PERSONAL FINANCIAL MANAGEMENT.

VerifiedAdded on 2023/04/07

|17

|3280

|206

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

PERSONAL FINANCIAL MANAGEMENT

1

PERSONAL FINANCES

Student’s name

Professor’s name

Assignment No

Date

1

PERSONAL FINANCES

Student’s name

Professor’s name

Assignment No

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PERSONAL FINANCIAL MANAGEMENT

2

INTRODUCTION

“The management of personal finance is a crucial aspect that needs to be thought of

before disseminating any decision that may affect the wealth status of an individual,” (Chan,

2010). This paper will major on the different elements of wealth, i.e., wealth planning and wealth

giving through various facets of tax planning and insurance planning as discussed below;

QUIZ 1

WEALTH PROTECTION- TAX PLANNING

An individual has the option to protect his or her wealth from additional liabilities by

utilizing the available incentives through efficient tax planning and insurance planning. Tax

planning and insurance planning are valuable tools that a person can use to minimize on the

outstanding liabilities.

1a. Tax avoidance vs. tax evasion

John, Hanlon & Nemit (2013), Tax avoidance is legal, and it involves an individual or

corporation avoiding or minimizing his tax liabilities through efficient tax planning. That is by

utilizing the available tax incentives to reduce the tax liability. Tax evasion is an illegal activity

whereby the individual or corporation avoids to pay taxes for example by transferring assets or

by stating a lower income than the actual.

Examples of tax avoidance

I. Dr. Smart can make use of the CPF contributions for instance by making high savings thus

reducing the tax liability.

2

INTRODUCTION

“The management of personal finance is a crucial aspect that needs to be thought of

before disseminating any decision that may affect the wealth status of an individual,” (Chan,

2010). This paper will major on the different elements of wealth, i.e., wealth planning and wealth

giving through various facets of tax planning and insurance planning as discussed below;

QUIZ 1

WEALTH PROTECTION- TAX PLANNING

An individual has the option to protect his or her wealth from additional liabilities by

utilizing the available incentives through efficient tax planning and insurance planning. Tax

planning and insurance planning are valuable tools that a person can use to minimize on the

outstanding liabilities.

1a. Tax avoidance vs. tax evasion

John, Hanlon & Nemit (2013), Tax avoidance is legal, and it involves an individual or

corporation avoiding or minimizing his tax liabilities through efficient tax planning. That is by

utilizing the available tax incentives to reduce the tax liability. Tax evasion is an illegal activity

whereby the individual or corporation avoids to pay taxes for example by transferring assets or

by stating a lower income than the actual.

Examples of tax avoidance

I. Dr. Smart can make use of the CPF contributions for instance by making high savings thus

reducing the tax liability.

PERSONAL FINANCIAL MANAGEMENT

3

II. Filing for an assessment that is separate with that of his wife will also get tax benefits to

them.

III. Dr. Smart can also avoid tax liabilities by reducing the amounts of dividends received from

the company and instead retain the profits.

Examples of tax evasion

I. Dr. Smart can illegally avoid paying taxes by filing an incorrect return on his income that is

lower than the actual salary he gets.

II. Also, he may evade taxes by transferring some of his assets to another person to reduce his

tax liability.

III. Dr. Smart can evade paying taxes through claiming illegitimate tax reliefs that he should

not claim.

It is evident that by utilizing the available tax incentives, Dr. Smart can avoid or reduce

his tax liabilities legally without breaking the law instead of evading from paying taxes. Tax

evasion is considered as an illegal activity that may cause one to be charged fines or even being

jailed depending on the offense that one has committed.

1b(i) Tax implications

A tax implication is considered as the effect that a tax policy of a given tax system in

your country has on your income or profits gained. The tax implication on a given income is

provided as per the Income Tax Act of Singapore;

3

II. Filing for an assessment that is separate with that of his wife will also get tax benefits to

them.

III. Dr. Smart can also avoid tax liabilities by reducing the amounts of dividends received from

the company and instead retain the profits.

Examples of tax evasion

I. Dr. Smart can illegally avoid paying taxes by filing an incorrect return on his income that is

lower than the actual salary he gets.

II. Also, he may evade taxes by transferring some of his assets to another person to reduce his

tax liability.

III. Dr. Smart can evade paying taxes through claiming illegitimate tax reliefs that he should

not claim.

It is evident that by utilizing the available tax incentives, Dr. Smart can avoid or reduce

his tax liabilities legally without breaking the law instead of evading from paying taxes. Tax

evasion is considered as an illegal activity that may cause one to be charged fines or even being

jailed depending on the offense that one has committed.

