Corporate and Financial Accounting Analysis of Rio Tinto and BHP Billiton

VerifiedAdded on 2022/10/16

|12

|2765

|429

AI Summary

Contents Introduction 2 Part A 2 Items recorded under owner’ equity section 2 Movement of each item with reason 3 Items recorded under liability section 4 Movement of each item with reason 5 Advantages or disadvantages of each sources of fund 7 Part B 7 Conclusion 8 References 9 Introduction The objective of the report is to discuss the accounting trends present in the Australian companies Rio Tinto and BHP Billiton. Further, below mentioned report is segregated into two parts, the part A of the report highlight the details about recording equity and

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Corporate and Financial Accounting

Corporate and Financial Accounting

[Type the document subtitle]

Laptop04011

[Pick the date]

Corporate and Financial Accounting

[Type the document subtitle]

Laptop04011

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate and Financial Accounting 1

Abstract

The paper analyse the different heads present in the owner’s equity and liability head of the

organizations. Rio Tinto and BHP Billiton are the two companies discussed in the below

mentioned paper. Three year analysis of both the organization is elaborated to identify the

changes in the heads of the balance sheet. Further, elaboration of movement of these heads will

help the prospective people to analyse the growth of the company in the business environment.

Advantages and disadvantages of different sources of funds is discussed in the paper with the

analysis of three different types of organization prevailing in the business environment.

Abstract

The paper analyse the different heads present in the owner’s equity and liability head of the

organizations. Rio Tinto and BHP Billiton are the two companies discussed in the below

mentioned paper. Three year analysis of both the organization is elaborated to identify the

changes in the heads of the balance sheet. Further, elaboration of movement of these heads will

help the prospective people to analyse the growth of the company in the business environment.

Advantages and disadvantages of different sources of funds is discussed in the paper with the

analysis of three different types of organization prevailing in the business environment.

Corporate and Financial Accounting 2

Contents

Introduction......................................................................................................................................2

Part A...............................................................................................................................................2

Items recorded under owner’ equity section................................................................................2

Movement of each item with reason............................................................................................3

Items recorded under liability section..........................................................................................4

Movement of each item with reason............................................................................................5

Advantages or disadvantages of each sources of fund................................................................7

Part B...............................................................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Contents

Introduction......................................................................................................................................2

Part A...............................................................................................................................................2

Items recorded under owner’ equity section................................................................................2

Movement of each item with reason............................................................................................3

Items recorded under liability section..........................................................................................4

Movement of each item with reason............................................................................................5

Advantages or disadvantages of each sources of fund................................................................7

Part B...............................................................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Corporate and Financial Accounting 3

Introduction

The objective of the report is to discuss the accounting trends present in the Australian

companies Rio Tinto and BHP Billiton. Both the organizations are market leaders and

competitors present in the mining and petroleum industry of Australia. Further, below mentioned

report is segregated into two parts, the part A of the report highlight the details about recording

equity and liability section in the financial statements of the company and the movement of each

and every item recorded. Further, the second part of the report evaluate concepts used by small

proprietary, large and reporting organizations and the implication of the classification of the

companies in these three different ways. Analysis of the company Rio Tinto and BHP Billiton

evaluates the ways in which different aspects of the company present in equity and liability

section has fluctuated in a time period of three years (Hill, Price, and Ruch 2018).

Part A

Items recorded under owner’ equity section

Owner’s fund refers to fund that elaborates the proportion of the total value of company’s assets

that can be claimed by the owner. These funds are the net worth of the organization that is a part

of the assets of the organization after all the liabilities are paid off. The heads present in owner’s

equity fund for the company Rio Tinto are common stock, additional paid-up capital, retained

earnings, and accumulated other comprehensive income. Common stock in the equity fund refers

to the fund that involves the amount of shares that possess voting rights in the business. These

shares are also called ordinary shares. This stock represent the ownerships of the shareholders in

the company. Major stocks of the company are issued in this format only. Further Additional

paid-in capital refers to the amount over and above par value of shares (Fleckenstein, and

Longstaff 2018).

This is the amount that comes after deducting the par value from the issue price. Par value is

minimum amount of a share and issue price is the price at which share are sold. It refers to the

amount that is left with the organization after providing dividend to the stakeholders.

Accumulated other comprehensive income refers to the unrealized gains or loss for the

Introduction

The objective of the report is to discuss the accounting trends present in the Australian

companies Rio Tinto and BHP Billiton. Both the organizations are market leaders and

competitors present in the mining and petroleum industry of Australia. Further, below mentioned

report is segregated into two parts, the part A of the report highlight the details about recording

equity and liability section in the financial statements of the company and the movement of each

and every item recorded. Further, the second part of the report evaluate concepts used by small

proprietary, large and reporting organizations and the implication of the classification of the

companies in these three different ways. Analysis of the company Rio Tinto and BHP Billiton

evaluates the ways in which different aspects of the company present in equity and liability

section has fluctuated in a time period of three years (Hill, Price, and Ruch 2018).

