Tax Consequences and Allowable Deductions

VerifiedAdded on 2019/09/20

|5

|1128

|397

Case Study

AI Summary

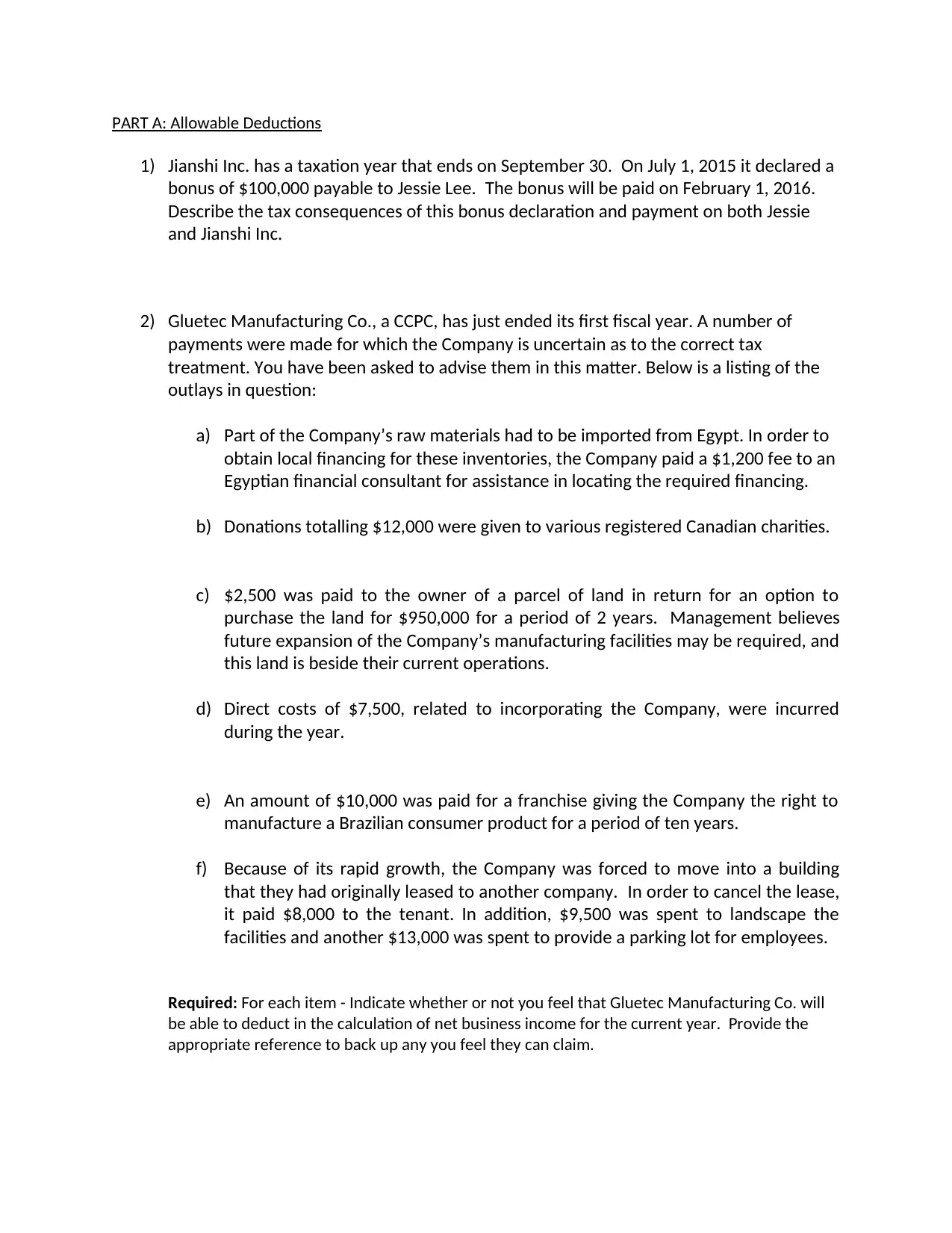

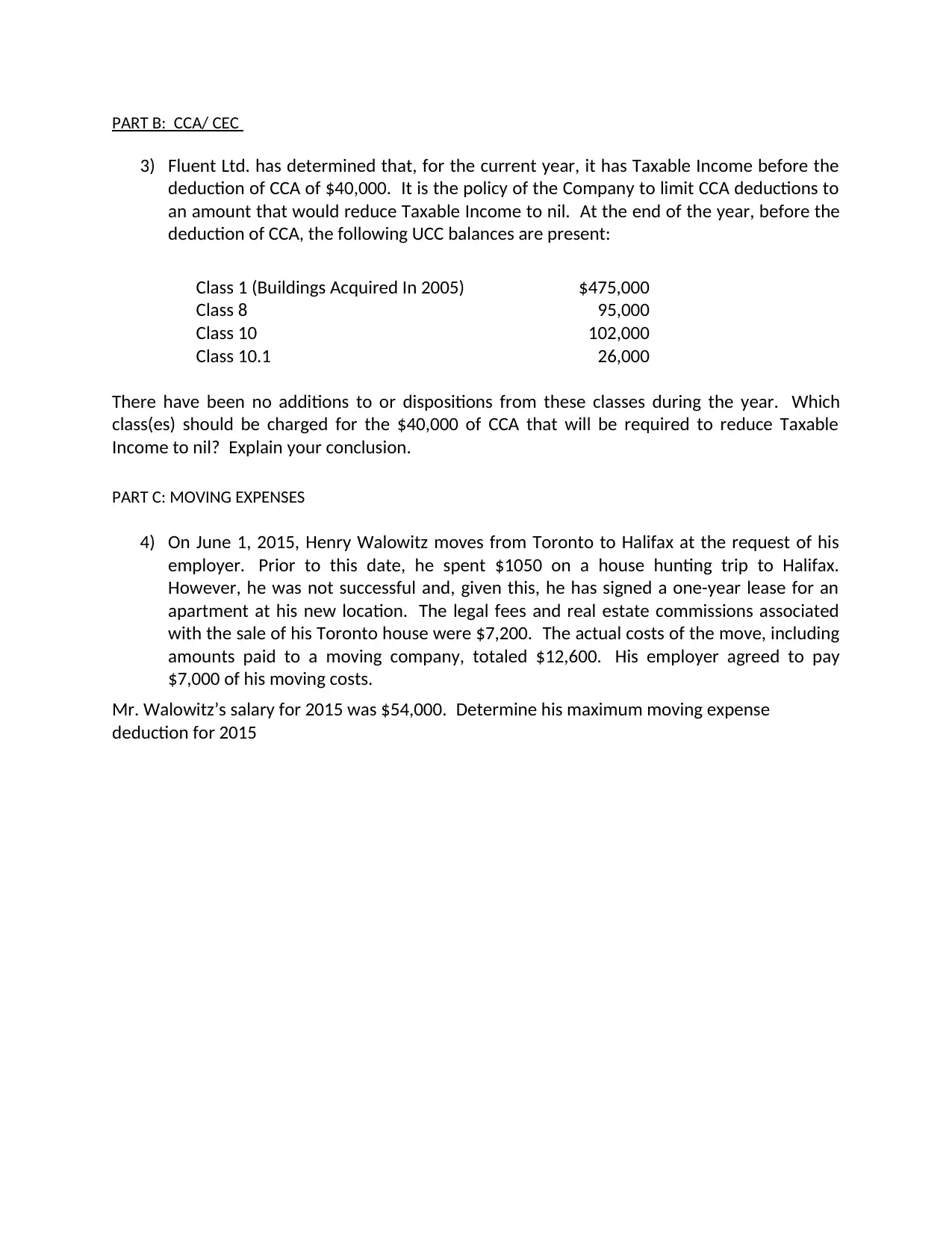

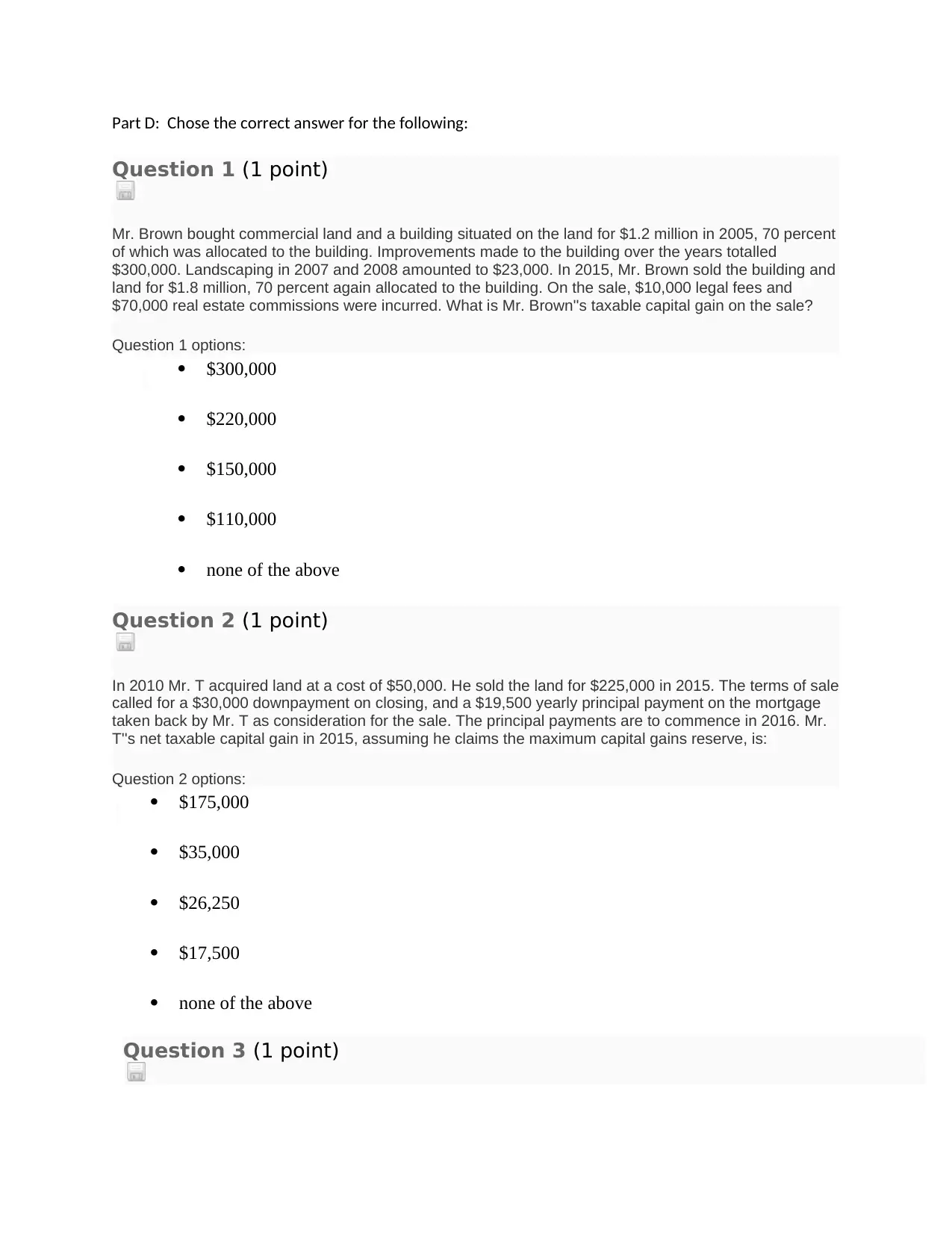

The assignment content consists of four parts: PART A - Allowable Deductions for Jianshi Inc. and Gluetec Manufacturing Co., discussing various outlays that may be deductible or not; PART B - CCA/CEC, where Fluent Ltd. has to determine the class(es) to charge for its CCA deductions; PART C - Moving Expenses, which involves Henry Walowitz's relocation from Toronto to Halifax and his employer's contribution towards his moving costs; and PART D - Chose the correct answer for five questions on various taxation topics, including capital gains and losses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.