Semester 1 2019: Inherent Risk Assessment Report of Mirvac Group

VerifiedAdded on 2023/03/31

|9

|1930

|185

Report

AI Summary

This report provides an inherent risk assessment of Mirvac Group (MRG) for PACC6002 AAS Semester 1 2019. It analyzes the company's business nature, previous audit results, non-routine transactions, and potential for fraudulent financial reporting. The assessment considers factors like the volatility of the property industry, reliance on equity capital, and the length of the auditor relationship. The report evaluates operating revenue, profit, equity, assets, and liabilities, concluding with an overall inherent risk level based on the company's risk model and internal controls. Key audit matters, such as the carrying value of inventories and fair values of investment properties, are also discussed. The report references ASA standards and academic literature to support its analysis and recommendations. Desklib offers a platform to explore similar assignments and resources for students.

PACC6002 AAS Semester 1 2019

Table of Contents

Attachment 1.......................................................................................................................................2

Part 1 Template – Information on Group’s chosen company..........................................................2

Attachment 2.......................................................................................................................................5

Part 2 Template – Overall inherent risk assessment.......................................................................5

References.........................................................................................................................................10

1

Table of Contents

Attachment 1.......................................................................................................................................2

Part 1 Template – Information on Group’s chosen company..........................................................2

Attachment 2.......................................................................................................................................5

Part 2 Template – Overall inherent risk assessment.......................................................................5

References.........................................................................................................................................10

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PACC6002 AAS Semester 1 2019

