Major Assignment: MAF101 Fundamentals of Finance - Trimester 1, 2019

VerifiedAdded on 2023/03/17

|14

|2639

|90

Homework Assignment

AI Summary

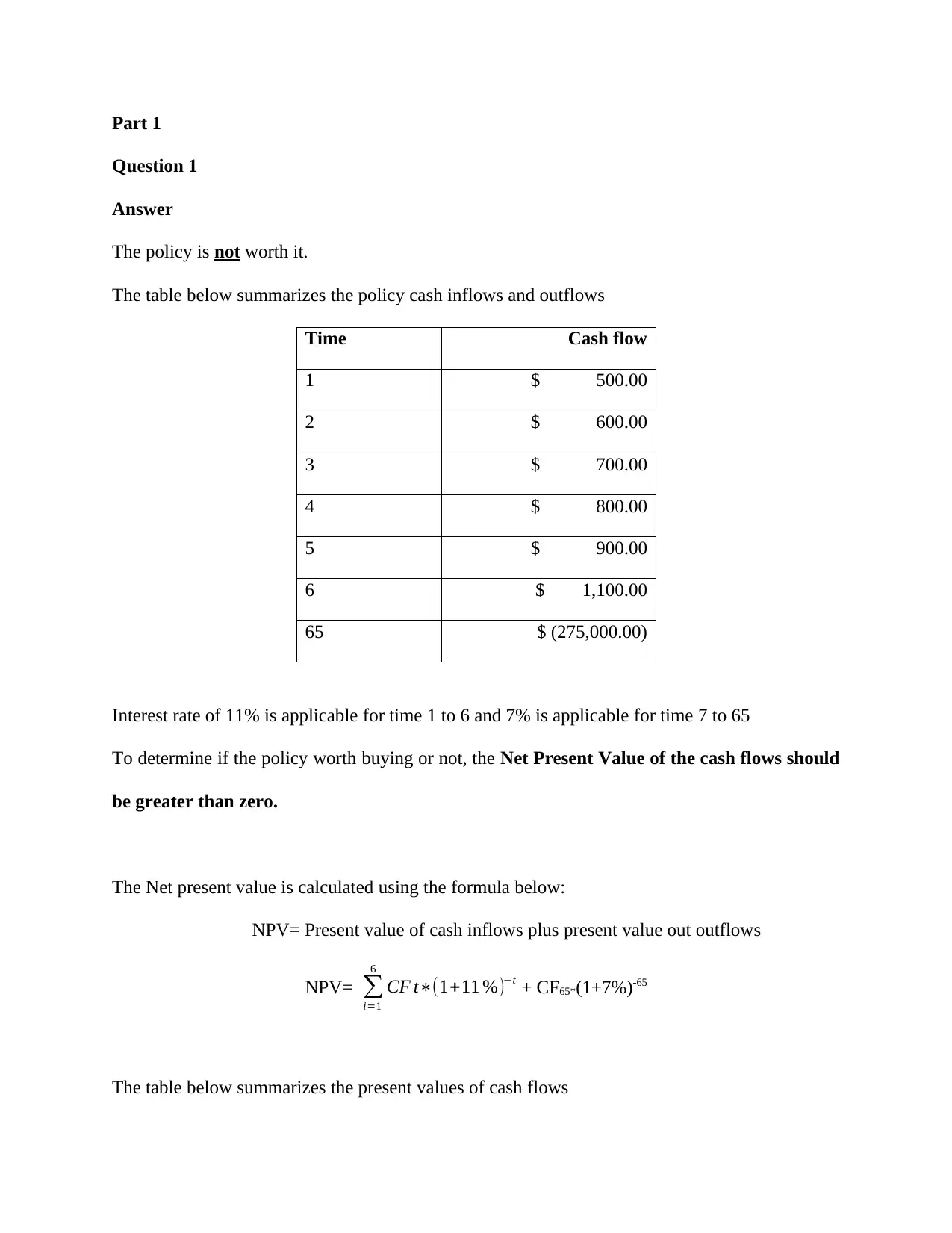

