Analyzing Financial Ratios and Investment Decisions for RT plc

VerifiedAdded on 2023/06/08

|7

|1472

|294

Report

AI Summary

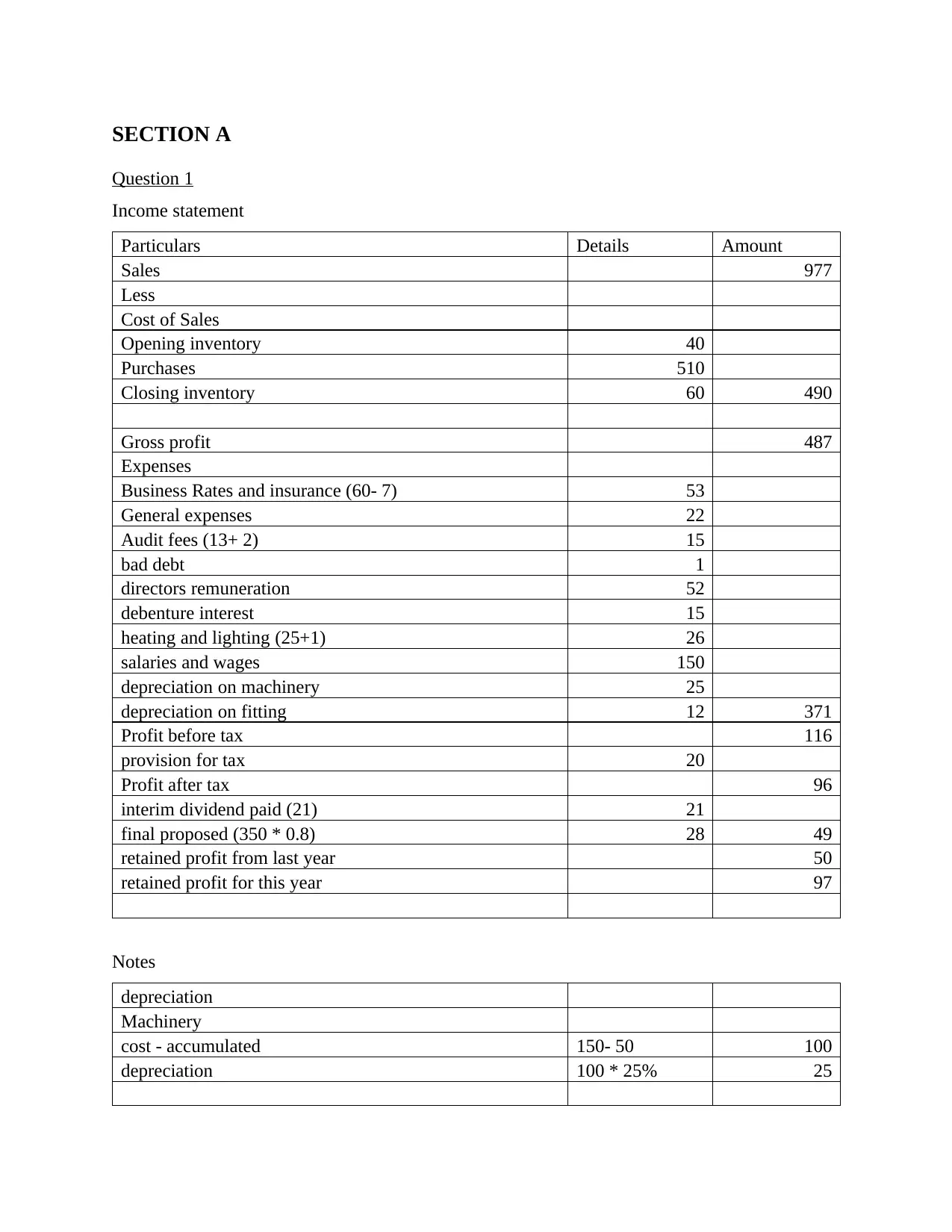

