Investment Decisions Analysis

5 Pages1556 Words43 Views

Added on 2020-05-11

Investment Decisions Analysis

Added on 2020-05-11

ShareRelated Documents

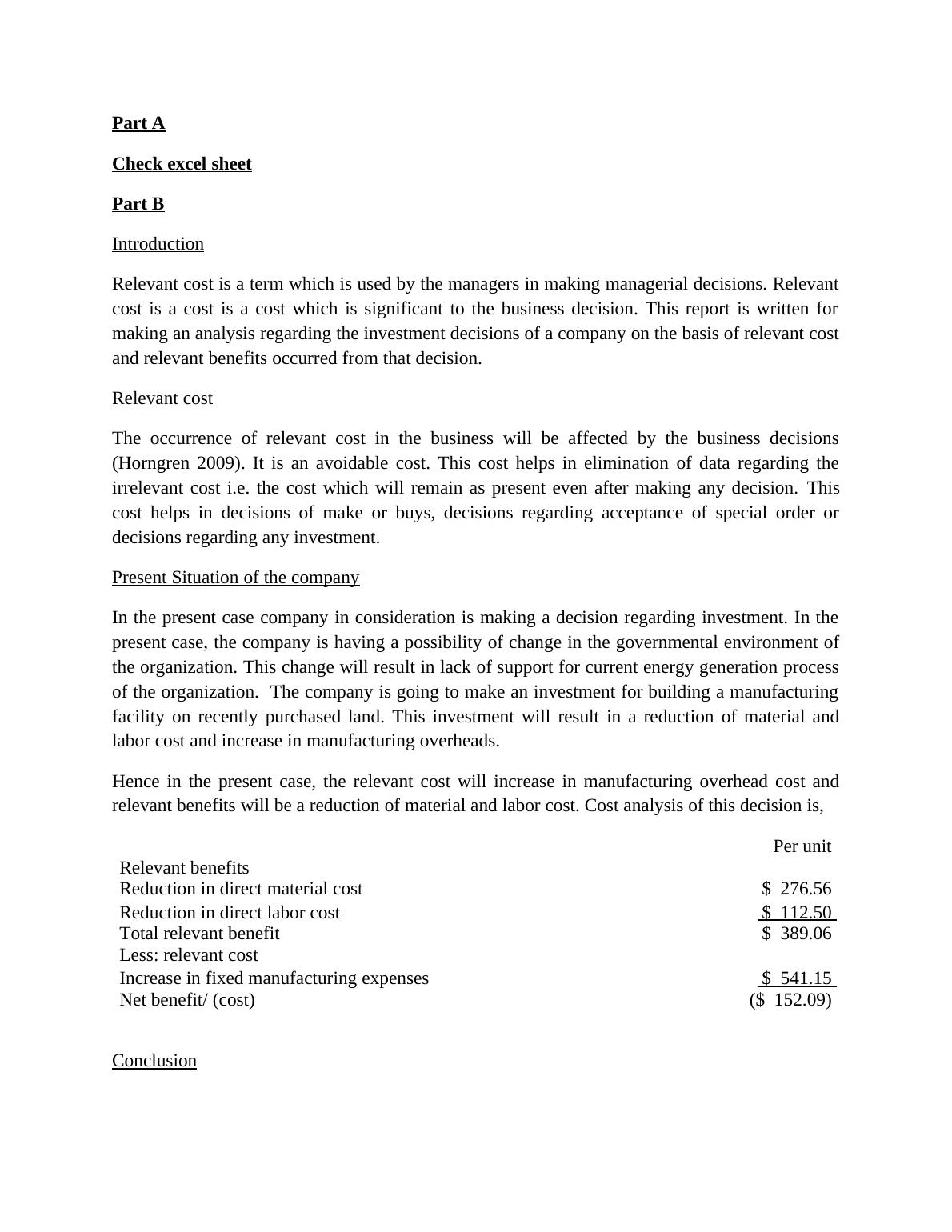

Part ACheck excel sheetPart BIntroductionRelevant cost is a term which is used by the managers in making managerial decisions. Relevantcost is a cost is a cost which is significant to the business decision. This report is written formaking an analysis regarding the investment decisions of a company on the basis of relevant costand relevant benefits occurred from that decision.Relevant costThe occurrence of relevant cost in the business will be affected by the business decisions[ CITATION Hor092 \l 1033 ]. It is an avoidable cost. This cost helps in elimination of data regardingthe irrelevant cost i.e. the cost which will remain as present even after making any decision. Thiscost helps in decisions of make or buys, decisions regarding acceptance of special order ordecisions regarding any investment.Present Situation of the companyIn the present case company in consideration is making a decision regarding investment. In thepresent case, the company is having a possibility of change in the governmental environment ofthe organization. This change will result in lack of support for current energy generation processof the organization. The company is going to make an investment for building a manufacturingfacility on recently purchased land. This investment will result in a reduction of material andlabor cost and increase in manufacturing overheads.Hence in the present case, the relevant cost will increase in manufacturing overhead cost andrelevant benefits will be a reduction of material and labor cost. Cost analysis of this decision is,Per unit Relevant benefitsReduction in direct material cost $ 276.56 Reduction in direct labor cost $ 112.50 Total relevant benefit $ 389.06 Less: relevant costIncrease in fixed manufacturing expenses $ 541.15 Net benefit/ (cost)($ 152.09) Conclusion