1b(i) Tax implications

A tax implication is considered as the effect that a tax policy of a given tax system in

your country has on your income or profits gained. The tax implication on a given income is

provided as per the Income Tax Act of Singapore;

PERSONAL FINANCIAL MANAGEMENT

4

I. Salary to Dr. Smart’s wife

The wages of the wife would be taxed under the husband’s if they controlled more than

twelve and a half percent (12 ½%) of the shares in the company. Before the year 2005, there was

just a combined assessment where a married woman’s income was charged under the husband’s

name unless she filed for an evaluation separate from the husband. The income/salary of Dr.

Smart’s wife is taxable at the rate of 15%-22%.

II. Director fee to Dr. Brilliant’s mother

The tax implication is that the mother’s income will be taxed separately as her income

and it will not be included to that of the son, Dr. Brilliant. Since the mother is residing in

Australia, we consider her to be a non-resident. The income should have been exempted from tax

but this does not apply if one is working as a director of a company thus the director fee of the

mother will be taxed at a rate of 22% which is withholding tax and at a rate of 20% if it is prior

to the year of income 2017.

If the mother was present in Singapore for 183 days, then her income will be taxed as a resident

of the country.

Calculation

NB: Assuming there is no other income

= 22% * $120,000

4

I. Salary to Dr. Smart’s wife

The wages of the wife would be taxed under the husband’s if they controlled more than

twelve and a half percent (12 ½%) of the shares in the company. Before the year 2005, there was

just a combined assessment where a married woman’s income was charged under the husband’s

name unless she filed for an evaluation separate from the husband. The income/salary of Dr.

Smart’s wife is taxable at the rate of 15%-22%.

II. Director fee to Dr. Brilliant’s mother

The tax implication is that the mother’s income will be taxed separately as her income

and it will not be included to that of the son, Dr. Brilliant. Since the mother is residing in

Australia, we consider her to be a non-resident. The income should have been exempted from tax

but this does not apply if one is working as a director of a company thus the director fee of the

mother will be taxed at a rate of 22% which is withholding tax and at a rate of 20% if it is prior

to the year of income 2017.

If the mother was present in Singapore for 183 days, then her income will be taxed as a resident

of the country.

Calculation

NB: Assuming there is no other income

= 22% * $120,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PERSONAL FINANCIAL MANAGEMENT

5

= 22/100 * $120,000

Ans = $ 26,400

The payment date of this withholding tax is due on the earliest of;

When the payment becomes due and is payable as per the contract or agreement.

When there is no agreement, it is on the date of the invoice.

When the account of the non-resident has been credited with the payment amount.

On the actual payment date.

Salary to sparkle

The income of sparkle will be taxed separately from the father. Sparkle is considered to

be a resident of Singapore, and we assume that he is an adult; thus, his income of $ 80,000 will

be taxed individually.

1b(ii) Tax liabilities for Dr. Smart

I. Company car

Cost of the car =$ 210,000

Running expenses = $ 25,000

Total mileage = $ 15,000

40% - business use

60% - private use

5

= 22/100 * $120,000

Ans = $ 26,400

The payment date of this withholding tax is due on the earliest of;

When the payment becomes due and is payable as per the contract or agreement.

When there is no agreement, it is on the date of the invoice.

When the account of the non-resident has been credited with the payment amount.

On the actual payment date.

Salary to sparkle

The income of sparkle will be taxed separately from the father. Sparkle is considered to

be a resident of Singapore, and we assume that he is an adult; thus, his income of $ 80,000 will

be taxed individually.

1b(ii) Tax liabilities for Dr. Smart

I. Company car

Cost of the car =$ 210,000

Running expenses = $ 25,000

Total mileage = $ 15,000

40% - business use

60% - private use

PERSONAL FINANCIAL MANAGEMENT

6

Business use = 40/100 * $15,000

= $ 6,000

Private use = 60/100 * 1500

= $ 9,000

Residual value = $ 32,000

Calculation

NB: Any expenses incurred in the course of business purposes is not taxable; thus, we will

deduct the $ 6,000 mileage expense incurred by Dr. smart and tax the private use mileage

expense of $ 9,000.

If the fuel expense is paid for by Dr. Smart;

3 divide by 7 * [(cost of the car – salvage value)/10] +($ 0.45 per kilometer * Private use

mileage)

= 3/7 * [($ 210,000 – 32,000)/10] + ($0.45 * $ 9,000)

= (3/7 *$ 178,000)/10 + $ 4,050

= $ 7,628.57 + $4,050

Ans = $ 11,678.57

If fuel is paid for by the employer;

3 divide by 7 * [(cost of the car – salvage value)/10] +($ 0.55 per kilometer * Private use

mileage)

6

Business use = 40/100 * $15,000

= $ 6,000

Private use = 60/100 * 1500

= $ 9,000

Residual value = $ 32,000

Calculation

NB: Any expenses incurred in the course of business purposes is not taxable; thus, we will

deduct the $ 6,000 mileage expense incurred by Dr. smart and tax the private use mileage

expense of $ 9,000.