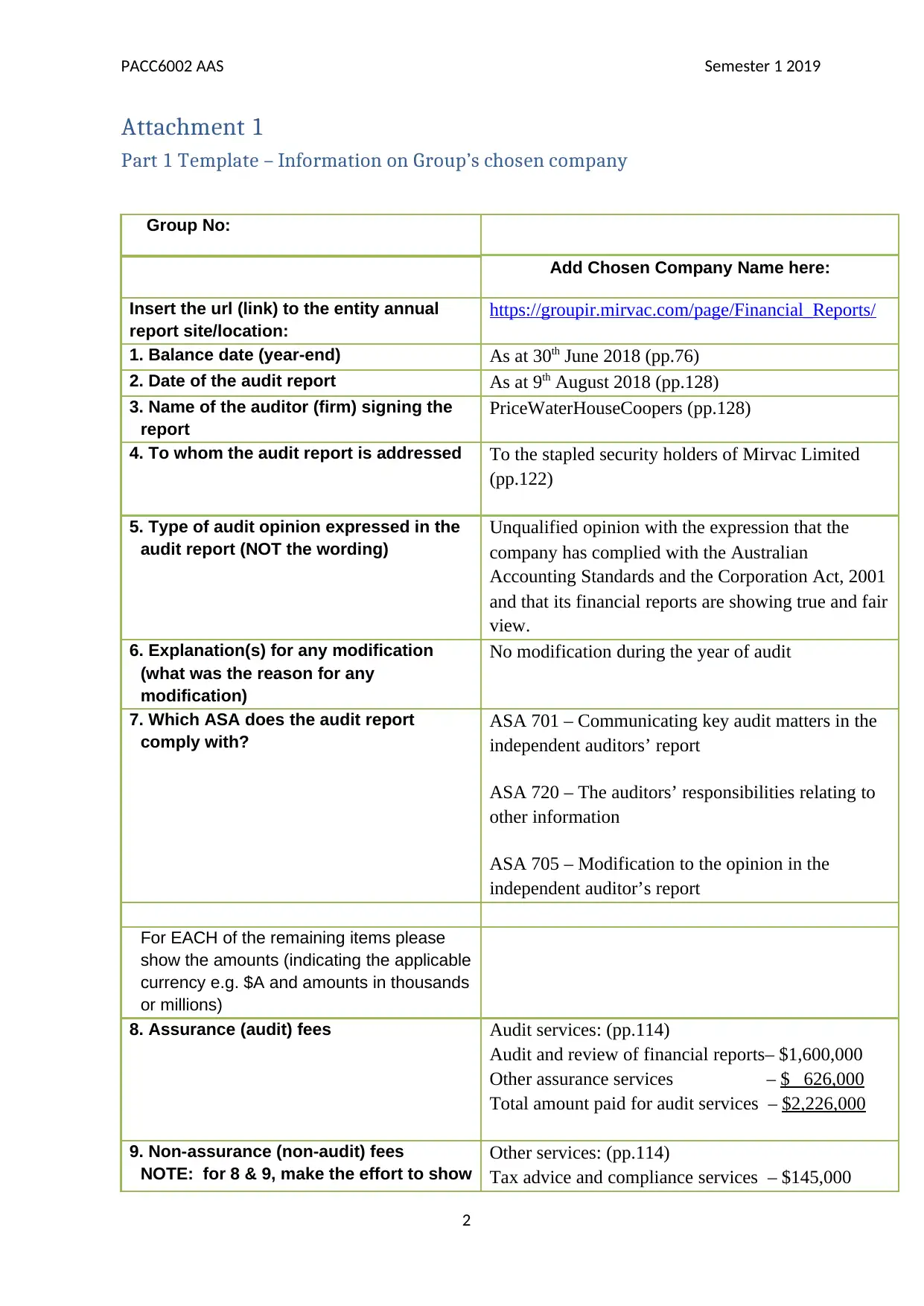

Attachment 1

Part 1 Template – Information on Group’s chosen company

Group No:

Add Chosen Company Name here:

Insert the url (link) to the entity annual

report site/location:

https://groupir.mirvac.com/page/Financial_Reports/

1. Balance date (year-end) As at 30th June 2018 (pp.76)

2. Date of the audit report As at 9th August 2018 (pp.128)

3. Name of the auditor (firm) signing the

report

PriceWaterHouseCoopers (pp.128)

4. To whom the audit report is addressed To the stapled security holders of Mirvac Limited

(pp.122)

5. Type of audit opinion expressed in the

audit report (NOT the wording)

Unqualified opinion with the expression that the

company has complied with the Australian

Accounting Standards and the Corporation Act, 2001

and that its financial reports are showing true and fair

view.

6. Explanation(s) for any modification

(what was the reason for any

modification)

No modification during the year of audit

7. Which ASA does the audit report

comply with?

ASA 701 – Communicating key audit matters in the

independent auditors’ report

ASA 720 – The auditors’ responsibilities relating to

other information

ASA 705 – Modification to the opinion in the

independent auditor’s report

For EACH of the remaining items please

show the amounts (indicating the applicable

currency e.g. $A and amounts in thousands

or millions)

8. Assurance (audit) fees Audit services: (pp.114)

Audit and review of financial reports– $1,600,000

Other assurance services – $ 626,000

Total amount paid for audit services – $2,226,000

9. Non-assurance (non-audit) fees

NOTE: for 8 & 9, make the effort to show

Other services: (pp.114)

Tax advice and compliance services – $145,000

2

Attachment 1

Part 1 Template – Information on Group’s chosen company

Group No:

Add Chosen Company Name here:

Insert the url (link) to the entity annual

report site/location:

https://groupir.mirvac.com/page/Financial_Reports/

1. Balance date (year-end) As at 30th June 2018 (pp.76)

2. Date of the audit report As at 9th August 2018 (pp.128)

3. Name of the auditor (firm) signing the

report

PriceWaterHouseCoopers (pp.128)

4. To whom the audit report is addressed To the stapled security holders of Mirvac Limited

(pp.122)

5. Type of audit opinion expressed in the

audit report (NOT the wording)

Unqualified opinion with the expression that the

company has complied with the Australian

Accounting Standards and the Corporation Act, 2001

and that its financial reports are showing true and fair

view.

6. Explanation(s) for any modification

(what was the reason for any

modification)

No modification during the year of audit

7. Which ASA does the audit report

comply with?