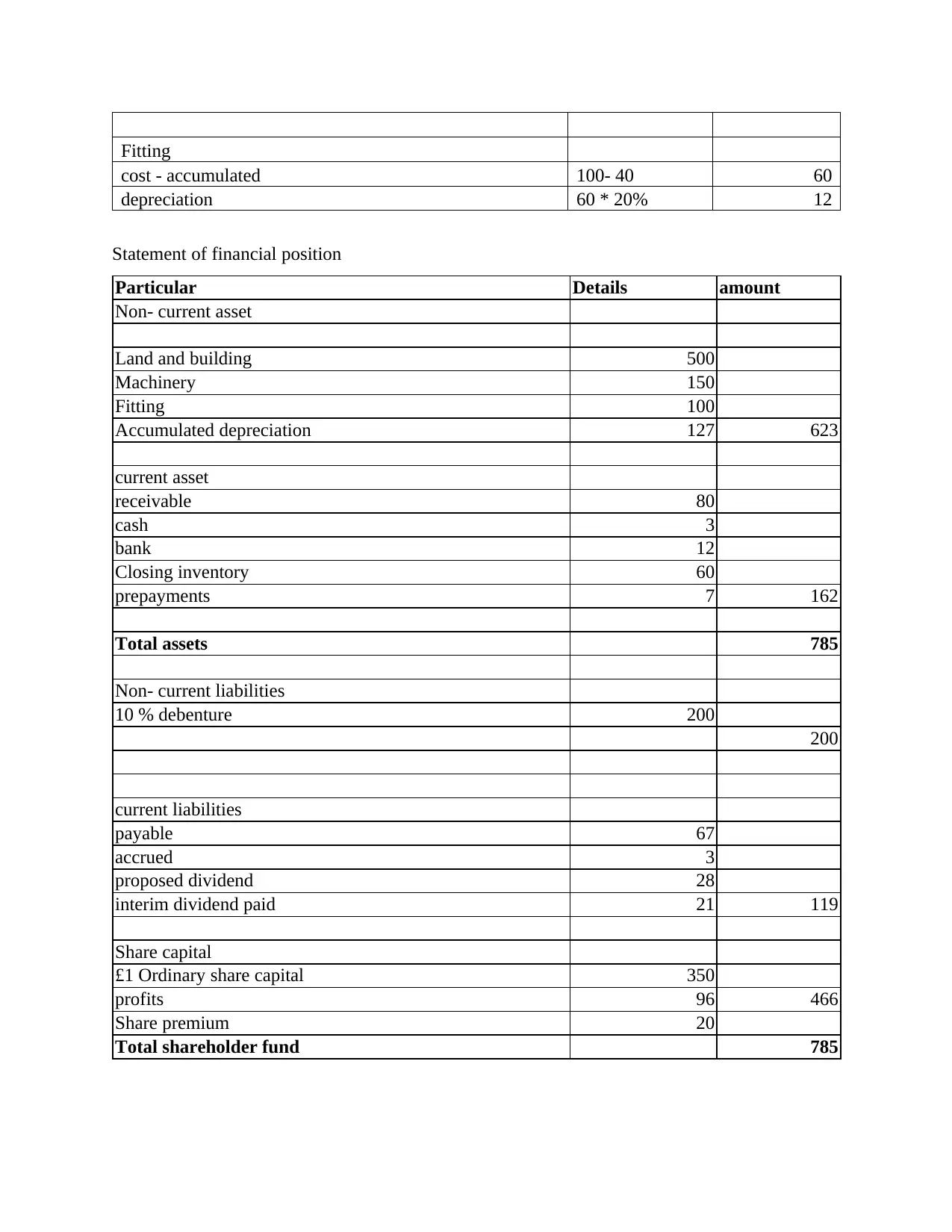

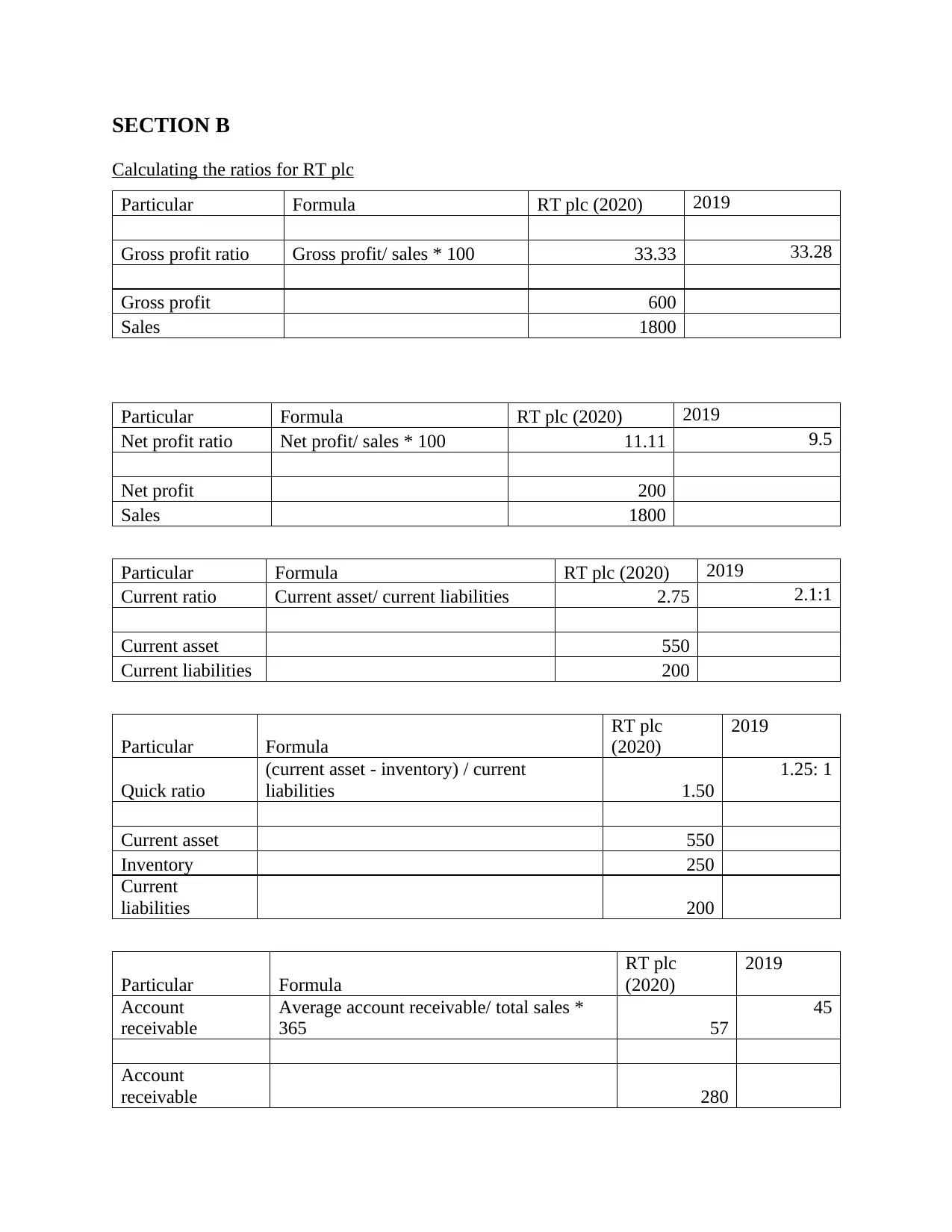

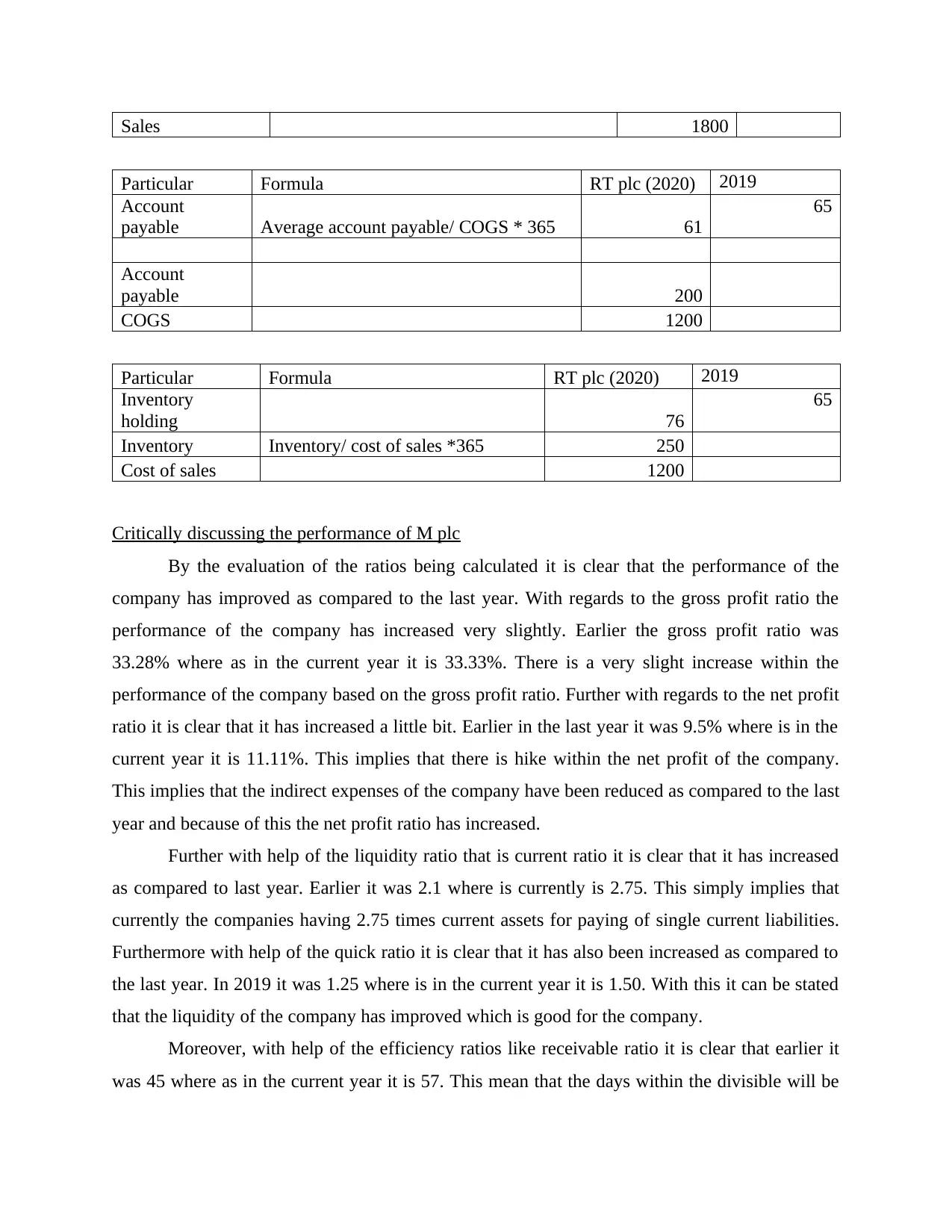

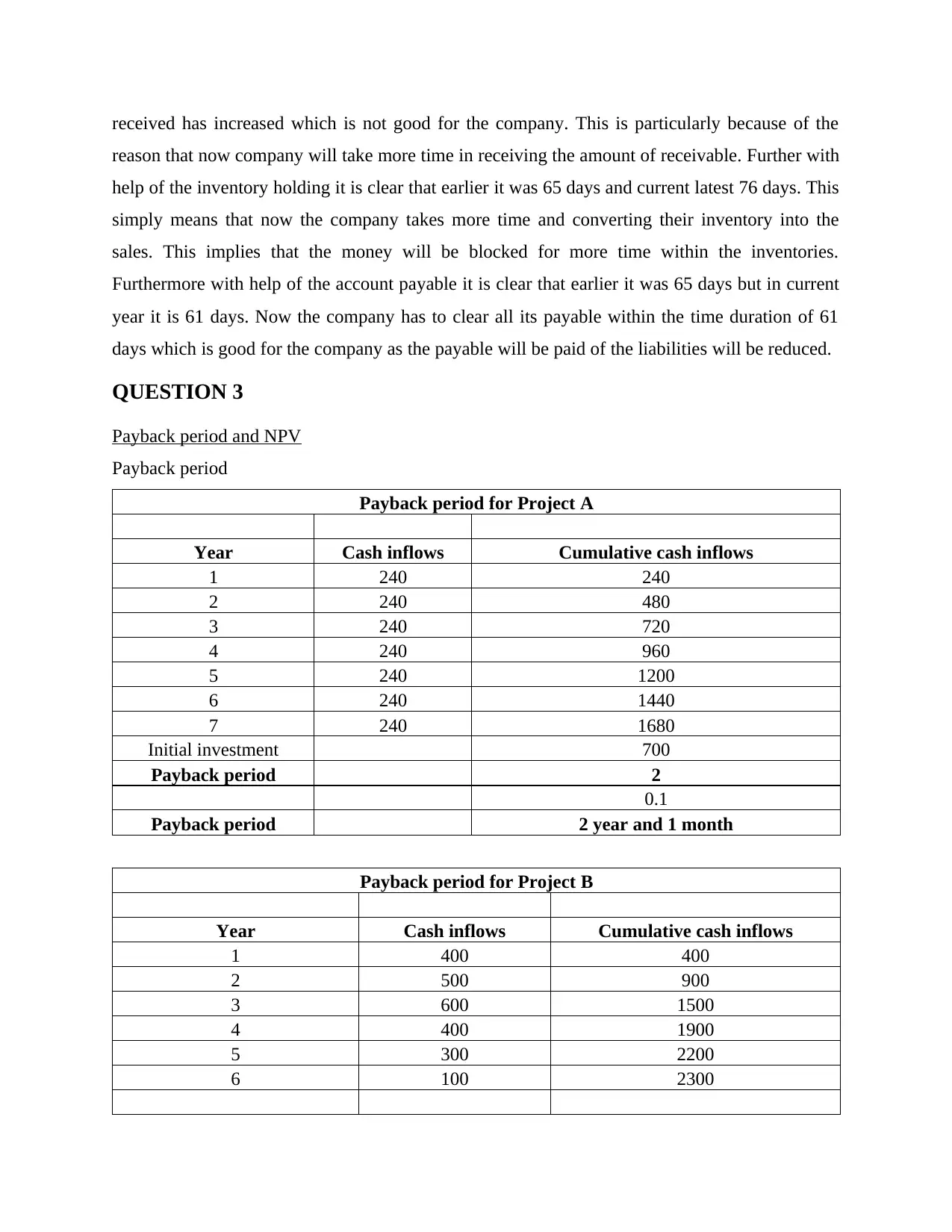

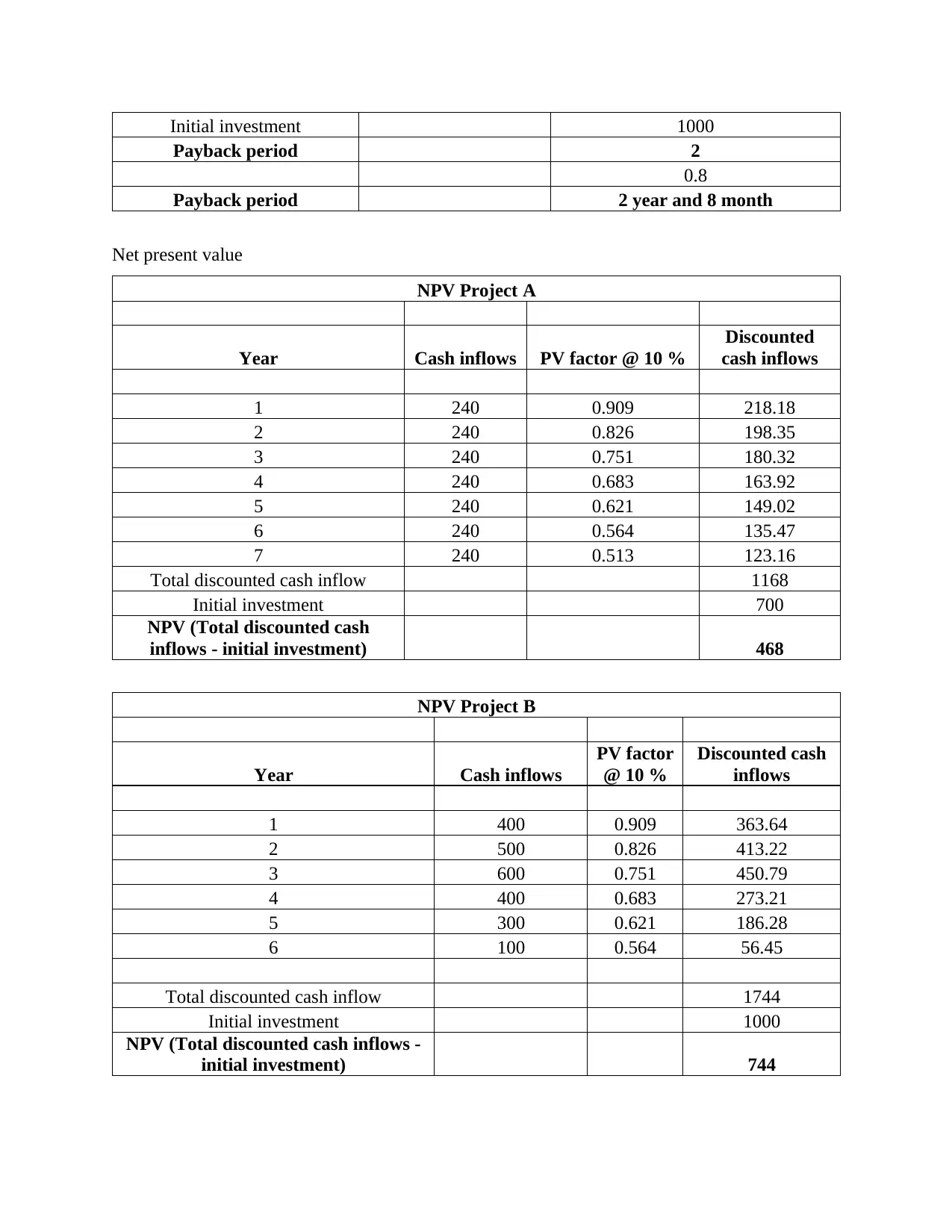