Part A

Items recorded under owner’ equity section

Owner’s fund refers to fund that elaborates the proportion of the total value of company’s assets

that can be claimed by the owner. These funds are the net worth of the organization that is a part

of the assets of the organization after all the liabilities are paid off. The heads present in owner’s

equity fund for the company Rio Tinto are common stock, additional paid-up capital, retained

earnings, and accumulated other comprehensive income. Common stock in the equity fund refers

to the fund that involves the amount of shares that possess voting rights in the business. These

shares are also called ordinary shares. This stock represent the ownerships of the shareholders in

the company. Major stocks of the company are issued in this format only. Further Additional

paid-in capital refers to the amount over and above par value of shares (Fleckenstein, and

Longstaff 2018).

This is the amount that comes after deducting the par value from the issue price. Par value is

minimum amount of a share and issue price is the price at which share are sold. It refers to the

amount that is left with the organization after providing dividend to the stakeholders.

Accumulated other comprehensive income refers to the unrealized gains or loss for the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate and Financial Accounting 4

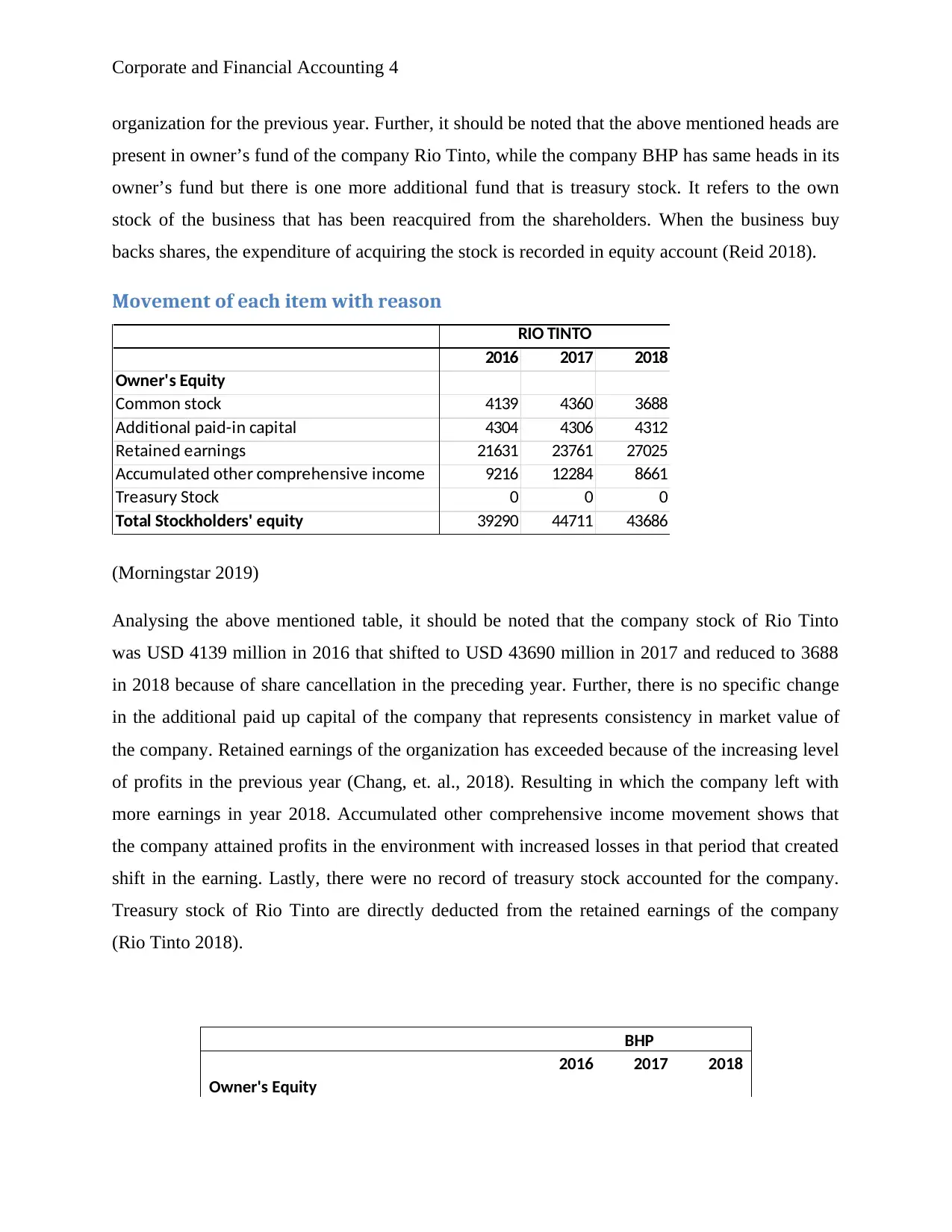

organization for the previous year. Further, it should be noted that the above mentioned heads are

present in owner’s fund of the company Rio Tinto, while the company BHP has same heads in its

owner’s fund but there is one more additional fund that is treasury stock. It refers to the own

stock of the business that has been reacquired from the shareholders. When the business buy

backs shares, the expenditure of acquiring the stock is recorded in equity account (Reid 2018).

