Financial Analysis Assignment: KPI, Budgeting, and Investment Analysis

VerifiedAdded on 2020/05/04

|8

|1197

|58

Homework Assignment

AI Summary

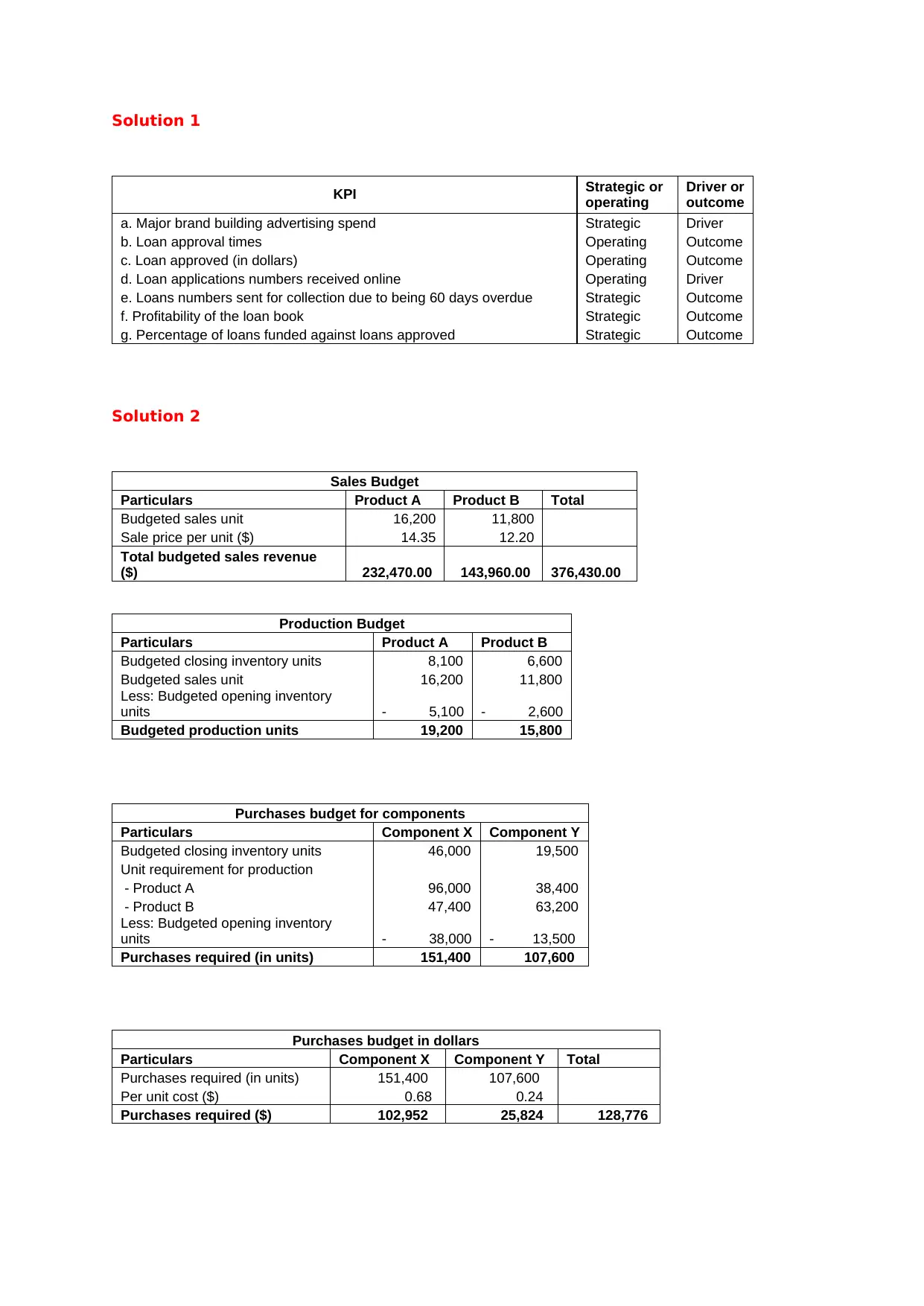

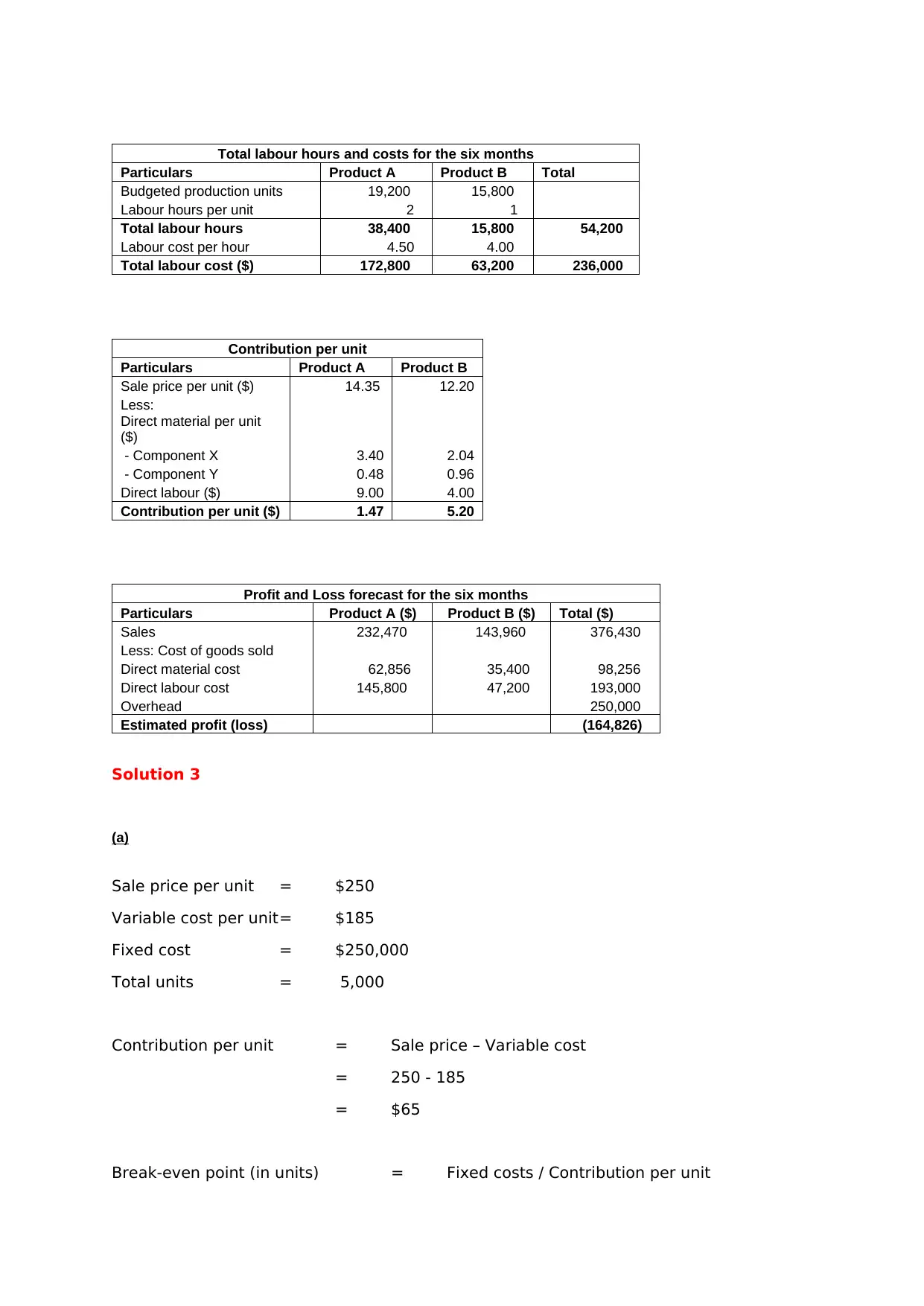

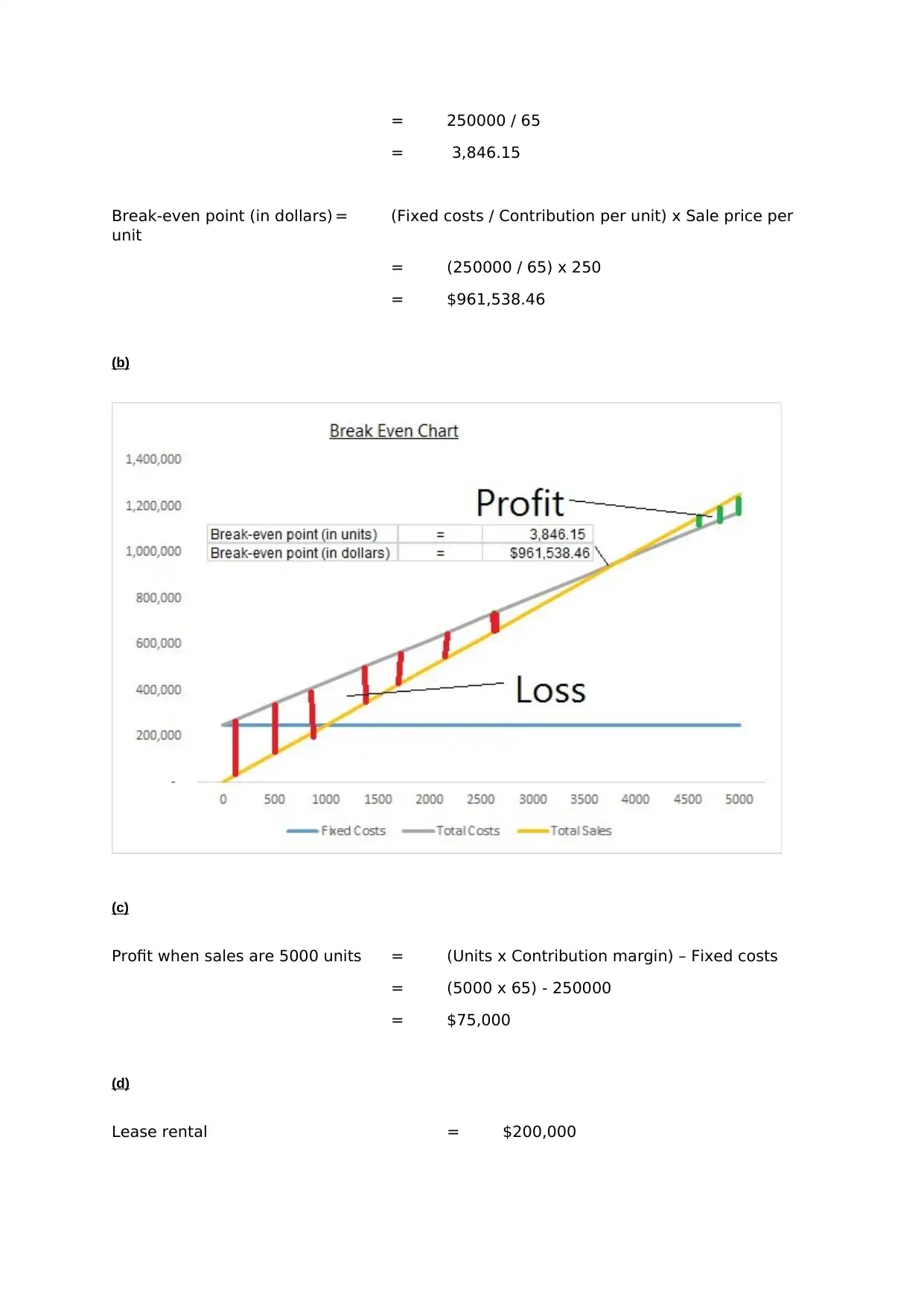