ASA 701 – Communicating key audit matters in the

independent auditors’ report

ASA 720 – The auditors’ responsibilities relating to

other information

ASA 705 – Modification to the opinion in the

independent auditor’s report

For EACH of the remaining items please

show the amounts (indicating the applicable

currency e.g. $A and amounts in thousands

or millions)

8. Assurance (audit) fees Audit services: (pp.114)

Audit and review of financial reports– $1,600,000

Other assurance services – $ 626,000

Total amount paid for audit services – $2,226,000

9. Non-assurance (non-audit) fees

NOTE: for 8 & 9, make the effort to show

Other services: (pp.114)

Tax advice and compliance services – $145,000

2

PACC6002 AAS Semester 1 2019

any breakdown showing what the fees

were for and who they were paid to.

Advisory services –$ 6,000

Total others services –$ 161,000

10. The industry (or industries) the

chosen entity operates in

Property, Investment, Retail Estate

11. Operating revenue $2,159 m(pp.75)

12. Operating profit before tax $1,166 m(pp.75)

13. Operating profit after tax $1,089 m(pp.75)

14. Equity $8,655 m(pp.76)

15. Total assets $13,345 m(pp.76)

16. Total liabilities $4,690 m(pp.76)

3

any breakdown showing what the fees

were for and who they were paid to.