Movement of each item with reason

2016 2017 2018

Owner's Equity

Common stock 4139 4360 3688

Additional paid-in capital 4304 4306 4312

Retained earnings 21631 23761 27025

Accumulated other comprehensive income 9216 12284 8661

Treasury Stock 0 0 0

Total Stockholders' equity 39290 44711 43686

RIO TINTO

(Morningstar 2019)

Analysing the above mentioned table, it should be noted that the company stock of Rio Tinto

was USD 4139 million in 2016 that shifted to USD 43690 million in 2017 and reduced to 3688

in 2018 because of share cancellation in the preceding year. Further, there is no specific change

in the additional paid up capital of the company that represents consistency in market value of

the company. Retained earnings of the organization has exceeded because of the increasing level

of profits in the previous year (Chang, et. al., 2018). Resulting in which the company left with

more earnings in year 2018. Accumulated other comprehensive income movement shows that

the company attained profits in the environment with increased losses in that period that created

shift in the earning. Lastly, there were no record of treasury stock accounted for the company.

Treasury stock of Rio Tinto are directly deducted from the retained earnings of the company

(Rio Tinto 2018).

BHP

2016 2017 2018

Owner's Equity

organization for the previous year. Further, it should be noted that the above mentioned heads are

present in owner’s fund of the company Rio Tinto, while the company BHP has same heads in its

owner’s fund but there is one more additional fund that is treasury stock. It refers to the own

stock of the business that has been reacquired from the shareholders. When the business buy

backs shares, the expenditure of acquiring the stock is recorded in equity account (Reid 2018).

Movement of each item with reason

2016 2017 2018

Owner's Equity

Common stock 4139 4360 3688

Additional paid-in capital 4304 4306 4312

Retained earnings 21631 23761 27025

Accumulated other comprehensive income 9216 12284 8661

Treasury Stock 0 0 0

Total Stockholders' equity 39290 44711 43686

RIO TINTO

(Morningstar 2019)

Analysing the above mentioned table, it should be noted that the company stock of Rio Tinto

was USD 4139 million in 2016 that shifted to USD 43690 million in 2017 and reduced to 3688

in 2018 because of share cancellation in the preceding year. Further, there is no specific change

in the additional paid up capital of the company that represents consistency in market value of

the company. Retained earnings of the organization has exceeded because of the increasing level

of profits in the previous year (Chang, et. al., 2018). Resulting in which the company left with

more earnings in year 2018. Accumulated other comprehensive income movement shows that

the company attained profits in the environment with increased losses in that period that created

shift in the earning. Lastly, there were no record of treasury stock accounted for the company.

Treasury stock of Rio Tinto are directly deducted from the retained earnings of the company

(Rio Tinto 2018).

BHP

2016 2017 2018

Owner's Equity

Corporate and Financial Accounting 5

Common stock 2243 2243 2243

Additional paid-in capital 0 0 0

Retained earnings 49542 52618 51064

Accumulated other comprehensive income 2538 2400 2290

Treasury Stock -33 -3 -5

Total Stockholders' equity 118953 117006 111993

(Morningstar 2019)

Further, talking about owner’s equity of BHP, it should be noted that the company did not buy

back any shares from the environment remaining the equity constant. Further, changes in

retained earnings of the organization elaborate increasing profits of the company after deduction

of all the expenses. Retained earnings head of the organization that means that even after

providing dividend to the shareholders, the organization is getting enough reserves to save.

Accumulated comprehensive earning for the organization is decrease which means that the

amount from the sale of securities that been incurred less in the previous year or less securities

have been sold. This amount is not reported in the incomes statement until the securities are sold.

Lastly, treasure stock of the BHP is represented in negative way because of expenditure incurred

by the organization. Although this amount is decreasing that means the level of expenditure to

incur the stock is reduced (BHP Billiton 2018).

Items recorded under liability section

Liabilities is the obligation of the organization that they need to pay to the creditors for the past

transactions. Initial items coming under liability head is account payable that represents the

amount the business need to pay to its creditors. This is the amount owned by the suppliers

against the company. Short term debts refers to the loan that the company need to repay within a

time span of one year. Capital lease represent the discounted prevent value of the lease over the

term plus interest accrued between the previous lease payments. Deferred revenue refers to

advance payment received whose services have not been delivered yet. Other current liabilities

are liabilities that cannot be assigned to a common head. All these liabilities mentioned above

form a part of current liabilities of the company (Robinson, et. al., 2015).