If the fuel expense is paid for by Dr. Smart;

3 divide by 7 * [(cost of the car – salvage value)/10] +($ 0.45 per kilometer * Private use

mileage)

= 3/7 * [($ 210,000 – 32,000)/10] + ($0.45 * $ 9,000)

= (3/7 *$ 178,000)/10 + $ 4,050

= $ 7,628.57 + $4,050

Ans = $ 11,678.57

If fuel is paid for by the employer;

3 divide by 7 * [(cost of the car – salvage value)/10] +($ 0.55 per kilometer * Private use

mileage)

PERSONAL FINANCIAL MANAGEMENT

7

= 3/7 * [($ 210,000 – 32,000)/10] + ($0.55 * $ 9,000)

= (3/7 *$ 178,000)/10 + $ 4,950

= $ 7,628.57 + $4,950

Ans = $ 12,578.57

II. An all-expenses-paid holiday to Bali

Amount = $ 8,500

Calculation

The amount of holiday expenses given to Dr. Smart and his family is subject to taxation.

The amount of holiday expense to be taxed is

Ans = $ 8,500

III. A partly furnished apartment

Period – 1 March 2018 to 31 December 2018

Annual value = $ 25,000

Dr. Smart and his family stayed in a self-rented bungalow before 1 March 2018.

calculation

The taxable accommodation value is determined based on some factors such as;

7

= 3/7 * [($ 210,000 – 32,000)/10] + ($0.55 * $ 9,000)

= (3/7 *$ 178,000)/10 + $ 4,950

= $ 7,628.57 + $4,950

Ans = $ 12,578.57

II. An all-expenses-paid holiday to Bali

Amount = $ 8,500

Calculation

The amount of holiday expenses given to Dr. Smart and his family is subject to taxation.

The amount of holiday expense to be taxed is

Ans = $ 8,500

III. A partly furnished apartment

Period – 1 March 2018 to 31 December 2018

Annual value = $ 25,000

Dr. Smart and his family stayed in a self-rented bungalow before 1 March 2018.

calculation

The taxable accommodation value is determined based on some factors such as;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PERSONAL FINANCIAL MANAGEMENT

8

1. The property’s annual value.

2. Whether it is fully furnished or partly furnished.

3. The number of days the employer provides accommodation to the employee.

4. If there is any rent that the employee pays.

5. The type of accommodation that has been provided (whether it is an apartment or a hotel).

6. The total income on the employment of the employee.

To get the taxable amount on the benefit of the housing;

The apartment’s yearly value (AV) less the annual rent the employee pays (AR)

If the apartment is partly furnished

40% of the property’s annual value

Therefore, the taxable amount =

(AV – AR) + (40% * AV)

Since there is no annual rent paid that is mentioned the taxable amount will be

= $ 25,000 + (40% * $ 25,000)

= $ 25,000 + $ 10,000

Ans = $ 50,000

Therefore, this is the amount of accommodation benefit that will be taxed in Dr. Smart’s

assessable income.

8

1. The property’s annual value.

2. Whether it is fully furnished or partly furnished.

3. The number of days the employer provides accommodation to the employee.

4. If there is any rent that the employee pays.

5. The type of accommodation that has been provided (whether it is an apartment or a hotel).

6. The total income on the employment of the employee.

To get the taxable amount on the benefit of the housing;

The apartment’s yearly value (AV) less the annual rent the employee pays (AR)

If the apartment is partly furnished

40% of the property’s annual value

Therefore, the taxable amount =

(AV – AR) + (40% * AV)

Since there is no annual rent paid that is mentioned the taxable amount will be

= $ 25,000 + (40% * $ 25,000)

= $ 25,000 + $ 10,000

Ans = $ 50,000

Therefore, this is the amount of accommodation benefit that will be taxed in Dr. Smart’s

assessable income.

PERSONAL FINANCIAL MANAGEMENT

9

1c(i) Share options assessable

The employee share option granted to Dr. Smart is subject to tax. The amount to be taxed

for the share option is the difference in the price that he bought the share at and the actual price

of the shares. Any profit gained from the process of exercising the share option is also subject to

taxation

Calculation

The amount of share option assessable is calculated by adding the difference in the

market price and the exercise price given multiplied by the no of shares granted in the share

option plan then add the gain or profit realized from the sale of the shares.