Advisory services –$ 6,000

Total others services –$ 161,000

10. The industry (or industries) the

chosen entity operates in

Property, Investment, Retail Estate

11. Operating revenue $2,159 m(pp.75)

12. Operating profit before tax $1,166 m(pp.75)

13. Operating profit after tax $1,089 m(pp.75)

14. Equity $8,655 m(pp.76)

15. Total assets $13,345 m(pp.76)

16. Total liabilities $4,690 m(pp.76)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PACC6002 AAS Semester 1 2019

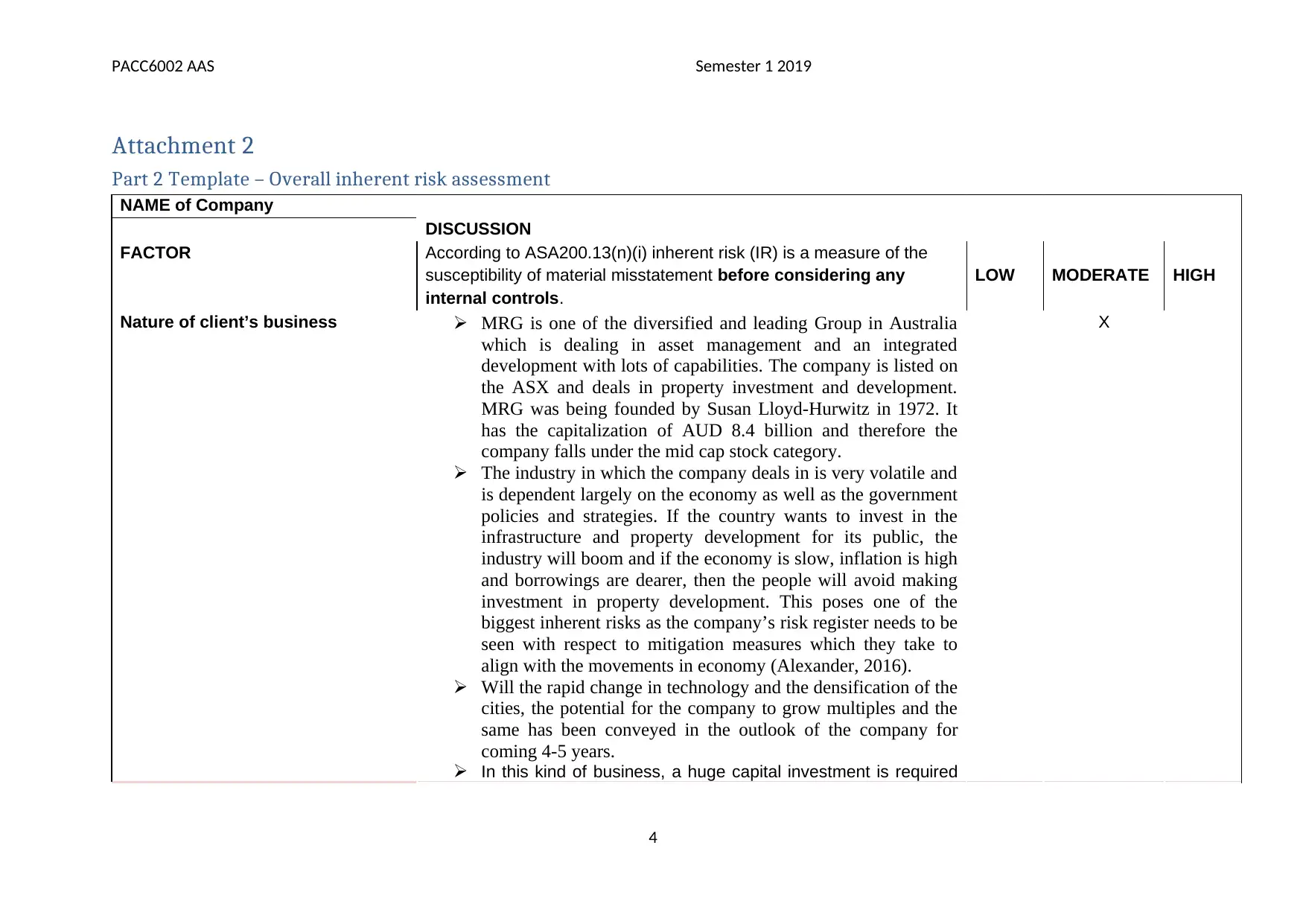

Attachment 2

Part 2 Template – Overall inherent risk assessment

NAME of Company

DISCUSSION

FACTOR According to ASA200.13(n)(i) inherent risk (IR) is a measure of the

susceptibility of material misstatement before considering any

internal controls.

LOW MODERATE HIGH

Nature of client’s business MRG is one of the diversified and leading Group in Australia

which is dealing in asset management and an integrated

development with lots of capabilities. The company is listed on

the ASX and deals in property investment and development.

MRG was being founded by Susan Lloyd-Hurwitz in 1972. It

has the capitalization of AUD 8.4 billion and therefore the

company falls under the mid cap stock category.

The industry in which the company deals in is very volatile and

is dependent largely on the economy as well as the government

policies and strategies. If the country wants to invest in the

infrastructure and property development for its public, the

industry will boom and if the economy is slow, inflation is high

and borrowings are dearer, then the people will avoid making

investment in property development. This poses one of the

biggest inherent risks as the company’s risk register needs to be

seen with respect to mitigation measures which they take to

align with the movements in economy (Alexander, 2016).

Will the rapid change in technology and the densification of the

cities, the potential for the company to grow multiples and the

same has been conveyed in the outlook of the company for

coming 4-5 years.

In this kind of business, a huge capital investment is required

X

4

Attachment 2

Part 2 Template – Overall inherent risk assessment

NAME of Company

DISCUSSION

FACTOR According to ASA200.13(n)(i) inherent risk (IR) is a measure of the

susceptibility of material misstatement before considering any

internal controls.

LOW MODERATE HIGH

Nature of client’s business MRG is one of the diversified and leading Group in Australia

which is dealing in asset management and an integrated

development with lots of capabilities. The company is listed on

the ASX and deals in property investment and development.

MRG was being founded by Susan Lloyd-Hurwitz in 1972. It

has the capitalization of AUD 8.4 billion and therefore the

company falls under the mid cap stock category.

The industry in which the company deals in is very volatile and

is dependent largely on the economy as well as the government

policies and strategies. If the country wants to invest in the

infrastructure and property development for its public, the

industry will boom and if the economy is slow, inflation is high

and borrowings are dearer, then the people will avoid making

investment in property development. This poses one of the

biggest inherent risks as the company’s risk register needs to be

seen with respect to mitigation measures which they take to

align with the movements in economy (Alexander, 2016).

Will the rapid change in technology and the densification of the

cities, the potential for the company to grow multiples and the

same has been conveyed in the outlook of the company for

coming 4-5 years.