Non-current liabilities of the organization include long term debts that are paid by the

organization over a period of time more than one year. Deferred tax liability refers to the liability

Common stock 2243 2243 2243

Additional paid-in capital 0 0 0

Retained earnings 49542 52618 51064

Accumulated other comprehensive income 2538 2400 2290

Treasury Stock -33 -3 -5

Total Stockholders' equity 118953 117006 111993

(Morningstar 2019)

Further, talking about owner’s equity of BHP, it should be noted that the company did not buy

back any shares from the environment remaining the equity constant. Further, changes in

retained earnings of the organization elaborate increasing profits of the company after deduction

of all the expenses. Retained earnings head of the organization that means that even after

providing dividend to the shareholders, the organization is getting enough reserves to save.

Accumulated comprehensive earning for the organization is decrease which means that the

amount from the sale of securities that been incurred less in the previous year or less securities

have been sold. This amount is not reported in the incomes statement until the securities are sold.

Lastly, treasure stock of the BHP is represented in negative way because of expenditure incurred

by the organization. Although this amount is decreasing that means the level of expenditure to

incur the stock is reduced (BHP Billiton 2018).

Items recorded under liability section

Liabilities is the obligation of the organization that they need to pay to the creditors for the past

transactions. Initial items coming under liability head is account payable that represents the

amount the business need to pay to its creditors. This is the amount owned by the suppliers

against the company. Short term debts refers to the loan that the company need to repay within a

time span of one year. Capital lease represent the discounted prevent value of the lease over the

term plus interest accrued between the previous lease payments. Deferred revenue refers to

advance payment received whose services have not been delivered yet. Other current liabilities

are liabilities that cannot be assigned to a common head. All these liabilities mentioned above

form a part of current liabilities of the company (Robinson, et. al., 2015).

Non-current liabilities of the organization include long term debts that are paid by the

organization over a period of time more than one year. Deferred tax liability refers to the liability

Corporate and Financial Accounting 6

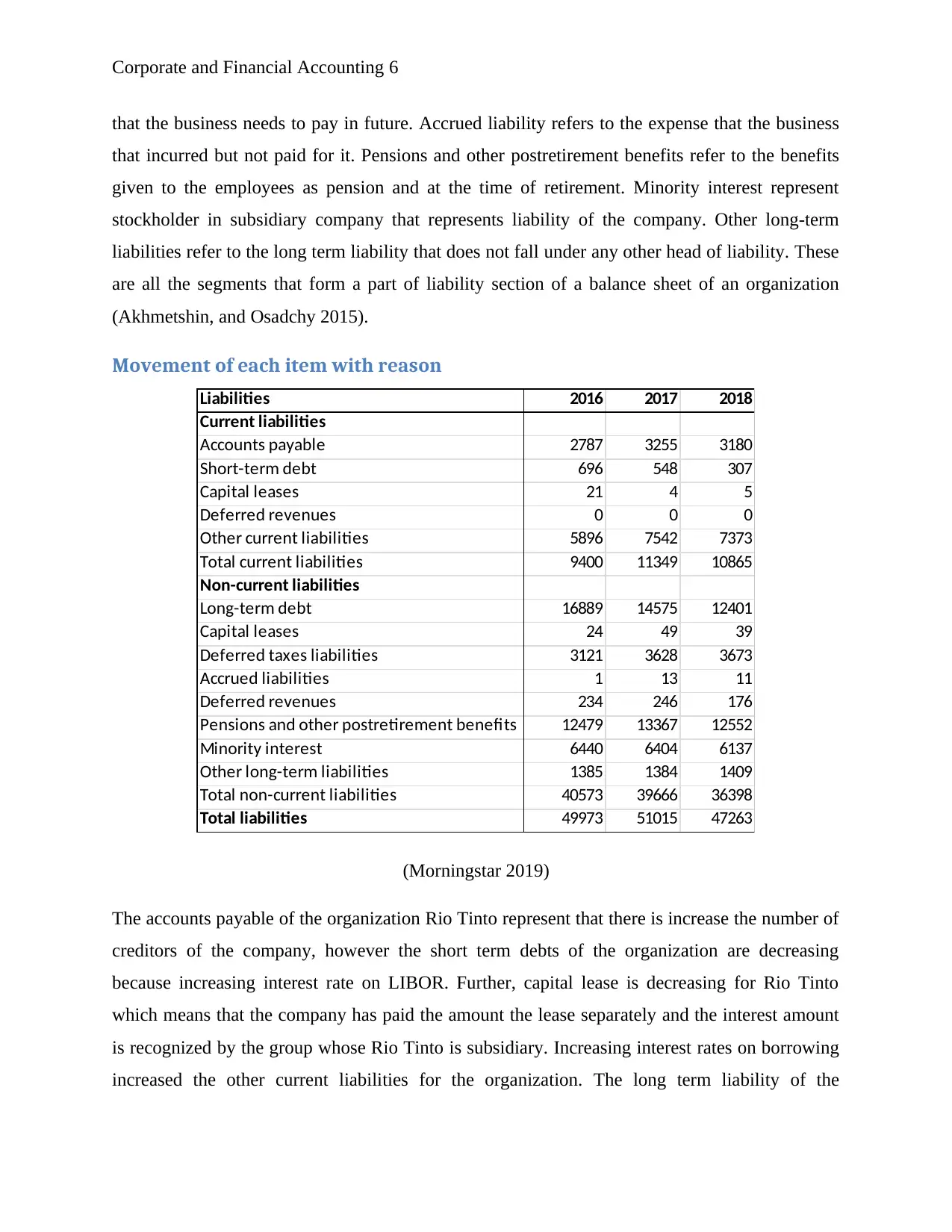

that the business needs to pay in future. Accrued liability refers to the expense that the business

