Financial Analysis Assignment: Breakeven, Investment, and Budgeting

VerifiedAdded on 2020/05/04

|9

|1262

|38

Homework Assignment

AI Summary

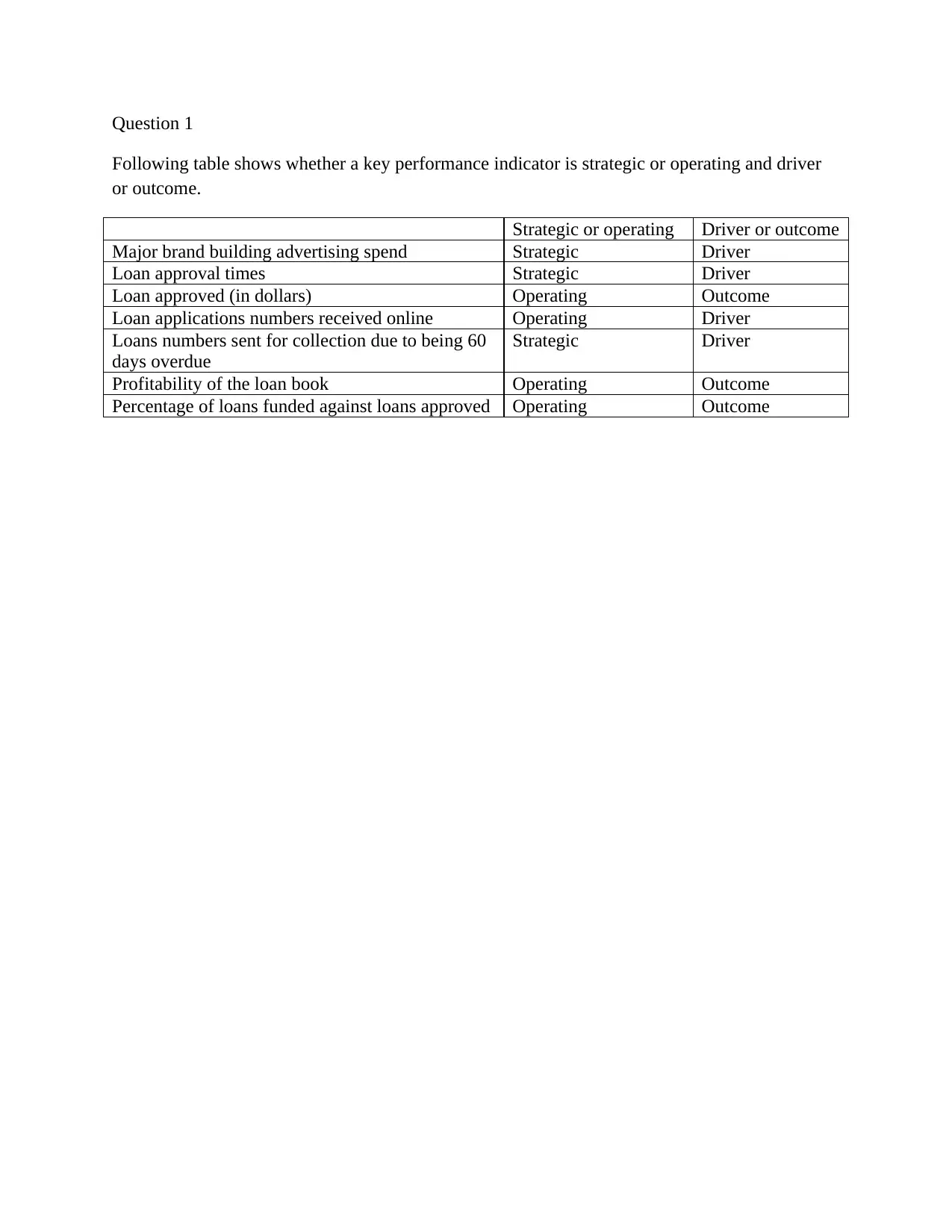

