Performance Management: Costing, Variance Analysis, and Budgeting

VerifiedAdded on 2023/01/10

|12

|3217

|66

Homework Assignment

AI Summary

This document presents a comprehensive solution to a performance management assignment. The solution begins with an analysis of costing methods, including overhead absorption using labor hours and activity-based costing, along with an evaluation of the results. It then delves into variance analysis, computing material usage, mix, and yield variances, and discusses the problems associated with the current system of calculating and reporting variances. The assignment also explores target costing, outlining its steps and application in a case study. Finally, it compares zero-based budgeting and incremental budgeting. The assignment covers topics like sensitivity analysis, cost per unit calculation, and various budgeting techniques, providing a detailed overview of performance management principles.

PERFORMANCE

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

a) Cost per unit absorbing the overheads on basis of the labour hours.......................................1

b) Cost per unit absorbing the overheads on basis of Activity Based Costing Approach...........1

c) Evaluation of the results obtained in the above two techniques..............................................2

d) Use of Sensitivity analysis helping the managers to cope the uncertainties...........................3

QUESTION 2..................................................................................................................................4

(a) Computation of variance........................................................................................................4

(b) Problems with the current system of calculating and reporting variances.............................5

QUESTION 3..................................................................................................................................6

(a) Deriving target costing steps..................................................................................................6

(b) Application at C Co................................................................................................................6

QUESTION 4..................................................................................................................................7

Zero based budgeting and the Incremental Budgeting is different from each other and it

provides optimal solution for the perfect planning between them..............................................7

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

a) Cost per unit absorbing the overheads on basis of the labour hours.......................................1

b) Cost per unit absorbing the overheads on basis of Activity Based Costing Approach...........1

c) Evaluation of the results obtained in the above two techniques..............................................2

d) Use of Sensitivity analysis helping the managers to cope the uncertainties...........................3

QUESTION 2..................................................................................................................................4

(a) Computation of variance........................................................................................................4

(b) Problems with the current system of calculating and reporting variances.............................5

QUESTION 3..................................................................................................................................6

(a) Deriving target costing steps..................................................................................................6

(b) Application at C Co................................................................................................................6

QUESTION 4..................................................................................................................................7

Zero based budgeting and the Incremental Budgeting is different from each other and it

provides optimal solution for the perfect planning between them..............................................7

REFERENCES..............................................................................................................................10

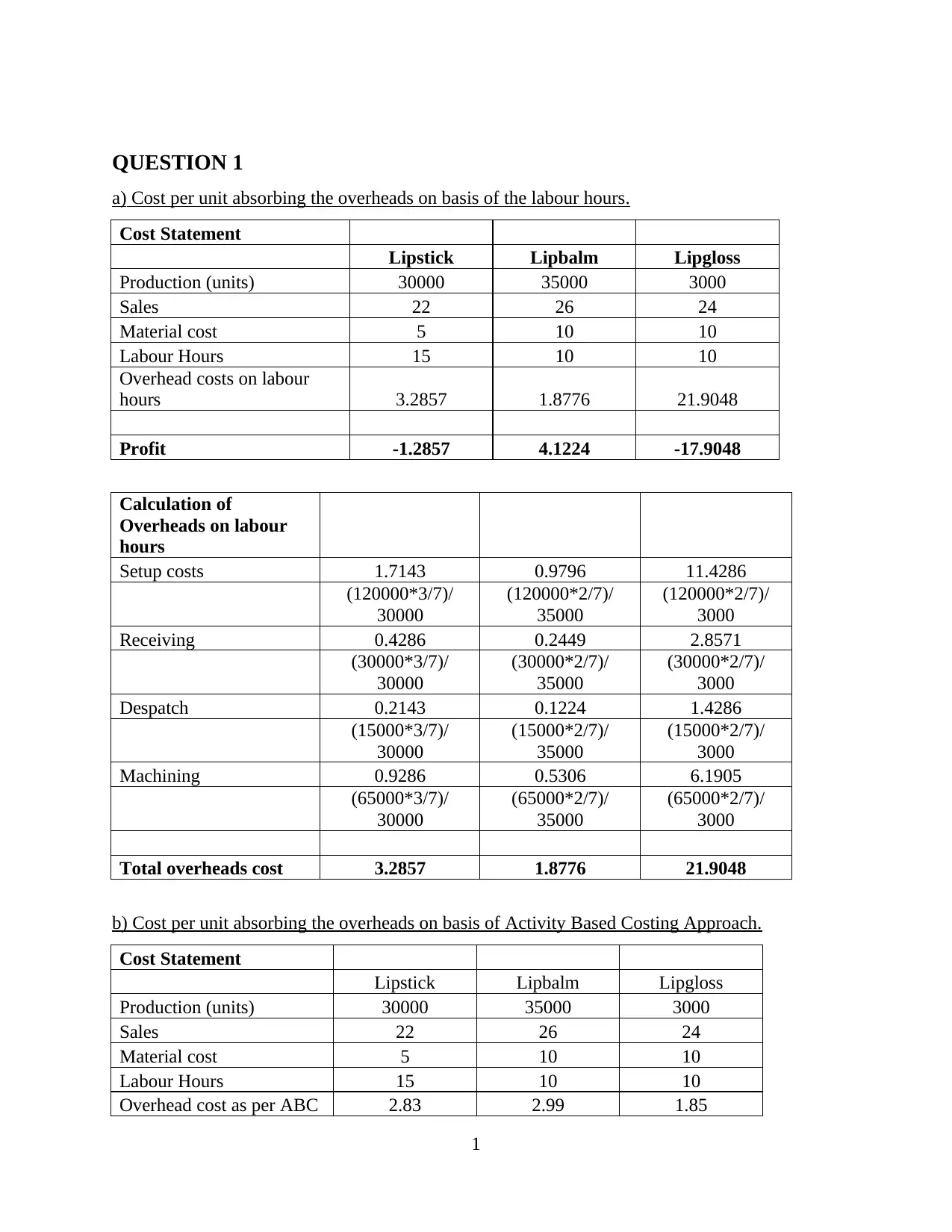

QUESTION 1

a) Cost per unit absorbing the overheads on basis of the labour hours.