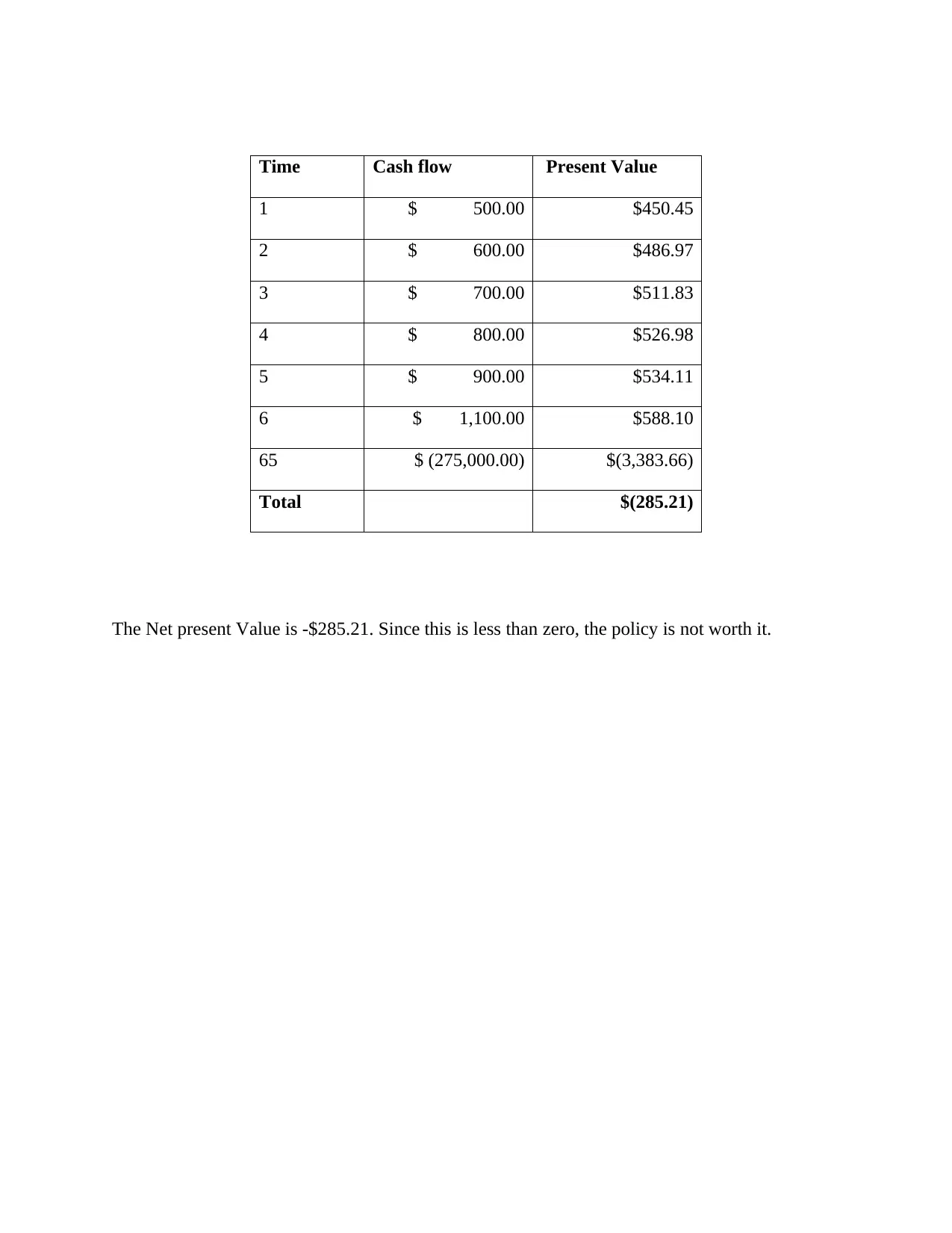

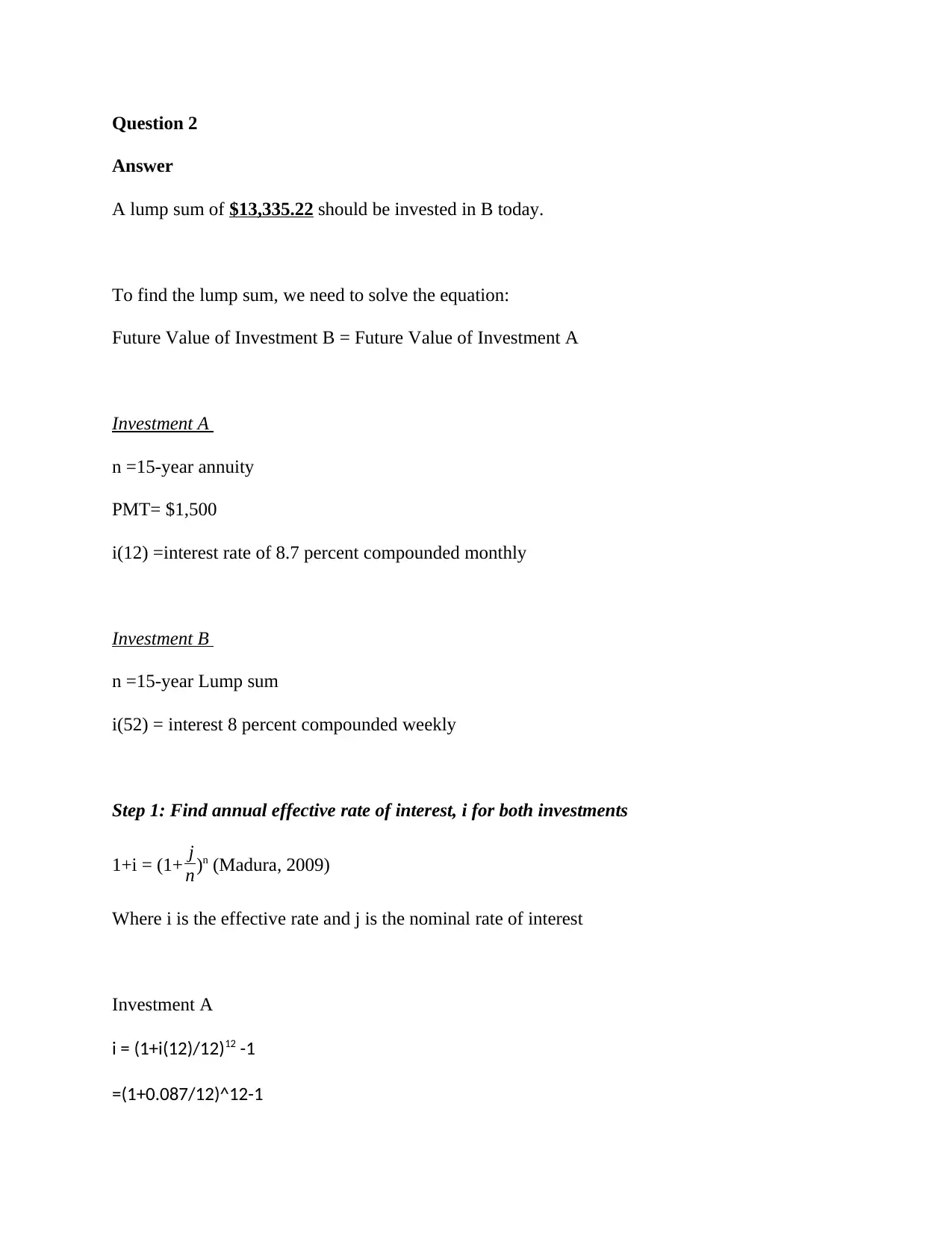

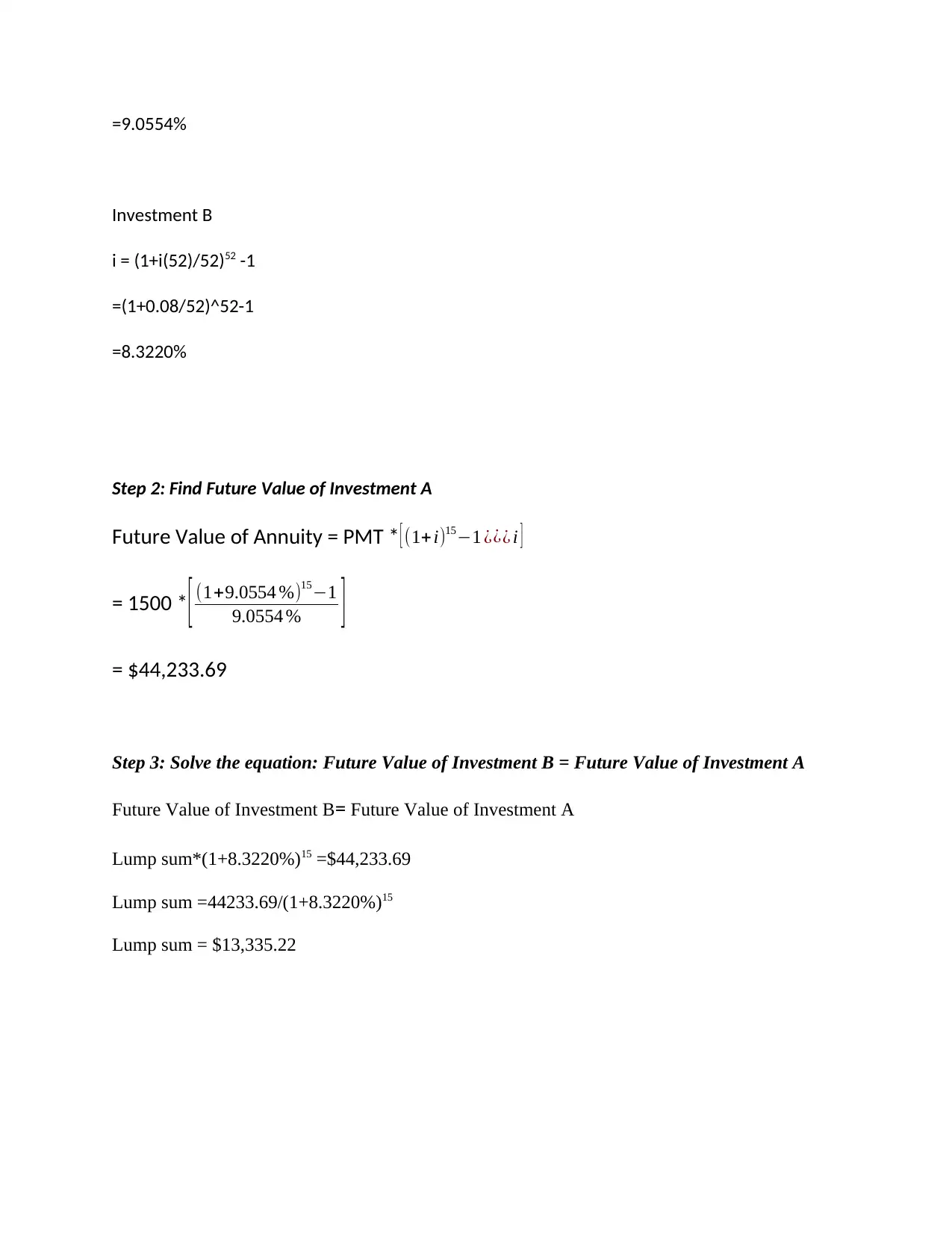

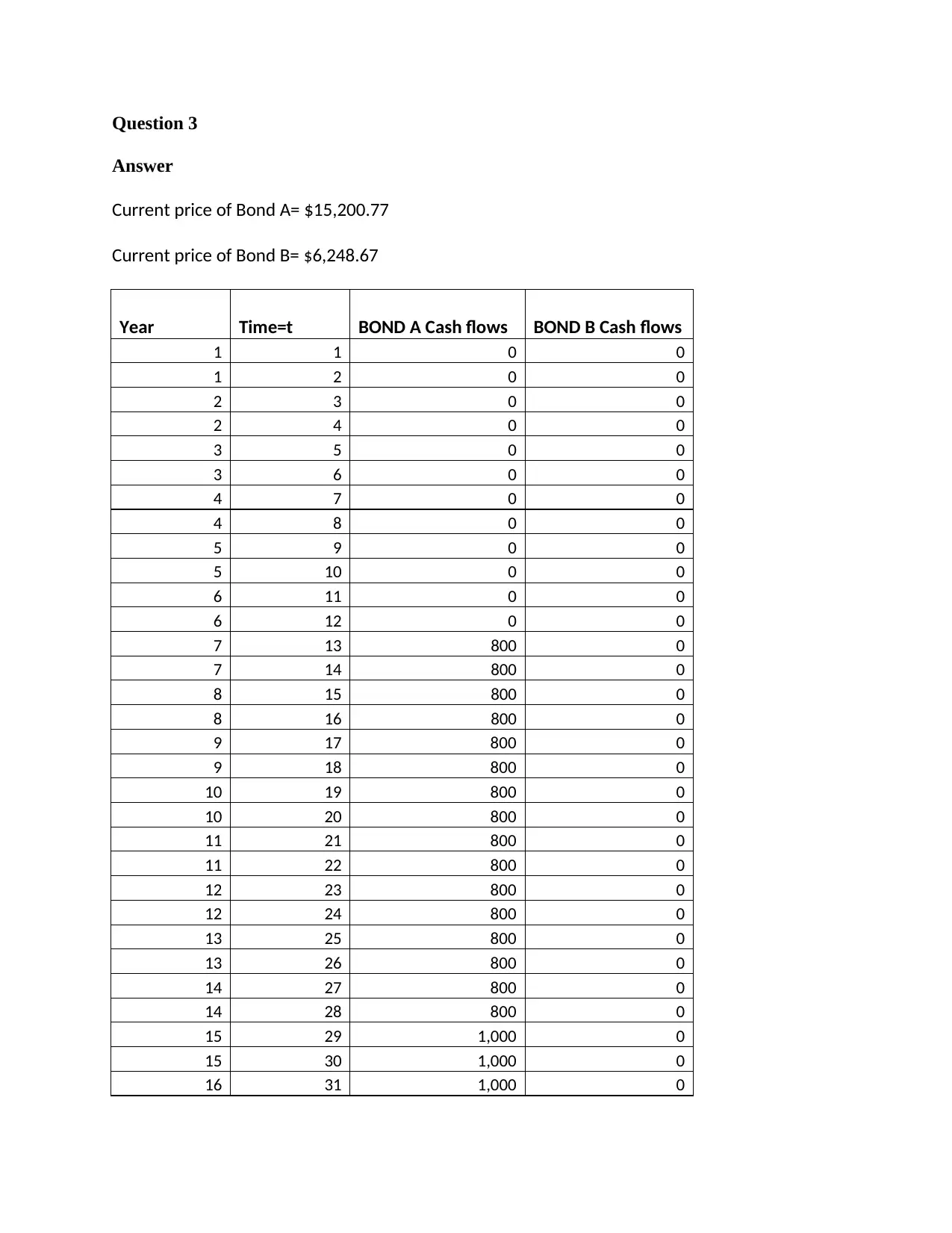