Exercised option – 50,000 shares at a market price of $ 1.50 at 30TH July, 2018

Option price = $ 1.00

Shares sold – 50,000 shares at $ 2.80

Profit realised = $ 90,000

Exercised option – 50,000 shares at a market price of $ 1.80 on 1ST August, 2018

The total amount of share option assessable for taxation purpose =

= ($ 1.50 - $ 1.00 * 50,000 shares) + $ 90,000 + ($ 1.80 - $ 1.00 * 50,000 shares)

= ($ 0,50 * 50, 000 shares) + $ 90,000 + ($ 0.80 * 50,0000 shares)

= $ 25,000 + $ 90,000 + $ 40,0000

Ans = $ 155,000

9

1c(i) Share options assessable

The employee share option granted to Dr. Smart is subject to tax. The amount to be taxed

for the share option is the difference in the price that he bought the share at and the actual price

of the shares. Any profit gained from the process of exercising the share option is also subject to

taxation

Calculation

The amount of share option assessable is calculated by adding the difference in the

market price and the exercise price given multiplied by the no of shares granted in the share

option plan then add the gain or profit realized from the sale of the shares.

Exercised option – 50,000 shares at a market price of $ 1.50 at 30TH July, 2018

Option price = $ 1.00

Shares sold – 50,000 shares at $ 2.80

Profit realised = $ 90,000

Exercised option – 50,000 shares at a market price of $ 1.80 on 1ST August, 2018

The total amount of share option assessable for taxation purpose =

= ($ 1.50 - $ 1.00 * 50,000 shares) + $ 90,000 + ($ 1.80 - $ 1.00 * 50,000 shares)

= ($ 0,50 * 50, 000 shares) + $ 90,000 + ($ 0.80 * 50,0000 shares)