Cost Statement

Lipstick Lipbalm Lipgloss

Production (units) 30000 35000 3000

Sales 22 26 24

Material cost 5 10 10

Labour Hours 15 10 10

Overhead costs on labour

hours 3.2857 1.8776 21.9048

Profit -1.2857 4.1224 -17.9048

Calculation of

Overheads on labour

hours

Setup costs 1.7143 0.9796 11.4286

(120000*3/7)/

30000

(120000*2/7)/

35000

(120000*2/7)/

3000

Receiving 0.4286 0.2449 2.8571

(30000*3/7)/

30000

(30000*2/7)/

35000

(30000*2/7)/

3000

Despatch 0.2143 0.1224 1.4286

(15000*3/7)/

30000

(15000*2/7)/

35000

(15000*2/7)/

3000

Machining 0.9286 0.5306 6.1905

(65000*3/7)/

30000

(65000*2/7)/

35000

(65000*2/7)/

3000

Total overheads cost 3.2857 1.8776 21.9048

b) Cost per unit absorbing the overheads on basis of Activity Based Costing Approach.

Cost Statement

Lipstick Lipbalm Lipgloss

Production (units) 30000 35000 3000

Sales 22 26 24

Material cost 5 10 10

Labour Hours 15 10 10

Overhead cost as per ABC 2.83 2.99 1.85

1

a) Cost per unit absorbing the overheads on basis of the labour hours.

Cost Statement

Lipstick Lipbalm Lipgloss

Production (units) 30000 35000 3000

Sales 22 26 24

Material cost 5 10 10

Labour Hours 15 10 10

Overhead costs on labour

hours 3.2857 1.8776 21.9048

Profit -1.2857 4.1224 -17.9048

Calculation of

Overheads on labour

hours

Setup costs 1.7143 0.9796 11.4286

(120000*3/7)/

30000

(120000*2/7)/

35000

(120000*2/7)/

3000

Receiving 0.4286 0.2449 2.8571

(30000*3/7)/

30000

(30000*2/7)/

35000

(30000*2/7)/

3000

Despatch 0.2143 0.1224 1.4286

(15000*3/7)/

30000

(15000*2/7)/

35000

(15000*2/7)/

3000

Machining 0.9286 0.5306 6.1905

(65000*3/7)/

30000

(65000*2/7)/

35000

(65000*2/7)/

3000

Total overheads cost 3.2857 1.8776 21.9048

b) Cost per unit absorbing the overheads on basis of Activity Based Costing Approach.