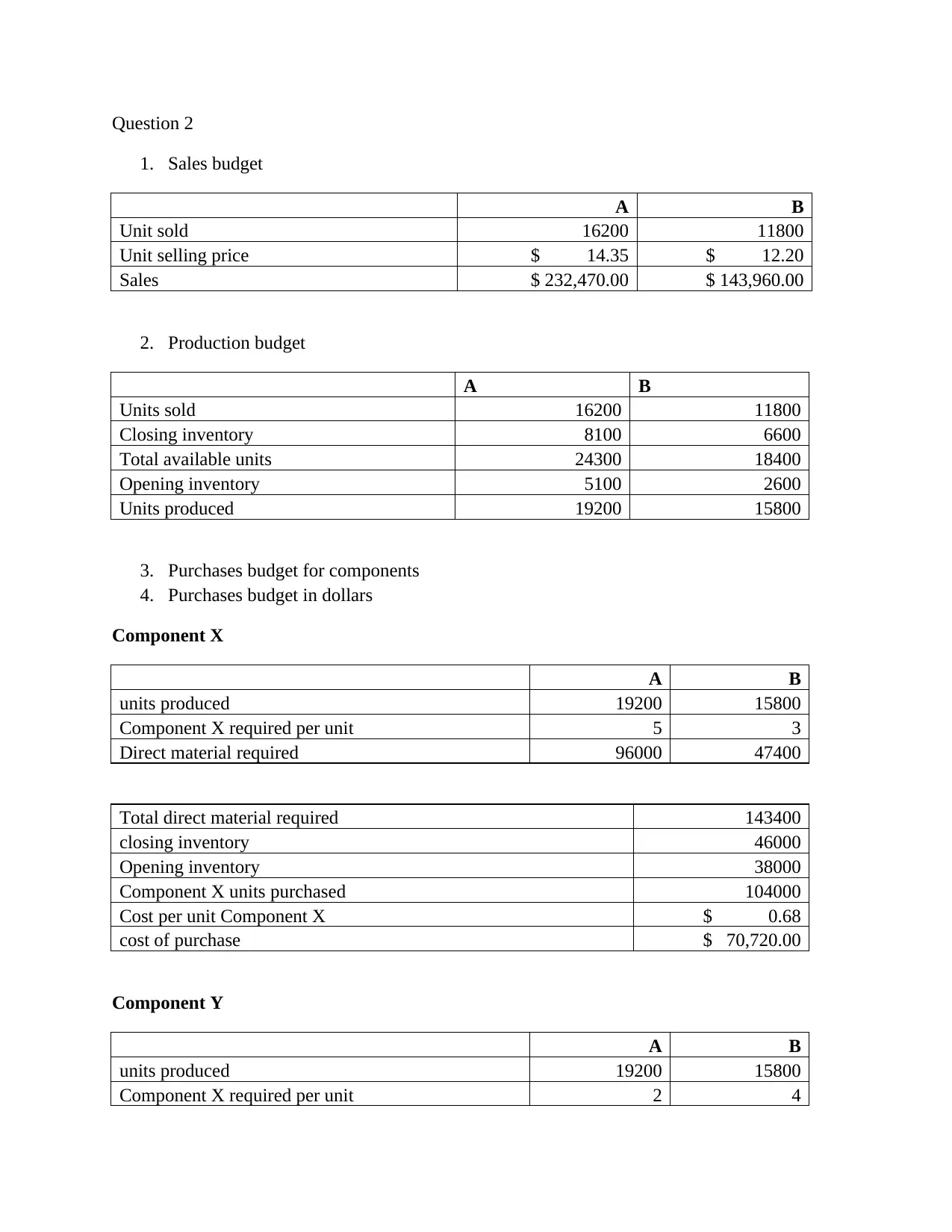

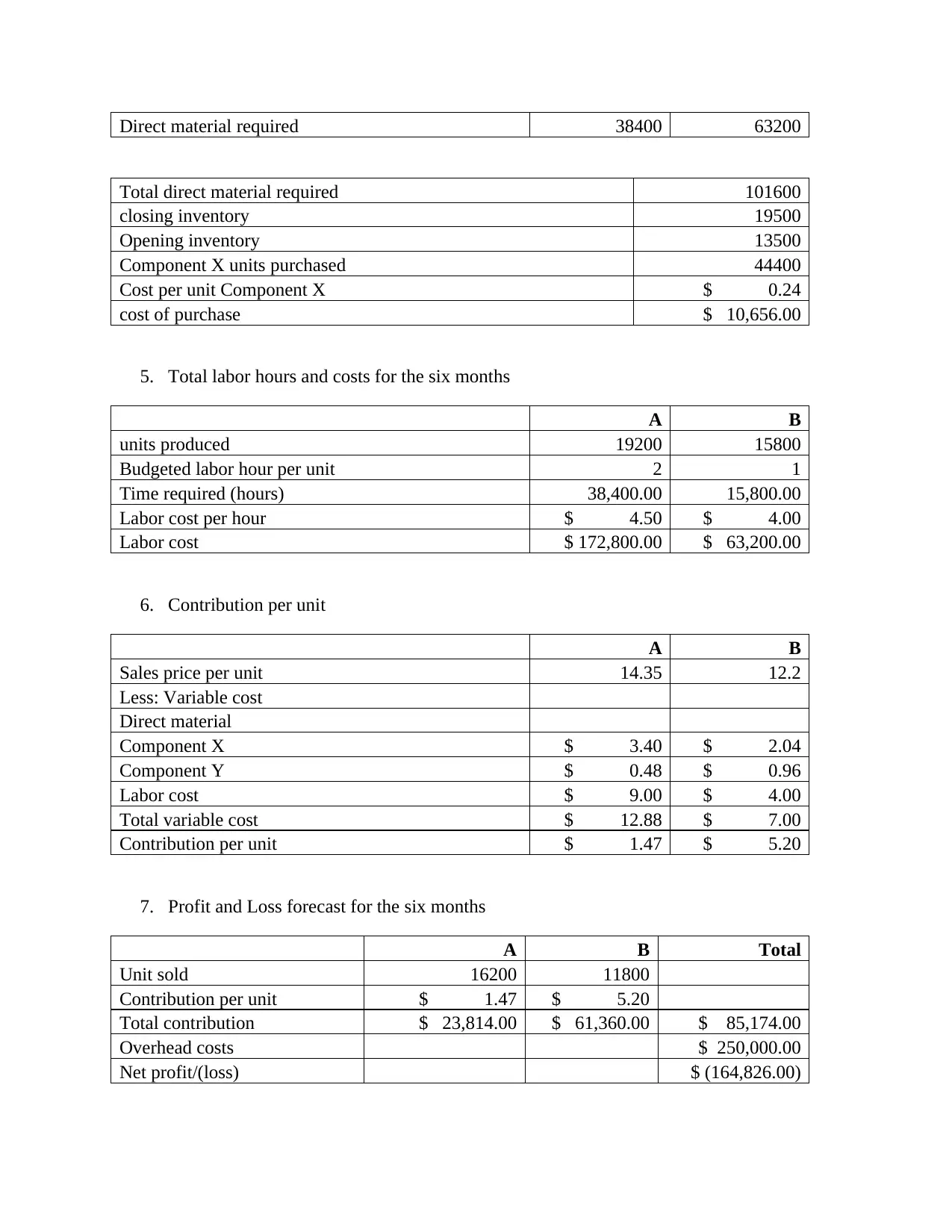

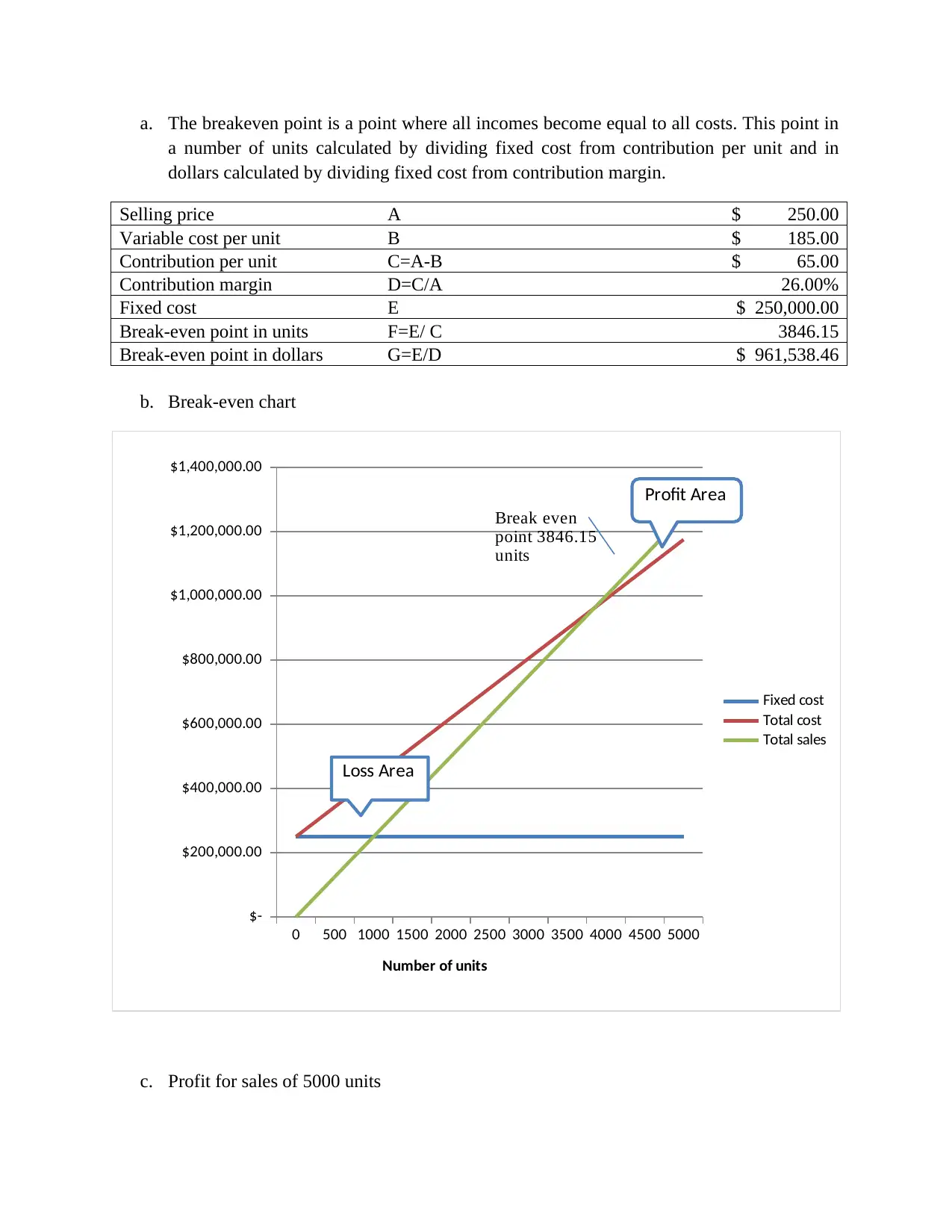

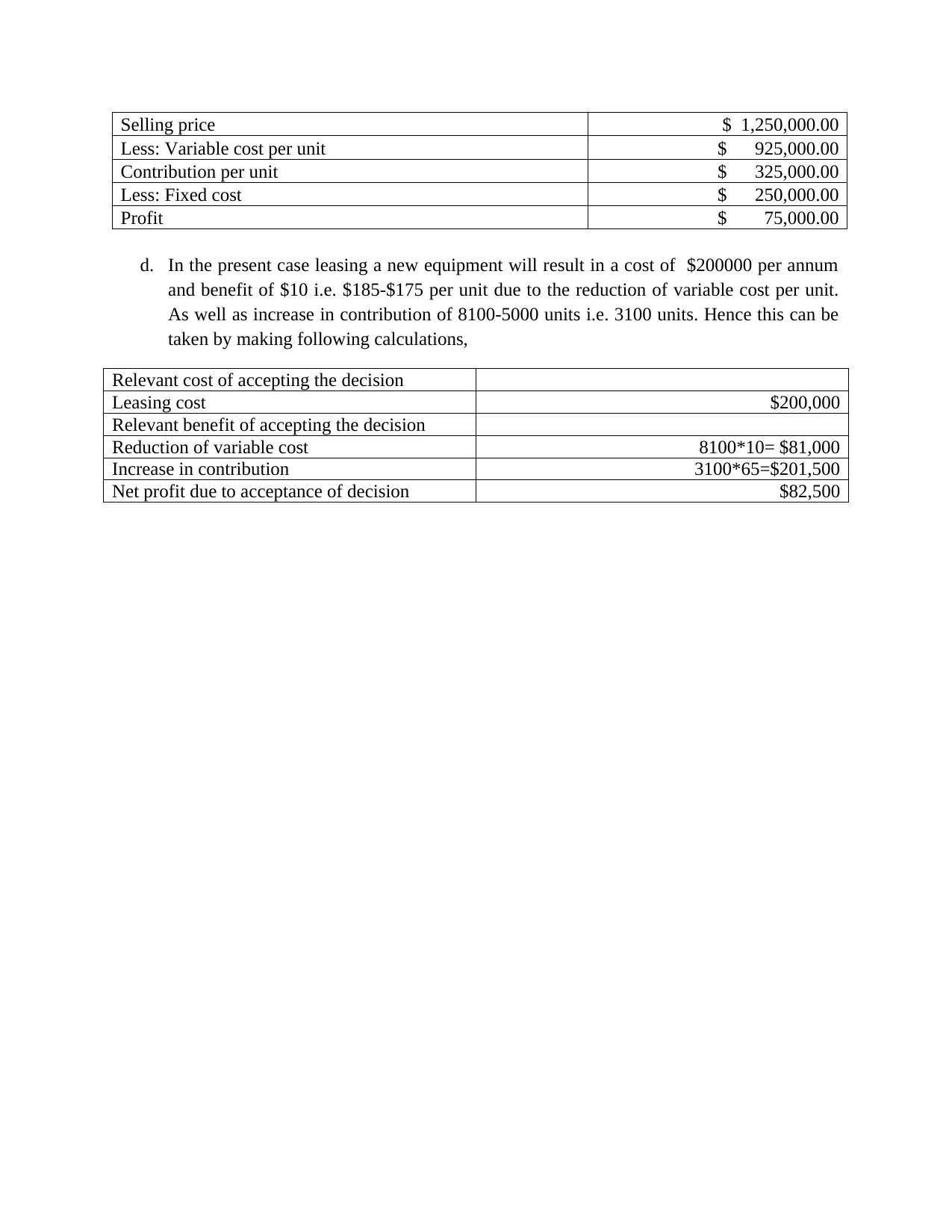