In this kind of business, a huge capital investment is required

X

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PACC6002 AAS Semester 1 2019

which may be in terms of equity or in debt. In case of Mirvac

Group, most of the investment is backed by equity capital.

Despite all this, the share prices have dropped and one of the

inherent risks posed here is the quality of the management of

the company. One of the other major risk is from the

competitors and the technology in the sector.

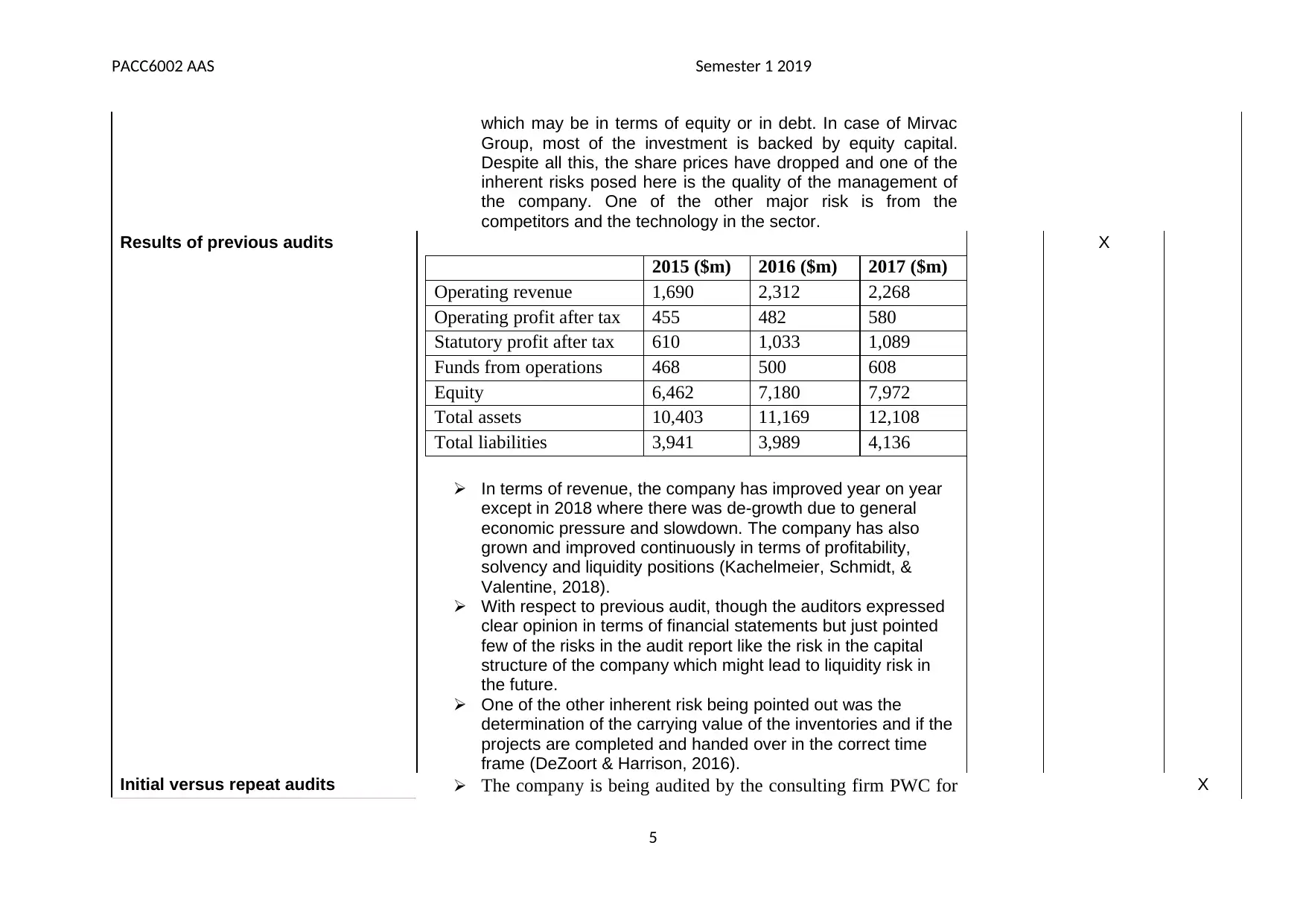

Results of previous audits

2015 ($m) 2016 ($m) 2017 ($m)