= $ 25,000 + $ 90,000 + $ 40,0000

Ans = $ 155,000

PERSONAL FINANCIAL MANAGEMENT

10

Therefore, this is the amount of share option assessable for tax purposes

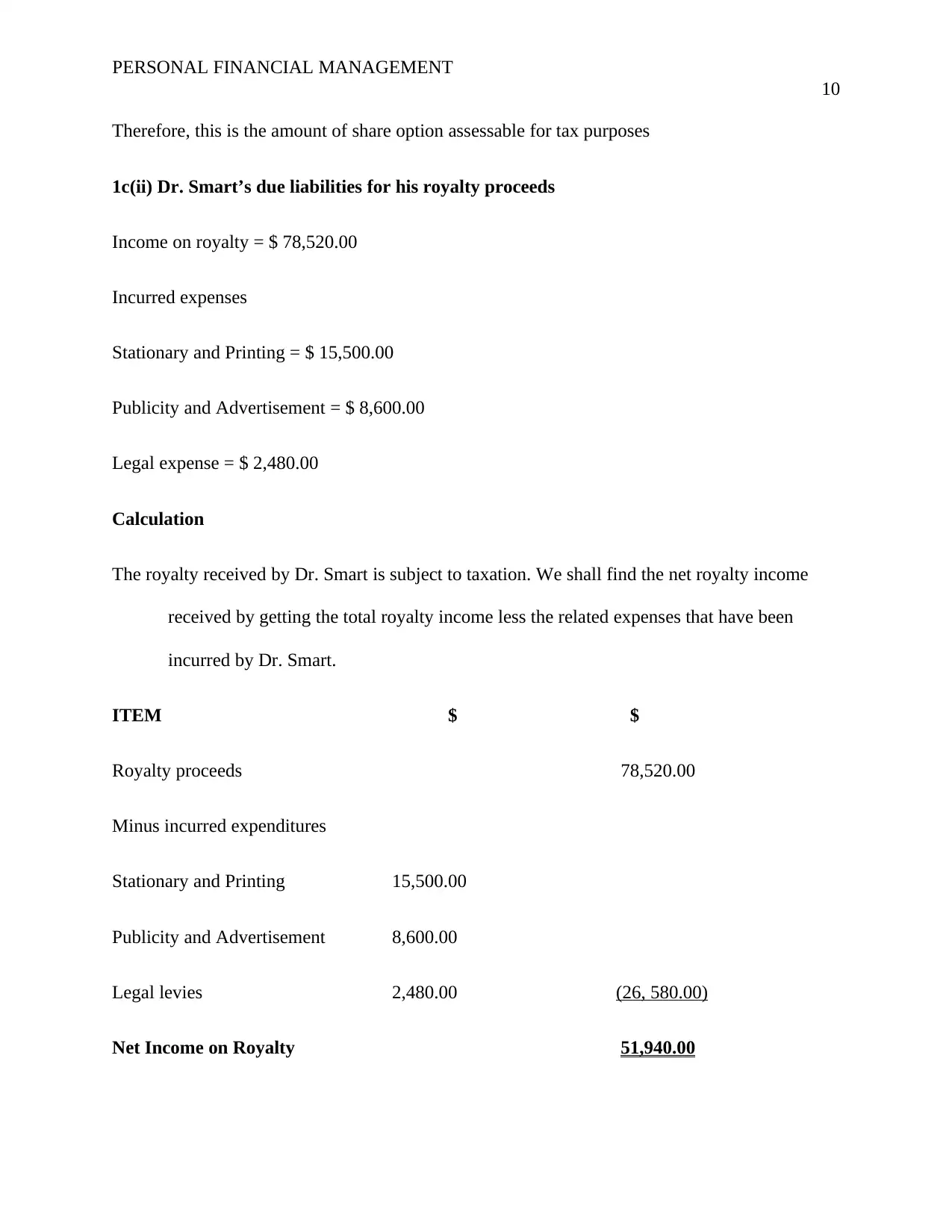

1c(ii) Dr. Smart’s due liabilities for his royalty proceeds

Income on royalty = $ 78,520.00

Incurred expenses

Stationary and Printing = $ 15,500.00

Publicity and Advertisement = $ 8,600.00

Legal expense = $ 2,480.00

Calculation

The royalty received by Dr. Smart is subject to taxation. We shall find the net royalty income

received by getting the total royalty income less the related expenses that have been

incurred by Dr. Smart.

ITEM $ $

Royalty proceeds 78,520.00

Minus incurred expenditures

Stationary and Printing 15,500.00

Publicity and Advertisement 8,600.00

Legal levies 2,480.00 (26, 580.00)

Net Income on Royalty 51,940.00

10

Therefore, this is the amount of share option assessable for tax purposes

1c(ii) Dr. Smart’s due liabilities for his royalty proceeds

Income on royalty = $ 78,520.00

Incurred expenses

Stationary and Printing = $ 15,500.00

Publicity and Advertisement = $ 8,600.00

Legal expense = $ 2,480.00

Calculation

The royalty received by Dr. Smart is subject to taxation. We shall find the net royalty income

received by getting the total royalty income less the related expenses that have been

incurred by Dr. Smart.

ITEM $ $

Royalty proceeds 78,520.00

Minus incurred expenditures

Stationary and Printing 15,500.00

Publicity and Advertisement 8,600.00

Legal levies 2,480.00 (26, 580.00)

Net Income on Royalty 51,940.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PERSONAL FINANCIAL MANAGEMENT

11

The net royalty income of $ 51,940 will be subject to taxation.

QUIZ 3

WEALTH GIVING – ESTATE ARRANGEMENT

The objective of wealth giving can be achieved through effective planning of your estate.

When a person plans for his or her estate, it ensures that the property is well managed and

distributed during his/ her lifetime and even after death.

a(i) The aspect of wealth giving involves the transfer of the estates, and in this, various

terms are used;

ESTATE TRANSFER

Refers to the available approaches of transferring the estate of a dead person without

using the probate process, as these approaches are viewed as dominant to the will of that person

or the intestate laws of succession.

TESTACY(TESTATE)

The state where one dies and has made and left a will that is considered to be valid;

likewise cast as not only superseding that individual’s will but also the intestate succession laws.

RIGHT OF OWNERSHIP

The legally enforceable claim of the survivor of a deceased person to the property of the

dead; a distinguishing characteristic of joint tenancy; a widely recognized form of will substitute.

11

The net royalty income of $ 51,940 will be subject to taxation.

QUIZ 3

WEALTH GIVING – ESTATE ARRANGEMENT

The objective of wealth giving can be achieved through effective planning of your estate.

When a person plans for his or her estate, it ensures that the property is well managed and

distributed during his/ her lifetime and even after death.

a(i) The aspect of wealth giving involves the transfer of the estates, and in this, various

terms are used;

ESTATE TRANSFER

Refers to the available approaches of transferring the estate of a dead person without

using the probate process, as these approaches are viewed as dominant to the will of that person

or the intestate laws of succession.

TESTACY(TESTATE)

The state where one dies and has made and left a will that is considered to be valid;

likewise cast as not only superseding that individual’s will but also the intestate succession laws.

RIGHT OF OWNERSHIP

The legally enforceable claim of the survivor of a deceased person to the property of the

dead; a distinguishing characteristic of joint tenancy; a widely recognized form of will substitute.

PERSONAL FINANCIAL MANAGEMENT

12

BENEFICIARY DESIGNATION

The CPF and insurance policies use this provision to signify one that has the right to

acquire the takings of a person who has died; an ancillary form of a will that is recognized

extensively.

INTESTACY (INTESTATE)

It is the state where one dies, and he/she has not left a valid will; similarly, it is used to

describe the person who has died and has not left behind a will that is considered to be accurate.

a(ii) TRUST AND WILL VALIDITY

The soundness of this statement is questionable because the will is the disposition of

assets after the grantor’s death while a trust helps the grantor to control his assets even before he/

she dies. According to the aspects of wealth giving, a trust is deemed to be valid only when the

legal documents have been executed, and a transfer of property or assets has been made into the

trust. The grantor with the help of a trustee can manage the trust when he/she is still alive, i.e.,

before death and after death, he/ she can choose a trustee of his/her choice to manage the trust.

