Performance Management Report: Variance Analysis and Strategic Costing

VerifiedAdded on 2022/11/24

|12

|2854

|200

Report

AI Summary

This report delves into the realm of performance management, commencing with a detailed variance calculation for direct materials and labor, analyzing the company's production efficiency, and exploring the application of a Just-in-Time manufacturing system. The report proceeds to evaluate the impact of current and alternative policies, including contribution calculations and alignment with international guidelines. Section B further investigates lifecycle costing, outlining profit per unit over a three-year period, and addressing associated challenges. The report also examines the elements of a cost of quality report and its role in reducing costs and improving profitability. Finally, it explores the application of strategic cost management techniques in modern production environments, including strategic sourcing, world-class manufacturing, business process reengineering, and total quality management, providing a comprehensive overview of financial performance and cost control.

PERFORMANCE

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A.....................................................................................................................................4

Question 1...................................................................................................................................4

Variance calculation....................................................................................................................4

B)Performance of company........................................................................................................5

c) Just in time manufacturing system..........................................................................................6

Question 2...................................................................................................................................6

SECTION B.....................................................................................................................................8

Question 3...................................................................................................................................8

Question 5...................................................................................................................................9

REFERENCES..............................................................................................................................12

SECTION A.....................................................................................................................................4

Question 1...................................................................................................................................4

Variance calculation....................................................................................................................4

B)Performance of company........................................................................................................5

c) Just in time manufacturing system..........................................................................................6

Question 2...................................................................................................................................6

SECTION B.....................................................................................................................................8

Question 3...................................................................................................................................8

Question 5...................................................................................................................................9

REFERENCES..............................................................................................................................12

