Financial Performance Analysis: Ariel Ltd. vs Snowy Ltd. Report

VerifiedAdded on 2019/10/18

|5

|717

|165

Report

AI Summary

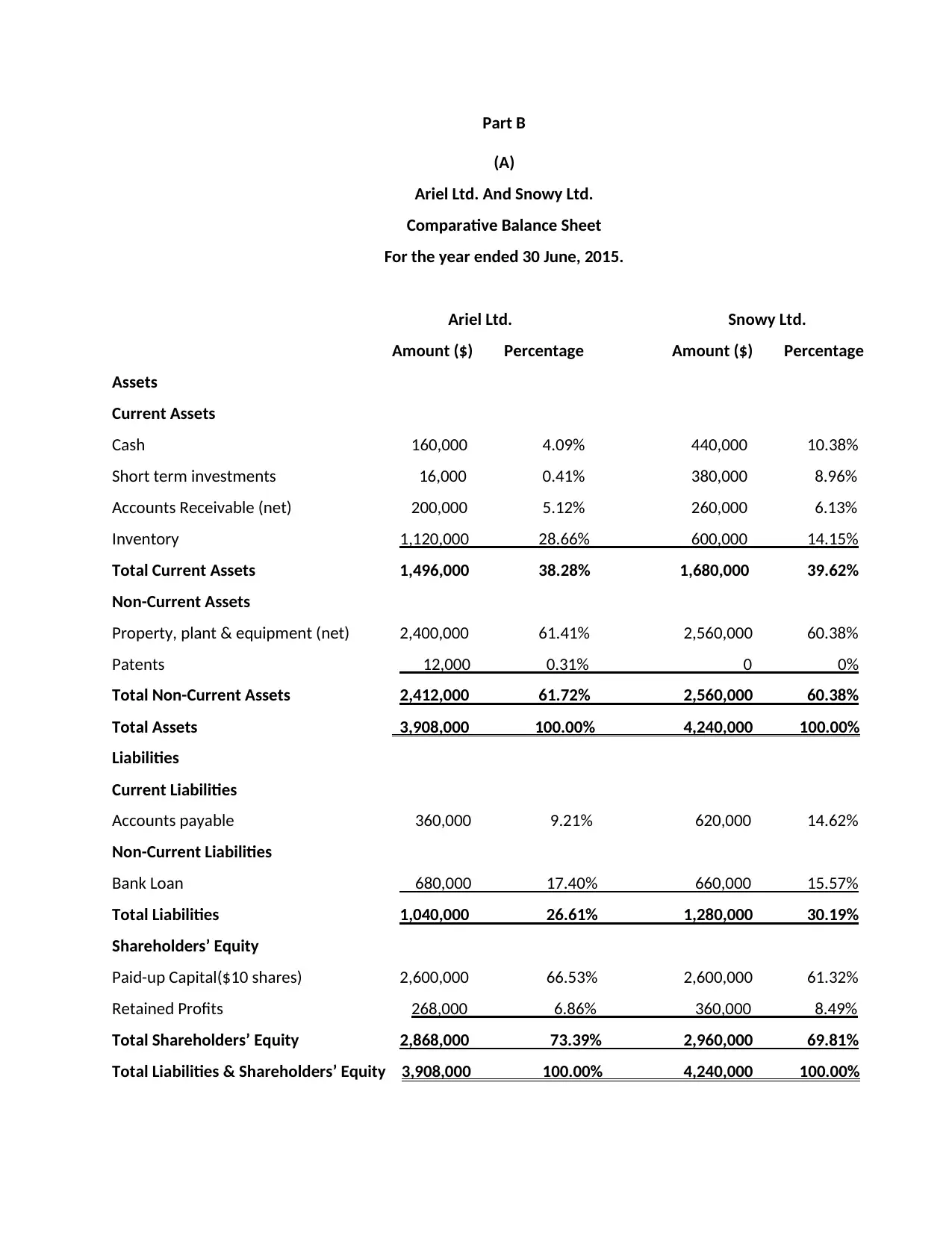

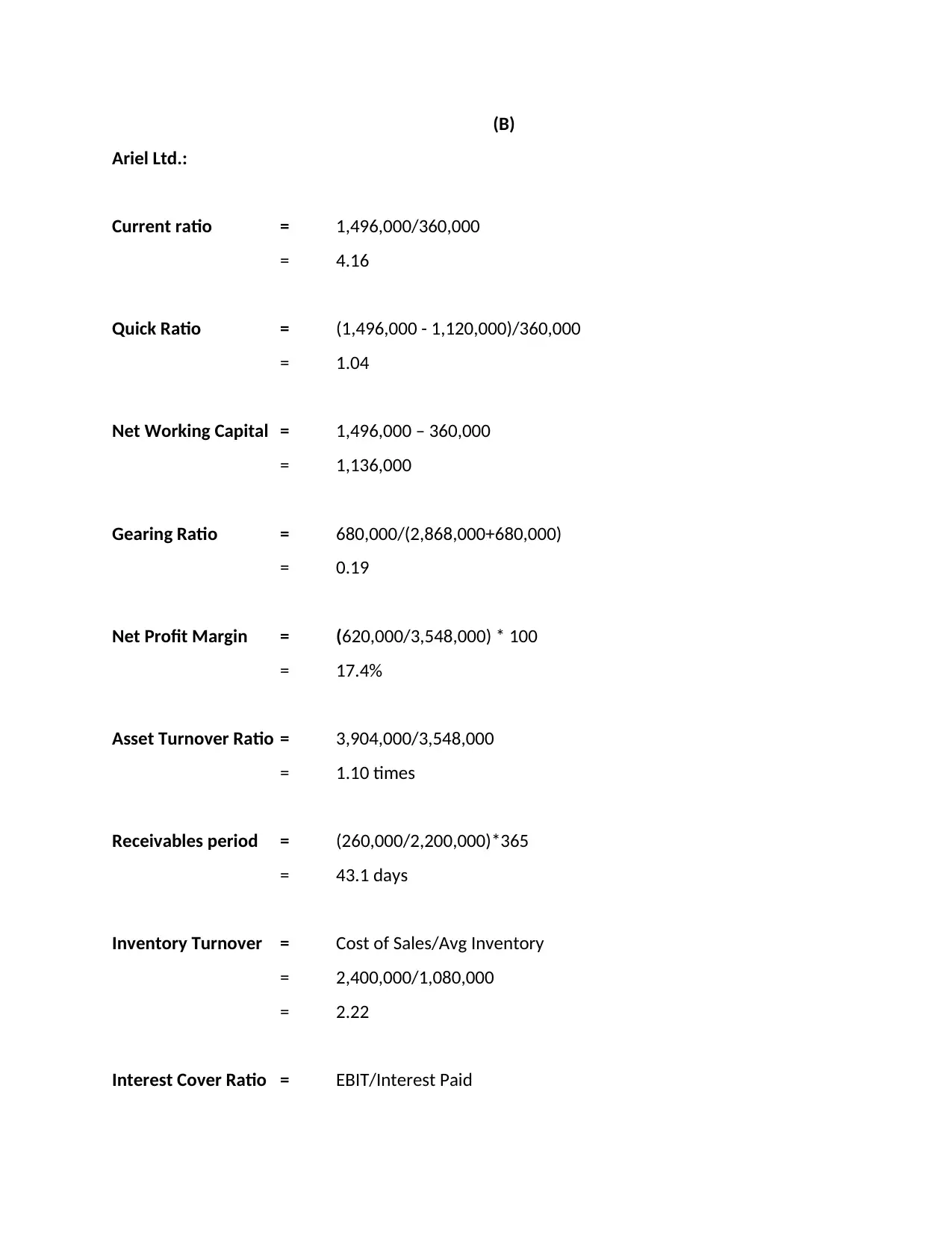

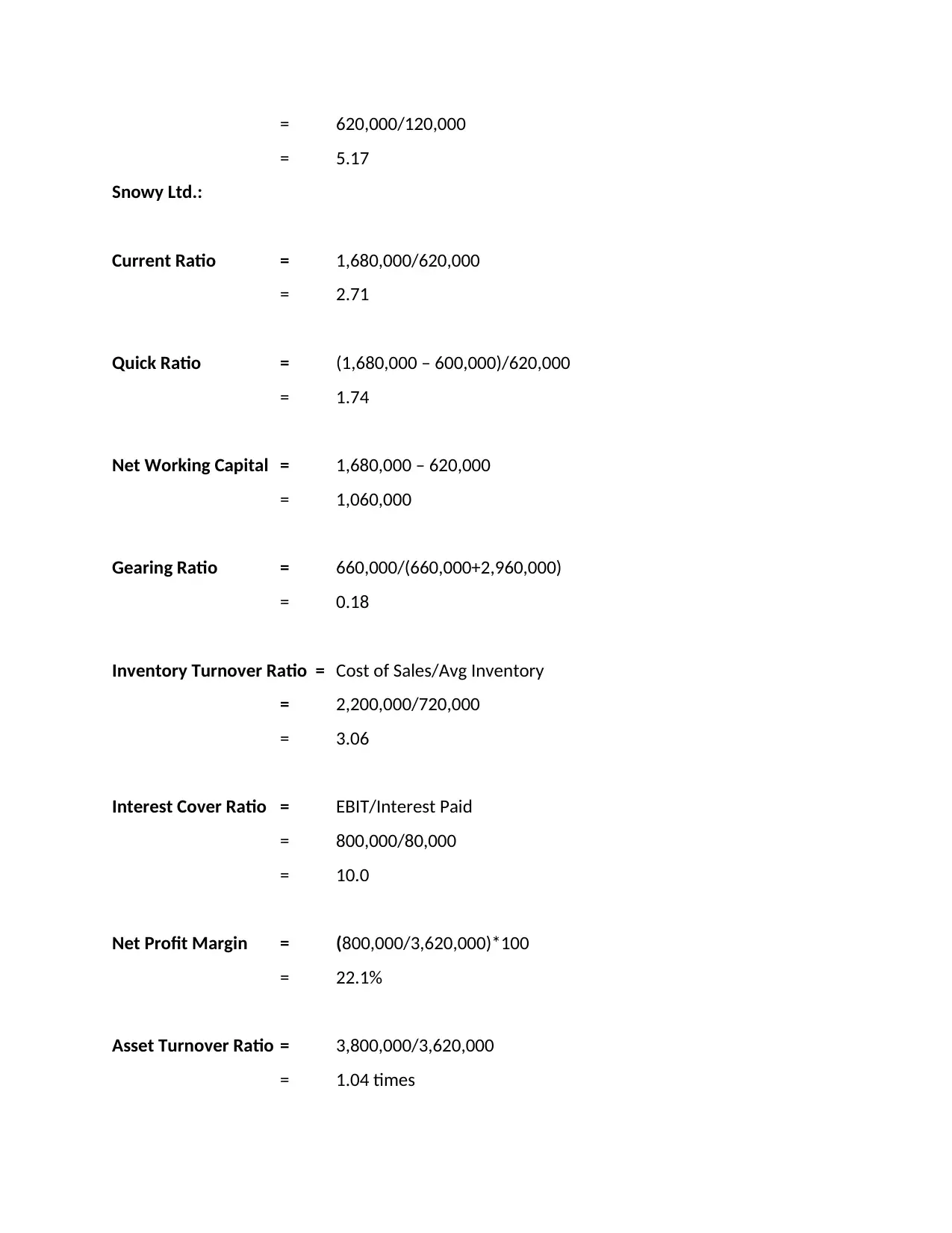

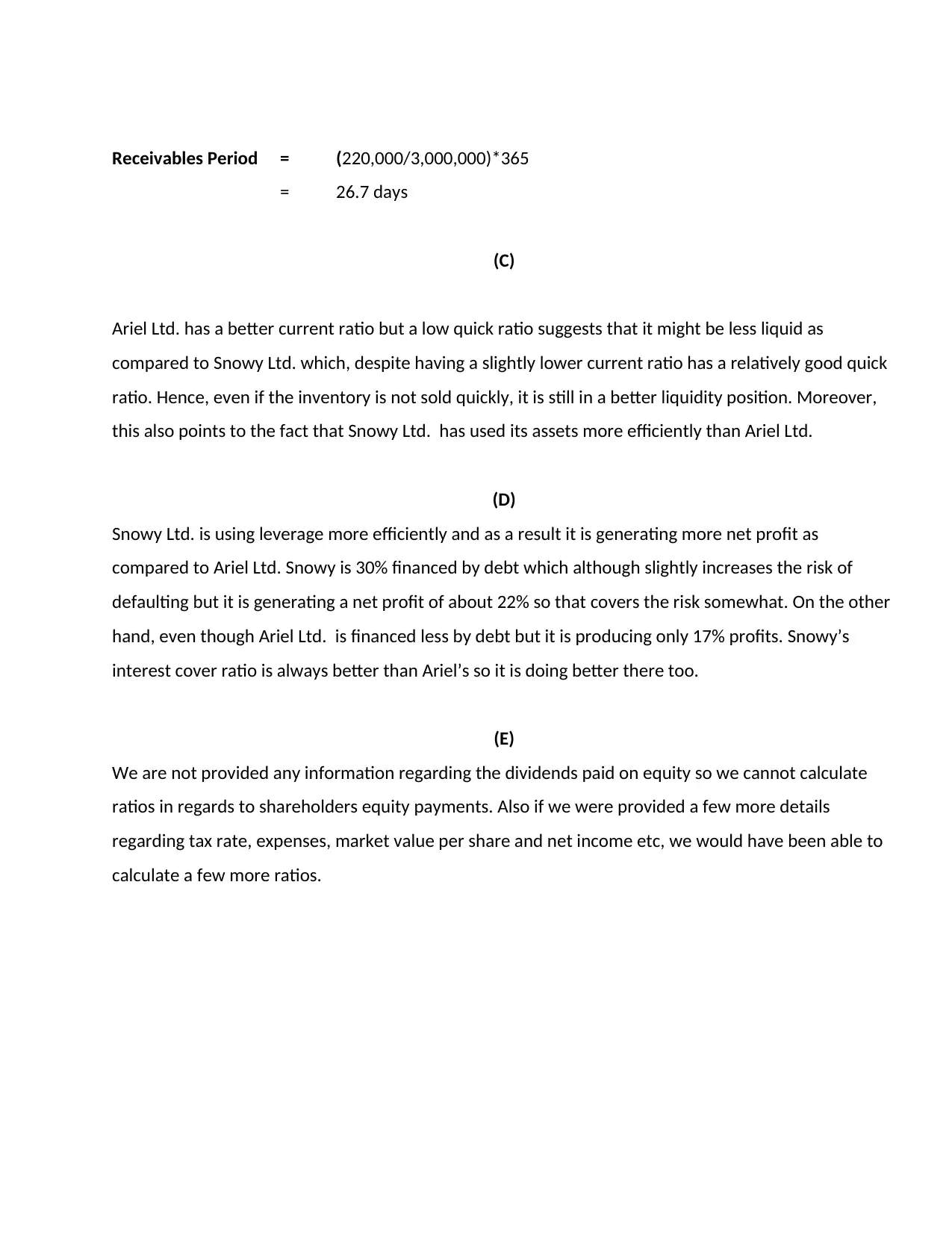

This report presents a comparative financial analysis of Ariel Ltd. and Snowy Ltd. for the year ended June 30, 2015. It begins with a detailed comparison of their balance sheets, including current and non-current assets, liabilities, and shareholders' equity, with percentage breakdowns. The report then calculates and compares key financial ratios for both companies, such as current ratio, quick ratio, net working capital, gearing ratio, net profit margin, asset turnover ratio, receivables period, inventory turnover ratio, and interest cover ratio. The analysis highlights differences in liquidity, efficiency, and profitability, with Snowy Ltd. demonstrating stronger performance in several areas. The report also provides an accountant's perspective on transaction analysis and the importance of financial reporting in assessing a company's performance. Finally, the report acknowledges the limitations due to missing data, such as dividend information and additional financial details like tax rates and market value per share, which would have allowed for a more comprehensive ratio analysis.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.