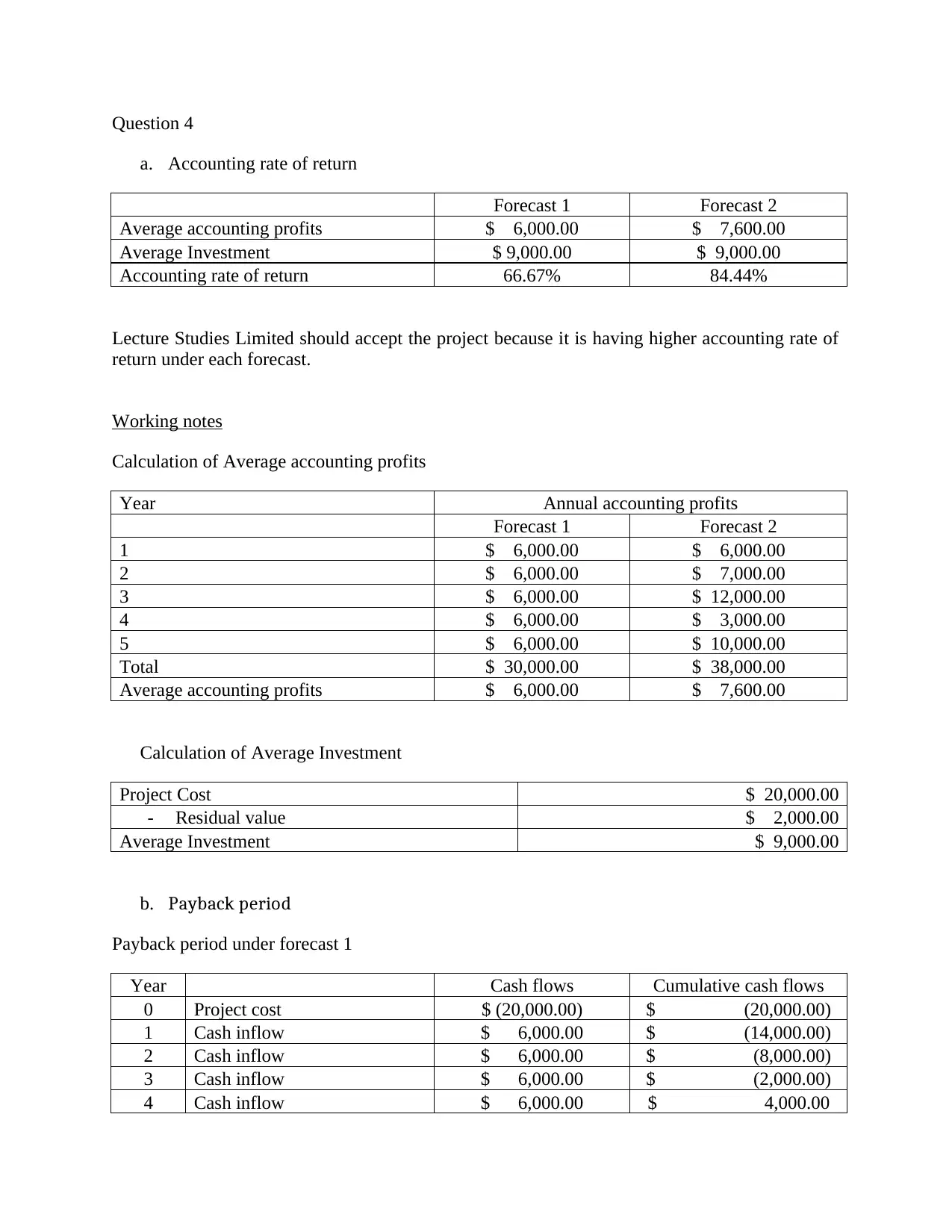

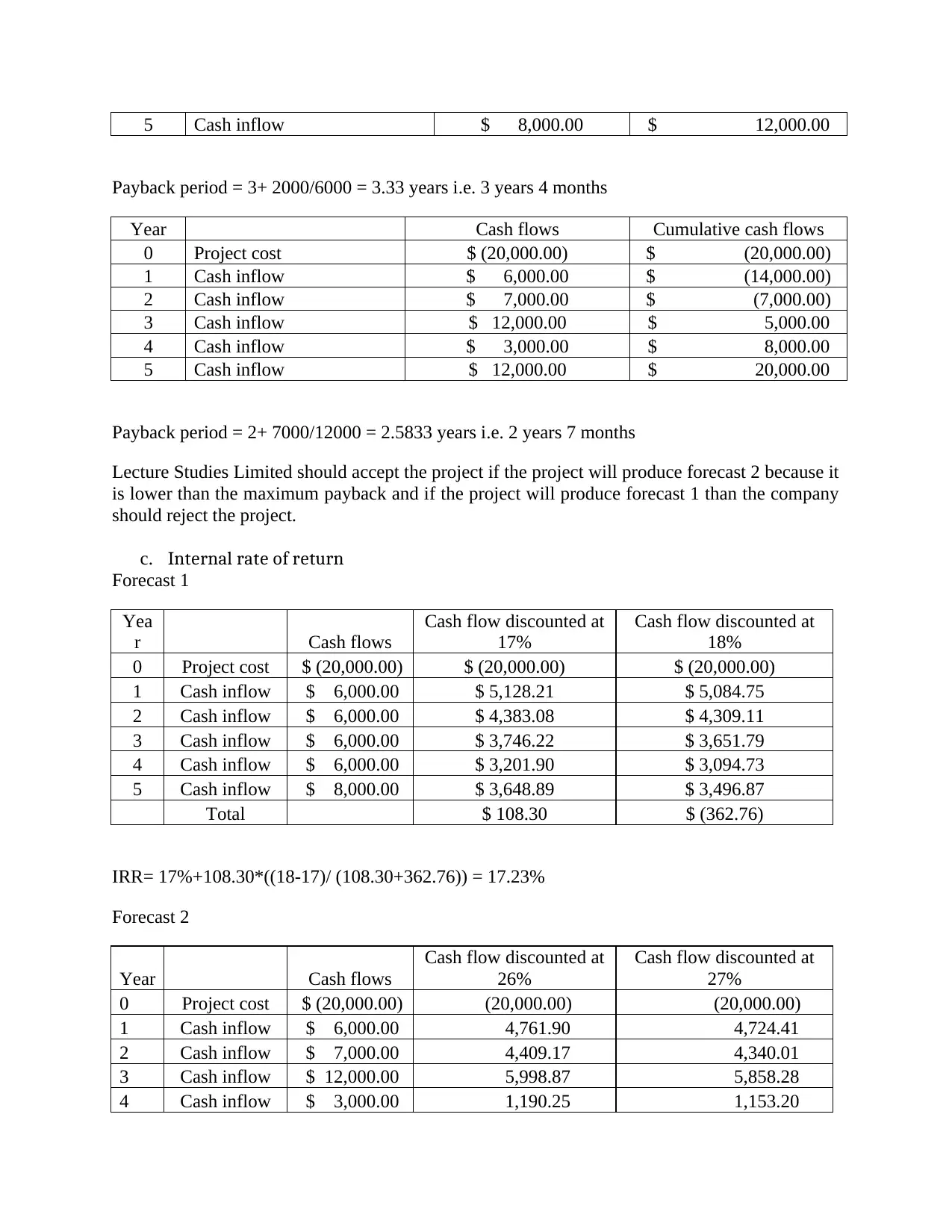

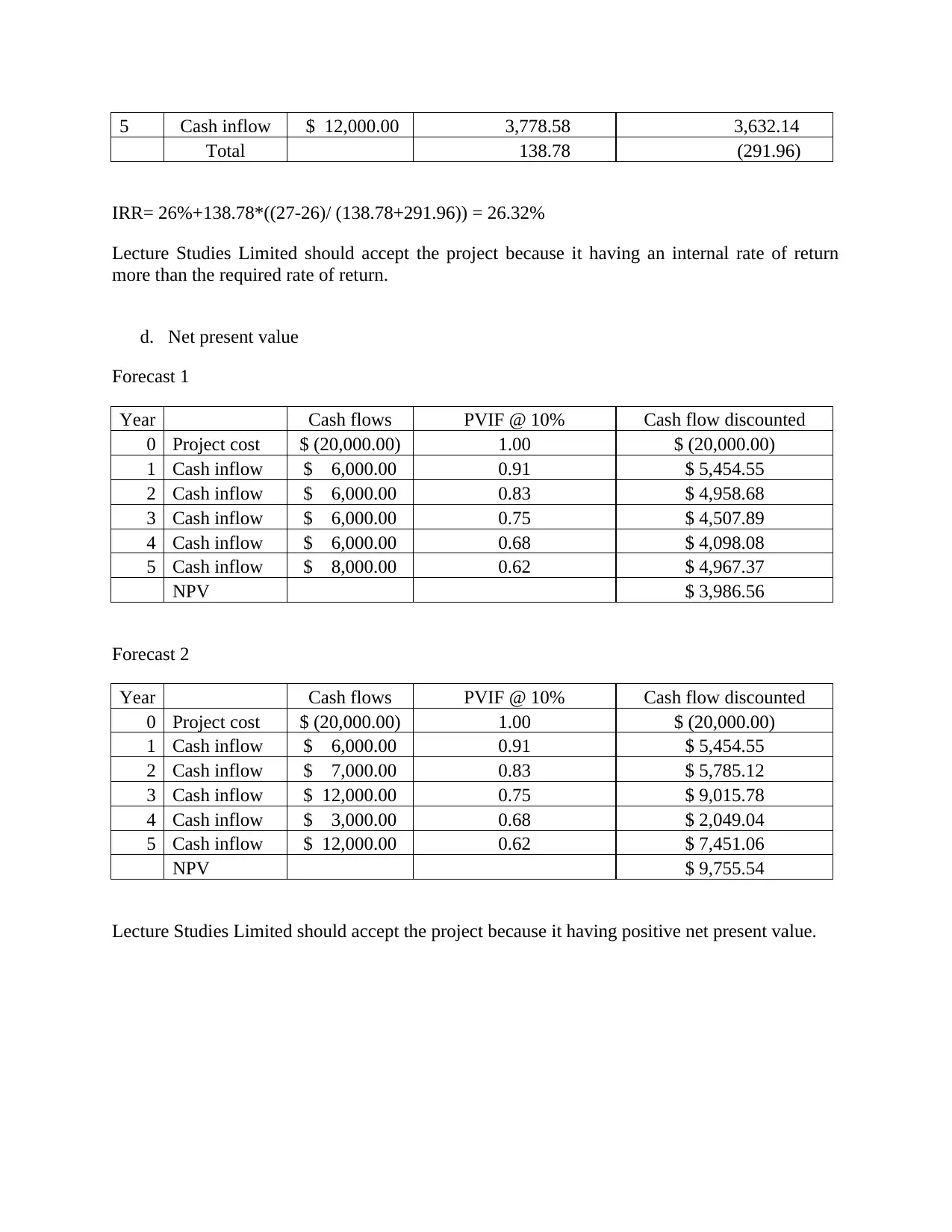

This finance assignment solution covers several key areas of financial analysis. The first question analyzes key performance indicators (KPIs), categorizing them as strategic or operating and driver or outcome-based. The second question focuses on budgeting, including sales, production, and purchases budgets, along with contribution margin and profit and loss forecasts. The third question explores breakeven analysis, calculating the breakeven point in units and dollars, and evaluating the impact of leasing new equipment. Finally, the fourth question delves into investment appraisal techniques, including accounting rate of return (ARR), payback period, internal rate of return (IRR), and net present value (NPV), with calculations for two different forecast scenarios, providing recommendations based on the results.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.