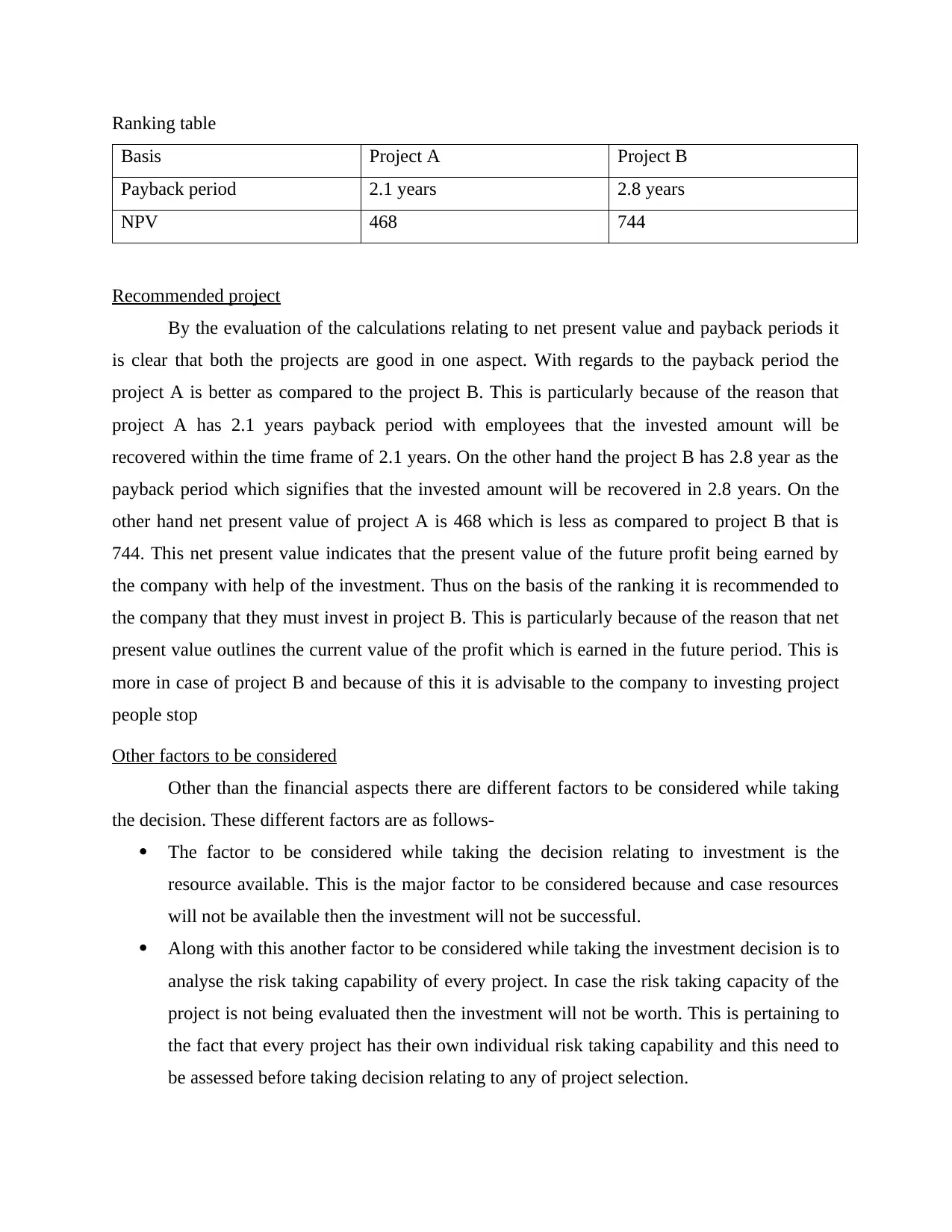

This report provides a comprehensive financial analysis of RT plc, utilizing ratio analysis to assess the company's performance and liquidity over two years (2019 and 2020). It examines key metrics such as gross profit ratio, net profit ratio, current ratio, and quick ratio, alongside efficiency ratios like receivable days, inventory holding period, and payable days. The analysis reveals slight improvements in profitability and liquidity, but also highlights concerns regarding receivable and inventory management. Furthermore, the report evaluates two investment projects (A and B) using payback period and net present value (NPV) methods, ultimately recommending Project B due to its higher NPV, while also considering non-financial factors like resource availability and risk tolerance. The document is available on Desklib, a platform offering a wealth of study resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.