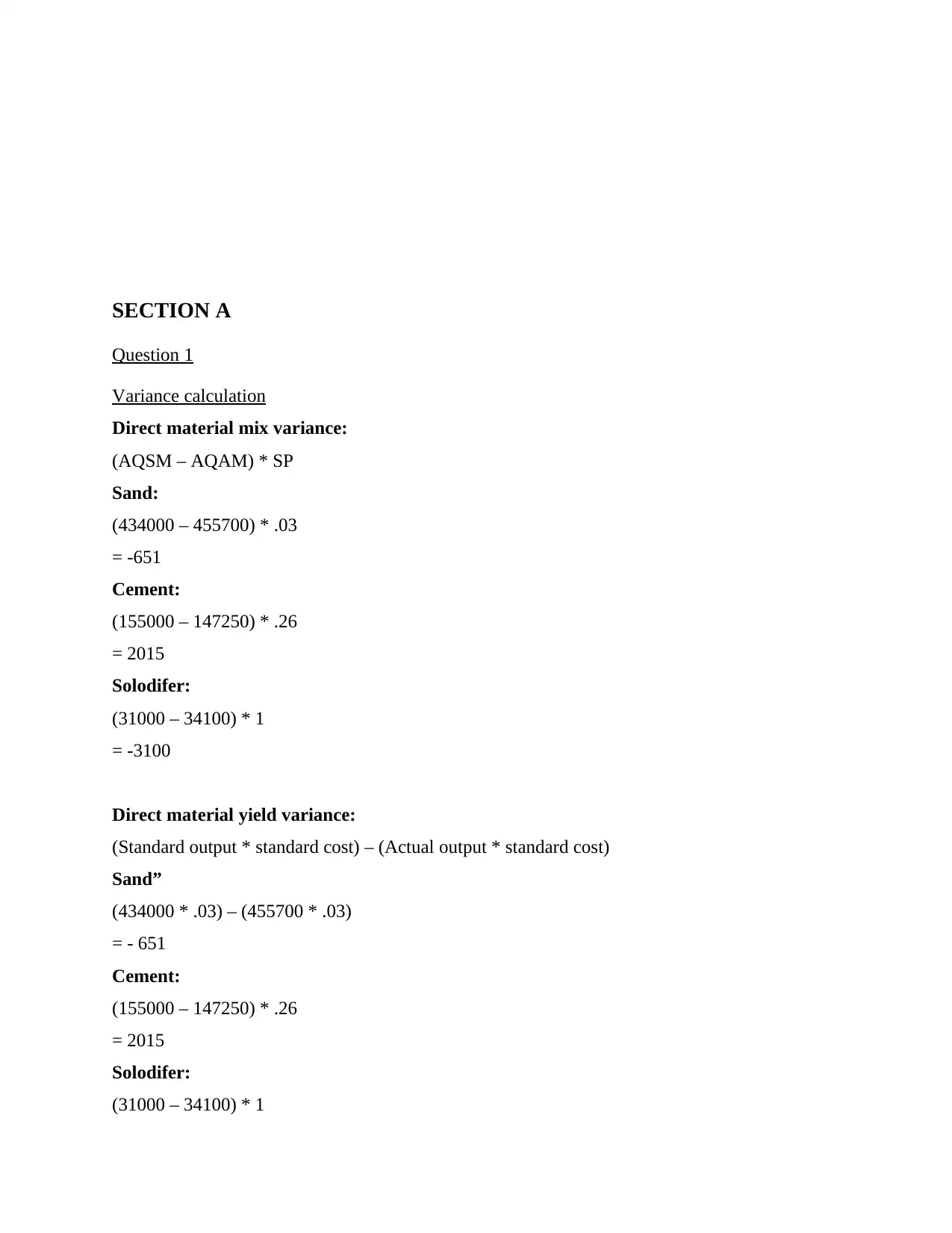

SECTION A

Question 1

Variance calculation

Direct material mix variance:

(AQSM – AQAM) * SP

Sand:

(434000 – 455700) * .03

= -651

Cement:

(155000 – 147250) * .26

= 2015

Solodifer:

(31000 – 34100) * 1

= -3100

Direct material yield variance:

(Standard output * standard cost) – (Actual output * standard cost)

Sand”

(434000 * .03) – (455700 * .03)

= - 651

Cement:

(155000 – 147250) * .26

= 2015

Solodifer:

(31000 – 34100) * 1

Question 1

Variance calculation

Direct material mix variance:

(AQSM – AQAM) * SP

Sand:

(434000 – 455700) * .03

= -651

Cement:

(155000 – 147250) * .26

= 2015

Solodifer:

(31000 – 34100) * 1

= -3100

Direct material yield variance:

(Standard output * standard cost) – (Actual output * standard cost)

Sand”

(434000 * .03) – (455700 * .03)

= - 651

Cement:

(155000 – 147250) * .26

= 2015

Solodifer:

(31000 – 34100) * 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= -3100

(Hence, the price remain the same which also could not change any result in respect to the

material usage variance and the material yield variance)

Direct labour mix variance

(Actual hrs used at standard mix – Actual hrs used at actual mix) * standard price

= (12 – 11.28) * 1.8

= 1.296

Direct labour yield variance

(Actual hrs used at standard mix – Actual output hrs used at standard mix) * standard price

= (5640 - 5828 ) * 1.8

= -338.4

Fixed overhead expenditure variance

Budgeted fixed overhead – Actual fixed overhead

= 30000 * .75 – 39432

= -16932

Fixed overhead volume capcity variance

Standard price * ( Budgeted hours – Actual Hours)

= .75 (30000 * 18 / 60 – 9114)

= -85.5

Fixed overhead volume efficiency variance

(Actual hours * fixed overhead rate) – (Standard hours * fixed overhead rate)

= (9114 * 2.75) – (9000 * 2.5)

= 2563.5

B)Performance of company

The performance of the business entity is found very effective as the production was

more than the expected or the standard level of activity. The role of the efficiency of the business

entity is very significant in nature that can certainly indicated and demonstrated the fact that the

factors certainly influence the business performance under the respective market. The production

(Hence, the price remain the same which also could not change any result in respect to the

material usage variance and the material yield variance)

Direct labour mix variance

(Actual hrs used at standard mix – Actual hrs used at actual mix) * standard price

= (12 – 11.28) * 1.8

= 1.296

Direct labour yield variance

(Actual hrs used at standard mix – Actual output hrs used at standard mix) * standard price

= (5640 - 5828 ) * 1.8

= -338.4

Fixed overhead expenditure variance

Budgeted fixed overhead – Actual fixed overhead

= 30000 * .75 – 39432

= -16932

Fixed overhead volume capcity variance

Standard price * ( Budgeted hours – Actual Hours)

= .75 (30000 * 18 / 60 – 9114)