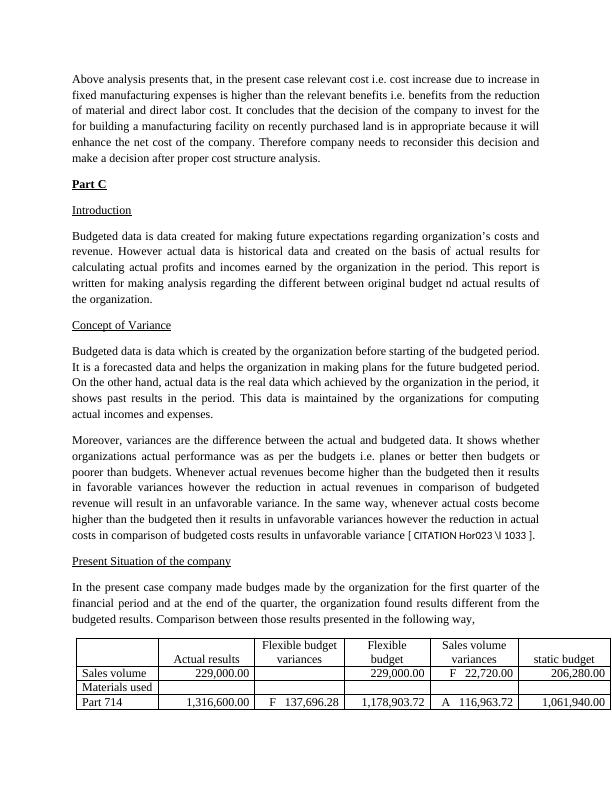

Above analysis presents that, in the present case relevant cost i.e. cost increase due to increase infixed manufacturing expenses is higher than the relevant benefits i.e. benefits from the reductionof material and direct labor cost. It concludes that the decision of the company to invest for thefor building a manufacturing facility on recently purchased land is in appropriate because it willenhance the net cost of the company. Therefore company needs to reconsider this decision andmake a decision after proper cost structure analysis.Part CIntroductionBudgeted data is data created for making future expectations regarding organization’s costs andrevenue. However actual data is historical data and created on the basis of actual results forcalculating actual profits and incomes earned by the organization in the period. This report iswritten for making analysis regarding the different between original budget nd actual results ofthe organization.Concept of VarianceBudgeted data is data which is created by the organization before starting of the budgeted period.It is a forecasted data and helps the organization in making plans for the future budgeted period.On the other hand, actual data is the real data which achieved by the organization in the period, itshows past results in the period. This data is maintained by the organizations for computingactual incomes and expenses.Moreover, variances are the difference between the actual and budgeted data. It shows whetherorganizations actual performance was as per the budgets i.e. planes or better then budgets orpoorer than budgets. Whenever actual revenues become higher than the budgeted then it resultsin favorable variances however the reduction in actual revenues in comparison of budgetedrevenue will result in an unfavorable variance. In the same way, whenever actual costs becomehigher than the budgeted then it results in unfavorable variances however the reduction in actualcosts in comparison of budgeted costs results in unfavorable variance [ CITATION Hor023 \l 1033 ].Present Situation of the companyIn the present case company made budges made by the organization for the first quarter of thefinancial period and at the end of the quarter, the organization found results different from thebudgeted results. Comparison between those results presented in the following way,Actual resultsFlexible budgetvariancesFlexiblebudgetSales volumevariancesstatic budgetSales volume229,000.00 229,000.00 F 22,720.00 206,280.00 Materials usedPart 7141,316,600.00 F 137,696.28 1,178,903.72 A 116,963.72 1,061,940.00

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Different Types of Management Accounting Informationlg...

|15

|906

|88

Assignment Economics and Financelg...

|12

|2114

|154

Modern Cost Management Accountinglg...

|5

|1179

|29

Report On Nature & Role Of Management Accountinglg...

|19

|5154

|43

Analysis of cost of Exquisite using absorption costinglg...

|19

|5677

|54

Accounting and Financial Managementlg...

|10

|1978

|88