Operating revenue 1,690 2,312 2,268

Operating profit after tax 455 482 580

Statutory profit after tax 610 1,033 1,089

Funds from operations 468 500 608

Equity 6,462 7,180 7,972

Total assets 10,403 11,169 12,108

Total liabilities 3,941 3,989 4,136

In terms of revenue, the company has improved year on year

except in 2018 where there was de-growth due to general

economic pressure and slowdown. The company has also

grown and improved continuously in terms of profitability,

solvency and liquidity positions (Kachelmeier, Schmidt, &

Valentine, 2018).

With respect to previous audit, though the auditors expressed

clear opinion in terms of financial statements but just pointed

few of the risks in the audit report like the risk in the capital

structure of the company which might lead to liquidity risk in

the future.

One of the other inherent risk being pointed out was the

determination of the carrying value of the inventories and if the

projects are completed and handed over in the correct time

frame (DeZoort & Harrison, 2016).

X

Initial versus repeat audits The company is being audited by the consulting firm PWC for X

5

which may be in terms of equity or in debt. In case of Mirvac

Group, most of the investment is backed by equity capital.

Despite all this, the share prices have dropped and one of the

inherent risks posed here is the quality of the management of

the company. One of the other major risk is from the

competitors and the technology in the sector.

Results of previous audits

2015 ($m) 2016 ($m) 2017 ($m)

Operating revenue 1,690 2,312 2,268

Operating profit after tax 455 482 580

Statutory profit after tax 610 1,033 1,089

Funds from operations 468 500 608

Equity 6,462 7,180 7,972

Total assets 10,403 11,169 12,108

Total liabilities 3,941 3,989 4,136

In terms of revenue, the company has improved year on year

except in 2018 where there was de-growth due to general

economic pressure and slowdown. The company has also

grown and improved continuously in terms of profitability,

solvency and liquidity positions (Kachelmeier, Schmidt, &

Valentine, 2018).

With respect to previous audit, though the auditors expressed

clear opinion in terms of financial statements but just pointed

few of the risks in the audit report like the risk in the capital

structure of the company which might lead to liquidity risk in

the future.

One of the other inherent risk being pointed out was the

determination of the carrying value of the inventories and if the

projects are completed and handed over in the correct time

frame (DeZoort & Harrison, 2016).

X

Initial versus repeat audits The company is being audited by the consulting firm PWC for X

5

PACC6002 AAS Semester 1 2019

the last 10 years Mirvac Group and it had three different audit

partners during this term namely, R l Gavin till 2010, the other

is Matthew Lunn from 2011 to 2015; MRG2011, MRG2012,

MRG2013, MRG2014, MRG2015. Since 2016 to 2019 Jane

Reilly is been audit partner. MRG2016, MRG2017, MRG2018.

Since 2010, each audit performed, the auditor has issued an

unmodified opinion, which increases the inherent risk in the

company (Bumgarner & Vasarhelyi, 2018). Since the auditor

has not been changed for a while, it is quite clear that the

independence might have been compromised in this case

considering the long relationship and it certainly poses a risk on

the internal control as well as financials of the company.

Therefore, not only the audit partners but the auditors should

also be changed from time to time.

In order to improving the transparency of the quality of audit

and auditors independently, companies must change their audit

partner every five year is required by Act 2001. Therefore,

based on the above assessment, the inherent risk level is

defined as high.

Quantity of non-routine

transactions

The non-routine transactions are the ones which are non-

recurring in nature and happens once a while. Some of the

examples include losses by fire, natural climates, etc. It also

means acquisition of major property, write off of assets or even

implementation of new product (Knechel & Salterio, 2016).

The same poses the inherent risk as the company’s

management may not have sufficient and adequate knowledge

and expertise to record that type of transaction correctly in the

books which may lead to misstatement and therefore it is one of

the major inherent risk. Since it is one time event, so the risk of

adjustments by the management is also high and therefore the

auditors needs to check on the same carefully.