Cost Statement

Lipstick Lipbalm Lipgloss

Production (units) 30000 35000 3000

Sales 22 26 24

Material cost 5 10 10

Labour Hours 15 10 10

Overhead cost as per ABC 2.83 2.99 1.85

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

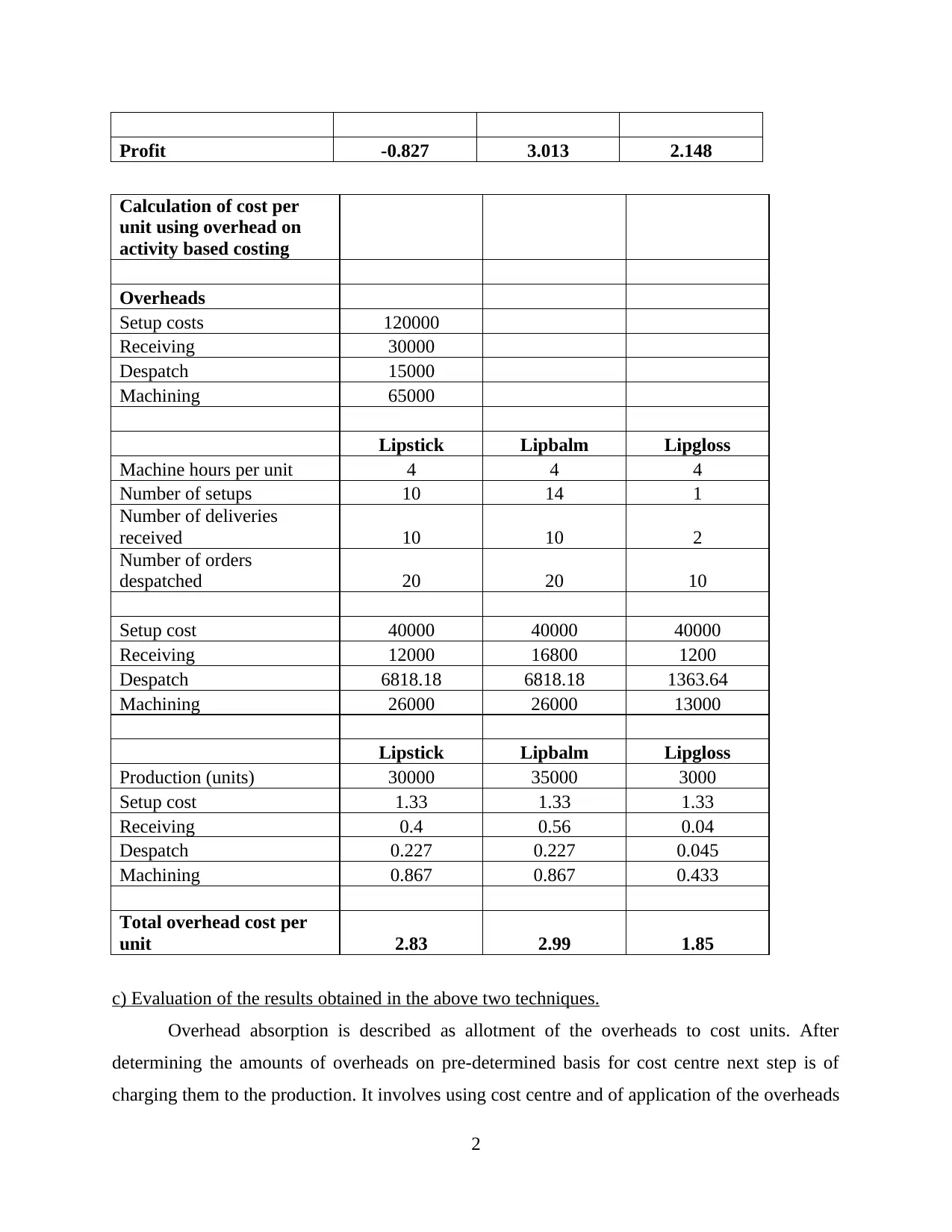

Profit -0.827 3.013 2.148

Calculation of cost per

unit using overhead on

activity based costing

Overheads

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

Lipstick Lipbalm Lipgloss

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries

received 10 10 2

Number of orders

despatched 20 20 10

Setup cost 40000 40000 40000

Receiving 12000 16800 1200

Despatch 6818.18 6818.18 1363.64

Machining 26000 26000 13000

Lipstick Lipbalm Lipgloss

Production (units) 30000 35000 3000

Setup cost 1.33 1.33 1.33

Receiving 0.4 0.56 0.04

Despatch 0.227 0.227 0.045

Machining 0.867 0.867 0.433

Total overhead cost per

unit 2.83 2.99 1.85

c) Evaluation of the results obtained in the above two techniques.

Overhead absorption is described as allotment of the overheads to cost units. After

determining the amounts of overheads on pre-determined basis for cost centre next step is of

charging them to the production. It involves using cost centre and of application of the overheads

2

Calculation of cost per

unit using overhead on

activity based costing

Overheads

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

Lipstick Lipbalm Lipgloss

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries

received 10 10 2

Number of orders

despatched 20 20 10

Setup cost 40000 40000 40000

Receiving 12000 16800 1200

Despatch 6818.18 6818.18 1363.64

Machining 26000 26000 13000

Lipstick Lipbalm Lipgloss

Production (units) 30000 35000 3000

Setup cost 1.33 1.33 1.33

Receiving 0.4 0.56 0.04

Despatch 0.227 0.227 0.045

Machining 0.867 0.867 0.433

Total overhead cost per

unit 2.83 2.99 1.85

c) Evaluation of the results obtained in the above two techniques.

Overhead absorption is described as allotment of the overheads to cost units. After

determining the amounts of overheads on pre-determined basis for cost centre next step is of

charging them to the production. It involves using cost centre and of application of the overheads

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to products passing from the cost centre. Application of the overheads is known as absorption

that could also be described as charging the overheads to production. There are various methods

that are used by the organisation for absorbing the cost to production of goods and services

(Bititci, Cocca and Ates, 2016). In the absorption of overhead using labour hours overheads are

calculate using the labours hours incurred for production of each product. The method is used by

various industries for absorbing the overhead occurred by company.

Other method is activity based costing method for the absorption of overheads. This is a

method in which overhead are proportioned on the basis of different cost centres. Overhead are

distributed on the basis of cost centre decided by management for different overheads incurred.

Overhead cost under both the methods is different as the basis of allocation is different under

both the methods. Absorption on the basis of labour is not adequate as the works are performed

by machines and the time taken by the product to complete may be same but charging costs on

the basis of this does not give reliable measure (Bianchi, 2016). On the other costs centres

provide more accurate allocation of the costs as the costs are divided on the actual proportion of

the cost related to the overheads.

d) Use of Sensitivity analysis helping the managers to cope the uncertainties.

Sensitivity analysis refers to study on how uncertainty in output of mathematical systems or

model could be allocated and divided to the different sources of uncertainties in the inputs.

Increased understanding of relationships and output variables in the systems or model is required

under sensitivity analysis. Related practice of the uncertainty analysis has greater focus over

uncertainty quantification and the propagation of the uncertainty. Sensitivity analysis helps the

managers in identifying the probable uncertainties that could affect the business operations.

Managers using sensitivity analysis tests robustness of results of the models or systems in

presence of the uncertainty(Glas, Henne and Essig, 2018). It involves using various models and

mathematical techniques on the basis of which future estimates are made by the managers and

evaluates various techniques that are associated with the outcomes.

Managers are using the model in financial analysis for analysing how different values of the

set of the independent variables affecting the specific dependent variables under the specific

conditions. Managers are identifying the opaque functions or process attached with inputs used

in producing the products and services. Managers before taking the decision analyse the probable

outcomes associated with the decisions. They identify the various factors that could influence the

3

that could also be described as charging the overheads to production. There are various methods

that are used by the organisation for absorbing the cost to production of goods and services

(Bititci, Cocca and Ates, 2016). In the absorption of overhead using labour hours overheads are

calculate using the labours hours incurred for production of each product. The method is used by

various industries for absorbing the overhead occurred by company.