= -85.5

Fixed overhead volume efficiency variance

(Actual hours * fixed overhead rate) – (Standard hours * fixed overhead rate)

= (9114 * 2.75) – (9000 * 2.5)

= 2563.5

B)Performance of company

The performance of the business entity is found very effective as the production was

more than the expected or the standard level of activity. The role of the efficiency of the business

entity is very significant in nature that can certainly indicated and demonstrated the fact that the

factors certainly influence the business performance under the respective market. The production

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

was expected as 30000 and the actual was 31000 that certainly indicate that company has

achieved better production of the material. This can demonstrate the fact that the actual

production output is more than the budgets that could certainly influence the business operations

of the entity (Singh and Verma, 2018). The organisation is exploring different types of material

such as sand, cement and solidifier. All three are the different types of material usage that can

indicate the business unit to effectively consume the material use.

c) Just in time manufacturing system

Just in time manufacturing system is a process that indicate about the production based

on the requirements. Under this company initiate the production process at the time of the need

of the product. The supply under this is very specific and very fast forward so that at any point if

the company need material than the availability become smooth. This is a standard practice of

just in time when the business entity explore the material and utilises it in such way that

company get to easily convert the material into final production. Standard costing system is all

about setting standards regarding the cost of material consumption to set the proper pricing

(Mishra Wu and Sarkar, 2021). The business entity consume the collaborative approach for the

just in time and standard costing where the standards are set regarding the cost and the

manufacturing process start with the just in time practice. Both the practices are combined to

make the best level of control over the process. Both the approaches are very specific as the

standard cost strategically allow the company to charge prices against the material consumption

and the just in time system favour the business entity to run manufacturing only when it is

required for the business unit. Both the practices strategically empower the organisation to

control the costing. This make product more cost friendly and also enhances the profit margins of

the business unit.

Question 2

(a) Impact of current policy

The existing policy is to transfer the product to other department. This policy certainly

increases the cost of the production. AS the transfer cost £20. This cost is extra and included just

as a charge of transferring the product to other department. Company can consume the

alternative policy where it can keep the product in the same department that will further reduces

achieved better production of the material. This can demonstrate the fact that the actual

production output is more than the budgets that could certainly influence the business operations

of the entity (Singh and Verma, 2018). The organisation is exploring different types of material

such as sand, cement and solidifier. All three are the different types of material usage that can

indicate the business unit to effectively consume the material use.

c) Just in time manufacturing system

Just in time manufacturing system is a process that indicate about the production based

on the requirements. Under this company initiate the production process at the time of the need

of the product. The supply under this is very specific and very fast forward so that at any point if

the company need material than the availability become smooth. This is a standard practice of

just in time when the business entity explore the material and utilises it in such way that

company get to easily convert the material into final production. Standard costing system is all

about setting standards regarding the cost of material consumption to set the proper pricing

(Mishra Wu and Sarkar, 2021). The business entity consume the collaborative approach for the

just in time and standard costing where the standards are set regarding the cost and the

manufacturing process start with the just in time practice. Both the practices are combined to

make the best level of control over the process. Both the approaches are very specific as the

standard cost strategically allow the company to charge prices against the material consumption

and the just in time system favour the business entity to run manufacturing only when it is

required for the business unit. Both the practices strategically empower the organisation to

control the costing. This make product more cost friendly and also enhances the profit margins of

the business unit.

Question 2

(a) Impact of current policy

The existing policy is to transfer the product to other department. This policy certainly

increases the cost of the production. AS the transfer cost £20. This cost is extra and included just

as a charge of transferring the product to other department. Company can consume the

alternative policy where it can keep the product in the same department that will further reduces

the transfer cost. This would certainly increase the profitability of the business unit. This policy

is effective enough to maximise the profit of the business unit.

(b) Contribution calculation

Marple division:

22 – 8 – 4- 3

= 7

Poirot division:

80 – 40 - 10 – 8 - 5

= 17

Christie Division

= 7 + 17

= 24

Alternative option

= 80 – 10 – 8 – 5 – 8 – 4 – 3

= 42

Alternative policy achieve objectives

The alternative policy allow the company to achieve the cost minimisation objective,

profit making objective, customer satisfaction objective and brand value maximisation

objectives. All these are the four different objectives that could have been addressed by the

alternative policy (Song And et.al., 2020). This practice would favour the business unit to

certainly empower and favour the business entity to mitigate different objectives that can support

and favour the business unit to achieve the various business objectives. The role of the policy is

significant in nature that can favour the suborganisation to empower the various aspects and

objectives of the business entity.

