,400

(3) Average costs

This method is a mid-way between both the approaches which use average prices for the

inventory sales and closing stock valuation as well (Harris and Harris, 2017). The average price

of the stock is computed by applying the following formula, presented below:

Averrage price = Total costs of material / total number of units

Date Items

Purchase Sale Closing stock

Units

Unit

price

Total

cost

Unit

s

Uni

t

pric

e

Total

cost Units

Unit

price

Total

cost

Jan-1

Beginnin

g stock 500 £20 £10,000 500 20

£10,00

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jan-

18 purchase 800 £24 £19,200

1,300 29,200/1300

= 22.46

£29,20

0

Jan-

25 Purchase 700 £26 £18,200

2,000 47,400/2000

= 23.7

£47,40

0

Jan-

25 Sales 1400 23.7 £33,180

Jan-

31

Closing

inventory

600 23.7 14,220

Q.4. Calculation of cost of goods sold under FIFO, LIFO and average cost method

First in first out Last in first out Average cost

Units

Unit

price COGS Units

Unit

price COGS Units

Unit

price COGS

Sales on

Jabn-25

500 £20 £10,000 700 £26 £18,200 1400 £23.7 £33,180

800 £24 £19,200 700 £24 £16,800

100 £26 £2,600

Cost of

sale 1400 £31,800 1400U £35,000 1400 £23.7 £33,180

Findings and analysis: From the outcom of the cost of goods sold under different

inventory valuation methods, it is founded lowest under FIFO to 31,800. It is so because items

that has been sold were valued at the inventory of first purchase which was 20 and 24. However,

in LIFO, inventory items were sold at high price of 26 and 24 therefore cost of sales is founded

high to 35,000. On the other side, average costs indicates avergae cost of 33,180 because in this,

sold items were valued at cost of 23.7 each unit.

Question 5

A. Identifying critical success factors and performance indicators

Customer experience: Price and quality are the main two key success factors that Smart

looks needs to undertake for enhancing experience level of customers. Moreover, now

there are several retailers who offer clothes to the customers (Comans and et.al., 2013). In

this, by offering quality apparel at affordable prices Smart Looks can maximize customer

18 purchase 800 £24 £19,200

1,300 29,200/1300

= 22.46

£29,20

0

Jan-

25 Purchase 700 £26 £18,200

2,000 47,400/2000

= 23.7

£47,40

0

Jan-

25 Sales 1400 23.7 £33,180

Jan-

31

Closing

inventory

600 23.7 14,220

Q.4. Calculation of cost of goods sold under FIFO, LIFO and average cost method

First in first out Last in first out Average cost

Units

Unit

price COGS Units

Unit

price COGS Units

Unit

price COGS

Sales on

Jabn-25

500 £20 £10,000 700 £26 £18,200 1400 £23.7 £33,180

800 £24 £19,200 700 £24 £16,800

100 £26 £2,600

Cost of

sale 1400 £31,800 1400U £35,000 1400 £23.7 £33,180

Findings and analysis: From the outcom of the cost of goods sold under different

inventory valuation methods, it is founded lowest under FIFO to 31,800. It is so because items

that has been sold were valued at the inventory of first purchase which was 20 and 24. However,

in LIFO, inventory items were sold at high price of 26 and 24 therefore cost of sales is founded

high to 35,000. On the other side, average costs indicates avergae cost of 33,180 because in this,

sold items were valued at cost of 23.7 each unit.

Question 5

A. Identifying critical success factors and performance indicators

Customer experience: Price and quality are the main two key success factors that Smart

looks needs to undertake for enhancing experience level of customers. Moreover, now

there are several retailers who offer clothes to the customers (Comans and et.al., 2013). In

this, by offering quality apparel at affordable prices Smart Looks can maximize customer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

experience. Further, by making evaluation of sales revenue and profitability aspect with

the historical values Smart Looks can assess the impact of action undertaken.

Supplier and product quality: Clothing retailer can build highly prominent relationship

with the suppliers by making payment on time. Besides this, smart looks can enhance and

maintain the quality of clothes by using relevant tools and techniques such TQM (Kaplan

and Atkinson, 2015). Company can measure the satisfaction level of customers in relation

to product quality by taking feedback from them.

Operations efficiency: Smart looks can increase operational efficiency by making high

care of manufacturing equipments. Further, by encouraging personnel towards better

performance operational efficiency can be enhanced (Li, Richardson and Tuna, 2014).

Output generated by the firm is a main indicator which in turn helps in assessing the

extent to which operational efficiency is increased.

Reducing maintenance spending: Smart Looks can control spending by using high tech

equipments and employing budgetary control tool. By comparing the current spending

level of maintenance with planned Smart Looks can assess the level of deviations. In this

way, by undertaking strategic action for improvement Smart Look can attain success.

Cost reduction and profit maximization: By employing budgeting techniques Smart

Looks can make control on cost level. Further, by eliminating undesirable activities from

plan firm can reduce the level of cost significantly (Lord, 2007). This in turn helps in

maximizing profit to a great extent and thereby helps in achieving success.

B.

1. Identifying the ways through which cost level can be reduced

Cost is the one of the main elements that has direct impact on the profit margin

generated by firm. Hence, it is vital for Smart looks to make control on cost level and thereby

enjoys high profit margin. In this regard, by employing variance analysis or standard costing

method business unit make evaluation of performance of each department on a periodical basis.