Other method is activity based costing method for the absorption of overheads. This is a

method in which overhead are proportioned on the basis of different cost centres. Overhead are

distributed on the basis of cost centre decided by management for different overheads incurred.

Overhead cost under both the methods is different as the basis of allocation is different under

both the methods. Absorption on the basis of labour is not adequate as the works are performed

by machines and the time taken by the product to complete may be same but charging costs on

the basis of this does not give reliable measure (Bianchi, 2016). On the other costs centres

provide more accurate allocation of the costs as the costs are divided on the actual proportion of

the cost related to the overheads.

d) Use of Sensitivity analysis helping the managers to cope the uncertainties.

Sensitivity analysis refers to study on how uncertainty in output of mathematical systems or

model could be allocated and divided to the different sources of uncertainties in the inputs.

Increased understanding of relationships and output variables in the systems or model is required

under sensitivity analysis. Related practice of the uncertainty analysis has greater focus over

uncertainty quantification and the propagation of the uncertainty. Sensitivity analysis helps the

managers in identifying the probable uncertainties that could affect the business operations.

Managers using sensitivity analysis tests robustness of results of the models or systems in

presence of the uncertainty(Glas, Henne and Essig, 2018). It involves using various models and

mathematical techniques on the basis of which future estimates are made by the managers and

evaluates various techniques that are associated with the outcomes.

Managers are using the model in financial analysis for analysing how different values of the

set of the independent variables affecting the specific dependent variables under the specific

conditions. Managers are identifying the opaque functions or process attached with inputs used

in producing the products and services. Managers before taking the decision analyse the probable

outcomes associated with the decisions. They identify the various factors that could influence the

3

outputs and results of operation. Business is associated with various uncertainties and it is

essential for the managers to deal with the uncertainties effectively for achieving the desired

goals and objectives of the company. Sensitivity analysis provides the managers to analyse the

uncertainties in advance and prepare the organisation to deal with the uncertainties positively.

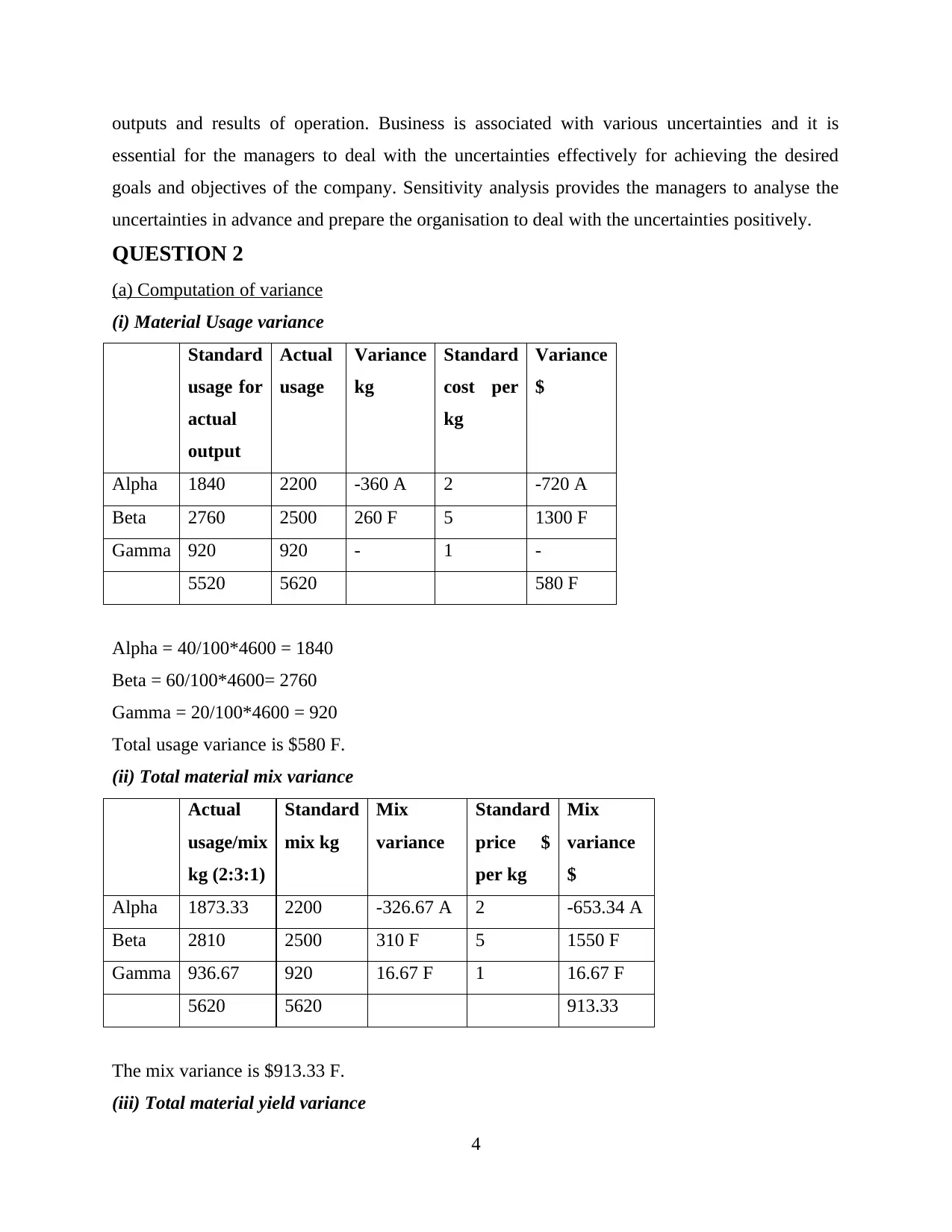

QUESTION 2

(a) Computation of variance

(i) Material Usage variance

Standard

usage for

actual

output

Actual

usage

Variance

kg

Standard

cost per

kg

Variance

$

Alpha 1840 2200 -360 A 2 -720 A

Beta 2760 2500 260 F 5 1300 F

Gamma 920 920 - 1 -

5520 5620 580 F

Alpha = 40/100*4600 = 1840

Beta = 60/100*4600= 2760

Gamma = 20/100*4600 = 920

Total usage variance is $580 F.