Alternative policy mitigate international guidelines

The international guidelines is more like consumer oriented and favour the target

customer's need and requirements. The alternative policy would reduce the transfer cost that

would also allow the company to offer the product at a best price possible. This would certainly

allow the business entity to mitigate the international guidelines where the product are sale based

on the needs and requirements of the potential customers (Dillon, Oliveira and Abbasi, 2017).

This is essential for the business unit to ensure the proper form of development at an

is effective enough to maximise the profit of the business unit.

(b) Contribution calculation

Marple division:

22 – 8 – 4- 3

= 7

Poirot division:

80 – 40 - 10 – 8 - 5

= 17

Christie Division

= 7 + 17

= 24

Alternative option

= 80 – 10 – 8 – 5 – 8 – 4 – 3

= 42

Alternative policy achieve objectives

The alternative policy allow the company to achieve the cost minimisation objective,

profit making objective, customer satisfaction objective and brand value maximisation

objectives. All these are the four different objectives that could have been addressed by the

alternative policy (Song And et.al., 2020). This practice would favour the business unit to

certainly empower and favour the business entity to mitigate different objectives that can support

and favour the business unit to achieve the various business objectives. The role of the policy is

significant in nature that can favour the suborganisation to empower the various aspects and

objectives of the business entity.

Alternative policy mitigate international guidelines

The international guidelines is more like consumer oriented and favour the target

customer's need and requirements. The alternative policy would reduce the transfer cost that

would also allow the company to offer the product at a best price possible. This would certainly

allow the business entity to mitigate the international guidelines where the product are sale based

on the needs and requirements of the potential customers (Dillon, Oliveira and Abbasi, 2017).

This is essential for the business unit to ensure the proper form of development at an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

international level. The international standard are more like customer friendly and oriented in

nature. Transfer pricing must be favourable only when it is consuming extra cost to transfer the

product and require some level of modification that can only entertain through transfer the

production. The international guidelines allow the transfer only when it is required. The

alternative policy would support the international guidelines.

nature. Transfer pricing must be favourable only when it is consuming extra cost to transfer the

product and require some level of modification that can only entertain through transfer the

production. The international guidelines allow the transfer only when it is required. The

alternative policy would support the international guidelines.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION B