It is advisable for one to have a will before dying as it ensures that the wealth is left for

the family is protected and is distributed as per the wishes of the individual owning the estate

other than dying intestate. For example, dying without leaving a valid will thus a probate process

will take place, and the estate left behind is distributed according to the succession act.

12

BENEFICIARY DESIGNATION

The CPF and insurance policies use this provision to signify one that has the right to

acquire the takings of a person who has died; an ancillary form of a will that is recognized

extensively.

INTESTACY (INTESTATE)

It is the state where one dies, and he/she has not left a valid will; similarly, it is used to

describe the person who has died and has not left behind a will that is considered to be accurate.

a(ii) TRUST AND WILL VALIDITY

The soundness of this statement is questionable because the will is the disposition of

assets after the grantor’s death while a trust helps the grantor to control his assets even before he/

she dies. According to the aspects of wealth giving, a trust is deemed to be valid only when the

legal documents have been executed, and a transfer of property or assets has been made into the

trust. The grantor with the help of a trustee can manage the trust when he/she is still alive, i.e.,

before death and after death, he/ she can choose a trustee of his/her choice to manage the trust.

It is advisable for one to have a will before dying as it ensures that the wealth is left for

the family is protected and is distributed as per the wishes of the individual owning the estate

other than dying intestate. For example, dying without leaving a valid will thus a probate process

will take place, and the estate left behind is distributed according to the succession act.

PERSONAL FINANCIAL MANAGEMENT

13

a(iii) REVOCATION OF AN INSURANCE NOMINATION OF BENEFICIARIES

As per the insurance act set, for one to validly revoke the nomination of beneficiaries in

his or her insurance policy, he/ she needs to have two witnesses who may be the trustees

appointed or other persons above twenty-one years old and should not be the nominees stated in

the policy.

To determine if Dr. Smart requires the permission of the wife or children to revoke the

nomination of beneficiaries depends on the type of insurance or trust that he has set. For a

revocable kind of trust, Dr. Smart does not require any permission from anyone because he has

the powers to revoke as he wishes, but for an irrevocable type on trust, he will need the consent

of the wife and children as they are the beneficiaries before rescinding any nomination.

b. FEASIBILITY OF USING THE NAME “SMART TUA HUAT” ONLY

Dr. smart has used different names in his assets’ titles to indicate legal ownership, but in

his will, he only wants to use “Smart Tua Huat” i.e.

He uses “Smart” on his house title deeds.

“Smart Chin Chye” on his car registration.

“Smart Tua Huat” on his other assets.

Despite having been known for the many years as “Smart Tua Huat,” it is advisable that

he uses all the names available in his assets’ titles when he writes his will because there will be

implications if he only uses one name when writing his will.

If Dr. Smart only uses one name, the implication is that the will be valid in respect of

assets that just have the name written or applied in his will and the rest of the assets will be

13

a(iii) REVOCATION OF AN INSURANCE NOMINATION OF BENEFICIARIES

As per the insurance act set, for one to validly revoke the nomination of beneficiaries in

his or her insurance policy, he/ she needs to have two witnesses who may be the trustees

appointed or other persons above twenty-one years old and should not be the nominees stated in

the policy.

To determine if Dr. Smart requires the permission of the wife or children to revoke the

nomination of beneficiaries depends on the type of insurance or trust that he has set. For a

revocable kind of trust, Dr. Smart does not require any permission from anyone because he has

the powers to revoke as he wishes, but for an irrevocable type on trust, he will need the consent

of the wife and children as they are the beneficiaries before rescinding any nomination.

b. FEASIBILITY OF USING THE NAME “SMART TUA HUAT” ONLY

Dr. smart has used different names in his assets’ titles to indicate legal ownership, but in

his will, he only wants to use “Smart Tua Huat” i.e.

He uses “Smart” on his house title deeds.

“Smart Chin Chye” on his car registration.

“Smart Tua Huat” on his other assets.

Despite having been known for the many years as “Smart Tua Huat,” it is advisable that

he uses all the names available in his assets’ titles when he writes his will because there will be

implications if he only uses one name when writing his will.

If Dr. Smart only uses one name, the implication is that the will be valid in respect of

assets that just have the name written or applied in his will and the rest of the assets will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PERSONAL FINANCIAL MANAGEMENT

14

deemed to have no convincing will thus may be distributed in probate process rather than the

stated intention of Dr. Smart.

c. AVOIDING ESTATE PLANNING PITFALLS BY DR. SMART

Straus (2017) claims that, as far as inheritance is concerned, it is good to anticipate

conflicts in a family. It is because estate planning issues are a significant throwback to

challenged families. It means therefore that particular aspects and conditions need preparations.

