Tax Implications of Deductions and Capital Gains Analysis

VerifiedAdded on 2019/09/20

|5

|1128

|397

Homework Assignment

AI Summary

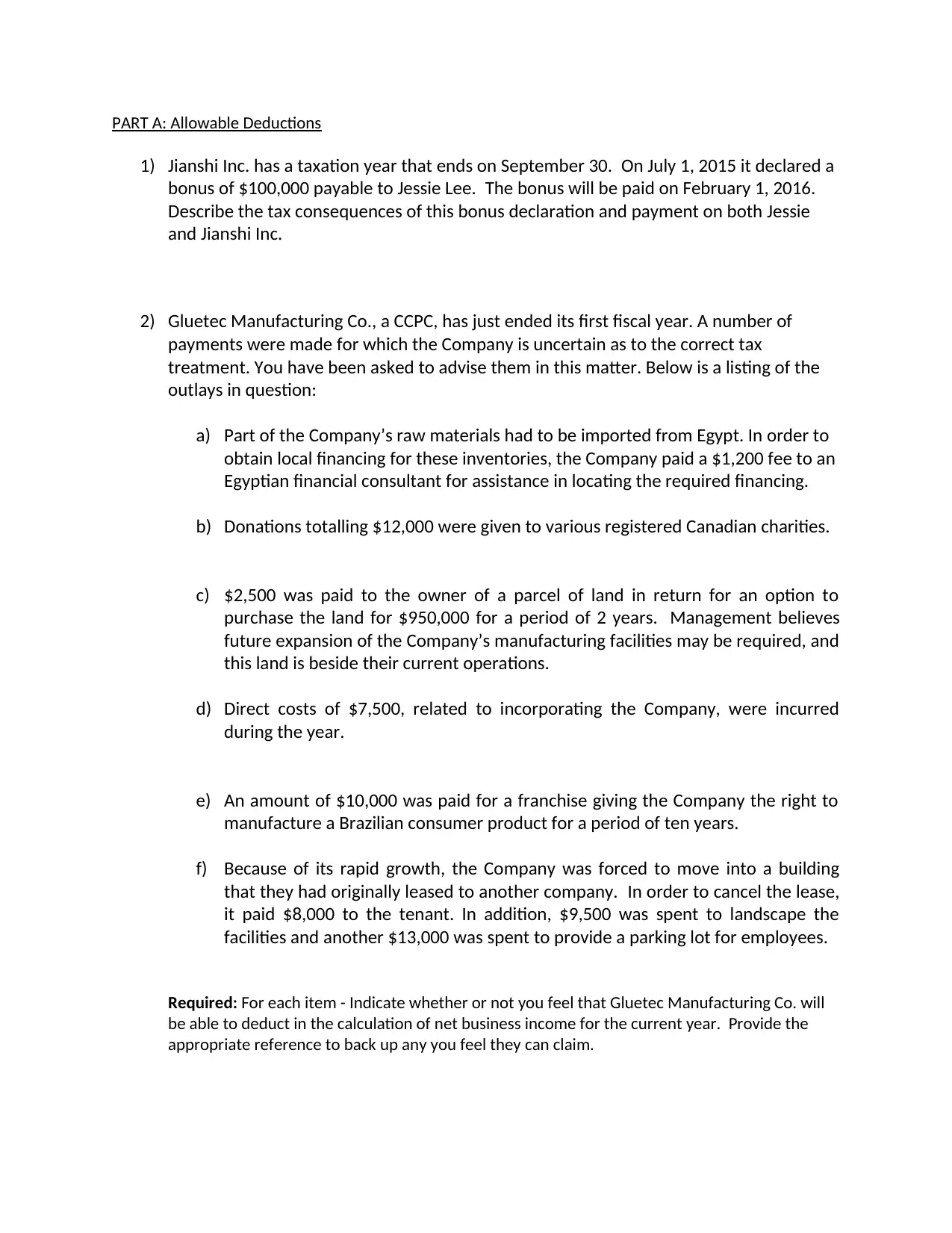

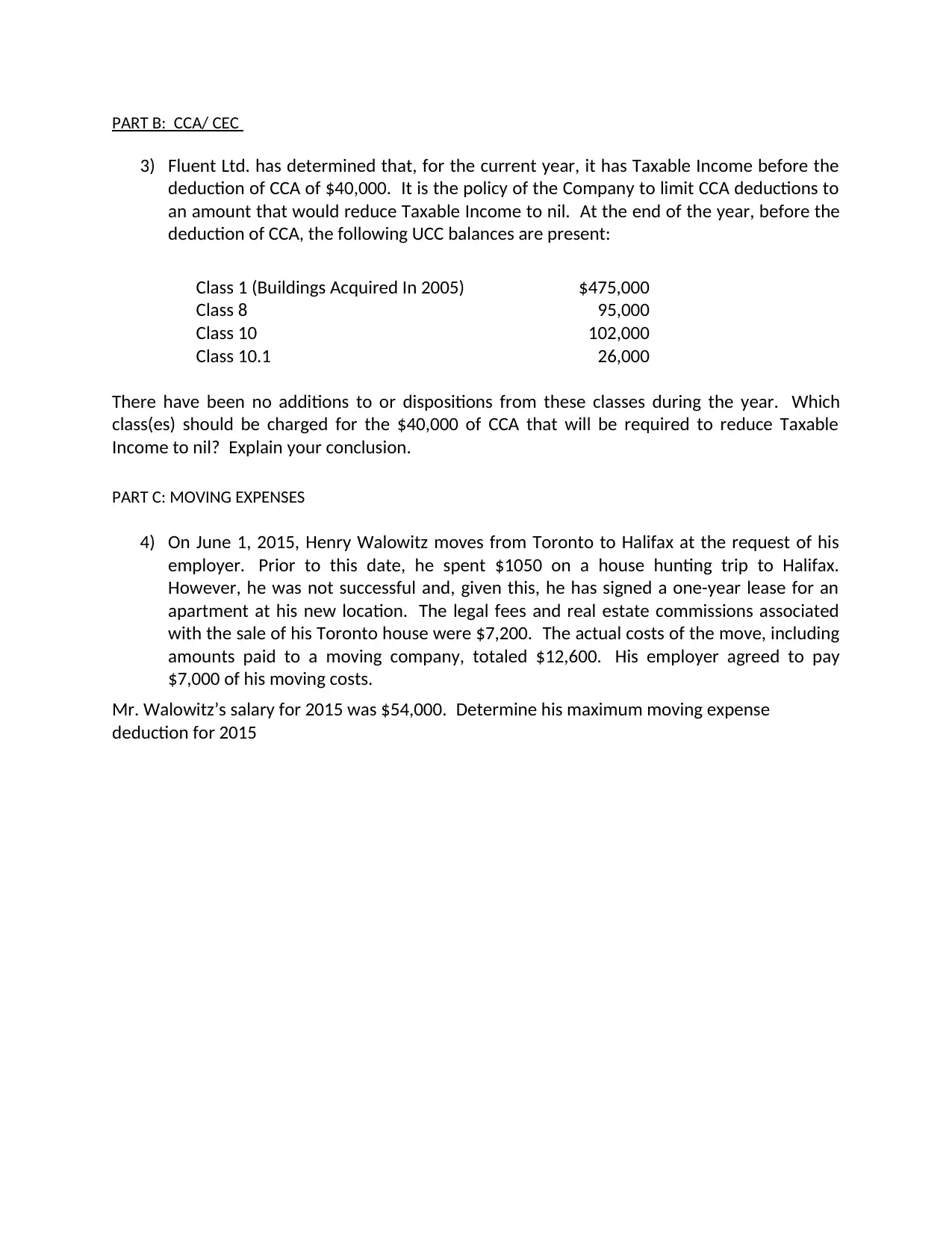

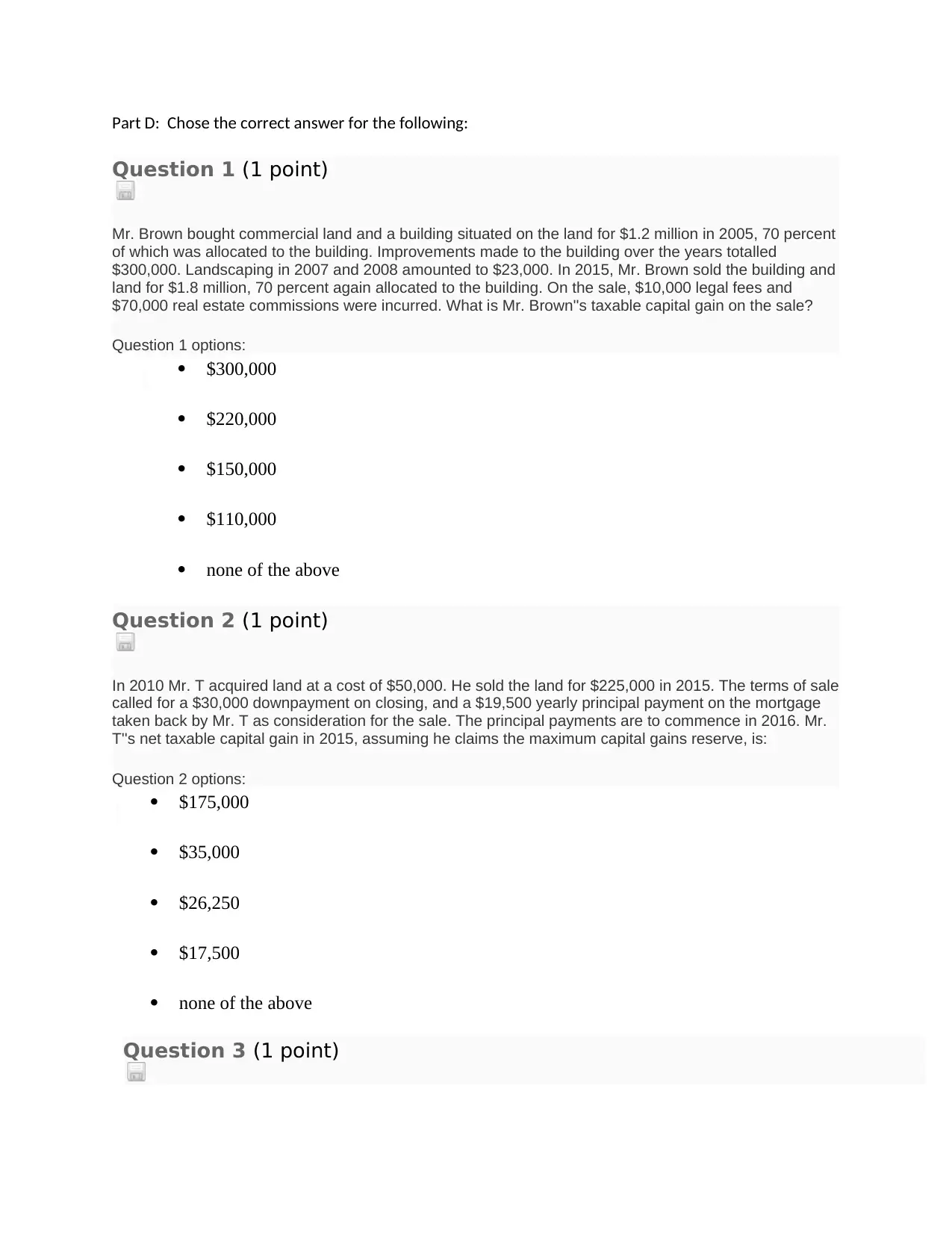

This assignment addresses several aspects of Canadian corporate and personal taxation. Part A analyzes the tax consequences of a bonus declaration and payment for Jianshi Inc. and Jessie Lee, and examines the deductibility of various expenses for Gluetec Manufacturing Co. Part B focuses on Capital Cost Allowance (CCA) calculations, determining which asset classes should be charged to reduce taxable income to zero for Fluent Ltd. Part C deals with moving expenses, calculating the maximum moving expense deduction for Henry Walowitz. Finally, Part D presents multiple-choice questions on capital gains, including the sale of land and buildings, and the treatment of principal residences. The assignment covers a range of tax topics, including allowable deductions, CCA, moving expenses, and capital gains.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.