Question 3

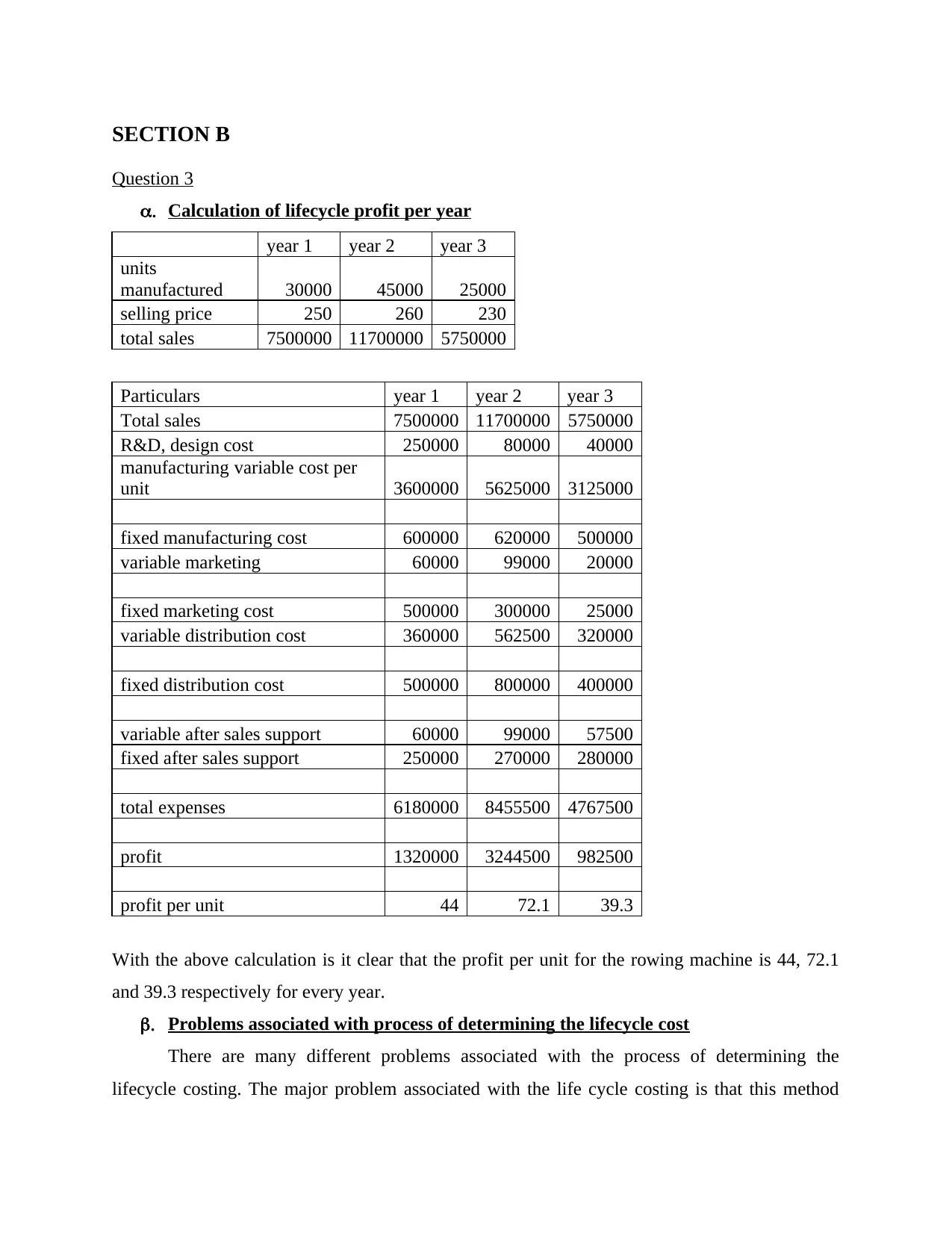

a. Calculation of lifecycle profit per year

year 1 year 2 year 3

units

manufactured 30000 45000 25000

selling price 250 260 230

total sales 7500000 11700000 5750000

Particulars year 1 year 2 year 3

Total sales 7500000 11700000 5750000

R&D, design cost 250000 80000 40000

manufacturing variable cost per

unit 3600000 5625000 3125000

fixed manufacturing cost 600000 620000 500000

variable marketing 60000 99000 20000

fixed marketing cost 500000 300000 25000

variable distribution cost 360000 562500 320000

fixed distribution cost 500000 800000 400000

variable after sales support 60000 99000 57500

fixed after sales support 250000 270000 280000

total expenses 6180000 8455500 4767500

profit 1320000 3244500 982500

profit per unit 44 72.1 39.3

With the above calculation is it clear that the profit per unit for the rowing machine is 44, 72.1

and 39.3 respectively for every year.

b. Problems associated with process of determining the lifecycle cost

There are many different problems associated with the process of determining the

lifecycle costing. The major problem associated with the life cycle costing is that this method

Question 3

a. Calculation of lifecycle profit per year

year 1 year 2 year 3

units

manufactured 30000 45000 25000

selling price 250 260 230

total sales 7500000 11700000 5750000

Particulars year 1 year 2 year 3

Total sales 7500000 11700000 5750000

R&D, design cost 250000 80000 40000

manufacturing variable cost per

unit 3600000 5625000 3125000

fixed manufacturing cost 600000 620000 500000

variable marketing 60000 99000 20000

fixed marketing cost 500000 300000 25000

variable distribution cost 360000 562500 320000

fixed distribution cost 500000 800000 400000

variable after sales support 60000 99000 57500

fixed after sales support 250000 270000 280000

total expenses 6180000 8455500 4767500

profit 1320000 3244500 982500

profit per unit 44 72.1 39.3

With the above calculation is it clear that the profit per unit for the rowing machine is 44, 72.1

and 39.3 respectively for every year.