In case a person marries again, it says that he must balance on how to deal with emotional and

any financial needs of the spouses together with his children. If the children are not in good

terms, then you are supposed to make careful choices on the executors of your property. Being

the parent, you need to take preventive initiatives.

You need to take charge of family peace to minimize family conflicts in the future.

Dr smart has the following available actions to avoid the pitfalls due to estate planning;

I. Dr. Smart should keep on updating his estate plan regularly. This activity is as a result of

circumstances such as a change in the composition structure of the estate that he owns.

When he gets divorced or marries another woman etc. in this case Dr. smart had written

in his will that he wants to leave the Toyota to his niece, Jennifer but before the will was

executed the Toyota was involved in an accident thus giving rise to the need of Dr. smart

updating his will.

II. Dr. Smart should make choices that are logical and also defensible. He should postulate

who is to be left in charge in the case of his death, for example, he may appoint his

spouse/ wife or one of his trusted children, and this should be done with thoughtful

14

deemed to have no convincing will thus may be distributed in probate process rather than the

stated intention of Dr. Smart.

c. AVOIDING ESTATE PLANNING PITFALLS BY DR. SMART

Straus (2017) claims that, as far as inheritance is concerned, it is good to anticipate

conflicts in a family. It is because estate planning issues are a significant throwback to

challenged families. It means therefore that particular aspects and conditions need preparations.

In case a person marries again, it says that he must balance on how to deal with emotional and

any financial needs of the spouses together with his children. If the children are not in good

terms, then you are supposed to make careful choices on the executors of your property. Being

the parent, you need to take preventive initiatives.

You need to take charge of family peace to minimize family conflicts in the future.

Dr smart has the following available actions to avoid the pitfalls due to estate planning;

I. Dr. Smart should keep on updating his estate plan regularly. This activity is as a result of

circumstances such as a change in the composition structure of the estate that he owns.

When he gets divorced or marries another woman etc. in this case Dr. smart had written

in his will that he wants to leave the Toyota to his niece, Jennifer but before the will was

executed the Toyota was involved in an accident thus giving rise to the need of Dr. smart

updating his will.

II. Dr. Smart should make choices that are logical and also defensible. He should postulate

who is to be left in charge in the case of his death, for example, he may appoint his

spouse/ wife or one of his trusted children, and this should be done with thoughtful

PERSONAL FINANCIAL MANAGEMENT

15

consideration and without bias to avoid conflicts that may come up in future in the

family.

III. Dr. Smart should make sure that he understands the estate plan that he has written and

signed upon and avoid just relying on the estate planner to do everything without getting

an understanding of what is happening.

IV. Having beneficiary designations that are outdated is another pitfall in estate planning that

Dr. Smart should avoid. He should ensure that he has updated his beneficiary designation

from time to time so that the assets are sure to be distributed to the right persons or the

beneficiaries that he wishes.

V. It is also necessary that Dr. Smart ensures that his retirement plans and the trust plans if

any are coordinated. An example of another estate planning pitfall that is evident when

the grantor names the wrong trust as a beneficiary resulting to higher taxes being

charged. He should ensure that the confidence he wants to designate as a beneficiary

meets the required qualifications and if it does not then, he should go for individuals

rather than the trust.

VI. Another option available to Dr. Smart to avoid the pitfalls is to have discussions that are

open with his family to discuss the particular assets if any. It is advisable to do if there is

a circumstance such as the family business succession or even care of a child that is

handicapped or any other available individual cases in the family.

VII. Dr. smart is also advised to address any available property that is personal on a separate

basis as this is a significant source of family conflict. Dr. Smart can achieve this by

keeping a list separate from the other listings; it contains the instructions of how to

distribute the personal property to the specifically mentioned individuals.

15

consideration and without bias to avoid conflicts that may come up in future in the

family.

III. Dr. Smart should make sure that he understands the estate plan that he has written and

signed upon and avoid just relying on the estate planner to do everything without getting

an understanding of what is happening.

IV. Having beneficiary designations that are outdated is another pitfall in estate planning that

Dr. Smart should avoid. He should ensure that he has updated his beneficiary designation

from time to time so that the assets are sure to be distributed to the right persons or the

beneficiaries that he wishes.

V. It is also necessary that Dr. Smart ensures that his retirement plans and the trust plans if

any are coordinated. An example of another estate planning pitfall that is evident when

the grantor names the wrong trust as a beneficiary resulting to higher taxes being

charged. He should ensure that the confidence he wants to designate as a beneficiary

meets the required qualifications and if it does not then, he should go for individuals

rather than the trust.