that incurred but not paid for it. Pensions and other postretirement benefits refer to the benefits

given to the employees as pension and at the time of retirement. Minority interest represent

stockholder in subsidiary company that represents liability of the company. Other long-term

liabilities refer to the long term liability that does not fall under any other head of liability. These

are all the segments that form a part of liability section of a balance sheet of an organization

(Akhmetshin, and Osadchy 2015).

Movement of each item with reason

Liabilities 2016 2017 2018

Current liabilities

Accounts payable 2787 3255 3180

Short-term debt 696 548 307

Capital leases 21 4 5

Deferred revenues 0 0 0

Other current liabilities 5896 7542 7373

Total current liabilities 9400 11349 10865

Non-current liabilities

Long-term debt 16889 14575 12401

Capital leases 24 49 39

Deferred taxes liabilities 3121 3628 3673

Accrued liabilities 1 13 11

Deferred revenues 234 246 176

Pensions and other postretirement benefits 12479 13367 12552

Minority interest 6440 6404 6137

Other long-term liabilities 1385 1384 1409

Total non-current liabilities 40573 39666 36398

Total liabilities 49973 51015 47263

(Morningstar 2019)

The accounts payable of the organization Rio Tinto represent that there is increase the number of

creditors of the company, however the short term debts of the organization are decreasing

because increasing interest rate on LIBOR. Further, capital lease is decreasing for Rio Tinto

which means that the company has paid the amount the lease separately and the interest amount

is recognized by the group whose Rio Tinto is subsidiary. Increasing interest rates on borrowing

increased the other current liabilities for the organization. The long term liability of the

that the business needs to pay in future. Accrued liability refers to the expense that the business

that incurred but not paid for it. Pensions and other postretirement benefits refer to the benefits

given to the employees as pension and at the time of retirement. Minority interest represent

stockholder in subsidiary company that represents liability of the company. Other long-term

liabilities refer to the long term liability that does not fall under any other head of liability. These

are all the segments that form a part of liability section of a balance sheet of an organization

(Akhmetshin, and Osadchy 2015).

Movement of each item with reason

Liabilities 2016 2017 2018

Current liabilities

Accounts payable 2787 3255 3180

Short-term debt 696 548 307

Capital leases 21 4 5

Deferred revenues 0 0 0

Other current liabilities 5896 7542 7373

Total current liabilities 9400 11349 10865

Non-current liabilities

Long-term debt 16889 14575 12401

Capital leases 24 49 39

Deferred taxes liabilities 3121 3628 3673

Accrued liabilities 1 13 11

Deferred revenues 234 246 176

Pensions and other postretirement benefits 12479 13367 12552

Minority interest 6440 6404 6137

Other long-term liabilities 1385 1384 1409

Total non-current liabilities 40573 39666 36398

Total liabilities 49973 51015 47263

(Morningstar 2019)

The accounts payable of the organization Rio Tinto represent that there is increase the number of

creditors of the company, however the short term debts of the organization are decreasing

because increasing interest rate on LIBOR. Further, capital lease is decreasing for Rio Tinto

which means that the company has paid the amount the lease separately and the interest amount

is recognized by the group whose Rio Tinto is subsidiary. Increasing interest rates on borrowing

increased the other current liabilities for the organization. The long term liability of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting 7