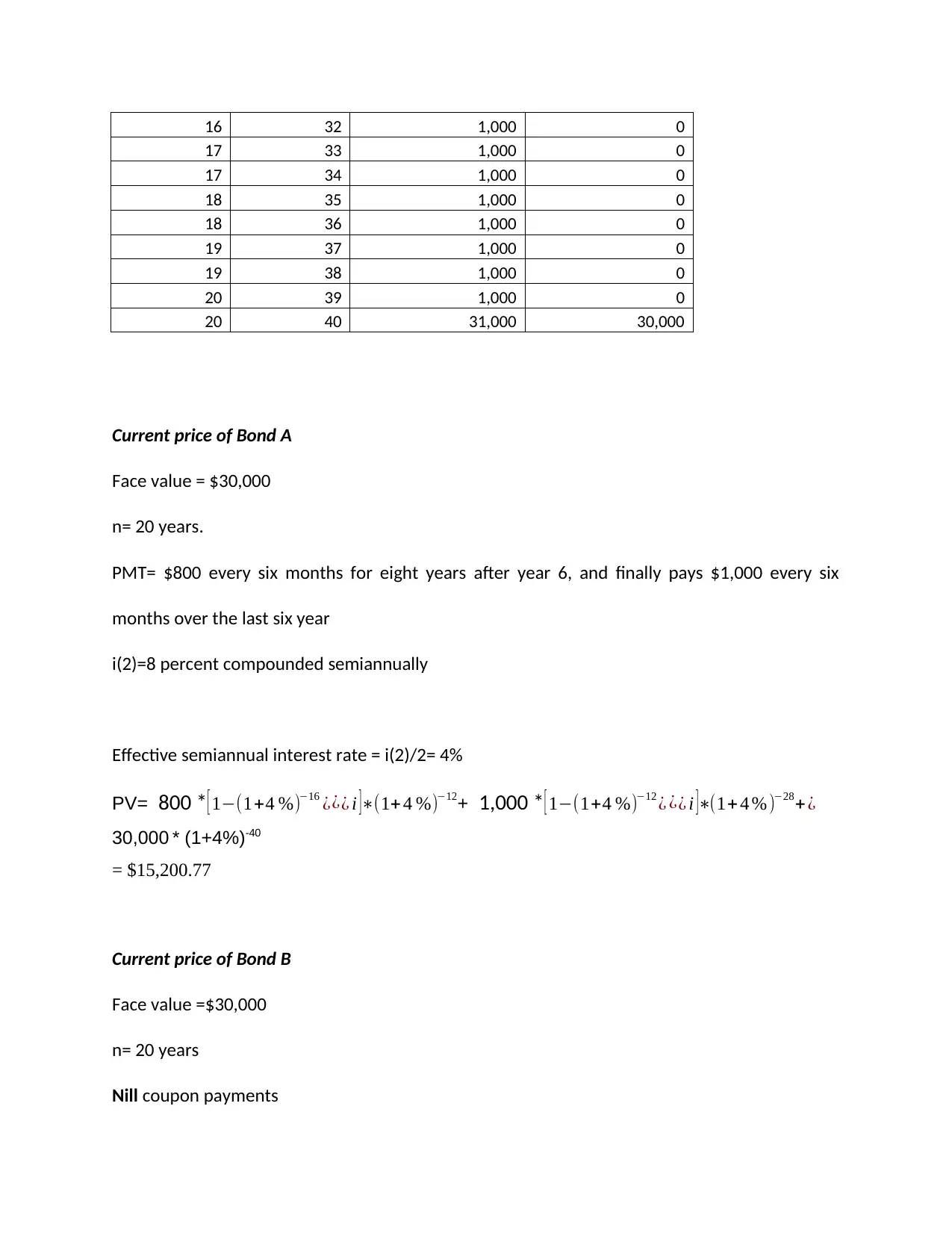

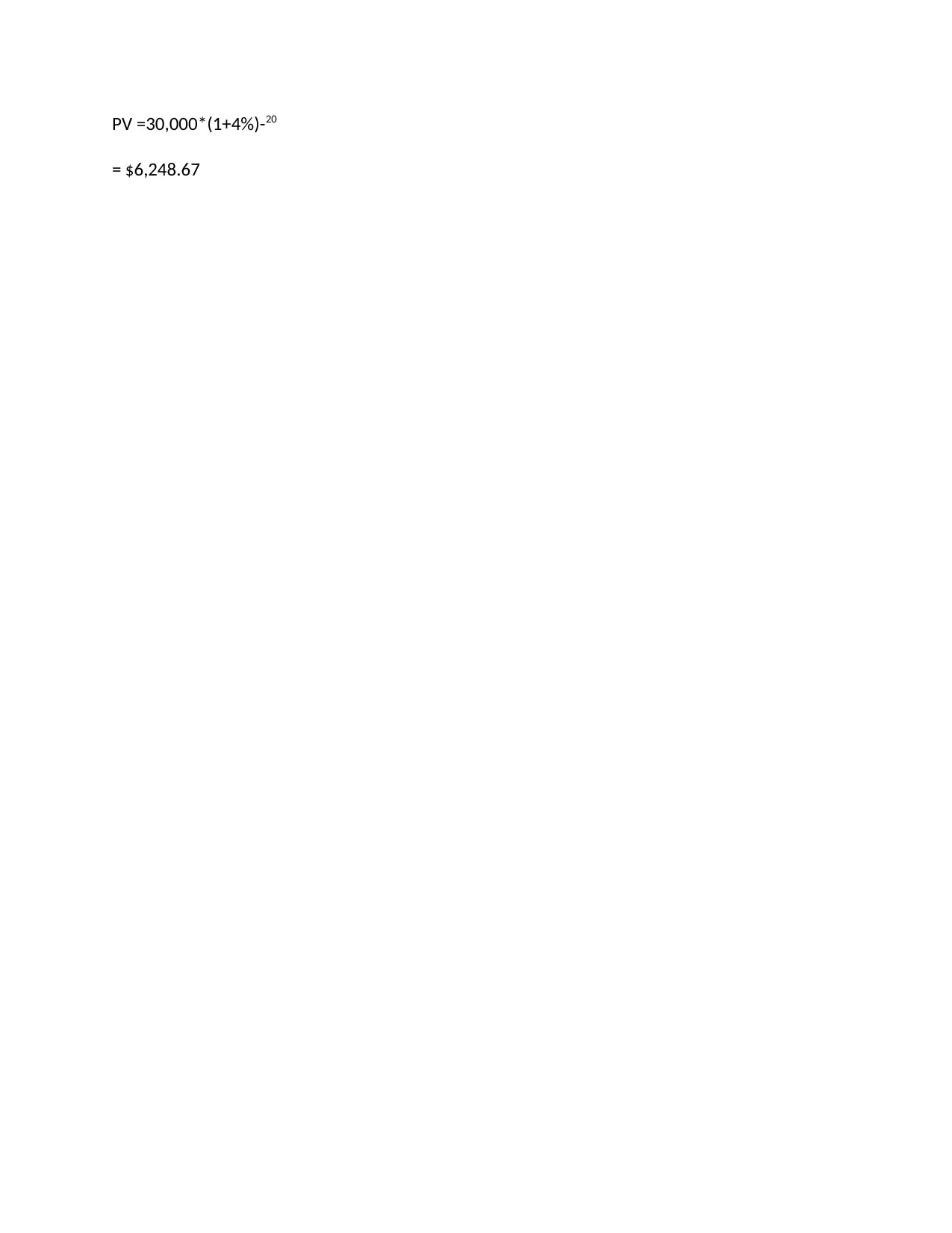

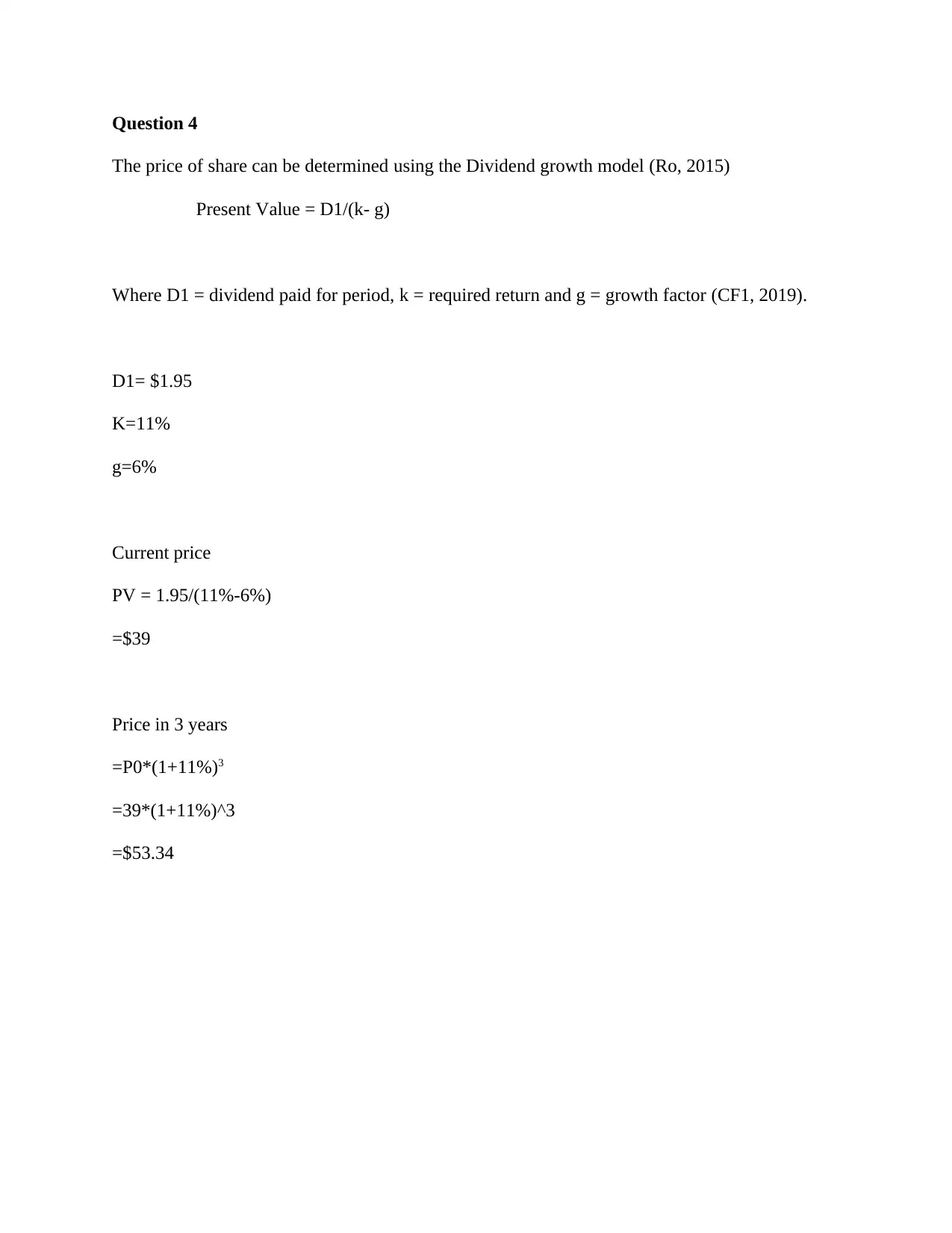

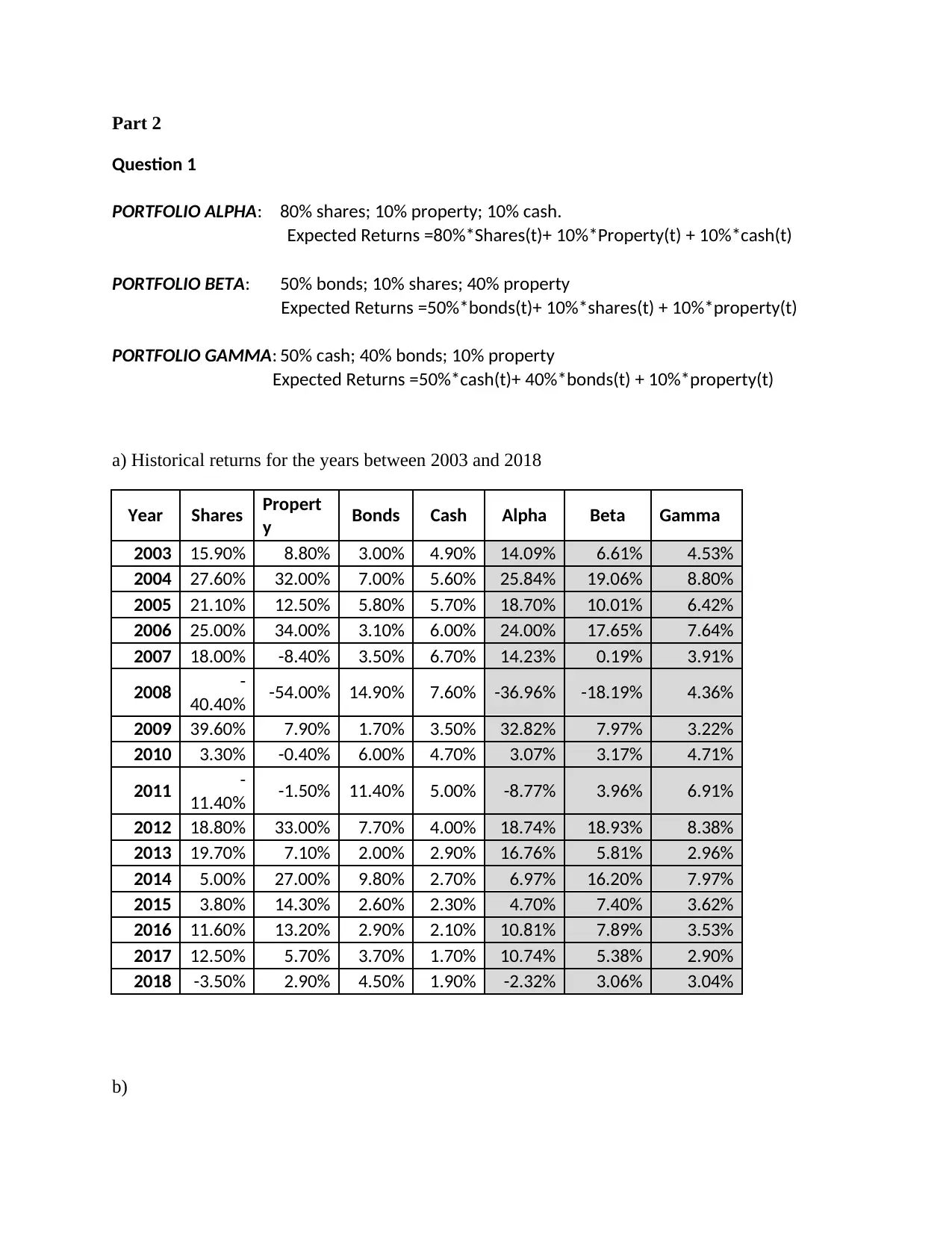