Some of the non-routine transactions in case of Mirvac Group

X

6

the last 10 years Mirvac Group and it had three different audit

partners during this term namely, R l Gavin till 2010, the other

is Matthew Lunn from 2011 to 2015; MRG2011, MRG2012,

MRG2013, MRG2014, MRG2015. Since 2016 to 2019 Jane

Reilly is been audit partner. MRG2016, MRG2017, MRG2018.

Since 2010, each audit performed, the auditor has issued an

unmodified opinion, which increases the inherent risk in the

company (Bumgarner & Vasarhelyi, 2018). Since the auditor

has not been changed for a while, it is quite clear that the

independence might have been compromised in this case

considering the long relationship and it certainly poses a risk on

the internal control as well as financials of the company.

Therefore, not only the audit partners but the auditors should

also be changed from time to time.

In order to improving the transparency of the quality of audit

and auditors independently, companies must change their audit

partner every five year is required by Act 2001. Therefore,

based on the above assessment, the inherent risk level is

defined as high.

Quantity of non-routine

transactions

The non-routine transactions are the ones which are non-

recurring in nature and happens once a while. Some of the

examples include losses by fire, natural climates, etc. It also

means acquisition of major property, write off of assets or even

implementation of new product (Knechel & Salterio, 2016).

The same poses the inherent risk as the company’s

management may not have sufficient and adequate knowledge

and expertise to record that type of transaction correctly in the

books which may lead to misstatement and therefore it is one of

the major inherent risk. Since it is one time event, so the risk of

adjustments by the management is also high and therefore the

auditors needs to check on the same carefully.

Some of the non-routine transactions in case of Mirvac Group

X

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PACC6002 AAS Semester 1 2019

is payment for investment property, change in the value of cash

flow hedge and therefore the treatment of same in accounting

books should be checked clearly.

Quantity of estimates and

judgement required for accounts

The company has used a number of estimations and

assumptions while preparation of the financial statements.

These assumptions and estimates may be biased in favour of

the company for reflecting good financial position and

performance of the company towards the investor and

therefore it poses high level of inherent risk. This is based on

positive accounting theory whereby the management adopts

decision on the accounting policies to be followed in the

company (Sithole, Chandler, Abeysekera, & Paas, 2017).

Being a property development company, the valuation of

inventory and properties and the provision against the same is

based on a number of factors and therefore it needs to be

clearly checked by the auditor. Some of the other areas of

estimates are provision for doubtful debt, provision for warranty

expenses, etc. Thus, it can be said that the inherent risk is high

here.

X

Potential for fraudulent financial

reporting & misappropriation of

assets (fraud risk factors, see ASA

240)

ASA 240 discusses on the fraud risk factors which are related

to fraudulent financial reporting and misappropriation of assets.

This management may use such measures in order to overstate

or understate the profitability, etc. and therefore there should be

additional audit procedures to check upon the possibility of

same in the company (Heminway, 2017).

In the case of Mirvac Group, the auditors have been checking

for the possibility of fraud risk factors and the chances of

material misstatements in the company and the same has

been mentioned in the auditors’ report and basis their report, it

can be said that the inherent risk is low.

X

List any other factors (can you see

any illustrations in your client’s

annual report of the examples in

There are several other factors which have been mentioned in

the auditors’ report under the section key audit matters. Some

of such matters which could pose the inherent risk are:

X

7

is payment for investment property, change in the value of cash

flow hedge and therefore the treatment of same in accounting

books should be checked clearly.

Quantity of estimates and

judgement required for accounts

The company has used a number of estimations and

assumptions while preparation of the financial statements.

These assumptions and estimates may be biased in favour of

the company for reflecting good financial position and

performance of the company towards the investor and

therefore it poses high level of inherent risk. This is based on

positive accounting theory whereby the management adopts

decision on the accounting policies to be followed in the

company (Sithole, Chandler, Abeysekera, & Paas, 2017).