(ii) Total material mix variance

Actual

usage/mix

kg (2:3:1)

Standard

mix kg

Mix

variance

Standard

price $

per kg

Mix

variance

$

Alpha 1873.33 2200 -326.67 A 2 -653.34 A

Beta 2810 2500 310 F 5 1550 F

Gamma 936.67 920 16.67 F 1 16.67 F

5620 5620 913.33

The mix variance is $913.33 F.

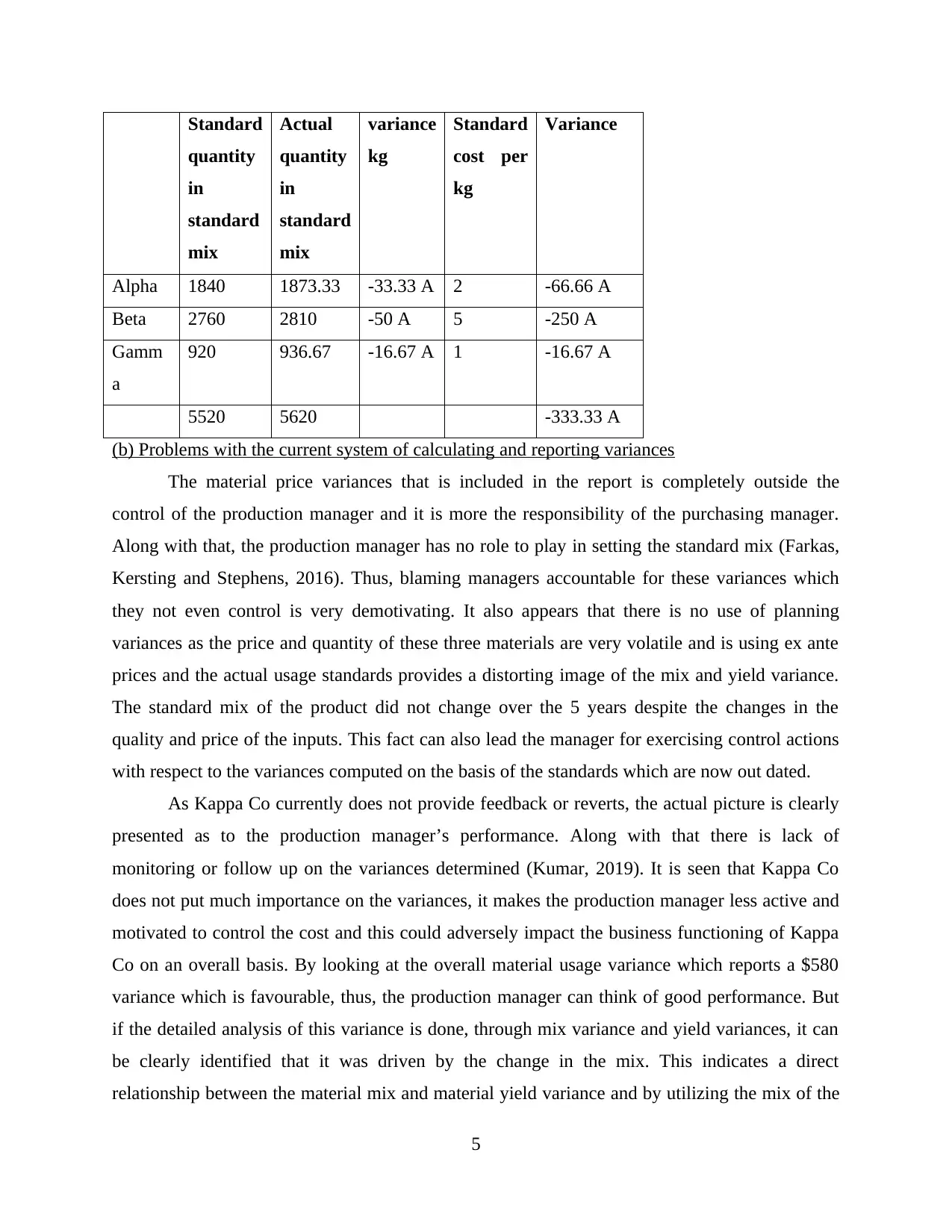

(iii) Total material yield variance

4

essential for the managers to deal with the uncertainties effectively for achieving the desired

goals and objectives of the company. Sensitivity analysis provides the managers to analyse the

uncertainties in advance and prepare the organisation to deal with the uncertainties positively.

QUESTION 2

(a) Computation of variance

(i) Material Usage variance

Standard

usage for

actual

output

Actual

usage

Variance

kg

Standard

cost per

kg

Variance

$

Alpha 1840 2200 -360 A 2 -720 A

Beta 2760 2500 260 F 5 1300 F

Gamma 920 920 - 1 -

5520 5620 580 F

Alpha = 40/100*4600 = 1840

Beta = 60/100*4600= 2760

Gamma = 20/100*4600 = 920

Total usage variance is $580 F.