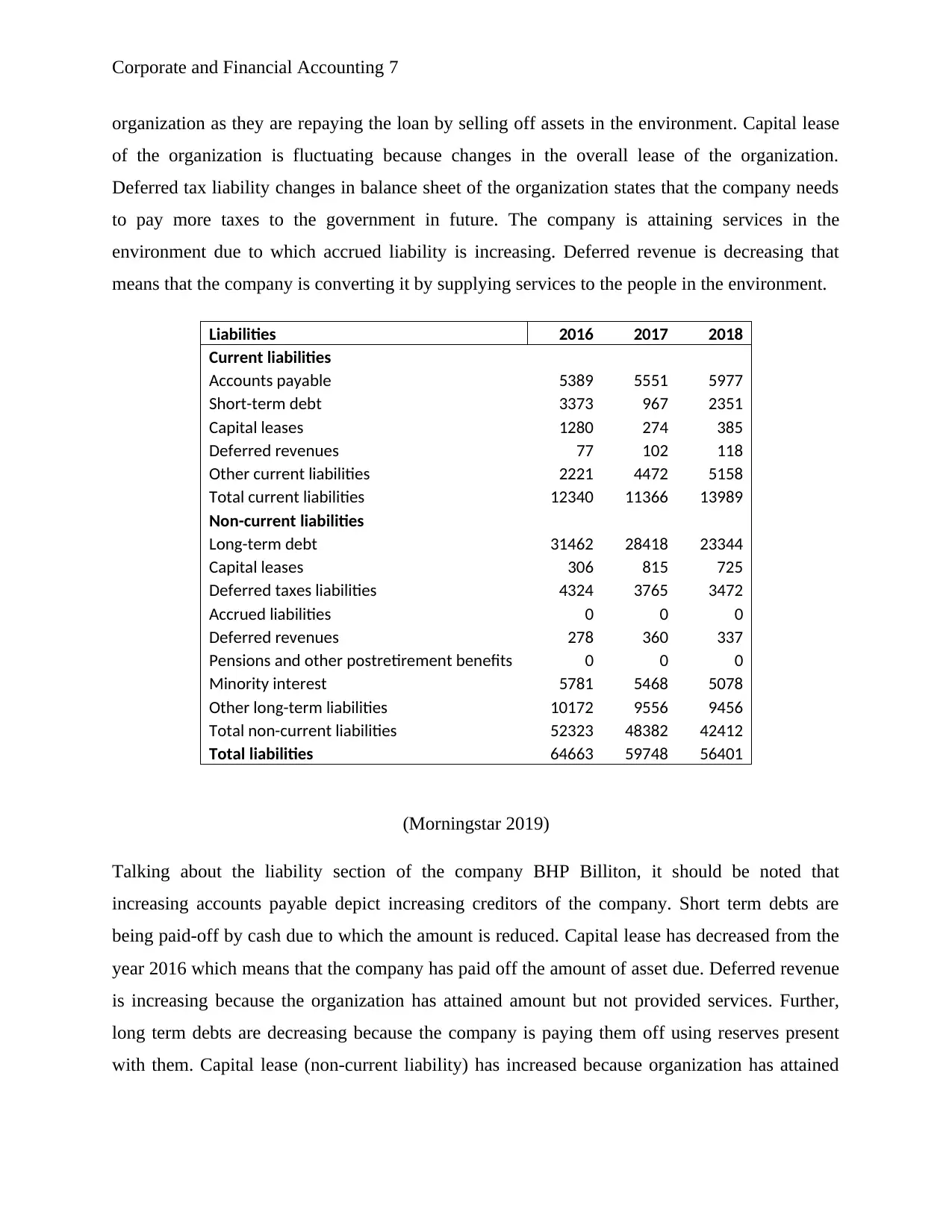

organization as they are repaying the loan by selling off assets in the environment. Capital lease

of the organization is fluctuating because changes in the overall lease of the organization.

Deferred tax liability changes in balance sheet of the organization states that the company needs

to pay more taxes to the government in future. The company is attaining services in the

environment due to which accrued liability is increasing. Deferred revenue is decreasing that

means that the company is converting it by supplying services to the people in the environment.

Liabilities 2016 2017 2018

Current liabilities

Accounts payable 5389 5551 5977

Short-term debt 3373 967 2351

Capital leases 1280 274 385

Deferred revenues 77 102 118

Other current liabilities 2221 4472 5158

Total current liabilities 12340 11366 13989

Non-current liabilities

Long-term debt 31462 28418 23344

Capital leases 306 815 725

Deferred taxes liabilities 4324 3765 3472

Accrued liabilities 0 0 0

Deferred revenues 278 360 337

Pensions and other postretirement benefits 0 0 0

Minority interest 5781 5468 5078

Other long-term liabilities 10172 9556 9456

Total non-current liabilities 52323 48382 42412

Total liabilities 64663 59748 56401

(Morningstar 2019)

Talking about the liability section of the company BHP Billiton, it should be noted that

increasing accounts payable depict increasing creditors of the company. Short term debts are

being paid-off by cash due to which the amount is reduced. Capital lease has decreased from the

year 2016 which means that the company has paid off the amount of asset due. Deferred revenue

is increasing because the organization has attained amount but not provided services. Further,

long term debts are decreasing because the company is paying them off using reserves present

with them. Capital lease (non-current liability) has increased because organization has attained

organization as they are repaying the loan by selling off assets in the environment. Capital lease

of the organization is fluctuating because changes in the overall lease of the organization.

Deferred tax liability changes in balance sheet of the organization states that the company needs

to pay more taxes to the government in future. The company is attaining services in the

environment due to which accrued liability is increasing. Deferred revenue is decreasing that

means that the company is converting it by supplying services to the people in the environment.