b. Problems associated with process of determining the lifecycle cost

There are many different problems associated with the process of determining the

lifecycle costing. The major problem associated with the life cycle costing is that this method

spreads the expenses relating to the asset out evenly over several years (Al-Naser and Mohamed,

2017). In addition to this another drawback of problem associated with the life cycle costing

method is that it assumes that the asset will remain productive for the years when it is new and

later on its capacity will reduce. In addition to this another drawback attached with the use of this

method is that it is time consuming. This is particularly because of the reason that when each and

every cost relating to the asset need to be calculate then it takes a lot of time.

c. Main element of cost of quality report and how it assists in reducing cost and

improving profitability

The cost of quality is being defined as the methodology which assist company to

determine the fact that which resources are used for activities which prevent poor quality and to

improve and apprises the quality of the product or service. This is essential because of quality

report will not be managed and made in proper and effective manner then this will improve the

performance. the major element of cost of quality report involves the prevention cost, appraisal

cost, internal failure cost and external failure cost (Janjić, Karapavlović and Damjanović, 2017).

These reports help the business to reduce the cost and to improve the profitability of the

company. this is pertaining to the fact that under this all the cost are being recorded and company

can analyse that how the cost can be minimised. This minimisation of the cost will result in

increase in the profitability of the company.

Question 5

a. Use of strategic cost management technique in modern production environment

The strategic cost management is being defined as the cost management techniques

which are assistive in reducing the cost along with strengthening the position of the business. this

majorly aims at combining the decision making structure with the cost information for the

reinforcing the business strategy as a whole. There are many different types of cost management

strategies and techniques which assist the business in managing and maintaining the production

of the company in the modern production environment (Adigbole and Osemene, 2019). For the

successful implementation of the just in time (JIT) production principle within the modern

production environment there need to be proper use of these different strategic cost management

techniques. Hence there are many different types of the strategies relating to strategic cost

management which are discussed as follows-

2017). In addition to this another drawback of problem associated with the life cycle costing

method is that it assumes that the asset will remain productive for the years when it is new and

later on its capacity will reduce. In addition to this another drawback attached with the use of this

method is that it is time consuming. This is particularly because of the reason that when each and

every cost relating to the asset need to be calculate then it takes a lot of time.

c. Main element of cost of quality report and how it assists in reducing cost and

improving profitability

The cost of quality is being defined as the methodology which assist company to

determine the fact that which resources are used for activities which prevent poor quality and to

improve and apprises the quality of the product or service. This is essential because of quality

report will not be managed and made in proper and effective manner then this will improve the

performance. the major element of cost of quality report involves the prevention cost, appraisal

cost, internal failure cost and external failure cost (Janjić, Karapavlović and Damjanović, 2017).

These reports help the business to reduce the cost and to improve the profitability of the

company. this is pertaining to the fact that under this all the cost are being recorded and company

can analyse that how the cost can be minimised. This minimisation of the cost will result in

increase in the profitability of the company.

Question 5

a. Use of strategic cost management technique in modern production environment

The strategic cost management is being defined as the cost management techniques

which are assistive in reducing the cost along with strengthening the position of the business. this

majorly aims at combining the decision making structure with the cost information for the

reinforcing the business strategy as a whole. There are many different types of cost management

strategies and techniques which assist the business in managing and maintaining the production

of the company in the modern production environment (Adigbole and Osemene, 2019). For the

successful implementation of the just in time (JIT) production principle within the modern

production environment there need to be proper use of these different strategic cost management

techniques. Hence there are many different types of the strategies relating to strategic cost

management which are discussed as follows-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic sourcing- strategic sourcing is being defined as the process of developing

channels at lowest total cost and not focus only on the lowest purchase price. In the

modern production environment, the strategic sourcing is being used as this is the

procurement process which connects the data collected with the market research to reach

to minimum expenses (Verma and Aggarwal, 2021). There are generally three steps in

strategic sourcing wherein first stage involves team to complete the survey over total

expenditure. Further the next step is to conduct the supplier market assessment. The last

step is to have supplier survey for developing supplier to analyse which supplier is

providing the at lowest prices.

World class manufacturing- this is a tool which combines the manufacturing and the

engineering for producing the automotive solutions for the leading global brands. This

involves the different set of policies, practices, principles and concept developed for the

management and operation of manufacturing companies. In the modern manufacturing

environment, the world class manufacturing is very helpful as it is a process driven

approach which is applicable in managing the overall business work flow and result in

proper and effective working of the business.