(ii) Total material mix variance

Actual

usage/mix

kg (2:3:1)

Standard

mix kg

Mix

variance

Standard

price $

per kg

Mix

variance

$

Alpha 1873.33 2200 -326.67 A 2 -653.34 A

Beta 2810 2500 310 F 5 1550 F

Gamma 936.67 920 16.67 F 1 16.67 F

5620 5620 913.33

The mix variance is $913.33 F.

(iii) Total material yield variance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard

quantity

in

standard

mix

Actual

quantity

in

standard

mix

variance

kg

Standard

cost per

kg

Variance

Alpha 1840 1873.33 -33.33 A 2 -66.66 A

Beta 2760 2810 -50 A 5 -250 A

Gamm

a

920 936.67 -16.67 A 1 -16.67 A

5520 5620 -333.33 A

(b) Problems with the current system of calculating and reporting variances

The material price variances that is included in the report is completely outside the

control of the production manager and it is more the responsibility of the purchasing manager.

Along with that, the production manager has no role to play in setting the standard mix (Farkas,

Kersting and Stephens, 2016). Thus, blaming managers accountable for these variances which

they not even control is very demotivating. It also appears that there is no use of planning

variances as the price and quantity of these three materials are very volatile and is using ex ante

prices and the actual usage standards provides a distorting image of the mix and yield variance.

The standard mix of the product did not change over the 5 years despite the changes in the

quality and price of the inputs. This fact can also lead the manager for exercising control actions

with respect to the variances computed on the basis of the standards which are now out dated.

As Kappa Co currently does not provide feedback or reverts, the actual picture is clearly

presented as to the production manager’s performance. Along with that there is lack of

monitoring or follow up on the variances determined (Kumar, 2019). It is seen that Kappa Co

does not put much importance on the variances, it makes the production manager less active and

motivated to control the cost and this could adversely impact the business functioning of Kappa

Co on an overall basis. By looking at the overall material usage variance which reports a $580

variance which is favourable, thus, the production manager can think of good performance. But

if the detailed analysis of this variance is done, through mix variance and yield variances, it can

be clearly identified that it was driven by the change in the mix. This indicates a direct

relationship between the material mix and material yield variance and by utilizing the mix of the

5

quantity

in

standard

mix

Actual

quantity

in

standard

mix

variance

kg

Standard

cost per

kg

Variance

Alpha 1840 1873.33 -33.33 A 2 -66.66 A

Beta 2760 2810 -50 A 5 -250 A

Gamm

a

920 936.67 -16.67 A 1 -16.67 A

5520 5620 -333.33 A

(b) Problems with the current system of calculating and reporting variances

The material price variances that is included in the report is completely outside the

control of the production manager and it is more the responsibility of the purchasing manager.

Along with that, the production manager has no role to play in setting the standard mix (Farkas,

Kersting and Stephens, 2016). Thus, blaming managers accountable for these variances which

they not even control is very demotivating. It also appears that there is no use of planning

variances as the price and quantity of these three materials are very volatile and is using ex ante

prices and the actual usage standards provides a distorting image of the mix and yield variance.

The standard mix of the product did not change over the 5 years despite the changes in the

quality and price of the inputs. This fact can also lead the manager for exercising control actions

with respect to the variances computed on the basis of the standards which are now out dated.

As Kappa Co currently does not provide feedback or reverts, the actual picture is clearly

presented as to the production manager’s performance. Along with that there is lack of

monitoring or follow up on the variances determined (Kumar, 2019). It is seen that Kappa Co

does not put much importance on the variances, it makes the production manager less active and

motivated to control the cost and this could adversely impact the business functioning of Kappa

Co on an overall basis. By looking at the overall material usage variance which reports a $580

variance which is favourable, thus, the production manager can think of good performance. But

if the detailed analysis of this variance is done, through mix variance and yield variances, it can

be clearly identified that it was driven by the change in the mix. This indicates a direct

relationship between the material mix and material yield variance and by utilizing the mix of the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inputs which varied from the standards which has resulted into the savings of $913.33. Along

with that, the change in mix could have impacted the quality and as a result sales would have

been affected and no such information is provided about it.

QUESTION 3

(a) Deriving target costing steps

Step 1: The product or the service should be developed as per the requirement and the need of

the customers and thus, it will help in attracting adequate sales volumes.

Step 2: After this. target price is set based on the perceived value of the product. This is therefore

based on the market price prevailing in the market.

Step 3: Then the required target operating profit per unit is determined. This can eb either based

on the return on sales or return on investment (Vin and et.al, 2019).

Step 4: The target cost is determined by subtracting the target profit from the target price of the

product.

Step 5: In case there is a cost gap, efforts will be made to reduce the gap. Techniques like value

engineering can be used for looking at value chain functions of business.

Step 6: Last is negotiating with the customers which helps in determining whether to proceed

with the project or not.

(b) Application at C Co

Difficulties in implementation

For target costing, it is important to define service provided. The C Co provides wide

range of services to its client; thus, the definition of the services will vary. Different

target costs are required to be derived for various services provided.

C Co has regular and one-off clients, for regular client’s services is being repeated which

makes it easy to target cost for these jobs. But in case of one-off clients, there might not

be any data in comparable nature available which makes it difficult to set the target cost.