VI. Another option available to Dr. Smart to avoid the pitfalls is to have discussions that are

open with his family to discuss the particular assets if any. It is advisable to do if there is

a circumstance such as the family business succession or even care of a child that is

handicapped or any other available individual cases in the family.

VII. Dr. smart is also advised to address any available property that is personal on a separate

basis as this is a significant source of family conflict. Dr. Smart can achieve this by

keeping a list separate from the other listings; it contains the instructions of how to

distribute the personal property to the specifically mentioned individuals.

PERSONAL FINANCIAL MANAGEMENT

16

VIII. Dr. Smart may also appoint a committee to ensure transparency and constant checks on

the inheritance matters in case need arises. Having a committee will ensure that there is

honesty, there is communication to the non-fiduciary beneficiaries, provides that there is

minimal resentment and the available people can share the available workload. The case

of Bruce, for example, he has been added in the will of Dr. Smart because of the threats

to disclose some past indiscretions. Dr. Smart’s wife is aware of this, and during the

execution of the will she may point out this issue, and this may nullify Bruce from being

given the inheritance of $ 100,000 from Dr. Smart’s estate. The available committee

members that have been appointed may assist in advising on the way forward concerning

this case.

CONCLUSION

Becker (2009), claims that most inheritance problems are but inherited they aren’t

inevitable but acquired and genetic. Disputes that arise from inheritance can be prevented as one

can predict and explain them in advance. These inheritance issues can be mitigated through

efficient estate planning procedures. For one to have a desirable wealth status, he/she may use

the various facets of insurance planning and tax planning (Aronoff & John, 2016)

REFERENCES

Aronoff C., & John W., (2016) Family Business Governance: Maximising family and business

potential.

Becker S. G., (2009) A Treatise on the Family. Harvard University Press.

16

VIII. Dr. Smart may also appoint a committee to ensure transparency and constant checks on

the inheritance matters in case need arises. Having a committee will ensure that there is

honesty, there is communication to the non-fiduciary beneficiaries, provides that there is

minimal resentment and the available people can share the available workload. The case

of Bruce, for example, he has been added in the will of Dr. Smart because of the threats

to disclose some past indiscretions. Dr. Smart’s wife is aware of this, and during the

execution of the will she may point out this issue, and this may nullify Bruce from being

given the inheritance of $ 100,000 from Dr. Smart’s estate. The available committee

members that have been appointed may assist in advising on the way forward concerning

this case.

CONCLUSION

Becker (2009), claims that most inheritance problems are but inherited they aren’t

inevitable but acquired and genetic. Disputes that arise from inheritance can be prevented as one

can predict and explain them in advance. These inheritance issues can be mitigated through

efficient estate planning procedures. For one to have a desirable wealth status, he/she may use

the various facets of insurance planning and tax planning (Aronoff & John, 2016)

REFERENCES

Aronoff C., & John W., (2016) Family Business Governance: Maximising family and business

potential.

Becker S. G., (2009) A Treatise on the Family. Harvard University Press.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PERSONAL FINANCIAL MANAGEMENT

17

Chan P., (2010) Managing Your Personal Finances (2nd edition). Mc Graw Hill.

Gitman L. J., Joehnk M. D. & Billingsley R., (2013) Personal Financial Planning.

Joan S. R. & Christie R., (2015) Managing your personal finances. Cengage Learning.

John R. G., Hanlon M., & Nemit S., (2013) Incentives for tax planning and avoidance: Evidence

from the field. The Accounting Review 89 (3), 991-1023.

Richard A. B., Stewart C. M., & Marcus J., (2012) Fundamentals of Corporate Finance.

McGraw–Hill.

Springer J. W., (2016) Managing personal finances,74-84.

Ting H. W., (2011) Financial literacy and personal financial planning in Klang Valley, Malaysia.

International Journal of Economics and Management 5(1), 149-168.

17

Chan P., (2010) Managing Your Personal Finances (2nd edition). Mc Graw Hill.

Gitman L. J., Joehnk M. D. & Billingsley R., (2013) Personal Financial Planning.

Joan S. R. & Christie R., (2015) Managing your personal finances. Cengage Learning.

John R. G., Hanlon M., & Nemit S., (2013) Incentives for tax planning and avoidance: Evidence

from the field. The Accounting Review 89 (3), 991-1023.

Richard A. B., Stewart C. M., & Marcus J., (2012) Fundamentals of Corporate Finance.

McGraw–Hill.

Springer J. W., (2016) Managing personal finances,74-84.

Ting H. W., (2011) Financial literacy and personal financial planning in Klang Valley, Malaysia.

International Journal of Economics and Management 5(1), 149-168.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.