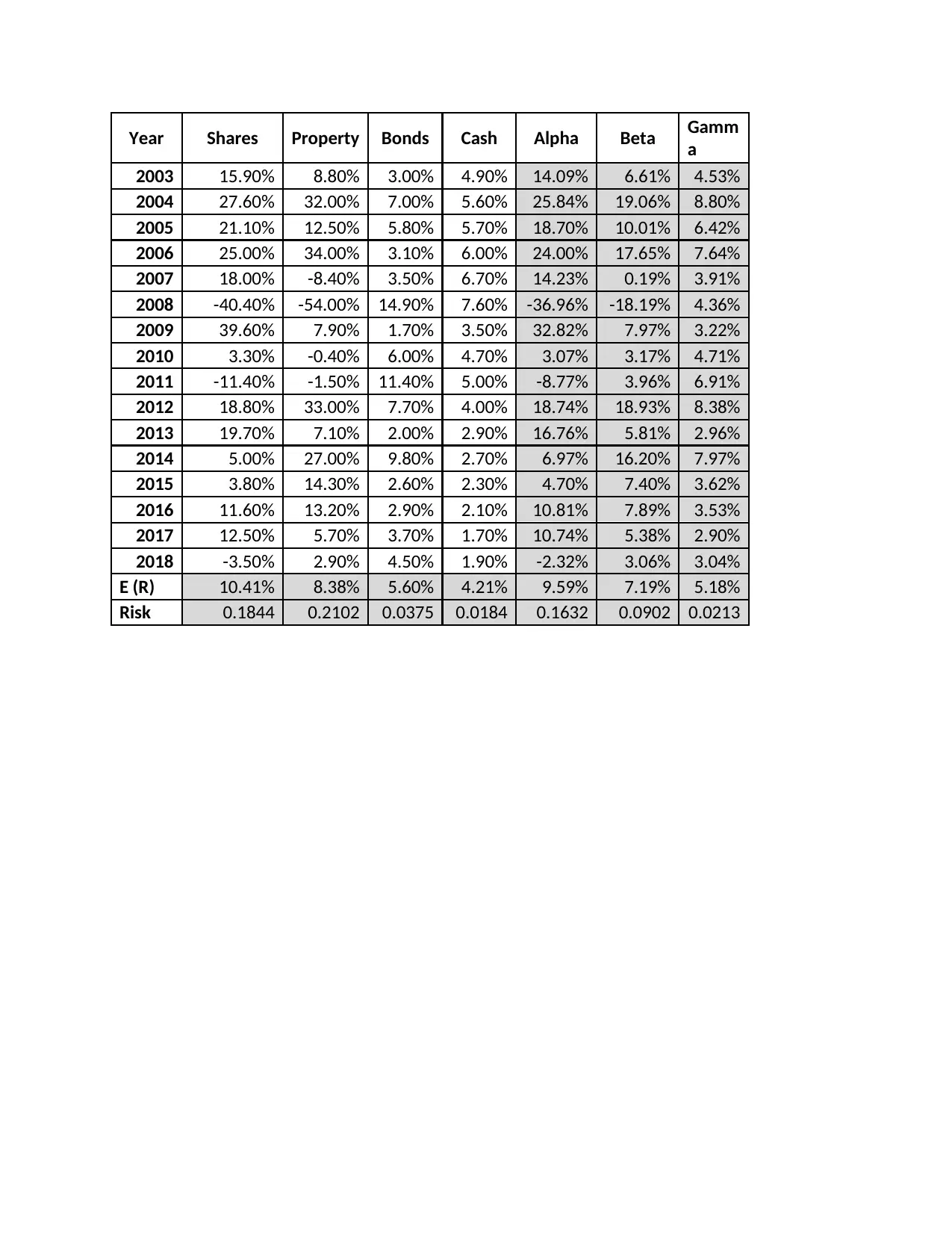

This assignment solution for MAF101, Fundamentals of Finance, covers several key financial concepts. Part 1 includes calculations for net present value, lump sum investments, bond pricing, and share valuation using the dividend growth model. Part 2 focuses on portfolio analysis, exploring the returns and risks associated with different investment strategies. It analyzes portfolio alpha, beta, and gamma, using historical data to assess risk and return profiles. The solution also addresses risk management principles, including diversifiable and non-diversifiable risks, the use of beta and standard deviation, and the implications of risk aversion. Finally, the assignment provides investment recommendations for different customer profiles based on their time horizons and risk tolerance.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.