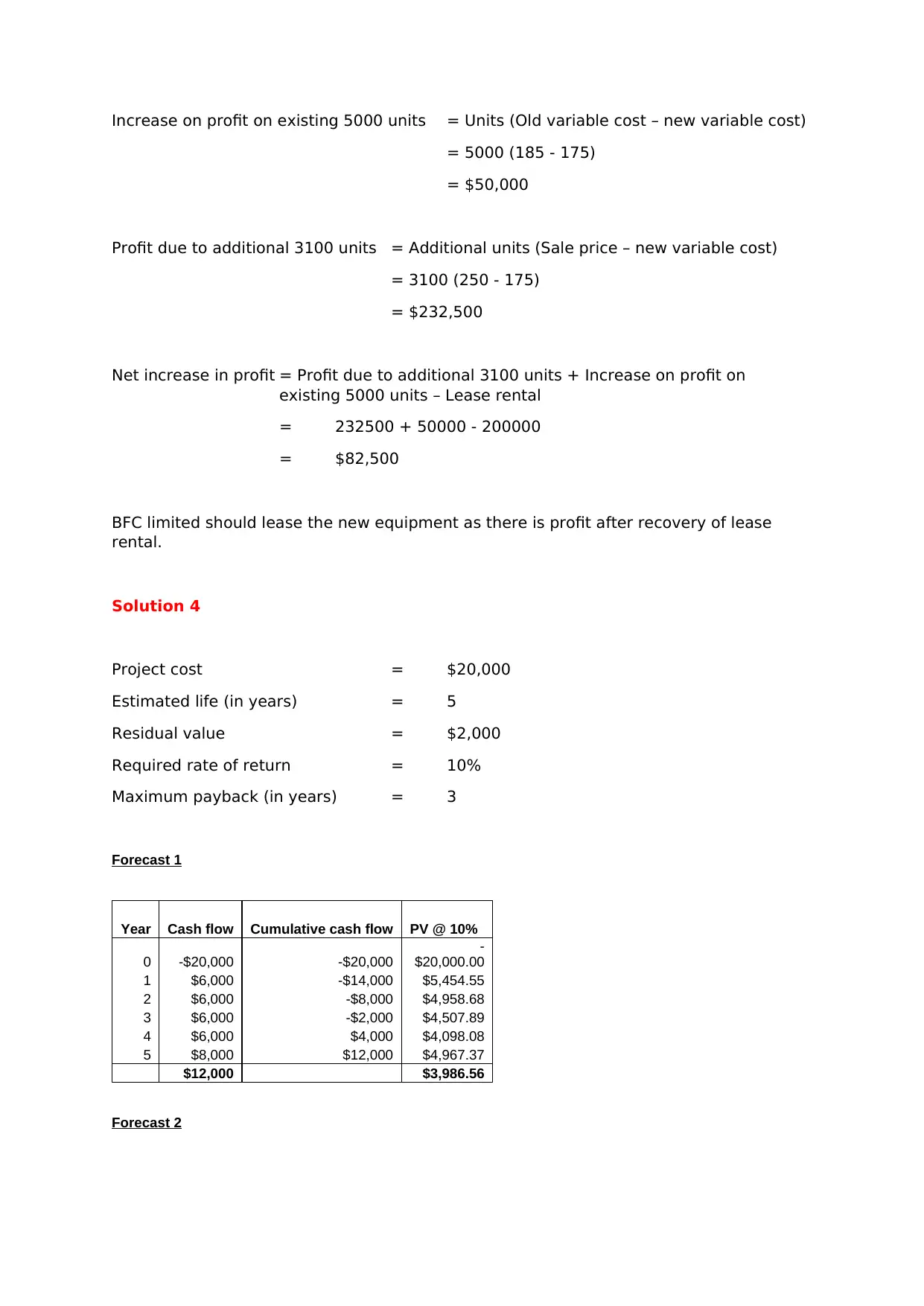

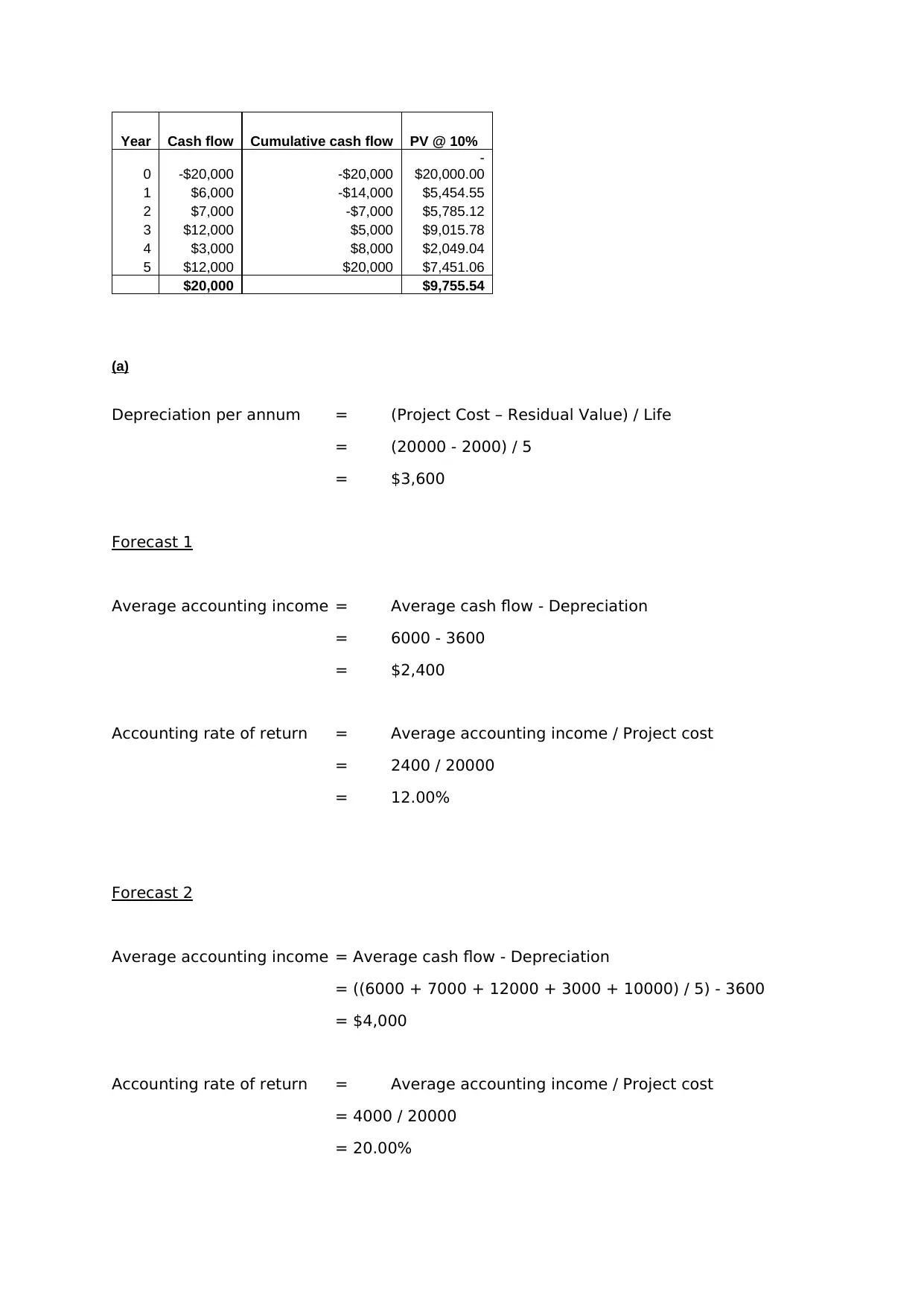

This finance assignment solution provides comprehensive answers to various financial analysis problems. Solution 1 focuses on Key Performance Indicators (KPIs), categorizing them as strategic drivers, operating drivers, and outcomes. Solution 2 presents sales and production budgets for two products, including detailed calculations for sales revenue, production units, purchases, labor costs, and contribution per unit. Solution 3 explores break-even analysis, profit calculations, and the impact of new equipment, considering lease rentals and variable cost changes. Finally, Solution 4 evaluates an investment project using different capital budgeting techniques, including accounting rate of return (ARR), payback period, internal rate of return (IRR), and net present value (NPV), with a comparative analysis of two forecast scenarios and a final recommendation based on the results.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.