Business process re- engineering – the Business Process Reengineering (BPR) is a

practice which assist in rethinking and redesigning of the manner a work need to be done

for attaining objective of business. in the modern production environment this is very

important because BPR will provide ways of working within the modern world. this

majorly involve focus on use of modern technology for enhancing the data and next they

alter the functional areas for effective management.

Total quality management- it is a system or structure approach which assist in overall

management of the company. the major focus of this process is to improve the quality

and if quality is already good then it need to be maintained. For working effectively in

the modern production environment it is very essential that the TQM is managed so that

the output of the operations is better and effective.

Thus, all these aspects collectively assist in proper and effective management of the business and

attaining the objectives in proper and effective manner. Hence, in case these principles ate

effectively applied in the business then this will result in effective production and attainment of

the business objectives.

channels at lowest total cost and not focus only on the lowest purchase price. In the

modern production environment, the strategic sourcing is being used as this is the

procurement process which connects the data collected with the market research to reach

to minimum expenses (Verma and Aggarwal, 2021). There are generally three steps in

strategic sourcing wherein first stage involves team to complete the survey over total

expenditure. Further the next step is to conduct the supplier market assessment. The last

step is to have supplier survey for developing supplier to analyse which supplier is

providing the at lowest prices.

World class manufacturing- this is a tool which combines the manufacturing and the

engineering for producing the automotive solutions for the leading global brands. This

involves the different set of policies, practices, principles and concept developed for the

management and operation of manufacturing companies. In the modern manufacturing

environment, the world class manufacturing is very helpful as it is a process driven

approach which is applicable in managing the overall business work flow and result in

proper and effective working of the business.

Business process re- engineering – the Business Process Reengineering (BPR) is a

practice which assist in rethinking and redesigning of the manner a work need to be done

for attaining objective of business. in the modern production environment this is very

important because BPR will provide ways of working within the modern world. this

majorly involve focus on use of modern technology for enhancing the data and next they

alter the functional areas for effective management.

Total quality management- it is a system or structure approach which assist in overall

management of the company. the major focus of this process is to improve the quality

and if quality is already good then it need to be maintained. For working effectively in

the modern production environment it is very essential that the TQM is managed so that

the output of the operations is better and effective.

Thus, all these aspects collectively assist in proper and effective management of the business and

attaining the objectives in proper and effective manner. Hence, in case these principles ate

effectively applied in the business then this will result in effective production and attainment of

the business objectives.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Impact firms factor for the successful implementation of JIT production principles

There are many different factors which creates an impact over the successful

implementation of the JIT production principles. Hence, it is essential for the company that they

must effectively take into consideration all these factors.

Close geographical proximity of supplier and customer- at time of implementing the JIT

principles there need to be a close proximity of geographical proximity of supplier and

customers. This is because of the reason that when the supplier and consumer will be

placed nearby then this will result in effective implementation of the principles of JIT

(Shehadeh, 2017).

Highly competitive market- this also assist in effective implementation of the JIT

principles. This is particularly because of the reason that when the market will be highly

competitive then this will result in the effective management of operations and company

will be competent in facing the intense competition.

Flexible manufacturing technology- the flexible manufacturing system (FMS) is being

designed in order to be readily adapted to changes within the quantity of goods being

produced. This will also assist in proper management of the overall production and

reduction of the labour and other cost as well.

Low degree of vertical integration- for having successful implementation of the JIT

production principles it is essential to consider the degree of vertical integration as well.

this is particularly because of the reason that if there is option of vertical integration then

this will improve the working efficiency of the company.

There are many different factors which creates an impact over the successful

implementation of the JIT production principles. Hence, it is essential for the company that they

must effectively take into consideration all these factors.

Close geographical proximity of supplier and customer- at time of implementing the JIT

principles there need to be a close proximity of geographical proximity of supplier and

customers. This is because of the reason that when the supplier and consumer will be

placed nearby then this will result in effective implementation of the principles of JIT

(Shehadeh, 2017).

Highly competitive market- this also assist in effective implementation of the JIT

principles. This is particularly because of the reason that when the market will be highly

competitive then this will result in the effective management of operations and company

will be competent in facing the intense competition.