Being a property development company, the valuation of

inventory and properties and the provision against the same is

based on a number of factors and therefore it needs to be

clearly checked by the auditor. Some of the other areas of

estimates are provision for doubtful debt, provision for warranty

expenses, etc. Thus, it can be said that the inherent risk is high

here.

X

Potential for fraudulent financial

reporting & misappropriation of

assets (fraud risk factors, see ASA

240)

ASA 240 discusses on the fraud risk factors which are related

to fraudulent financial reporting and misappropriation of assets.

This management may use such measures in order to overstate

or understate the profitability, etc. and therefore there should be

additional audit procedures to check upon the possibility of

same in the company (Heminway, 2017).

In the case of Mirvac Group, the auditors have been checking

for the possibility of fraud risk factors and the chances of

material misstatements in the company and the same has

been mentioned in the auditors’ report and basis their report, it

can be said that the inherent risk is low.

X

List any other factors (can you see

any illustrations in your client’s

annual report of the examples in

There are several other factors which have been mentioned in

the auditors’ report under the section key audit matters. Some

of such matters which could pose the inherent risk are:

X

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PACC6002 AAS Semester 1 2019

ASA 315, Appendix 2 and ASA

570.A2)

1. Appropriateness of carrying value of the inventories in the

books;

2. Fair values of the investment properties and the assumptions

in this regard;

3. Recoverability of the deferred tax assets based on the

forecasted income statement of the company

Thus, in order to check these, the auditor should take help of the

experts and also put additional audit procedures in place to minimise

the inherent risk (Linden & Freeman, 2017).

Conclusion:

Overall inherent risk level

While preparation of the overall audit plan, the first step that

the auditor should take is to fix the materiality limit as it guides

the auditor in fixing the further course of action and identifying

which all areas needs to be checked on priority.

On the overall assessment of the company’s risk model and

the mitigation measures designed by the company and the

internal control practiced in the company, it can be said that

the company has moderate level on inherent risk.

8

ASA 315, Appendix 2 and ASA

570.A2)

1. Appropriateness of carrying value of the inventories in the

books;

2. Fair values of the investment properties and the assumptions

in this regard;

3. Recoverability of the deferred tax assets based on the

forecasted income statement of the company

Thus, in order to check these, the auditor should take help of the

experts and also put additional audit procedures in place to minimise

the inherent risk (Linden & Freeman, 2017).

Conclusion:

Overall inherent risk level

While preparation of the overall audit plan, the first step that

the auditor should take is to fix the materiality limit as it guides

the auditor in fixing the further course of action and identifying

which all areas needs to be checked on priority.

On the overall assessment of the company’s risk model and

the mitigation measures designed by the company and the

internal control practiced in the company, it can be said that

the company has moderate level on inherent risk.

8

PACC6002 AAS Semester 1 2019

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-431.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory and Application, 20(1), 7-51.

DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting fraud within organization. Journal of Business Ethics, 1-18.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and Organic Documents. SSRN, 1-35.

Kachelmeier, S., Schmidt, J., & Valentine, K. (2018). The disclaimer effect of disclosing critical audit matters in the auditor’s report. SSRN, 2(1), 1-39.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business Ethics Quarterly, 27(3), 353-379. Retrieved from

https://doi.org/10.1017/beq.2017.1

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of attention on learning accounting. Journal of Educational

Psychology, 109(2), 220. Retrieved from http://psycnet.apa.org/buy/2016-21263-001

9

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-431.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory and Application, 20(1), 7-51.

DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting fraud within organization. Journal of Business Ethics, 1-18.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and Organic Documents. SSRN, 1-35.

Kachelmeier, S., Schmidt, J., & Valentine, K. (2018). The disclaimer effect of disclosing critical audit matters in the auditor’s report. SSRN, 2(1), 1-39.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business Ethics Quarterly, 27(3), 353-379. Retrieved from

https://doi.org/10.1017/beq.2017.1

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of attention on learning accounting. Journal of Educational

Psychology, 109(2), 220. Retrieved from http://psycnet.apa.org/buy/2016-21263-001

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.