Some of the work requires specialist. For instance, cleaning the restaurant and the

cooking space after occurrence of food poisoning will require to implement specialist

techniques along with the adherence to the regulations with which the C Co might not be

familiar. It may be difficult to establish the market price for this service, therefore,

making it tough to determine the target cost.

Benefits to C Co

6

with that, the change in mix could have impacted the quality and as a result sales would have

been affected and no such information is provided about it.

QUESTION 3

(a) Deriving target costing steps

Step 1: The product or the service should be developed as per the requirement and the need of

the customers and thus, it will help in attracting adequate sales volumes.

Step 2: After this. target price is set based on the perceived value of the product. This is therefore

based on the market price prevailing in the market.

Step 3: Then the required target operating profit per unit is determined. This can eb either based

on the return on sales or return on investment (Vin and et.al, 2019).

Step 4: The target cost is determined by subtracting the target profit from the target price of the

product.

Step 5: In case there is a cost gap, efforts will be made to reduce the gap. Techniques like value

engineering can be used for looking at value chain functions of business.

Step 6: Last is negotiating with the customers which helps in determining whether to proceed

with the project or not.

(b) Application at C Co

Difficulties in implementation

For target costing, it is important to define service provided. The C Co provides wide

range of services to its client; thus, the definition of the services will vary. Different

target costs are required to be derived for various services provided.

C Co has regular and one-off clients, for regular client’s services is being repeated which

makes it easy to target cost for these jobs. But in case of one-off clients, there might not

be any data in comparable nature available which makes it difficult to set the target cost.

Some of the work requires specialist. For instance, cleaning the restaurant and the

cooking space after occurrence of food poisoning will require to implement specialist

techniques along with the adherence to the regulations with which the C Co might not be

familiar. It may be difficult to establish the market price for this service, therefore,

making it tough to determine the target cost.

Benefits to C Co

6

The target costing is useful in competitive market and thus, is required to accept the

market price for their products. Therefore, C Co is operating competitive market offering

specialist services.It is clear that the recent drop in sales is because of the increase in the

price which lead to loss of customers. C Co cannot ignore the market price for the

cleaning services and cannot pass on cost increases like done earlier. Target cost will

thus, help it to focus on the market price of the similar services which is provided by its

competitors.

After determining the target cost, if the C Co finds the cost gaps, it will the have to

analyse its internal processes and cost appropriately. It should establish why the price was

increased first and if it cannot achieve any reduction in the prices, then it should consider

from where it can source the cheaper non-chemical products from the various other

alternative sources or suppliers. Thus, based on this, it can be said that the target costing

is beneficial for the C Co by helping it to focus on the cost reduction and also focusing on

customer retention.

QUESTION 4

Zero based budgeting and the Incremental Budgeting is different from each other and it provides

optimal solution for the perfect planning between them.

Budgeting is one of the important part in business that is included in the financial

planning. Budgets are to be prepared by the organisation for every year. Budgets are the

spending plans of company for making effective allocation and utilisation of the resources.

Budgeting enables the company to move in right direction for achieving the goals and objectives

of business. Along with the time traditional method of budgeting has been evolved as per the

needs and requirements of organisation. Various methods are used in the budgeting for financial

planning

Zero based budgeting is the method of budgeting where all the expenses are justified for

each new period. Process of zero based budgeting involves starting from zero base. Zero based

budgeting does not consider the budgets of previous years for preparing budgets for current year.

Adequate analysis of the factors is made by the management before the budgets are prepared by

the company for current year (Gerrish, 2016). Zero based budgeting requires the company to

justify each and every time that is included in the budgets. Zero based budgeting allows the

7

market price for their products. Therefore, C Co is operating competitive market offering

specialist services.It is clear that the recent drop in sales is because of the increase in the

price which lead to loss of customers. C Co cannot ignore the market price for the

cleaning services and cannot pass on cost increases like done earlier. Target cost will

thus, help it to focus on the market price of the similar services which is provided by its

competitors.

After determining the target cost, if the C Co finds the cost gaps, it will the have to

analyse its internal processes and cost appropriately. It should establish why the price was

increased first and if it cannot achieve any reduction in the prices, then it should consider

from where it can source the cheaper non-chemical products from the various other

alternative sources or suppliers. Thus, based on this, it can be said that the target costing

is beneficial for the C Co by helping it to focus on the cost reduction and also focusing on

customer retention.

QUESTION 4

Zero based budgeting and the Incremental Budgeting is different from each other and it provides

optimal solution for the perfect planning between them.

Budgeting is one of the important part in business that is included in the financial

planning. Budgets are to be prepared by the organisation for every year. Budgets are the

spending plans of company for making effective allocation and utilisation of the resources.

Budgeting enables the company to move in right direction for achieving the goals and objectives

of business. Along with the time traditional method of budgeting has been evolved as per the

needs and requirements of organisation. Various methods are used in the budgeting for financial

planning

Zero based budgeting is the method of budgeting where all the expenses are justified for

each new period. Process of zero based budgeting involves starting from zero base. Zero based

budgeting does not consider the budgets of previous years for preparing budgets for current year.

Adequate analysis of the factors is made by the management before the budgets are prepared by

the company for current year (Gerrish, 2016). Zero based budgeting requires the company to

justify each and every time that is included in the budgets. Zero based budgeting allows the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

strategic goals that are to be implemented in budgeting process for tying them to the specific

functional areas of company where costs are grouped first for & then measured against prior

results and the current expectations

Incremental budgeting is a method of traditional budgeting where the budgets are prepared

taking budget of current year or actual performance as base with the incremental amount then

being added for new budgeted period. The incremental amounts are the adjustments for various

things influencing the budget for the period like increases in the costs and sales prices, inflation

and such other factors. Incremental budgeting is a process of budgeting based over the idea that

new budgets could be developed through marginal changes to budget for current year. among the

various methods of budgeting used by the businesses incremental budgeting is considered as

most conservative approach.