By making assessment and identifying deviations Smart looks can strategic action for

improvement within the suitable time frame (What is Budgeting? What is a Budget, 2017). In

this way, by taking timely action level of overspending can be reduced to a great extent. In

addition to this, by employing zero bases budgeting technique clothing retailer can make suitable

the historical values Smart Looks can assess the impact of action undertaken.

Supplier and product quality: Clothing retailer can build highly prominent relationship

with the suppliers by making payment on time. Besides this, smart looks can enhance and

maintain the quality of clothes by using relevant tools and techniques such TQM (Kaplan

and Atkinson, 2015). Company can measure the satisfaction level of customers in relation

to product quality by taking feedback from them.

Operations efficiency: Smart looks can increase operational efficiency by making high

care of manufacturing equipments. Further, by encouraging personnel towards better

performance operational efficiency can be enhanced (Li, Richardson and Tuna, 2014).

Output generated by the firm is a main indicator which in turn helps in assessing the

extent to which operational efficiency is increased.

Reducing maintenance spending: Smart Looks can control spending by using high tech

equipments and employing budgetary control tool. By comparing the current spending

level of maintenance with planned Smart Looks can assess the level of deviations. In this

way, by undertaking strategic action for improvement Smart Look can attain success.

Cost reduction and profit maximization: By employing budgeting techniques Smart

Looks can make control on cost level. Further, by eliminating undesirable activities from

plan firm can reduce the level of cost significantly (Lord, 2007). This in turn helps in

maximizing profit to a great extent and thereby helps in achieving success.

B.

1. Identifying the ways through which cost level can be reduced

Cost is the one of the main elements that has direct impact on the profit margin

generated by firm. Hence, it is vital for Smart looks to make control on cost level and thereby

enjoys high profit margin. In this regard, by employing variance analysis or standard costing

method business unit make evaluation of performance of each department on a periodical basis.

By making assessment and identifying deviations Smart looks can strategic action for

improvement within the suitable time frame (What is Budgeting? What is a Budget, 2017). In

this way, by taking timely action level of overspending can be reduced to a great extent. In

addition to this, by employing zero bases budgeting technique clothing retailer can make suitable

allocation and thereby would become able to spend money in an effectual way. All such

techniques provide high level of assistance in avoid high spending and thereby helps in

maintaining suitable cost level.

2. Assessing the manner in which quality can be enhanced

Quality of the fabric is one of the main factors that have great impact on the decision

making of customers. Hence, by undertaking total quality management technique Smart Looks

can evolve high level of satisfaction among the customers. It is continual improvement technique

which places emphasis on making improvement in the process, products or services. Hence,

TQM may be served as a strategic and systematic approach which lays high level of focus on

identifying defects and thereby helps in taking action for improvement within the suitable time

fame (What is total quality management (TQM), 2017). Hence, expectation level of stakeholders

can be met by Smart Looks through the means of total quality management technique. Moreover,

such technique enables firm to enhance the efficiency level of operations.

TASK 2

Q.6.

(A). Meaning of budget

Budget is a financial plan that is prepared by the business manmagers to find out the

amount of money being available for the spending purpose and also estimates the projected

expenditures in the future period. Thus, the key focus of it is to figure out the amount of expected

earnings of the business from sales and the prospective expenses as a result of material purchase,

labor’s wages and other fixed & varible spending (Deegan, 2013). The excess of incoming of

revenues over the monetary outgoings, expenses is reported as surplus or deficit, and helps in

making proper planning & strategies for optimum allocation and use of funds for curtailing cost

and maximizing sales to assure adequate surplus.

(B). Purpose or objectives of budgetary planning

The main key objectives or purpose behind constructing budgets are enumerated here

below:

techniques provide high level of assistance in avoid high spending and thereby helps in

maintaining suitable cost level.

2. Assessing the manner in which quality can be enhanced

Quality of the fabric is one of the main factors that have great impact on the decision

making of customers. Hence, by undertaking total quality management technique Smart Looks

can evolve high level of satisfaction among the customers. It is continual improvement technique

which places emphasis on making improvement in the process, products or services. Hence,

TQM may be served as a strategic and systematic approach which lays high level of focus on

identifying defects and thereby helps in taking action for improvement within the suitable time

fame (What is total quality management (TQM), 2017). Hence, expectation level of stakeholders

can be met by Smart Looks through the means of total quality management technique. Moreover,

such technique enables firm to enhance the efficiency level of operations.

TASK 2

Q.6.

(A). Meaning of budget

Budget is a financial plan that is prepared by the business manmagers to find out the

amount of money being available for the spending purpose and also estimates the projected

expenditures in the future period. Thus, the key focus of it is to figure out the amount of expected

earnings of the business from sales and the prospective expenses as a result of material purchase,

labor’s wages and other fixed & varible spending (Deegan, 2013). The excess of incoming of

revenues over the monetary outgoings, expenses is reported as surplus or deficit, and helps in

making proper planning & strategies for optimum allocation and use of funds for curtailing cost

and maximizing sales to assure adequate surplus.

(B). Purpose or objectives of budgetary planning

The main key objectives or purpose behind constructing budgets are enumerated here

below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23