Liabilities 2016 2017 2018

Current liabilities

Accounts payable 5389 5551 5977

Short-term debt 3373 967 2351

Capital leases 1280 274 385

Deferred revenues 77 102 118

Other current liabilities 2221 4472 5158

Total current liabilities 12340 11366 13989

Non-current liabilities

Long-term debt 31462 28418 23344

Capital leases 306 815 725

Deferred taxes liabilities 4324 3765 3472

Accrued liabilities 0 0 0

Deferred revenues 278 360 337

Pensions and other postretirement benefits 0 0 0

Minority interest 5781 5468 5078

Other long-term liabilities 10172 9556 9456

Total non-current liabilities 52323 48382 42412

Total liabilities 64663 59748 56401

(Morningstar 2019)

Talking about the liability section of the company BHP Billiton, it should be noted that

increasing accounts payable depict increasing creditors of the company. Short term debts are

being paid-off by cash due to which the amount is reduced. Capital lease has decreased from the

year 2016 which means that the company has paid off the amount of asset due. Deferred revenue

is increasing because the organization has attained amount but not provided services. Further,

long term debts are decreasing because the company is paying them off using reserves present

with them. Capital lease (non-current liability) has increased because organization has attained

Corporate and Financial Accounting 8

more assets in the environment. Minority interest is being paid by the company due to which it is

decreasing.

Advantages or disadvantages of each sources of fund

Personal Savings: advantage of this source of fund is that it helps the owners to attain complete

control on the functions of the company. This process eliminates repaying to money or interest to

third party. Further, disadvantage of this process is that it increase the risk for the organization as

in case of failure of business, only the owner would tolerate the liability for the company.

Ownership Capital: This type of sourcing of finance let the organization to sell shares of the

company to the public in the environment. The benefit of this type of process is that it helps the

organization to share the risk with people in the environment. Also, under this type of sourcing

the company does not need to repay any amount nor in the form of interest as well. Disadvantage

of this type of process is that ownership is diluted that differentiates the decision making power

among people as well. This type of sourcing also requires time and efforts and high costing as

well (Weinstein, and Barden 2017).

Loan and Finance: under this type of process, the company takes loans from banks or other

institutions. The benefit of this type of process that it does not share ownership in the

environment. The company does not need to invest time and efforts to attain loan in the

environment. The disadvantage of this process is that the company need to pay high interest in

the environment (Brown, Boon, and Pitt 2017).

Part B

Small proprietary organization refers to the organization that has its assets less than $12.5

million in one financial year. This type of organization has employees less than 50 people and

earns gross operating revenue of less than $25 million in one financial year. If the organization

attains assets more than $12.5 million in a year or the number of employees or gross operating

revenue increases from $25 million then it means that the organization is large scale proprietary

organization. Reporting entity refers to a government owned organization whose objective is to

either serve customers or attain profits for the profitability of government (ASIC 2019). The

implication of compliance and reporting requirement it should be noted that high regulations are

more assets in the environment. Minority interest is being paid by the company due to which it is

decreasing.

Advantages or disadvantages of each sources of fund

Personal Savings: advantage of this source of fund is that it helps the owners to attain complete

control on the functions of the company. This process eliminates repaying to money or interest to

third party. Further, disadvantage of this process is that it increase the risk for the organization as

in case of failure of business, only the owner would tolerate the liability for the company.

Ownership Capital: This type of sourcing of finance let the organization to sell shares of the

company to the public in the environment. The benefit of this type of process is that it helps the

organization to share the risk with people in the environment. Also, under this type of sourcing

the company does not need to repay any amount nor in the form of interest as well. Disadvantage

of this type of process is that ownership is diluted that differentiates the decision making power

among people as well. This type of sourcing also requires time and efforts and high costing as

well (Weinstein, and Barden 2017).

Loan and Finance: under this type of process, the company takes loans from banks or other

institutions. The benefit of this type of process that it does not share ownership in the

environment. The company does not need to invest time and efforts to attain loan in the

environment. The disadvantage of this process is that the company need to pay high interest in

the environment (Brown, Boon, and Pitt 2017).

Part B

Small proprietary organization refers to the organization that has its assets less than $12.5

million in one financial year. This type of organization has employees less than 50 people and

earns gross operating revenue of less than $25 million in one financial year. If the organization

attains assets more than $12.5 million in a year or the number of employees or gross operating

revenue increases from $25 million then it means that the organization is large scale proprietary

organization. Reporting entity refers to a government owned organization whose objective is to

either serve customers or attain profits for the profitability of government (ASIC 2019). The

implication of compliance and reporting requirement it should be noted that high regulations are

Corporate and Financial Accounting 9

implied on a reporting organization because the government holds the shares of this organization.

Further, the small proprietary organization hold low degree of compliance in the environment as

compared to large proprietary (Gooris, and Peeters 2016).

Conclusion

Concluding the above mentioned facts, the report highlighted information about the company

Rio Tinto and BHP Billiton. The owner’s fund and liability head details are developed and

changes in each segment is defined. Further, the advantage and disadvantage of each source of

fund is elaborated in the paper. With classification of different types of organizations.

implied on a reporting organization because the government holds the shares of this organization.

Further, the small proprietary organization hold low degree of compliance in the environment as

compared to large proprietary (Gooris, and Peeters 2016).