Incremental budgeting like zero based budgeting is not started from the zero base. Zero

based budgeting involves detailed analysis for preparing the budgets every time the budget is

prepared by management. Zero based budgeting is useful in planning where the budget is

prepared for the products that are changing at more frequent basis and are influenced by the

external factors. This reduces the variations in the actual and budgeted figures to the minimum as

the budgets are prepared analysing all the factors thoroughly (Cappelli and Tavis, 2016).

However it is not always beneficial for the organisation as it involves increased efforts and time

to analyse the factors. This time could be better utilised by the managers elsewhere and also the

method is expensive for the business as detailed study is made. It takes considerable time for

preparing the final budgets. It lacks coordination with the other departments of organisation. The

process does not allow the departments to have control over the process as the budgets are new

every year.

Incremental budgeting on the other is method that is based over traditional budgeting in

which the budgets for current year are made on the basis of previous budgets. In this budgeting

method management do not put considerable time to analyse the factors associated with the

budgets. Only the factors influencing the budgets are adjusted in the current budgets and it do not

provides for the analysis of factors that were wrong in previous budgets (DeNisi and Murphy,

2017). As the budgets are prepared on the previous budgets errors and mistakes of previous years

are repeated many of the times. This makes the planning ineffective and due to this control over

the processes and activities could not be made.

8

functional areas of company where costs are grouped first for & then measured against prior

results and the current expectations

Incremental budgeting is a method of traditional budgeting where the budgets are prepared

taking budget of current year or actual performance as base with the incremental amount then

being added for new budgeted period. The incremental amounts are the adjustments for various

things influencing the budget for the period like increases in the costs and sales prices, inflation

and such other factors. Incremental budgeting is a process of budgeting based over the idea that

new budgets could be developed through marginal changes to budget for current year. among the

various methods of budgeting used by the businesses incremental budgeting is considered as

most conservative approach.

Incremental budgeting like zero based budgeting is not started from the zero base. Zero

based budgeting involves detailed analysis for preparing the budgets every time the budget is

prepared by management. Zero based budgeting is useful in planning where the budget is

prepared for the products that are changing at more frequent basis and are influenced by the

external factors. This reduces the variations in the actual and budgeted figures to the minimum as

the budgets are prepared analysing all the factors thoroughly (Cappelli and Tavis, 2016).

However it is not always beneficial for the organisation as it involves increased efforts and time

to analyse the factors. This time could be better utilised by the managers elsewhere and also the

method is expensive for the business as detailed study is made. It takes considerable time for

preparing the final budgets. It lacks coordination with the other departments of organisation. The

process does not allow the departments to have control over the process as the budgets are new

every year.

Incremental budgeting on the other is method that is based over traditional budgeting in

which the budgets for current year are made on the basis of previous budgets. In this budgeting

method management do not put considerable time to analyse the factors associated with the

budgets. Only the factors influencing the budgets are adjusted in the current budgets and it do not

provides for the analysis of factors that were wrong in previous budgets (DeNisi and Murphy,

2017). As the budgets are prepared on the previous budgets errors and mistakes of previous years

are repeated many of the times. This makes the planning ineffective and due to this control over

the processes and activities could not be made.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

REFERENCES

Books and Journals

DeNisi, A.S. and Murphy, K.R., 2017. Performance appraisal and performance management:

100 years of progress?. Journal of Applied Psychology. 102(3).p.421.

Cappelli, P. and Tavis, A., 2016. The performance management revolution. Harvard Business

Review.94(10).pp.58-67.

Gerrish, E., 2016. The impact of performance management on performance in public

organizations: A meta‐analysis. Public Administration Review.76(1). pp.48-66.

Glas, A.H., Henne, F.U. and Essig, M., 2018. Missing performance management and

measurement aspects in performance-based contracting. International Journal of

Operations & Production Management.

Bianchi, C., 2016. Dynamic performance management (Vol. 1). Berlin: Springer.

Bititci, U., Cocca, P. and Ates, A., 2016. Impact of visual performance management systems on

the performance management practices of organisations. International Journal of

Production Research. 54(6).pp.1571-1593.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35.

pp.56-68.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Vin, H.M. and et.al, 2019. System and method of deriving appropriate target operating

environment. U.S. Patent 10,255,111.

10

Books and Journals

DeNisi, A.S. and Murphy, K.R., 2017. Performance appraisal and performance management:

100 years of progress?. Journal of Applied Psychology. 102(3).p.421.

Cappelli, P. and Tavis, A., 2016. The performance management revolution. Harvard Business

Review.94(10).pp.58-67.

Gerrish, E., 2016. The impact of performance management on performance in public

organizations: A meta‐analysis. Public Administration Review.76(1). pp.48-66.

Glas, A.H., Henne, F.U. and Essig, M., 2018. Missing performance management and

measurement aspects in performance-based contracting. International Journal of

Operations & Production Management.

Bianchi, C., 2016. Dynamic performance management (Vol. 1). Berlin: Springer.

Bititci, U., Cocca, P. and Ates, A., 2016. Impact of visual performance management systems on

the performance management practices of organisations. International Journal of

Production Research. 54(6).pp.1571-1593.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35.

pp.56-68.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Vin, H.M. and et.al, 2019. System and method of deriving appropriate target operating

environment. U.S. Patent 10,255,111.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.