Flexible manufacturing technology- the flexible manufacturing system (FMS) is being

designed in order to be readily adapted to changes within the quantity of goods being

produced. This will also assist in proper management of the overall production and

reduction of the labour and other cost as well.

Low degree of vertical integration- for having successful implementation of the JIT

production principles it is essential to consider the degree of vertical integration as well.

this is particularly because of the reason that if there is option of vertical integration then

this will improve the working efficiency of the company.

REFERENCES

Books and Journals

Adigbole, E. and Osemene, O., 2019. Strategic Cost Management And Accuracy Of Cost

Information In Selected Manufacturing Firms In Lagos And Ogun States, Nigeria.

International Journal of Accounting and Finance (IJAF). 8(1). pp.129-151.

Al-Naser, K. H. Y. and Mohamed, R., 2017. The integration between strategic cost management

techniques to improve the performance of Iraqi manufacturing companies. Asian Journal of

Finance & Accounting. 9(1). pp.210-223.

Dillon, M., Oliveira, F. and Abbasi, B., 2017. A two-stage stochastic programming model for

inventory management in the blood supply chain. International Journal of Production

Economics. 187. pp.27-41.

Janjić, V., Karapavlović, N. and Damjanović, J., 2017. Techniques of strategic cost

management–the case of Serbia. Teme, pp.441-455.

Mishra, U., Wu, J. Z. and Sarkar, B., 2021. Optimum sustainable inventory management with

backorder and deterioration under controllable carbon emissions. Journal of Cleaner

Production. 279. p.123699.

Shehadeh, M. A., 2017. Comprehensive Study on Strategic Management Accounting Techniques

in Jordan Banks. Asian Journal of Management. 8(2). pp.353-356.

Singh, D. and Verma, A., 2018. Inventory management in supply chain. Materials Today:

Proceedings. 5(2). pp.3867-3872.

Song, J.S. And et.al., 2020. Capacity and inventory management: Review, trends, and

projections. Manufacturing & Service Operations Management. 22(1). pp.36-46.

Verma, T. and Aggarwal, R., 2021. Developing a Framework to Study the Impact of Contingent

Factors on Business Performance Using Strategic Cost Management: A Meta-Analysis

Study. In Big Data Analytics for Improved Accuracy, Efficiency, and Decision Making in

Digital Marketing (pp. 227-253). IGI Global.

Books and Journals

Adigbole, E. and Osemene, O., 2019. Strategic Cost Management And Accuracy Of Cost

Information In Selected Manufacturing Firms In Lagos And Ogun States, Nigeria.

International Journal of Accounting and Finance (IJAF). 8(1). pp.129-151.

Al-Naser, K. H. Y. and Mohamed, R., 2017. The integration between strategic cost management

techniques to improve the performance of Iraqi manufacturing companies. Asian Journal of

Finance & Accounting. 9(1). pp.210-223.

Dillon, M., Oliveira, F. and Abbasi, B., 2017. A two-stage stochastic programming model for

inventory management in the blood supply chain. International Journal of Production

Economics. 187. pp.27-41.

Janjić, V., Karapavlović, N. and Damjanović, J., 2017. Techniques of strategic cost

management–the case of Serbia. Teme, pp.441-455.

Mishra, U., Wu, J. Z. and Sarkar, B., 2021. Optimum sustainable inventory management with

backorder and deterioration under controllable carbon emissions. Journal of Cleaner

Production. 279. p.123699.

Shehadeh, M. A., 2017. Comprehensive Study on Strategic Management Accounting Techniques

in Jordan Banks. Asian Journal of Management. 8(2). pp.353-356.

Singh, D. and Verma, A., 2018. Inventory management in supply chain. Materials Today:

Proceedings. 5(2). pp.3867-3872.

Song, J.S. And et.al., 2020. Capacity and inventory management: Review, trends, and

projections. Manufacturing & Service Operations Management. 22(1). pp.36-46.

Verma, T. and Aggarwal, R., 2021. Developing a Framework to Study the Impact of Contingent

Factors on Business Performance Using Strategic Cost Management: A Meta-Analysis

Study. In Big Data Analytics for Improved Accuracy, Efficiency, and Decision Making in

Digital Marketing (pp. 227-253). IGI Global.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.