Conclusion

Concluding the above mentioned facts, the report highlighted information about the company

Rio Tinto and BHP Billiton. The owner’s fund and liability head details are developed and

changes in each segment is defined. Further, the advantage and disadvantage of each source of

fund is elaborated in the paper. With classification of different types of organizations.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate and Financial Accounting 10

References

Akhmetshin, E.M. and Osadchy, E.A., 2015. New requirements to the control of the maintenance

of accounting records of the company in the conditions of the economic insecurity. International

Business Management, 9(5), pp.895-902.

ASIC., (2019) Are you a large or small proprietary company [online]. Available from <

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/are-you-a-large-or-small-proprietary-company/> [Accessed on 26 Sep. 19].

BHP Billiton., (2018) Annual Reporting 2018 [online]. Available from <

https://www.bhp.com/investor-centre/annual-reporting-2018> [Accessed on 26 Sep. 19].

Brown, T.E., Boon, E. and Pitt, L.F., 2017. Seeking funding in order to sell: Crowdfunding as a

marketing tool. Business Horizons, 60(2), pp.189-195.

Chang, X.S., Fu, K., Li, T., Tam, L. and Wong, G., 2018. Corporate environmental liabilities and

capital structure.

Fleckenstein, M. and Longstaff, F.A., 2018. Shadow funding costs: Measuring the cost of

balance sheet constraints (No. w24224). National Bureau of Economic Research.

Gooris, J. and Peeters, C., 2016. Fragmenting global business processes: A protection for

proprietary information. Journal of International Business Studies, 47(5), pp.535-562.

Hill, M., Price, R.A. and Ruch, G.W., 2018. An Alternative Approach to Distinguishing

Liabilities from Equity: Internal Capital versus External Capital. Available at SSRN 3086824.

Morningstar., (2019) BHP Group Ltd BHP [online]. Available from <

http://financials.morningstar.com/balance-sheet/bs.html?t=BHP®ion=aus&culture=en-US>

[Accessed on 26 Sep. 19].

Morningstar., (2019) Rio Tinto PLC ADR [online]. Available from <

http://financials.morningstar.com/balance-sheet/bs.html?t=RIO®ion=usa&culture=en-US>

[Accessed on 26 Sep. 19].

References

Akhmetshin, E.M. and Osadchy, E.A., 2015. New requirements to the control of the maintenance

of accounting records of the company in the conditions of the economic insecurity. International

Business Management, 9(5), pp.895-902.

ASIC., (2019) Are you a large or small proprietary company [online]. Available from <

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/are-you-a-large-or-small-proprietary-company/> [Accessed on 26 Sep. 19].

BHP Billiton., (2018) Annual Reporting 2018 [online]. Available from <

https://www.bhp.com/investor-centre/annual-reporting-2018> [Accessed on 26 Sep. 19].

Brown, T.E., Boon, E. and Pitt, L.F., 2017. Seeking funding in order to sell: Crowdfunding as a

marketing tool. Business Horizons, 60(2), pp.189-195.

Chang, X.S., Fu, K., Li, T., Tam, L. and Wong, G., 2018. Corporate environmental liabilities and

capital structure.

Fleckenstein, M. and Longstaff, F.A., 2018. Shadow funding costs: Measuring the cost of

balance sheet constraints (No. w24224). National Bureau of Economic Research.

Gooris, J. and Peeters, C., 2016. Fragmenting global business processes: A protection for

proprietary information. Journal of International Business Studies, 47(5), pp.535-562.

Hill, M., Price, R.A. and Ruch, G.W., 2018. An Alternative Approach to Distinguishing

Liabilities from Equity: Internal Capital versus External Capital. Available at SSRN 3086824.

Morningstar., (2019) BHP Group Ltd BHP [online]. Available from <

http://financials.morningstar.com/balance-sheet/bs.html?t=BHP®ion=aus&culture=en-US>

[Accessed on 26 Sep. 19].

Morningstar., (2019) Rio Tinto PLC ADR [online]. Available from <

http://financials.morningstar.com/balance-sheet/bs.html?t=RIO®ion=usa&culture=en-US>

[Accessed on 26 Sep. 19].

Corporate and Financial Accounting 11

Reid, W., 2018. The meaning of company accounts. UK: Routledge.

Rio Tinto., (2018) Annual Report 2018 [online]. Available from <

http://www.riotinto.com/documents/RT_2018_annual_report.pdf> [Accessed on 26 Sep. 19].

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Weinstein, S. and Barden, P., 2017. The complete guide to fundraising management. John Wiley

& Sons.

Reid, W., 2018. The meaning of company accounts. UK: Routledge.

Rio Tinto., (2018) Annual Report 2018 [online]. Available from <

http://www.riotinto.com/documents/RT_2018_annual_report.pdf> [Accessed on 26 Sep. 19].

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Weinstein, S. and Barden, P., 2017. The complete guide to fundraising management. John Wiley

& Sons.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.